Providing financial services in Germany - luther … · Providing financial services in Germany ......

5

Legal and Tax Advice | www.luther-lawfirm.com Providing financial services in Germany Most UK companies active in the banking and financial services industry currently benefit from the so called “European Passport” which allows to provide regulated services cross border or through branch offices in the EU/EEA on basis of the UK license. The “European Passport” is, inter alia, available for credit institutions, MiFID firms, payment services providers, fund managers as well as insurance undertakings and insurance intermediaries. A “hard Brexit” by which access to the European single market is capped will most likely result in a loss of the “European Passport” for UK firms. Thus, firms will not be able to provide services on basis of UK licenses. However, this guide has been prepared for the assistance of those interested in setting up a fully licensed subsidiary in Germany. It intends to answer some of the important, broad questions that may arise during the process. When specific problems occur in practice, it will often be necessary to obtain appropriate professional advice.

Transcript of Providing financial services in Germany - luther … · Providing financial services in Germany ......

Legal and Tax Advice | www.luther-lawfirm.com

Providing financial services in Germany Most UK companies active in the banking and financial services industry currently benefit from the so called “European Passport” which allows to provide regulated services cross border or through branch offices in the EU/EEA on basis of the UK license. The “European Passport” is, inter alia, available for credit institutions, MiFID firms, payment services providers, fund managers as well as insurance undertakings and insurance intermediaries.

A “hard Brexit” by which access to the European single market is capped will most likely result in a loss of the “European Passport” for UK firms. Thus, firms will not be able to provide services on basis of UK licenses.

However, this guide has been prepared for the assistance of those interested in setting up a fully licensed subsidiary in Germany. It intends to answer some of the important, broad questions that may arise during the process. When specific problems occur in practice, it will often be necessary to obtain appropriate professional advice.

