Public Financial Management, Inc. · 2015. 10. 22. · INFORMATION FOR BIDDERS $2,450,000 CLARE...

80

NEW ISSUE Ratings ¹†: Standard & Poor’s: AA (Build America Mutual Assurance Company) Book-Entry-Only Standard & Poor’s: A (underlying rating) TAX STATUS: In the opinion of Thrun Law Firm, P.C., Bond Counsel, assuming continued compliance by the School District with certain requirements of the Internal Revenue Code of 1986, as amended (the “Code”), interest on the Bonds is excluded from gross income for federal income tax purposes, as described in the opinion, and the Bonds and interest thereon are exempt from all taxation in the State of Michigan, except inheritance and estate taxes and taxes on gains realized from the sale, payment or other disposition thereof. The School District has designated the Bonds as “QUALIFIED TAX-EXEMPT OBLIGATIONS” within the meaning of the Code, and has covenanted to comply with those requirements of the Code necessary to continue the exclusion of interest on the Bonds from gross income for federal income tax purposes. $2,450,000 CLARE PUBLIC SCHOOLS Counties of Clare and Isabella State of Michigan 2015 School Building and Site Bonds (General Obligation - Unlimited Tax) PURPOSE AND SECURITY: The Bonds were authorized at an election on August 4, 2015, for the purpose of partially remodeling, furnishing and refurnishing, and equipping and reequipping school district buildings; acquiring, installing and equipping instructional technology for school district buildings, together with related infrastructure improvements; purchasing school buses; developing, equipping and improving a playground; and developing and improving sites. The Bonds will pledge the full faith, credit and resources of the School District for payment of the principal and interest thereon, and will be payable from ad valorem taxes, which may be levied without limitation as to rate or amount as provided by Article IX, Section 6, of the Michigan Constitution of 1963. BOOK-ENTRY-ONLY: Unless otherwise required by the initial purchaser of the Bonds, the Bonds are issuable only as fully registered bonds without coupons, and when issued, will be registered in the name of Cede & Co., as Bondholder and nominee for The Depository Trust Company (“DTC”), New York, New York. DTC will act as securities depository for the Bonds. Purchases of beneficial interests in the Bonds will be made in book-entry only form, in the denominations of $5,000 or any integral multiple thereof. Purchasers will not receive certificates representing their beneficial interest in Bonds purchased. So long as Cede & Co. is the Bondholder, as nominee of DTC, references herein to the Bondholders or registered owners shall mean Cede & Co., as aforesaid, and shall not mean the Beneficial Owners of the Bonds. See BOOK-ENTRY ONLY SYSTEM herein. PAYMENT OF BONDS: Interest on the Bonds will be payable semiannually on May 1 and November 1 of each year commencing on May 1, 2016. The Bonds will be registered Bonds, of the denomination of $5,000 or multiples thereof not exceeding for each maturity the principal amount of such maturity. The principal and interest shall be payable at the corporate trust office of U.S. Bank National Association, Detroit, Michigan (the “Paying Agent”) or such other Paying Agent as the School District may hereafter designate by notice mailed to the registered owner not less than sixty (60) days prior to any interest payment date. So long as DTC or its nominee, Cede & Co., is the Bondholder, such payments will be made directly to such Bondholder. Disbursement of such payments to the Beneficial Owners is the responsibility of DTC Participants and Indirect Participants, as more fully described herein. Interest shall be paid when due by check or draft mailed to the registered owner as shown on the registration books as of the fifteenth day of the month preceding the payment date for each interest payment. BOND INSURANCE: The scheduled payment of principal and interest on the Bonds when due will guaranteed under a municipal bond insurance policy to be issued concurrently with the delivery of the Bonds by Build America Mutual Assurance Company (“BAM”). See “Appendix F – Municipal Bond Insurance and Specimen Policy”. Dated: November 10, 2015 Principal Due: May 1 of each year as shown below MATURITY SCHEDULE (Base CUSIP§: 180060) Year Amount Interest Rate Yield CUSIP§ Year Amount Interest Rate Yield CUSIP§ 2016 $100,000 2.00% 0.55% CP8 2022 $245,000 2.00% 1.75% CV5 2017 135,000 2.00 0.80 CQ6 2023 270,000 2.00 1.95 CW3 2018 155,000 2.00 1.00 CR4 2024 295,000 2.25 2.10 CX1 2019 175,000 2.00 1.10 CS2 2025 320,000 3.00 2.25 CY9 2020 195,000 2.00 1.30 CT0 2026 340,000 3.00 2.40 CZ6 2021 220,000 2.00 1.50 CU7 City Securities Corporation PRIOR REDEMPTION: Bonds of this issue maturing in the years 2016 through 2025, inclusive, shall not be subject to redemption prior to maturity. Bonds or portions of Bonds in multiples of $5,000 of this issue maturing in the year 2026 shall be subject to redemption prior to maturity as described herein. See “PRIOR REDEMPTION - Optional Redemption” herein. BOND COUNSEL: The Bonds will be offered when, as and if issued by the School District subject to the approving legal opinion of Thrun Law Firm, P.C., East Lansing, Michigan. THIS COVER PAGE CONTAINS INFORMATION FOR A QUICK REFERENCE ONLY. IT IS NOT A SUMMARY OF THIS ISSUE. INVESTORS MUST READ THE ENTIRE OFFICIAL STATEMENT TO OBTAIN INFORMATION ESSENTIAL TO THE MAKING OF AN INFORMED INVESTMENT DECISION. Additional information relative to this Bond issue may be obtained from: Public Financial Management, Inc. 3989 Research Park Drive Ann Arbor, Michigan 48108 734-668-6688 OFFICIAL STATEMENT DATED: OCTOBER 19, 2015 ¹ For an explanation of ratings, see “CREDIT RATINGS” herein. † As of the date of delivery § Copyright 2015, American Bankers Association. CUSIP data herein is provided by Standard & Poor’s CUSIP Service Bureau, a division of the McGraw-Hill Companies, Inc. The School District shall not be responsible for the selection of CUSIP numbers, nor any representation made as to their correctness on the Bonds or as indicated above.

Transcript of Public Financial Management, Inc. · 2015. 10. 22. · INFORMATION FOR BIDDERS $2,450,000 CLARE...

NEW ISSUE Ratings ¹†: Standard & Poor’s: AA (Build America Mutual Assurance Company)Book-Entry-Only Standard & Poor’s: A (underlying rating)

TAX STATUS: In the opinion of Thrun Law Firm, P.C., Bond Counsel, assuming continued compliance by the School District with certain requirements of the Internal Revenue Code of 1986, as amended (the “Code”), interest on the Bonds is excluded from gross income for federal income tax purposes, as described in the opinion, and the Bonds and interest thereon are exempt from all taxation in the State of Michigan, except inheritance and estate taxes and taxes on gains realized from the sale, payment or other disposition thereof. The School District has designated the Bonds as “QUALIFIED TAX-EXEMPT OBLIGATIONS” within the meaning of the Code, and has covenanted to comply with those requirements of the Code necessary to continue the exclusion of interest on the Bonds from gross income for federal income tax purposes.

$2,450,000CLARE PUBLIC SCHOOLSCounties of Clare and Isabella

State of Michigan2015 School Building and Site Bonds(General Obligation - Unlimited Tax)

PURPOSE AND SECURITY: The Bonds were authorized at an election on August 4, 2015, for the purpose of partially remodeling, furnishing and refurnishing, and equipping and reequipping school district buildings; acquiring, installing and equipping instructional technology for school district buildings, together with related infrastructure improvements; purchasing school buses; developing, equipping and improving a playground; and developing and improving sites. The Bonds will pledge the full faith, credit and resources of the School District for payment of the principal and interest thereon, and will be payable from ad valorem taxes, which may be levied without limitation as to rate or amount as provided by Article IX, Section 6, of the Michigan Constitution of 1963.

BOOK-ENTRY-ONLY: Unless otherwise required by the initial purchaser of the Bonds, the Bonds are issuable only as fully registered bonds without coupons, and when issued, will be registered in the name of Cede & Co., as Bondholder and nominee for The Depository Trust Company (“DTC”), New York, New York. DTC will act as securities depository for the Bonds. Purchases of beneficial interests in the Bonds will be made in book-entry only form, in the denominations of $5,000 or any integral multiple thereof. Purchasers will not receive certificates representing their beneficial interest in Bonds purchased. So long as Cede & Co. is the Bondholder, as nominee of DTC, references herein to the Bondholders or registered owners shall mean Cede & Co., as aforesaid, and shall not mean the Beneficial Owners of the Bonds. See BOOK-ENTRY ONLY SYSTEM herein.

