PSA Presentation Security Industry Trends 2021

14

10/18/2021 1 Member of FINRA & SIPC PSA Presentation Security Industry Trends 2021 October 2021 Imperial Capital Brian W. Ruttenbur Managing Director Phone: (615) 293-8234 Email: [email protected] Imperial Capital Security Investor Conference Table of Contents 2 I. Introduction to Imperial Capital II. Security Industry Trends III. Systems Integration Landscape IV. COVID - What Has Changed? V. Activity by Well Funded Security Companies 1 2

Transcript of PSA Presentation Security Industry Trends 2021

10/18/2021

1

Member of FINRA & SIPC

PSA PresentationSecurity Industry Trends 2021

October 2021

Imperial Capital

Brian W. RuttenburManaging DirectorPhone: (615) 293-8234Email: [email protected]

Imperial Capital Security Investor Conference

Table of Contents

2

I. Introduction to Imperial Capital

II. Security Industry Trends

III. Systems Integration Landscape

IV. COVID - What Has Changed?

V. Activity by Well Funded Security Companies

1

2

10/18/2021

2

I. Introduction to Imperial Capital

Mr. Ruttenbur is a Managing Director in the Institutional Research Group. Mr. Ruttenbur has over 25 years of experience in investment and equity research and covers the Security Industry. He joined Imperial Capital in 2021. He was most recently a Director, Investment Banking at Drexel Hamilton where he successfully executed numerous transactions in both Defense and Cybersecurity sectors. His experience at Drexel Hamilton included Director of Equity Research, where he provided and published analysis on public companies in the Defense and Security space, as well as oversaw the Equity Research operations prior to transitioning to investment banking. Prior to Drexel Hamilton, Mr. Ruttenbur was Managing Director, Equity Research at BB&T Capital Market. As a research analyst, Mr. Ruttenbur is 2x ranked as a top analyst by the Wall Street Journal and 5x by Thomas Reuters for stock picking and earnings accuracy. Mr. Ruttenbur's experience includes firms CRT Sterne Agee Capital Group, Morgan Keegan, and SunTrust. Mr. Ruttenbur earned a BA from University of Tennessee and MAS from University of Montana and served as an officer in the USAF securing and transporting nuclear weapons.

Brian Ruttenbur, Managing Director

Security Industry Public Equities Research Coverage

4

Imperial Capital Security Companies Under Formal Research Coverage Imperial Capital Public Companies Monitored

3

4

10/18/2021

3

– Imperial Capital’s 18th Annual Security Conference is scheduled to take place on December 14 – 15, 2021 at the InterContinental New York Barclay

– Deepest Security coverage of any conference anywhere; from Technology to Services and Logical to Physical, crossing both Commercial-Industrial and Government markets including:

Access control

Alarm monitoring & home automation

Cloud Security and Privacy

Cyber Security & Intelligence

Critical Infrastructure

Risk Management & Safety

Drones & Counter UAS

Guard Services

Identity Solutions

Information Security

Surveillance Technology

Video & Analytics

Representative Security Investor Conference Presenting Companies

Imperial Capital Annual Security Conference

5

Representative Conference Industries

Conference Information

II. Security Industry Trends

5

6

10/18/2021

4

Public Company Multiple Expansion

Security Industry Market Returns

7

Dates EV/ EBITDA TTM Average EV/ Revenue TTM Average

2019 Year End 21.9x 3.0x

2020 Year End 33.3x 3.9x

2021 Q2 Close 28.5x 4.1x

-10%

0%

10%

20%

30%

40%

Imperial Capital Security Coverage Return vs. S&P 500 (SPX)

S&P (^SPX)

Imperial Capital Security Index

Sources: Bloomberg, CapIQ, and Imperial Capital, LLC.

