Pros and Cons of Bank Holding Companies:...

55

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. Presenting a live 90-minute webinar with interactive Q&A Pros and Cons of Bank Holding Companies: Determining Whether a Bank Holding Company Structure Makes Sense for Your Bank Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific THURSDAY, OCTOBER 12, 2017 Robert D. Klingler, Partner, Bryan Cave, Atlanta Clifford S. Stanford, Partner, Alston & Bird, Atlanta

Transcript of Pros and Cons of Bank Holding Companies:...

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Pros and Cons of Bank Holding Companies:

Determining Whether a Bank Holding

Company Structure Makes Sense for Your Bank

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, OCTOBER 12, 2017

Robert D. Klingler, Partner, Bryan Cave, Atlanta

Clifford S. Stanford, Partner, Alston & Bird, Atlanta

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Pros & Cons of Bank Holding Companies

Determining Whether a Bank Holding Company

Structure Makes Sense for Your Bank

October 12, 2017

Robert Klingler, Bryan Cave LLP

Cliff Stanford, Alston & Bird

Why are we discussing this?

6

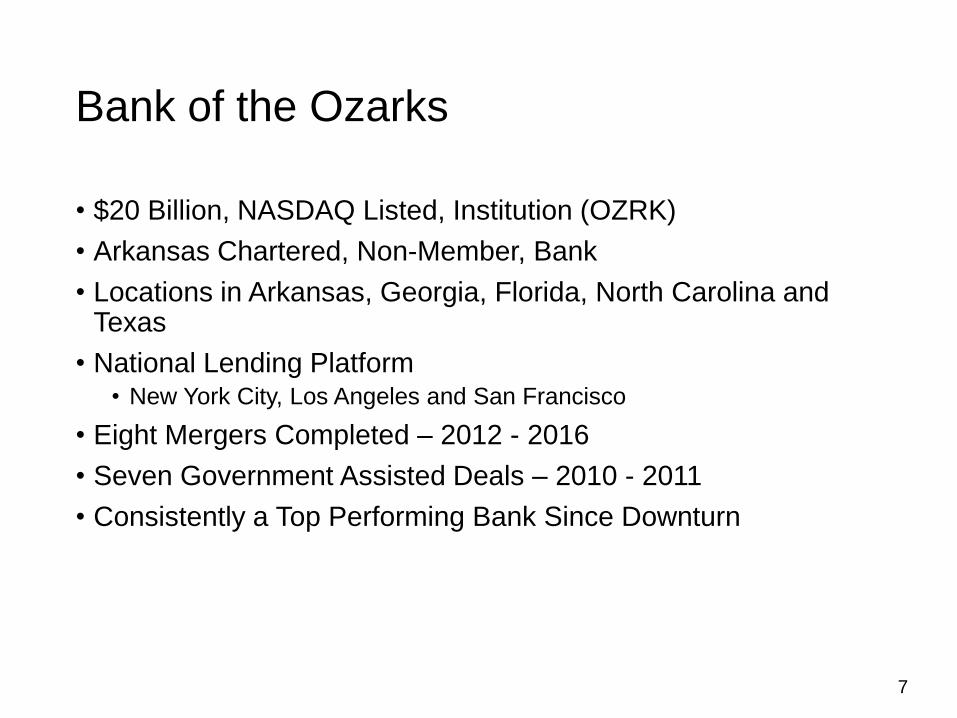

• $20 Billion, NASDAQ Listed, Institution (OZRK)

