PUBLIC FINANCIAL MANAGEMENT ACCOUNTING AND AUDIT ... · PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND...

36

PUBLIC FINANCIAL MANAGEMENT ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK June 2016 This publication is made possible by the support of the American people through the United States Agency for International Development (USAID). The contents of this report are the sole responsibility of Cardno Emerging Markets USA, Ltd. and do not necessarily reflect the views of USAID or the United States Government.

Transcript of PUBLIC FINANCIAL MANAGEMENT ACCOUNTING AND AUDIT ... · PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND...

PUBLIC FINANCIAL

MANAGEMENT

ACCOUNTING AND AUDIT

PARTICIPANT HANDBOOK

June 2016

This publication is made possible by the support of the American people through the United States Agency

for International Development (USAID). The contents of this report are the sole responsibility of Cardno Emerging Markets USA, Ltd. and do not necessarily reflect the views of USAID or the United States

Government.

I

Public Financial Management

Accounting and Audit

Participant Handbook

Prepared by: Cardno Emerging Markets USA, Ltd

Submitted to:

United States Agency for International Development

Contract No.:

Cooperative Agreement AID-617-10-00003

The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK I

TABLE OF CONTENTS FOREWORD .............................................................................................................................................................. III ACRONYMS ............................................................................................................................................................... IV

ABOUT THIS HANDBOOK ................................................................................................................................... V

1. PUBLIC FINANCIAL MANAGEMENT OVERVIEW .................................................................................1 1.1. OBJECTIVES .............................................................................................................................................. 1

1.2. WHAT IS PUBLIC FINANCIAL MANAGEMENT (PFM)? ............................................................. 1 1.3. CONTEXT OF PFM ................................................................................................................................ 1

1.4. RELEVANCE OF GOOD FINANCIAL MANAGEMENT .............................................................. 1 1.5. STATUS OF PFM AND CHALLENGES ............................................................................................. 1

1.5.1. Achievement of PFM Reforms .......................................................................................................... 2

1.6. ENABLING LEGAL FRAMEWORK .................................................................................................... 3 1.7. CONTENT OF ACCOUNTABILITY?................................................................................................ 3

1.7.1. The Accountability Cycle ................................................................................................................... 4 1.7.2. Key Accountability Support Documents........................................................................................ 4

1.8. ACTIVITY 1: PAYMENTS ACCOUNTABILITY .............................................................................. 5 2. ACCOUNTING-FINANCIAL REPORTING...............................................................................................6

2.1 OBJECTIVES .............................................................................................................................................. 6

2.2 WHAT IS ACCOUNTING ................................................................................................................... 6 2.2.1 Purpose of Accounting ............................................................................................................................ 6

2.2.2 Legal Requirements for Financial Reporting ...................................................................................... 6 2.3 FINANCIAL REPORTING PROCESS ................................................................................................. 6

2.4 MONTHLY FINANCIAL REPORTS.................................................................................................... 8 2.4.1 Quarterly Financial Statements ............................................................................................................. 8

2.4.2 Annual Financial Statements/Reports .................................................................................................. 9

2.5 ACTIVITY 2: FINANCIAL REPORTING ........................................................................................... 9 2.6 KEY STAKEHOLDERS AND THEIR ROLES IN FINANCIAL REPORTING............................ 9

2.7 TRANSPARENCY OF FINANCIAL INFORMATION.................................................................. 10 2.8 ACTIVITY 3: PUBLICATION OF FINANCIAL REPORTS AND OTHER OPERATIONAL

INFORMATION................................................................................................................................................... 10 2.9 WHAT TO PUBLISH ............................................................................................................................ 10

2.9.1 How to Publish ....................................................................................................................................... 10

2.10 BENEFITS OF PUBLISHING FINANCIAL STATEMENTS........................................................... 11 3. THE AUDIT PROCESS – OVERVIEW ....................................................................................................... 12

3.1 OBJECTIVES ............................................................................................................................................ 12 3.2 CONTEXT OF AUDIT ........................................................................................................................ 12

3.2.1 Purpose of Audits ................................................................................................................................... 12 3.3 LEGAL FRAMEWORK FOR PUBLIC SECTOR AUDITS IN UGANDA ................................. 12

3.4 TYPES OF AUDIT .................................................................................................................................. 13

3.5 THE AUDIT PROCESS ......................................................................................................................... 14 3.5.1 Activity 4 Internal /External Audit Cycle .......................................................................................... 14

3.6 KEY STAKEHOLDERS IN THE AUDIT PROCESS ....................................................................... 14 3.6.1 Activity 5: Roles of Audit stakeholders............................................................................................. 15

4. AUDIT REPORTS AND OPINION............................................................................................................ 16

4.1 OBJECTIVES ............................................................................................................................................ 16 4.2 CONTEXT OF AUDIT REPORTS .................................................................................................... 16

4.3 AUDIT REPORTS LEGAL PROCESSES............................................................................................ 16 4.4 PURPOSE OF AUDIT REPOERTS ..................................................................................................... 17

4.5 ACTIVITY 6: AUDIT REPORTS COMMUNICATION ................................................................ 17 4.6 PROCESS REPORTS ISSUED TO THE AUDITOR GENERAL .................................................. 17

4.7 KEY ELEMENTS OF A MANAGEMENT LETTER ......................................................................... 17

4.8 TYPES OF AUDIT OPINIONS ........................................................................................................... 17 5. COMMON AUDIT FINDINGS IN LOWER LOCAL GOVERNMENTS .......................................... 19

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK II

5.1 OBJECTIVES ............................................................................................................................................ 19

5.2 CONTEXT OF AUDIT FINDINGS................................................................................................... 19 5.2.1 Common Audit Findings and Queries ............................................................................................... 19

5.2.2 Budgeting Related Queries .................................................................................................................. 19 5.2.3 Revenue Related Queries..................................................................................................................... 19

5.2.4 Procurement Related Queries ............................................................................................................ 20 5.2.5 Expenditure/Accounting Related Queries ........................................................................................ 20

5.2.6 Asset Management Queries ................................................................................................................. 20

5.2.7 Human Resource/Payroll Management Queries ............................................................................. 20 5.3 ACTIVITY 7: IMPLICATIONS OF UNRESOLVED AUDIT QUERIES ...................................... 21

5.4 CASE STUDIES ON COMMON AUDIT FINDINGS ................................................................... 21 6. FRAUD RISK NATURE AND DETECTION............................................................................................ 23

6.1 OBJECTIVES ............................................................................................................................................ 23 6.2 CONTEXT OF FRAUD RISK ............................................................................................................. 23

6.3 COMMON METHODS OF FRAUD ................................................................................................. 23

6.3.1 Possible Causes of Fraudulent Practices ........................................................................................... 23 6.4 DETECTION AND INDICATORS OF FRAUD ............................................................................ 24

6.5 FRAUD MITIGATION MECHANISMS............................................................................................. 24 6.6 CASE STUDY DISCOVERY AND PREVENTION OF FRAUD IN SERVICE DELIVERY

UNITS IN SCHOOLS ......................................................................................................................................... 24

7. AUDIT FOLLOW-UP .................................................................................................................................... 26 7.1 OBJECTIVES ............................................................................................................................................ 26

7.2 CONTEXT OF AUDIT FOLLOW-UP ............................................................................................. 26 7.2.1 Purpose/Benefits of Audit follow-up.................................................................................................. 26

7.3 THE AUDIT FOLLOW-UP PROCESS.............................................................................................. 26 7.4 INGREDIENTS FOR SUCCESSFUL AUDIT FOLLOW-UP BY KEY STAKEHOLDERS ...... 27

7.4.1 Roles of Key Stakeholders in Audit Follow-Up .............................................................................. 27

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK III

FOREWORD The Government of Uganda has been undertaking continual reforms in PFM and the USAID-funded Strengthening Decentralization for Sustainability (SDS) Program has been supporting some elements in the reform framework initially in the 35 partner districts and currently 50 partner districts. The program has been involved in capacity building training and support in the areas of Revenue mobilization, integrated planning and budget, procurement and contract management, budget support grants for funding social services such as HIV/AIDs. SDS validation surveys and reviews by other government agencies indicate that there has been considerable improvement in Public Financial Management (PFM) functions at the respective Local Governments. The reduction in adverse external audit opinions and the increase the unqualified audit opinions supports the assertion of improvements in scrutiny and oversight of collection and utilization of public funds and resources including grants. Despite the successes and improvements that have been registered in PFM systems, there are still voices that seem to indicate that the improvements do not appear to be translating into marked improved services delivery more especially in health sector. SDS therefore has evolved a peer to peer learning strategy that is being rolled out to sub counties using the recently prepared cadre of trainers. This TA is particularly aimed at evolving strategies that will improve accountability and elimination of negative audit findings that have an indirect impact on the level of service delivery. Finally, I wish to extend our gratitude to personnel who have rendered support in production of this Handbook. We appreciate acceptance to support the delivery of the roll out training by key stakeholders; the Ministry of Finance Planning and Economic Development (MoFPED), Ministry of Local Government (MoLG), Uganda Local Government Finance Commission (ULGFC), National Planning Authority (NPA), PPDA and the Office of the Auditor General (OAG). We shall remain grateful for the invaluable time and contribution. Denis Okwar Chief of Party SDS Program

