PT Bank Danamon Indonesia, Tbk Full Year … market loan has grown by ... SME, retail banking, ......

36

Untuk Anda, Bisa Slide 1 PT Bank Danamon Indonesia, Tbk Full Year 2013 Financial Results Jakarta, 12 February 2014

Transcript of PT Bank Danamon Indonesia, Tbk Full Year … market loan has grown by ... SME, retail banking, ......

Untuk Anda, Bisa

Slide 1

PT Bank Danamon Indonesia, Tbk

Full Year 2013 Financial Results

Jakarta, 12 February 2014

Untuk Anda, Bisa

Slide 2

Agenda

• 2013 Achievement

• Macroeconomy

• Indonesia Banking Sector and Automotive Industry

• Appendix

Untuk Anda, Bisa

Slide 3

2013 Achievement

Conscious effort to bring down LDR to 95.1%.

LDR

CASA rose Rp 10 trillion or 23% from the previous year (CAGR 5yr of 22%). CASA to deposits composition stood at 48% (2012: 47%).

CASA

Non-mass market loan has grown by 30% YoY and contributed to 48% of total loan (2012: 43%). This is in line with the bank’s strategy to capitalise on the SME and Commercial segments.

Rp 65.4 trillion30% YoY

Non-mass market loan

In 2013 total loans was Rp 135 trillion, an increase of 16% from the previous year.

Rp 135 trillion↑↑↑↑16% YoY

Loan

Better asset quality management is indicated by a decrease in NPL to 1.9% (2012: 2.4%) and a decrease in CoC to 2.6% (2012: 2.8%).

NPL 1.9%CoC 2.6%

Asset Quality

Robust growth of trade finance. Cash loans and non-cash loans increased 45% and 76%, respectively.

Cash↑↑↑↑45% YoYNon-cash↑↑↑↑76% YoY

Trade Finance

CASA Ratio (%)

2640 48

2008 2010 2013

LDR (%)

95.1103.5 105.4 99

1Q13 2Q13 3Q13 4Q13

Untuk Anda, Bisa

Slide 4

Liquidity : LDR was lowered to 95%

IDR Cost of Funds (%), LDR (%)

95.1

99

105.4103.5

8.88.18.0 8.1

6.25.24.84.6

1Q13 2Q13 3Q13 4Q13

◄ LDR

◄ ADMF CoF

◄ IDR CASA, TD

CoF

IDR Yield (%), IDR Loans (Rp tn)

38%40%41%42%

62%60%59%58%

24.324.6

24.124.2

11.9 11.7 11.9 12.2

1Q13 2Q13 3Q13 4Q13

107.3 113.8 116.3 122.6

◄ Non Mass Mkt

+4w Yield

◄ Mass mkt

loans yield

NIM and Risk Adj NIM (%)

7.8 7.3 6.8 7.0

2.4 2.7 2.8 2.3

6.8

2.7

4Q12 1Q13 2Q13 3Q13 4Q13

Risk Adj NIM CoC

10.2 10.1 9.7 9.7 9.1• LDR was lower at the expense of NIM.

• Asset repricing for non mass-market loans was materialized in the second half of the year.

◄ Mass mkt

loans

◄ Non Mass Mkt

+4w loans

Untuk Anda, Bisa

Slide 5

Liquidity : Continue the use of borrowings and long

term funding for growth amid rising price of liquidity

• ADMF is financed through bonds and long term borrowing at fixed price to address interest rate risk and assets liability duration mismatch.

• Long term borrowing of subsidiaries and other liquid assets provided 34% LDR saving.

Capital

59%

LT

Fund.

1%

Bonds

40%

ADMF Source of Funds

Capital

21%

LT.

Fund.

39%

Bonds

40%

2010 2013

Rp 6.4 tn Rp 28.7 tn

LDR 2013 (%)

26.4 24.8

121.5

95.1 96.7

87.4

BDI Stand

Alone

BDI +

ADMF

Loans

LDR Consol Loan to

Funding

▲

ADMF

loans

LT. Fund

▼

ADMF - JF vs Self Finance (Rp tn)

78% 67% 49% 39%

22%33% 51% 61%

2010 2011 2012 2013

JF Self Fin

30.7

41.445.6

47.9

Untuk Anda, Bisa

Slide 6

CASA Journey : Continues effort to increase CASA

ratio from 26% to 48%

Customer Deposits (Rp tn)

26%41%

48%

52%

59%74%

2008 2011 2013

CASA TD

75.488.1

110.8CAGR CASA 5yr 22%

• CASA grew CAGR 22% driven by 4 champion products, enhancement of acquisition strategy, improving products and services as well as sales capacity.

Customers People & Infrastructure Product / Services

• Grow the customer base focusing on self employed and affluent segment

• Leverage Adira and DSP – 2 Adira branches and all DSP branches were upgraded to full service

• Roll out mobile apps and branchless banking, branch revamping

• 15 new privilege centers, 8 new mobile branches

• Improve skills and increase +/- 1,000 number of sales force to nearly 3,000 by end of 2013 from 2008.

• Financial Supply Chain to boost funding

• X-sell, new Bancassurance and CASA products

• Speed up process, reduce queuing time • Centralized complaint handling system

Untuk Anda, Bisa

Slide 7

CASA journey: Financial Supply Chain to boost funding

• Financial Supply Chain (FSC) is a joint program between SME, retail banking, ADMF and DSP to optimize funding

capacity targeting principal/anchors down to distributors

nationwide

• Today, Danamon involves anchors and distributors to support

this project.• Average growth per month of FSC funding is 5%

• 63% of FSC Funding is composed by CASA

FSC Funding Project (Rp bn)

693

572703

1,0541,024

668

656770

1,158 1,138

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13

O/S Ave. Bal

70%

CASA VC Project

(Rp mn)

474

4,621

Dec-12 Dec-13

O/S

No of Acct

191

482

Dec-12 Dec-13

152%

• CASA supply chain is one of Danamon’s

funding programs

specifically targeting

distributor, retailers,

students, individual/employees

particularly to boost

CASA in certain area.