• Arkansas Chartered, Non-Member, Bank

• Locations in Arkansas, Georgia, Florida, North Carolina and Texas

• National Lending Platform • New York City, Los Angeles and San Francisco

• Eight Mergers Completed – 2012 - 2016

• Seven Government Assisted Deals – 2010 - 2011

• Consistently a Top Performing Bank Since Downturn

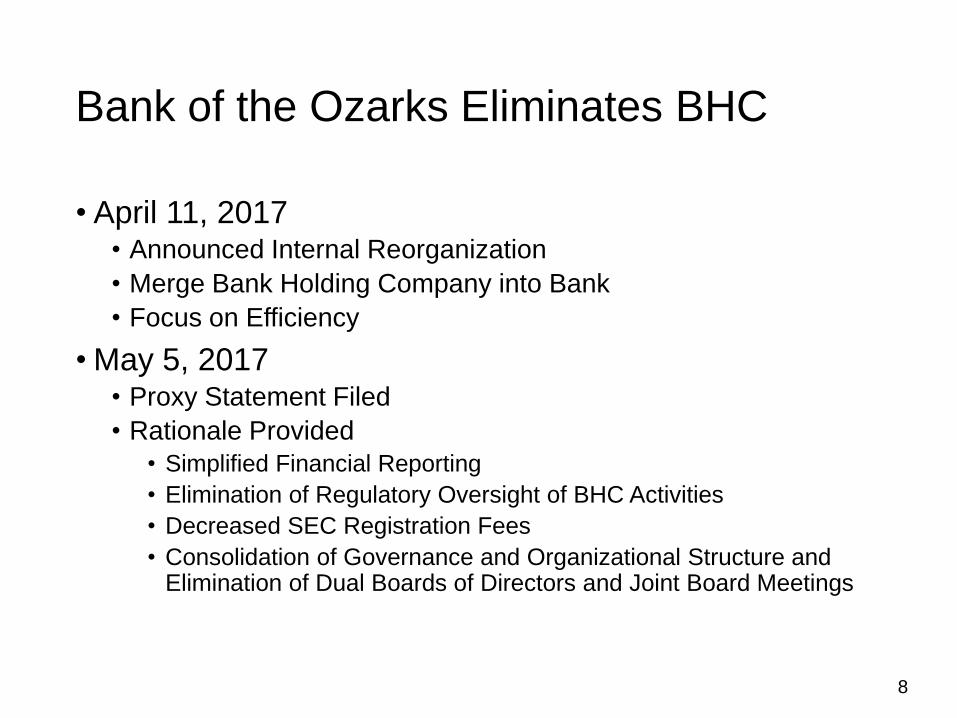

Bank of the Ozarks

7

• April 11, 2017 • Announced Internal Reorganization

• Merge Bank Holding Company into Bank

• Focus on Efficiency

• May 5, 2017 • Proxy Statement Filed

• Rationale Provided

• Simplified Financial Reporting

• Elimination of Regulatory Oversight of BHC Activities

• Decreased SEC Registration Fees

• Consolidation of Governance and Organizational Structure and Elimination of Dual Boards of Directors and Joint Board Meetings