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK IV

ACRONYMS

AO Accounting Officer

CAO Chief Administration Officer

CDO Community Development Officer

CIID Criminal Intelligence and Investigation Department

DDP District Development Plan

DEC District Executive Committee

DEO District Education Officer

DHO District Health Officer

DSC District Service Commission

DTPC District Technical Planning Committee

HLG Higher Local Government

HoD Head of Department

HoF Head of Finance

HoIA Head of Internal Audit

IA Internal Auditor

IAG Internal Auditor General

IGG Inspector General of Government

IT Information Technology

LED Local Economic Development

LGFAR Local Government Financial and Accounting Regulations

LGPAC Local Government Public Accounts Committee

LGs Local Governments

LLG Lower Local Government

LPO Local Purchase Order

LST Local Service Tax

MOE Ministry of Education

MoFPED Ministry of Finance, Planning and Economic Development

MoLG Ministry of Local Government

MTR Mid Term Review

NDP National Development Plan

OAG Office of the Auditor General

OBT Output Budgeting Tool

PBF Performance Based Financing

PFM Public Financial Management

RDC Resident District Commissioner

RFA Request for Application

SDS Strengthening Decentralization Sustainability

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK V

ABOUT THIS HANDBOOK The Handbook is intended to support development of a cadre of trainers in a strategy of Peer to Peer learning to be used in all the partnering districts in Uganda, with a special emphasis on lower local governments. More focus will be laid on recent reforms in the PFM framework. There has been two significant reforms within the PFM framework; (1) PFM Reform Strategy -2011/12-2016/17 and (2) introduction of the PFM Act 2015. The overall expected outcome of this peer to peer learning will help in skills transfer and in turn a spinoff in increased value for money in service delivery. The manual will focus on key areas and components within the PFM that have been of public concern due to the direct impact on level of service delivery. These will be discussed under the following topics:

Overview and Context of PFM

Financial Reporting Framework

Audit Processes- Internal And External Audits

Audit Reports

Fraud Risk

Common Audit Findings The main training methodology will be the experiential learning style which will include short explanatory and consensus building lectures, discussions and presentations.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 1

1. PUBLIC FINANCIAL MANAGEMENT OVERVIEW 1.1. OBJECTIVES The overall objectives of the training are to give the participants a broad perspective of the financial management in LLGS. By the end of the session, the participants should be able to:

Explain the meaning of Public Financial Management (PFM)

Explain the Public Finance Management Cycle

Explain the importance of financial management in a LLG

Discuss some of the practical limitations to financial management in LLGs 1.2. WHAT IS PUBLIC FINANCIAL MANAGEMENT (PFM)? Financial Management comprises of processes and actions taken by political and administrative leaders of a LLG to acquire funds, allocate them over different activities and time periods and use them in the most economic, efficient and effective manner with a view to achieving the goals and objectives of the LLG 1.3. CONTEXT OF PFM

PFM is an essential part of governance and in the context of LLGs, PFM is concerned with processes within:

Policy formulation, (

Resource mobilization and allocation,

Resource utilization and recording (Expenditure management),

Monitoring and supervision,

Scrutiny and oversight activities. Without good PFM practices there is an increased risk of fiscal imbalances, weak accountability, political capture and deterioration in the quality of public services and may undermine the gains so far made under decentralization policy initiative. The key expected outcome is utilization of resources efficiently and delivering value for money to respective residents. The link between quality of services and resources makes the status of PFM critical success factor in sustainable development. 1.4. RELEVANCE OF GOOD FINANCIAL MANAGEMENT LLG must ensure that there good financial management for the following reasons:

To ensure that the local authority has enough revenue to carry out its main responsibilities to the community to an acceptable level

To ensure that the financial resources available are used in accordance with the political priorities of the local authority

To ensure that financial resources are used legally and honestly

To ensure that the local authority has enough money, at all times, to pay for its obligations or debts and that it is not highly indebted

To ensure that those who run the LG are provided with adequate information for discharging their responsibilities and the public is provided with information about the usage of funds.

1.5. STATUS OF PFM AND CHALLENGES

Recent reviews and audits on local government PFM mechanisms revealed significant weaknesses in overall processes. These weaknesses range from lack of control systems for safe guarding against abuse, misuse, fraud, and irregularities to inefficient cash management, collusion practices in procurement, contract management, unrealistic budgeting, poor

Commented [SN1]: Is it Public Finance Mgt or Public Financial Mgt?

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 2

accountability and weak compliance with internal controls. Some specific challenges that appeared repetitive basing on reports of the OAG and PPDA procurement reviews at LGs, included:

Limited compliance with laws and regulations particularly PPDA and accountability

Limited or absence of participatory planning and budgeting undermining program ownership

Generally low implementation supervision and monitoring both the quality and quantity of outputs in service delivery.

Low local revenue mobilization leading to inadequate funds to finance the Budget

Unpredictable and late release of funds by HLGs

Continual audit queries in procurement management

Inadequate feedback loop with service beneficiaries

Limited and delayed follow up of audit and inspection findings which undermines accountability

Poor record keeping- low timely and quality financial reporting and accountability;

Instances of wasteful use of resources (including sadly irregularities like embezzlement) are still common

1.5.1. Achievement of PFM Reforms Following a series of consistent interventions by both the ministry of Finance, Planning and Economic Development (MoFPED) and Ministry of Local Government (MoLG), there has been some significant positive achievements in PFM framework. Specific achievements relating to local governments are depicted in the following areas:

Leadership and good governance: Good governance has a direct impact in determining the quality of service delivery. The introduction of the PFM Act 2015 has strengthened the powers of the PS/ST to demand that action is taken on audit queries.

Policy Framework and Planning: The LLG development plan is linked to the District Development Plan and harmonized with the National Development Plan.

Revenue mobilization and Administration: Systematic management of local revenue processes is key in addressing discretional local government priorities. Generally the revenue volumes at local government

have increased although there are still challenges in revenue assessments and maintaining updated and accurate registers. There has also been less reported political disruptive action over the last two years.

Resource allocation and Prioritization: The recent reviews by the Ministry of Finance and Economic Development on the district development plans and budgeting process generally show that production of budgets are aligned to district development plans and government policies with increased level of participation in development planning and budgeting.

Predictability and Control in Budget Execution: Budget control systems are an assurance that financial resources are used legally and honestly. Recent review under the PFM reform strategy indicates that the utilization

and control of public funds, although not yet perfect, has been largely successful though some challenges of accumulation of domestic arrears and frequent supplementary still remain. Releases are regular and are not less than 99% of the amounts planned. In 2015/16 grants were merged and reduced to 13 and will be a maximum of 3 transfers in 2016/17 budget year, implying minimal control on resource allocation by the centre. The reporting framework has improved significantly except for bottlenecks in some local governments using IFMIS/OBT. IFMIS now extended to over 75 Lgs.

Cash flow Management: Management must ensure that the LLG has sufficient money to pay for its obligations or debts. Payrolls have now been decentralized and funds send directly to a special salary account for the districts.

This has also had a resultant effect of easing the collection of LGST from employees within respective districts. Introduction of an “Online Transfers Information Management System” [OTMIS] enables computation of IPFs automatically so districts are able to know what is expected in a timely manner. Funds for schools are remitted during school holidays, funds for agriculture now follow the season and development funds are now “front loaded” with 100% being disbursed by the start of the third quarter of the financial year. In effect the Straight Through Processing System [STPS] has been extended to all frontline service providers and the district.

Comprehensiveness and Transparency: Timely and appropriate accountability requires record keeping, documentation, rules and compliance. Whereas the OBT is not yet fully web based, the MoFPED published quarterly

reports on the website for public access. A public call centre has been established for citizens to call in and make any enquiries about

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 3

expenditures on any program at national and local government level, toll free-0800229229, responds to all languages in Uganda. For more transparency and focus on outputs, a Program Based Budget System [PBBS] will commence in March 2016 and be effective for the next financial budget year.

Oversight, Internal Audit and scrutiny Function: in a bid to eliminate negative audit findings, CAOs and Senior Assistant Secretaries (SAS)/ Town Clerks should increase vigilance in preparation of action papers for council to discuss recommendations of LGPAC. In the last audit there was only one local government1 with a disclaimer

of opinion and 27 qualifications, which is a tremendous improvement. Commissioner for internal audit established under the MoFPED and this position will be upgraded to Internal Auditor General [IAG] for continuous follow up and correction. The IAG works closely with the OAG, the IGG and Police to ensure that action is actually taken as desired. It is hoped that this will increase liaison with district PACs and the CAO. Audit and scrutiny by Parliament continues to improve although some challenges manifest in a number of Lgs.

Information management: LGs with some IT and data management systems have not put sufficient measures to control these systems. The OAG has had several negative comments in respect to IT management such as data security and integrity. More LGs are now using IFMIS and even in the absence of web based reporting it is possible to

use other hybrid systems to ensure accurate and computerised reporting. The manual systems have been significantly reduced. 1.6. ENABLING LEGAL FRAMEWORK

Improvements have r been possible and supported by relevant legal framework:

The Constitution especially Article 164(2)

Public Financial and Accountability Act 2003

PFM Act 2015 especially section 11(90

Local Governments Act

Public Procurement and Disposal of Assets (PPDA) Act

Budget Act 2001

The Audit Act

The local government Financial and Accounting Manual [LGFAM]

1.7. CONTENT OF ACCOUNTABILITY? Accountability is a stewardship role that requires officers and leaders to explain how the resources were used and to show justification for such usage. The peoples' mandate is assumed to be given by the vote and approval of a manifesto.