• The major contributors for this project are SME

and Retail Banking.

Untuk Anda, Bisa

Slide 8

Loans grew 16% yoy. Non-mass market grew strongly.

57% 56% 54% 53% 52%

6% 6% 7% 6% 7%

26% 27%27% 27% 28%

11% 11%12%

13%14%

4Q12 1Q13 2Q13 3Q13 4Q13

Loan Composition Rp trillion

116 117124

129

Loan Growth

%

Rp billion 2012 2013 ����YoY

� Wholesale 12,663 18,828 49%

� SMEC* 30,544 37,606 23%

� Retail 7,115 8,988 26%

� Mass

Market66,063 69,961 6%

Total 116,385 135,383 16%

* SME and Commercial segments

135

Untuk Anda, Bisa

Slide 9

9.9

3.82.2 1.9

11.7

4.32.7 2.2

Java, Bali, Lampung,

NTT, NTB

Sumatra Kalimantan Sulawesi + E.Ind

2012 2013

SME Loans (Rp tn)

11.3

14.2

17.8

21

2010 2011 2012 2013

SME : Loan to SME shows a robust growth

Aver.loans size

Relationship officers

Loan disbursed(Rp tn)

1.38bn/cust.

1.61 bn/cust.

1.84 bn/cust.

2.10 bn/cust.

333 391 482 487

6.6 8.1 10.1 11.0

% to total loan

13.6% 14.0% 15.3% 15.5% BDI SME NPL

290292

189 242

1.41.41.32.6

2010 2011 2012 2013

Rp bn %

SME Loans by Region (Rp tn)

CAGR 23%

59,854 59,353 60,462 61,450# of Customers

2013201220112010

18%

13%24%

18%

Untuk Anda, Bisa

Slide 10

SME : Balancing strong loan growth and benign NPL,

enforcing funding capacity.

Customers People & Infrastructure Product / Services

• Target of 10% increase in number of

customers in 2014

• Utilize activity and promotional event to

gain volume & top up portfolio

• Customised approach and pricing

strategy for high end customer with

sensitive pricing

• Double marketing effort to create a

robust communication

• Expand of 100 new networks in 2014 (12

networks realised in Jan 2014)

• Increase head count for about 20%,

including +400 headcounts for the new SME

branches

• Increse people’s competence through

internal training and professional

certification

• Targets of 22% - 25% CAGR for total

lending and funding.

• Intensify Danamon Online Banking and

Cash@Work

• Building strengh through Financial Supply

Chain (FSC)

SME CASA (Rp tn)

5.5

3.4 3.8

4.9

2010 2011 2012 2013

CAGR 18%

Constr.

2% , 0.5%

Property

5% , 1.1%

Household

58% , 1.4%

Others

17% , 0.4%Trading

16% , 2.2%

Mining,

Quarrying

2% , 6.2%

2013 SME Loans by Industry (%), NPL (%)

Rp 20,971 bn

Untuk Anda, Bisa

Slide 11

Trade Finance : Robust growth above 30% per annum.

Cash Loans (Rp tn)

9.8

6.9

4.43.4

2010 2011 2012 2013

Non-cash Loans (Rp tn)

9.9

5.64.9

4.2

2010 2011 2012 2013

CAGR 43%

Customers People & Infrastructure Product / Services / Coverage

• Robust growth driven by Corporate and

Commercial segment, rose by 48% y-y

to Rp 4.3tn and 40% y-y to Rp 5.1tn

• Danamon is investing New Trade Finance

System (NTFS) to add more customer touch

point.

• More than 25 trade specialists

• Centralized Trade Operation, enabling

Danamon to process and serve efficiently

• Generic, Structured, Commodity Financing

& Syariah (e.g. L/C, trust receipt, guarantee,

outgoing collection service, outgoing

collection financing)

• Trade Service Point at Port (TSPP) in

Jakarta, Medan and Surabaya for Import

Tax Payment and B/L endorsement

• Trade representatives in 14 big cities in

Java, Sumatra, Kalimantan, Sulawesi.

CAGR 34%

Best Trade Finance bank in Indonesia by Exporta

2011, 2012, 2013

Best Local Trade Bank2009

by Euromoney

The Best Trade Bank 2007 - 2009

by FinanceAsia

The Best Trade Bank In Indonesia 2006by Asiamoney

The Best Trade Bank2005 - 2012

Best Local Cash Management Bank in Indonesia by Asiamoney

2009 - 2011

Untuk Anda, Bisa

Slide 12

Corporate and Commercial Funding

(Rp tn)

32.3

17.920.3

24.3

2010 2011 2012 2013

Corporate and Commercial : Ample growth with

preserved asset quality accounted for 26% of loan book.

Corporate NPL

18.8

10.712.5 12.7

1.13.83.43.9

2010 2011 2012 2013

Rp bn %

Commercial NPL

16.6

8.410.0

12.7

0.31.63.35.2

2010 2011 2012 2013

Rp bn %

Others

, 77%

Corp,

Comm.

, 23%

Others

, 74%

Corp.,

Comm.

, 26%

2010 2013

Corporate and Commercial Lending

Portion

CAGR 22%

CAGR 26%CAGR 21%

Untuk Anda, Bisa

Slide 13

ADMF Loans (Rp tn)

47.9

30.541.1

45.2

2010 2011 2012 2013

ADMF : 2W share shift compensated by 4W. Healthy

growth in second semester.