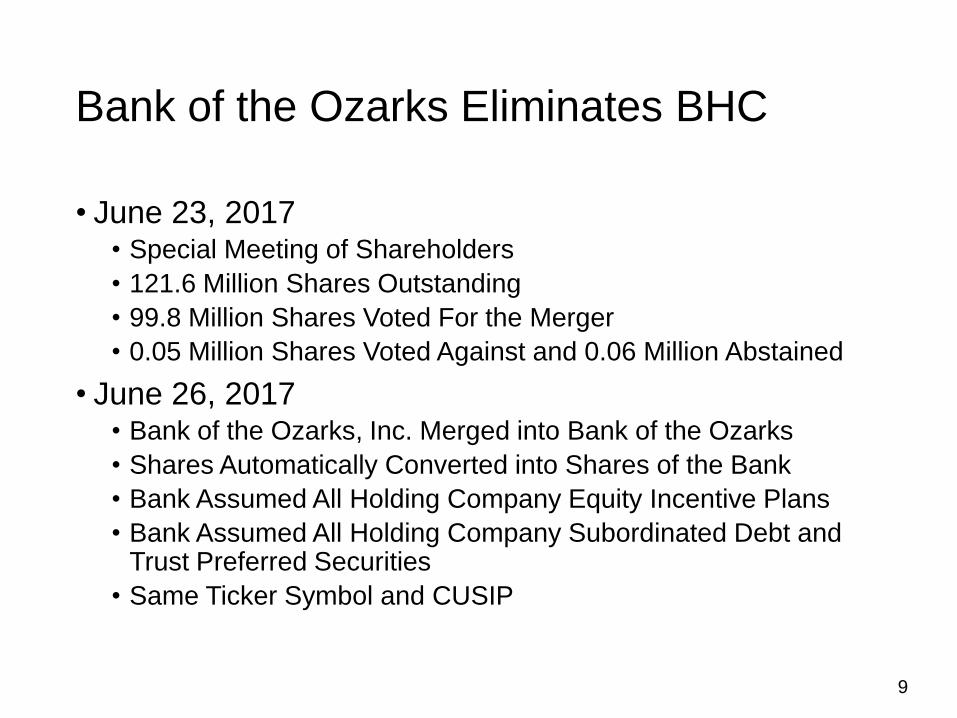

Bank of the Ozarks Eliminates BHC

8

• June 23, 2017 • Special Meeting of Shareholders

• 121.6 Million Shares Outstanding

• 99.8 Million Shares Voted For the Merger

• 0.05 Million Shares Voted Against and 0.06 Million Abstained

• June 26, 2017 • Bank of the Ozarks, Inc. Merged into Bank of the Ozarks

• Shares Automatically Converted into Shares of the Bank

• Bank Assumed All Holding Company Equity Incentive Plans

• Bank Assumed All Holding Company Subordinated Debt and Trust Preferred Securities

• Same Ticker Symbol and CUSIP

Bank of the Ozarks Eliminates BHC

9

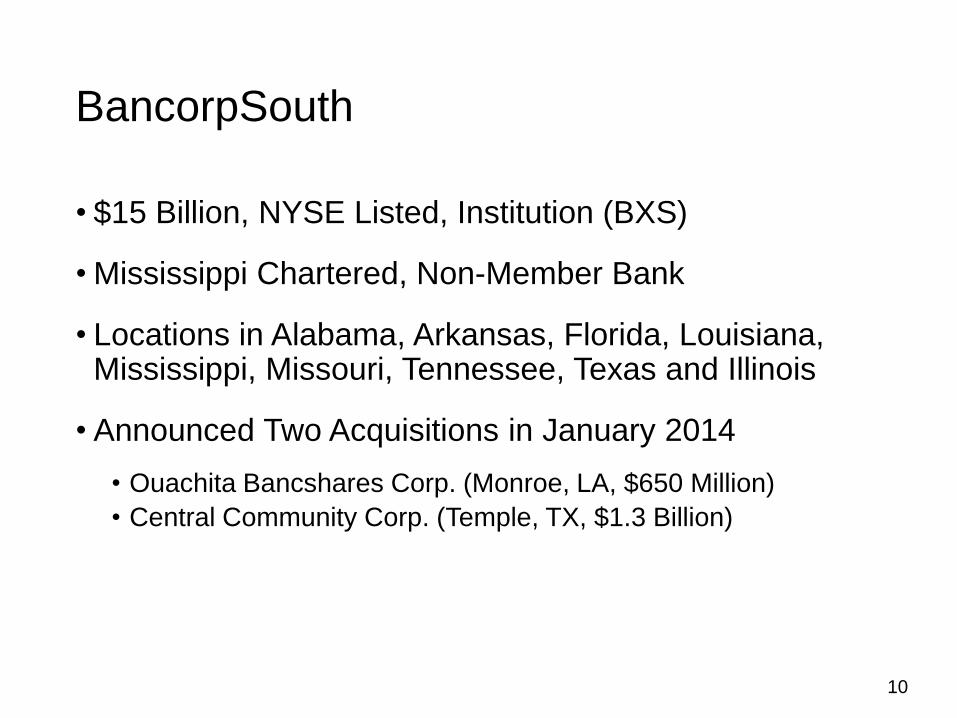

• $15 Billion, NYSE Listed, Institution (BXS)

• Mississippi Chartered, Non-Member Bank

• Locations in Alabama, Arkansas, Florida, Louisiana, Mississippi, Missouri, Tennessee, Texas and Illinois

• Announced Two Acquisitions in January 2014

• Ouachita Bancshares Corp. (Monroe, LA, $650 Million)

• Central Community Corp. (Temple, TX, $1.3 Billion)