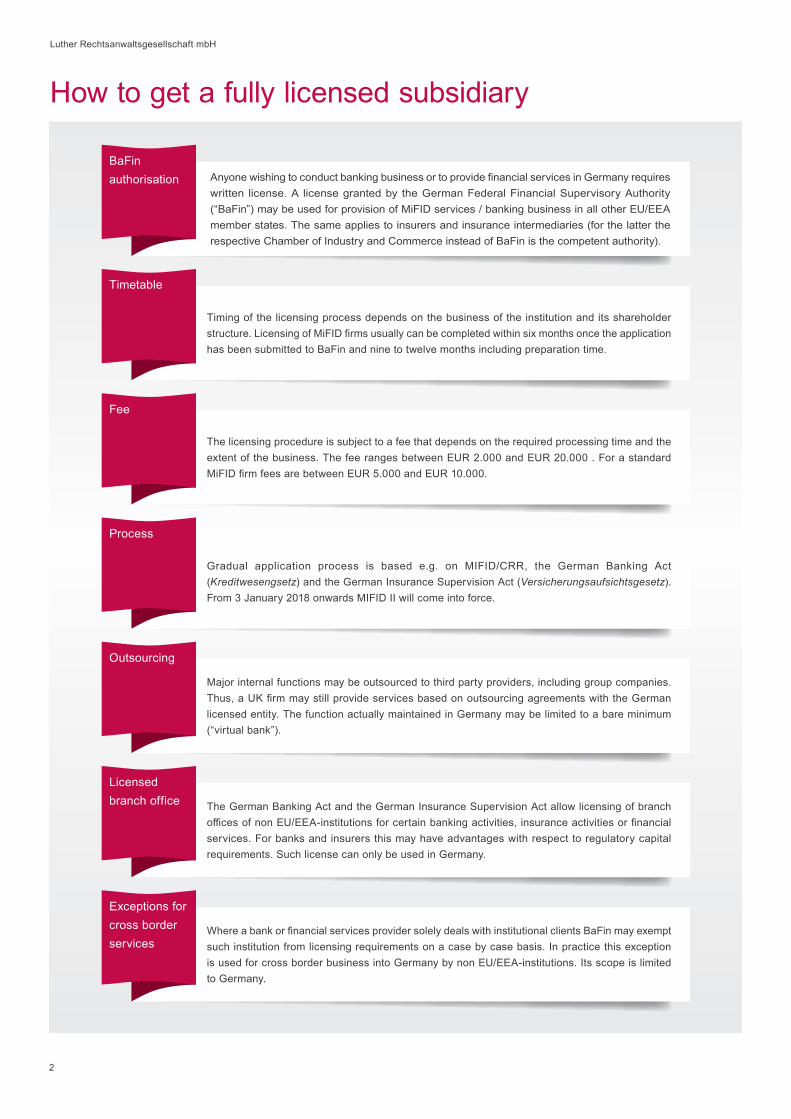

How to get a fully licensed subsidiary

Anyone wishing to conduct banking business or to provide financial services in Germany requires written license. A license granted by the German Federal Financial Supervisory Authority (“BaFin”) may be used for provision of MiFID services / banking business in all other EU/EEA member states. The same applies to insurers and insurance intermediaries (for the latter the respective Chamber of Industry and Commerce instead of BaFin is the competent authority).

BaFin authorisation

Timing of the licensing process depends on the business of the institution and its shareholder structure. Licensing of MiFID firms usually can be completed within six months once the application has been submitted to BaFin and nine to twelve months including preparation time.

Timetable

The licensing procedure is subject to a fee that depends on the required processing time and the extent of the business. The fee ranges between EUR 2.000 and EUR 20.000 . For a standard MiFID firm fees are between EUR 5.000 and EUR 10.000.

Fee

Gradual application process is based e.g. on MIFID/CRR, the German Banking Act (Kreditwesengsetz) and the German Insurance Supervision Act (Versicherungsaufsichtsgesetz). From 3 January 2018 onwards MIFID II will come into force.

Process

Major internal functions may be outsourced to third party providers, including group companies. Thus, a UK firm may still provide services based on outsourcing agreements with the German licensed entity. The function actually maintained in Germany may be limited to a bare minimum (“virtual bank”).

Outsourcing

The German Banking Act and the German Insurance Supervision Act allow licensing of branch offices of non EU/EEA-institutions for certain banking activities, insurance activities or financial services. For banks and insurers this may have advantages with respect to regulatory capital requirements. Such license can only be used in Germany.

Licensed branch office

Where a bank or financial services provider solely deals with institutional clients BaFin may exempt such institution from licensing requirements on a case by case basis. In practice this exception is used for cross border business into Germany by non EU/EEA-institutions. Its scope is limited to Germany.

Exceptions for cross border services

Luther Rechtsanwaltsgesellschaft mbH

2

Corporate requirements

Financial services institutions must be established as a corporation. Almost all German companies are limited liability companies (GmbHs) or stock corporations (AGs).

AG: The AG is a publicly held company comparable to the Public Limited Company (plc) in the United Kingdom.

The capital minimum requirement is EUR 50.000.

The AG has to have at least one director. AGs with a share capital of more than EUR 3m. have to appoint at least two directors if no exemption has been included in the constitution.

GmbH: The GmbH is a privately held company comparable to the Limited Liability Company (Ltd) in the United Kingdom.

The capital minimum requirement is EUR 25.000. One director is sufficient.

The shares of an AG may be publicly traded on a stock exchange, whereas those of a GmbH may not.

Tax

Corporate income tax: German resident companies are subject to corporate income tax (CIT) on their worldwide profits, but double tax treaties (DTT, ‘Doppelbesteuerungsabkommen’) might restrict this local taxation right.

Municipal trade tax: Municipal trade tax is also levied on income with some adjustments.

Tax rates: Germany does not have a nationally consistent total income tax burden level, depending instead on locally set varying trade tax levels. The German income tax rate for corporations is 25-33%.

