Provisions of Tax Audit - Final 29.08.2016 BCAS (Uploading) · · 2017-10-17AY 1998-99 -Scope...

35

29‐08‐2016 1 Organised By TAXATION COMMITTEE of BOMBAY CHARTERED ACCOUNTANTS’ SOCIETY By PARESH H. CLERK BANSI S. MEHTA & CO. August 27, 2016 EVOLUTION APPLICABILITY PRESUMPTIVE TAXATION PENALTIES CEILING LIMITS REPORTING REQUIREMENTS DOCUMENTATION AND AUDIT PROCEDURES ERRORS IN TAX AUDIT REPORT August 27, 2016

Transcript of Provisions of Tax Audit - Final 29.08.2016 BCAS (Uploading) · · 2017-10-17AY 1998-99 -Scope...

29‐08‐2016

1

Organised

By

TAXATION COMMITTEEof

BOMBAY CHARTERED ACCOUNTANTS’ SOCIETY

By

PARESH H. CLERK

BANSI S. MEHTA & CO.

August 27, 2016

EVOLUTION

APPLICABILITY

PRESUMPTIVE TAXATION

PENALTIES

CEILING LIMITS

REPORTING REQUIREMENTS

DOCUMENTATION AND AUDIT PROCEDURES

ERRORS IN TAX AUDIT REPORTAugust 27, 2016

29‐08‐2016

2

Introduced by the Finance Act, 1984 Memorandum explaining the provisions of Finance Bill, 1984 -

“a proper audit for tax purposes would ensure that the books of account andother records are properly maintained….It can also facilitate theadministration of tax laws…..The time of assessing officers thus saved couldbe utilised for attending to more important investigational aspects of a case”

Sequence of Events…

AY 1984-85 - Introduction of Tax Audit Provisions AY 1998-99 - Scope enlarged for the business under presumptive

tax referred to in Sections 44AD / 44AE / 44AF AY 1999-00 - Form 3CC and 3CE eliminated

- Revision of Rule 6G of Income-Tax Rules, 1962- Revision of Forms 3CA, 3CB and 3CD

AY 2004-05 - Scope enlarged for the business under presumptive tax referred to in Section 44 BB /44 BBB

August 27, 2016

...Sequence of Events

AY 2004-05 - Revision of all Forms AY 2006-07 - Significant change in Form 3CD AY 2008-09 - Elimination of requirement to furnish report with

return AY 2013-14 - Mandatory E-filing of Tax Audit Report –

Mandatory Registration for CA signing the Report AY 2014-15 - Significant change in Form 3CD AY 2017-18 - Scope enlarged for the business under presumptive

tax referred to in Section 44 ADA

August 27, 2016

29‐08‐2016

3

APPLICABILITY

August 27, 2016

• Total sales, turnover or gross receiptsexceeds ` 1 croreBusiness

• Total gross receipts exceeds ` 25 lakh(From AY 2017-18 : exceeds ` 50 lakh) Profession

• Taxable income claimed to be lower thanthe deemed income under Sections44AD, 44ADA, 44AE, 44BB or 44BBB

Special Cases

Section 44AB - Applies to every person carrying on -

August 27, 2016

29‐08‐2016

4

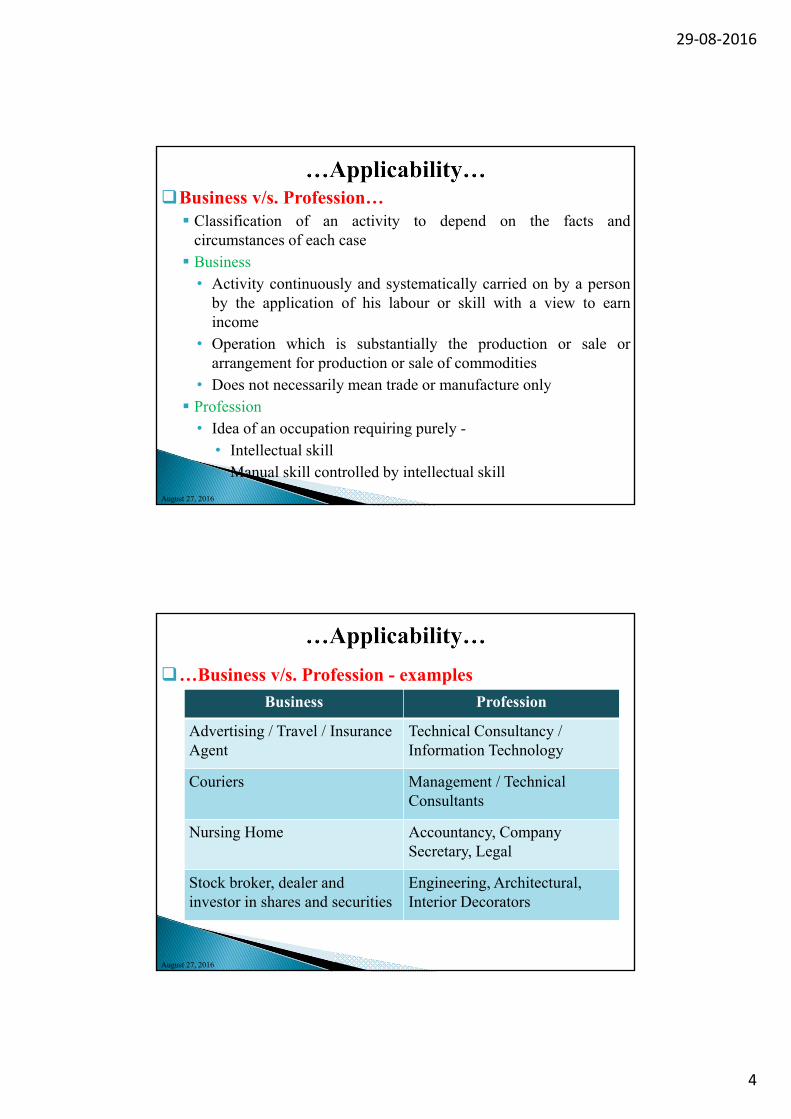

Business v/s. Profession… Classification of an activity to depend on the facts and

circumstances of each case Business• Activity continuously and systematically carried on by a person

by the application of his labour or skill with a view to earnincome

• Operation which is substantially the production or sale orarrangement for production or sale of commodities