BancorpSouth

10

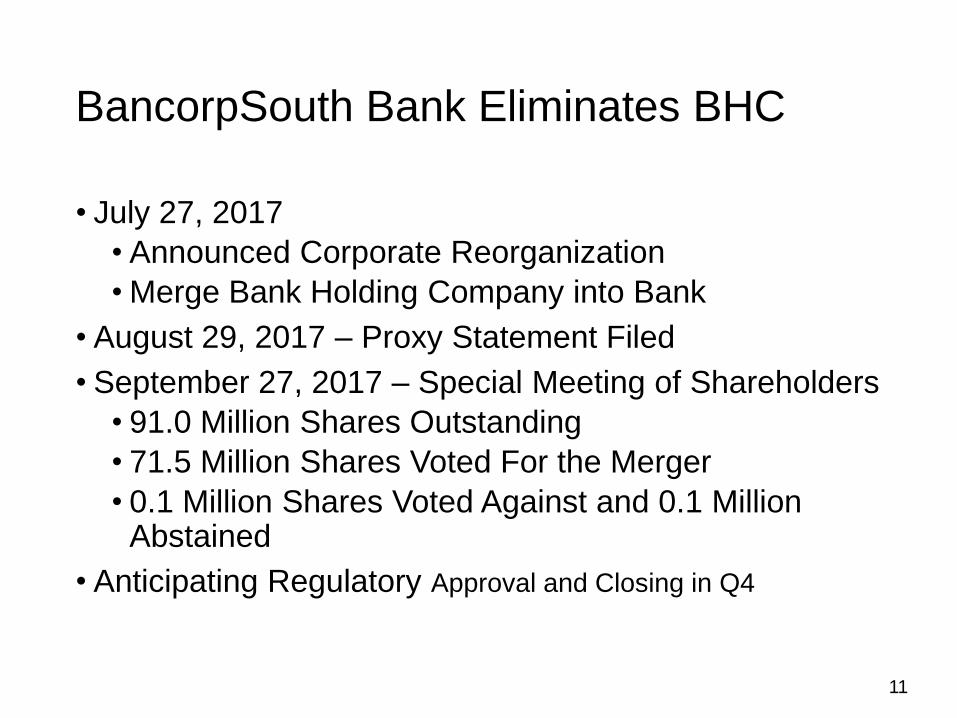

• July 27, 2017

• Announced Corporate Reorganization

• Merge Bank Holding Company into Bank

• August 29, 2017 – Proxy Statement Filed

• September 27, 2017 – Special Meeting of Shareholders

• 91.0 Million Shares Outstanding

• 71.5 Million Shares Voted For the Merger

• 0.1 Million Shares Voted Against and 0.1 Million Abstained

• Anticipating Regulatory Approval and Closing in Q4

BancorpSouth Bank Eliminates BHC

11

Framing the Discussion

12

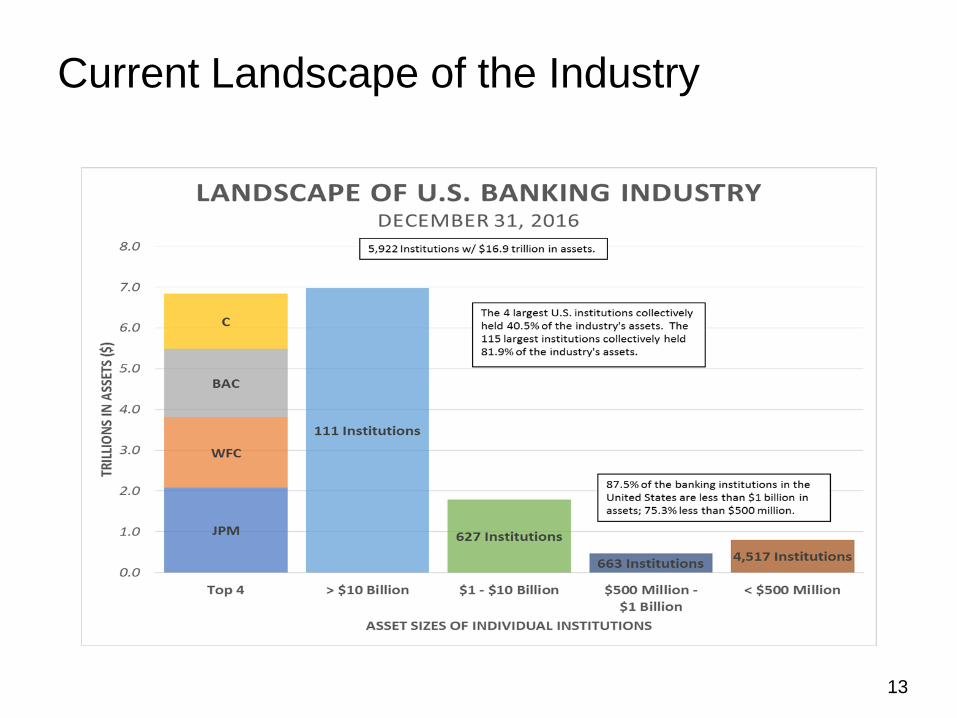

