Provisions and contingencies - WIRC and contingencies.pdf · IAS 37 Provisions, contingent...

30

IAS 37 Provisions, contingent liabilities & contingent assets 1 Provisions Contingent Liabilities Contingent Assets Summary Disclosures

-

Upload

duongtuyen -

Category

Documents

-

view

244 -

download

4

Transcript of Provisions and contingencies - WIRC and contingencies.pdf · IAS 37 Provisions, contingent...

IAS 37Provisions, contingent liabilities & contingent assets

1

Provisions

Contingent Liabilities

Contingent Assets

Summary

Disclosures

Provisions - recognition

• A provision is defined as a liability of uncertain timing or

amount (IAS 37.10-11)

• A provision shall be recognised when: (IAS 37.14)

obligation

2

– An entity has a present legal or constructive obligation

as a result of a past event; and

– It is probable outflow of resources embodying

economic benefits required to settle the obligation; and

– A reliable estimate can be made of the obligation.

If these conditions are not met, no provision shall be recognised

Provisions – recognition

Obligations resulting from a past event (IAS 37.10)

• Obligating event creates a legal or constructive obligation that results in an entity having no realistic alternative to settling that obligation.

• Legal obligation derives from a contract (through its explicit or implicit terms); legislation; or other operation of law.

3

terms); legislation; or other operation of law.

• Constructive obligation is an obligation that derives from an entity's actions where:

• (a) by an established pattern of past practice, published policies or a sufficiently specific current statement, the entity has indicated to other parties that it will accept certain responsibilities; and

• (b) as a result, the entity has created a valid expectation on the part of those other parties that it will discharge those responsibilities

Recognition

Example Scenario 1

As required by local legislation, Entity A gives warranties at the time of sale to purchasers of its products. Under the terms of the warranty the manufacturer undertakes to make good, by repair or replacement, manufacturing defects that become apparent within

4

replacement, manufacturing defects that become apparent within a period of three years from the date of sale.

On past experience, it is probable there will be some claims under the warranties.

Should a provision be recognised?

Recognition

Example Scenario 2

• On 28 December 20X8 Entity B has been fined CU10,000 for causing

unlawful environmental damage.

• A new law is being debated in parliament and is virtually certain to be

passed making Entity B responsible for cleaning up the damage and

making it necessary for the company to alter its machines in order to

5

making it necessary for the company to alter its machines in order to

become more environmentally friendly.

• The expected cost of the clean-up is £1,000,000 and of the machines

£50,000.

At the year ended 31 Dec 20X8, should the followingcosts be provided for:

(a) Costs of rectifying the damage?(b) Cost of modifying machines?

Provisions – measurement

Best estimate

• Amount recognised shall be the entity’s best estimate of the expenditure required to settle the obligation at the reporting date (IAS 37.36)

– what the entity would rationally pay to settle or to transfer it to a 3rd party (IAS 37.37)

6

transfer it to a 3 party (IAS 37.37)

– involves judgement and experience (IAS 37.38)

– uncertainties dealt with by various means depending on circumstances (IAS 37.39-40)

• large population of items use 'expected value' (weighting of possible outcomes by probabilities)

• where range of outcomes is continuous and each outcome as likely as others, use mid-point of range

• single item use most likely outcome unless other possible outcome suggest a higher or lower amount