The PFM Act under section 2 is more specific on this purpose. The focus on accountability is further made under PFM Act section 11(g) and s 12(2). An accounting officer who fails to account for a financial year will be suspended until necessary steps to do so have been undertaken. Accountability is a responsibility of the accounting officer personally! Specific mandate is deemed to be given by a participatory process during formulation of the District Development Plan which spells out the objectives and goals. Accountability therefore must reflect at all times a relationship between spending and the DDP. The process of DDP implementation is through budget preparation, approval, implementation and reporting. The PFM Reform strategy alludes to this requirement as a means of ensuring transparency. The establishment of Internal Auditor General is based on the expectation of quarterly reporting which will be consolidated annually. Lgs are expected to inform residents on spending and performance on the budget using any suitable media. Overall financial accountability is done through preparation and council approval of monthly, Quarterly and annual performance reports. All statements must be validated by production of documentary evidence of money received and money spent. The key challenge has been failure to ensure evidenced accountability although is not adequate, any paper evidence must be supported by monitoring reports and physical assets and other forms of outputs and outcomes.

1 Nakapipirit Town Council

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 4

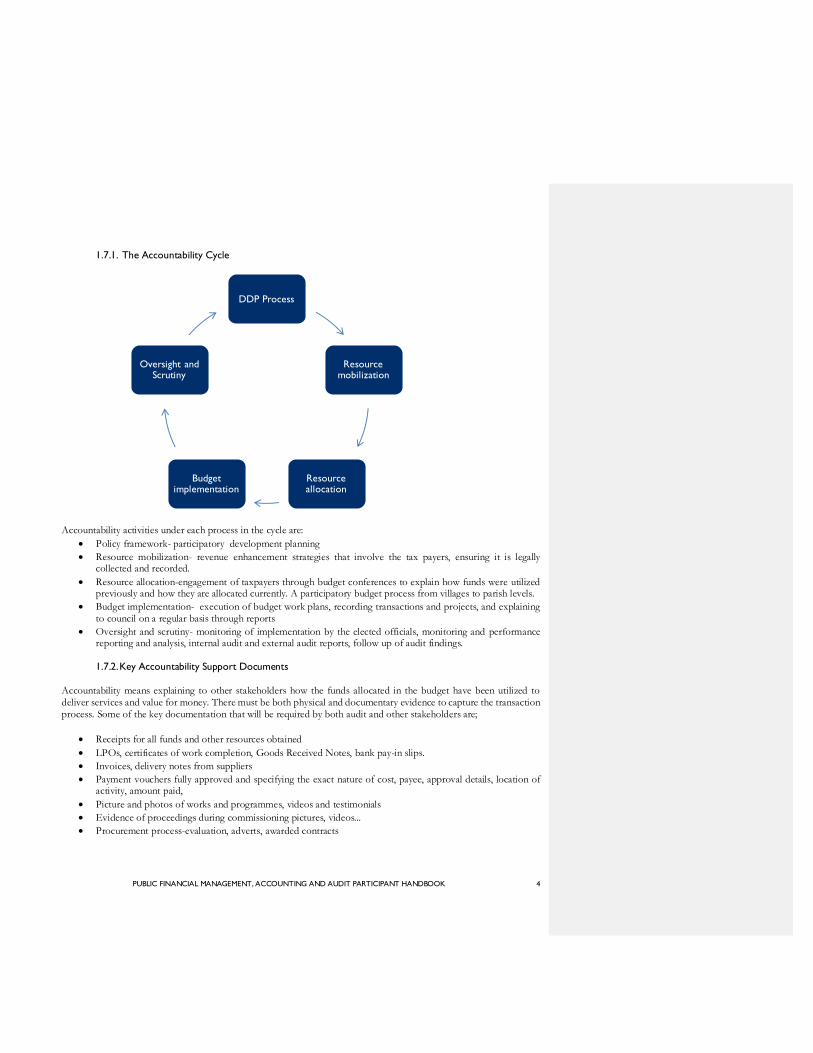

1.7.1. The Accountability Cycle

Accountability activities under each process in the cycle are:

Policy framework- participatory development planning

Resource mobilization- revenue enhancement strategies that involve the tax payers, ensuring it is legally collected and recorded.

Resource allocation-engagement of taxpayers through budget conferences to explain how funds were utilized previously and how they are allocated currently. A participatory budget process from villages to parish levels.

Budget implementation- execution of budget work plans, recording transactions and projects, and explaining to council on a regular basis through reports

Oversight and scrutiny- monitoring of implementation by the elected officials, monitoring and performance reporting and analysis, internal audit and external audit reports, follow up of audit findings.

1.7.2. Key Accountability Support Documents

Accountability means explaining to other stakeholders how the funds allocated in the budget have been utilized to deliver services and value for money. There must be both physical and documentary evidence to capture the transaction process. Some of the key documentation that will be required by both audit and other stakeholders are;

Receipts for all funds and other resources obtained

LPOs, certificates of work completion, Goods Received Notes, bank pay-in slips.

Invoices, delivery notes from suppliers

Payment vouchers fully approved and specifying the exact nature of cost, payee, approval details, location of activity, amount paid,

Picture and photos of works and programmes, videos and testimonials

Evidence of proceedings during commissioning pictures, videos...

Procurement process-evaluation, adverts, awarded contracts

DDP Process

Resource mobilization

Resource allocation

Budget implementation

Oversight and Scrutiny

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 5

1.8. ACTIVITY 1: PAYMENTS ACCOUNTABILITY

I. What information should be shown on a payment voucher? II. Discuss the purpose of each detail on the voucher

III. What documents should be attached on a voucher for payment of construction of a bore hole?

IV. Discuss the purpose of each document that is attached or referenced.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 6

2. ACCOUNTING-FINANCIAL REPORTING 2.1 OBJECTIVES By the end of the training, participants will be able to:

Explain meaning and purpose of accounting process

Recognize the various financial records and books of accounts of a LLG 2.2 WHAT IS ACCOUNTING Local Governments Accounting may be defined as the process of providing reports on how the resources of the lower local government have been utilized over a specified period of time. It is one of the most important functions in the proper management of local governments. These reports must be prepared and submitted to relevant authorities by the chief officers or Heads of Departments who are required to fulfill their accountability obligations.

2.2.1 Purpose of Accounting

Besides providing information about operations, there other purposes that may be served by accounting information:

Compliance with Legal Requirements: PFM Act S12(2) , Section 86 of the LGs Act CAP 243, Section 31 of the Public Finance and Accountability Act, 2003, and Regulation 68 of Local Government Financial and Accounting Regulations (LGFARs), 2007, require all local government councils and administrative units to produce financial statements.

Budget Performance and Control: periodic reporting on budget performance helps management to take appropriate and timely decisions and control. Comparing outputs with standards and indicators.

Gauge effectiveness and efficiency- Accounting Officers are expected to formulate appropriate service delivery indicators to be used to gauge the impact of the PFM Strategy initiatives on service delivery. Reference

may be made to the NDP and DDP Service Delivery indicators and targets, for example number of children passing in grade one at PLE. Financial reporting helps LGs to determine different levels of performance.

Monitor Utilization of Funds and service delivery: how much revenue was raised, how it was utilized and whether there was equity in allocation of these resources. Financial reports aim at determining whether funds have been utilized as planned in the service delivery chain, PFM Act s12(2)..

Feedback to Stakeholders: whether there is a surplus, to show the financial strength of the local government in terms of assets owned (e.g. cash) and liabilities due, reflection on the quality of service delivery being reported on, help to demonstrate that policy is being carried out effectively and efficiently.

Timely Action: In case of diversion of funds, overspending on budget lines, unaccounted expenditure and so on, management will always take timely action, if there has been timely reporting.

Preparation for auditing and verification purposes by keeping track of past transactions

2.2.2 Legal Requirements for Financial Reporting

The reporting requirements are mandatory and are intended to enforce accountability of the local government to the relevant stakeholders and are generally guided the following legal framework:

The PFM Act which came into force March 2015

Section 86 of the LGs Act CAP 243,

The National Audit Act sections 16-25

Regulation 68 of Local Government Financial and Accounting Regulations (LGFARs), 2007, require all local government councils and administrative units to produce financial statements.

Local Governments are required to produce monthly, quarterly and annual financial statements. Reports show both the resources spent and activities implemented in that period.