Current Landscape of the Industry

13

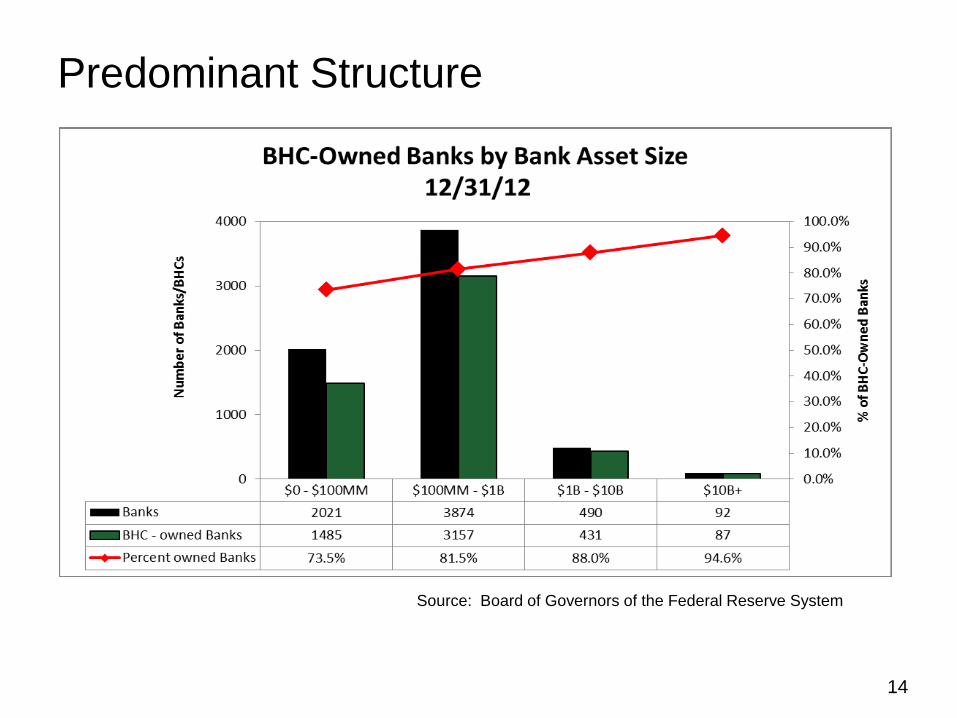

Predominant Structure

Source: Board of Governors of the Federal Reserve System

14

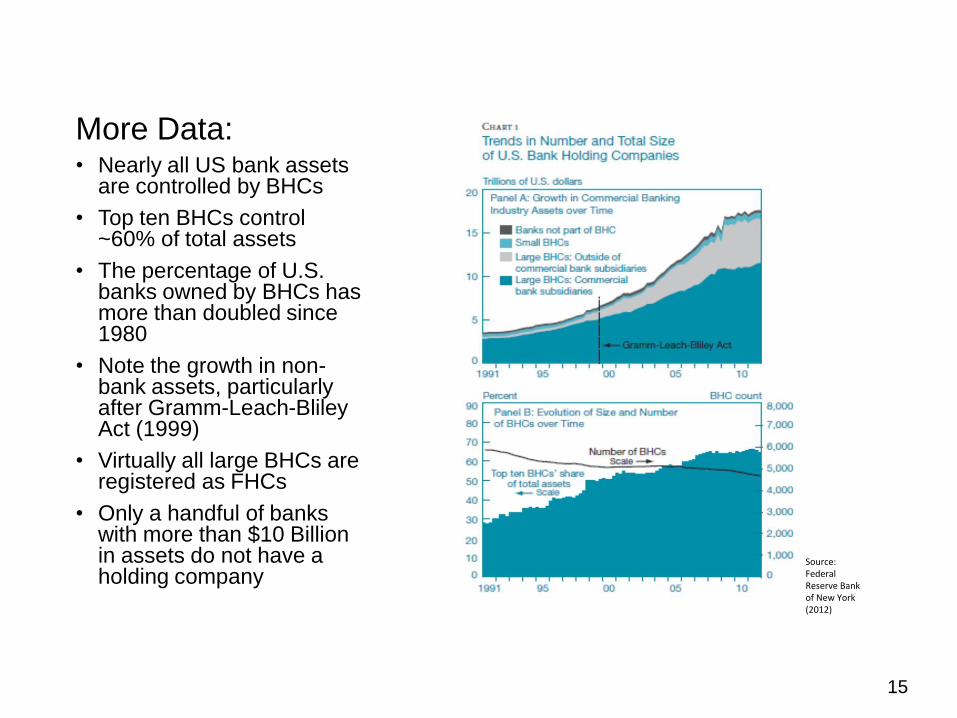

More Data: • Nearly all US bank assets

are controlled by BHCs

• Top ten BHCs control ~60% of total assets

• The percentage of U.S. banks owned by BHCs has more than doubled since 1980

• Note the growth in non-bank assets, particularly after Gramm-Leach-Bliley Act (1999)

• Virtually all large BHCs are registered as FHCs

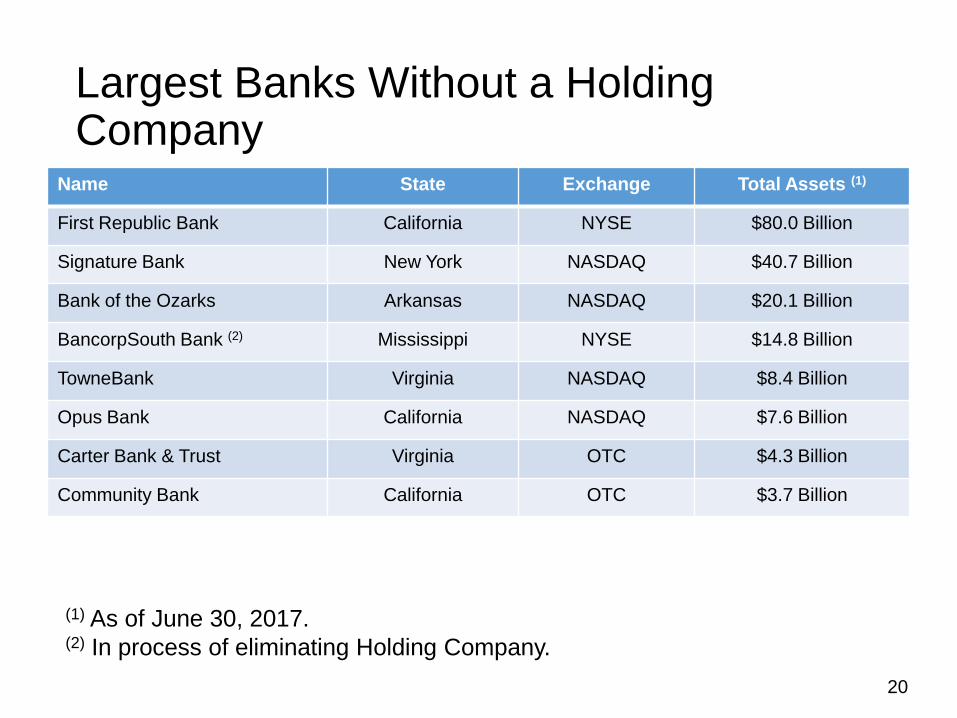

• Only a handful of banks with more than $10 Billion in assets do not have a holding company

Source: Federal Reserve Bank of New York (2012)

15

• Above $10 Billion

– 115 Banks; 4 without a Holding Company

• Above $1 Billion

– Over 93% Have Holding Companies

• Below $1 Billion

– Over 82% Have Holding Companies

• As of June 30, 2017

– 562 Independent Banks (<$0.2 Trillion)

– 3,847 One Bank Holding Companies ($5.9 Trillion)

– 602 Banks / 231 Multi Bank Holding Companies ($9.9 Trillion)

– 776 Federal and State Savings Associations ($1.2 Trillion)