Provisions – measurement

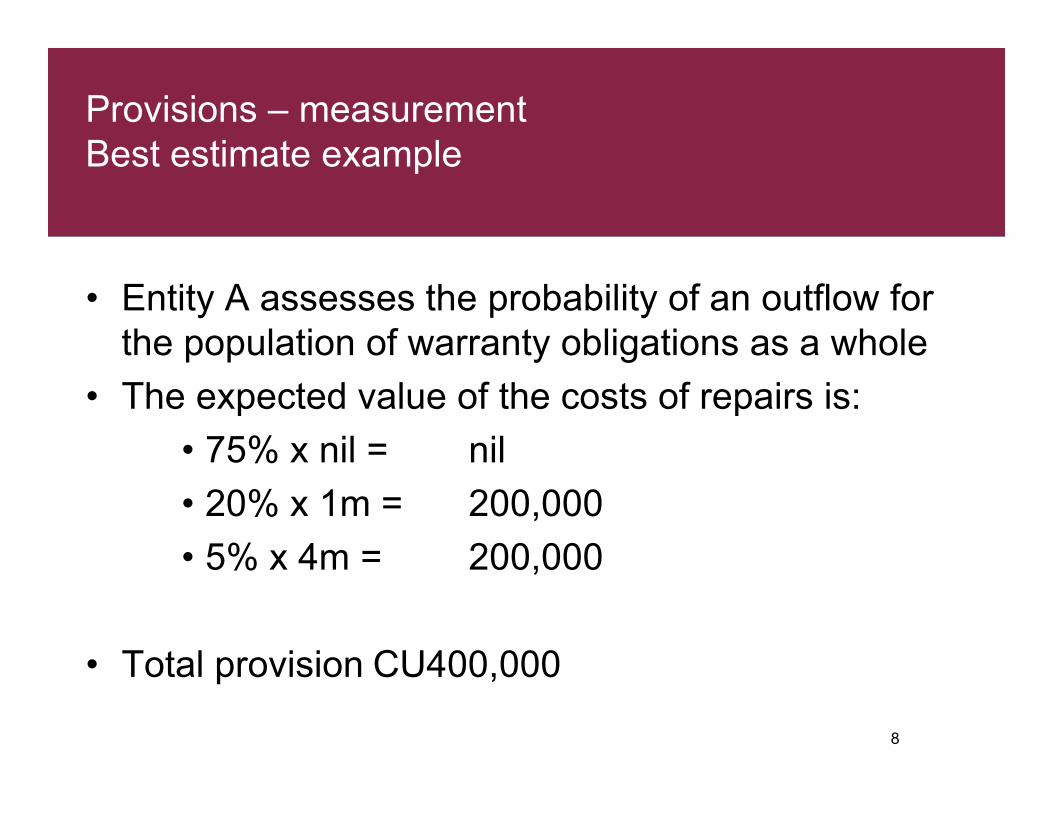

Best estimate example

• Entity A sells goods with a warranty under which customers are covered for the cost of repairs of any manufacturing defects that become apparent within the first six months after purchase.

• If minor defects were detected in all products sold, repair costs of CU1million would result.

• If major defects were detected in all products sold, repair costs of

7

• If major defects were detected in all products sold, repair costs of CU4million would result.

• The entity's past experience and future expectations indicate that, for the coming year:

– 75% of the goods sold will have no defects

– 20% of the goods sold will have minor defects

– 5% of the goods sold will have major defects.

What amount will entity A provide for this obligation?

Provisions – measurement

Best estimate example

• Entity A assesses the probability of an outflow for

the population of warranty obligations as a whole

• The expected value of the costs of repairs is:

8

• The expected value of the costs of repairs is:

• 75% x nil = nil

• 20% x 1m = 200,000

• 5% x 4m = 200,000

• Total provision CU400,000

Provisions – measurement

Other factors to consider

• Take into account risks and uncertainties (IAS 37.42)

• Uncertainty does not justify overly prudent provisions (IAS 37.43)

• Discount to present value where material (IAS 37.45-47)

• Reflect future events when sufficient evidence exists that

9

• Reflect future events when sufficient evidence exists that they will occur (IAS 37.48–50)

• Do not take into account gains from expected disposal of assets, even if closely linked to event giving rise to the provision (IAS 37.51-52)

• Review at each balance sheet date and adjust to reflect current best estimate (IAS 37.59)

• Use provision only for expenditures for which it was originally recognised (IAS 37.61)

Reimbursements (IAS 37.53-58)

• An entity may be able to look to another party to pay all or

part of the expenditure required to settle a provision

– eg insurance contract, indemnity clauses or supplier warranties

• Recognise reimbursement from another party only when

10

• Recognise reimbursement from another party only when

virtually certain to be received

• Reimbursement amount shall not exceed provision amount

• Treat reimbursement as a separate asset – do not net off

the provision amount

• Can present income statement amount net of the

reimbursement amount

Provisions – application issues

If an entity has a contract that is onerous (ie unavoidable

costs of meeting obligations exceed benefits expected to be

Provisions shall not be recognised for future operating

losses (expectation of such may indicate impairment of

assets – see IAS 36) (IAS 37.63-65)

11

costs of meeting obligations exceed benefits expected to be

received), the present obligation under the contract shall be

recognised as a provision (IAS 37.66-69)

CONTRACT

Restructuring provisions are only recognised when an

entity has a detailed formal plan for the restructuring and has

raised a valid expectation in those affected that it will carry

out the restructuring by starting to implement it or announcing

its main features (IAS 37.70-83)

Restructuring provisions

Example

• Entity A made a public announcement on 23 March 20X8 that it will close its London factory in May and relocate to Scotland. This will result in some staff being made redundant and some being relocated. It will also result in a new senior manager being recruited externally and trained to run the new factory.

