Public Pensions - University of Victoria -...

22

Public Pensions Economics 325 Martin Farnham

Transcript of Public Pensions - University of Victoria -...

Public Pensions

Economics 325 Martin Farnham

Why Pensions?

• Typically people work between the ages of about 20 and 65. – Younger people depend on parents to support

them – Older people depend on accumulated wealth, kids,

and/or society to support them • Pensions provide income support for people

in retirement – Can alternatively be thought of as savings or

insurance

Basics of Canadian Pension System

• 3 components – Old Age Security Program (financed out of general

revenues) • Old Age Security Pension (OAS) • Guaranteed Income Supplement (GIS) • Allowance program • These programs provide basic income support (most

people get the same amount, regardless of earnings during working years)

– Canada/Quebec Pension Plans (CPP/QPP) • Benefits tied to contributions; those who earn more and

pay in more, earn higher benefits (kind of like EI) • Provides disability insurance

Basics of Canadian Pension System

– CPP/QPP (continued) • Financed from employee contributions

• Private pensions make up third component of Canadian system – Registered Retirement Savings Plan (RRSPs),

Registered Pension Plan • Long-term viability of these programs is

cause of some concern – Public components (OAS, CPP/QPP) are “pay as

you go” systems – Contributions today don’t get put in a bank

account; they get paid out as benefits immediately

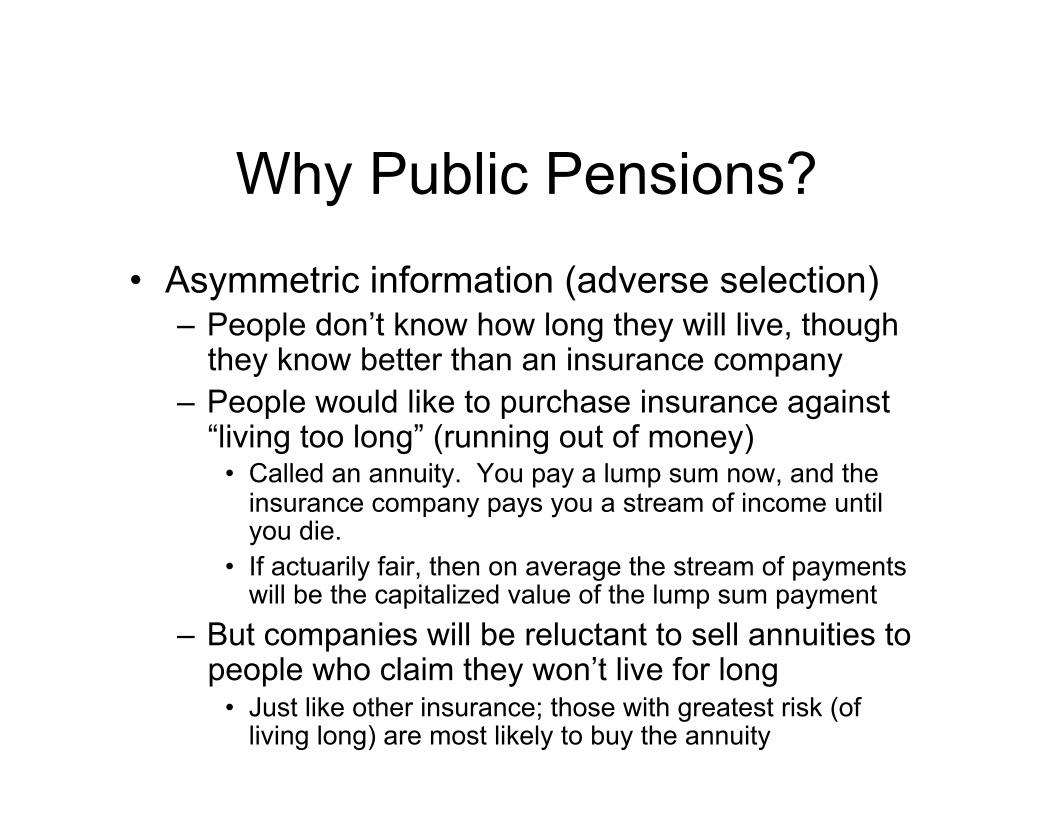

Why Public Pensions?

• Asymmetric information (adverse selection) – People don’t know how long they will live, though

they know better than an insurance company – People would like to purchase insurance against

“living too long” (running out of money) • Called an annuity. You pay a lump sum now, and the

insurance company pays you a stream of income until you die.

• If actuarily fair, then on average the stream of payments will be the capitalized value of the lump sum payment

– But companies will be reluctant to sell annuities to people who claim they won’t live for long

• Just like other insurance; those with greatest risk (of living long) are most likely to buy the annuity

Why Public Pensions?

• Paternalism – Maybe the government feels people are myopic.

Don’t plan well for future – Assumes people are not fully rational – Government holds peoples’ hands by forcing them

to save (by forced contributions to CPP, for example)

– Figures people will thank them someday – Also prevents people from failing to save and so

then going on welfare when they run out of money

Why Public Pensions?

