PT Indosat Tbk 1Q 2015 Results -...

29

PT Indosat Tbk 1Q 2015 Results

-

Upload

phungquynh -

Category

Documents

-

view

216 -

download

0

Transcript of PT Indosat Tbk 1Q 2015 Results -...

PT Indosat Tbk 1Q 2015 Results

2 Indosat Presentation 1Q 2015 Results

Agenda

Financial and Operational Highlights

Management Focus and Key Updates

Supplemental Information

3

Financial and Operational Highlights

4 Indosat Presentation 1Q 2015 Results

1Q15 QoQ Overview

Consolidated Revenue decreased 4.3% to IDR 6,093 billion

EBITDA increased 5.9% to IDR 2,604 billion, EBITDA Margin reached 42.7%

Loss Attributable to Owners of The Company decreased to a loss of IDR 456 billion

Free Cash Flow increased to IDR 481 billion

5 Indosat Presentation 1Q 2015 Results

1Q15 YoY Overview

Consolidated Revenue increased 5.5% to IDR 6,093 billion

EBITDA flat at IDR 2,604 billion, EBITDA Margin reached 42.7%

Profit Attributable to Owners of The Company decreased to a loss of IDR 456 billion

Free Cash Flow decreased to IDR 481 billion

6 Indosat Presentation 1Q 2015 Results

Financial Highlights

Operating Revenue

EBITDA

EBITDA Margin

Profit /Loss Attributable to Owners of the Company

6,093

1Q-14* 1Q-15 YoY

5.5%

2,604 -

42.7% -2.5ppt

-456 -157.2%

6,093

4Q-14 1Q-15 QoQ

-4.3%

2,604 5.9%

42.7% 4.1ppt

-456 31.4%

in IDR billion

• Network modernization completion leading to revenue growth YoY • EBITDA margin pressure due to higher operational costs from network expansion

5,773

2,607

45.2%

797

6,368

2,459

38.6%

-664

* Restated due to implementation of PSAK 24 (revised 2013)

7 Indosat Presentation 1Q 2015 Results

833 861 845 887 916 900

328 261 281 292 262 290

Segment Revenue Overview

Operating Revenue Breakdown

in IDR billion

3Q-14

-4.3% QoQ +5.5% YoY

4Q-14

5,840 5,773

2Q-14 1Q-14 4Q-13

Cellular

Fixed Data

Fixed Voice

+10.8% / +11.4%

-1.8% / +4.5%

-5.5% / +5.4%

• All revenue segments developing well in Q1 compared to same period last year

QoQ / YoY

6,056

4,895 4,714 4,651 4,925

6,104

1Q-15

5,190

6,368

4,903

6,093

8 Indosat Presentation 1Q 2015 Results

Cellular revenue performance

Voice

SMS

Data

VAS

-2.6%

1Q15 YoY

-3.3%

54.5%

28.6%

-5.0%

1Q15 QoQ

0.5%

0.6%

-4.0% Increase VAS usage from various gaming & content packages

Migration to data continues to impact voice and SMS usage and revenue

Increase data usage from attractive data offerings.

9 Indosat Presentation 1Q 2015 Results

59.6 59.7 54.9 54.2

63.2 66.5

Cellular customer base

4Q-14

+11.4% YoY +5.3% QoQ

3Q-14 2Q-14 1Q-14 4Q-13

Number of cellular customers

in million

4Q-14 3Q-14 2Q-14 1Q-14 4Q-13

in million

• Significant customer additions due to aggressive acquisition campaigns following improved network quality perception