• The entity has identified the following estimated costs of restructuring:

12

• The entity has identified the following estimated costs of restructuring:

– CU160,000 redundancy costs

– CU220,000 relocation and retraining of existing staff

– CU90,000 recruitment and training cost of new manager

– CU140,000 relocation and re-installation of plant and inventories

– CU73,000 costs of remaining non-cancellable lease term - London

– CU57,000 operating losses up to date of relocation

– CU38,000 marketing costs to revamp corporate image

What costs can entity A provide for at 31 March 20X8?

Restructuring provisions

Example solution

• Entity A can provide for the following:

– CU160,000 redundancy costs

– CU73,000 costs of remaining non-cancellable lease term - London

• The following are costs associated with ongoing operations

13

• The following are costs associated with ongoing operations and so cannot be recognised in a restructuring provision

– CU220,000 relocation and retraining of existing staff

– CU90,000 recruitment and training cost of new manager

– CU140,000 relocation and re-installation of plant and inventories

– CU57,000 operating losses up to date of relocation

– CU38,000 marketing costs to revamp corporate image

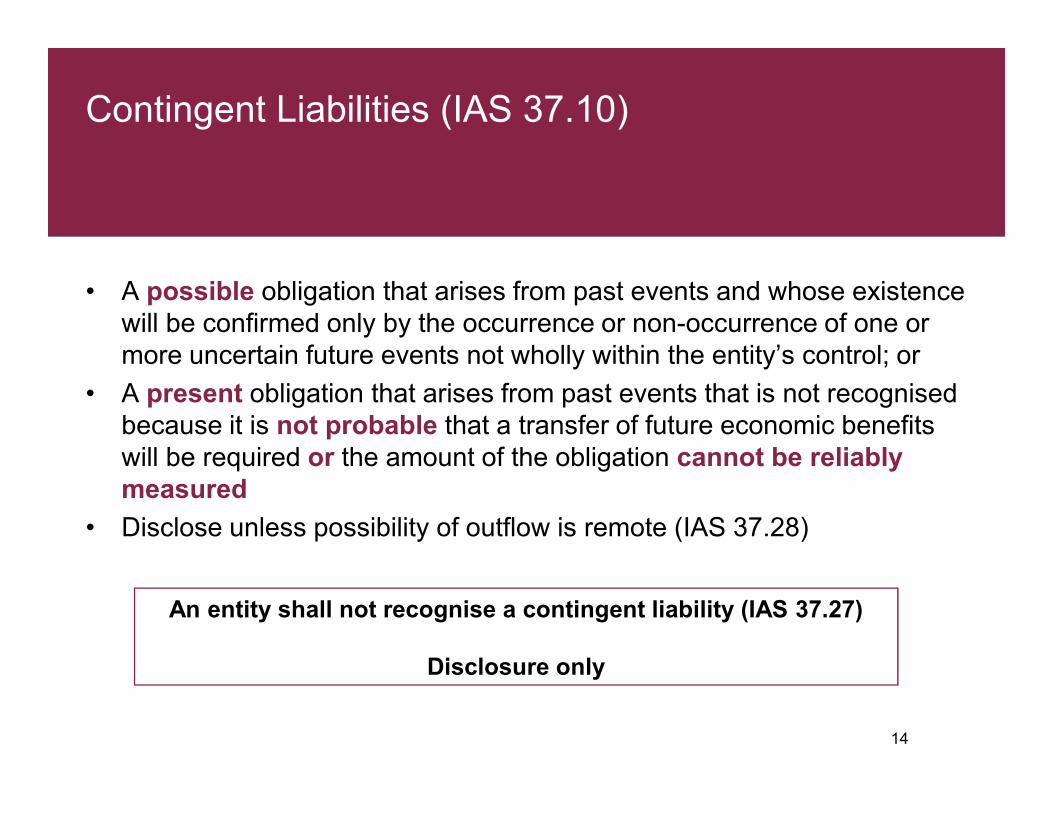

Contingent Liabilities (IAS 37.10)