2.3 FINANCIAL REPORTING PROCESS

The management of public funds activities is vested in the accounting officer, which means that the taxpayers and other stakeholders are not actively engaged in operations and execution of budgets. In line with the stewardship concept, the operational mangers must explain how the resources were utilized in achievement of the objectives of stakeholders as agreed in the planning and budget process. The objective of record keeping in a local government is to provide financial

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 7

accountability for the actions of the different managers and staff. Financial accounting systems must ultimately end with relevant and reliable information in form of financial reports. Financial reports should have good attributes such as; accurate, complete, understandable, reliable, timely, comprehensive, and standardized for purposes of comparability and for ease of interpretation and analysis. Generically financial reports are concerned with Revenue records such as Revenue registers, receipt books, tax ticket registers and assessment forms (files), revenue collection cashbooks and Expenditure records such as Payment vouchers, payroll, vote books, abstracts, ledgers, etc. Recording of Local Revenues and other Receipts All funds received at local governments should be properly receipted using the official receipts and posted in the relevant Cashbooks. Receipts are to be prepared in triplicate and completed in indelible ink. The original copy goes to the payee; duplicates are used to support accounting entries, and the triplicate remains in the book. Wherever possible, the use of carbonized receipts is recommended. Erasures are not allowed; instead the receipt is cancelled if there is an error and a new one made. Each sub-county should maintain a collection register to enter daily, the number and amount of each receipt or license issued. Where a sub-county is using a computerized accounting system daily posting is easy. Knowing daily cash balances is extremely helpful. Books of Accounts The purpose of accounting books is to create a permanent record of the financial transactions of the local government. Data will be extracted from the source documents and “posted” to the books of accounts. This will also allow for the proper classification and summarization of such data by using relevant “accounts” for each item according to the chart of accounts, reference to the LGFAM and the LGFARs. Cashbooks The local council has to maintain a separate cashbook for each of its bank accounts. The purpose of a cashbook is to maintain a record of cash coming in and going out and the balances at any particular date. All cashbooks maintained by a local government must be reconciled with bank statements monthly. Abstracts The purpose of abstracts is to classify and collect expenditures and revenues. The abstract will have columns for expenditure items (e.g. stationery, wages, fuel,) and revenue (e.g. grants, LST). The total for each column in the abstract is posted to the ledger regularly. These are maintained for both revenue and expenditure. Ledgers These are the main books of accounts. An account will be opened in the ledger for each item of revenue and expenditure. The main ledger used is the general ledger, however subsidiary ledgers may be maintained for particular items e.g. debtors (so that individual debtor accounts are kept in the debtors ledger). In computerized systems, verified entries are “booked” in the general ledger. Assets Register These are maintained to record the non-current assets of a Local Government. Each asset has its page in the assets register to record date of purchase, price, location, use, source of funds, assume cash accounting value and disposals. Stock Book This is used to record stores i.e. stores in and out and balance at hand. Each store item will have its page in the stock book. Vote Book This is used for budgetary control and commitments. Record all amounts budgeted for each item or revenue and expenditure and post payments and commitments so as to avoid overspending.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 8

Payment Vouchers All payments made by local governments must be recorded and effected by way of approved payment voucher. They must be supported by relevant documents including LPOs, delivery notes, invoices, contracts, and duly approved by the Sub-county Chief, (SAS). The commitment must be recorded in the vote book to guide the SAS before approval and then reconciled before payment is affected. Checks or Electronic Funds Transfers (EFTs) are prepared on the strength of payment vouchers. All payment vouchers must be stamped “PAID” after the payments are made. Registers have to be maintained for recording the details and amounts in the vouchers, and of checks/EFTs issued 2.4 MONTHLY FINANCIAL REPORTS

The Head of Finance (HLG and LLG) is responsible for producing the following financial statements at the end of each month and forward them to the Executive Committee (District/Municipal/Town Council and Sub-county Executive Committee) through the Chief Executive (CAO, Town Clerk and SAS) not later than 15th of the following month:

A Trial Balance – a statement showing in separate columns the totals of debits and credit entries in the General Ledger. Note: This is a technical statement/report, therefore prepared by finance staff.

A consolidated statement of income and expenditure for all recurrent and development revenues and expenditures of the council. The statement should include year to date performance in comparison to the budget. It is also a measure of budget performance during the month.

A Statement of Financial Position (Balance Sheet) at the end of the month. This provides information about the assets, liabilities and ownership of the local government.

Heads of Department are required to produce the following financial statements at the end of each month and forward them to the Head of Finance not later than 7th of the following month:

Financial statements for all recurrent and development revenues and expenditures of their departments.

Bank reconciliation statements and supporting copies of bank statements for their departments.

Descriptive monthly progress reports and key departmental output performance reports.

2.4.1 Quarterly Financial Statements

The Head of Finance is responsible for producing the following financial statements at the end of each Quarter and forward them to the Executive Committee (District and LLG Executive Committees) through the Chief Executive not later than 15th of the month following end of the Quarter:

A Year to Date Trial Balance – a statement showing in separate columns the totals of debits and credit entries in the General Ledger. Note: This is a technical statement/report, therefore prepared by finance staff.

A consolidated statement of income and expenditure for all recurrent and development revenues and expenditures of the council for the year to date. The statement should include the current Quarter’s performance in comparison to the Budget. It is also a measure of budget performance during the quarter.

A Statement of Financial Position (Balance Sheet) at the end of the Quarter. This is also a technical statement/report, therefore prepared by finance staff.

Heads of Department are required to produce the following financial statements at the end of each Quarter and forward them to the Head of Finance not later than 7th of the month following the Quarter:

Financial statements for all recurrent and development revenues and expenditures of their departments.

Bank reconciliation statements and supporting copies of bank statements for their departments.

Descriptive Quarterly progress reports and key departmental output performance reports. Output Budgeting Tool (OBT) helps to generate most of these reports. This report should indicate in details, activities implemented during the quarter against their budgets and targets.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 9

2.4.2 Annual Financial Statements/Reports

Section 86 of the LG Act CAP 243 requires the Chief Administrative Officer to produce financial statements of the Council within three months after the end of each accounting period, for submission to the Auditor General and must include the following:

I. Trial Balance II. Income and Expenditure Statement

III. Statement of Financial Position (Balance Sheet) IV. Statement of Cash Flow

The financial statements must be accompanied by the following notes and schedules:

Accounting Policies followed in the preparation of financial statements

Details of Income

Details of Expenditure

Bank Reconciliation Statements

Certificates of balances of all Council accounts from the banks

Schedules of interest and advances

Schedules of debtors and creditors

Schedules of fixed assets

Updated staff list

Board of Survey Report 2.5 ACTIVITY 2: FINANCIAL REPORTING

2.6 KEY STAKEHOLDERS AND THEIR ROLES IN FINANCIAL REPORTING

The LGFARs 2007 places a number of financial reporting roles under each key player in the local government. These range from the Accounting Officer/Chief Executive to Heads of Department and other public officers.

Chief Executive (CAO, TC, SAS) – Regulation 9 (h) of LGFARs 2007, requires preparation and submission to the Auditor General, the statement of final accounts of council for audit within three months after the end of each financial year. Section 31 (1) (b) of the Public Finance and Accountability Act, 2003 also provides similar requirement.

Head of Finance – Regulation 11 (k, r and u), requires co-ordination of preparation of the annual accounts of council for audit and prepare financial statements and returns as required by LG Act CAP 243, and LGFARs 2007.

Heads of Department – Regulation 13 (e) of LGFARs 2007, requires all Heads of Department to submit to the Head of Finance financial and progress reports within seven days after the end of each month.

District Hospitals – Regulation 61 (3), requires Medical Superintendents to prepare hospital financial statements in accordance with LGFARs 2007 and submit the same to the Chief Administrative Officer on a monthly basis. The same regulation requires for each financial year, preparation and presentation of income and expenditure to the council as part of final accountability for the year.

Health Centres – Regulation 62(4) of LGFARs 2007, requires In-charge Health Centres to prepare and submit to SAS financial statements in accordance with LGFARs 2007 on a monthly basis, and also income and expenditure statements as part of final accountability for the year.

Secondary Schools – Regulation 63 (2) of LGFARs 2007, requires Secondary School Head teachers to account to council at the end of each academic term and income and expenditure statements to be presented to the council at the end of each calendar year.

References are made to the formats in the LGFAM. One member of group will illustrate and explain

how the format is arranged and describe the processes leading to the completion of these accounts including who is responsible for each stage

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 10

Primary Schools – Regulation 64(6) of LGFARs 2007 requires Head teachers to account to Sub-county council (through SAS) at the end of each academic term, and also income and expenditure statements at the end of each calendar year.

Other Public Officers – Regulation 14 (f), requires prompt preparation and submission of financial returns and statements as required by any law, financial regulation, or instructions from the Head of Finance or any other authority.

Executive Committee (District, Municipal, Town Council and Sub-county) – Regulation 7(k) of LGFARs 2007, requires the Executive Committee to review periodic performance reports and recommend actions where necessary.

2.7 TRANSPARENCY OF FINANCIAL INFORMATION This part deals with the publication of local government financial information for the citizens, NGOs and CSOs and others users. Publication improves transparency and accountability at the local level and leads to good financial management. 2.8 ACTIVITY 3: PUBLICATION OF FINANCIAL REPORTS AND OTHER OPERATIONAL

INFORMATION

2.9 WHAT TO PUBLISH

Plans and Budgets

Government grants e.g. Local Government Management and Service Delivery (LGMSD ) grants, conditional and unconditional grants

Monthly, quarterly and annual accounts

Contracts Committee minutes

Donor grants

Financial decisions of the Council and or its committees

Agendas of Council and its committee

The standards of performance achieved by the different sectors of the local government (e.g. unit cost statistics like students – teacher ratios, immunization coverage, etc.)

Reports of the LG Public Accounts Committee

Lists of approved suppliers and contractors.

2.9.1 How to Publish

Notice Boards – located within and outside. The major disadvantage here is that few citizens are able to read such notices.

Local Press – this involves putting the necessary information in the local newspapers. To reduce on the cost of this, only significant data should be selected and highlighted.

Local Radio Programmes – these could be done monthly (to reduce on cost). All important financial reports for the local government during the past one month could then be aired on the radio.