PAYMENT OF BONDS: Interest on the Bonds will be payable semiannually on May 1 and November 1 of each year commencing on May 1, 2016. The Bonds will be registered Bonds, of the denomination of $5,000 or multiples thereof not exceeding for each maturity the principal amount of such maturity. The principal and interest shall be payable at the corporate trust office of U.S. Bank National Association, Detroit, Michigan (the “Paying Agent”) or such other Paying Agent as the School District may hereafter designate by notice mailed to the registered owner not less than sixty (60) days prior to any interest payment date. So long as DTC or its nominee, Cede & Co., is the Bondholder, such payments will be made directly to such Bondholder. Disbursement of such payments to the Beneficial Owners is the responsibility of DTC Participants and Indirect Participants, as more fully described herein. Interest shall be paid when due by check or draft mailed to the registered owner as shown on the registration books as of the fifteenth day of the month preceding the payment date for each interest payment.

BOND INSURANCE: The scheduled payment of principal and interest on the Bonds when due will guaranteed under a municipal bond insurance policy to be issued concurrently with the delivery of the Bonds by Build America Mutual Assurance Company (“BAM”). See “Appendix F – Municipal Bond Insurance and Specimen Policy”.

Dated: November 10, 2015 Principal Due: May 1 of each year as shown below

MATURITY SCHEDULE(Base CUSIP§: 180060)

Year AmountInterest

Rate Yield CUSIP§ Year AmountInterest

Rate Yield CUSIP§2016 $100,000 2.00% 0.55% CP8 2022 $245,000 2.00% 1.75% CV52017 135,000 2.00 0.80 CQ6 2023 270,000 2.00 1.95 CW32018 155,000 2.00 1.00 CR4 2024 295,000 2.25 2.10 CX12019 175,000 2.00 1.10 CS2 2025 320,000 3.00 2.25 CY92020 195,000 2.00 1.30 CT0 2026 340,000 3.00 2.40 CZ62021 220,000 2.00 1.50 CU7

City Securities CorporationPRIOR REDEMPTION: Bonds of this issue maturing in the years 2016 through 2025, inclusive, shall not be subject to redemption prior to maturity. Bonds or portions of Bonds in multiples of $5,000 of this issue maturing in the year 2026 shall be subject to redemption prior to maturity as described herein. See “PRIOR REDEMPTION - Optional Redemption” herein.

BOND COUNSEL: The Bonds will be offered when, as and if issued by the School District subject to the approving legal opinion of Thrun Law Firm, P.C., East Lansing, Michigan.

This cover page conTains informaTion for a quick reference only. iT is noT a summary of This issue. invesTors musT read The enTire official sTaTemenT To obTain informaTion essenTial To The making of an informed invesTmenT decision.

Additional information relative to this Bond issue may be obtained from:

Public Financial Management, Inc.3989 Research Park Drive

Ann Arbor, Michigan 48108734-668-6688

official sTaTemenT daTed: ocTober 19, 2015

¹ For an explanation of ratings, see “CREDIT RATINGS” herein.† As of the date of delivery§ Copyright 2015, American Bankers Association. CUSIP data herein is provided by Standard & Poor’s CUSIP Service Bureau, a division of the McGraw-Hill

Companies, Inc. The School District shall not be responsible for the selection of CUSIP numbers, nor any representation made as to their correctness on the Bonds or as indicated above.

Build America Mutual Assurance Company (“BAM”) makes no representation regarding the Bonds or the advisability of investingin the Bonds. In addition, BAM has not independently verified, makes no representation regarding, and does not accept anyresponsibility for the accuracy or completeness of this Official Statement or any information or disclosure contained herein, oromitted herefrom, other than with respect to the accuracy of the information regarding BAM supplied by BAM and presented underthe heading “MUNICIPAL BOND INSURANCE & SPECIMEN POLICY” in Appendix F herein.

CLARE PUBLIC SCHOOLS201 E. State StreetClare, MI 48617

Phone: 989-386-9945Fax: 989-386-6055

BOARD OF EDUCATION

PRESIDENTFrank Thomas Weaver

Term Expires December 2016

VICE PRESIDENTSteven L. Stark

Term Expires December 2016

SECRETARYCarol J. Santini

Term Expires December 2016

TREASURERSusan M. Murawski

Term Expires December 2016

TRUSTEESBenjamin A. Browning

Term Expires December 2018

Loren ColeTerm Expires December 2018

John L. MillerTerm Expires December 2018

SUPERINTENDENTDouglas O. Fillmore

BUSINESS MANAGERLynn M. Graham

PROFESSIONAL SERVICES

PAYING AGENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . U.S. Bank National Association

BOND COUNSEL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thrun Law Firm, P.C.

FINANCIAL CONSULTANT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Public Financial Management, Inc.

iii

TABLE OF CONTENTS

Page

INFORMATION FOR BIDDERS . . . . . . . . . . . . . . . . . 1PURPOSE AND SECURITY . . . . . . . . . . . . . . . . . 1PRIOR REDEMPTION . . . . . . . . . . . . . . . . . . . . . 1NOTICE OF SALE . . . . . . . . . . . . . . . . . . . . . . . . . 2BOOK-ENTRY ONLY SYSTEM . . . . . . . . . . . . . 2TAX PROCEDURES . . . . . . . . . . . . . . . . . . . . . . . 4TRANSFER OUTSIDE BOOK-ENTRY-ONLY

SYSTEM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4SOURCES OF SCHOOL OPERATING

REVENUE . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5MICHIGAN PROPERTY TAX REFORM . . . . . . . 6LITIGATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6TAX MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

State of Michigan . . . . . . . . . . . . . . . . . . . . . . . 6Federal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Original Issue Premium . . . . . . . . . . . . . . . . . . 7Future Developments . . . . . . . . . . . . . . . . . . . . 7

QUALIFIED BY THE MICHIGAN DEPARTMENTOF TREASURY . . . . . . . . . . . . . . . . . . . . . . . 8

CONTINUING DISCLOSURE . . . . . . . . . . . . . . . 8BOND COUNSEL’S RESPONSIBILITY . . . . . . . 8FINANCIAL CONSULTANT’S OBLIGATION . . 9CREDIT RATINGS . . . . . . . . . . . . . . . . . . . . . . . . 9ESTIMATED SOURCES AND

USES OF FUNDS . . . . . . . . . . . . . . . . . . . . . 10

GENERAL FINANCIAL INFORMATION . . . . . . . . 11AREA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11POPULATION . . . . . . . . . . . . . . . . . . . . . . . . . . . 11PROPERTY VALUATIONS . . . . . . . . . . . . . . . . 11

Historical Valuations . . . . . . . . . . . . . . . . . . . 11Per Capita Valuation . . . . . . . . . . . . . . . . . . . 12Industrial Facilities Tax (IFT) . . . . . . . . . . . . 12

TAX BASE COMPOSITION . . . . . . . . . . . . . . . . 13MAJOR TAXPAYERS . . . . . . . . . . . . . . . . . . . . . 13CONSTITUTIONAL MILLAGE ROLLBACK . . 14TAX RATES - (Per $1,000 of Valuation) . . . . . . . 14

Clare Public Schools . . . . . . . . . . . . . . . . . . . 14Other Major Taxing Units . . . . . . . . . . . . . . . 14

STATE AID PAYMENTS . . . . . . . . . . . . . . . . . . 14TAX LEVIES AND COLLECTIONS . . . . . . . . . 15LABOR FORCE . . . . . . . . . . . . . . . . . . . . . . . . . . 15PENSION FUND . . . . . . . . . . . . . . . . . . . . . . . . . 16OTHER POST-EMPLOYMENT BENEFITS . . . 17

DEBT STATEMENT . . . . . . . . . . . . . . . . . . . . . . 17DIRECT DEBT . . . . . . . . . . . . . . . . . . . . . . . . . . . 17OVERLAPPING DEBT . . . . . . . . . . . . . . . . . . . . 17DEBT RATIOS . . . . . . . . . . . . . . . . . . . . . . . . . . . 17DEBT HISTORY . . . . . . . . . . . . . . . . . . . . . . . . . 17FUTURE FINANCING . . . . . . . . . . . . . . . . . . . . 18OTHER BORROWING . . . . . . . . . . . . . . . . . . . . 18LEGAL DEBT MARGIN . . . . . . . . . . . . . . . . . . . 18SCHOOL BOND QUALIFICATION AND LOAN

