PROVISIONAL TAX WORKSHOP. Who is liable for Prov Tax Registration as Prov Taxpayer Calculation of...

16

PROVISIONAL TAX WORKSHOP

-

Upload

dorcas-britney-fox -

Category

Documents

-

view

222 -

download

1

Transcript of PROVISIONAL TAX WORKSHOP. Who is liable for Prov Tax Registration as Prov Taxpayer Calculation of...

PROVISIONAL TAX

WORKSHOP

Who is liable for Prov Tax

Registration as Prov Taxpayer

Calculation of Prov Tax

Non-compliance to Procedures

POINTS FOR DISCUSSION

PROVISIONAL TAX

What is provisional tax?

It is not a separate kind of tax.

It is intended to assist taxpayers in meeting their tax liabilities.

It prevents large amounts being payable on assessment as it spreads liability over the tax year.

The provisional payment is based on an estimate of total taxable income derived by the taxpayer.

You will be required to make provision for your tax liability by making payments twice a year.

1. Half way through the year of assessment/tax year.

2. End of the year of assessment/ tax year.

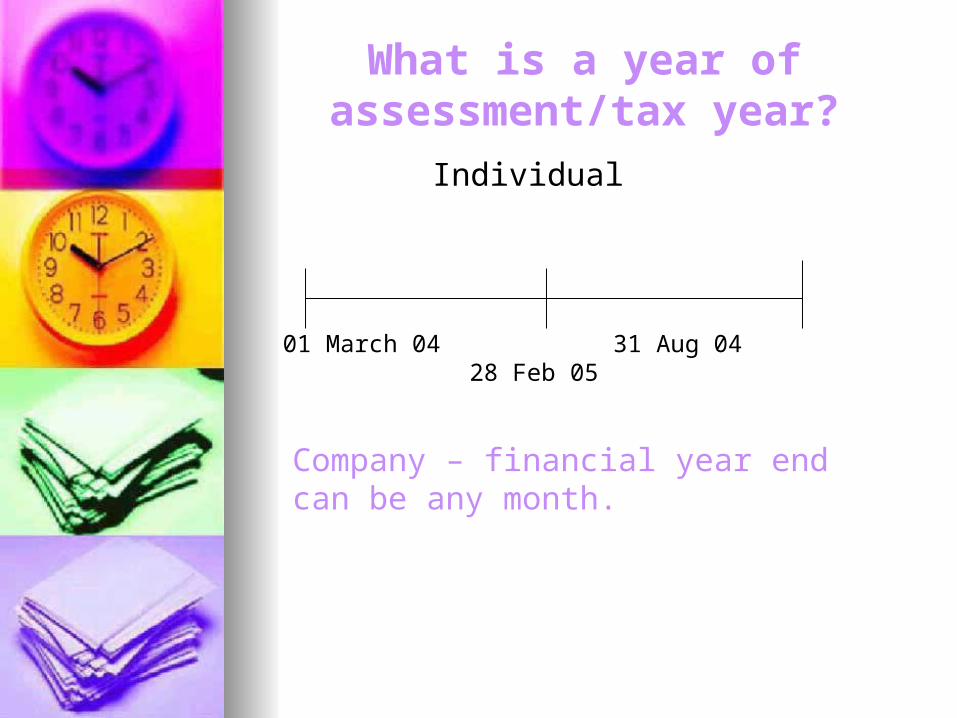

What is a year ofassessment/tax year?

Individual

01 March 04 31 Aug 04 28 Feb 05

Company – financial year end can be any month.

Who is liable for Provisional Tax?

Any person who derives income, other than remuneration, which exceeds R10 000 per annum (eg taxable investment income, business income, rental income)

under 65yrs – R15 000 exempt 65 and older – R22 000 exempt

Any director of a private co Any member of a close corp Any co, including a close corp