• A possible obligation that arises from past events and whose existence

will be confirmed only by the occurrence or non-occurrence of one or

more uncertain future events not wholly within the entity’s control; or

• A present obligation that arises from past events that is not recognised

14

• A present obligation that arises from past events that is not recognised

because it is not probable that a transfer of future economic benefits

will be required or the amount of the obligation cannot be reliably

measured

• Disclose unless possibility of outflow is remote (IAS 37.28)

An entity shall not recognise a contingent liability (IAS 37.27)

Disclosure only

Contingent Liabilities

Example

• Entity A faces a claim for an alleged breach of copyright. Management dispute the claim on the grounds that the alleged breach did not take place and their lawyers confirm that, based on the

15

and their lawyers confirm that, based on the evidence available, it is unlikely that the claim will succeed.

• In this case, management decide that there is no past obligating event so do not recognise a provision but disclose the matter as a contingent liability (unless the possibility of any outflow is considered as remote)

Contingent Assets

• A possible asset that arises from past events and whose existence will

be confirmed only by the occurrence or non-occurrence of one or more

uncertain future events not wholly within the entity’s control (IAS 37.10)

• Do not recognise unless realisation of income is virtually certain

16

• Do not recognise unless realisation of income is virtually certain

(IAS 37.33)

• Disclosure only if inflow of economic benefit is probable (IAS 37.34)

An entity shall not recognise a contingent asset (IAS 37.31)

Disclosure only

Summary – IAS 37.Appendix B

Provisions and contingent liabilities decision tree

Present obligation

and past event

Possibleobligation

Probable

Yes Yes

Yes

NoNo

No

17

Probableoutflow

Remote

Reliableestimate

Yes

Yes

YesNo

No (rare)

No

PROVIDE DISCLOSE NOTHING

Disclosures (IAS 37.84-92)

1. Movements during the period by each class of

provision

2. Description of each class of provision plus details of

uncertainties about the timing or amount of outflows

and details of any reimbursements

18

and details of any reimbursements

3. Details of contingent liabilities

4. Details of contingent assets

In some cases information will not be disclosed where it is not

practical to do so – but this fact must be disclosed (IAS 37.91)

In rare cases, detailed information will not be disclosed if it is expected

to seriously prejudice the position of the entity in a dispute with other

parties but entity still discloses some information (IAS 37.92)