PROGRAM . . . . . . . . . . . . . . . . . . . . . . . . . . 18

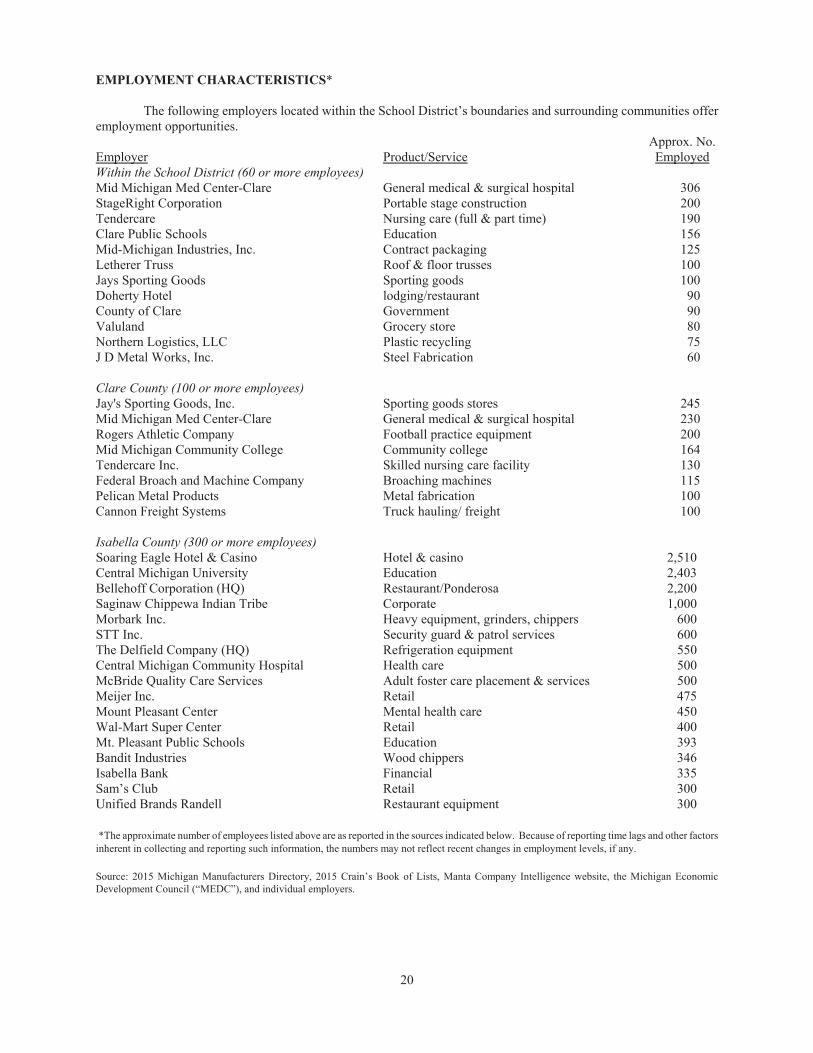

GENERAL ECONOMIC INFORMATION . . . . . . . . 19LOCATION AND AREA . . . . . . . . . . . . . . . . . . . 19POPULATION BY AGE . . . . . . . . . . . . . . . . . . . 19INCOME . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19EMPLOYMENT CHARACTERISTICS . . . . . . . 20EMPLOYMENT BREAKDOWN . . . . . . . . . . . . 21UNEMPLOYMENT . . . . . . . . . . . . . . . . . . . . . . . 21BANKING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

GENERAL SCHOOL INFORMATION . . . . . . . . . . . 22DESCRIPTION . . . . . . . . . . . . . . . . . . . . . . . . . . . 22BOARD OF EDUCATION . . . . . . . . . . . . . . . . . 22SCHOOL ENROLLMENT . . . . . . . . . . . . . . . . . . 22

Historical Enrollment . . . . . . . . . . . . . . . . . . . 22Enrollment by Grade . . . . . . . . . . . . . . . . . . . 22Projected Enrollment . . . . . . . . . . . . . . . . . . . 22

EXISTING SCHOOL FACILITIES . . . . . . . . . . . 23OTHER SCHOOLS . . . . . . . . . . . . . . . . . . . . . . . 23OTHER MATTERS . . . . . . . . . . . . . . . . . . . . . . . 24

APPENDIX A - BUDGET . . . . . . . . . . . . . . . . . . . . . A-1

APPENDIX B - AUDIT . . . . . . . . . . . . . . . . . . . . . . . B-1

APPENDIX C - FORM OF CONTINUINGDISCLOSURE AGREEMENT . . . . . . . . . . . . . . C-1

APPENDIX D - DRAFT LEGAL OPINION . . . . . . . D-1

APPENDIX E - DRAFT OFFICIAL NOTICE OF SALE . . . . . . . . . . . . . . . . . . . . . . . E-1

APPENDIX F - MUNICIPAL BOND INSURANCEAND SPECIMEN POLICY . . . . . . . . . . . . . . . . F-1

iv

INFORMATION FOR BIDDERS

$2,450,000 CLARE PUBLIC SCHOOLSCounties of Clare and Isabella

State of Michigan2015 School Building and Site Bonds(General Obligation - Unlimited Tax)

DATED: November 10, 2015

FIRST INTEREST: May 1, 2016

REGISTRATION: Principal and Interest

PAYING AGENT: U.S. Bank National Association, Detroit, Michigan

TAX DESIGNATION: QUALIFIED TAX - EXEMPT OBLIGATIONS

PRINCIPAL DUE: May 1, annually as shown the front cover

PURPOSE AND SECURITY

The Bonds were authorized at an election on August 4, 2015, for the purpose of partially remodeling, furnishingand refurnishing, and equipping and reequipping school district buildings; acquiring, installing and equippinginstructional technology for school district buildings, together with related infrastructure improvements; purchasingschool buses; developing, equipping and improving a playground; and developing and improving sites. The Bonds willpledge the full faith, credit and resources of the School District for payment of the principal and interest thereon, andwill be payable from ad valorem taxes, which may be levied without limitation as to rate or amount as provided byArticle IX, Section 6, of the Michigan Constitution of 1963.

PRIOR REDEMPTION

A. Optional Redemption.

Bonds of this issue maturing in the years 2016 through 2025, inclusive, shall not be subject to redemption priorto maturity. Bonds or portions of Bonds in multiples of $5,000 of this issue maturing in the year 2026 shall be subjectto redemption prior to maturity, at the option of the School District, in such order as the School District may determineand by lot within any maturity, on any date occurring on or after May 1, 2025, at par and accrued interest to the datefixed for redemption.

B. Notice of Redemption and Manner of Selection.

Notice of redemption of any Bond shall be given not less than thirty (30) days and not more than sixty (60) daysprior to the date fixed for redemption by mail to the registered owner at the registered address shown on the registrationbooks kept by the Paying Agent. The Bonds shall be called for redemption in multiples of $5,000 and Bonds ofdenominations of more than $5,000 shall be treated as representing the number of Bonds obtained by dividing the faceamount of the Bond by $5,000 and such Bonds may be redeemed in part. The notice of redemption for Bonds redeemedin part shall state that upon surrender of the Bond to be redeemed a new Bond or Bonds in an aggregate face amountequal to the unredeemed portion of the Bond surrendered shall be issued to the registered owner thereof.

If less than all of the Bonds of any maturity shall be called for redemption prior to maturity, unless otherwiseprovided, the particular Bonds or portions of Bonds to be redeemed shall be selected by lot by the Paying Agent, in theprincipal amounts designated by the School District. Any Bonds selected for redemption will cease to bear interest onthe date fixed for redemption, whether presented for redemption or not, provided funds are on hand to redeem saidBonds. Upon presentation and surrender of such Bonds at the corporate trust office of the Paying Agent, such Bondsshall be paid and redeemed.

1

So long as the book-entry-only system remains in effect, in the event of a partial redemption the Paying Agentwill give notice to Cede & Co., as nominee of DTC, only, and only Cede & Co. will be deemed to be a holder of theBonds. DTC is expected to reduce the credit balances of the applicable DTC Participants in respect of the Bonds andin turn the DTC Participants are expected to select those Beneficial Owners whose ownership interests are to beextinguished or reduced by such partial redemption, each by such method as DTC or such DTC Participants, as the casemay be, deems fair and appropriate in its sole discretion.

NOTICE OF SALE

See “APPENDIX E - DRAFT OFFICIAL NOTICE OF SALE,” for further information regarding this issue.

BOOK-ENTRY ONLY SYSTEM

The information in this section has been furnished by The Depository Trust Company, New York, New York("DTC"). No representation is made by U.S. Bank National Association, Detroit, Michigan (the “Paying Agent”) as to thecompleteness or accuracy of such information or as to the absence of material adverse changes in such informationsubsequent to the date hereof. No attempt has been made by the School District or the Paying Agent to determine whetherDTC is or will be financially or otherwise capable of fulfilling its obligations. Neither the School District nor the PayingAgent will have any responsibility or obligation to Direct Participants, Indirect Participants (both as defined below) or thepersons for which they act as nominees with respect to the Bonds, or for any principal, premium, if any, or interest paymentthereof.

The Depository Trust Company ("DTC"), New York, NY, will act as securities depository for the securities (the"Securities"). The Securities will be issued as fully-registered securities registered in the name of Cede & Co. (DTC'spartnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully-registeredSecurity certificate will be issued for each issue of the Securities, each in the aggregate principal amount of such issue, andwill be deposited with DTC. If, however, the aggregate principal amount of any issue exceeds $500 million, one certificatewill be issued with respect to each $500 million of principal amount, and an additional certificate will be issued with respectto any remaining principal amount of such issue.

