PT SARATOGA INVESTAMA SEDAYA TBKsaratoga-investama.com/wp-content/uploads/2016/03/Saratoga... · 2...

27

PT SARATOGA INVESTAMA SEDAYA TBK 9M 2015 Results November 2015

Transcript of PT SARATOGA INVESTAMA SEDAYA TBKsaratoga-investama.com/wp-content/uploads/2016/03/Saratoga... · 2...

1

PT SARATOGA INVESTAMA SEDAYA TBK

9M 2015 Results

November 2015

2

Disclaimer

“These materials have been prepared by PT Saratoga Investama Sedaya, Tbk (the “Company”) from various internal sources and have not been independently verified. These materials are for information purposes only and do not constitute or form part of an offer, solicitation or invitation of any offer to buy or subscribe for any securities of the Company, in any jurisdiction, nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract, commitment or investment decision whatsoever. Any decision to purchase or subscribe for any securities of the Company should be made after seeking appropriate professional advice.

These materials contain embedded statements that constitute forward-looking statements. These statements include descriptions regarding the intent, belief or current expectations of the Company or its officers with respect to the consolidated results of operations and financial condition of the Company. These statements can be recognized by the use of words whether or not explicitly stated such as “expects,” “plan,” “will,” “estimates,” “projects,” “intends,” or words of similar meaning. Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ from those in the forward-looking statements as a result of various factors and assumptions. The Company has no obligation and does not undertake to revise forward-looking statements to reflect future events or circumstances.

No representation or warranty, expressed or implied, is made and no reliance should be placed on the accuracy, fairness or completeness of the information presented or contained in these materials. The Company or any of its affiliates, advisers or representatives accepts no liability whatsoever for any loss howsoever with respect to any use or reliance upon any of the information presented or contained in these materials. The information presented or contained in these materials is subject to change without notice and its accuracy is not guaranteed.”

3

CORPORATE INFORMATION

4

Saratoga, a Leading Active Investment Company

Infrastructure Consumer

Power Roads Telecomm-unications

Automotive Property

PT Unitras Pertama Edwin Soeryadjaya Sandiaga S. Uno Public

29.2% 31.5% 29.2% 10.2%

Natural Resources

Agriculture Oil & Gas Metals & Mining

Leading active investment company in Indonesia with an estimated NAV of IDR 15tn

Listed on the IDX in 2013 among the top 100 largest market capitalization stocks in IDX

Invested in early-stage, growth-stage, and special situation opportunities and actively engaged with investee

companies’ management teams in unlocking value of investments

Focus on key sectors of the Indonesian economy: Consumer, Infrastructure and Natural Resources

Lifestyle

22 Operating Companies: 11 Publicly Listed & 11 Non-Listed >40,000 Employees

Generating >USD 6 B Revenue

Data presented are as of 30 Sep 2015

IDR/USD as of 30 Sep 2015 = 14,657

Source: Company information

5

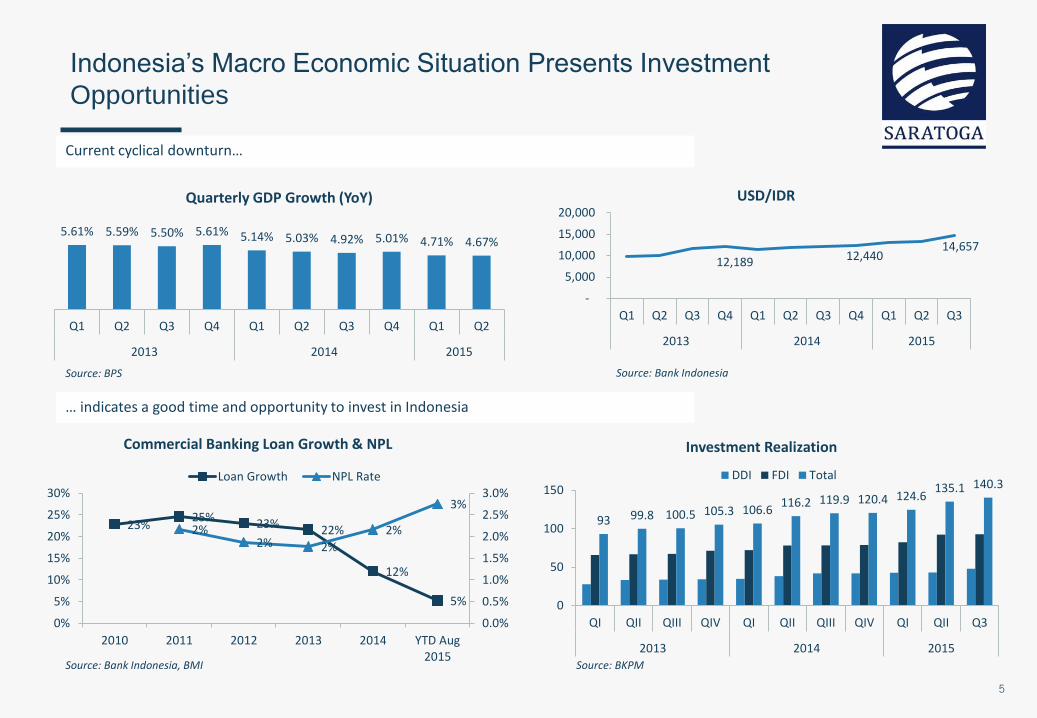

Indonesia’s Macro Economic Situation Presents Investment

Opportunities

5.61% 5.59% 5.50% 5.61% 5.14% 5.03% 4.92% 5.01% 4.71% 4.67%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2013 2014 2015

Quarterly GDP Growth (YoY)

12,189 12,440 14,657

-

5,000

10,000

15,000

20,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2013 2014 2015

USD/IDR

Source: BPS Source: Bank Indonesia

93 99.8 100.5 105.3 106.6 116.2 119.9 120.4 124.6

135.1 140.3

0

50

100

150

QI QII QIII QIV QI QII QIII QIV QI QII Q3

2013 2014 2015

Investment Realization

DDI FDI Total

Source: BKPM

23% 25% 23% 22%

12%

5%

2% 2% 2%

2%

3%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014 YTD Aug2015

Commercial Banking Loan Growth & NPL

Loan Growth NPL Rate

Source: Bank Indonesia, BMI

Current cyclical downturn…

… indicates a good time and opportunity to invest in Indonesia

6

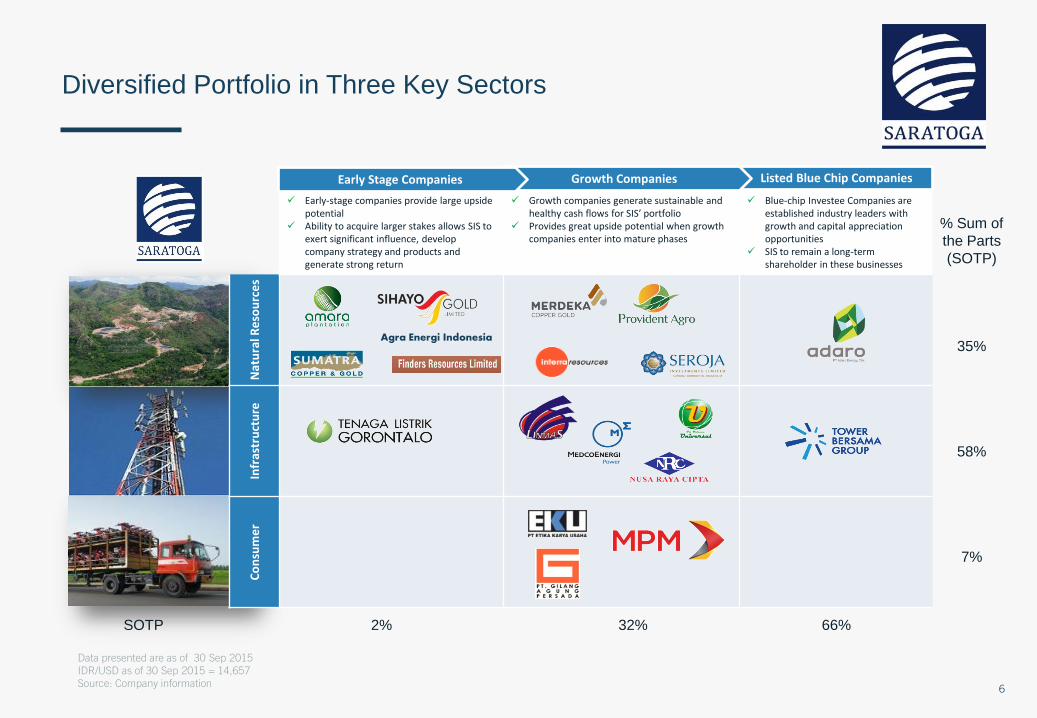

Diversified Portfolio in Three Key Sectors

Early-stage companies provide large upside potential

Ability to acquire larger stakes allows SIS to exert significant influence, develop company strategy and products and generate strong return