Security Industry Capital Raises and Stock Based Compensation Trends

8

• In the last twelve months, over $10 billion was raised in Equity and Debt markets by the IC Security Co’s • Stock Based Comp. grew at a Compound Annual Growth Rate (CAGR) of ~47.4% from 2016-2020

Funding Type CompaniesCapital Raised

(TTM)

Equity Alarm, Identiv, Cognyte, Evolv, SnapOne, Latch,

SmartRent

$1.8 Billion

Debt Vivint, Evolv $1.2 Billion

Convertible Debt Alarm $0.5 Billion

Refinancing Vivint, Verisure $6.9 Billion

IC Security Coverage Capital Raising and Allocation

Security Industry Aggregate Stock Based Compensation

$7B

$10B

$22B

$17B

$33B

$B

$5B

$10B

$15B

$20B

$25B

$30B

$35B

2016 2017 2018 2019 2020

Sources: Bloomberg, CapIQ, and Imperial Capital, LLC.

7

8

10/18/2021

5

Trends Integrators Should Be Focused On

Six Major Trends for Integrators

Convergence1 Demand for Smart Home Devices2

9

Move To Touchless Security

Impact of Big Tech3 4 Permanent Change to the Office

5 Flow of Big Money Changing the Landscape6

Convergence of IoT, Home Automation, and Alarm Monitoring

Alarm Monitoring market operates under a long-established model where high-margin recurring revenue is used to subsidize initial costs

IoT and Home Automation markets are beginning to produce highly desired consumer products, but the lack of an integrated offering with a compelling service model limits recurring revenue potential

IoT and Home Automation can use Alarm Monitoring to provide a jumpstart to growth by piggybacking on its business model and can also offer its new, innovative devices as a breath of fresh air to the Security market

10

Alarm Monitoring is unlocking the IoT and Home Automation business

IoT – $7 billion

50 billion devices connected to the Internet means higher demand for products and services

Penetration of security devices is lower with an additional 60 million households interested in a security and / or Home Automation system

Producing consumer products that capture and analyze home data

Struggling to monetize innovative technology

Hard to capture recurring revenue

The way people are approaching home security systems is evolving with the growth of IoT. Alarm systems have been established in millions of homes and are at the forefront of connecting devices in the home

Established recurring revenue business model

New capabilities require upgraded features (interactive services) and better, newer connectivity (4G / 5G, IP)

Equipment in place to capture data

Limited ability to date to communicate and use data

The Home Automation market is expected to grow to over $60 billion by 2024

Home Automation's growth is inevitable with new technologies creating more demand, better functionality, and higher end-user satisfaction

Established market for convenience and control solutions

Desire to integrate entire home (including security)

Smart phone and app determines all aspects of life

Alarm Monitoring – $55 billion

Home Automation – $23 billionSource: Imperial Capital, LLC.

9

10

10/18/2021

6

Consumers require and prefer ease-of-use over technical innovation and have gravitated towards less complicated technologies (e.g., master controls of connected devices)

At the same time there are supply chain issues and inflation

Source: iControl.

65%Outdoor Lighting

72%Thermostat

65%Cameras

68%Master Remote

71%Doors

Demand for Smart Home DevicesMost Desired Consumer Smart Home Devices

11

After the acquisition in 2014, Google has struggled to grow their Nest product offerings

In 2020, Google discontinue Nest and made a $450 million investment in ADT

Amazon Google

Amazon expanded its product offering beyond the front door after its acquisition of Ring, making it a player in the entire smart home market

Amazon has been active with their M&A activity, acquiring Ring, Blink, and Eero as well as an investment in ecobee (smart thermostat)

Ring’s popularity continues to grow but has faced consistent security and privacy concerns of their products

Impact of Big Tech

12

Amazon/Ring and Google/Nest: Big Tech’s performance in the home security and automation market

Sources: Company Reports and Imperial Capital, LLC.

11

12

10/18/2021

7

Flow of Big Money Changing the Landscape

Recent Moves Could Change the Industry Landscape

Buying HHI from Spectrum Brands for $4.3 billion

(brands - Kwikset, Baldwin, Weiser, Pfister and National Hardware)

Entering a partnership with Google for ~$450 million

Buying LiftMaster garage-door openers for $5 billion

Public companies and SPACs chasing deals (Alarm.com $500mm Convert, Latch $460mm,

SmartRent +$500mm, PE active, Public Companies Active –Much more to come)

ADT

Assa Abloy Blackstone

Other Deals

Sources: Company Reports, Bloomberg, CapIQ, and Imperial Capital, LLC.