35% of total loans

37% of total loans

18% of tot. pf. / 52% of ADMF

25% of tot. pf / 68% of ADMF

17% of tot. pf / 49% of ADMF

13% of tot. pf / 35% of ADMF

CAGR 16%

CAGR 6%

2W Unit Sales and ADMF Mkt Shr

7,7717,373 8,0447,064

12.615.715.815.7

2010 2011 2012 2013

Industry sales (000)

ADMF Mkt Shr (%)

4W Unit Sales and ADMF Mkt Shr

1,230765

8941,116

5.45.66.65.2

2010 2011 2012 2013

Industry sales (000)

ADMF Mkt Shr (%)

CAGR 31%

CAGR 2%CAGR 17%

2W Loans (Rp tn)

24.720.6

25.4 25.4

2010 2011 2012 2013

4W Loans (Rp tn)

23.6

10.516.4

20.3

2010 2011 2012 2013

Note: loans include acquisition cost, exclude interest receivables

Untuk Anda, Bisa

Slide 14

ADMF : Repo assets and loss on repo assets has been

manageable

0.53%0.47% 0.46%

0.40%

0.02% 0.03% 0.04% 0.02%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

2010 2011 2012 2013

All Stock >180 days

Repo Assets as % of Receivables (%)

• % Repo / ENR was

manageable at 0.4%

• Old Inventory (>180 days) was

kept at 0.02%

• LOR Rate relatively showed

manageable trend

26%

27%

27%

22%

0%

10%

20%

30%

40%

50%

20

10

20

11

20

12

20

13

%LOR

24%

Loss on Repo Assets – Average (%)

Customers People & Infrastructure Product / Services / Coverage

• Customer Satisfaction Program & Adira

Club Member

• Dealer and agent management to secure

repeat order, develop lower cost payment

point, offer a total dealer support system

to retain good dealers and increase sales

• Upgrade staffs’ skill to support total

dealer relationship, productivity

• Business Process Redesign to improve

operating efficiency

• Business Network Redesign to improve

the productivity of network.

• Product differentiation through cross-

selling/bundling with financial products.

Untuk Anda, Bisa

Slide 15

SEMM : Challenges in Java remain, asset quality at

manageable level. DSP Loans (Rp tn) and Gross NPL (%)

15.3 16.418.8 19.9

5.95.35.65.1

2010 2011 2012 2013

15% of total loans

19% of total loans

Loans by Region (Rp tn)

8.8

4.2 5.7

18.8

8.8

4.76.3

19.9

Java Sulawesi and

East

Sumatra Total

2012 2013

10%14%

-1%

• Strategic Business Alliance increased by

22%

• To increase funding by 24% to Rp 1.6tn

• Launched Bancassurance Primajaga

• Improved productivity at collection has

improved recovery by 36% in Q4-14

• Dedicated semi secured sales specialists

: 1,117 AOs to serve 1,217 units

Product / Services / Coverage / FundingCustomers People & Infrastructure

• Boost upper tier micro to reach Rp 1.3tn

from Rp 333b in 2013

• Increase agri by 30% to reach Rp 3.2tn

• Referral program through DSP prime

customers (3,000 referrors)

• Implementation of CPA (credit process

application) in all branches

• Mobile Collection

• Direct reporting of credit officers to Risk in

hub & spoke branches

• Implement Hub and Spoke models in

selected Java and Jakarta units

• In 2014 plan to merge 137 units , while

170 Pasar units in Java and Jakarta area

will be converted into functional office.

• Optimize capacity (10% reduction of non

performer)

• Competency building (increase

knowledge scoring target)

6%

Untuk Anda, Bisa

Slide 16

Adira Insurance : Strong growth of GWP and number

of active policy

Gross Written Premium (Rp bn)

1,792

1,085

1,4741,605

2010 2011 2012 2013

No of Active Policy (000)

7,623

4,680

5,660 5,799

2010 2011 2012 2013

% 2010 2011 2012 2013

RBC 401 337 234 205*

CIR 31 32 35 40

RoE 36 38 36 29

RoA 15 14 11 9

• GWP in 2013 was Rp1,792bn or increased by 12%YoY.

• No. of active policies was 7,6mn or increased by 31%YoY.

CAGR 18% CAGR 18%

* Lower RBC and RoA from 2011 to 2012 due to the implementation IFRS Insurance

Untuk Anda, Bisa

Slide 17

2013 GWP by Source of Business

Others

13%

Group

69%

Strategic

Ind

6%

Finance

Ind

12%

Adira Insurance : Leading Indicators

Customers People & Infrastructure Products / Services / Coverages

• Call center serves 24 hour and during

2013 receive 79thousands number of

calls

• Workshop partner as of 2013 was 428

workshops

• Health business supported by 619

Hospitals

• Supported by 1,078 employees in 53 outlets

by end of 2013

• In 2013 launched Travellin, medicillin &

autocillin mobile apps (blackberry & google

play)

• Health insurance includes hospitalization,

outpatient, dental & optical care.

• Travel insurance covers losses whilst

travelling abroad & locally, coverage include

PA, medical, travel delay, cancellation, loss

of baggage & others

2013 GWP by Class of Business

Auto

63%

Engineeri

ng

5%

Others

20%

HE

3%

Property

9%

660 (37%)Non MV

Rp bn

MV 1,133 (63%)Rp 1,792 bn568 (31%)Non Grp

Rp bn

Group 1,224 (69%)

Rp 1,792 bn

Untuk Anda, Bisa

Slide 18

Bancassurance excluding one time

fee (Rp bn)

171

104140 129

2010 2011 2012 2013

Cash Management (Rp bn)

253

192216 228

2010 2011 2012 2013

Fee Income : Non credit related fee rose 12% driven by

general insurance, cash management, and bancassurance.