Growth companies generate sustainable and healthy cash flows for SIS’ portfolio

Provides great upside potential when growth companies enter into mature phases

Blue-chip Investee Companies are established industry leaders with growth and capital appreciation opportunities

SIS to remain a long-term shareholder in these businesses

Nat

ura

l Re

sou

rce

s In

fras

tru

ctu

re

Co

nsu

me

r

SOTP 2% 32% 66%

% Sum of

the Parts

(SOTP)

35%

58%

7%

Agra Energi Indonesia

Listed Blue Chip Companies Growth Companies Early Stage Companies

Data presented are as of 30 Sep 2015

IDR/USD as of 30 Sep 2015 = 14,657

Source: Company information

7

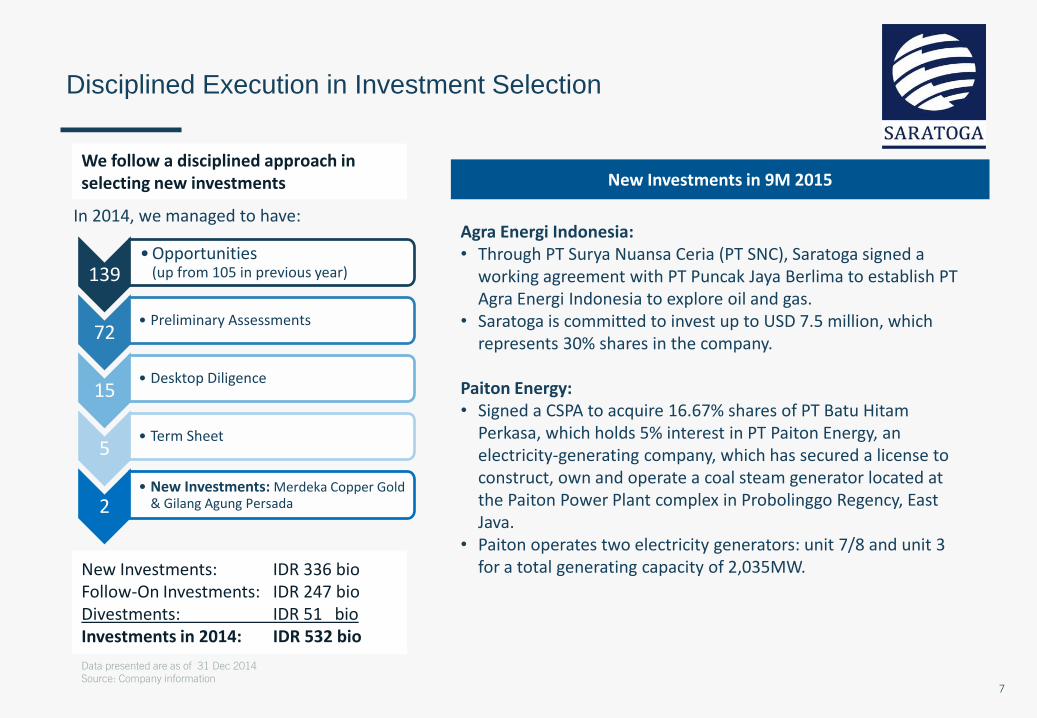

Disciplined Execution in Investment Selection

139 • Opportunities

(up from 105 in previous year)

72 • Preliminary Assessments

15 • Desktop Diligence

5 • Term Sheet

2 • New Investments: Merdeka Copper Gold

& Gilang Agung Persada

We follow a disciplined approach in selecting new investments

New Investments: IDR 336 bio Follow-On Investments: IDR 247 bio Divestments: IDR 51 bio Investments in 2014: IDR 532 bio

New Investments in 9M 2015

Data presented are as of 31 Dec 2014

Source: Company information

Agra Energi Indonesia: • Through PT Surya Nuansa Ceria (PT SNC), Saratoga signed a

working agreement with PT Puncak Jaya Berlima to establish PT Agra Energi Indonesia to explore oil and gas.

• Saratoga is committed to invest up to USD 7.5 million, which represents 30% shares in the company.

Paiton Energy: • Signed a CSPA to acquire 16.67% shares of PT Batu Hitam

Perkasa, which holds 5% interest in PT Paiton Energy, an electricity-generating company, which has secured a license to construct, own and operate a coal steam generator located at the Paiton Power Plant complex in Probolinggo Regency, East Java.

• Paiton operates two electricity generators: unit 7/8 and unit 3 for a total generating capacity of 2,035MW.

In 2014, we managed to have:

8

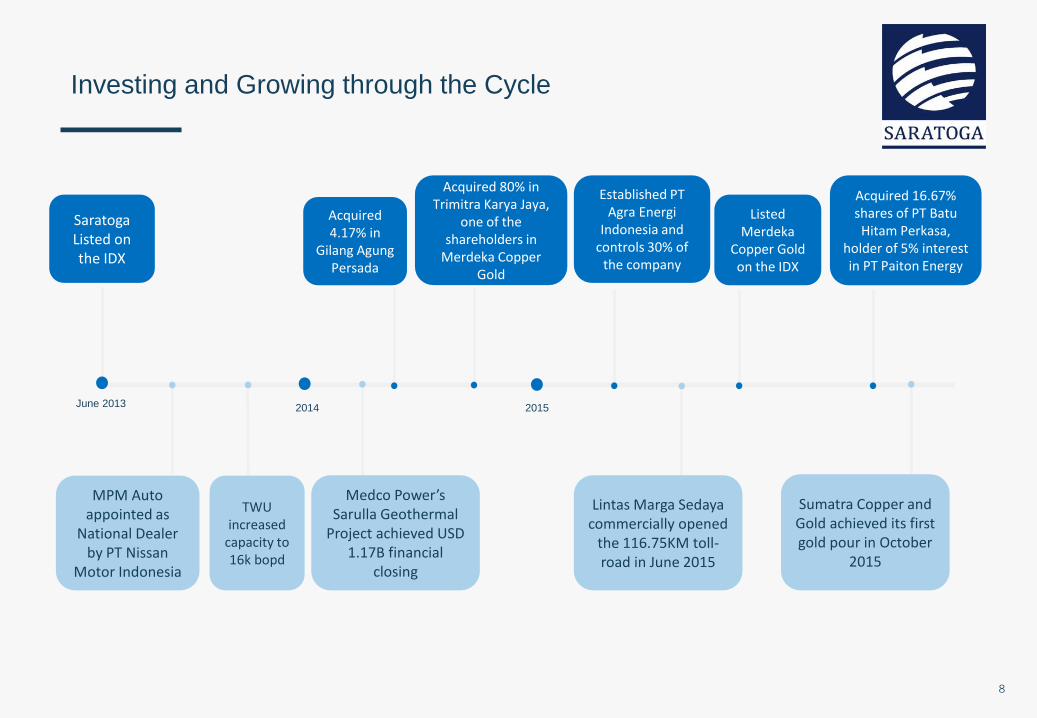

Investing and Growing through the Cycle

Saratoga Listed on the IDX

June 2013

MPM Auto appointed as

National Dealer by PT Nissan

Motor Indonesia

TWU increased

capacity to 16k bopd

2014

Medco Power’s Sarulla Geothermal

Project achieved USD 1.17B financial

closing

Acquired 4.17% in

Gilang Agung Persada

Acquired 80% in Trimitra Karya Jaya,

one of the shareholders in

Merdeka Copper Gold

Listed Merdeka

Copper Gold on the IDX

2015

Established PT Agra Energi

Indonesia and controls 30% of

the company

Lintas Marga Sedaya commercially opened

the 116.75KM toll-road in June 2015

Sumatra Copper and Gold achieved its first gold pour in October

2015

Acquired 16.67% shares of PT Batu

Hitam Perkasa, holder of 5% interest in PT Paiton Energy

9

PORTFOLIO HIGHLIGHTS

10

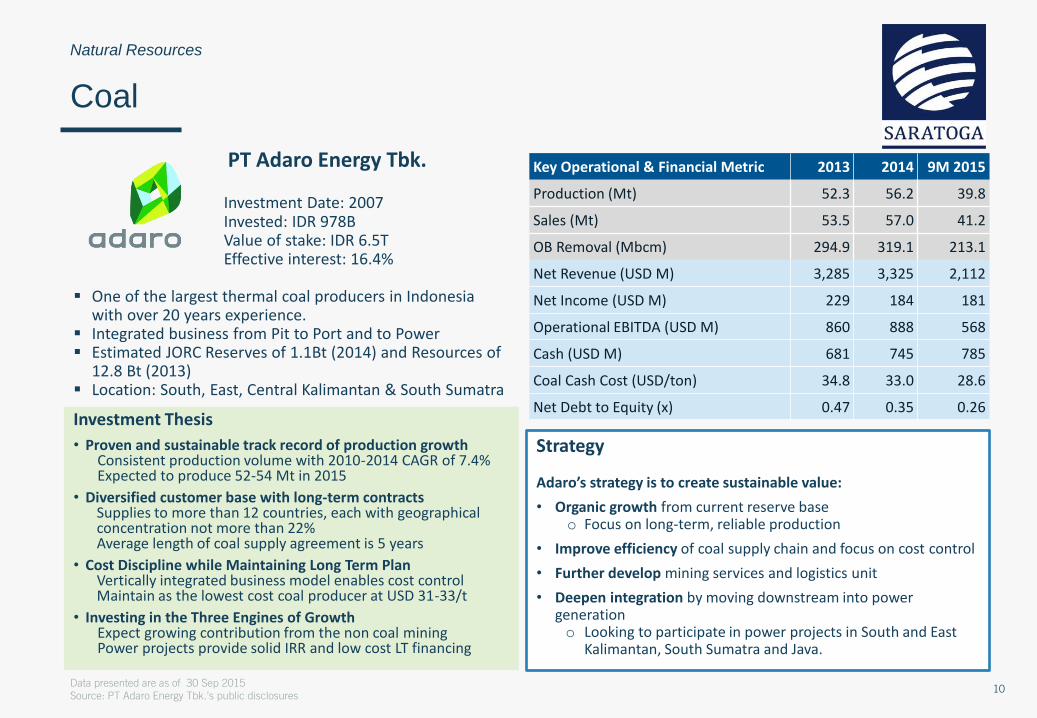

Natural Resources

Coal

PT Adaro Energy Tbk. Investment Date: 2007 Invested: IDR 978B Value of stake: IDR 6.5T Effective interest: 16.4% One of the largest thermal coal producers in Indonesia

with over 20 years experience. Integrated business from Pit to Port and to Power Estimated JORC Reserves of 1.1Bt (2014) and Resources of

12.8 Bt (2013) Location: South, East, Central Kalimantan & South Sumatra

Investment Thesis

• Proven and sustainable track record of production growth Consistent production volume with 2010-2014 CAGR of 7.4% Expected to produce 52-54 Mt in 2015

• Diversified customer base with long-term contracts Supplies to more than 12 countries, each with geographical concentration not more than 22% Average length of coal supply agreement is 5 years

• Cost Discipline while Maintaining Long Term Plan Vertically integrated business model enables cost control Maintain as the lowest cost coal producer at USD 31-33/t

• Investing in the Three Engines of Growth Expect growing contribution from the non coal mining Power projects provide solid IRR and low cost LT financing

Strategy Adaro’s strategy is to create sustainable value:

• Organic growth from current reserve base o Focus on long-term, reliable production

• Improve efficiency of coal supply chain and focus on cost control

• Further develop mining services and logistics unit

• Deepen integration by moving downstream into power generation o Looking to participate in power projects in South and East

Kalimantan, South Sumatra and Java.

Key Operational & Financial Metric 2013 2014 9M 2015

Production (Mt) 52.3 56.2 39.8

Sales (Mt) 53.5 57.0 41.2

OB Removal (Mbcm) 294.9 319.1 213.1

Net Revenue (USD M) 3,285 3,325 2,112

Net Income (USD M) 229 184 181

Operational EBITDA (USD M) 860 888 568

Cash (USD M) 681 745 785

Coal Cash Cost (USD/ton) 34.8 33.0 28.6

Net Debt to Equity (x) 0.47 0.35 0.26

Data presented are as of 30 Sep 2015

Source: PT Adaro Energy Tbk.’s public disclosures

11

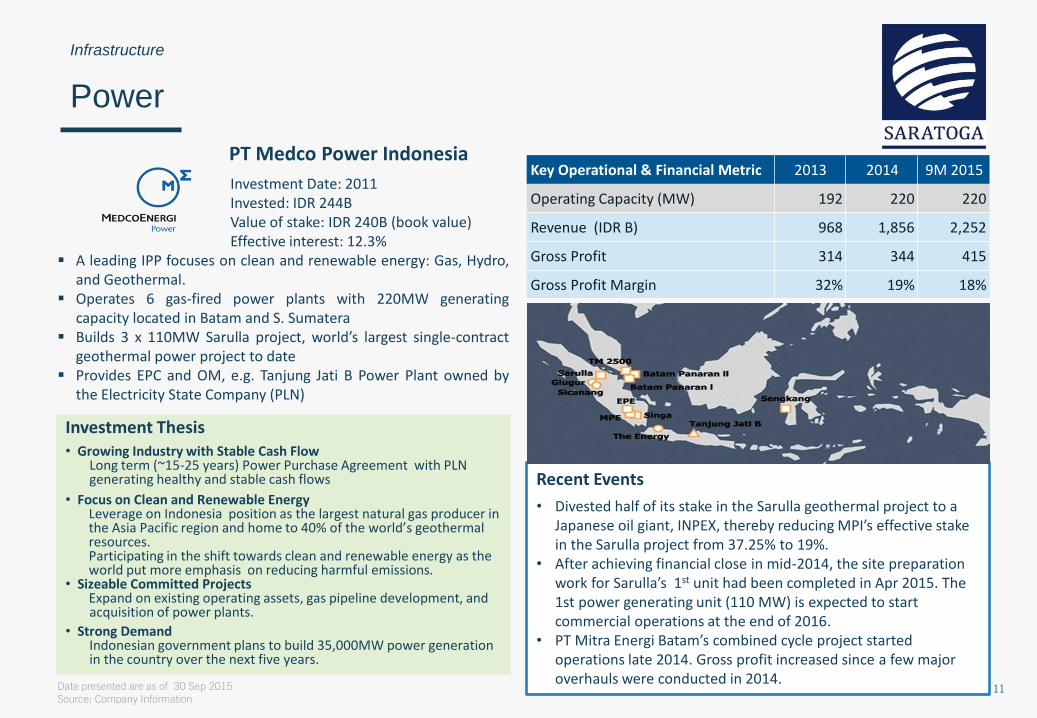

Infrastructure

Power

PT Medco Power Indonesia

Investment Date: 2011 Invested: IDR 244B Value of stake: IDR 240B (book value) Effective interest: 12.3% A leading IPP focuses on clean and renewable energy: Gas, Hydro,

and Geothermal. Operates 6 gas-fired power plants with 220MW generating

capacity located in Batam and S. Sumatera Builds 3 x 110MW Sarulla project, world’s largest single-contract

geothermal power project to date Provides EPC and OM, e.g. Tanjung Jati B Power Plant owned by

the Electricity State Company (PLN)

Investment Thesis

• Growing Industry with Stable Cash Flow Long term (~15-25 years) Power Purchase Agreement with PLN generating healthy and stable cash flows

• Focus on Clean and Renewable Energy Leverage on Indonesia position as the largest natural gas producer in the Asia Pacific region and home to 40% of the world’s geothermal resources. Participating in the shift towards clean and renewable energy as the world put more emphasis on reducing harmful emissions.

• Sizeable Committed Projects Expand on existing operating assets, gas pipeline development, and acquisition of power plants.

• Strong Demand Indonesian government plans to build 35,000MW power generation in the country over the next five years.

Key Operational & Financial Metric 2013 2014 9M 2015

Operating Capacity (MW) 192 220 220

Revenue (IDR B) 968 1,856 2,252

Gross Profit 314 344 415

Gross Profit Margin 32% 19% 18%

Recent Events

• Divested half of its stake in the Sarulla geothermal project to a Japanese oil giant, INPEX, thereby reducing MPI’s effective stake in the Sarulla project from 37.25% to 19%.

• After achieving financial close in mid-2014, the site preparation work for Sarulla’s 1st unit had been completed in Apr 2015. The 1st power generating unit (110 MW) is expected to start commercial operations at the end of 2016.

• PT Mitra Energi Batam’s combined cycle project started operations late 2014. Gross profit increased since a few major overhauls were conducted in 2014.