Permanent Change to Office Life

We Suspect COVID-19 Will Permanently Reduce the Investment into Commercial Offices

14

• According to a study by Mercer University, 70% of companies saying a blend of in-person and remote working will be the new normal

• 29% of employers will implement remote work 1 to 2 days a week, with 17% making the remote option the majority of days, as many as 3 to 4 days a week

Pre-COVID Post-COVID

13

14

10/18/2021

8

Move to Touchless and Frictionless Security Solutions

15

Pre-COVID

Post-COVID

Commercial SecurityResidential Security Event Security

Alarm.com Front Door Security Identiv Commercial Security Solutions Evolv Tech Metal Detector System

IC Security Coverage Raised Record Levels of Capital (last 18 Months)

16

*All Values in Billions

Public Security Companies Raised $10.4B in Capital in the last 18 Months

$7.4$1.2

$1.8

$0.5Refinancing

Equity

Debt

• Vivant raised $800m in senior notes at 5.75% due 2029

• Evolv Technologies raised $34.5m in debt

• Latch raised $470m in a SPAC (~32x EV/TTM Sales)

• SmartRent raised ~$500m in a SPAC

• Vivant extended $1.35 B of outstanding debts by 3.5 years in June, 2021 – saving $50m in interest expense

• REZI refinanced $0.95 B in Feb, 2021 – lowering interest expense

• Verisure refinanced 4.4 B euros of debt in January 2021

Convertible Notes• Alarm.com raised $500m in

convertible debt notes at 0% with 48% upside to current share prices

Sources: Company Reports, Bloomberg, CapIQ, and Imperial Capital, LLC.

15

16

10/18/2021

9

III. Systems Integration Landscape

Market Description

Sources: Imperial Capital

Super Regional Integrators

Regional Integrators

Global & National integrators have superior operating scale, but typically lack sufficient responsiveness to effectively

serve local / regional end-users

Systems Integration Market Structure

Global & National

Integrators

~3,000 small integrators

Limited number of mid-size players leaves a gap between national service providers and local operators

Super Regional integrators have good service in a region but can’t always handle national scale

Systems Integration Overview

18

Large, growing and highly fragmented market with one of the more active M&A segments of the security industry

17

18

10/18/2021

10

Sources: OMDIA

Overall Addressable Market($ in billions)

6.2%

Systems Integration Market

$77.0 $77.0 $81.9

$89.4 $96.7

$104.3

2019 2020 2021 2022 2023 2024

The addressable market for systems integration is presently ~$77 billion

The systems integration market is projected to grow at a 6.2% CAGR from $77 billion in 2020 to $104 billion in 2024

2020 saw very little growth due mostly in part to COVID-19 lockdowns

19

Systems Integration Market Update

Growth Drivers Emerging / Disruptive Technologies

Cloud-based managed services driving recurring revenues

Government spending on security projects

Global terrorism, active shooters, general unrest

Price rationalization (cameras, servers, cloud storage)

Convergence of point products into complete solutions

Increasing enterprise focus on workplace security and safety

Convergence of information and actionable intelligence

Better “command and control” software for Physical Security Information Management (“PSIM”)

Easier to install and deploy solutions from supplier, cutting install time and complexity, thus reducing the roll of the integrator

Intersection of security technology and business process optimization – video analytics

Cloud based technology

Challenges

Movement to SaaS based business models

More technologically sophisticated & integrated solutions

Cybersecurity

20

Fragmented Market Non-recurring Revenue

The market is dominated by several large players with economies of scale and national reach (e.g., Convergint, ADT, JCI, etc.). These companies have grown through a combination of organic growth and roll-up acquisitions

Increasing focus and attention for security integrators to create recurring revenue streams through managed services models