• Missing information; costly planning – Maybe people lack the skills or knowledge to plan – Government could plan for them, hence saving

them the costs of figuring it out themselves – Why isn’t this a particularly good argument?

• Government could just provide people with needed information; put pension calculators online and offer financial advice to those who need it

• Arguably, with this information and assistance, people could best plan for themselves, rather than having government decide for them what their savings should be

Redistribution • The public pension system provides another

way to redistribute income – Wealthy get lower ratio of benefits/contributions

than poor – OAS gives everyone a basic amount (yet income

taxes are higher for wealthy which implies some redistribution)

– Public pensions don’t discriminate against people on basis of gender, for instance

• Private market would charge more to women for an annuity, because they live longer; so public pensions redistribute toward women (who tend to be poorer in retirement) from men

• Current debate in US over indexing benefits to life expectancy (i.e. pay less to people who will live longer)

Why Are Public Pensions Pay as-you-go?

• Pay-as-you-go financing pays current benefits out of current contributions – Your and your parents’ CPP contributions finance

your grandparents’ benefits – Your benefits will be paid out of your kids and

grandkids contributions • Under alternative financing arrangement,

government could manage a big bank account where everyone’s contributions go to earn interest until they retire – System of individual accounts (Bush tried to push

this in US)

Pay-as-you-go Finance

• Pay as you go financing is sometimes called Ponzi financing – Charles Ponzi was a con artist who went around

running pyramid investment schemes. – Sign on a few investors, then pay them high

returns by signing on more investors and handing the new investors’ money over to the old investors

– Scheme generates money for old investors until new people refuse to sign on

• Need a bigger crowd of new investors in each stage…hence the name pyramid scheme

• Eventually new round of potential investors worries they won’t get paid back and so refuse to contribute--pyramid collapses

Is CPP/QPP a Ponzi-Scheme?

• Under growing population and productivity growth, CPP/QPP flourished – Both sources of growth have declined – Now there is some concern that young generation

will pull out; system would certainly collapse if they did

• Why would young pull out? If they believe they won’t get benefits, why should they pay in?

• Many young people would rather take their chances with private accounts…put their own money where they’re (virtually) guaranteed to get it back.

• Now in both Canada and US there are calls for reform of the system

Why Choose Pay-as-you-go over Private Accounts?

• Politically it’s more viable to start – Voters alive today can shift costs to unborn

generations • If the economy is growing fast, then

contributions can grow more quickly than money in a bank account – This worked well for Canada and US in 1960s, not

so well after 1970s productivity slowdown • In some cases, exigent circumstances

required establishing benefit payments immediately (e.g. US in Great Depression)

Effects of Public Pensions on Behaviour

• Saving (could go up or down) – If government is forcing you to save, your private

saving is likely to decline in response – If your benefits are tied to choice of retirement

age, this may affect your decision to retire • If rules don’t allow you to work and collect benefits at the

same time, you may quit work earlier; in anticipation of this you may save more earlier in life

– Some people like to transfer wealth to their children in the form of an inheritance

• CPP/QPP reverses this transfer, by giving money from young to old

• Parents may try to undo this transfer by increasing bequests; will save more to do this.

Effect on Saving: Empirical Evidence

• Results generally suggest some negative impact on saving overall (most studies on US) – Feldstein (1974) found strongly negative effect of

US Social Security on saving • Famous paper, because the initial result was due to a

programming error • His RA’s fault (supposedly!) • Revised results found smaller effect

– Other studies have disputed his revised findings • Munnell finds much smaller effect when controlling for

unemployment (though effect on saving is still negative) • Burbidge suggests small negative effect in Canada

Effect of Public Pensions on Retirement Timing

• Certain program rules can create incentive for people to retire early – If government claws back benefits for people who

continue working, people will be more likely to retire early

– Retirement ages in Canada have decreased since the 1960s when public pensions were implemented

– But this decrease is part of a 100 year trend started long before the introduction of such programs.

Some Details on Canadian System

• Old Age Security Program – Started in 1927 with Old Age Pension Act

• Originally pensions were means tested (more you earn, the less you get)