Data presented are as of 30 Sep 2015

Source: Company Information

12

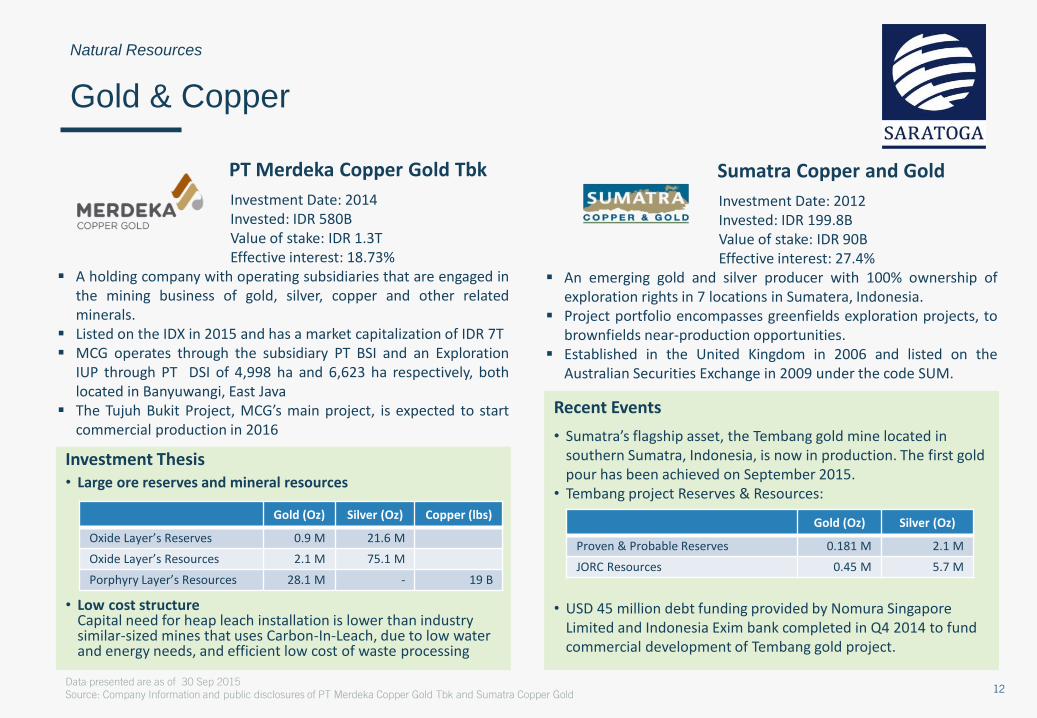

Natural Resources

Gold & Copper

PT Merdeka Copper Gold Tbk

Investment Date: 2014 Invested: IDR 580B Value of stake: IDR 1.3T Effective interest: 18.73% A holding company with operating subsidiaries that are engaged in

the mining business of gold, silver, copper and other related minerals.

Listed on the IDX in 2015 and has a market capitalization of IDR 7T MCG operates through the subsidiary PT BSI and an Exploration

IUP through PT DSI of 4,998 ha and 6,623 ha respectively, both located in Banyuwangi, East Java

The Tujuh Bukit Project, MCG’s main project, is expected to start commercial production in 2016

Sumatra Copper and Gold

Investment Date: 2012 Invested: IDR 199.8B Value of stake: IDR 90B Effective interest: 27.4% An emerging gold and silver producer with 100% ownership of

exploration rights in 7 locations in Sumatera, Indonesia. Project portfolio encompasses greenfields exploration projects, to

brownfields near-production opportunities. Established in the United Kingdom in 2006 and listed on the

Australian Securities Exchange in 2009 under the code SUM.

Investment Thesis

• Large ore reserves and mineral resources • Low cost structure

Capital need for heap leach installation is lower than industry similar-sized mines that uses Carbon-In-Leach, due to low water and energy needs, and efficient low cost of waste processing

Gold (Oz) Silver (Oz) Copper (lbs)

Oxide Layer’s Reserves 0.9 M 21.6 M

Oxide Layer’s Resources 2.1 M 75.1 M

Porphyry Layer’s Resources 28.1 M - 19 B

Recent Events

• Sumatra’s flagship asset, the Tembang gold mine located in southern Sumatra, Indonesia, is now in production. The first gold pour has been achieved on September 2015.

• Tembang project Reserves & Resources: • USD 45 million debt funding provided by Nomura Singapore

Limited and Indonesia Exim bank completed in Q4 2014 to fund commercial development of Tembang gold project.

Gold (Oz) Silver (Oz)

Proven & Probable Reserves 0.181 M 2.1 M

JORC Resources 0.45 M 5.7 M

Data presented are as of 30 Sep 2015

Source: Company Information and public disclosures of PT Merdeka Copper Gold Tbk and Sumatra Copper Gold

13

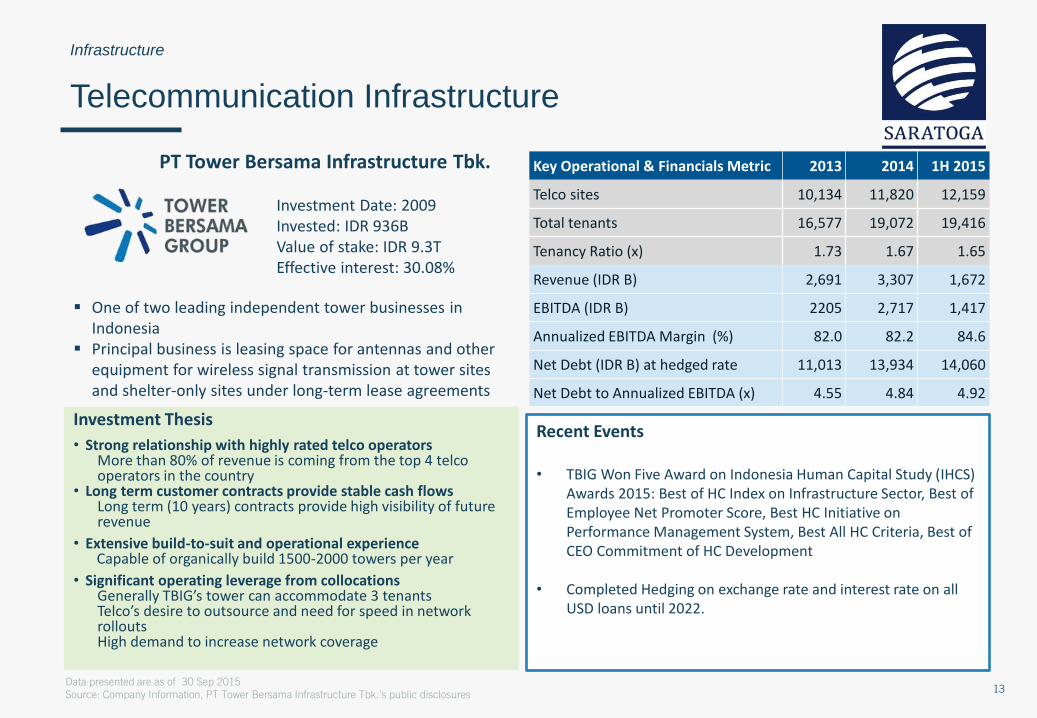

Infrastructure

Telecommunication Infrastructure

PT Tower Bersama Infrastructure Tbk. Investment Date: 2009 Invested: IDR 936B Value of stake: IDR 9.3T Effective interest: 30.08%

One of two leading independent tower businesses in Indonesia

Principal business is leasing space for antennas and other equipment for wireless signal transmission at tower sites and shelter-only sites under long-term lease agreements

Investment Thesis

• Strong relationship with highly rated telco operators More than 80% of revenue is coming from the top 4 telco operators in the country

• Long term customer contracts provide stable cash flows Long term (10 years) contracts provide high visibility of future revenue

• Extensive build-to-suit and operational experience Capable of organically build 1500-2000 towers per year

• Significant operating leverage from collocations Generally TBIG’s tower can accommodate 3 tenants Telco’s desire to outsource and need for speed in network rollouts High demand to increase network coverage

Recent Events • TBIG Won Five Award on Indonesia Human Capital Study (IHCS)

Awards 2015: Best of HC Index on Infrastructure Sector, Best of Employee Net Promoter Score, Best HC Initiative on Performance Management System, Best All HC Criteria, Best of CEO Commitment of HC Development

• Completed Hedging on exchange rate and interest rate on all USD loans until 2022.