5.8

0.1

-4.8

-0.7

9.0

3.3

1Q-15 1Q-15

Net cellular customers additions

10 Indosat Presentation 1Q 2015 Results

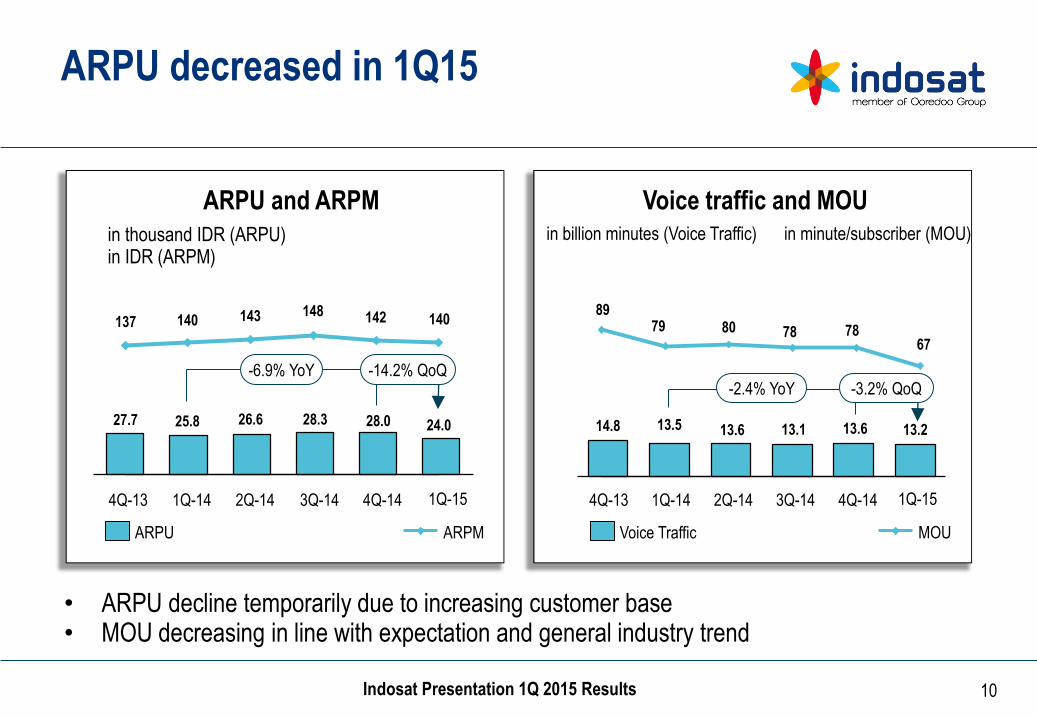

89 79 80 78 78

67

137 140 143 148 142 140

14.8 13.5 13.6 13.1 13.6 13.2

ARPU decreased in 1Q15

Voice traffic and MOU

-2.4% YoY

4Q-14

-3.2% QoQ

3Q-14 2Q-14 1Q-14 4Q-13

Voice Traffic

in billion minutes (Voice Traffic) in minute/subscriber (MOU)

MOU

• ARPU decline temporarily due to increasing customer base • MOU decreasing in line with expectation and general industry trend

ARPU and ARPM

27.7 25.8 26.6 28.3 28.0 24.0

3Q-14 2Q-14 1Q-14 4Q-13

-14.2% QoQ -6.9% YoY

4Q-14

ARPU

in thousand IDR (ARPU) in IDR (ARPM)

ARPM

1Q-15 1Q-15

11 Indosat Presentation 1Q 2015 Results

67 60 61

57 59 56

12,871 15,372

19,185 20,911

29,891

39,880

Strong data usage

Data usage

in TByte

+33.4% QoQ +159.4% YoY

4Q-14 3Q-14 2Q-14 1Q-14 4Q-13

SMS delivered

in billion

-6.4% YoY

4Q-14 3Q-14

-4.6% QoQ

2Q-14 1Q-14 4Q-13

• Number of data users growing, stimulated by improved network and customer experience and higher smartphone penetration

1Q-15 1Q-15

12 Indosat Presentation 1Q 2015 Results

Operational expenses

Cost of Service (CoS)

Depreciation and Amortization

Personnel

Marketing

as percentage of revenue

General and Administration

Total Expenses

• Network related expenses increasing with a wider modernized network • Moderate go to market expenses in Q1 vs. a traditional festive Q4 season

Total Operating Expenses

4Q-13

42.4%

38.9%

8.7%

4.0%

5.1%

99.1%

60.2%

1Q-14*

41.4%

34.4%

7.3%

2.8%

3.4%

89.3%

54.9%

2Q-14*

43.4%

33.6%

7.4%

3.6%

4.1%

115.5%

58.6%

3Q-14*

42.7%

33.4%

7.4%

4.9%

3.0%

91.4%

58.0%

Provision for IM2 Legal Case 23.3%

4Q-14*

45.2%

35.1%

6.9%

5.9%

3.8%

96.8%

61.7%

1Q-15

42.9%

33.9%

7.4%

3.0%

3.8%

91.2%

57.3%

* Restated due to implementation of PSAK 24 (revised 2013)

13 Indosat Presentation 1Q 2015 Results

2,410 2,607 2,425 2,569 2,459 2,604

EBITDA Performance

EBITDA and EBITDA margin

+5.9% QoQ -0.1% YoY

4Q-14 3Q-14 2Q-14 1Q-14* 4Q-13

EBITDA

in IDR billion

39.8%

EBITDA Margin

• 1Q15 EBITDA margin in line with guidance • Revenue development improving with

continued good cost management

45.1% 41.5% 42.1%

38.6% 42.7%

1Q-15

* Restated due to implementation of PSAK 24 (revised 2013)