Rp 1,536bn

Distribution of Fee Income

2013 (%)

Others

28%Gen ins

45%

Cash Mgt

16%

Bancas.

Excl one

time fees

11%

General Insurance (Rp bn)

687

504

618 664

2010 2011 2012 2013

Note : General insurance including investment fees

CAGR 10%

CAGR 18%

CAGR 11%

Untuk Anda, Bisa

Slide 19

BDI NPL (%)

2.4 1.9 1.42.2

6.4

0.92.0 2.0 2.0

3.0

8.0

1.0

Trading Household Property Agri Mining Construction

2012 2013

Asset Quality :BDI Loans by are dominated by trading

industry. NPL by economic sector remain benign.

BDI Loans by Industry (% of total loans)

3126.4

7 4.4 2.3 1.8

33.1

21

6.9 4.4 2.2 1.9

Trading Household Property Agri Mining Construction

2012 2013

Industry Loans by Industry (% of total loans)

18.2

29.8

5.6 5.1 3.7 3.8

19.6

28.1

5.9 5.3 3.8 3.7

Trading Household Property Agri Mining Construction

2012 2013

• Trading loans rose driven by Commercial and Corporate segment

Industry NPL (%)

2.91.6 1.6 1.8 1.3

3.92.6

1.6 1.9 1.6 1.5

3.8

Trading Household Property Agri Mining Construction

2012 2013

• NPL in mining industry was driven by Corporate segment.

Untuk Anda, Bisa

Slide 20

Highlights of Balance Sheet

Rp billion 2012 2013 ����YoY 1Q13 2Q13 3Q13 4Q13

Total Assets 155,791 184,237 18% 153,785 158,103 173,094 184,237

Loans (gross) 116,385 135,383 16% 117,484 123,935 129,065 135, 383

Government Bonds 4,063 5,598 38% 4,066 3,895 5,548 5,598

Total Deposits 115,926 139,858 21% 114,028 118,741 130,611 139,858

Current Account 15,854 21,132 33% 15,845 15,631 20,705 21,132

Savings 27,270 32,053 18% 25,940 25,991 26,494 32,053

Time Deposit 48,552 57,621 19% 47,205 51,316 55,123 57,621

Borrowings and LT.

Fundings24,252 29,052 20% 25,038 25,803 28,288 29,052

Equity 28,494 31,251 10% 29,504 29,234 30,228 31,251

Untuk Anda, Bisa

Slide 21

Highlights of Income Statement

Rp billion 2012 2013 ����YoY 1Q13 2Q13 3Q13 4Q13

Net Interest Income 12,922 13,531 5% 3,334 3,349 3,421 3,427

Non-Interest Income 4,433 4,929 11% 1,122 1,253 1,322 1,232

Operating Income 17,355 18,460 6% 4,456 4,602 4,743 4,659

Cost of Credit (2,984) (3,184) 7% (770) (828) (835) (751)

Risk Adjusted Op.

Income14,371 15,276 6% 3,686 3,774 3,908 3,908

Operating Expenses (8,809) (9,695) 10% (2,308) (2,391) (2,507) (2,489)

Net Profit after Tax 4,012 4,042 1% 1,005 980 1,022 1,035

Untuk Anda, Bisa

Slide 22

Key Ratios

149.1130.8119.4107.444.4149.1104.7Coverage (LLP/NPL) – Non Mass Mkt

% 2012 2013 ����YoY 1Q13 2Q13 3Q13 4Q13

Net Interest Margin 10.1 9.6 -0.5 10.1 9.7 9.7 9.1

Cost of Credit 2.8 2.6 -0.2 2.7 2.8 2.7 2.3

Cost / Income 50.8 52.5 1.7 51.8 52.0 52.8 53.4

ROAA 2.7 2.5 -0.2 2.7 2.5 2.5 2.3

ROAE 16.2 14.5 -1.7 14.4 14.2 14.8 14.7

Assets to Capital (x) 6.3 6.7 0.3 5.7 6.0 6.4 6.7

Stand Alone Loan to Funding * 89.2 86.6 -2.6 89.1 91.9 87.6 86.6

Consolidated Loan to Funding * 89.5 87.4 -1.7 89.4 91.1 88.4 87.4

Regulatory LDR 100.7 95.1 -5.6 103.5 105.4 99.0 95.1

Stand Alone CAR 18.4 17.5 -0.9 20.0 18.4 18.1 17.5

Consolidated CAR 18.9 17.9 -1.0 20.1 18.7 18.3 17.9

NPL – Gross 2.4 1.9 -0.5 2.5 2.4 2.2 1.9

Impairment (LLP/Total Loans) 2.6 2.4 -0.2 2.6 2.6 2.6 2.4

Coverage (LLP/NPL) – Mass Mkt 117.1 121.0 3.9 112.7 112.0 115.2 121.0

*) Loan to funding is defined as (Loans + Reserves with BI + Cash in Vault + HTM bonds) / (Third Party Deposits + net borrowing and Long term

funding + net capital)

Untuk Anda, Bisa

Slide 23

Opex Turnover(%)

6.06.06.06.4

2010 2011 2012 2013

Cost to Income Ratio (%)