Key Operational & Financials Metric 2013 2014 1H 2015

Telco sites 10,134 11,820 12,159

Total tenants 16,577 19,072 19,416

Tenancy Ratio (x) 1.73 1.67 1.65

Revenue (IDR B) 2,691 3,307 1,672

EBITDA (IDR B) 2205 2,717 1,417

Annualized EBITDA Margin (%) 82.0 82.2 84.6

Net Debt (IDR B) at hedged rate 11,013 13,934 14,060

Net Debt to Annualized EBITDA (x) 4.55 4.84 4.92

Data presented are as of 30 Sep 2015

Source: Company Information, PT Tower Bersama Infrastructure Tbk.’s public disclosures

14

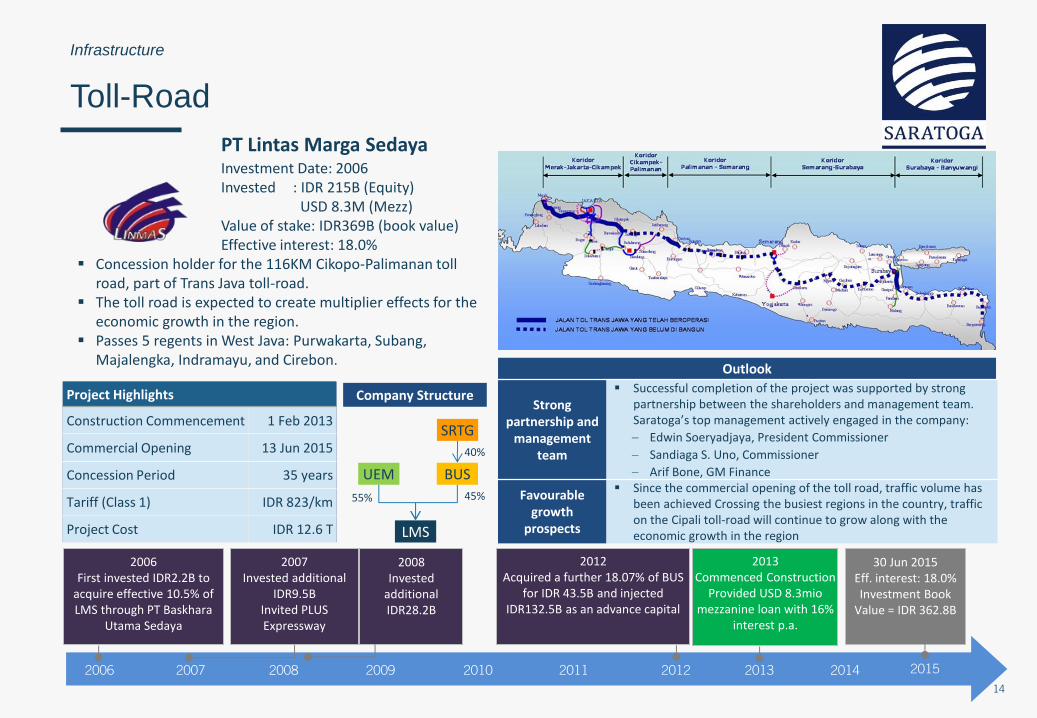

Infrastructure

Toll-Road

PT Lintas Marga Sedaya

Investment Date: 2006 Invested : IDR 215B (Equity) USD 8.3M (Mezz) Value of stake: IDR369B (book value) Effective interest: 18.0% Concession holder for the 116KM Cikopo-Palimanan toll

road, part of Trans Java toll-road. The toll road is expected to create multiplier effects for the

economic growth in the region. Passes 5 regents in West Java: Purwakarta, Subang,

Majalengka, Indramayu, and Cirebon. Outlook

Strong partnership and

management team

Successful completion of the project was supported by strong partnership between the shareholders and management team. Saratoga’s top management actively engaged in the company:

– Edwin Soeryadjaya, President Commissioner

– Sandiaga S. Uno, Commissioner

– Arif Bone, GM Finance

Favourable growth

prospects

Since the commercial opening of the toll road, traffic volume has been achieved Crossing the busiest regions in the country, traffic on the Cipali toll-road will continue to grow along with the economic growth in the region

Project Highlights

Construction Commencement 1 Feb 2013

Commercial Opening 13 Jun 2015

Concession Period 35 years

Tariff (Class 1) IDR 823/km

Project Cost IDR 12.6 T

Company Structure

UEM BUS

LMS

55% 45%

SRTG

40%

2006 First invested IDR2.2B to

acquire effective 10.5% of LMS through PT Baskhara

Utama Sedaya

2012 Acquired a further 18.07% of BUS

for IDR 43.5B and injected IDR132.5B as an advance capital

30 Jun 2015 Eff. interest: 18.0% Investment Book

Value = IDR 362.8B

2008 Invested

additional IDR28.2B

2010 2011 2013 2006 2008 2009 2012 2014 2015 2007

2013 Commenced Construction

Provided USD 8.3mio mezzanine loan with 16%

interest p.a.

2007 Invested additional

IDR9.5B Invited PLUS Expressway

15

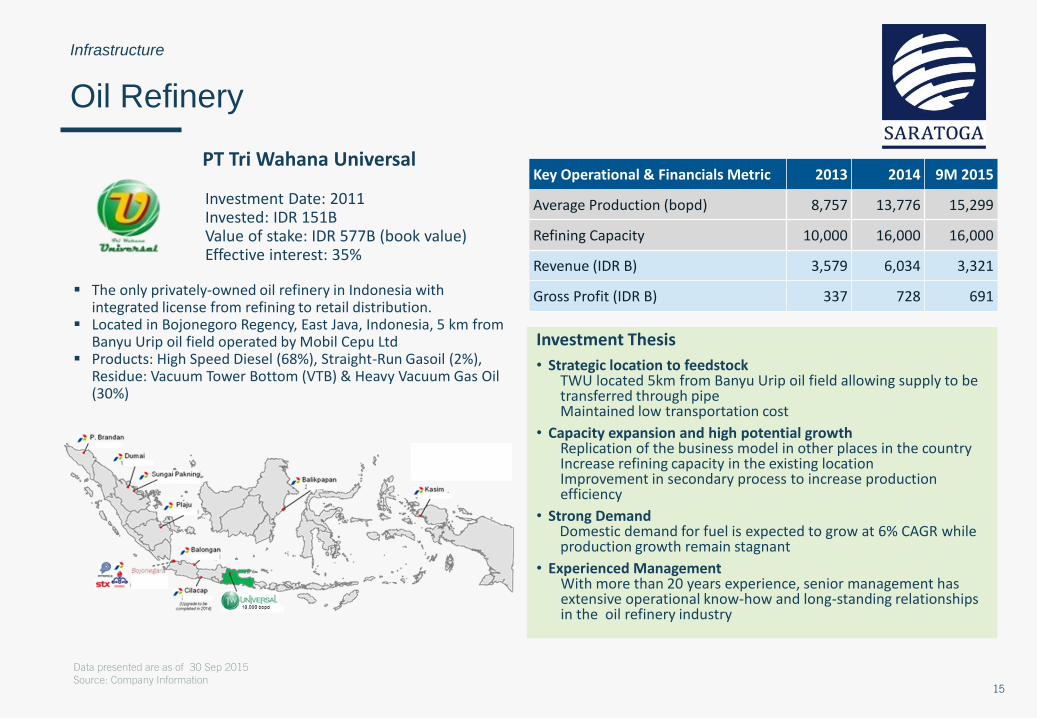

Infrastructure

Oil Refinery

PT Tri Wahana Universal Investment Date: 2011 Invested: IDR 151B Value of stake: IDR 577B (book value) Effective interest: 35% The only privately-owned oil refinery in Indonesia with

integrated license from refining to retail distribution. Located in Bojonegoro Regency, East Java, Indonesia, 5 km from

Banyu Urip oil field operated by Mobil Cepu Ltd Products: High Speed Diesel (68%), Straight-Run Gasoil (2%),

Residue: Vacuum Tower Bottom (VTB) & Heavy Vacuum Gas Oil (30%)

Investment Thesis

• Strategic location to feedstock TWU located 5km from Banyu Urip oil field allowing supply to be transferred through pipe Maintained low transportation cost

• Capacity expansion and high potential growth Replication of the business model in other places in the country Increase refining capacity in the existing location Improvement in secondary process to increase production efficiency

• Strong Demand Domestic demand for fuel is expected to grow at 6% CAGR while production growth remain stagnant

• Experienced Management With more than 20 years experience, senior management has extensive operational know-how and long-standing relationships in the oil refinery industry