Written documents should be distributed to NGOs, CBOs, LCs, opinion leaders and the like. However as this is a costly exercise, statements need to be summarized so that only important information is published.

I. What causes delays in the preparation of financial reports?

II. What is the plan to overcome the challenge?

III. Should financial information be published? Which information should be published?

IV. What should be the method of publication?

V. Are there any benefits derived from publication of such information?

VI. Any risks from publication of operational information?

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 11

Regular Meetings with communities and end users (e.g. with school management committees, Health Management Committee, project management committees etc) to inform them of financial matters and activity progress.

2.10 BENEFITS OF PUBLISHING FINANCIAL STATEMENTS

Often information is with held under the guise of confidentiality, a case that is now guide by the information and communications Act. Some of the following maybe benefits accruing from open publication of financial and other operating information:

Increased socialization of plans and budgets relating to citizens compact with a local government

Promotes citizens’ level of involvement in planning/budgeting.

Increased awareness on the utilization of taxpayers’ money

Promotes Transparency in dealings with public resources

May enhance revenue collection (taxpayers will understand that the money they pay is appropriately utilized).

Gives opportunity to taxpayers and other stakeholders to evaluate information about local government funded activities.

Makes it easier for the public, NGOs, CSOs and other interested parties to make comparisons of, and judgments upon the performance of their local governments.

Supports councillors to make more informed and rational decisions when dealing with their electorate and to judge their performance.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 12

3. THE AUDIT PROCESS – OVERVIEW 3.1 OBJECTIVES The expected output is that by the end of this training the participants should be able to:

Explain why auditing is necessary for a LLG

Understand the various types of audits

Explain the purposes for conducting audits

Identify the various types of audits

Identify the various types of auditors 3.2 CONTEXT OF AUDIT

An audit is an independent review or examination of the operations and financial records of a local government to determine the level of truth and fairness of the operations and records. Therefore, auditing is the process of determining whether the statements produced by the management of an organization and the information contained in them fairly represent the underlying facts on which such information has been based. The PFM Act section 50 and 51 now requires half yearly and annual audits as a means to squeeze accountability. This process is also in line with the PFM reform strategy of enhancing accountability..

3.2.1 Purpose of Audits

To give an assurance to all stakeholders that the goals and objectives of the LLG are being achieved

To confirm that systems for the delivery of services are working as intended.

To ensure Value for Money in the operations of LGs

To enhance the credibility of the assertions made by management., that for example all reported activities actually occurred and the reported assets actually exist

To Improve public confidence in the accounts and management

Check on authenticity and reliability of the accounts, that no fraud exists and that the stewardship function has been well executed

To check compliance with legal requirements

To ensure that there has been compliance with the requirement of the legal framework for public sector audits in Uganda.

Determine the adequacy of internal control systems in place

Ascertain whether the local government receives value for money in its activities 3.3 LEGAL FRAMEWORK FOR PUBLIC SECTOR AUDITS IN UGANDA The Constitution Article 163(3) and Section 13, 16, 19 of the National Audit Act provides a mandate for the OAG. At the same time The Constitution under Article 164(2) and Article 196 spells out the importance of accountability of public funds. These articles are enabled by the Local government Act sections 86 which provides that the Auditor General may carry out surprise audits, investigations or any other audit considered necessary. The National Audit Act 7 more specifically under section 16 provides for a requirement and powers of the OAG to conduct audits for all local governments “the accounts of every local government council and every administrative unit shall be audited annually by the Auditor General or by an auditor appointed by the Auditor General. Other related legal framework.. Other regulatory framework for local government audit may be found under:

The Constitution of the Republic of Uganda, Article 164 &196 [the implication of this Article should be fully understood]

Local Governments Act Cap 243 section 86-90

The National Audit Act 2008 enables Article 163 of the Constitution of Uganda.

LGFARs 2007 gives an overview of financial management and accounting functions in the local governments.

LGIAM 2007, provided guidance for internal audit function in local governments.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 13

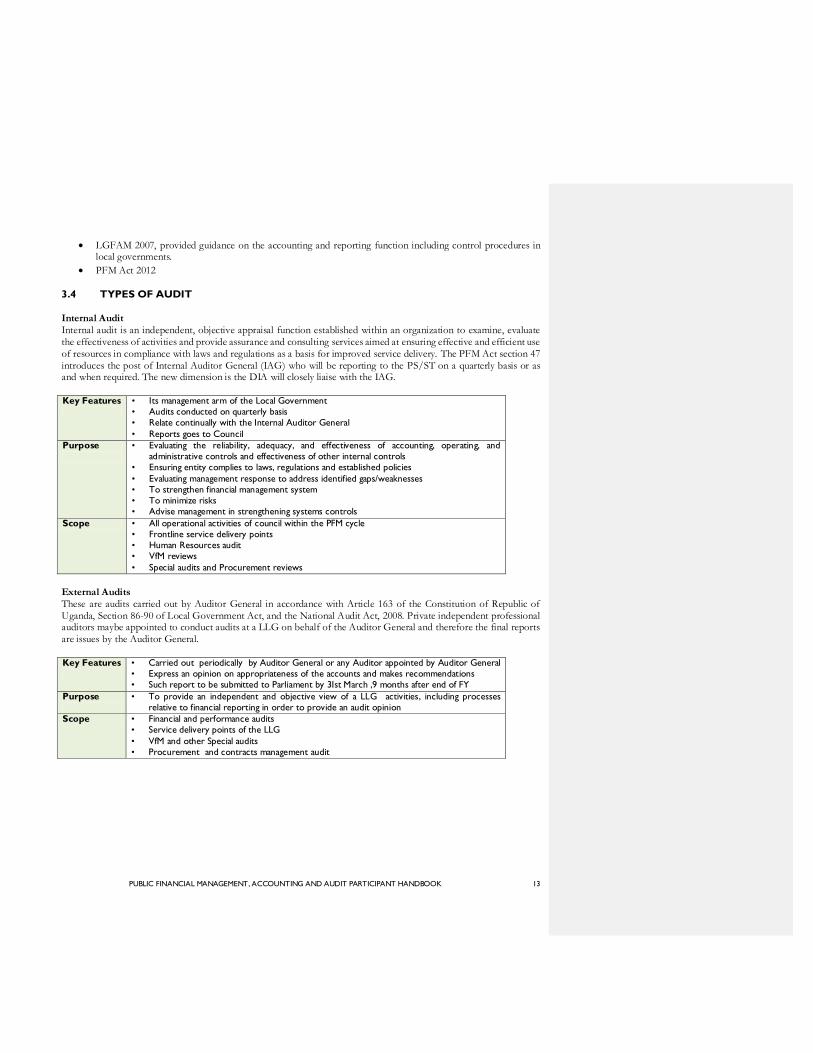

LGFAM 2007, provided guidance on the accounting and reporting function including control procedures in local governments.

PFM Act 2012

3.4 TYPES OF AUDIT

Internal Audit Internal audit is an independent, objective appraisal function established within an organization to examine, evaluate the effectiveness of activities and provide assurance and consulting services aimed at ensuring effective and efficient use of resources in compliance with laws and regulations as a basis for improved service delivery. The PFM Act section 47 introduces the post of Internal Auditor General (IAG) who will be reporting to the PS/ST on a quarterly basis or as and when required. The new dimension is the DIA will closely liaise with the IAG.

Key Features

• Its management arm of the Local Government • Audits conducted on quarterly basis • Relate continually with the Internal Auditor General

• Reports goes to Council

Purpose

• Evaluating the reliability, adequacy, and effectiveness of accounting, operating, and administrative controls and effectiveness of other internal controls

• Ensuring entity complies to laws, regulations and established policies

• Evaluating management response to address identified gaps/weaknesses • To strengthen financial management system • To minimize risks • Advise management in strengthening systems controls

Scope • All operational activities of council within the PFM cycle • Frontline service delivery points • Human Resources audit • VfM reviews

• Special audits and Procurement reviews

External Audits These are audits carried out by Auditor General in accordance with Article 163 of the Constitution of Republic of Uganda, Section 86-90 of Local Government Act, and the National Audit Act, 2008. Private independent professional auditors maybe appointed to conduct audits at a LLG on behalf of the Auditor General and therefore the final reports are issues by the Auditor General. Key Features

• Carried out periodically by Auditor General or any Auditor appointed by Auditor General • Express an opinion on appropriateness of the accounts and makes recommendations • Such report to be submitted to Parliament by 3Ist March ,9 months after end of FY

Purpose

• To provide an independent and objective view of a LLG activities, including processes relative to financial reporting in order to provide an audit opinion