52.550.851.649.7

2010 2011 2012 2013

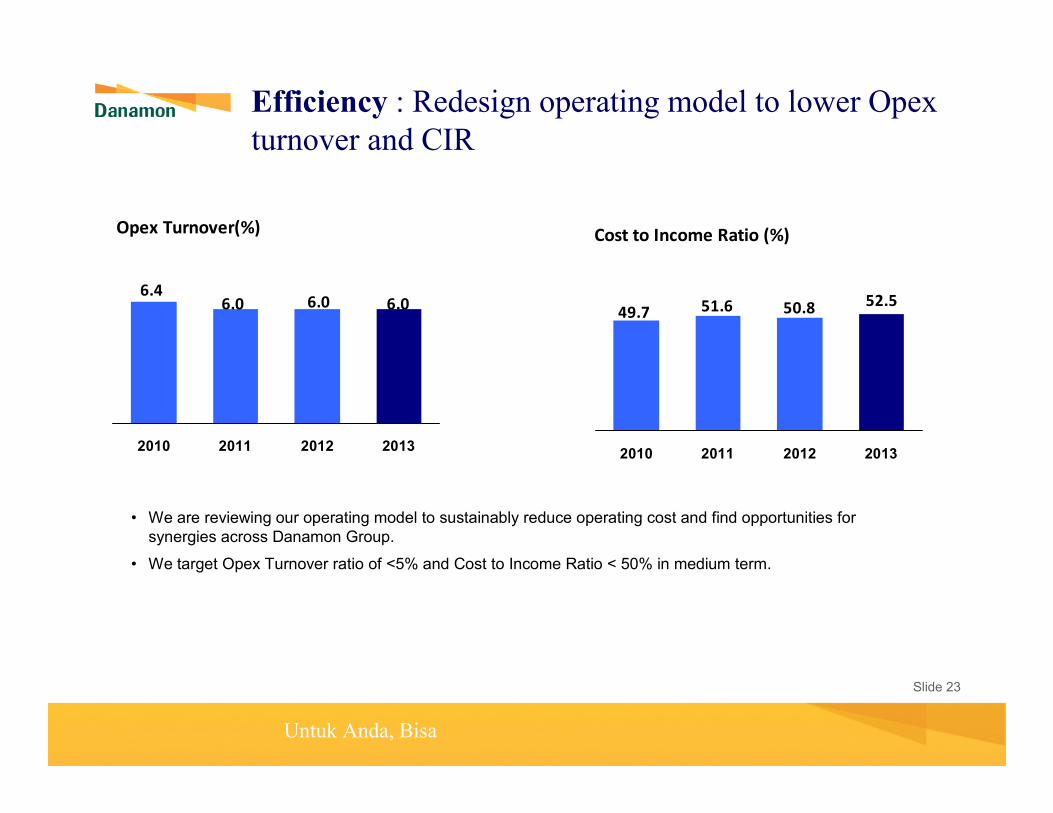

Efficiency : Redesign operating model to lower Opex

turnover and CIR

• We are reviewing our operating model to sustainably reduce operating cost and find opportunities for synergies across Danamon Group.

• We target Opex Turnover ratio of <5% and Cost to Income Ratio < 50% in medium term.

Untuk Anda, Bisa

Slide 24

Ample capitalization for growth

RWA / Total Assets Capital Adequacy Ratio (%)