– Traditional integration model yields low margins and valuations

– Expanding SaaS offering and cloud offerings across access control (ACaaS), video surveillance as a service (VSaaS), remote video monitoring as a service (MVSaaS) and analytics

COVID Headwinds

Systems are increasingly being integrated with other IT infrastructure, such as HR, POS and building automation systems, which is driving more complex systems and opportunities for hosted / managed services

2020 was a tough year for security integrators with government mandated lockdowns and labor shortages

– Commercial sites began using work-from-home environment to update infrastructure with less employee/customer disruption

– Backlogs have grown, 2H-21 likely to show a strong continued rebound

Current Systems Integration Market

Systems Integration Market Future Outlook

19

20

10/18/2021

11

IV. COVID - What Has Changed?

COVID-19 Impact on Current Market Conditions

22

Good

Bad

• Security/Safety has been elevated as a priority in all areas of life

• Smart Automation has gotten better and widely acceptable

• Supply Chain Issues (Allegion lowered guidance 10/1/21)

• Product Shortages

Ugly

• Labor is a free agent

• Inflation

• Competition

Products

Labor

• Inflation – price increases are being implemented and passed along

• Supply Disruptions/Delays

• Competition (companies using their BS)

• Inflation

• COVID

• Hiring and Keeping the Best employees

Capital

• Access to Capital

• Cost of Capital - Inflation/Interest Rates

Key Concerns For IntegratorsThe Good, Bad, and Ugly

Changing Industry and Integrator Dynamics

21

22

10/18/2021

12

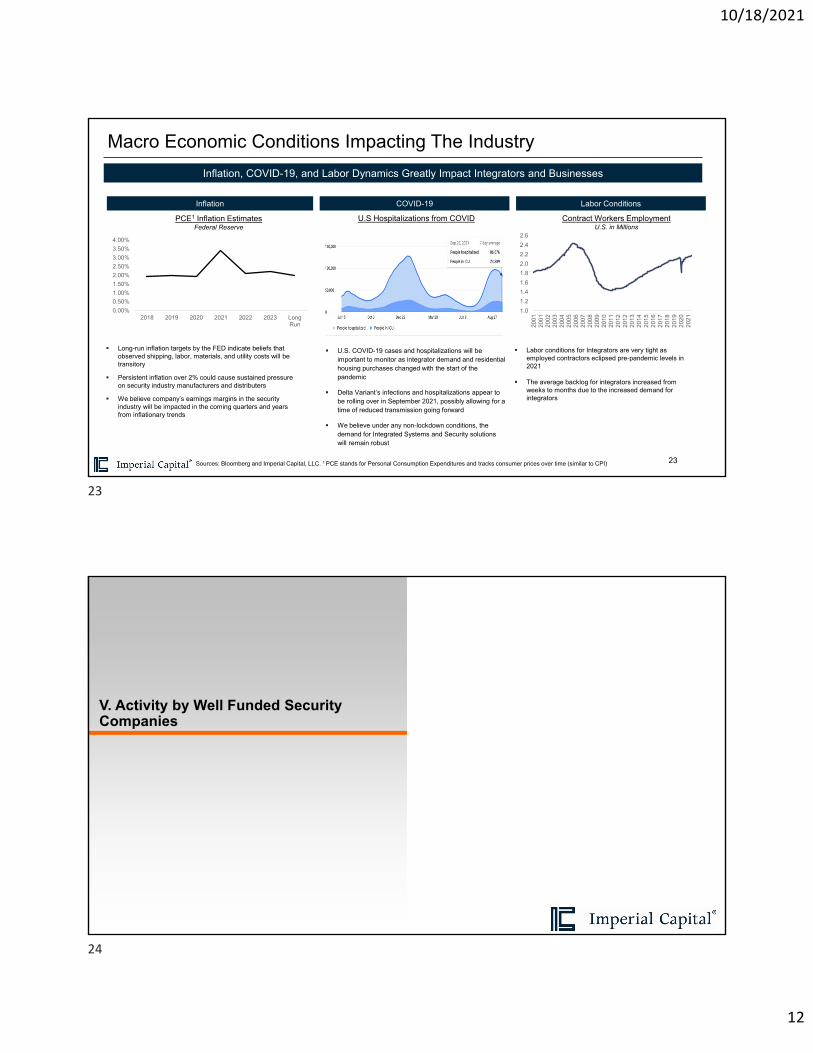

Macro Economic Conditions Impacting The Industry

23

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

2018 2019 2020 2021 2022 2023 LongRun

Inflation COVID-19 Labor Conditions

PCE1 Inflation Estimates Federal Reserve

U.S Hospitalizations from COVID Contract Workers Employment U.S. in Millions

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

200

12

001

200

22

003

200

42

005

200

62

007

200

82

009

201

02

011

201

22

012

201

32

014

201

52

016

201

72

018

201

92

020

202

1

Long-run inflation targets by the FED indicate beliefs that observed shipping, labor, materials, and utility costs will be transitory

Persistent inflation over 2% could cause sustained pressure on security industry manufacturers and distributers

We believe company’s earnings margins in the security industry will be impacted in the coming quarters and years from inflationary trends

U.S. COVID-19 cases and hospitalizations will be important to monitor as integrator demand and residential housing purchases changed with the start of the pandemic