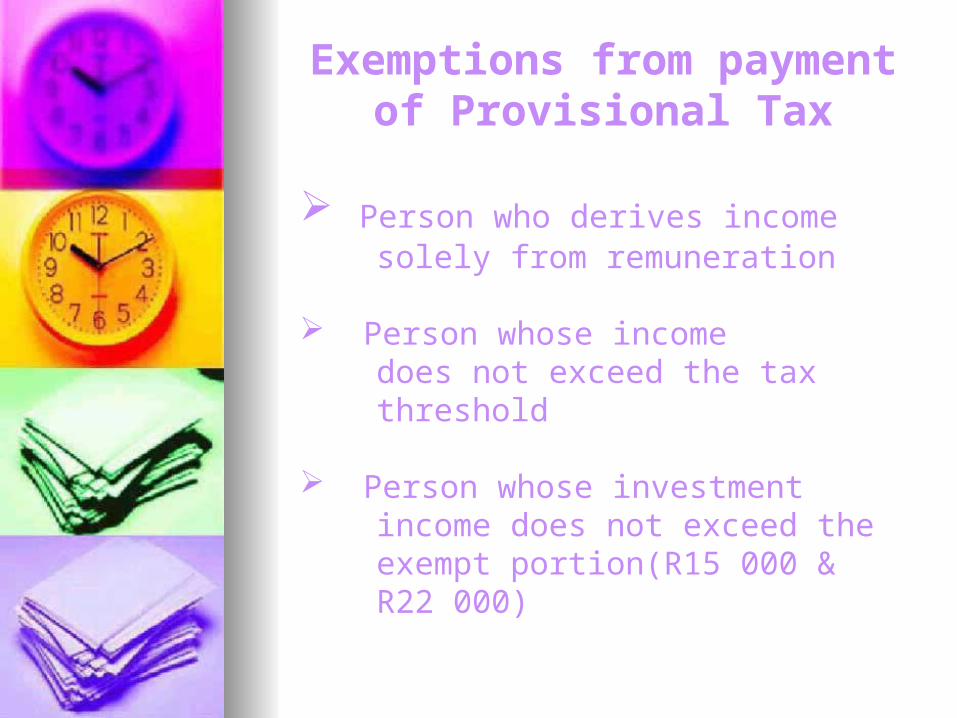

Exemptions from payment

of Provisional Tax

Person who derives income solely from remuneration

Person whose income does not exceed the tax threshold

Person whose investment income does not exceed the exempt portion(R15 000 & R22 000)

Registration as Provisional Taxpayer

Written application for registration as a provisional taxpayer must reach SARS within 30 days of becoming liable for the payment of prov tax.

Non-submission will result in int & penalties being levied on late payments and late renditions (First time a letter to waive int & penalties will be accepted, the second time not)

When must prov tax be paid?

1st payment > Within 6mnths from the commencement of the year of assessment. > Half of the estimated tax liability for the full year

2nd payment > Not later than the last day of the year of assessment. > Total actual tax liability for the full year less first payment.

Calculation of Prov Tax

Every prov taxpayer must submit an estimate of the total taxable income which will be derived during the relevant tax year.

Payment Methods:

Cash Cheque FNB Bank Payments Internet Banking E-Filing

E-Filing is an electronic system thatenables taxpayers to: - Submit returns electronically(IRP6) - Make payments electronically.

Please visit www.sars.gov.za

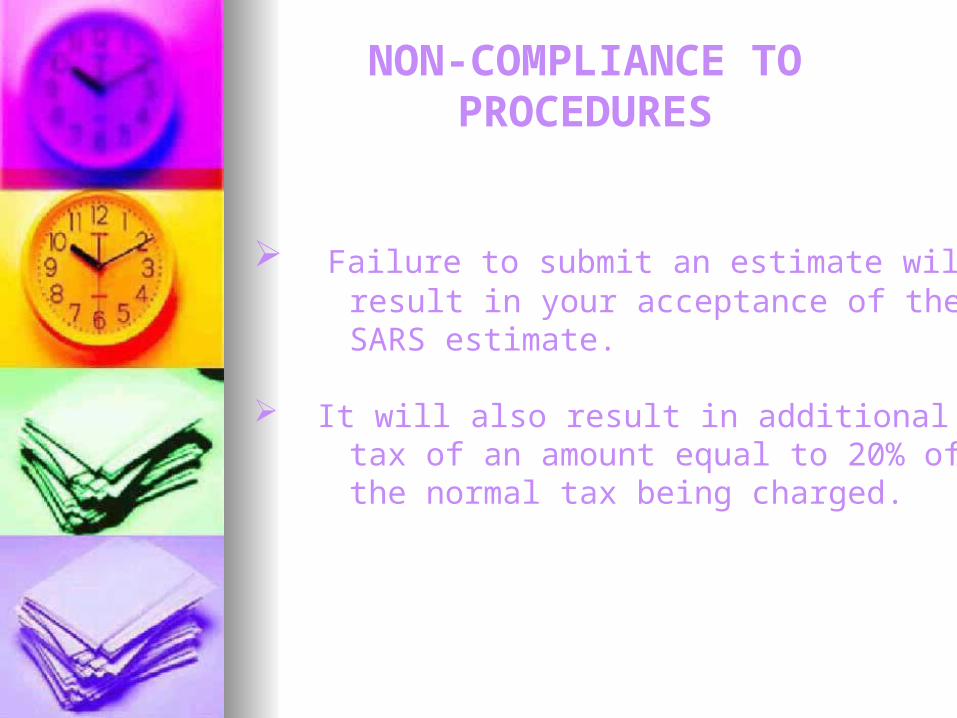

Failure to submit an estimate will result in your acceptance of the SARS estimate.

It will also result in additional tax of an amount equal to 20% of the normal tax being charged.

NON-COMPLIANCE TOPROCEDURES