14 Indosat Presentation 1Q 2015 Results

Normalized net loss bridge

-71

797

-456 -456

Normalized net profit

Net profit

-157.2% YoY +1219.9% YoY

1Q-15 1Q-14* 1Q-13

in IDR billion in IDR billion 1Q-15

• 1Q15 net loss impacted mainly by IDR depreciation

Normalized Net – FX Loss Reported

375

* Restated due to implementation of PSAK 24 (revised 2013)

-81

15 Indosat Presentation 1Q 2015 Results

2.31 2.58

2.72

25,042 27,174 27,398

2.05 2.25

2.38

22,226 23,649 23,924

Balance sheet

Gross debt* and gross debt/EBITDA Net debt* and net debt/EBITDA

1Q-14 1Q-13 1Q-15

+0.8% YoY

Gross Debt

in IDR billion

Gross Debt/EBITDA

1Q-15 1Q-13 1Q-14

+1.2% YoY

Net Debt Net Debt/EBITDA

in IDR billion

• Slight increase on debt level YoY due to Rupiah depreciation

* IDR 3.4tn, IDR 3.7tn and IDR 4.1tn of obligation under finance lease are included in 1Q13, 1Q14 and 1Q15 respectively

16 Indosat Presentation 1Q 2015 Results

24.0 27.5

28.6 25.7 25.4

23.1

1,452 1,590 1,669 1,566 1,618

1,409

Free Cash Flow & Capex

Free cash flow

in IDR billion

-1,045

1,319

876

356

-206

481

4Q-14 3Q-14 2Q-14 1Q-14 4Q-13

Capex and Capex/Revenue

4Q-14 3Q-14 2Q-14 1Q-14 4Q-13

Capex

in IDR billion

Capex/Revenue

• FCF strengthening with improved operating CF generation and moderating capex • Capex to revenue trend improving

1Q-15

1Q-15

17 Indosat Presentation 1Q 2015 Results

286 261 177

120 111 99

Network Development

Number of BTS

18,871 19,892 20,585 21,420 22,166 22,212

5,409 6,363 13,328

15,962 18,063 18,544

+1.3 QoQ +55.2% YoY

4Q-14 3Q-14 2Q-14 1Q-14 4Q-13

2G 3G

Cellular Revenue per BTS

In IDR million

1Q 2015 1Q 2014

XL

Indosat

Telkomsel

• Network modernization, phase 2 in Java, to be completed in Q3 2015 • Strong network performance in already modernized areas

24,280 26,255

33,913 37,382

1Q-15

40,229 40,756

18 Indosat Presentation 1Q 2015 Results

1Q in summary

Management Focus and Key Updates

20 Indosat Presentation 1Q 2015 Results

Develop adjacent and new businesses

Increase cost efficiencies enabling continued investments

Improve monetization on the strong growth of data users and increasing traffic

Leverage modernized network and improved customer experience driving revenue growth

Our Focus

LTE roll out to further enhance data experience

21 Indosat Presentation 1Q 2015 Results

2015 Guidance

FY 2014 Actual FY 2015 Guidance

Consolidated Revenue Growth 1.0% In line with market

EBITDA Margin* 41.7% Low to Mid 40’s

Cash CAPEX IDR 6.4 trillion IDR 6.5 - 7.5 trillion

* Restated due to implementation of PSAK 24 (revised 2013)

22 Indosat Presentation 1Q 2015 Results

Thank You

Any further questions?

Upcoming events AGMS 2015

Indosat Investor Relations Jl. Medan Merdeka Barat No. 21 Jakarta - 10110 Tel: +62 21 30442615 [email protected]

23 Indosat Presentation 1Q 2015 Results

Disclaimer

• PT Indosat Tbk ( “Indosat” or “Company” ) cautions investors that certain statements contained in this document state its management's intentions, hopes, beliefs, expectations, or predictions of the future are forward-looking statements

• The Company wishes to caution the reader that forward-looking statements are not historical facts and are only estimates or predictions. Actual results may differ materially from those projected as a result of risks and uncertainties including, but not limited to:

• The Company’s ability to manage domestic and international growth and maintain a high level of customer service

• Future sales growth

• Market acceptance of the Company’s product and service offerings

• The Company’s ability to secure adequate financing or equity capital to fund our operations

• Network expansion

• Performance of the Company’s network and equipment

• The Company’s ability to enter into strategic alliances or transactions

• Cooperation of incumbent local exchange carriers in provisioning lines and interconnecting our equipment

• Regulatory approval processes

• Changes in technology

• Price competition

• Other market conditions and associated risks

• The company undertakes no obligation to update publicly any forward-looking statements, whether as a result of future events, new information, or otherwise

• Please be also advised that the information provided herein are merely issued to coincide with the release of Ooredoo QSC (formerly known as Qatar Telecom QSC) results for the year ended 31 December 2013, as the Company’s indirect majority shareholder that consolidates Indosat’s results in its financial statements. Subject to the completion of, including but not limited to the audit by the Public Accountant Firm on the Company’s consolidated financial statements which are prepared in accordance with the Indonesian Financial Accounting Standards (IFAS), Indosat expects to file and release its consolidated financial statements for the year ended 31 December 2013 on 30 April 2014 at the latest (“Indosat’s Official Release”). Accordingly, the information provided herein may differ from what is contained in Indosat's Official Release.