Key Operational & Financials Metric 2013 2014 9M 2015

Average Production (bopd) 8,757 13,776 15,299

Refining Capacity 10,000 16,000 16,000

Revenue (IDR B) 3,579 6,034 3,321

Gross Profit (IDR B) 337 728 691

Data presented are as of 30 Sep 2015

Source: Company Information

16

FINANCIAL OVERVIEW

17

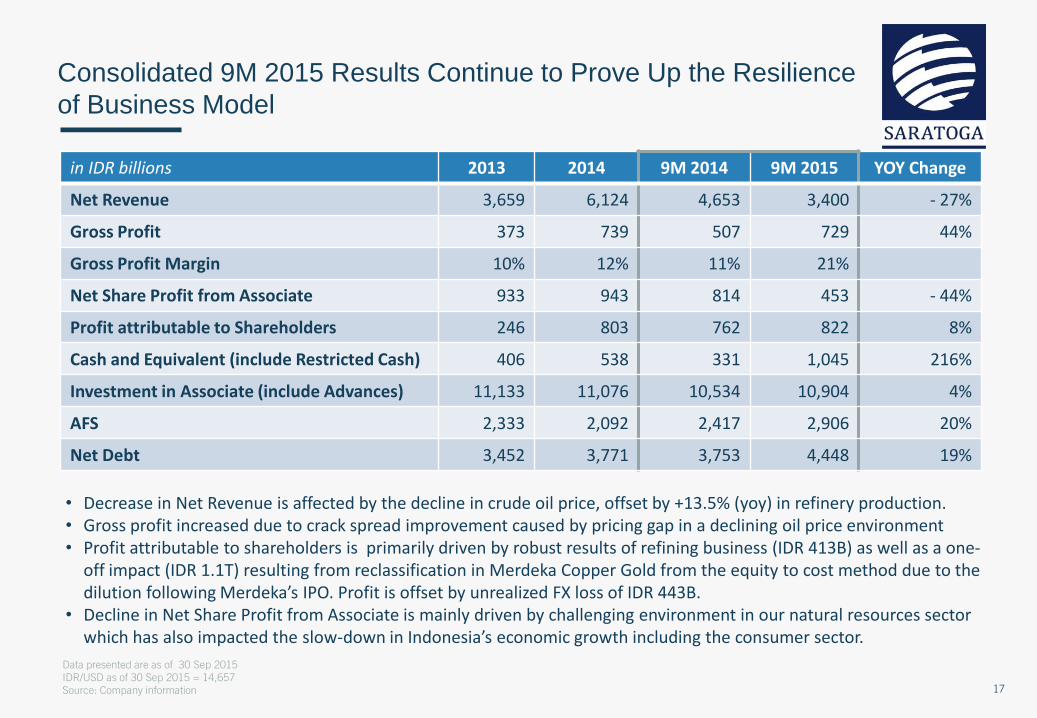

Consolidated 9M 2015 Results Continue to Prove Up the Resilience

of Business Model

in IDR billions 2013 2014 9M 2014 9M 2015 YOY Change

Net Revenue 3,659 6,124 4,653 3,400 - 27%

Gross Profit 373 739 507 729 44%

Gross Profit Margin 10% 12% 11% 21%

Net Share Profit from Associate 933 943 814 453 - 44%

Profit attributable to Shareholders 246 803 762 822 8%

Cash and Equivalent (include Restricted Cash) 406 538 331 1,045 216%

Investment in Associate (include Advances) 11,133 11,076 10,534 10,904 4%

AFS 2,333 2,092 2,417 2,906 20%

Net Debt 3,452 3,771 3,753 4,448 19%

• Decrease in Net Revenue is affected by the decline in crude oil price, offset by +13.5% (yoy) in refinery production. • Gross profit increased due to crack spread improvement caused by pricing gap in a declining oil price environment • Profit attributable to shareholders is primarily driven by robust results of refining business (IDR 413B) as well as a one-

off impact (IDR 1.1T) resulting from reclassification in Merdeka Copper Gold from the equity to cost method due to the dilution following Merdeka’s IPO. Profit is offset by unrealized FX loss of IDR 443B.

• Decline in Net Share Profit from Associate is mainly driven by challenging environment in our natural resources sector which has also impacted the slow-down in Indonesia’s economic growth including the consumer sector.

Data presented are as of 30 Sep 2015

IDR/USD as of 30 Sep 2015 = 14,657

Source: Company information

18

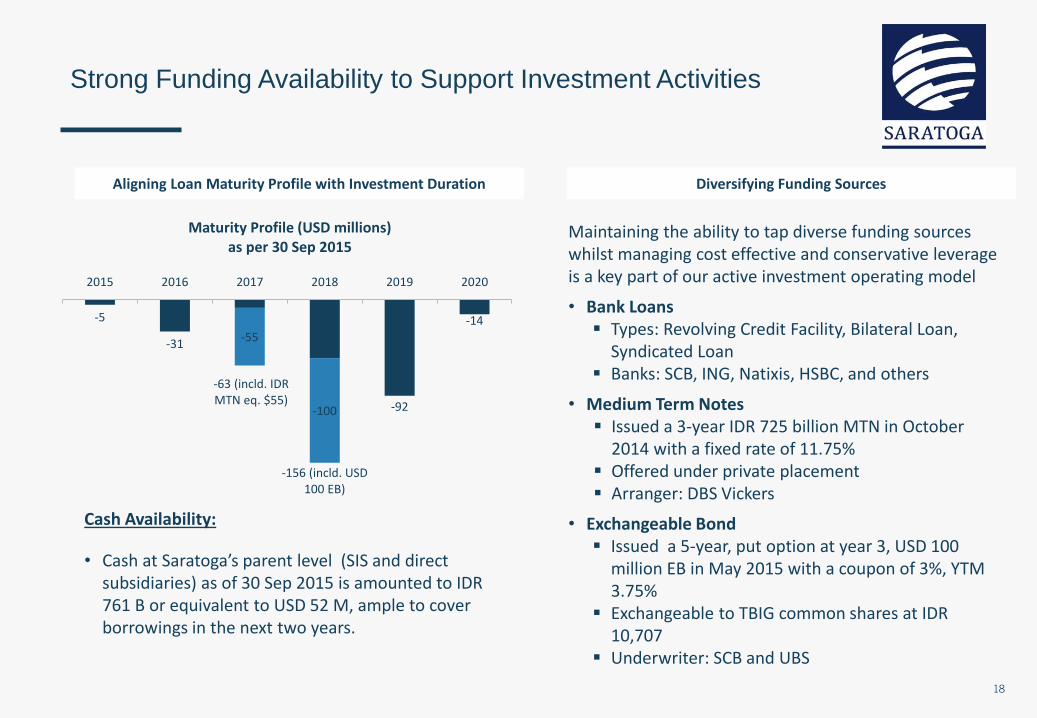

Strong Funding Availability to Support Investment Activities

Aligning Loan Maturity Profile with Investment Duration

-5

-31

-63 (incld. IDR MTN eq. $55)

-156 (incld. USD 100 EB)

-92

-14 -55

-100

2015 2016 2017 2018 2019 2020

Maturity Profile (USD millions) as per 30 Sep 2015

Diversifying Funding Sources

Maintaining the ability to tap diverse funding sources whilst managing cost effective and conservative leverage is a key part of our active investment operating model

• Bank Loans Types: Revolving Credit Facility, Bilateral Loan,

Syndicated Loan Banks: SCB, ING, Natixis, HSBC, and others

• Medium Term Notes Issued a 3-year IDR 725 billion MTN in October

2014 with a fixed rate of 11.75% Offered under private placement Arranger: DBS Vickers

• Exchangeable Bond Issued a 5-year, put option at year 3, USD 100

million EB in May 2015 with a coupon of 3%, YTM 3.75%

Exchangeable to TBIG common shares at IDR 10,707

Underwriter: SCB and UBS

Cash Availability:

• Cash at Saratoga’s parent level (SIS and direct subsidiaries) as of 30 Sep 2015 is amounted to IDR 761 B or equivalent to USD 52 M, ample to cover borrowings in the next two years.

19

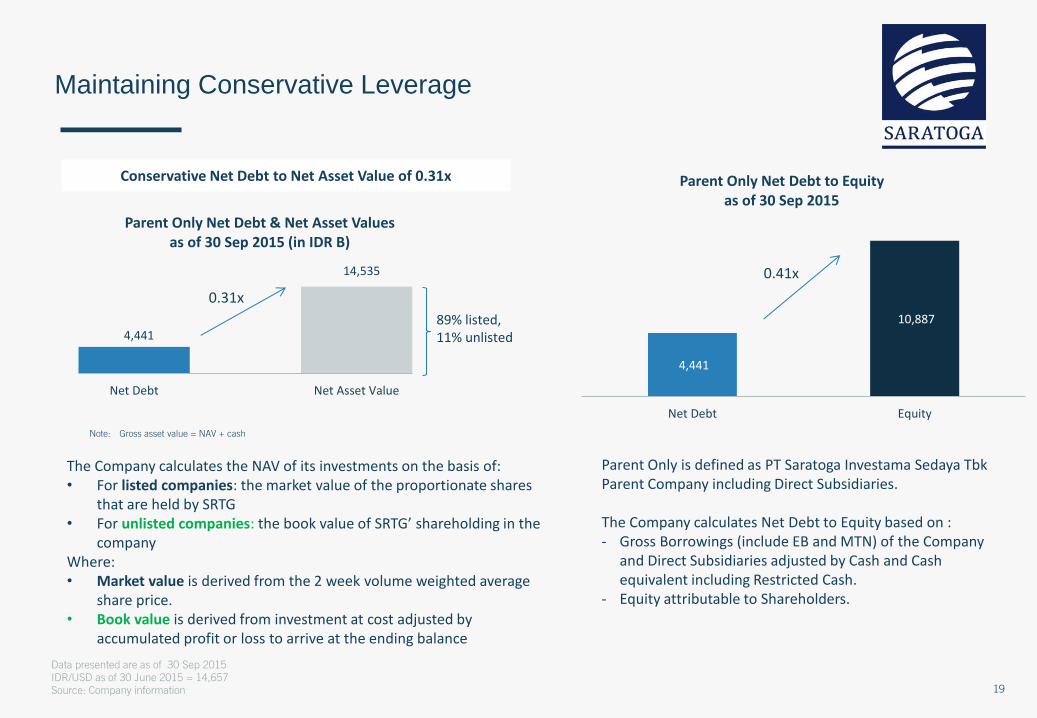

4,441

10,887

Net Debt Equity

Parent Only Net Debt to Equity as of 30 Sep 2015

Maintaining Conservative Leverage

The Company calculates the NAV of its investments on the basis of: • For listed companies: the market value of the proportionate shares