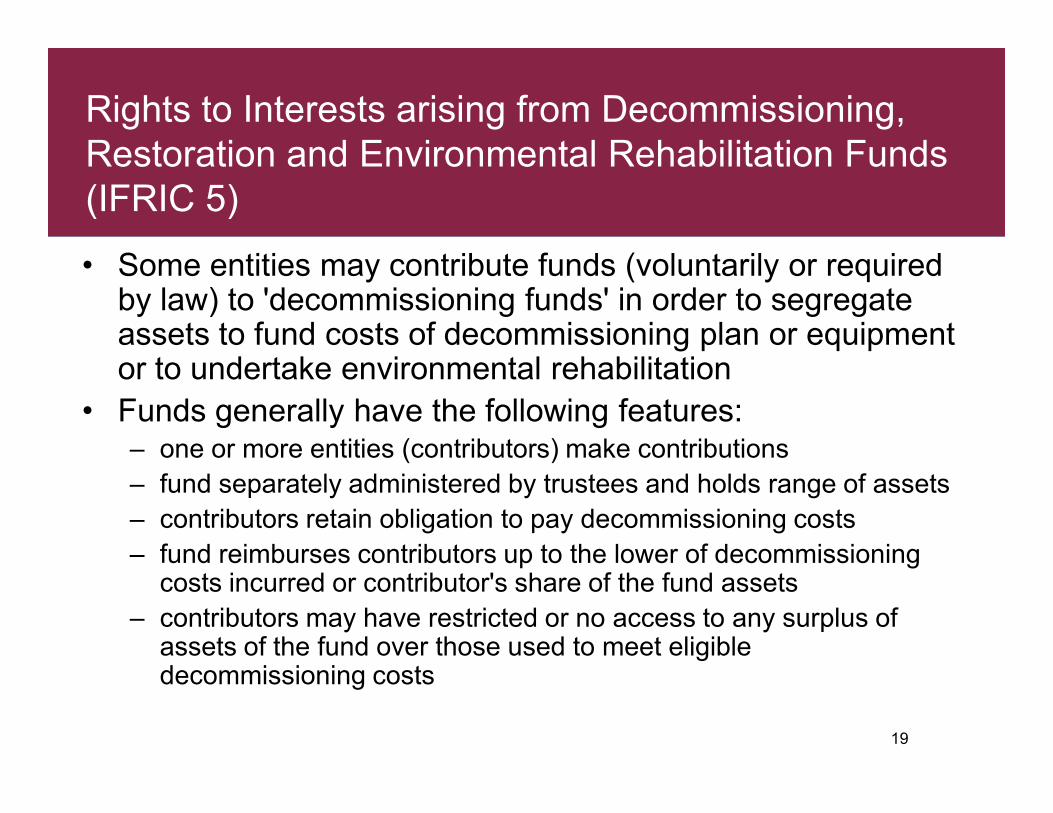

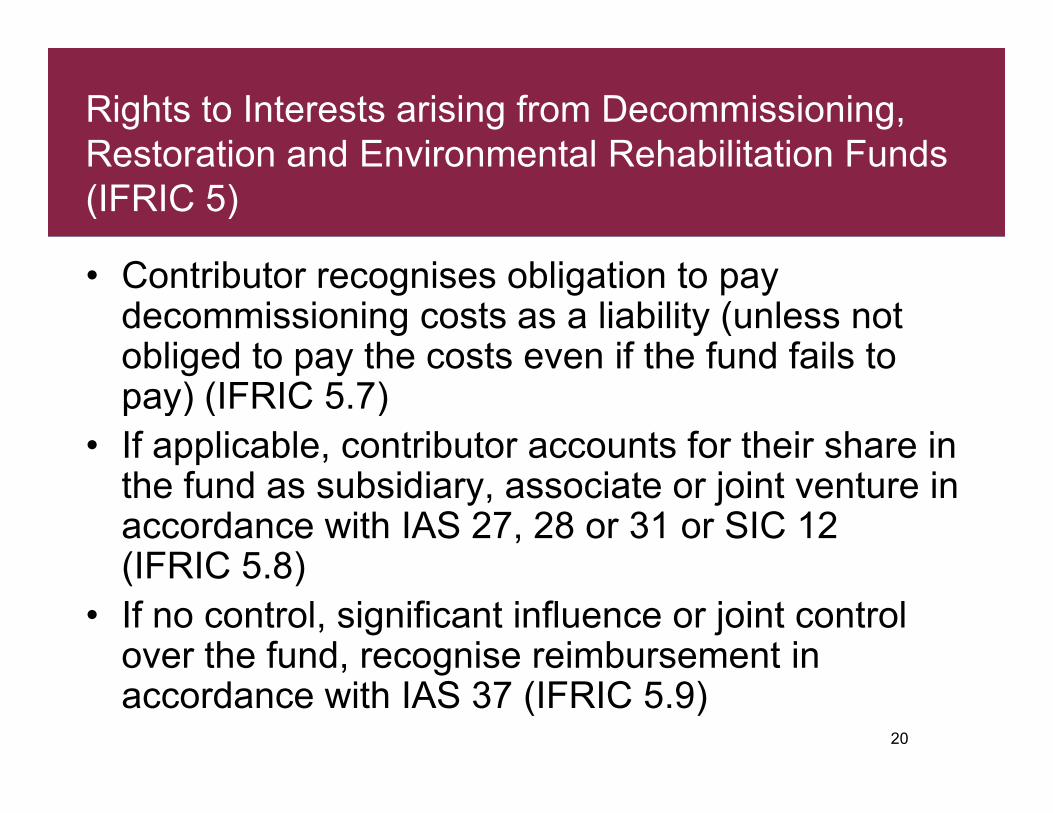

Rights to Interests arising from Decommissioning,

Restoration and Environmental Rehabilitation Funds

(IFRIC 5)

• Some entities may contribute funds (voluntarily or required by law) to 'decommissioning funds' in order to segregate assets to fund costs of decommissioning plan or equipment or to undertake environmental rehabilitation

• Funds generally have the following features:

19

• Funds generally have the following features:– one or more entities (contributors) make contributions

– fund separately administered by trustees and holds range of assets

– contributors retain obligation to pay decommissioning costs

– fund reimburses contributors up to the lower of decommissioning costs incurred or contributor's share of the fund assets