Scope • Financial and performance audits • Service delivery points of the LLG

• VfM and other Special audits • Procurement and contracts management audit

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 14

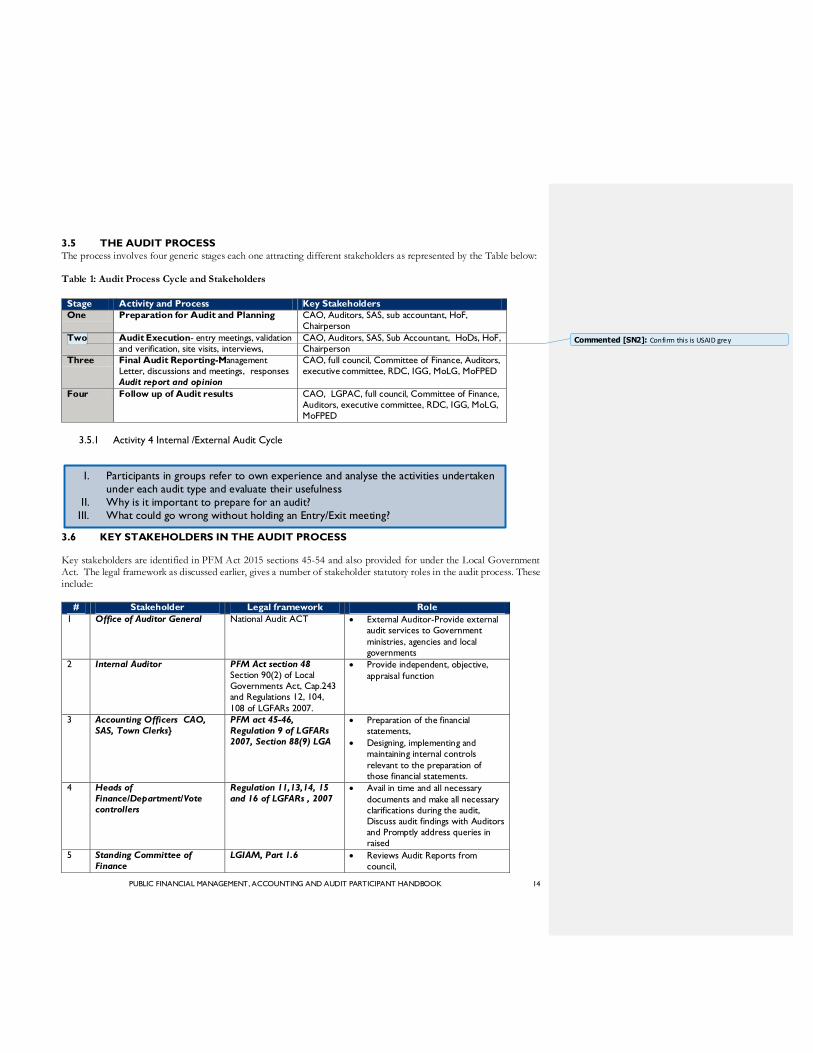

3.5 THE AUDIT PROCESS

The process involves four generic stages each one attracting different stakeholders as represented by the Table below: Table 1: Audit Process Cycle and Stakeholders

Stage Activity and Process Key Stakeholders

One Preparation for Audit and Planning CAO, Auditors, SAS, sub accountant, HoF, Chairperson

Two Audit Execution- entry meetings, validation and verification, site visits, interviews,

CAO, Auditors, SAS, Sub Accountant, HoDs, HoF, Chairperson

Three Final Audit Reporting-Management Letter, discussions and meetings, responses Audit report and opinion

CAO, full council, Committee of Finance, Auditors, executive committee, RDC, IGG, MoLG, MoFPED

Four Follow up of Audit results

CAO, LGPAC, full council, Committee of Finance, Auditors, executive committee, RDC, IGG, MoLG, MoFPED

3.5.1 Activity 4 Internal /External Audit Cycle

3.6 KEY STAKEHOLDERS IN THE AUDIT PROCESS

Key stakeholders are identified in PFM Act 2015 sections 45-54 and also provided for under the Local Government Act. The legal framework as discussed earlier, gives a number of stakeholder statutory roles in the audit process. These include:

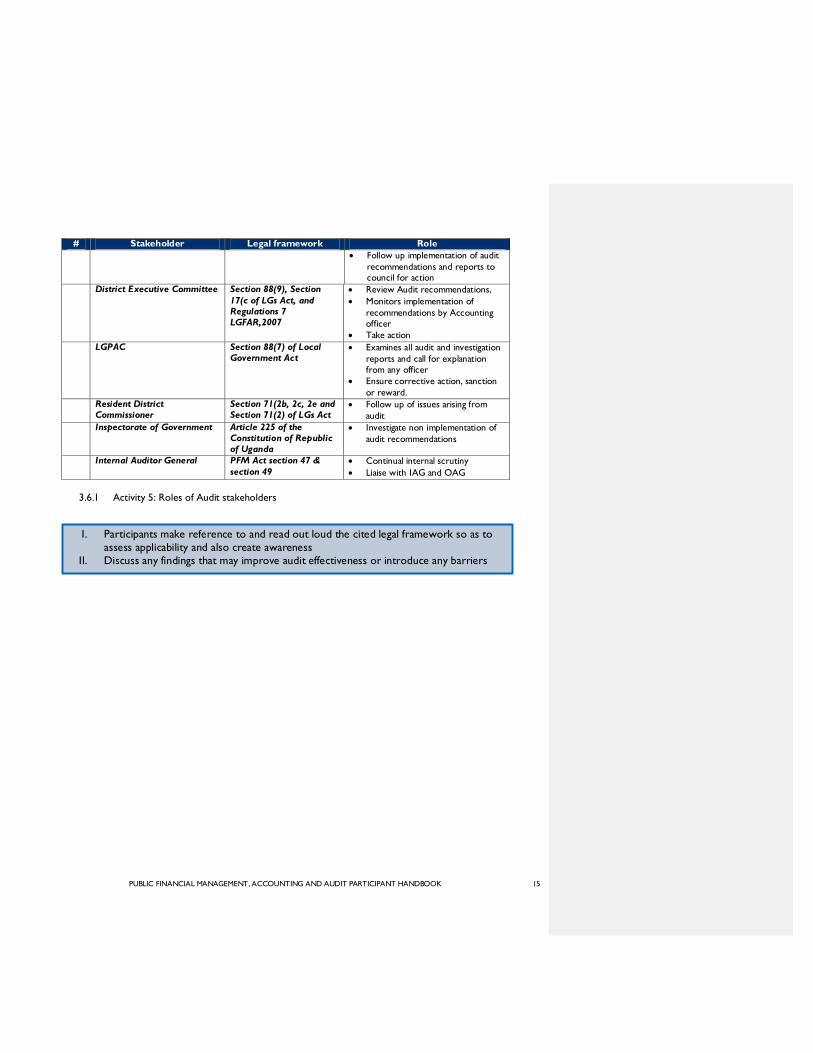

# Stakeholder Legal framework Role

1 Office of Auditor General National Audit ACT External Auditor-Provide external audit services to Government

ministries, agencies and local governments

2 Internal Auditor PFM Act section 48 Section 90(2) of Local Governments Act, Cap.243 and Regulations 12, 104,

108 of LGFARs 2007.

Provide independent, objective,

appraisal function

3 Accounting Officers CAO, SAS, Town Clerks}

PFM act 45-46, Regulation 9 of LGFARs 2007, Section 88(9) LGA

Preparation of the financial statements,

Designing, implementing and maintaining internal controls

relevant to the preparation of those financial statements.

4 Heads of Finance/Department/Vote controllers

Regulation 11,13,14, 15 and 16 of LGFARs , 2007

Avail in time and all necessary

documents and make all necessary clarifications during the audit, Discuss audit findings with Auditors and Promptly address queries in raised

5 Standing Committee of Finance

LGIAM, Part 1.6 Reviews Audit Reports from council,

I. Participants in groups refer to own experience and analyse the activities undertaken

under each audit type and evaluate their usefulness

II. Why is it important to prepare for an audit?

III. What could go wrong without holding an Entry/Exit meeting?

Commented [SN2]: Confirm this is USAID grey

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 15

# Stakeholder Legal framework Role

Follow up implementation of audit

recommendations and reports to council for action

District Executive Committee Section 88(9), Section

17(c of LGs Act, and Regulations 7 LGFAR,2007

Review Audit recommendations,

Monitors implementation of

recommendations by Accounting officer

Take action

LGPAC Section 88(7) of Local Government Act

Examines all audit and investigation

reports and call for explanation from any officer

Ensure corrective action, sanction

or reward.

Resident District Commissioner

Section 71(2b, 2c, 2e and Section 71(2) of LGs Act

Follow up of issues arising from

audit

Inspectorate of Government Article 225 of the Constitution of Republic of Uganda

Investigate non implementation of

audit recommendations

Internal Auditor General PFM Act section 47 &

section 49 Continual internal scrutiny

Liaise with IAG and OAG

3.6.1 Activity 5: Roles of Audit stakeholders

I. Participants make reference to and read out loud the cited legal framework so as to

assess applicability and also create awareness

II. Discuss any findings that may improve audit effectiveness or introduce any barriers

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 16

4. AUDIT REPORTS AND OPINION 4.1 OBJECTIVES

By the end of the session the participants should be able to:

Explain the various audit reports

Cite the relevant legal framework

Explain the meaning and impact of different audit opinions

Request for audit reports

Explain the meaning of management letter and its relevance 4.2 CONTEXT OF AUDIT REPORTS

There are two types of reports, the Internal and external Audit reports. Section 90 of Local Government Act Cap 243 requires an Internal Auditor to produce Internal Audit Reports. The PFM Act 2015 section 47 provided for an Internal Auditor General who may liaise with the LG internal Auditor on a continual basis and sharing of reports on a quarterly basis. An audit report is a signed, written document, which presents the purpose, scope and results of the Audit. Results of the audit may include; findings, recommendations and conclusions (opinions). Note: This report is the primary means to communicate with key stakeholders namely:

The Parliament (External audits)

Ministries, Agencies and Local Governments (MALGs)

Local Government Chairperson

Chief Administrative Officer/ Town Clerk /Sub-County Chiefs

Local Government Public Accounts Committee

Development partners

4.3 AUDIT REPORTS LEGAL PROCESSES

In respect to external audits, Section 16 (2) of the National Audit Act, states that “The AG shall report to Parliament on the accounts audited. The key purpose of the OAG report is to provide an independent and objective audit opinion on LG activities, including processes relative to financial reporting, Rules based compliance, reporting disclosure requirements and value for money. The final report is circularized widely and it is also on the Website of the OAG.