Dividend distribution: Under UK-German DTT a reduction of taxes to be withheld down to 5% is possible. Under the EU Parent Subsidiary Directive even a full exemption from withholding taxes is possible. Currently, it is unclear if the Directive can still be applied after Brexit.

Transfer pricing: For cross-border transactions, transfer pricing documentation needs to be prepared in order to ensure

tax deductibility of expenses and to minimize the risk of future income adjustments.

Data protection

Legislation is based on EU Directives, but national German Data Protection Law applies accordingly. Exchange of data to countries outside the European Economic Area requires specific guarantees. EU General Data Protection Regulation will apply from 25 May 2018.

Employment law

Statutes and general information: In Germany a great number of fragmented statutes exist, which set minimum standards. The level of protection provided by the German labor statutes is relatively high, e.g. a high degree of protection against dismissal, high health and safety standards and various participation rights.

Social insurance: The main components of German’s social security system are retirement insurance, unemployment insurance, employee accident insurance and health insurance. The employees and the employer each pay half of the contributions to social insurance, except for accident insurance, which is financed by the employer alone. The amount of these joint contributions depends upon the gross income of the individual employee. It amounts to around 40% of the gross salary, about 20% for the employee and the employer.

Minimum wage: Since 1st January 2015 a general minimum wage of EUR 8,50 per hour applies to the employees in Germany. From 2017 onwards the minimum wage will be EUR 8,84 per hour. The minimum wage commission is going to revise the minimum wage every 2 years.

Works council: Each business regularly employing five or more persons has to allow its employees to establish a works council, but the formation is not mandatory. A works council is an organization representing workers in discussions with the employer. It has its own rights, e.g. codetermination rights, participation rights, including information and consultation rights.

Corporate codetermination: Corporate codetermination is codetermination through the supervisory board (Aufsichtsrat). It oversees officers and is e.g. responsible for appointing and dismissing the managing directors.

3

0

Our locations

Brussels

Luxembourg Singapore

ShanghaiYangon

Our international offices in important European and Asian markets

Our offices in Germany

BerlinCologneDusseldorfEssenFrankfurt a. M.HamburgHanoverLeipzigMunichStuttgart

London

Luther Rechtsanwaltsgesellschaft mbH

4

0

Our locations

Brussels

Luxembourg Singapore

ShanghaiYangon

Our international offices in important European and Asian markets

Our offices in Germany

BerlinCologneDusseldorfEssenFrankfurt a. M.HamburgHanoverLeipzigMunichStuttgart

London

Key contacts

London

Luxembourg

Corporate

Employment law

Dr. Thomas KuhnlePartnerLondon/StuttgartPhone +49 711 9338 [email protected]

York-Alexander von MassenbachLondonPhone +44 207 002 53 48york-alexander.von.massenbach@ luther-lawfirm.com

Dr. Klaus Schaffner PartnerLeipzigPhone +49 341 5299 [email protected]

Prof. Dr. Robert von Steinau-SteinrückPartnerBerlinPhone +49 30 52133 [email protected]

Capital market

Banking/Finance

Tax

Data protection

Insurance law

Dr. Jörgen Tielmann LL.M.PartnerHamburgPhone +49 40 18067 [email protected]

Ingo WegerichPartnerFrankfurt a.M.Phone +49 69 27229 [email protected]

Dr. Rolf KobabePartnerHamburgPhone +49 40 18067 [email protected]

Ulrich SiegemundPartnerFrankfurt a.M.Phone +49 69 27229 [email protected]

Silvia C. BauerPartnerColognePhone +49 221 9937 [email protected]

Dr. Alexander Mönnig E.M.L.E., LL.M. (Manchester)CounselHamburgPhone +49 40 18067 [email protected]

Hervé Leclercq PartnerLuxembourgPhone +352 27484 [email protected]

Legal and Tax Advice | www.luther-lawfirm.com1703

17