• Does not necessarily mean trade or manufacture only Profession• Idea of an occupation requiring purely -• Intellectual skill• Manual skill controlled by intellectual skill

August 27, 2016

…Business v/s. Profession - examples

Business Profession

Advertising / Travel / Insurance Agent

Technical Consultancy / Information Technology

Couriers Management / Technical Consultants

Nursing Home Accountancy, CompanySecretary, Legal

Stock broker, dealer and investor in shares and securities

Engineering, Architectural, Interior Decorators

August 27, 2016

29‐08‐2016

5

Turnover… – Term not defined in the Act - Aggregate amountreceived or receivable for which sales are effected or services rendered

Included : Sale of scrap Sale proceeds of any shares, securities, debentures – held as stock-in-trade

Not included : Sale proceeds of fixed assets Sale proceeds of property Sale proceeds of any shares, securities, debentures – held as investments

Excise duty or sales tax recovered are credited in separate accounts andpayments to authority are debited to same account

Service tax - There is issue in uploading the return of income in marginalcases, if the tax audit limit is breached with the service tax amount ?

August 27, 2016

…Turnover To deduct from the turnover : Discount allowed Turnover discount Special rebate (if it is in the nature of trade discount)

Goods returned (even if returns are from the earlier years)

Not to deduct from the turnover : Cash Discount

Special rebate (if it is in the nature of commission on sales)

August 27, 2016

29‐08‐2016

6

Turnover… – Term not defined in the Act - All receipts in cash/kindarising from carrying on business/profession

Included : Advance received and forfeited from customers Liquidated Damages Hire charges of cold storage

Net surplus in case of reimbursements / Out of pocket expenses – if notspecifically collected

Cash assistance / Duty Drawback for exports Commission, brokerage

Exchange difference on export sales

August 27, 2016

…Turnover Not included : Rental income not assessable as business income Reimbursement of custom duty / other charges collected by a clearing

agent Sale proceeds of assets held as fixed assets / investments

August 27, 2016

29‐08‐2016

7

…Sales, Turnover or Gross Receipts… For Security / Derivative Transactions

• In case of a day trader / speculatoro Sum total of differences, whether positive or negative

• Security derivative transactionso Sum total of differences, whether positive or negative, also

premium on sale of options• Commodity derivative transactions

o In case of settlement without delivery, sum total ofdifferences, whether positive or negative

o In case of delivery, total value of sales

August 27, 2016

…Sales, Turnover or Gross Receipts… For Leasing transactions

• Value of lease rentals or interest on lease financing should beforming part of receipts for computation of limits

For Hire purchase transactions• The sale on hire purchase is completed when the borrower exercises his

option to purchase

• When the option is exercised, the price of the equipment sold will beconsidered as turnover

• During the hire purchase period, the hire charges received shall form partof gross receipts