DTC, the world's largest securities depository, is a limited-purpose trust company organized under the New YorkBanking Law, a "banking organization" within the meaning of the New York Banking Law, a member of the FederalReserve System, a "clearing corporation" within the meaning of the New York Uniform Commercial Code, and a "clearingagency" registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934. DTC holds andprovides asset servicing for over 3.5 million issues of U.S. and non-U.S. equity issues, corporate and municipal debt issues,and money market instruments (from over 100 countries) that DTC's participants ("Direct Participants") deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions indeposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants'accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S.and non-U.S. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations.DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation ("DTCC"). DTCC is the holdingcompany for DTC, National Securities Clearing Corporation and Fixed Income Clearing Corporation, all of which areregistered clearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is alsoavailable to others such as both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearingcorporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly("Indirect Participants"). DTC has a Standard & Poor's rating of AA+. The DTC Rules applicable to its Participants areon file with the Securities and Exchange Commission. More information about DTC can be found at www.dtcc.com.

Purchases of Securities under the DTC system must be made by or through Direct Participants, which will receivea credit for the Securities on DTC's records. The ownership interest of each actual purchaser of each Security ("BeneficialOwner") is in turn to be recorded on the Direct and Indirect Participants' records. Beneficial Owners will not receive writtenconfirmation from DTC of their purchase. Beneficial Owners are, however, expected to receive written confirmationsproviding details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participantthrough which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Securities are tobe accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners.Beneficial Owners will not receive certificates representing their ownership interests in Securities, except in the event thatuse of the book-entry system for the Securities is discontinued.

2

To facilitate subsequent transfers, all Securities deposited by Direct Participants with DTC are registered in thename of DTC's partnership nominee, Cede & Co., or such other name as may be requested by an authorized representativeof DTC. The deposit of Securities with DTC and their registration in the name of Cede & Co. or such other DTC nomineedo not effect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Securities;DTC's records reflect only the identity of the Direct Participants to whose accounts such Securities are credited, which mayor may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account oftheir holdings on behalf of their customers.

Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to IndirectParticipants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangementsamong them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Ownersof Securities may wish to take certain steps to augment the transmission to them of notices of significant events with respectto the Securities, such as redemptions, tenders, defaults, and proposed amendments to the Security documents. For example,Beneficial Owners of Securities may wish to ascertain that the nominee holding the Securities for their benefit has agreedto obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their namesand addresses to the registrar and request that copies of notices be provided directly to them.

Redemption notices shall be sent to DTC. If less than all of the Securities within an issue are being redeemed,DTC's practice is to determine by lot the amount of the interest of each Direct Participant in such issue to be redeemed.

Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to Securities unlessauthorized by a Direct Participant in accordance with DTC's MMI Procedures. Under its usual procedures, DTC mails anOmnibus Proxy to School District as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.'sconsenting or voting rights to those Direct Participants to whose accounts Securities are credited on the record date(identified in a listing attached to the Omnibus Proxy).

Redemption proceeds, distributions, and dividend payments on the Securities will be made to Cede & Co., or suchother nominee as may be requested by an authorized representative of DTC. DTC's practice is to credit Direct Participants'accounts upon DTC's receipt of funds and corresponding detail information from School District or Paying Agent, onpayable date in accordance with their respective holdings shown on DTC's records. Payments by Participants to BeneficialOwners will be governed by standing instructions and customary practices, as is the case with securities held for theaccounts of customers in bearer form or registered in "street name," and will be the responsibility of such Participant andnot of DTC, Paying Agent, or School District, subject to any statutory or regulatory requirements as may be in effect fromtime to time. Payment of redemption proceeds, distributions, and dividend payments to Cede & Co. (or such other nomineeas may be requested by an authorized representative of DTC) is the responsibility of School District or Paying Agent,disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement of such paymentsto the Beneficial Owners will be the responsibility of Direct and Indirect Participants.

A Beneficial Owner shall give notice to elect to have its Securities purchased or tendered, through its Participant,to Paying Agent, and shall effect delivery of such Securities by causing the Direct Participant to transfer the Participant'sinterest in the Securities, on DTC's records, to Paying Agent. The requirement for physical delivery of Securities inconnection with an optional tender or a mandatory purchase will be deemed satisfied when the ownership rights in theSecurities are transferred by Direct Participants on DTC's records and followed by a book-entry credit of tenderedSecurities to Paying Agent's DTC account.

DTC may discontinue providing its services as depository with respect to the Securities at any time by givingreasonable notice to the School District or Paying Agent. Under such circumstances, in the event that a successor depositoryis not obtained, Security certificates are required to be printed and delivered.

The School District may decide to discontinue use of the system of book-entry-only transfers through DTC (ora successor securities depository). In that event, Security certificates will be printed and delivered to DTC.

The information in this section concerning DTC and DTC's book-entry system has been obtained from sourcesthat the School District believes to be reliable, but the School District takes no responsibility for the accuracy thereof.

3

TAX PROCEDURES

Article IX, Section 3, of the Michigan Constitution provides that the proportion of true cash value at whichproperty shall be assessed shall not exceed 50% of true cash value. The Michigan Legislature by statute has providedthat property shall be assessed at 50% of its true cash value, except as described below. The Michigan Legislature or theelectorate may at some future time reduce the percentage below 50% of true cash value.

On March 15, 1994, the electors of the State approved an amendment to the Michigan Constitution permittingthe Legislature to authorize ad valorem taxes on a non-uniform basis. The legislation implementing this constitutionalamendment added a new measure of property value known as "Taxable Value." Beginning in 1995, taxable property hastwo valuations -- State equalized valuation ("SEV") and Taxable Value. Property taxes are levied on Taxable Value.Generally, Taxable Value of property is the lesser of (a) the Taxable Value of the property in the immediately precedingyear, adjusted for losses, and increased or reduced by the lesser of the inflation rate or 5%, plus additions, or (b) theproperty's current SEV. Under certain circumstances, therefore, the Taxable Value of property may be different fromthe same property's SEV.

When property is sold or transferred, Taxable Value is adjusted to the SEV, which under existing law is 50%of the current true cash value. The Taxable Value of new construction is equal to current SEV. Taxable Value and SEVof existing property are also adjusted annually for additions and losses.

Responsibility for assessing taxable property rests with the local assessing officer of each township and city.Any property owner may appeal the assessment to the local board of review, to the Michigan Tax Tribunal, andultimately to the Michigan Courts.

The Michigan Constitution also mandates a system of equalization for assessments. Although the assessors foreach local unit of government within a county are responsible for actually assessing at 50% of true cash value, adjustedfor Taxable Value purposes, the final SEV and Taxable Value are arrived at through several steps. Assessments areestablished initially by the municipal assessor. Municipal assessments are then equalized to the 50% levels as determinedby the county's department of equalization. Thereafter, the State equalizes the various counties in relation to each other.SEV is important, aside from its use in determining Taxable Value for the purpose of levying ad valorem property taxes,because of its role in the spreading of taxes between overlapping jurisdictions, the distribution of various State aidprograms, State revenue sharing and in the calculation of debt limits.

Property that is exempt from property taxes, e.g., churches, government property, public schools, is not includedin the SEV and Taxable Value data in the Official Statement. Property granted tax abatements under Act 198, Public Actsof Michigan, 1974, amended, is recorded on a separate tax roll while subject to tax abatement. The valuation oftax-abated property is based upon SEV but is not included in either the SEV or Taxable Value data in the OfficialStatement except as noted. Under limited circumstances, other state laws permit the partial abatement of certain taxesfor other types of property for periods of up to 12 years.

TRANSFER OUTSIDE BOOK-ENTRY-ONLY SYSTEM

In the event that the book-entry-only system is discontinued, the following provisions would apply to the Bonds. The Paying Agent shall keep the registration books for the Bonds (the “Bond Register”) at its corporate trust office. Subject to the further conditions contained in the Resolutions, the Bonds may be transferred or exchanged for one ormore Bonds in different authorized denominations upon surrender thereof at the corporate trust office of the PayingAgent by the registered owners or their duly authorized attorneys; upon surrender of any Bonds to be transferred orexchanged, the Paying Agent shall record the transfer or exchange in the Bond Register and shall authenticatereplacement bonds in authorized denominations; during the fifteen (15) days immediately preceding the date of mailing(the “Record Date”) of any notice of redemption or any time following the mailing of any notice of redemption, thePaying Agent shall not be required to effect or register any transfer or exchange of any Bond which has been selectedfor such redemption, except the Bonds properly surrendered for partial redemption may be exchanged for new Bondsin authorized denominations equal in the aggregate to the unredeemed portion; the School District and Paying Agentshall be entitled to treat the registered owners of the Bonds, as their names appear in the Bond Register as of theappropriate dates, as the owners of such Bonds for all purposes under the Resolutions. No transfer or exchange madeother than as described above and in the Resolutions shall be valid or effective for any purposes under the Resolutions.