– contributors may have restricted or no access to any surplus of assets of the fund over those used to meet eligible decommissioning costs

Rights to Interests arising from Decommissioning,

Restoration and Environmental Rehabilitation Funds

(IFRIC 5)

• Contributor recognises obligation to pay decommissioning costs as a liability (unless not obliged to pay the costs even if the fund fails to pay) (IFRIC 5.7)

20

pay) (IFRIC 5.7)

• If applicable, contributor accounts for their share in the fund as subsidiary, associate or joint venture in accordance with IAS 27, 28 or 31 or SIC 12(IFRIC 5.8)

• If no control, significant influence or joint control over the fund, recognise reimbursement in accordance with IAS 37 (IFRIC 5.9)

Dismantling, decommissioning and restoration costs

(IAS 16.16(c) and IAS 16.18)

• The cost of an item of property, plant and equipment includes the initial estimate of the costs of an obligation to dismantle and remove the item and to restore the site on which it is located IAS 16.16(c)) unless incurred as a consequence of using the item to produce inventories

• IAS 2 Inventories applies to costs of obligations for dismantling, etc.

21

• IAS 2 Inventories applies to costs of obligations for dismantling, etc. incurred as a consequence of inventory production

An example would be a liability that was recognised by the operator of an oil rig for costs it expects to incur in future when the plant is decommissioned.

DR Cost of asset

CR Provision (IAS 37/IFRIC 1)

with best estimate of the cost of decommissioning

Changes in existing dismantling, decommissioning

and restoration costs – IFRIC 1

The estimated decommissioning costs may change for three reasons:

Revision of estimated outflows

eg estimate amount or timing of

Cost model

Add to or deduct from the cost

22

eg estimate amount or timing of decommissioning or restoration costs may change

Revision of the market-based discount rate (including changes in time value of money and liability-specific risks)

Unwinding of the discount due to the passage of time

Add to or deduct from the cost of PPE

Revaluation model

Adjust the revaluation surplus

In each case

Depreciate prospectively over the remaining life of the asset

Recognise in P&L as finance cost as it incurs –capitalisation is not permitted

Changes in existing dismantling, decommissioning

and restoration costs – IFRIC 1

Example

• Entity A has a nuclear power plant and a related

decommissioning liability

• The nuclear power plant

– started operating on 1 January 20X0

23

– started operating on 1 January 20X0

– has a useful life of 40 years

• Initial cost was CU120,000, including an amount for

decommissioning costs of CU10,000 – which represented

CU70,400 in estimated cash flows payable in 40 years

discounted at a risk-adjusted rate of 5% (which is

unchanged at 31 Dec 20X9)

How is this reflected in the accounts at 31 December 20X9?

Changes in existing dismantling, decommissioning

and restoration costs – IFRIC 1

Example continued

• Book value of plant is CU90,000 (120k less 30k depreciation –10/40x120)

• Liability has grown to CU16,300 due to unwinding of the discount (annual entry to DR finance cost CR liability)

On 31 December 2009, the entity estimates that, as a result of

24

• Accordingly, the entity adjusts the decommissioning liability from CU16,300 to CU8,300

– Dr decommissioning liability CU8,000

– Cr cost of asset CU8,000

On 31 December 2009, the entity estimates that, as a result of

technological advances, the net present value of the decommissioning

liability has decreased by CU8,000

How is this reflected in the accounts at 31 December 20Y0?

Changes in existing dismantling, decommissioning

and restoration costs – IFRIC 1

Example continued

• At 1 January 20Y0 the carrying value of the asset

is CU82,000 (cost 120k less accumulated

depreciation 30k less decommissioning adjustment

25

depreciation 30k less decommissioning adjustment

8k)

• Depreciation expense for 20Y0 is CU2,733 (82k /

30 years)

• Finance cost for unwinding discount is CU415

(CU8,300 @ 5%) so liability increases to CU8,715

Liabilities arising from Participating in a Specific

Market - Waste Electrical and Electronic Equipment

(IFRIC 6)

• IFRIC 6 provides guidance on the recognition of producers'

liabilities for waste management under the EU Directive on

WE&EE which regulates the collection, treatment, recovery

and environmentally sound disposal of waste equipment in

26

and environmentally sound disposal of waste equipment in

respect of sales of historical household equipment

• Directive requires that the cost of waste management for

historical household equipment should be borne

proportionately by producers that are active in the market

during the measurement period specified by the legislation

– eg in proportion to their respective share of the market by type of

equipment

Liabilities arising from Participating in a Specific

Market - Waste Electrical and Electronic Equipment

(IFRIC 6)

• The issue addressed is, in the context of the

decommissioning of WE&EE, what constitutes the

obligating event in accordance with IAS 37.14(a) for the

recognition of a provision for waste management costs. Is

27

recognition of a provision for waste management costs. Is

it:

– the manufacture or sale of the historical household

equipment?