% 4Q12 1Q13 2Q13 3Q13 4Q13

CAR w/ Credit

Risk23.4 25.6 23.5 22.8 22.0

Market Risk

Charge0.0 0.0 0.1 0.1 0.0

Operational

Risk Charge4.5 5.4 4.7 4.4 4.1

CAR

Consolidated18.9 20.1 18.7 18.3 17.9

18.318.920.1

18.717.9

18.4

20.0

17.518.118.4

4Q12 1Q13 2Q13 3Q13 4Q13

Consolidated Stand Alone

RWA BDI Only RWA Consolidated

18.4

19.6

18.217.8

17.3

0.5

0.5

0.50.5

0.6

4Q12 1Q13 2Q13 3Q13 4Q13

Tier 1 Capital Tier 2 Capital

Tier 1 and Tier 2 capital ratio (%) -

Consol

67%68%72%69%68%

4Q12 1Q13 2Q13 3Q13 4Q13

84%86%90%88%84%

4Q12 1Q13 2Q13 3Q13 4Q13

RWA Other Assets

18.9

20.1

18.718.3

17.9

Untuk Anda, Bisa

Slide 25

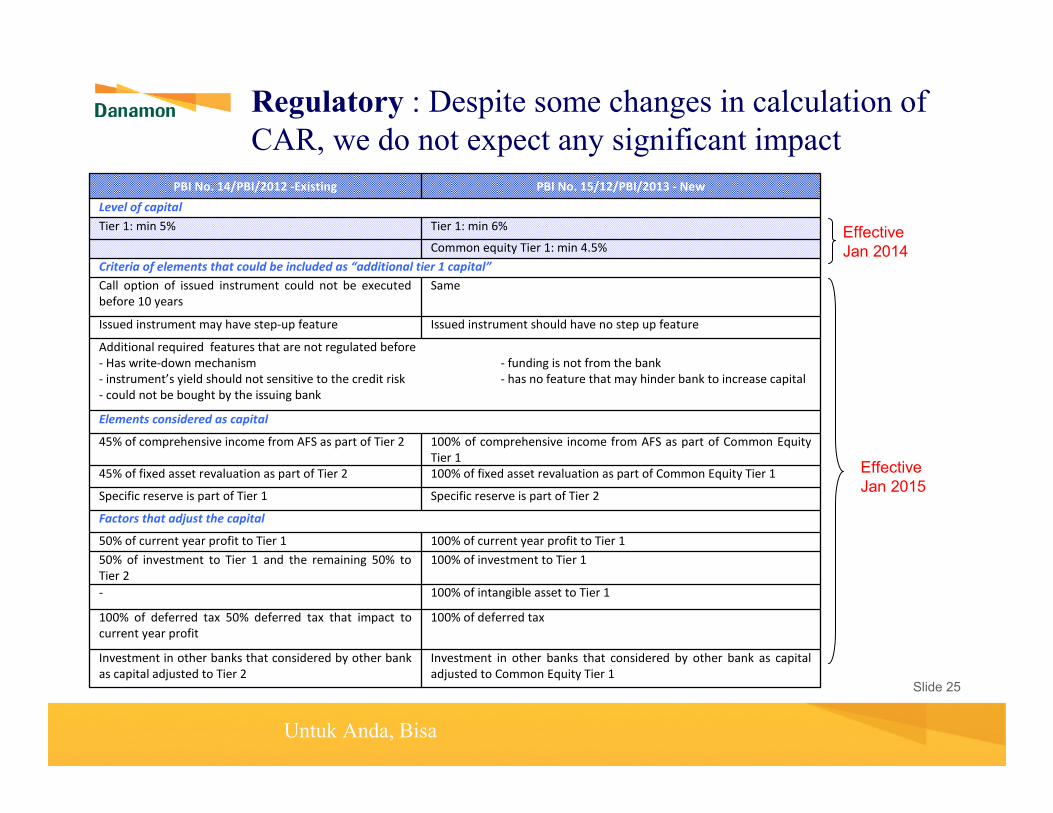

Regulatory : Despite some changes in calculation of

CAR, we do not expect any significant impact

Specific reserve is part of Tier 2Specific reserve is part of Tier 1

100% of fixed asset revaluation as part of Common Equity Tier 145% of fixed asset revaluation as part of Tier 2

100% of comprehensive income from AFS as part of Common Equity

Tier 1

45% of comprehensive income from AFS as part of Tier 2

Elements considered as capital

100% of deferred tax100% of deferred tax 50% deferred tax that impact to

current year profit

100% of intangible asset to Tier 1-

100% of investment to Tier 150% of investment to Tier 1 and the remaining 50% to

Tier 2

100% of current year profit to Tier 150% of current year profit to Tier 1

Factors that adjust the capital

Investment in other banks that considered by other bank as capital

adjusted to Common Equity Tier 1

Investment in other banks that considered by other bank

as capital adjusted to Tier 2

Issued instrument should have no step up featureIssued instrument may have step-up feature

SameCall option of issued instrument could not be executed

before 10 years

Criteria of elements that could be included as “additional tier 1 capital”

Additional required features that are not regulated before

- Has write-down mechanism - funding is not from the bank

- instrument’s yield should not sensitive to the credit risk - has no feature that may hinder bank to increase capital

- could not be bought by the issuing bank

Common equity Tier 1: min 4.5%

Tier 1: min 6%

PBI No. 15/12/PBI/2013 - New

Tier 1: min 5%

Level of capital

PBI No. 14/PBI/2012 -Existing

Effective Jan 2014

Effective Jan 2015

Untuk Anda, Bisa

Slide 26

Regulatory : We are ready for the additional buffer

required by BI

1 – 2.5%1 – 2.5%1 – 2.5%1 – 2.5%Surcharge D-SIB

0 – 2.5%0 – 2.5%0 – 2.5%0 – 2.5%Countercyclical Buffer

CAR Type 2013 2014 2015 2016 2017 2018 2019

Total minimum CAR still based on Risk Profile Risk Rating:

• Rating 1 : CAR min 8%

• Rating 2 : CAR min 9-<10%

• Rating 3 : CAR min 10-<11%

• Rating 4 & 5 : CAR min 11-<14%

No Change

Conservation Buffer 0.625% 1.25% 1.875% 2.5%

Untuk Anda, Bisa

Slide 27

Agenda

• 2013 Achievement

• Macroeconomy

• Indonesia Banking Sector and Automotive Industry

• Appendix

Untuk Anda, Bisa

Slide 28

Growth Outlook: Relatively stable in 2014

Economic Growth

• GDP growth in Q4 came out better than expected at (-1.42%qtq) 5.72%yoy. That led to a better full year 2013 growth at 5.78%yoy

• Private consumption still support growth as retail sales growth remained stable. Car sales and motorcycle sales was also seen stabilizing in Dec

• Investment was seen slowing down as affected from the policy rate hike

• This year, we expect the economy to grow relatively steady, and could grow by 5.73% yoy as impact of the interest rate hike will materialize, but may be cushioned by support from election spending.

Retail Sales

Growth Outlook

%yoy

Car & Motorcycle Sales

%

Jun-06 Sep-07 Dec-08 Mar-10 Jun-11 Sep-12 Dec-13

100

50

0

-50

-100

100

50

0

-50

-100

Motorcycle sales

(% y-o-y, rhs)

Car sales: GAI

(% y-o-y)

4.6 6.2 6.5 6.2 5.8 5.7 6.2

2.78

6.96

3.794.3

8.7

4.9

4.6

2009 2010 2011 2012 2013E 2014E 2015E

GDP Inflation (YE)%, yoy

Retail Sales

Q3-08 Q2-09 Q1-10 Q4-10 Q3-11 Q2-12 Q1-13 Q4-13

8

6

4

2

0

-2

40

30

20

10

0

-10

% y-o-yGDP growth

Consumption

Investment (RHS)

% y-o-y

Government (RHS)