• Installments towards principal repayment to be excluded

August 27, 2016

29‐08‐2016

8

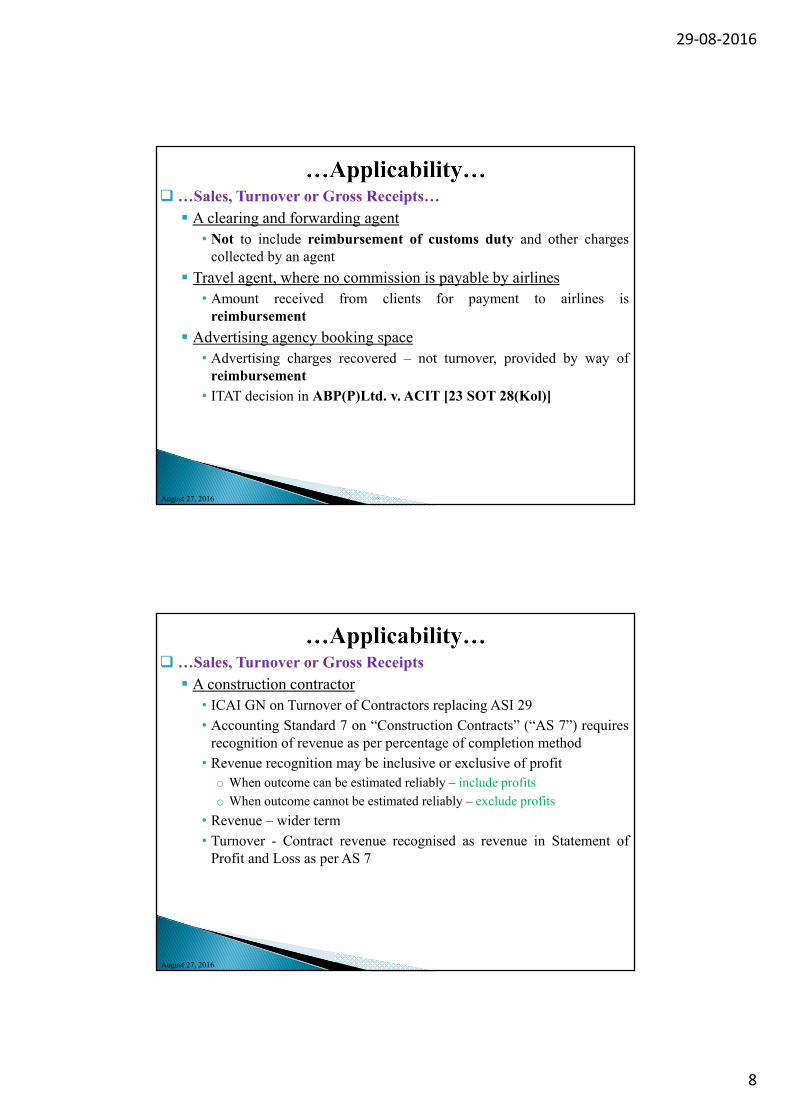

…Sales, Turnover or Gross Receipts… A clearing and forwarding agent

• Not to include reimbursement of customs duty and other chargescollected by an agent

Travel agent, where no commission is payable by airlines• Amount received from clients for payment to airlines is

reimbursement

Advertising agency booking space• Advertising charges recovered – not turnover, provided by way of

reimbursement• ITAT decision in ABP(P)Ltd. v. ACIT [23 SOT 28(Kol)]

August 27, 2016

…Sales, Turnover or Gross Receipts A construction contractor

• ICAI GN on Turnover of Contractors replacing ASI 29• Accounting Standard 7 on “Construction Contracts” (“AS 7”) requires

recognition of revenue as per percentage of completion method• Revenue recognition may be inclusive or exclusive of profit

o When outcome can be estimated reliably – include profits

o When outcome cannot be estimated reliably – exclude profits

• Revenue – wider term

• Turnover - Contract revenue recognised as revenue in Statement ofProfit and Loss as per AS 7

August 27, 2016

29‐08‐2016

9

In case of Charitable Trust : Required only if the trust carries on business Turnover exceeds ` 100 lakh Audit only of business carried on by trust – Not all activities Separate audit required under Sections 12A / 10(23C) for entire

trust, including business

August 27, 2016

Issues… Accounting year of assessee has changed from calendar year to FY.

The accounts have been drawn up from January, 2015 to March,2016 which are audited. Should separate accounts for PY beprepared ?Section 3 – “Previous Year” means FY immediately preceding

the AYTax Auditor to prepare a separate Statement of Profit and Loss

and Balance Sheet for period April 1, 2015 to March 31, 2016Accounts to be prepared on basis of financials audited by

Statutory AuditorsUse Form 3CB - As statutory audit is carried out with respect to

accounting year and not the relevant FY which is different fromthe accounting year, that is, for the PY which is not under anyother law

August 27, 2016

29‐08‐2016

10

… Issues… A foreign company has business income of ` 2 crore in India. It

does not have a permanent establishment in India. Whether thecompany is required to get its books audited under Section 44AB?

Para 6.3 of the GN – Section 44AB does not distinguishbetween a resident or a non-resident

Non-resident assessee is required to get his accounts audited andfurnish report under Section 44AB, if its turnover exceeds theprescribed limits

Since, the business income of non-resident exceeds limit of Rs. 1crore, provisions of Section 44AB to apply

August 27, 2016

…Issues… An assessee has 3 businesses. The turnover of business A, B and C

being ` 80 lakh, ` 70 lakh and ` 65 lakh, respectively. Separatebooks of account are maintained for all the businesses. Comment -• Will the tax audit under Section 44AB be applicable? Limits of sales / turnover / gross receipts for an assessee to be

calculated for all businesses carried on by him The aggregate turnover from all businesses exceeds the ` 1

crore limit, hence, tax audit applicable• Particulars of all businesses be reported in a single Form No.

3CD?... Two possibilities• Separate Tax Auditor appointed for individual businesses• One Tax Auditor for audit of all businesses

August 27, 2016

29‐08‐2016

11

…Issues… For AY 2016-17, an assessee is carrying on business as well as

engaged in profession. Total sales, turnover or gross receipts inbusiness are` 73 lakh (` 87 lakh) and receipts from the profession are ` 26lakh (` 22 lakh)

Whether the assessee is required to get his accounts audited ? Since professional receipts exceeds the prescribed limits, the

accounts of profession as well as business are required to beaudited

Since sales, turnover or gross receipts, as the case may be, arebelow the prescribed limits, no tax audit is applicable

August 27, 2016

…IssuesWhether following should be considered as a business or

profession–• A Chartered Accountant engaged in running coaching classes Possible view - Income from coaching classes run by a

Chartered Accountant is a return from professional activity Profession includes vocation and teaching is a vocation

• A software developer preparing and selling computer software tocompanies Preparing a software and selling the same to others is a

business activity Professional skills utilised for commercial purposes

August 27, 2016

29‐08‐2016

12

PRESUMPTIVE TAXATION

August 27, 2016

Profits and gains of eligible business of eligible assessee deemed to be 8%of : Total turnover, or

Higher income claimed to have been earned

Applicable to : Assessee, who is resident in India

• Individual, HUF and Partnership Firm but not Limited LiabilityPartnership (“LLP”) – Refer Explanation to Section 44AD

• Not claimed deductions under Sections 10A, 10AA, 10B, 10BA orPart C of Chapter VIA in relevant year

Not applicable to : Person carrying profession referred to in Section 44AA(1) Person earning / carrying commission or brokerage or agency business Those engaged in any business except plying, hiring or leasing goods

carriages referred to in Section 44AEAugust 27, 2016

29‐08‐2016

13

Eligibility Criteria : Total turnover or total gross receipts <= ` 1 Crore (the limit

increased to ` 2 Crore from AY 2017-18)• Refer CBDT Press Release dated June 20, 2016