Delta Variant’s infections and hospitalizations appear to be rolling over in September 2021, possibly allowing for a time of reduced transmission going forward

We believe under any non-lockdown conditions, the demand for Integrated Systems and Security solutions will remain robust

Labor conditions for Integrators are very tight as employed contractors eclipsed pre-pandemic levels in 2021

The average backlog for integrators increased from weeks to months due to the increased demand for integrators

Inflation, COVID-19, and Labor Dynamics Greatly Impact Integrators and Businesses

Sources: Bloomberg and Imperial Capital, LLC. 1 PCE stands for Personal Consumption Expenditures and tracks consumer prices over time (similar to CPI)

V. Activity by Well Funded Security Companies

23

24

10/18/2021

13

Historic Primary Market Activity in the Security Industry

25

33Total M&A Deals 1

Notable Movement Across the Industry

• ASSA Abloy is acquiring Spectrum Brands for $4.3 billion on September 8, 2021

• Blackstone acquisition of The Chamberlain Group which includes LiftMaster for $5 billion announced on September 2, 2021

Trailing Twelve Months Transactions

M&A Activity By Our Security Coverage and Tracked Companies (Refer to Page 4)

Sources: Company Reports, Bloomberg, CapIQ, and Imperial Capital, LLC. 1 Refer to page 4 of the companies' coverage and monitored by IC.

Historic High Multiples and Record High Rewards to Employees

26

33

Dates EV/ EBITDA TTM Average EV/ Revenue TTM Average

2019 Year End 21.9x 3.0x

2020 Year End 33.3x 3.9x

2021 Q2 Close 28.5x 4.1x

Public Company Multiple Expansion

$7B

$10B

$22B

$17B

$33B

$B

$5B

$10B

$15B

$20B

$25B

$30B

$35B

2016 2017 2018 2019 2020

Security Industry Aggregate Stock Based Compensation

Sources: Bloomberg, CapIQ, and Imperial Capital, LLC.

25

26

10/18/2021

14

Public Companies & PE Guidance For Capital Investments

27

Making technology add-ons ($600mm cash)

Under pressure to post Assa Abloy move – Just lowered guidance due to supply chain issues

$36mm in cash and wanting to make small acquisitions

$472mm Cash - Under pressure to acquire, potentially discounting solutions to gain revenue traction (at the expense of NT profits)

$36mm cash no Debt and $30-40mm of CF annually - wanting to acquire (Home Automation/ Access Control)

The move by Blackstone into the sector pushes other large PE players to follow suite.

~500mm Cash - Under pressure to acquire. Aggressively hiring sales/marketing teams

Trying to get to $1 billion in U.S. Revenue in the next 5 years from ~$100mm currently

Examples of Large Players Plans to Invest In the Industry

Sources: Company Reports, Bloomberg, CapIQ, and Imperial Capital, LLC.

27