Untuk Anda, Bisa

Slide 29

External Trade (BPS data)USD bn, %yoy

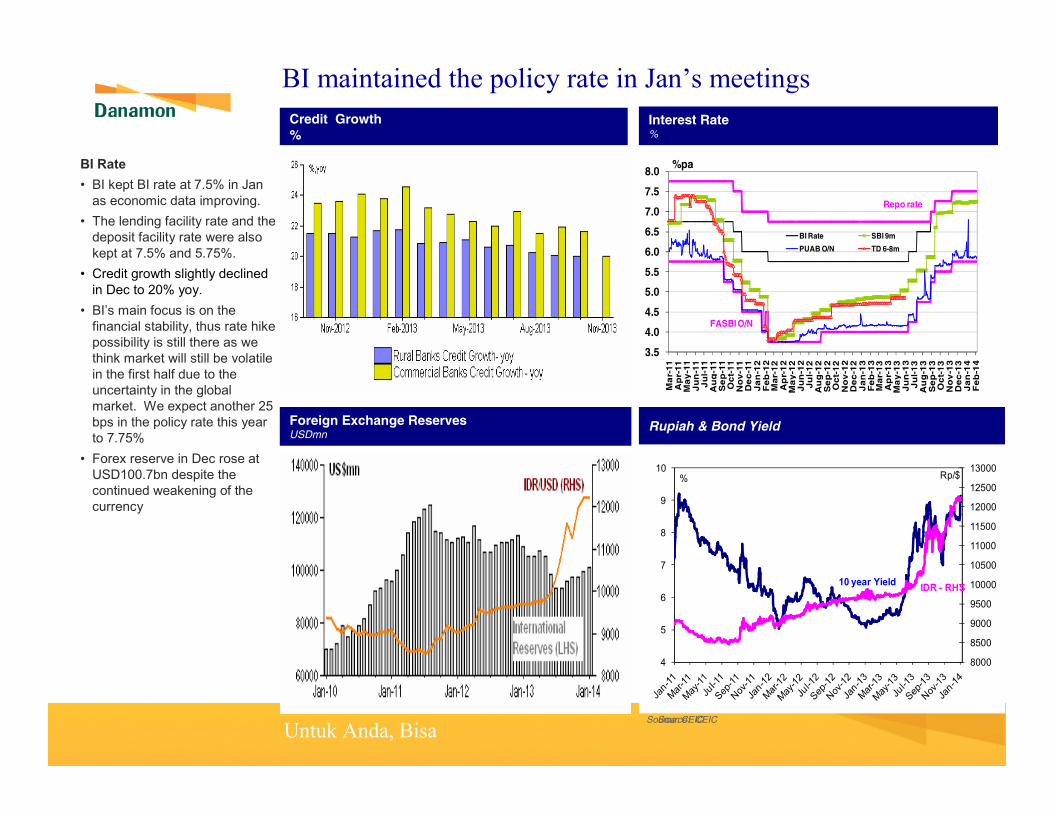

Positive result on inflation and trade data

Headline Vs. Core Inflation%yoy

Inflation

• Inflation rose to1.07%yoy (8.22%yoy) in Jan due to seasonally high food price and impact of LPG price hike, but the impact in some part was overshadowed by the implementation of the new base year 2012=100 (from previously 2007=100)

• We expect the YE inflation to be relatively low at 4.9%, though still noting some upside risk due to the potentially electricity rate hike for some of the industrial users.

External Trade & BoP

• We see a significantly wider surplus in the trade balance in Dec at USD1.5bn

• The surplus was driven by a jump in exports, though this may be caused by the front-running of raw mineral exports. Imports declined slightly .

BoP

• Expect the CA deficit to record

-3.53%of GDP in 2013. This year the CA deficit may improve to -2.9% of GDP.

Source: BI, CEIC

Balance of Payment (USD Mn)

Source: BPS, CEIC

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Current Account

Capital and Financial Account

Overall Balance

US$ Mn

-50

-35

-20

-5

10

25

40

55

70

85

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

010203040506070809101112010203040506070809101112 1 2 3 4 5 6 7 8 9 101112

2011 2012 2013

Trade Balance (lhs)

Export (fob)

Import (cif)

USD bn %YoY

Dec-10 Dec-11 Dec-12 Dec-13

9

8

7

6

5

4

3

Inflation

Headline (%yoy ) Core (%y oy )

Balance of Payment (USD Mn)

Untuk Anda, Bisa

Slide 30

BI maintained the policy rate in Jan’s meetings

Interest Rate%

Source: CEIC

Foreign Exchange ReservesUSDmn

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Mar-11

Apr-11

May-11

Jun-11

Jul-11

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-12

Feb-12

Mar-12

Apr-12

May-12

Jun-12

Jul-12

Aug-12

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

BI Rate SBI 9m

PUAB O/N TD 6-8m

%pa

FASBI O/N

Repo rate

Source: CEIC

Credit Growth

%

BI Rate

• BI kept BI rate at 7.5% in Jan as economic data improving.

• The lending facility rate and the deposit facility rate were also kept at 7.5% and 5.75%.

• Credit growth slightly declined in Dec to 20% yoy.

• BI’s main focus is on the financial stability, thus rate hike possibility is still there as we think market will still be volatile in the first half due to the uncertainty in the global market. We expect another 25 bps in the policy rate this year to 7.75%

• Forex reserve in Dec rose at USD100.7bn despite the continued weakening of the currency

Rupiah & Bond Yield

8000

8500

9000

9500

10000

10500

11000

11500

12000

12500

13000

4

5

6

7

8

9

10% Rp/$

IDR - RHS10 year Yield

Untuk Anda, Bisa

Slide 31

Agenda

• 2013 Achievement

• Macroeconomy

• Indonesia Banking Sector and Automotive Industry

• Appendix

Untuk Anda, Bisa

Slide 32

Banking and Automotive Industry

ADMF Monthly Market Share

FY13, market share mcy 12.6%; car 5.4%

Automotive Industry

2-Wheeler 8,018 7,047 7,769 10% -12%

4-Wheeler 894 1,116 1,227 10% 5%

FY13FY12YoY B/(W)

FY11Industry ADMF

Unit sales ('000)

Nov-12 Nov-13

Assets 3,653 4,103 4,263 4,818 17% 16% 3.7% 3.6%

Loans 2,200 2,631 2,708 3,214 22% 16% 4.3% 4.1%

Deposits 2,785 3,131 3,225 3,563 14% 16% 2.8% 2.8%

Current accounts 653 736 767 870 18% 28% 1.9% 2.1%

Savings 898 1,012 1,077 1,138 12% 12% 2.5% 2.5%

Time deposits 1,234 1,383 1,381 1,555 12% 14% 3.4% 3.5%

NPAT 75.1 84.9 92.8 98.5 16% 1% 4.2% 3.7%

NIM (%) 5.9 5.5 5.5 4.9 (0.6) (0.4)