Deeming provisions : No deduction under Sections 30 to 38Written Down Value (“WDV”) of assets deemed to be reworked

with depreciation allowance No deduction in case of the assessee firm for: Expenditure in the nature of salary, remuneration, interest

paid to partners as per Section 40(b) Till AY 2016-17 : If profits claimed to be lower than 8% and if the total income

exceeds basic exemption limit, books of account to be maintainedand tax audit applicable

August 27, 2016

From AY 2017-18 –

o Bar of 5 years…:

When assessee declares profit under the presumptive taxation for any year,and in any of 5 subsequent years, the assessee voluntarily does not offer hisincome to tax under Section 44AD, not eligible for the declaration underSection 44AD for subsequent 5 years

• Non-applicability of Section 44AD on account of turnover exceedingthreshold limit in any year – not to consider as default so as to excludethe assessee from benefit of presumptive taxation in later year, ifapplicable

• In any of the 5 subsequent years where Section 44AD is not applicable,assessee to maintain books of account and tax audit applicable

Issues• When should first year of declaration under Section 44AD be – only after

amendment or even before?

• How 5 years period to be computed – starting from each year, or as block?

• How should 5 years of exclusion be computed - Each year or block?August 27, 2016

29‐08‐2016

14

Explanatory Memorandum – …For example, an eligible assessee claims to be taxed an

presumptive basis under section 44AD for AY 2017-18 and offersincome of Rs. 8 lakh on the turnover of Rs. 1 crore

For AY 2018-19 and AY 2019-20 also he offers income inaccordance with the provisions of section 44AD. However, for AY2020-21, he offers income of Rs. 4 lakhs turnover of Rs. 1 crore. Inthis case since he has not offered income in accordance with theprovisions of section 44AD for five consecutive assessment years,after AY 2017-18, he will not be eligible to claim the benefit ofsection 44AD for next five assessment years i.e. from AY 2021-22 to2025-26

August 27, 2016

…From AY 2017-18 – Bar of 5 years – Illustration

Facility of advance tax payment in entirety before March 15 of therelevant FY instead of periodical installment payments Available – if not paid, levy of interest under Section 234B and 234C Till AY 2016-17, no interest under Sections 234B and 234C as no

advance tax payable

AY Situation 1 Situation 2

2017-18 Yes Yes

2018-19 Yes No

2019-20 No Yes

Presumptive taxation schemenot available for AYs

2020-21 to 2024-25 2019-20 to 2023-24

YesNo

Offers income under presumptive taxation schemeVoluntarily opts out of presumptive taxation scheme

August 27, 2016

29‐08‐2016

15

Applicable w.e.f. April 1, 2017 (for PY 2016-17) Applicable to : Assessee, who is resident in India

• Individual, HUF and Partnership Firm but not LLP – Refer Explanation toSection 44ADA

Engaged in profession as per Section 44AA(1)• Covers profession of law, medicine, engineering, architecture, accountancy

or technical consultancy or interior decoration or any other profession asnotified by CBDT

• Not to apply to services such as commission and brokerage activities ofinsurance agents and others, etc.

Eligibility Criteria : Total gross receipts <= ` 50 lakh

• Iswar’s Committee’s Recommendations - ` 1 Crore and 33.33 % of GrossReceipts

August 27, 2016

Income from profession presumed to be 50% of : Total gross receipts or

In case of higher income earned – such higher amount Deeming provisions : No deduction under Sections 30 to 38

WDV of assets deemed to be reworked with depreciation allowance –even unabsorbed depreciation to lapse

No specific provision for deduction in case of the assessee firm for: Expenditure in the nature of remuneration and interest paid to partners as

per Section 40(b)

Bar of 5 years No such concept – Option each year

Facility of advance tax payment in entirety before March 15 of the relevantFY instead of periodical installment payments

Not AvailableAugust 27, 2016

29‐08‐2016

16

Situations Firm Partner whose income is <= ` 50 lakh

Firm’s revenue > ` 50 lakh • Not eligible forpresumptive taxation

• Claim expenditure oninterest and remuneration

• Sections 44AA and 44ABapplicable

•To pay tax on interest andremuneration deducted byfirm•Not to consider share ofprofit as part of grossreceipt

Firm’s revenue <= ` 50lakh

• Presumptive taxation• No deduction for interest

and remuneration• No tax audit

• Fully exempt income –Share of Profit

• Not to consider this asseparate gross receipt

August 27, 2016

Section 44AA - Maintenance of books of account Non-applicability from maintaining books of account and tax audit, if the

assessee opts for presumptive taxation• No specific exclusion, but Section 44AA(1) meant for computing taxable

income

• Obligation created in case where lower profits are declared

August 27, 2016

29‐08‐2016

17

XYZ, a partnership firm, is covered under Section 44ADA During the year, XYZ had availed a loan from PQR Co. of Rs. 20

lakhs @ 10% While paying the interest, XYZ failed to deduct and deposit TDS Section 40(a)(ia) and Section 44ADA – Non-obstante provisions While computing presumptive income @ 50% of gross receipts, can

tax authority disallow payment of interest under Section 40(a)(ia) andmake addition to income determined on presumptive basis? Jaharlal Mukherjee v. I.T.O [AY 2008-09] [ITA No. 73/Kol/2014] I.T.O v. Mark Construction [2012] [23 taxmann.com 398 (Kol)]

August 27, 2016

Clause 12 - Profit and loss assessable on presumptive basis…

August 27, 2016

Amount of profits/gains credited/debited to the Statement of Profit andLoss to be stated