4

SOURCES OF SCHOOL OPERATING REVENUE

On March 15, 1994, the electors of the State of Michigan approved a ballot proposition to amend the StateConstitution of 1963, in part, to increase the State sales tax from 4% to 6% as part of a complex plan to restructure thesource of funding of public education (K-12) in order to reduce reliance on local property taxes for school operatingpurposes and to reduce the per pupil finance resource disparities among school districts. The Legislature has appropriatedfunds to establish a base foundation allowance in 2015/16 ranging from $7,391 to $8,169 per pupil, depending upon thedistrict's 1993/94 revenue. In the future, the foundation allowance may be adjusted annually by an index based upon thechange in revenues to the State school aid fund and change in the total number of pupils statewide and the spread betweenthe high and low per pupil allowance is reduced. The foundation allowance is funded by locally raised property taxes plusState aid. The revenues for the State's contribution to the foundation allowance are derived from a mix of taxing sources,including, but not limited to, a statewide property tax of 6 mills on all taxable property¹, a State sales and use tax, a realestate transfer tax and a cigarette tax. See "STATE AID PAYMENTS" in this Official Statement for further information.

School districts are required to levy a local property tax of not more than 18 mills or the number of mills leviedin 1993 for school operating purposes, whichever is less, on non-homestead properties² in order for the school district toreceive its per pupil foundation allowance. An intermediate school district may seek voter approval for three enhancementmills for distribution to local constituent school districts on a per pupil basis. Proceeds of the enhancement mills are notcounted toward the foundation allowance. Furthermore, school districts whose per pupil foundation allowance in 2015/16calculates to an amount in excess of $8,169 are authorized to levy additional millage to obtain the foundation allowance,first by levying such amount of the 18 mills against homestead property³ as is necessary to hold themselves harmless and,if the 18 mills is insufficient, to then levy such additional mills against all property uniformly as is necessary to obtain thefoundation allowance. The School District's per pupil foundation allowance does not exceed $8,169, and the School Districtdoes not levy such additional millage. State aid appropriations and the payment schedule for state aid may be changed bythe Legislature at any time. See “STATE AID PAYMENTS” in this Official Statement for further information.

Public Act 196 of 2014 ("Act 196") amended the State School Aid Act for the 2014/15 fiscal year and increasedthe School District's per pupil foundation allowance to $7,126. Act 196 included a one-time equity per pupil funding of$125 per pupil that the School District is receiving because its foundation allowance would otherwise be below $7,126. Act 196 included an additional payment to the School District to partially offset increases in the retirement plancontribution rate for the period October 1, 2014 to September 30, 2015. Act 196 also included grant funding equal to $50per pupil (a $2 decline in the per pupil amount as compared to 2013/14) for school districts if they satisfy 7 out of 9 "bestpractices" relating to health and other benefits coverage, competitive bidding for certain vendor services, schools of choice,online instruction programs or blended learning opportunities, a dashboard/report card of the School District's financialmanagement efforts, compensation methods for teachers and administrators that significantly factor performance andaccomplishments, use of collective bargaining agreements that omit statutorily prohibited subjects of bargaining,implementation of a comprehensive guidance and counseling program, and opportunities for K to 8 pupils to completecoursework or other learning experiences equivalent to 1 credit in a language other than English. The Board andAdministration satisfied such "best practices" requirements and the School District included such grant funding in its2014/15 General Fund Budget.

Public Act 85 of 2015 ("Act 85") amended the State School Aid Act for the 2015/16 fiscal year and increased theSchool District's per pupil foundation allowance to $7,391. The 2015/16 per pupil foundation allowance is calculated basedupon the 2014/2015 per pupil foundation allowance, plus the 2014/15 per pupil equity payment, plus $140 for a netincrease per pupil of 105 for the School District. The prior fiscal year's per pupil equity payment and "best practices" and"performance based" grants are eliminated. Act 85 also increased funding for at risk students and appropriated new fundsfor early literacy, career and technical education middle college, and college and career preparation programs for eligibleschool districts. The Board and Administration anticipate that the School District will be eligible for said additional fundingand the School District has included such funding in its 2015/16 General Fund Budget.

¹ “Taxable property” does not include industrial personal property.

² “Non-homestead property” includes all taxable property other than principal residence, qualified agricultural property, qualified forestryproperty, supportive housing property, property occupied by a public school academy and industrial personal property. Commercialpersonal property is exempt from the first 12 mills of not more than 18 mills levied by school districts.

³ “Homestead property”, in this context, means principal residence, qualified agricultural property, qualified forestry property, supportivehousing property, property occupied by a public school academy, industrial personal property and commercial personal property.

5

THE SOURCES OF THE SCHOOL DISTRICT'S OPERATING REVENUE DO NOT IMPACT THETAXING AUTHORITY OF THE SCHOOL DISTRICT FOR PAYMENT OF GENERAL OBLIGATION UNLIMITEDTAX SCHOOL BONDS AND DO NOT AFFECT THE OBLIGATION OF THE SCHOOL DISTRICT TO LEVYTAXES FOR PAYMENT OF DEBT SERVICE ON GENERAL OBLIGATION UNLIMITED TAX BONDS OF THESCHOOL DISTRICT, INCLUDING THE BONDS OFFERED HEREIN.

MICHIGAN PROPERTY TAX REFORM

On November 5, 2013, March 28, 2014, and April 1, 2014, Governor Snyder signed into law a package of billsamending and replacing legislation enacted in 2012 to phase-out most personal property taxes in Michigan. The bills werecontingent on Michigan voters approving a ballot question authorizing a new municipal entity, the Local CommunityStabilization Authority ("LCSA"), to levy a local component of the statewide use tax and distribute that revenue to localunits of government to offset their revenue losses resulting from the personal property tax reform. On August 5, 2014,voters approved that ballot question.

The bill package, together with the original 2012 legislation, created two new exemptions from the personalproperty tax. Under the "small taxpayer exemption," the commercial and industrial personal property of each owner witha combined true cash value in a local tax collecting unit of less than $80,000 is exempt from ad valorem taxes in thatcollecting unit beginning in 2014. For businesses that do not qualify for the "small taxpayer exemption," all "eligiblemanufacturing personal property" (personal property used more than 50% of the time in industrial processing or directintegrated support) purchased and placed into service before 2006 or during or after 2013 becomes exempt beginning in2016. Taxation on "eligible manufacturing personal property" placed into service after 2006 but before 2013 will bephased-out over time; with the exemption taking effect after the property has been in service for the immediately preceding10 years. The legislation extends certain personal property tax exemptions and tax abatements for technology parks,industrial facilities and enterprise zones that were to expire after 2012, until the voter-approved personal property taxexemptions take effect.

Pursuant to voter approval in August 2014, the legislation also includes a formula to reimburse school districtsfor 100% of their lost operating millage revenue and lost sinking fund millage revenue. To provide the reimbursement, thelegislation reduces the state share of the use tax and authorizes the LCSA to levy a local component of the use tax anddistribute that revenue to qualifying local units. However, the reimbursement for the school district's operating millage willcome from the state use tax component, which is deposited into the school state aid fund.¹ While the legislation providesreimbursement for prospective school operating losses, school districts will only be reimbursed for debt losses attributableto debt obligations that voters approved before January 1, 2013 or were incurred before January 1, 2013. For the 2014-2015and 2015-2016 fiscal years, the State of Michigan will appropriate sufficient funds to the LCSA to reimburse schooldistricts for such debt losses.

Because the Bonds are associated with debt obligations that received voter approval before January 1, 2013,the School District will be reimbursed for debt millage revenue it could have otherwise generated to make payments onthe Bonds.

¹ Because the reimbursement funds are deposited into the state school aid fund, the legislature may, in the future, change the funding formulas in theState School Aid Act of 1979 or appropriate funds therein for other purposes.

LITIGATION

The School District has not been served with any litigation, administrative action or proceeding, nor, to theknowledge of the School District, is there threatened any litigation restraining or enjoining the issuance or delivery ofthe Bonds or in any manner questioning the proceedings and authority under which the Bonds are to be issued oraffecting the validity of the Bonds.

TAX MATTERS

State of Michigan

In the opinion of Thrun Law Firm, P.C., East Lansing, Michigan (“Bond Counsel”), based on its examinationof the documents described in its opinion, under existing State statutes, regulations and court decisions, the Bonds andthe interest thereon are exempt from all taxation in the State of Michigan, except inheritance and estate taxes and taxeson gains realized from the sale, payment or other disposition thereof.

6

Federal

In the opinion of Bond Counsel based upon its examination of the documents described in its opinion, underexisting statutes, regulations, rulings and court decisions, the interest on the Bonds is excluded from gross income forfederal income tax purposes and is not an item of tax preference for purposes of the federal alternative minimum taximposed on individuals and corporations. It should be noted, however, that certain corporations must take into accountinterest on the Bonds in determining adjusted net current earnings for the purpose of computing the alternative minimumtax imposed on such corporations. The opinions set forth in the preceding sentences are subject to the condition that theSchool District comply with all requirements of the Internal Revenue Code of 1986, as amended (the “Code”), that mustbe satisfied subsequent to the issuance of the Bonds in order that interest thereon be, or continue to be, excluded fromgross income for federal income tax purposes. Failure to comply with certain of such requirements may cause theinclusion of interest on the Bonds in gross income for federal income tax purposes to be retroactive to the date ofissuance of the Bonds. Bond Counsel will express no opinion regarding other federal tax consequences arising withrespect to the Bonds.