that are held by SRTG • For unlisted companies: the book value of SRTG’ shareholding in the

company Where: • Market value is derived from the 2 week volume weighted average

share price. • Book value is derived from investment at cost adjusted by

accumulated profit or loss to arrive at the ending balance

Conservative Net Debt to Net Asset Value of 0.31x

Note: Gross asset value = NAV + cash

89% listed, 11% unlisted

0.41x

4,441

14,535

Net Debt Net Asset Value

Parent Only Net Debt & Net Asset Values as of 30 Sep 2015 (in IDR B)

0.31x

Data presented are as of 30 Sep 2015

IDR/USD as of 30 June 2015 = 14,657

Source: Company information

Parent Only is defined as PT Saratoga Investama Sedaya Tbk Parent Company including Direct Subsidiaries. The Company calculates Net Debt to Equity based on : - Gross Borrowings (include EB and MTN) of the Company

and Direct Subsidiaries adjusted by Cash and Cash equivalent including Restricted Cash.

- Equity attributable to Shareholders.

20

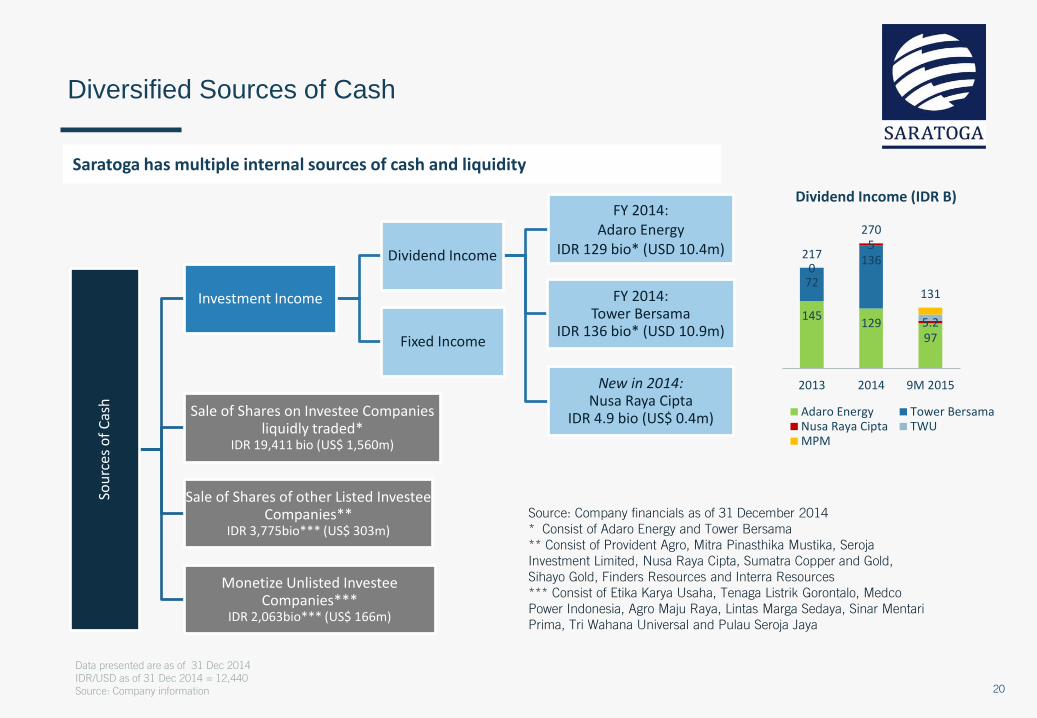

Sou

rces

of

Cas

h

Investment Income

Dividend Income

FY 2014: Adaro Energy

IDR 129 bio* (USD 10.4m)

FY 2014: Tower Bersama

IDR 136 bio* (USD 10.9m)

New in 2014: Nusa Raya Cipta

IDR 4.9 bio (US$ 0.4m)

Fixed Income

Sale of Shares on Investee Companies liquidly traded*

IDR 19,411 bio (US$ 1,560m)

Sale of Shares of other Listed Investee Companies**

IDR 3,775bio*** (US$ 303m)

Monetize Unlisted Investee Companies***

IDR 2,063bio*** (US$ 166m)

Diversified Sources of Cash

Saratoga has multiple internal sources of cash and liquidity

Source: Company financials as of 31 December 2014

* Consist of Adaro Energy and Tower Bersama

** Consist of Provident Agro, Mitra Pinasthika Mustika, Seroja

Investment Limited, Nusa Raya Cipta, Sumatra Copper and Gold,

Sihayo Gold, Finders Resources and Interra Resources

*** Consist of Etika Karya Usaha, Tenaga Listrik Gorontalo, Medco

Power Indonesia, Agro Maju Raya, Lintas Marga Sedaya, Sinar Mentari

Prima, Tri Wahana Universal and Pulau Seroja Jaya

Data presented are as of 31 Dec 2014

IDR/USD as of 31 Dec 2014 = 12,440

Source: Company information

97 129

145

136

72

5.2

5

0

131

270

217

9M 201520142013

Dividend Income (IDR B)

Adaro Energy Tower BersamaNusa Raya Cipta TWUMPM

21

KEY INVESTMENT HIGHLIGHTS

22

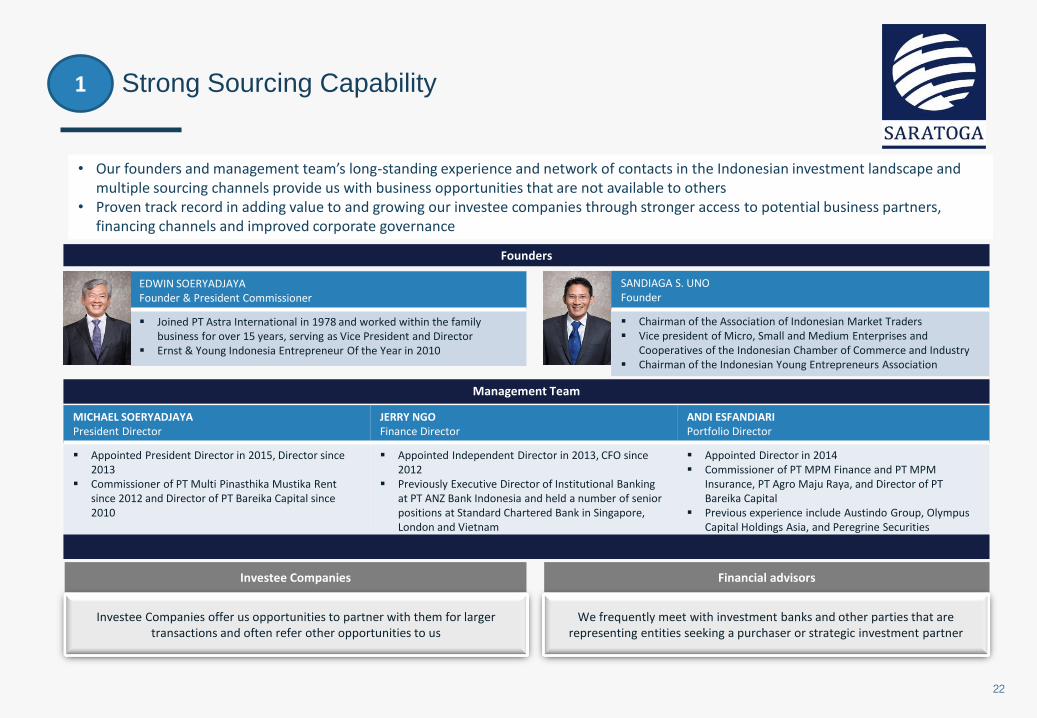

Strong Sourcing Capability

Founders

Management Team

• Our founders and management team’s long-standing experience and network of contacts in the Indonesian investment landscape and multiple sourcing channels provide us with business opportunities that are not available to others

• Proven track record in adding value to and growing our investee companies through stronger access to potential business partners, financing channels and improved corporate governance