If the amount assessable does not match with amount included in theStatement of Profit and Loss

• Note mentioning that amount as per Statement of Profit and Loss isnot actual amount of profit under the relevant section may be given

29‐08‐2016

18

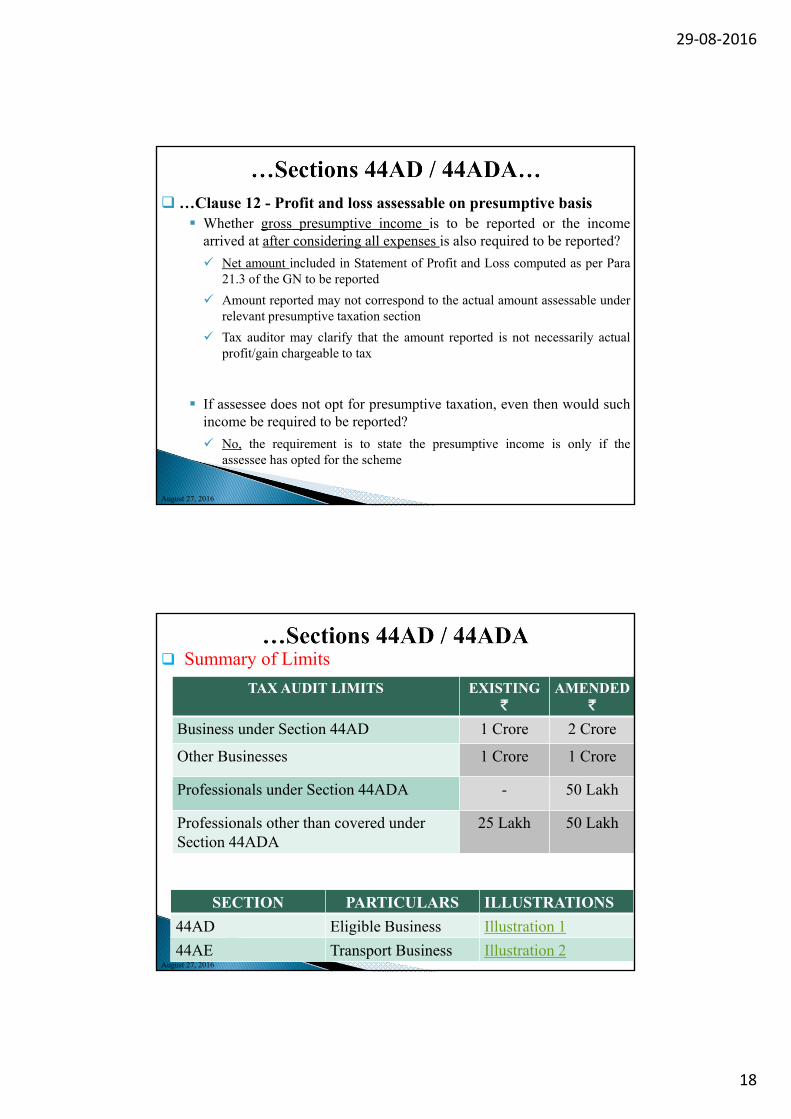

…Clause 12 - Profit and loss assessable on presumptive basis Whether gross presumptive income is to be reported or the income

arrived at after considering all expenses is also required to be reported?

Net amount included in Statement of Profit and Loss computed as per Para21.3 of the GN to be reported

Amount reported may not correspond to the actual amount assessable underrelevant presumptive taxation section

Tax auditor may clarify that the amount reported is not necessarily actualprofit/gain chargeable to tax

If assessee does not opt for presumptive taxation, even then would suchincome be required to be reported?

No, the requirement is to state the presumptive income is only if theassessee has opted for the scheme