There are additional federal tax consequences relative to the Bonds and the interest thereon. The following isa general description of some of these consequences but is not intended to be complete or exhaustive and investorsshould consult with their tax advisors with respect to these matters. Prospective purchasers of the Bonds should be awarethat (i) interest on the Bonds is included in the effectively connected earnings and profits of certain foreign corporationsfor purposes of calculating the branch profits tax imposed by Section 884 of the Code, (ii) interest on the Bonds maybe subject to a tax on excess net passive income of certain S Corporations imposed by Section 1375 of the Code, (iii)interest on the Bonds is included in the calculation of modified adjusted gross income for purposes of determining thetaxability of social security or railroad retirement benefits, (iv) the receipt of interest on the Bonds by life insurancecompanies may affect the federal tax liability of such companies, (v) in the case of property and casualty insurancecompanies, the amount of certain loss deductions otherwise allowed is reduced by a specific percentage of, among otherthings, interest on the Bonds,(vi) holders of the Bonds may not deduct interest on indebtedness incurred or continuedto purchase or carry the Bonds, and (vii) commercial banks, thrift institutions and other financial institutions may deducttheir costs of carrying certain obligations such as the Bonds.

Original Issue Premium

For federal income tax purposes, the difference between the initial offering prices to the public (excludingbondhouses and brokers) at which certain Bonds, as set forth on the cover of this Official Statement, are sold and theamounts payable at maturity thereof (the “Premium Bonds”), constitutes for the original purchasers of the PremiumBonds an amortizable bond premium. Such amortizable bond premium is not deductible from gross income but is takeninto account by certain corporations in determining adjusted current earnings for the purpose of computing the alternativeminimum tax, which may also affect liability for the branch profits tax imposed by Section 884 of the Code. The amountof amortizable bond premium allocable to each taxable year is generally determined on the basis of a taxpayer’s yieldto maturity determined by using the taxpayer’s basis (for purposes of determining loss on sale or exchange) of suchPremium Bonds and compounding at the close of each six-month accrual period. The amount of amortizable bondpremium allocable to each taxable year is deducted from the taxpayer’s adjusted basis of such Premium Bonds todetermine taxable gain upon disposition (including sale, redemption or payment on maturity) of such Premium Bonds.

Future Developments

No assurance can be given that any future legislation or clarifications or amendments to the Code, if enactedinto law, will not contain proposals which could cause the interest on the Bonds to be subject directly or indirectly tofederal or state income taxation, adversely affect the market price or marketability of the Bonds, or otherwise preventbondholders from realizing the full current benefit of the status of the interest thereon.

It is to be understood that the rights of the holders of the Bonds and the enforceability thereof may be subjectto bankruptcy, insolvency, reorganization, moratorium and other similar laws affecting creditors’ rights heretofore orhereafter enacted to the extent constitutionally applicable and that their enforcement may also be subject to the exerciseof judicial discretion in appropriate cases.

INVESTORS SHOULD CONSULT WITH THEIR TAX ADVISORS AS TO THE TAX CONSEQUENCESOF THEIR ACQUISITION, HOLDING OR DISPOSITION OF THE BONDS, INCLUDING THE TREATMENT OFORIGINAL ISSUE PREMIUM.

7

QUALIFIED BY THE MICHIGAN DEPARTMENT OF TREASURY

The School District has received a letter from the Department of Treasury of the State of Michigan stating thatthe School District is in material compliance with the criteria of the Revised Municipal Finance Act, Act No. 34, PublicActs of Michigan, 2001 (“Act 34”) for a municipality to be granted “qualified status” to issue municipal securitieswithout further approval by the Michigan Department of Treasury.

CONTINUING DISCLOSURE

Prior to delivery of the Bonds the School District will execute a Continuing Disclosure Agreement (the“Agreement”) for the benefit of the holders of the Bonds and Beneficial Owners to send certain information annuallyand to provide notice of certain events to certain information repositories pursuant to the requirements of Rule 15c2-12(b)(5) (the “Rule”) adopted by the Securities and Exchange Commission under the Securities Exchange Act of 1934. The information to be provided on an annual basis, the events which will be noticed on an occurrence basis, and the otherterms of the Agreement are set forth in “APPENDIX C - FORM OF CONTINUING DISCLOSURE AGREEMENT.” Additionally, the School District shall provide certain annual financial information and operating data, generallyconsistent with the information in the tables under the headings “PROPERTY VALUATIONS - Historical Valuations”“MAJOR TAXPAYERS”, “TAX RATES - Clare Public Schools”, “STATE AID PAYMENTS”, “TAX LEVIES ANDCOLLECTIONS”, “LABOR FORCE”, “PENSION FUND”, “DEBT STATEMENT - DIRECT DEBT”, “SCHOOLBOND QUALIFICATION AND LOAN PROGRAM”, “SCHOOL ENROLLMENT” and “GENERAL FUND BUDGETSUMMARY” herein.

A failure by the School District to comply with the Agreement will not constitute an event of default under theResolutions authorizing issuance of the Bonds and holders of the Bonds or Beneficial Owners are limited to the remediesdescribed in the Agreement. A failure by the School District to comply with the Agreement must be reported inaccordance with the Rule and must be considered by any broker, dealer or municipal securities dealer beforerecommending the purchase or sale of the Bonds in the secondary market. Consequently, such failure may adverselyaffect the transferability and liquidity of the Bonds and their market price.

Except as disclosed below, the School District has not in the previous five years, failed to comply, in all materialrespects, with any previous continuing disclosure agreements executed by the School District pursuant to the Rule. Whilethe School District filed its audited financial statements and annual disclosure information timely over the past five yearsin compliance, in all material respects, with the previous continuing disclosure agreements executed by the SchoolDistrict, the School District filed late material event notices of, the rating on its bonds qualified for the State School BondLoan Program and ratings affecting the bond insurer for certain prior bond issues of the School District. To the best ofthe School District’s knowledge, the School District did not receive notification from bond insurer or the rating agenciesof the rating changes for the bond insurer or the State School Bond Loan Program.

BOND COUNSEL’S RESPONSIBILITY

The fees of Thrun Law Firm, P.C., East Lansing, Michigan (“Bond Counsel”) for services rendered inconnection with its approving opinion are expected to be paid from Bond proceeds. Except to the extent necessary toissue its approving opinion as to the validity of the Bonds and tax matters relating to the Bonds and the interest thereon,and except as stated below, Bond Counsel has not been retained to examine or review, and has not examined or reviewedany financial documents, statements or materials that have been or may be furnished in connection with the authorization,issuance or marketing of the Bonds and accordingly will not express any opinion with respect to the accuracy orcompleteness of any such financial documents, statements or materials.

Bond Counsel has reviewed the statements made in this Official Statement on the cover page and under theheading "Information for Bidders", insofar as such statements summarize the language and effect of the Resolutions, theBonds, the Continuing Disclosure Agreement, the Constitution of the State of Michigan, the laws of the State ofMichigan and federal income tax laws and, further, the statements under such headings are fair and accurate summariesthereof in all material respects. Except as otherwise disclosed on pages herein, Bond Counsel has not been retained toreview and has not reviewed any other portion of this Official Statement for accuracy or completeness, and has not madeinquiry of any official or employee of the School District or any other person and has made no independent verificationof such other portions hereof, and further has not expressed and will not express an opinion as to any portions hereof.

8

FINANCIAL CONSULTANT’S OBLIGATION

Public Financial Management, Inc., Ann Arbor, Michigan (the "Financial Advisor"), has been retained by theSchool District to provide certain financial advisory services. The Financial Advisor assisted in the preparation of theOfficial Statement and in other matters relating to the planning, structuring and issuance of the Bonds.

The information contained in the Official Statement was prepared in part by the Financial Advisor and is basedon information supplied by various officials from records, statements and reports required by various local, county orstate agencies of the State of Michigan. To the best of the Financial Advisor's knowledge, all of the informationcontained in the Official Statement, which it assisted in preparing, while it may be summarized is complete and accurate. However, the Financial Advisor has not and will not independently verify the completeness and accuracy of theinformation contained in the Official Statement.

The Financial Advisor is a registered municipal advisor and is not engaged in the business of underwriting,marketing or trading of municipal securities or any other negotiable instrument. The Financial Advisor's duties,responsibilities and fees arise solely as financial advisor to the School District. The Financial Advisor's fees are expectedto be paid from Bond proceeds.

Further information concerning the Bonds may be secured from Public Financial Management, Inc., 3989Research Park Drive, Ann Arbor, Michigan 48108. Telephone: 734-668-6688.

CREDIT RATINGS

Standard & Poor's Ratings Services (“S&P”) has assigned, as the of the date of delivery of the Bonds, itsunderlying municipal bond rating of “A” to the Bonds.

S&P has also assigned its municipal bond rating of “AA” to the Bonds with the understanding that upon deliveryof the Bonds, a municipal bond insurance policy will be issued by Build America Mutual Assurance Company (“BAM”)to insure the Bonds.