Recipients of the report include:

The President

The Minister( MoFPED)

Minister responsible for Local Governments

Local Governments Public Accounts Committee

Local Government Finance Commission

The Inspectorate of Government

Resident District Commissioner

Discussion Questions:

I. Do all the recipients listed above get copies of the audit reports?

II. Is there appropriate follow up efforts by the respective recipients to ensure all

findings and recommendations in the audit reports are implemented?

III. Do recipients appreciate the content in the reports issued by both the internal and

external auditors?

IV. What happens when the District chairperson receives the report?

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 17

4.4 PURPOSE OF AUDIT REPOERTS

Generically and in most instances the reports serve the purpose of;

Notifying the various stakeholders of the results of the audit, The President, Parliament, Audit committees management…

Making recommendations on the weaknesses identified during the audit;

Evaluate whether previous findings and recommendation have been resolved;

Report on entire work undertaken by management and make recommendations to strengthen internal controls;

Propose remedial corrective actions to be taken to correct any errors identified. 4.5 ACTIVITY 6: AUDIT REPORTS COMMUNICATION

4.6 PROCESS REPORTS ISSUED TO THE AUDITOR GENERAL Draft Management Letter This captures details of issues of concern raised during the audit that require clarification and responses from management.

Final Management letter This is prepared by the External Auditor/OAG, prior to issuing the Final Audit Report. Management letter is one of the key results of an audit because it highlight weaknesses in the operations of an entity, raises the red flag for appropriate corrective action by management and oversight agencies and guide oversight bodies on proper procedures to apply, in order to solve the weaknesses, omissions and commissions observed during an audit.

4.7 KEY ELEMENTS OF A MANAGEMENT LETTER

Key elements of management letter are:

Criteria - Regulatory framework against which a violation is measured

Condition - The nature of the violation/weakness for example no books were written

Cause - The reason for violation e.g. it could be due to incompetence, negligence,

Consequence - Implication e.g. reduced reliability on the report

Recommendation- Suggestions for improvement. This is an area for consequent action by Over-sight bodies. 4.8 TYPES OF AUDIT OPINIONS

Section 19 of the National Audit Act (NAA) 2008, states that the Auditor General shall express an OPINION on the accounts based on the results of each audit.

I. Reading the recent audit reports, what information does it communicate? Is this

helpful?

II. Do the audit reports clearly communicate information needed by the key

stakeholders in improving service delivery?

III. What are the challenges?

IV. Evaluate the reports expected from the Internal Auditor

Discussion of Findings/Exit Meeting

Exit meetings should be convened and chaired by the Accounting Officer with

sector heads and Vote Controllers attending along with the Auditor

The Auditors present their findings and recommendations, focus areas of weakness

Respective officers provide clarifications and explanations to a query with

supporting evidence

If the Auditor is not satisfied, the query will be raised in the final management

letter

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 18

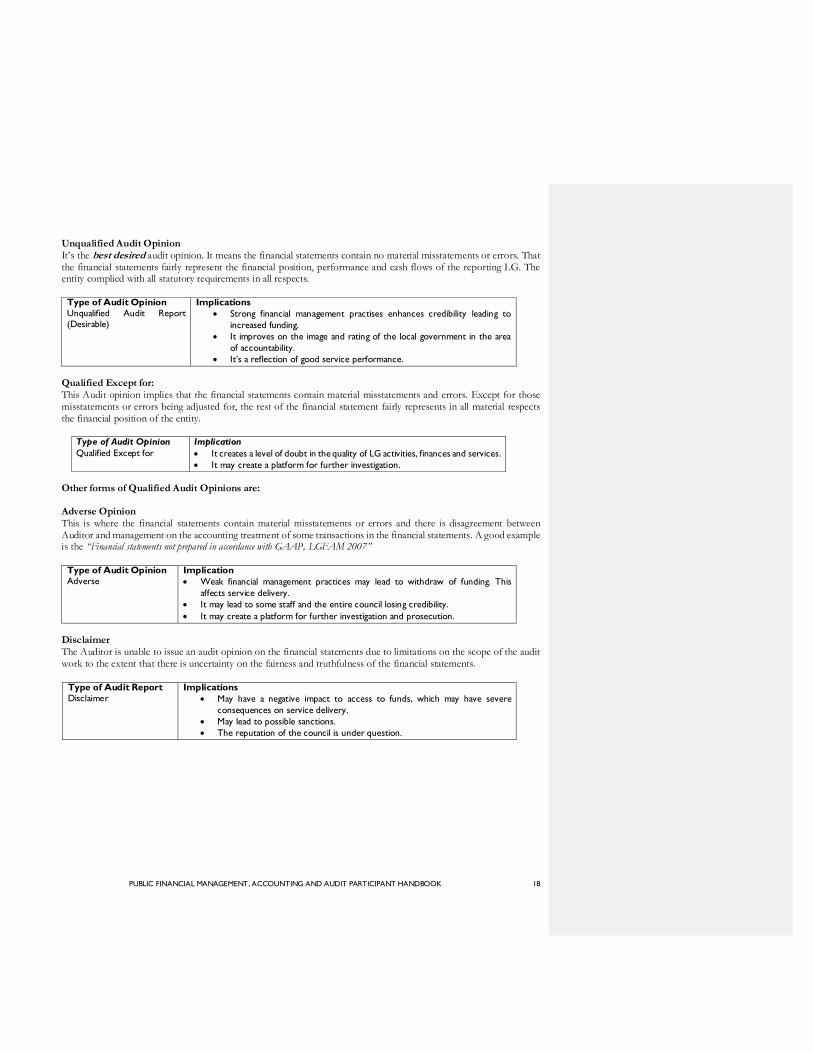

Unqualified Audit Opinion It’s the best desired audit opinion. It means the financial statements contain no material misstatements or errors. That the financial statements fairly represent the financial position, performance and cash flows of the reporting LG. The entity complied with all statutory requirements in all respects.

Type of Audit Opinion Unqualified Audit Report (Desirable)

Implications

Strong financial management practises enhances credibility leading to

increased funding.

It improves on the image and rating of the local government in the area

of accountability.

It’s a reflection of good service performance.

Qualified Except for: This Audit opinion implies that the financial statements contain material misstatements and errors. Except for those misstatements or errors being adjusted for, the rest of the financial statement fairly represents in all material respects the financial position of the entity.

Type of Audit Opinion

Qualified Except for

Implication

It creates a level of doubt in the quality of LG activities, finances and services.

It may create a platform for further investigation.

Other forms of Qualified Audit Opinions are: Adverse Opinion This is where the financial statements contain material misstatements or errors and there is disagreement between Auditor and management on the accounting treatment of some transactions in the financial statements. A good example is the “Financial statements not prepared in accordance with GAAP, LGFAM 2007”

Type of Audit Opinion Adverse

Implication

Weak financial management practices may lead to withdraw of funding. This

affects service delivery.

It may lead to some staff and the entire council losing credibility.

It may create a platform for further investigation and prosecution.

Disclaimer The Auditor is unable to issue an audit opinion on the financial statements due to limitations on the scope of the audit work to the extent that there is uncertainty on the fairness and truthfulness of the financial statements.

Type of Audit Report Disclaimer

Implications

May have a negative impact to access to funds, which may have severe

consequences on service delivery.

May lead to possible sanctions.

The reputation of the council is under question.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 19

5. COMMON AUDIT FINDINGS IN LOWER LOCAL GOVERNMENTS 5.1 OBJECTIVES

By the end of the session the participants should be able to:

Explain the context and background of negative findings

Explain the causes of the negative findings

Explain the implication of negative findings on service delivery

Discuss strategy for elimination of negative findings 5.2 CONTEXT OF AUDIT FINDINGS