– participation in the market during the measurement

period?

– the incurrence of costs in the performance of waste

management activities?

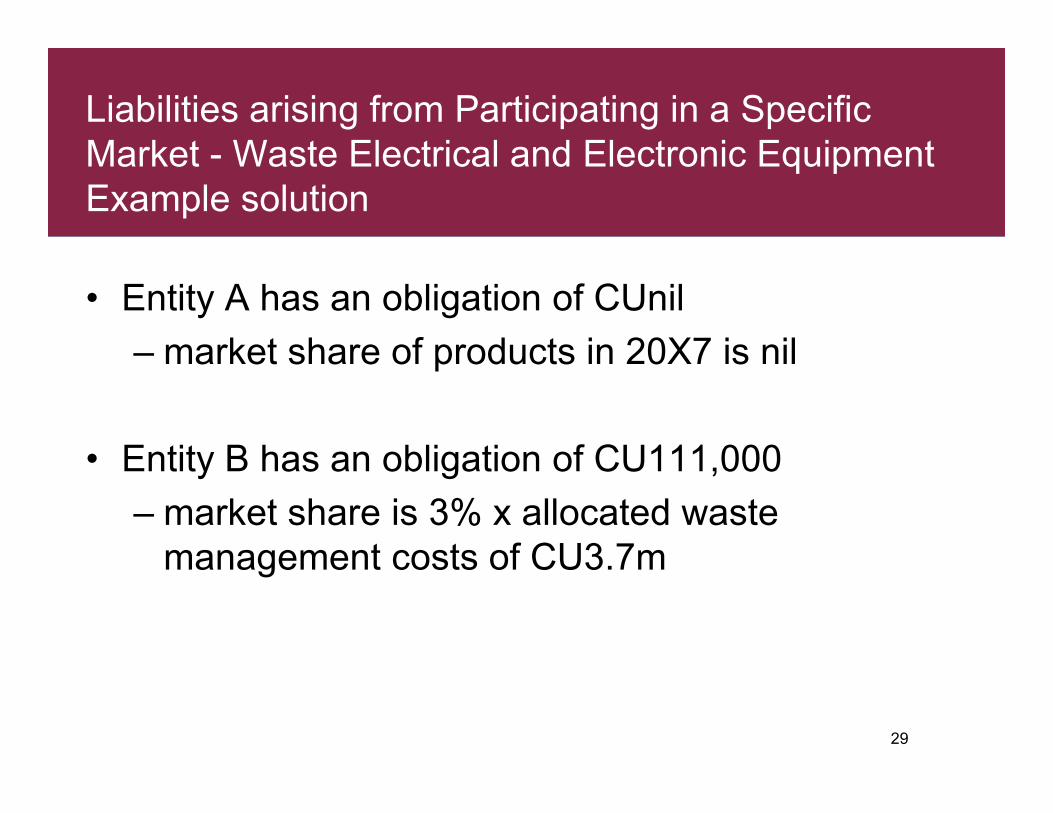

Liabilities arising from Participating in a Specific

Market - Waste Electrical and Electronic Equipment

Example

• WEEE Measurement period is the calendar year 20X7

• Waste management costs allocated to 20X7 = CU3.7m

• Entity A achieved 4% market share in relevant household electrical

equipment in 20X4 and 20X5 but discontinued its electrical equipment

operations by the end of 20X6

28

operations by the end of 20X6

• Entity B enters the relevant household equipment market in 20X7,

achieving a 3% share

• The average useful life of the electrical products is 2 years

How much should entities A and B recognise as a

provision for waste management costs in 20X7?

Liabilities arising from Participating in a Specific

Market - Waste Electrical and Electronic Equipment

Example solution

• Entity A has an obligation of CUnil

– market share of products in 20X7 is nil

29

• Entity B has an obligation of CU111,000

– market share is 3% x allocated waste

management costs of CU3.7m

Questions

30