August 27, 2016

TAX AUDIT LIMITS EXISTING`

AMENDED`

Business under Section 44AD 1 Crore 2 Crore

Other Businesses 1 Crore 1 Crore

Professionals under Section 44ADA - 50 Lakh

Professionals other than covered under Section 44ADA

25 Lakh 50 Lakh

Summary of Limits

SECTION PARTICULARS ILLUSTRATIONS

44AD Eligible Business Illustration 1

44AE Transport Business Illustration 2August 27, 2016

29‐08‐2016

19

PENALTIES

August 27, 2016

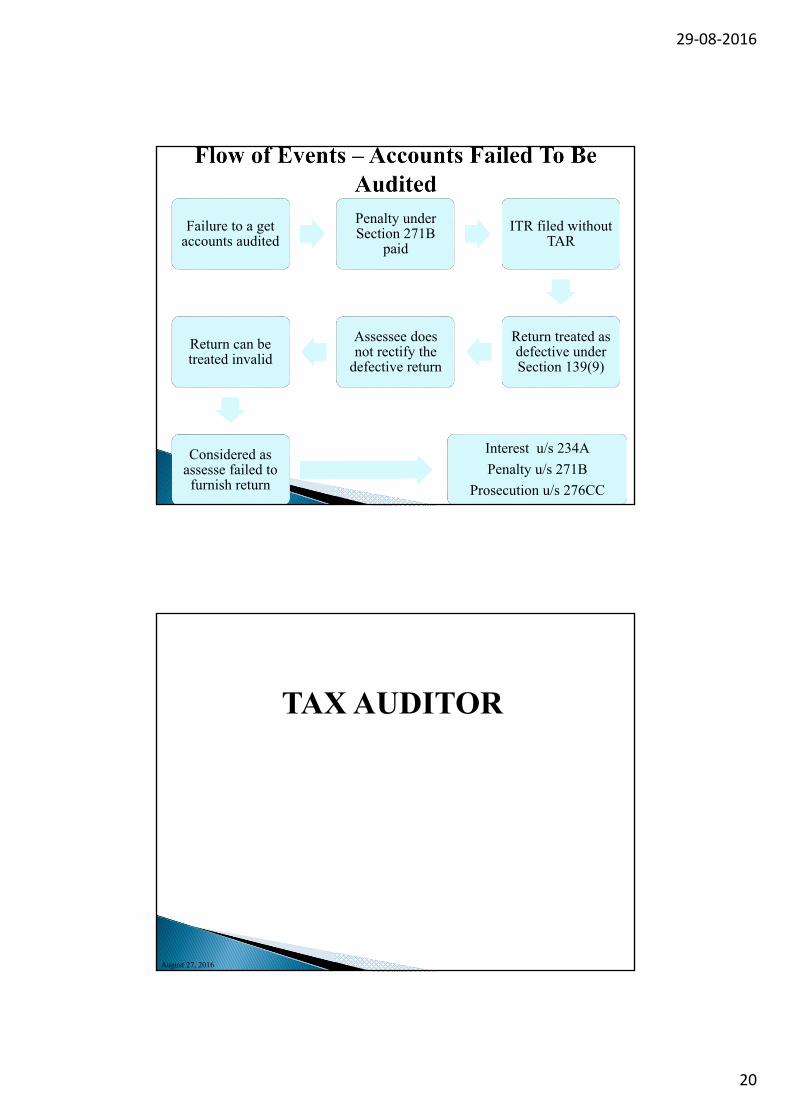

Section 271B – Failure to get accounts audited Penalty lower of –

• 0.5% of sales, turnover or gross receipts of the relevant PY• ` 1,50,000

Assessee is not absolved of his obligation to get the accountsaudited after payment of penalty

Assessee is required to get his books audited after default Section 273B – Penalty not to be imposed on certain cases If assessee proves that there was a reasonable cause for default Situational examples –

• Delay due to resignation of Tax auditor• Bonafide interpretation of the term “Turnover”• Death or physical inability of partner-in-charge of accounts• Natural calamities

August 27, 2016

29‐08‐2016

20

Failure to a get accounts audited

Penalty under Section 271B

paid

ITR filed without TAR

Return treated as defective under Section 139(9)

Assessee does not rectify the

defective return

Return can be treated invalid

Considered as assesse failed to furnish return

Interest u/s 234A

Penalty u/s 271B

Prosecution u/s 276CC

TAX AUDITOR

August 27, 2016

29‐08‐2016

21

The tax audit is to be carried out by an “Accountant” “Accountant” as per explanation to Section 288 (2) defines – ‘Chartered Accountant’ who is entitled to act as auditor of companies as per

Section 141 of the Companies Act, 2013 – includes a firm of CharteredAccountants

It cannot be done by any person other than Chartered Accountants Not necessary that statutory auditor to carry out the tax audit

Joint tax auditors may be appointed A member in part-time practice is not eligible to perform attest function,

including Tax Audit – ICAI Code of Ethics – Not to certify the financial statements Where he is employed or Concern where he or his firm or partner of him firm has a substantial interest

Internal Auditor cannot do tax auditMaintain a record of the tax audit assignments acceptedAugust 27, 2016

Maximum number = 60 Tax Audits In capacity of proprietor and partner the aggregate must not exceed 60

assignments

Calculation of 60 Audits

Includes Joint Audits Exclude –• Audits of branches as

separate units, as Headoffice and branch isconsidered as a single unit

• Audits under section 44ADand 44AE

August 27, 2016

29‐08‐2016

22

A firm has 4 partners. Each partner already has 4 Tax Auditassignments in their personal capacity. How many Tax Auditassignments can the firm undertake? Maximum number of audits that a firm can take in an assessment

year => 60 x 4 = 240 Since, the partners each have 4 Tax Audit assignments engaged in

personal capacity, the number of total assignments to be deductedas a partner’s capacity => 4 x 4 = 16

Total number of Tax Assignments that can be taken up by the firm=> 240-16 = 224

Limit of audits to be carried out by LLP ?

August 27, 2016

REPORTING REQUIREMENTS

August 27, 2016

29‐08‐2016

23

SR NO

FORMS PARTICULARS ILLUSTRATION

1 3CA Person carrying on business or professionand required to get under any other law toget his accounts audited

FORM 3CA

2 3CB Person carrying on business or professionand not covered in point 1

FORM 3CB

3 3CD Particulars to be furnished under section44AB shall be in this form

FORM 3CD

August 27, 2016

To indicate – Whether the statutory audit was conducted by the Tax auditor or any

other auditor; the name in case of any other auditor Whether the Audit Report, Audited Balance Sheet and Statement of Profit

and Loss and other documents to be part of or annexed thereto areannexed in Form No. 3CA

Reference as to the date of Statutory Audit Report To indicate – Whether the particulars required is annexed in Form No. 3CD Whether the particulars given in Form No. 3CD are true and correct Any observation/qualification

To examine - The books of account Other relevant documents

To state reasons, if any of the observations or qualifications To indicate if the branch audit is carried out, the same have been

consideredAugust 27, 2016

29‐08‐2016

24

Form 3CB

Opinion of Tax Auditor on whether the accounts

audited show a true and fair view

Statement of particulars to be furnished under Section 44AB annexed to auditor’s

report in Form 3CD

August 27, 2016

To indicate – Whether the Balance Sheet and Statement of Profit and Loss have been

examined by the Tax Auditor

Whether the Balance Sheet and Statement of Profit and Loss are attached toForm No. 3CB

Whether Balance Sheet and Statement of Profit and Loss are in agreement withthe books of account