The aforementioned ratings will reflect the sole view of the rating agency and there is no assurance that suchratings will be continued for any period of time, or that it will not be revised upwards or downwards or be withdrawn;a revision, suspension, or withdrawal of the rating may have an effect on the market price of these securities and shouldbe noted.

A brief description of the Standard & Poor’s rating definitions reads as follows:

Standard & Poor’s Ratings Services

Bonds rated “AAA” have the highest rating assigned. Capacity to pay interest and repayprincipal is extremely strong.

Bonds rated “AA” qualify as high quality debt obligations. Capacity to pay principal andinterest is very strong, and in the majority of instances they differ from “AAA” issues only in a smalldegree.

Bonds rated “A” have a strong capacity to pay principal and interest, although they aresomewhat more susceptible to the adverse effects of change in circumstances and economic conditions.

Bonds rated “BBB” are regarded as having an adequate capacity to pay interest and repayprincipal. Whereas it normally exhibits adequate protection parameters, adverse economic conditionsor changing circumstances are more likely to lead to a weakened capacity to pay interest and repayprincipal for debt in this category than in higher rated categories.

Plus (+) or Minus (-): To provide more detailed indications of credit quality, the ratings from“AA” to “BBB” may be modified by the addition of a plus or minus sign to show relative standingwithin the major rating categories.

9

ESTIMATED SOURCES AND USES OF FUNDS

Sources of FundsPar Amount of Bonds $2,450,000.00 Production 69,511.60 Total Sources $2,519,511.60

Uses of FundsCapital Projects Account $2,411,612.38Deposit to Debt Fund 37,021.60Underwriter's Discount 23,990.00Bond Insurance 8,500.00Costs of Issuance 38,387.62Total Uses $2,519,511.60

10

CLARE PUBLIC SCHOOLSGENERAL FINANCIAL INFORMATION¹

AREA

The School District encompasses an area of 124.3 square miles.

POPULATION

The estimated population totals for the School District and the U.S. Census reported for the City of Clareare as follows:

School City ofYear District* Clare2010 8,546 3,0712000 8,396 3,1731990 6,000 3,013

* Estimated based on an extrapolation of the U.S. Census figures of the local units within the School District.

PROPERTY VALUATIONS

In accordance with Act 539, Public Acts of Michigan, 1982, as amended, and Article IX, Section 3 of theMichigan Constitution, the ad valorem State Equalized Valuation (SEV) represents 50% of true cash value. SEV doesnot include any value of tax exempt property (e.g. churches, governmental property) or property granted tax abatementsunder Act 198, Public Acts of Michigan, 1974, as amended. As a result of Proposal A, ad valorem property taxesare assessed on the basis of taxable value, which is subject to assessment caps. SEV is used in the calculation ofdebt margin and true cash value. See “TAX PROCEDURES” herein for more information.

Taxable property in the School District is assessed by the local municipal assessor and is subject to review bythe County Equalization Department.

Historical Valuations*

Principal Non-Principal Total State EqualizedYear Residence Residence Taxable Value Valuation2015 $152,728,028 $91,205,318 $243,933,346 $301,726,277 2014 148,130,709 91,369,780 239,500,489 293,205,501 2013 147,226,583 92,149,599 239,376,182 288,989,153 2012 145,809,082 84,960,304 230,769,386 282,185,950 2011 143,447,313 86,068,934 229,516,247 288,553,795

* See "MICHIGAN PROPERTY TAX REFORM" herein for information regarding tax changes effective in the 2014 and 2016 tax years.

¹ Information included in this Official Statement under the headings “General Financial Information, “General Economic Information,” and “GeneralSchool Information” was obtained from the School District, unless otherwise noted.

11

0

5 0

1 0 0

1 5 0

2 0 0

2 5 0

3 0 0

3 5 0

2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5

M ill io n s

Y e a r

H is to ric a l Va lua tio ns

T a xa b le V a l ua t i o n S t a te E q u a li z ed V a lu a ti o n

2015 Taxable Value $243,933,346Plus: 2015 IFT Taxable Valuation* 3,931,940

Total Equivalent Valuation $247,865,286

* Millage is levied at half rate against the amount listed. See “PROPERTY VALUATIONS - Industrial Facilities Tax (IFT)” herein.

Per Capita Valuation

2015 Per Capita Taxable Value $28,543.572015 Per Capita State Equalized Valuation $35,306.142015 Per Capita Estimated True Cash Valuation $70,612.28

Industrial Facilities Tax (IFT)

Under the provisions of Act 198 of the Public Acts of Michigan, 1974 (“Act 198"), plant rehabilitation districtsand/or industrial development districts may be established. Businesses in these districts are offered certain property taxincentives to encourage restoration or replacement of obsolete facilities and to attract new facilities to the area. Anindustrial facilities tax (“IFT”) is paid, at a lesser effective rate and in lieu of ad valorem property taxes, on suchfacilities for a period of up to 12 years. Qualifying facilities are issued abatement certificates for specific periods.

After expiration of the abatement certificate, the then-current SEV of the facility is returned to the ad valoremtax roll. The owner of such facility may obtain a new certificate, provided it has complied with the provisions of Act198.

The 2015 Taxable Value for the properties which have been granted IFT abatements within the SchoolDistrict’s boundaries is $3,931,940 which is subsequently taxed at half rate. For further information see "PROPERTYVALUATIONS - Historical Valuations" herein.

As part of the phase-out of Michigan's property tax on personal property, if a facility and personal propertywithin that facility were subject to an industrial facilities exemption on December 31, 2011, that exemption will remainintact and continue to be subject to the industrial facilities tax until the expiration of the exemption at which time theeligible personal property associated with the industrial facilities exemption becomes exempt under the new law. See"MICHIGAN PROPERTY TAX REFORM" above.

12

Agricultural16.55%

Commercial15.73%

Industrial3.38%

Residential53.37%

Personal Commercial

2.30%

Personal Industrial

2.05%

Personal Utility6.62%

Taxable Valuation by Use

TAX BASE COMPOSITION†

A breakdown of the School District’s 2015 Taxable Value by municipality, class and use are as follows:

Principal¹ Non-Principal¹ Total Taxable Percent ofMunicipality Residence Residence Value TotalClare County

Arthur Township $5,018,352 $892,870 $5,911,222 2.42%Grant Township 35,086,138 12,358,712 47,444,850 19.45Hatton Township 5,351,872 1,301,528 6,653,400 2.73Sheridan Township 34,029,570 10,769,604 44,799,174 18.37City of Clare 30,001,229 43,474,895 73,476,124 30.12

Isabella County Vernon Township 26,474,361 8,570,642 35,045,003 14.37Wise Township 13,246,666 4,921,936 18,168,602 7.44City of Clare 3,519,840 8,915,131 12,434,971 5.10

TOTAL $152,728,028 $91,205,318 $243,933,346 100.00%

¹ See “SOURCES OF SCHOOL OPERATING REVENUE” in this Official Statement for further details.

Taxable Percent ofClass Value TotalReal Property $217,173,851 89.03% Personal Property 26,759,495 10.97TOTAL $243,933,346 100.00%

UseAgricultural $40,374,846 16.55%Commercial 38,372,248 15.73Industrial 8,242,737 3.38Residential 130,184,020 53.37Personal Commercial 5,599,500 2.30Personal Industrial 4,999,400 2.05Personal Utility 16,160,595 6.62TOTAL $243,933,346 100.00%

† See "MICHIGAN PROPERTY TAX REFORM" herein for information regarding tax changes effective in the 2014 and 2016 tax years

Source: Clare and Isabella Counties

MAJOR TAXPAYERS

The ten largest taxpayers in the School District and their 2015 Taxable Value totals and Industrial FacilitiesTax Valuation totals are as follows:

Taxable IFT TotalTaxpayer Product/Service Value + Valuation = Valuation

Consumers Energy Co Utility $15,415,241 $0 $15,415,241Alro Steel Corporation Steel 3,442,600 1,341,700 4,784,300R & R Real Estate Real estate 2,123,802 0 2,123,802Doherty Hotel, Inc. Hotel 2,011,300 0 2,011,300Stageright Corporation Sheet metal 1,364,200 632,300 1,996,500Tendercare Holdings LLC Nursing home 1,389,388 0 1,389,388Poet Brothers /Jay's Sporting Goods Retail 1,350,891 0 1,350,891Red Hook Properties/Jim's Body Shop Auto exterior repair 1,307,543 0 1,307,543Chodaka LLC Restaurant, groceries 1,294,000 0 1,294,000Packard Farms Agriculture 1,111,802 0 1,111,802TOTAL $30,810,767 $1,974,000 $32,784,767

The Taxable Valuations of the major taxpayers represent 12.63% of the School District's 2015 TaxableValuation of $243,933,346 and their Total Valuations represent 13.20% of the School District's Total EquivalentValuation of $247,865,286.