– 1952 • Universal pension (no longer means tested) of $40/

month – Full indexation of benefits introduced in 1973;

attempts to back away from this were shouted down

– OAS benefits (around $500/month) are taxed

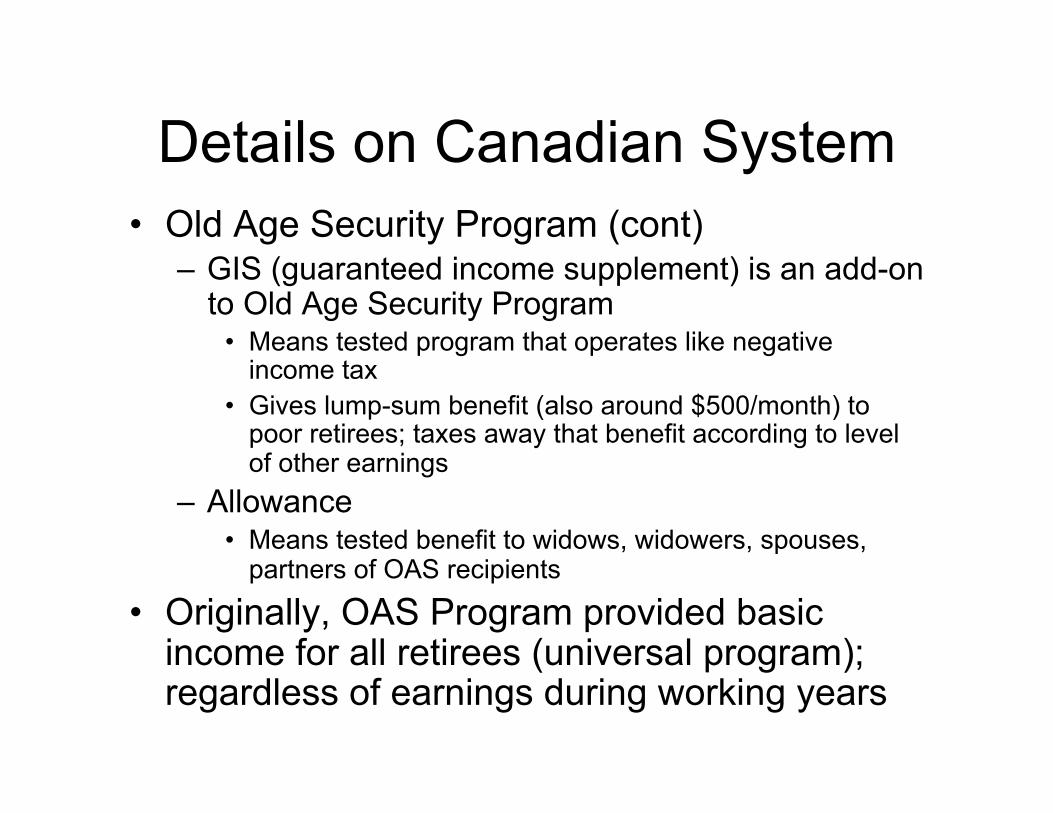

Details on Canadian System • Old Age Security Program (cont)

– GIS (guaranteed income supplement) is an add-on to Old Age Security Program

• Means tested program that operates like negative income tax

• Gives lump-sum benefit (also around $500/month) to poor retirees; taxes away that benefit according to level of other earnings

– Allowance • Means tested benefit to widows, widowers, spouses,

partners of OAS recipients

• Originally, OAS Program provided basic income for all retirees (universal program); regardless of earnings during working years

OAS Challenges

• In 1989, partial clawback of OAS benefits was introduced – Points to basic debate over whether programs

should be “universal” or “targetted” • Universal programs are viewed as easier to get political

support for • But it doesn’t make sense to “redistribute to everyone” • Further attempts at increasing clawback in ‘96 failed

• Population aging threatens viability of OAS. – Baby boom reaches age 65 in 2010 – If productivity growth remains strong enough, this

won’t be a problem

Some Details on Canadian System

• Canadian Pension Plan (CPP/QPP) – Differs from OAS Program in that people receive

benefits proportional to their contributions • High earners receive more benefits than low earners

• Basic components – Retirement benefits (regularly claimed starting at

age 65; options for early or late retirement exist) – Disability benefits (can collect these before regular

retirement age if you become disabled) – Survivor benefits (for spouse of primary income

earner) • CPP is more like insurance than OAS

Contribution Rates to CPP Have Grown Over Time

• Contribution rate in 1966 was 3.6%; more than funded current benefits – Founders expected contribution rates would

increase to 5.5% in 2030 – By 1996 contribution rates of 14.2% were

expected for 2030; why the increase? • Benefits expanded • Birth rates fell (so fewer paying in than expected) • Lifespans increased more than expected • Productivity slowed starting in mid-1970s • Disability claims have risen

1998 CPP Reforms

• Contribution changes – Contribution rate raised from 5.6% in 1996 to 9.9%

in 2003; set to hold there for rest of this century – Investment of reserve fund in securities

• Benefits changes (reductions) – Stricter eligibility rules for disability – Benefits based on Year’s Maximum Pensionable

Earnings of past 5 years (as opposed to past 3 years)--likely to reduce benefits paid out

– Limits on survivor and death benefits

Intergenerational Redistribution

• Different generations have fared differently under CPP – Those born in 1915 received $5.50 in benefits per

dollar contributed – Those born after 1975 are expected to receive

less than $0.50 per dollar contributed • Recent reforms make things worse for your generation

(at least on the contributions side) – Political opposition to intergenerational

redistribution may not be as strong as it could be, if young voters feel ties to older voters who benefit from such redistribution