Bank Holding Companies Remain Common

16

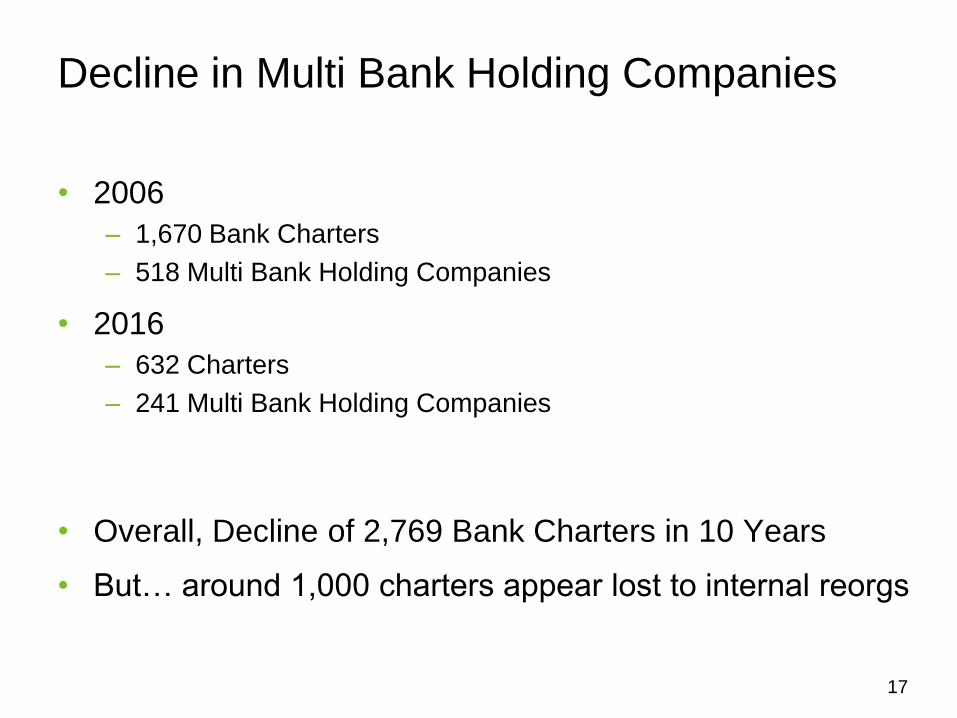

• 2006

– 1,670 Bank Charters

– 518 Multi Bank Holding Companies

• 2016

– 632 Charters

– 241 Multi Bank Holding Companies

• Overall, Decline of 2,769 Bank Charters in 10 Years

• But… around 1,000 charters appear lost to internal reorgs

Decline in Multi Bank Holding Companies

17

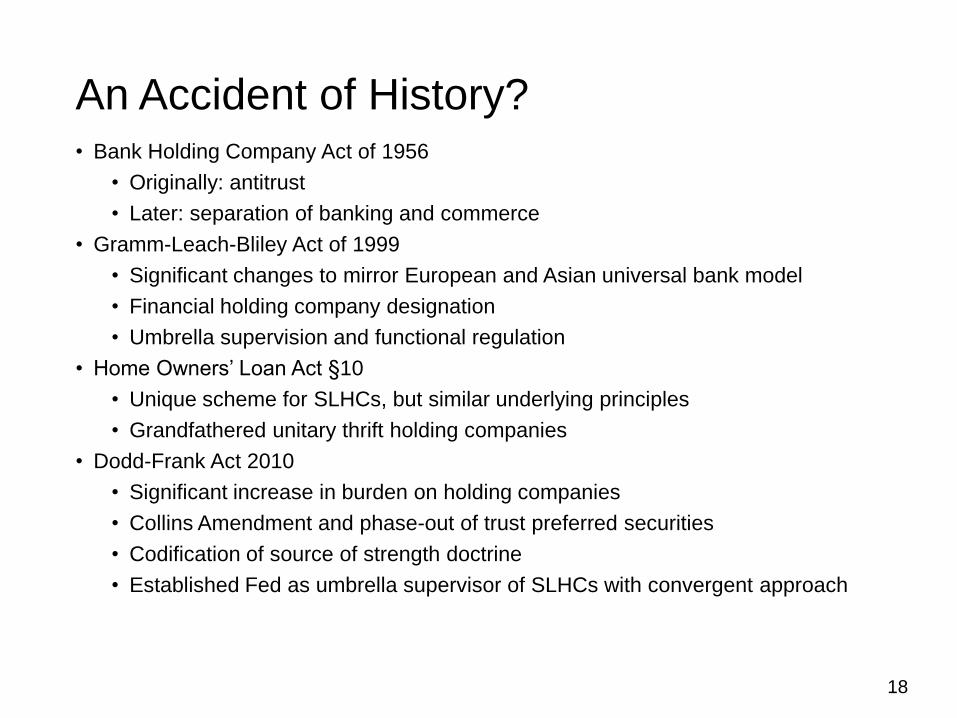

An Accident of History? • Bank Holding Company Act of 1956

• Originally: antitrust

• Later: separation of banking and commerce

• Gramm-Leach-Bliley Act of 1999

• Significant changes to mirror European and Asian universal bank model

• Financial holding company designation

• Umbrella supervision and functional regulation

• Home Owners’ Loan Act §10

• Unique scheme for SLHCs, but similar underlying principles

• Grandfathered unitary thrift holding companies

• Dodd-Frank Act 2010

• Significant increase in burden on holding companies

• Collins Amendment and phase-out of trust preferred securities

• Codification of source of strength doctrine

• Established Fed as umbrella supervisor of SLHCs with convergent approach

18

Challenging Assumptions

19

Name State Exchange Total Assets (1)

First Republic Bank California NYSE $80.0 Billion