Supplemental Information

26 Indosat Presentation 1Q 2015 Results

IM2 case development

On September 16, 2014, the South Jakarta Attorney Office (“Kejaksaan

Negeri Jakarta Selatan”), without preliminary notification, executed the

Supreme Court’s Decision on Mr. Indar Atmanto. The execution was done

based on a quotation of the Supreme Court’s Decision, which states, among

others, that (i) Mr. Indar Atmanto is found guilty and sentenced to eight

years imprisonment and charged with penalty of Rp300,000,000,- (if the

penalty is not paid, Mr. Indar Atmanto would serve an additional six months

imprisonment), and (ii) IM2 pay the losses sustained by the State amounting

to Rp1,358,343,346,674,-.

Subsequently, on January 16, 2015, Mr.Indar Atmanto and/or his lawyer or

IM2 received the document on the Supreme Court’s decision regarding the

litigation case. As of the issuance date of the consolidated financial

statements, Mr. Indar Atmanto and IM2 plan to conduct further legal act by

submitting a reconsideration request peninjauan kembali (”PK”).

On March 16, 2015, Mr. Indar Atmanto’s submission of judicial review

[Peninjauan Kembali (”PK”)] was officialy registered at the Corruption Court

under No. 08/AKTA.PID.SUS/PK/TPK/2015/PN.Jkt.Pst.

27 Indosat Presentation 1Q 2015 Results

Credit ratings improved Upgrade to AAA by Pefindo

On 7 January 2015, Standard and Poor’s (“S&P”) has affirmed its rating and outlook on Indosat (BB+/Stable/NR; axBBB+/--). The stable outlook reflects the outlook on the sovereign credit rating on Indonesia (BB+/Stable/B; axBBB+/axA-2). S&P expects Indosat's operating performance to remain stable over the next two years, given the company's focus on the data business. S&P assess Indosat's liquidity as "adequate" because the company's sources of liquidity are likely to cover its needs by more than 1.2x in the 12 months to Sept. 30, 2015.

On 3 February 2015, PEFINDO has affirmed “idAAA” rating of PT. Indosat Tbk’s Bond VI Year 2008 Seri B amounting to IDR320 billion that will mature on April 9, 2015. ISAT should be able to repay the maturing bond using its internal fund. At the end of 2014, it had cash and cash equivalent amounting to IDR3.5 trillion and unused credit facilities totalling almost IDR3.0 trillion.

On 1 April 2015, Moody's Investors Service says that PT Indosat Tbk's (Ba1 stable) overall FY2014

financial performance is in line with expectations, with an improved operating performance in the

second half of the year offsetting a weaker first half.

On 27 March 2015: Fitch Ratings has affirmed PT Indosat Tbk's (Indosat) Long-Term Foreign- and Local-Currency Issuer Default Ratings (IDR) at 'BBB'. The agency has also affirmed the Indonesia-based company's National Long-Term Rating at 'AAA(idn)'. The Outlook is Stable on the IDR and the National Long-Term Rating. Fitch has also affirmed the foreign-currency senior unsecured rating of 'BBB' and the National Long-Term Ratings on its IDR9trn bond programme and IDR1trn sukuk ijarah programme at 'AAA(idn)'.

28 Indosat Presentation 1Q 2015 Results

Debt maturity profile

Debt maturity profile*

In IDR trillion

2019 2018 2022 2017 2016 2015

IDR

USD in IDR

* Excluding obligation under capital lease

2021

9.13

1.47 0.52 0.26 0.26

1.92

1.97 2.78 0.50 2.27

0.36 1.50 0.36

2024

29 Indosat Presentation 1Q 2015 Results

Spectrum overview for top 4 cellular operators

10.0

900 Mhz

7.5

7.5

Indosat

Telkomsel

XL Axiata

20.0

1800 Mhz

22.5

22.5

10.0

2100 Mhz

15.0

15.0

in Mhz

Hutchison - 10.0 10.0

2.5

850 Mhz

3.5 – 5.0*

-

-

* Telkom and Bakrie Telekom have the same spectrum, differentiated by its operational areas

15.0**

2300 Mhz

15.0**

-

-

** Indosat/IM2: West Java exclude Bogor, Depok & Bekasi ; Telkom/Telkomsel: Maluku & North Maluku