Any observations / comments / discrepancies / inconsistencies

Whether all the information and explanations are received

Whether the accounts give a true and fair view

To indicate – Whether the particulars required is annexed in Form No. 3CD

Whether the particulars given in Form No. 3CD are true and correct

To state reasons in case of observations / qualifications

To indicate if the branch audit is carried out, the same have been considered

August 27, 2016

29‐08‐2016

25

Form 3CDForm 3CD

Part APart A

Clauses

1 to 8

Clauses

1 to 8

Part BPart B

Clauses

9 to 41

Clauses

9 to 41

August 27, 2016

August 27, 2016

29‐08‐2016

26

August 27, 2016

August 27, 2016

29‐08‐2016

27

August 27, 2016

August 27, 2016

29‐08‐2016

28

August 27, 2016

August 27, 2016

29‐08‐2016

29

DOCUMENTATION AND AUDIT PROCEDURES

“The skill of an accountant can always be ascertained by an inspection of his working papers.”

- Robert H. Montgomery, Montgomery’s Auditing, 1912

August 27, 2016

Appointment Letter of Appointment as Tax Auditors• In case of a company – Copy of Resolution of BOD or any other

authorisation• In case of a firm or proprietory concern – by Partner or by

proprietor or authorised person, as the case may be In case of new appointment• Letter of communication with the previous auditor• Obtain no objection

Engagement Letter• Signed by - Assessee and Tax Auditor• Indicate in detail - obligations of the Assessee and Tax Auditor

August 27, 2016

29‐08‐2016

30

Audit Planning Audit Programme• Specifying the team members involved -

• Clausewise allocation• Clausewise broad outlines for approach

• Work out Schedule / Timelines Detailed Tax Audit Checklist, if available

Audit Working Papers Signed Financials of the previous year Supporting documents for Form 3CD, e.g.-• TDS Remittances• Proof of payment statutory dues• Stock details

August 27, 2016

…Audit Working Papers Documentation of sample transactions verified and basis of such

sample selection Assessee’s responses to the queries raised Justification for any audit qualification Reconciliation of the figures as appearing in different statements /

workings - audited financial statements, tax computation, VATreturns, Service Tax returns, TDS returns, etc.,

If relied upon any decision – the text of such decisions If taken any expert’s views, those opinions Final Tax Audit Report duly signed and authenticated

August 27, 2016

29‐08‐2016

31

Permanent (Tax) Audit File About business Certificate of Registration PAN and TAN Registration Certificates under various Indirect Taxes in force, e.g.

- Service Tax Registration Certificate VAT Registration Certificate Copy of MOA and AOA or Partnership Deed or Bye Laws, as the

case may be Bank Account details Branch details Understanding the internal control systems of the assessee

Current (Tax) Audit File Clausewise working papers

August 27, 2016

August 27, 2016

29‐08‐2016

32

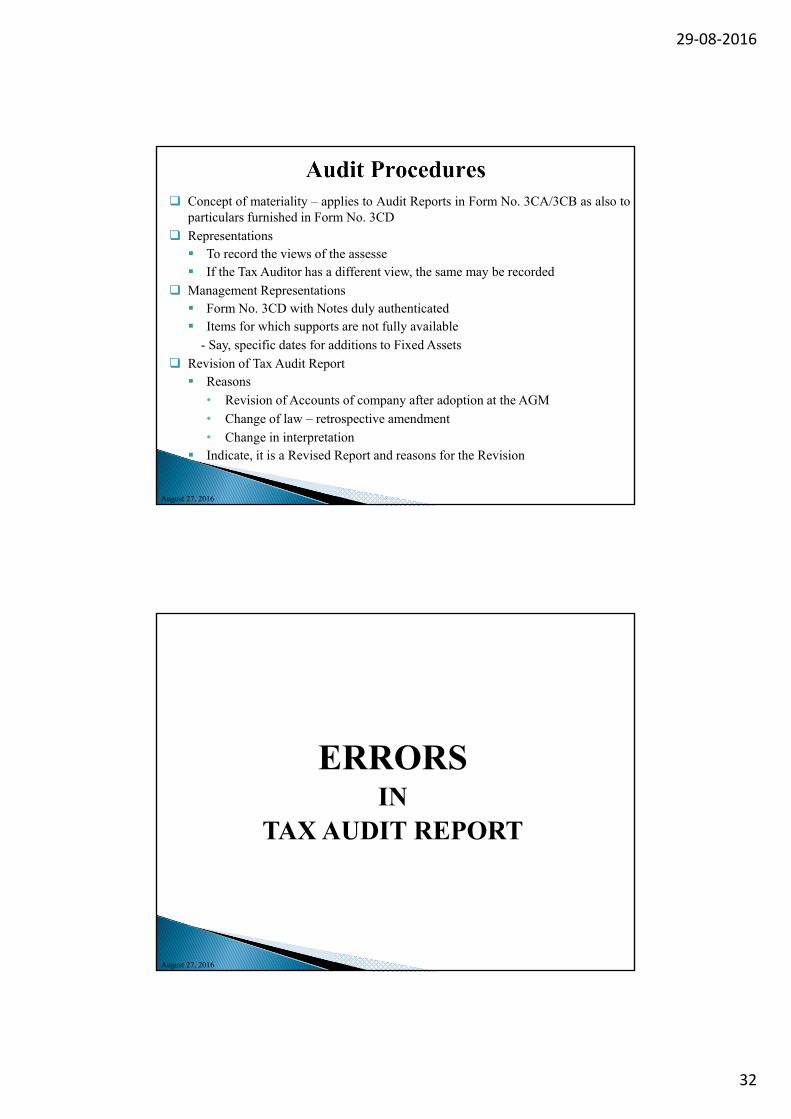

Concept of materiality – applies to Audit Reports in Form No. 3CA/3CB as also toparticulars furnished in Form No. 3CD