EDWIN SOERYADJAYA Founder & President Commissioner

Joined PT Astra International in 1978 and worked within the family business for over 15 years, serving as Vice President and Director

Ernst & Young Indonesia Entrepreneur Of the Year in 2010

SANDIAGA S. UNO Founder

Chairman of the Association of Indonesian Market Traders Vice president of Micro, Small and Medium Enterprises and

Cooperatives of the Indonesian Chamber of Commerce and Industry Chairman of the Indonesian Young Entrepreneurs Association

MICHAEL SOERYADJAYA President Director

JERRY NGO Finance Director

ANDI ESFANDIARI Portfolio Director

Appointed President Director in 2015, Director since 2013

Commissioner of PT Multi Pinasthika Mustika Rent since 2012 and Director of PT Bareika Capital since 2010

Appointed Independent Director in 2013, CFO since 2012

Previously Executive Director of Institutional Banking at PT ANZ Bank Indonesia and held a number of senior positions at Standard Chartered Bank in Singapore, London and Vietnam

Appointed Director in 2014 Commissioner of PT MPM Finance and PT MPM

Insurance, PT Agro Maju Raya, and Director of PT Bareika Capital

Previous experience include Austindo Group, Olympus Capital Holdings Asia, and Peregrine Securities

Investee Companies Financial advisors

Investee Companies offer us opportunities to partner with them for larger transactions and often refer other opportunities to us

We frequently meet with investment banks and other parties that are representing entities seeking a purchaser or strategic investment partner

1

23

Together with our partners, we grow our businesses to lead in their respective industries

Growing through Partnership

“We sought for a partner whose business focus and principles

are aligned with ours and one that we can trust.

PT Saratoga Investama Sedaya fits the criteria perfectly and

seven years later, our partnership is stronger than ever. In

many ways, a business partnership is similar to a marriage,

and we have found our partner in Saratoga.”

* UEM is Saratoga’s partner in building the 116KM Cipali toll-road

Dato’ Izzadin Idris

Group Managing Director

CEO, UEM Group Berhad

2

24

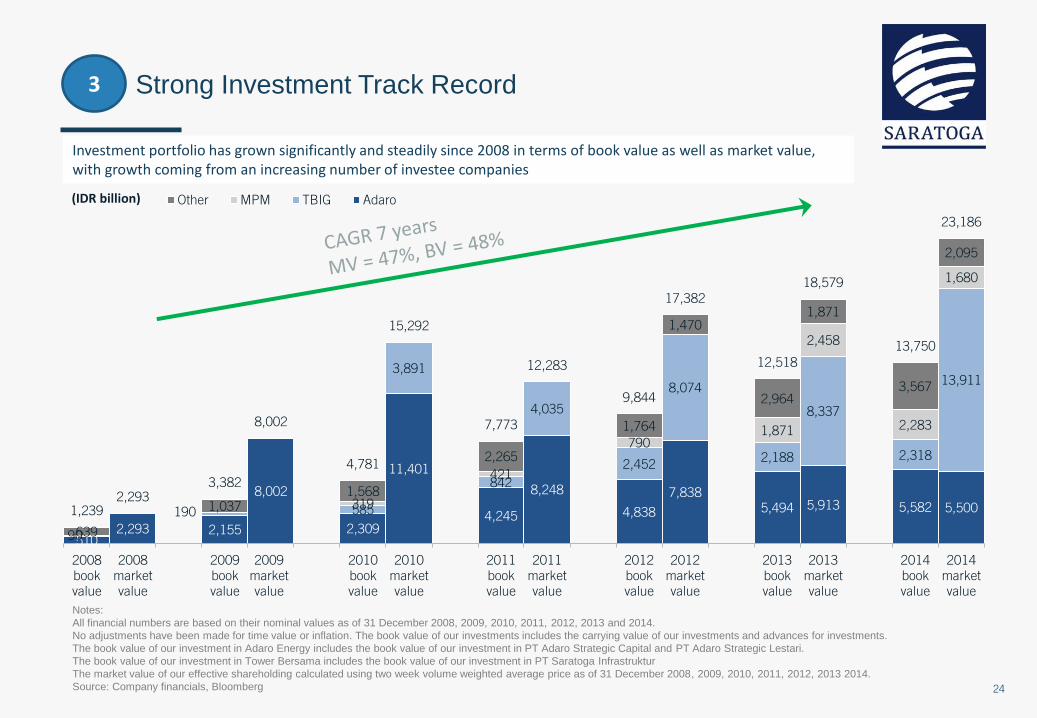

Strong Investment Track Record

510 2,293 2,155

8,002

2,309

11,401

4,245

8,248

4,838

7,838

5,494 5,913 5,582 5,500

90

190 585

3,891

842

4,035

2,452

8,074

2,188

8,337

2,318

13,911

319

421

790 1,871

2,458

2,283

1,680

639

1,037 1,568

2,265

1,764

1,470

2,964

1,871

3,567

2,095

1,239 2,293

3,382

8,002

4,781

15,292

7,773

12,283

9,844

17,382

12,518

18,579

13,750

23,186

2008

book

value

2008

market

value

2009

book

value

2009

market

value

2010

book

value

2010

market

value

2011

book

value

2011

market

value

2012

book

value

2012

market

value

2013

book

value

2013

market

value

2014

book

value

2014

market

value

(IDR billion) Other MPM TBIG Adaro

Investment portfolio has grown significantly and steadily since 2008 in terms of book value as well as market value, with growth coming from an increasing number of investee companies

Notes:

All financial numbers are based on their nominal values as of 31 December 2008, 2009, 2010, 2011, 2012, 2013 and 2014.

No adjustments have been made for time value or inflation. The book value of our investments includes the carrying value of our investments and advances for investments.

The book value of our investment in Adaro Energy includes the book value of our investment in PT Adaro Strategic Capital and PT Adaro Strategic Lestari.

The book value of our investment in Tower Bersama includes the book value of our investment in PT Saratoga Infrastruktur

The market value of our effective shareholding calculated using two week volume weighted average price as of 31 December 2008, 2009, 2010, 2011, 2012, 2013 2014.

Source: Company financials, Bloomberg

3

25

Sound investment strategy and corporate governance

framework

SIS is highly committed to ensuring that its investments satisfy its strict corporate governance framework and also cooperates with the International Finance Corporation to develop similar practices in investee companies

ENVIRONMENTAL

− Energy and water use

− Land clearance practices

− Emissions

− Levels of natural resources utilization

− Air and water pollution

− Waste management

− Activities in sensitive habitats

SOCIAL

− Local community relationships

− Minimum working age

− Minimum wage levels

− Health and safety record and procedures

− Union representation

− Security force usage

− Historical discrimination

− Relationships with NGOs

GOVERNANCE

− Anti-corruption policies

− Accounting and legal compliance

− Related party transactions

− Criminal conduct

− Pending or threatened litigation

− Historical transparency

INVESTMENT COMMITTEE

Provide independent recommendations on systems,

procedures and implementation thereof in areas related to

investment, capitalization of investment and divestments

activities, monitoring of investment performance and

active monitoring of investment risk profile

NOMINATION AND REMUNERATION COMMITTEE

Provide independent recommendations on the systems and

procedures related to succession programs and

identification of candidates for the Board of

Commissioners and Board of Directors

Provide independent recommendations on the

determination of remuneration of members of the Board of

Commissioners and Board of Directors

AUDIT COMMITTEE

Assist in implementing supervisory function, especially in

financial information management, effectiveness of

internal control systems, effectiveness of internal and

independent audit, implementation of risk management

and compliance with prevailing laws and regulations

INVESTMENT

CONSIDERATIONS

4

26

Summary

Saratoga, a partner for investors who wish to participate in the growth of early stage opportunities in Indonesia

PRUDENT APPROACH

PROVEN TRACK RECORD

• Proven track record of investment success in Indonesia

• Founders and management team’s long-standing experience and network of contacts in the investment landscape provide business opportunities that are not available to others

• Consistently adding value and growing our investee companies as evidenced in the completion of the Cipali toll-road project.

• Major portion of our investment portfolio consists of investments in the stable, established, blue chip companies

• Good Corporate Governance and Prudent Investment Process

• Conservative leverage and effective risk management

HIGH GROWTH POTENTIAL

• Focus on early stage, growth, and special situation opportunities with high growth potential. Our investments in Merdeka Copper Gold and Agra Energi Indonesia are cases in point.

• Continuously explore additional investments where Saratoga can add value

27

PT Saratoga Investama Sedaya Tbk. Correspondence Address:

Menara Karya 15th Floor

Jl. H.R. Rasuna Said Kav. 1-2

Jakarta 12950

For further information, please contact:

Leona Karnali: [email protected]

VI/2015/11