Source: Clare and Isabella Counties

13

CONSTITUTIONAL MILLAGE ROLLBACK

Article IX, Section 31 of the Michigan Constitution (also referred to herein as the “Headlee Rollback”) requiresthat if the total value of existing taxable property (State Equalized Valuation) in a local taxing unit, exclusive of newconstruction and improvements, increases faster than the U.S. Consumer Price Index from one year to the next, themaximum authorized tax rate for that local taxing unit must be reduced through a Millage Reduction Fraction unless newmillage is authorized by a vote of the electorate of the local taxing unit.

TAX RATES - (Per $1,000 of Valuation)†

Each school district, county, township, special authority and city has a geographical definition which constitutesa tax district. Since local school districts and the county overlap either a township or a city, and intermediate schooldistricts overlap local school districts and county boundaries, the result is many different tax rate districts.

Clare Public Schools 2015 2014 2013 2012 2011Operating Non-Principal Residence 18.0000 18.0000 17.5464 17.5464 18.0000Debt 3.2800 3.2800 3.2800 3.4400 3.5000

TOTAL PRINCIPAL RESIDENCE 3.2800 3.2800 3.2800 3.4400 3.5000TOTAL NON-PRINCIPAL RESIDENCE 21.2800 21.2800 20.8264 20.9864 21.5000

The School District levies 18 mills for operating purposes on non-principal residence property and authorizeddebt millage on all principal residence and non-principal residence property located within the School District. TheSchool District’s operating millage expires with the December 2016 levy. See “SOURCES OF SCHOOL OPERATINGREVENUE” in this Official Statement.

† See "MICHIGAN PROPERTY TAX REFORM" herein for information regarding tax changes effective in the 2014 and 2016 tax years

Other Major Taxing Units 2014 2013State Education Tax¹ 6.0000 6.0000Clare County 6.1072 5.8372City of Clare 19.0000 19.0000Isabella County 9.3996 9.1720Clare-Gladwin RESD 2.0385 2.0385Mid-Michigan Community College 1.2232 1.2232

¹ The State of Michigan levies 6.00 mills for school operating purposes on all principal residence and non-principal residence property located

within the School District. Source: Clare and Isabella Counties

STATE AID PAYMENTS

The School District's primary source of funding for operating costs is the State School Aid per pupil foundationallowance. The base foundation allowance has been set from $7,391 to $8,169 per pupil for fiscal year 2015/2016. Infuture years, this allowance may be adjusted by an index based upon the change in revenues to the state school aid fundand the change in the total number of pupils statewide. The State may reduce State School Aid appropriations at any timeif the State's revenues do not meet budget expectations. See "SOURCES OF SCHOOL OPERATING REVENUE" hereinfor additional information.

The following table shows a history and current estimates of the School District's total State School Aidrevenues, including categoricals and other amounts, the State Amount Received per Pupil and the Foundation Allowanceper Pupil.

14

State Amount FoundationReceived Allowance

Year Total per Pupil per Pupil2015/16 (Estimate) $10,717,923 $6,342 $7,3912014/15* 10,260,481 5,910 7,1262013/14 10,071,431 5,932 6,9662012/13 9,558,799 5,813 6,8462011/12 9,964,861 6,334 7,316

* The School District has received a $125 per pupil one-time equity payment for the 2014/15 fiscal year.Source: Michigan Department of Education

TAX LEVIES AND COLLECTIONS

The School District's fiscal year begins July 1 and ends June 30. School District property taxes are dueDecember 1 of each fiscal year and are payable without penalty or interest on or before the following February 14. Allreal property taxes remaining unpaid on March 1st of the fiscal year following the levy are turned over to the CountyTreasurers for collection. Clare and Isabella Counties (the “Counties”) annually pay from their Tax Payment Fundsdelinquent taxes on real property to all taxing units in the Counties, including the School District, shortly after the datedelinquent taxes are returned to the County Treasurers for collection.

A history of operating tax levies and collections for the School District are as follows:

Levy Operating Collections to Collections Plus FundingYear Tax Levy March 1 of Following Year To June 30 of Following Year2015 $1,639,277 N/A N/A2014 1,601,277 $1,505,916 94.04% $1,601,277 100.00%2013 1,623,305 1,533,381 94.46 1,623,305 100.002012 1,551,087 1,419,540 91.52 1,551,087 100.002011 1,536,213 1,385,852 90.21 1,536,213 100.00

The Tax Payment Fund is financed through the issuance of General Obligation Limited Tax Notes (GOLTNs) bythe Counties. Although the School District anticipates the continuance of this program by the Counties, the ability of theCounties to issue such GOLTNs is subject to market conditions at the time of offering. In addition, Act 206, Public Actsof Michigan, 1893, as amended, provides in part that: “The primary obligation to pay to the county the amount of taxesand interest on the taxes shall rest with the local taxing units and the state for the state education tax under the stateeducation tax act... If the delinquent taxes that are due and payable to the county are not received by the county for anyreason, the county has full right of recourse against the taxing unit or to the state for the state education tax... to recoverthe amount of the delinquent taxes and interest...” On the third Tuesday in July in each year, a tax sale is held by theCounties at which lands delinquent for taxes assessed in the third year preceding the sale, or in a prior year, are sold forthe total of the unpaid taxes of those years. Pursuant to Act 123, Public Acts of Michigan, 1999, as amended, property owners with taxes that are two years delinquent will be foreclosed and the property will be sold at public auction. Forexample, property owners who fail to pay their 2015 delinquent property taxes will lose their property in March 2018.

LABOR FORCE

A breakdown of the number of salaried employees of the School District and their affiliations with organizedgroups are as follows:

ContractEmployees Number Bargaining Unit ExpirationAdministrators 7 Non-Affiliated N/ATeachers 84 MEA 06/30/2016Secretaries 8 MEA 06/30/2016Aides 24 MEA 06/30/2016Maintenance/Custodians 14 Non-Affiliated N/ATransportation 10 Non-Affiliated N/ANon-Affiliated 9 N/A N/ATOTAL STAFF 156

The School District has not experienced a strike by any of its bargaining units within the past ten years.

15

PENSION FUND

For the period October 1 through September 30, the School District pays an amount equal to a percentage of itsemployees' wages to the Michigan Public School Employees Retirement System ("MPSERS"), which is administered bythe State of Michigan. These contributions are required by law and are calculated by using the contribution rates andperiods provided in the table below of the employees' wages. The employer contribution rate for employees who firstworked July 1, 2010 or later (Pension Plus members) for the time period July 1, 2010 to September 30, 2010 was 15.44%.For other employees, the rate was 16.94% through September 30, 2010. Effective October 1, 2010, the employercontribution rate for all employees except Pension Plus members increased to 19.41%. For Pension Plus members, theemployer contribution rate was 17.91%.

On June 28, 2010, the Michigan Court of Claims issued an injunction in response to a challenge to the authorityof the State to require employees who began working before July 1, 2010, to contribute 3% of reportable wages to theretiree health care trust at MPSERS. As a result, the State has adjusted the contribution rate due on employees wages paidbetween November 1, 2010 and September 30, 2011 to 20.66% for members who first worked prior to July 1, 2010 and19.16% for Pension Plus members. In March 2011, the Court of Claims granted the plaintiffs' motions for summarydisposition finding that the mandatory 3% contribution violated both the U.S. and Michigan Constitutions. The Stateappealed the ruling to the Michigan Court of Appeals. In August of 2012, the Court of Appeals affirmed the decision ofthe Court of Claims. The State of Michigan has filed an Application for Leave to Appeal with the Michigan Supreme Court.

On September 4, 2012, the governor signed Public Act 300 of 2012 ("Act 300") to reform MPSERS. Act 300made changes to employee contributions to their pensions and retiree health benefits, shifting the 3% pension contributionto retiree health benefits. Act 300 increased the amount retirees contribute to their health insurance, and employees arerequired to choose to increase contributions to their pension plan, maintain current contribution rates and freeze existingbenefits, or freeze existing pension benefits and move into a defined contribution plan. In addition, the legislation endedretiree health benefits for new hires. On November 29, 2012, the Ingham County Circuit Court, sitting as the Court ofClaims, ruled that the substantive provisions of the Act 300 were constitutional except for one particular provision relatingto an "election window" for healthcare benefits. The Legislature promptly adopted legislation which was signed into lawby the Governor addressing the constitutional concerns of the election window raised by the Court of Claims. Two publicschool employee unions appealed the Court of Claims decision to the Michigan Court of Appeals, which affirmed the Courtof Claims' ruling on January 14, 2014. The unions appealed the matter to the Michigan Supreme Court. On April 8, 2015,the Michigan Supreme Court upheld Act 300 by ruling that the required employee elections to participate and contributeto retiree healthcare and defined benefit pension plans are constitutional under both the Michigan and United StatesConstitutions. It is unknown at this time if plaintiffs will appeal this decision to the federal court. The Michigan SupremeCourt has not yet ruled on the mandatory 3% retiree health contributions made by members from July 2010 to September2012 before Act 300 took effect.