Representations To record the views of the assesse If the Tax Auditor has a different view, the same may be recorded

Management Representations Form No. 3CD with Notes duly authenticated Items for which supports are not fully available

- Say, specific dates for additions to Fixed Assets

Revision of Tax Audit Report Reasons

• Revision of Accounts of company after adoption at the AGM

• Change of law – retrospective amendment

• Change in interpretation Indicate, it is a Revised Report and reasons for the Revision

August 27, 2016

ERRORS IN

TAX AUDIT REPORT

August 27, 2016

29‐08‐2016

33

Comptroller and Auditor General (“CAG”) conducted entry meetingwith CBDT in February 2014, in which defaults of tax auditors werediscussed

Observations… Disclosed incorrect information on depreciation allowance

Additional Depreciation – Even if the asset is put to use for less than180 days, depreciation on actual plant and machinery acquired andinstalled was taken at 20% and not restricted to 50% thereof (withoutreference to any support for such treatment)

Incorrect information furnished in Tax Audit Report Unabsorbed business loss stated included amounts of the assessment

years beyond 8 years than the reporting year and also were notavailable for set off under Section 72

August 27, 2016

…ObservationsWrong information reported for various exemptions / deductions

Exemption allowed under Section 11 of the Act without obtaining reportunder Section 12A(b) in Form 10B

Non-disclosure of personal / capital expenditure resulting ininappropriately allowance

Mistakes in reporting cash payments exceeding ` 20,000 per day

Membership number is not mentioned

August 27, 2016

29‐08‐2016

34

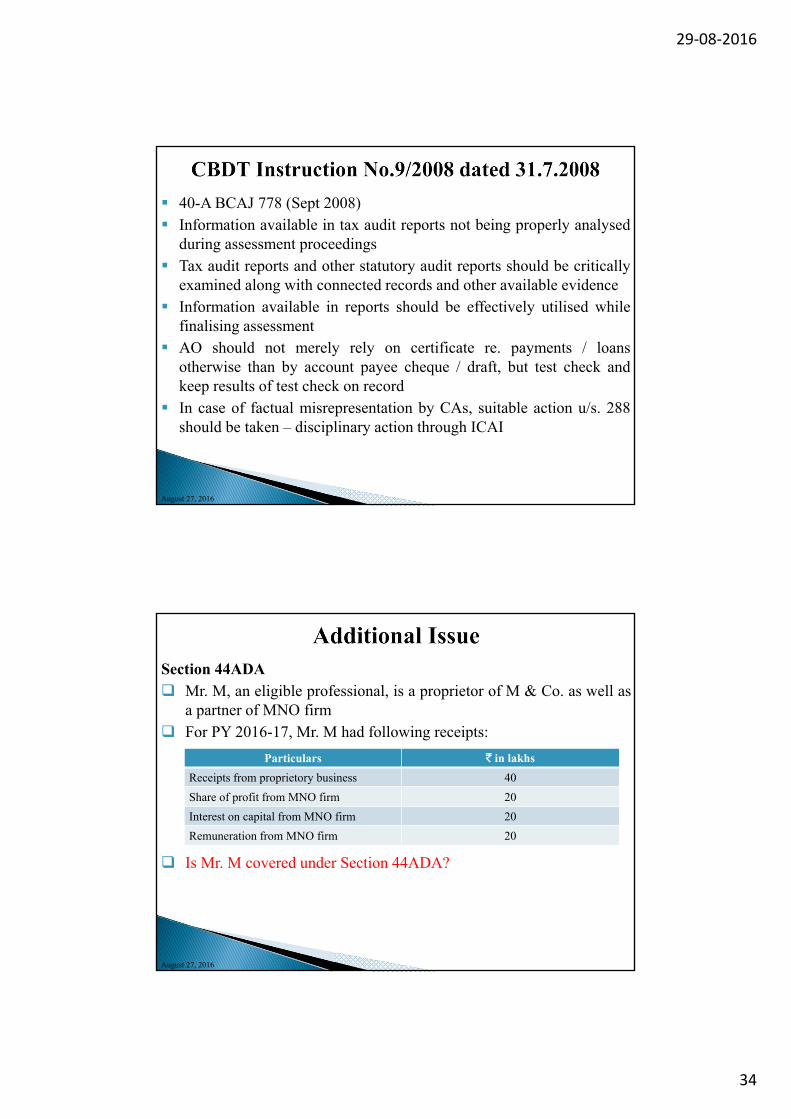

40-A BCAJ 778 (Sept 2008) Information available in tax audit reports not being properly analysed

during assessment proceedings Tax audit reports and other statutory audit reports should be critically

examined along with connected records and other available evidence Information available in reports should be effectively utilised while

finalising assessment AO should not merely rely on certificate re. payments / loans

otherwise than by account payee cheque / draft, but test check andkeep results of test check on record

In case of factual misrepresentation by CAs, suitable action u/s. 288should be taken – disciplinary action through ICAI

August 27, 2016

Section 44ADA Mr. M, an eligible professional, is a proprietor of M & Co. as well as

a partner of MNO firm For PY 2016-17, Mr. M had following receipts:

Is Mr. M covered under Section 44ADA?

Particulars ` in lakhs

Receipts from proprietory business 40

Share of profit from MNO firm 20

Interest on capital from MNO firm 20

Remuneration from MNO firm 20

August 27, 2016

29‐08‐2016

35

August 28, 2016August 27, 2016

August 28, 2016August 27, 2016