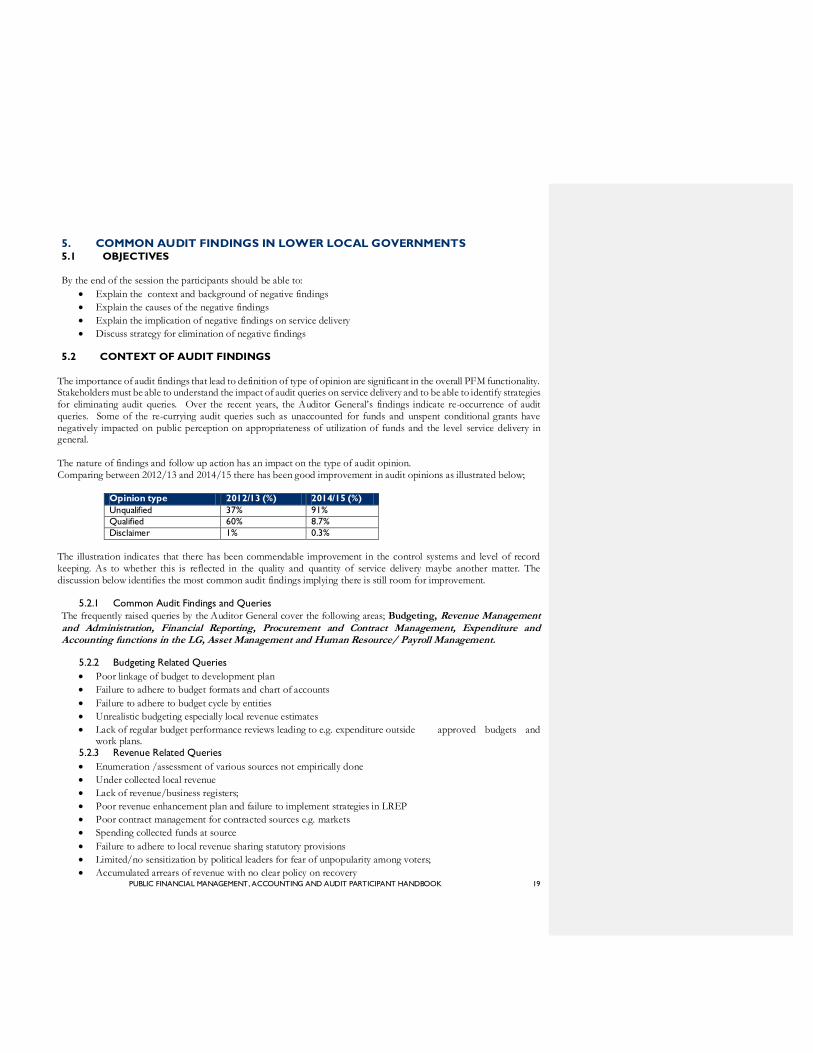

The importance of audit findings that lead to definition of type of opinion are significant in the overall PFM functionality. Stakeholders must be able to understand the impact of audit queries on service delivery and to be able to identify strategies for eliminating audit queries. Over the recent years, the Auditor General’s findings indicate re-occurrence of audit queries. Some of the re-currying audit queries such as unaccounted for funds and unspent conditional grants have negatively impacted on public perception on appropriateness of utilization of funds and the level service delivery in general. The nature of findings and follow up action has an impact on the type of audit opinion. Comparing between 2012/13 and 2014/15 there has been good improvement in audit opinions as illustrated below;

Opinion type 2012/13 (%) 2014/15 (%)

Unqualified 37% 91%

Qualified 60% 8.7%

Disclaimer 1% 0.3%

The illustration indicates that there has been commendable improvement in the control systems and level of record keeping. As to whether this is reflected in the quality and quantity of service delivery maybe another matter. The discussion below identifies the most common audit findings implying there is still room for improvement.

5.2.1 Common Audit Findings and Queries

The frequently raised queries by the Auditor General cover the following areas; Budgeting, Revenue Management and Administration, Financial Reporting, Procurement and Contract Management, Expenditure and Accounting functions in the LG, Asset Management and Human Resource/ Payroll Management.

5.2.2 Budgeting Related Queries

Poor linkage of budget to development plan

Failure to adhere to budget formats and chart of accounts

Failure to adhere to budget cycle by entities

Unrealistic budgeting especially local revenue estimates

Lack of regular budget performance reviews leading to e.g. expenditure outside approved budgets and work plans.

5.2.3 Revenue Related Queries

Enumeration /assessment of various sources not empirically done

Under collected local revenue

Lack of revenue/business registers;

Poor revenue enhancement plan and failure to implement strategies in LREP

Poor contract management for contracted sources e.g. markets

Spending collected funds at source

Failure to adhere to local revenue sharing statutory provisions

Limited/no sensitization by political leaders for fear of unpopularity among voters;

Accumulated arrears of revenue with no clear policy on recovery

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 20

Cash collected not banked in time (Revenue between chests (R.B.C). 5.2.4 Procurement Related Queries

Irregular payments-advance issue of engineer’s certificates and payment before execution of works

Procurement of goods, services and works directly without tendering, evaluation and contracting

Contracting without authority of Contracts Committee

Contracting Service Providers not pre-qualified by Contracts Committee

Unauthorized contract variation

Weak contract management e.g. lack of Contracts Registers, no contract supervisors

Certification of petty road claims by Sub-county Chiefs and Chairpersons for no work done

Delayed completion of works and over stretched contractors

Payment for unexecuted/incomplete or poor quality works

Inconsistencies in the contract documents/drawings.

Inconsistencies in the contract documents/drawings. 5.2.5 Expenditure/Accounting Related Queries

Unretired advances after 30 days lapse and lack of proper management of advances

Overpayment of salaries and Delayed settlement of payables

Outstanding cumulative commitments especially hospital utility bills

Nugatory expenditures e.g. penalty by the bank due to bounced for insufficient funds, URA penalty due to failure to remit tax deductions, court awards, etc.

Excessive commitments on fuel and lubricants

Unauthorized excess expenditures

Late submission of accounts contrary to Regulation 68 of LGFARs 2007

Un-vouched expenditures

Doubtful/Wasteful/nugatory expenditure and inflated payments

Inadequate supporting documents

Non-certification of Cash/ Bank Balances 5.2.6 Asset Management Queries

Failure to carry out boards of survey in line with the provisions of the LGFAM 2007

Failure to maintain up to date asset registers

Non depreciation of fixed assets especially in urban councils

Doubtful ownership of fixed assets, unsupported stores and other assets

Failure to maintain up to date store records such as stock cards, physical stock not matching with store records etc.

Non-disposal of old and redundant assets. 5.2.7 Human Resource/Payroll Management Queries

Overpayment of salaries including unexplained salary increases to staff/deliberate over payments

Un up-to-date or non-existing staff lists

Payroll reductions to more than 50% of employee salaries due to multiple loans

Poor records management/loss of staff files leading to delayed processing of employee benefits

Absence of a register /payroll for local pension /gratuity for contract staff

Unreported cases of absenteeism, abscondment, late coming etc.

Scanty manpower in some departments and failure to recruit /confirm staff2

2 Bududa district un filled posts

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 21

5.3 ACTIVITY 7: IMPLICATIONS OF UNRESOLVED AUDIT QUERIES

5.4 CASE STUDIES ON COMMON AUDIT FINDINGS CASE STUDY 1: Budget Performance extract The Budget performance of “Mafuta” District LG” for year ended 30th June, 2015 shows that here was a shortfall in revenue of UGX 455,000,000 and expenditure was in excess by UGX 680,000,000. According to the Auditor General, there was no satisfactory explanation given for the anomaly in the budget performance by management. Required:

Speculate on the possible causes Identify the queries and their possible causes and implications.

Make appropriate Recommendations. CASE STUDY 2: Expenditure/Administrative Advances During the audit of “ABC Municipal Council” for the FY 2014/15, the Auditor General revealed that there was no improvement in control over granting and management of advances. Advances amounting to UGX 150,000,000 were granted to officials who had not settled previous accounts, while other outstanding balances totalling UGX 80,000,000 were granted to employees of the Municipal Council but had since left service. In such a situation, prospects of full recovery of advances are remote. Required:

State the causes of outstanding personal and administrative advances

Recommend procedures for managing personal and administrative advances

What corrective action would you recommend to the Chief Executive, LGPAC and Executive Committee? CASE STUDY 3: Expenditure/Administrative Advances In the accounts of “Topowa sub county Council”, expenditure payments made without supporting documents totaled UGX 70,000,000 during the FY 2014/15 and payment vouchers for expenditure totaling UGX 50,000,000 were not availed for audit by Management. In the absence of complete documentation, this expenditure can be regarded as potentially fraudulent. Required:

For the issues raised, recommend actions to be taken to mitigate the queries

In the event the issues remain outstanding, what further actions do you recommend? CASE STUDY 4: General findings Audit Report for “Lapena district LG” for the financial year 2014/2015 dated: 31st, February 2016. Key issues:

Expenditure payments made without supporting documents totaled UGX 45,000,000.

Payment vouchers for expenditure totaling UGX 85,000,000 were not availed for audit by the Head of Finance.

Funds meant for the construction of a Health Centre II totaling UGX 80,000,000 were borrowed and paid as Councilors’ allowances. This amount was not refunded during the year.

Similarly, UGX 70,000,000 was borrowed from the SFG Account in the Education department to compensate a staff member who had won a Court case against unfair dismissal. Due to breakdown of foot and mouth

I. In reference to own local government, analyse the query type in recent report

II. What the expected impact of this occurrence is as described in the query on service

delivery

III. Who is responsible for the elimination of these queries?

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 22

disease, expected revenues from markets could not be realized and consequently the LG could not refund the money to the Education sector within the FY.

Cash balance of UGX 25,540,500 at the closure of the FY’s operations was not supported by any Cash Certificate.

Cash of UGX 12,908,000 received from “Apo Sub-county” on 31st December 2014 as 35% share of local revenue was only recorded in the Cash Book with no details of banking. It was later discovered that the funds had been spent by the District Cashier on the orders of the Head of Finance.

Payments for cleaning work worth UGX 15,044,000 was made to “Devine Technical Services Ltd” without contract details. The firm was reflected on the LG’s pre-qualified schedule.

Required:

In each of the above cases whom do you think is responsible for the anomaly, if any.

Explain how each of the above issues should be addressed by management.

PUBLIC FINANCIAL MANAGEMENT, ACCOUNTING AND AUDIT PARTICIPANT HANDBOOK 23