LDR (%) 78.8 83.6 83.6 90.0 (6.4) 2.7

NPL (%) 2.2 2.0 1.9 1.9 0.1 0.3

CAR (%) 16.1 17.4 17.4 18.7 1.3 (0.6)

Number of offices 14,797 16,067 16,625 18,303 14% -6%

Dec-11Rp trillion Nov-12 Dec-12Market ShareYoY B/(W)

Industry BDINov-13

Untuk Anda, Bisa

Slide 33

Agenda

• 2013 Achievement

• Macroeconomy

• Indonesia Banking Sector and Automotive Industry

• Appendix

Untuk Anda, Bisa

Slide 34

Danamon Rating

Daily share price and trading volumeBDMN IJ

The ultimate shareholder of AFI is Temasek Holding Pte. Ltd, an

investment holding company based in Singapore.

Ownership Structure

As of 30 December 2013

Number of

Shares

Ownership (%)

Asia Financial (Indonesia) Pte, Ltd. 6,457,558,472 67.4%

JPMCB - Franklin Templeton Inv.

Funds

613,019,888 6.4%

Public < 5% 2,514,065,005 26.2%

Total 9,584,643,365 100.00%

Danamon

PEFINDO

August 2013

Outlook Stable

LT General Obligation idAA+

Standard &

Poor’s

December 2013

Outlook

LT Foreign Issuer Credit

ST Foreign Issuer Credit

Stable

BB

B

LT Local Issuer Credit

ST Local Issuer Credit

BB

B

Fitch’s

August 2013

Outlook

LT Issuer Default Rating

ST Issuer Default Rating

Individual Rating

Support Rating

Viability

Stable

BB+

B

WD

3

bb+

National Long Term AA+ (idn)

Moody’s

October 2013

Outlook

Long Term Rating

Foreicn LT Bank Deposits

Local LT Bank Deposits

Bank Financial Strength

Foreign Currency ST Dept

Local Currency ST Debt

Stable

Baa3

Baa3

Baa3

D

P-3

P-3

0

10,000

20,000

30,000

40,000

50,000

60,000

Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

0

2,500

5,000

7,500Volume('000)Share Price

Untuk Anda, Bisa

Slide 35

Reconciliation with Newsletter

a b c d e f g h i

Net Interest

Income

Net Under-

writing

Income

Net Sharia

Interest

Income

Other

Operating

Income

Other

Operating

Expenses

Non Operating

Income

Non

Operating

Loss

Income

before Tax Taxes

Minority

Interest Income after Minority Interest

13,600 487 121 8,947 (17,550) - (75) 5,530 (1,371) (118) 4,042

a+c b+d e f+g h i

Net Interest

Income

Non-

Interest

Income

Operating

Income

Operating

Expenses

Pre-

Provision

Operating

Profit Cost of Credit

Non

Operating

Income/

(Loss) Taxes

Minority

Interest

Net Profit

after Tax

and

Minority

Interest Remark

13,720 9,435 23,155 (17,550) 5,605 - (75) (1,371) (118) 4,042

(189) (189) 189 - - LPS Deposit Insurance

- - (3) 3 - Loss on reposess assets

(27) (27) (27) 27 - Provision for ADMF acquisition cost

(139) (139) (139) 139 - Write off on amortization cost

(177) (177) 177 - - ADMF indirect acquisition cost

(3,777) (3,777) 3,777 - - Decrease in fair value of financial assets (MTM)

(9) (9) 9 - - Losses from sale of financial assets (marketable securities)

(6) (6) 6 - - - Losses from spot and derivative transaction (realised)

- 3,347 3,347 (3,347) - Impairment losses on financial assets

(354) (354) 354 - - Fees/commissions and administrative expenses

- 1 1 (1) - Allowance for possible losses on non earning assets

(16) (16) (4) (21) 21 - Others

13,531 4,929 18,460 (9,695) 8,766 (3,184) (52) (1,371) (118) 4,042

Newsletter

Analyst Briefing Presentation

Untuk Anda, Bisa

Slide 36

Thank You

Investor RelationsPT Bank Danamon Indonesia, TbkMenara Bank Danamon, 6th Floor

Jl. Prof. Dr. Satrio Kav. E4 No.6

Mega Kuningan, Jakarta 12950

Phone: +62 21 5799 1001-03Fax: +62 21 5799 1445

Email: [email protected]

IR Contacts:

Kienata – [email protected] Hermawan – [email protected]

Ridy Sudarma – [email protected]

Noorvia Kesuma – [email protected]

Disclaimer:This report has been prepared by PT Bank Danamon Indonesia Tbk independently and is circulated for the purpose of general information only. It is not intended to the specific person who may receive this report. The information in this report has been obtained from sources which we deem reliable. No warranty (expressed or implied) is made to the accuracy or completeness of the information. All opinions and estimates included in this report constitute our judgment as of this date and are subject to change without prior notice. We disclaim any responsibility or liability (expressed or implied) of PT Bank Danamon Indonesia Tbk and/or its affiliated companies and/or their respective employees and/or agents whatsoever and howsoever arising which may be brought against or suffered by any person as a result of acting in reliance upon the whole or any part of the contents of this report and neither PT Bank Danamon Indonesia Tbk and/or its affiliated companies and/or their respective employees and/or agents accepts liability for any errors, omissions or mis-statements, negligent or otherwise, in this report andany inaccuracy herein or omission here from which might otherwise arise.