Signature Bank New York NASDAQ $40.7 Billion

Bank of the Ozarks Arkansas NASDAQ $20.1 Billion

BancorpSouth Bank (2) Mississippi NYSE $14.8 Billion

TowneBank Virginia NASDAQ $8.4 Billion

Opus Bank California NASDAQ $7.6 Billion

Carter Bank & Trust Virginia OTC $4.3 Billion

Community Bank California OTC $3.7 Billion

Largest Banks Without a Holding Company

(1) As of June 30, 2017. (2) In process of eliminating Holding Company.

20

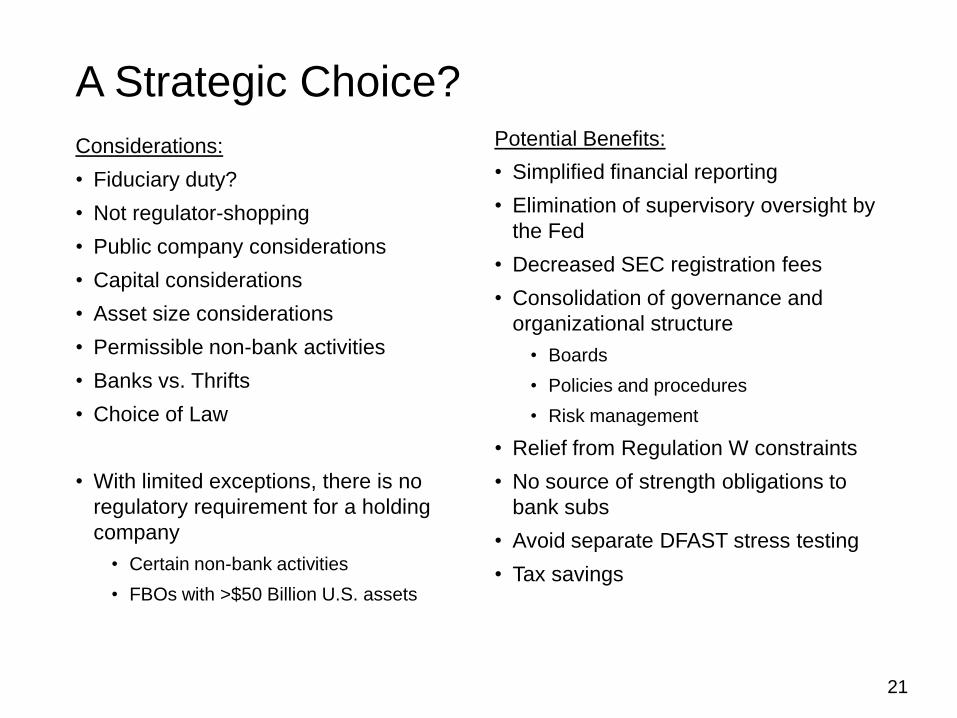

A Strategic Choice?

Considerations:

• Fiduciary duty?

• Not regulator-shopping

• Public company considerations

• Capital considerations

• Asset size considerations

• Permissible non-bank activities

• Banks vs. Thrifts

• Choice of Law

• With limited exceptions, there is no

regulatory requirement for a holding

company

• Certain non-bank activities

• FBOs with >$50 Billion U.S. assets

Potential Benefits:

• Simplified financial reporting

• Elimination of supervisory oversight by

the Fed

• Decreased SEC registration fees

• Consolidation of governance and

organizational structure

• Boards

• Policies and procedures

• Risk management

• Relief from Regulation W constraints

• No source of strength obligations to

bank subs

• Avoid separate DFAST stress testing

• Tax savings

21

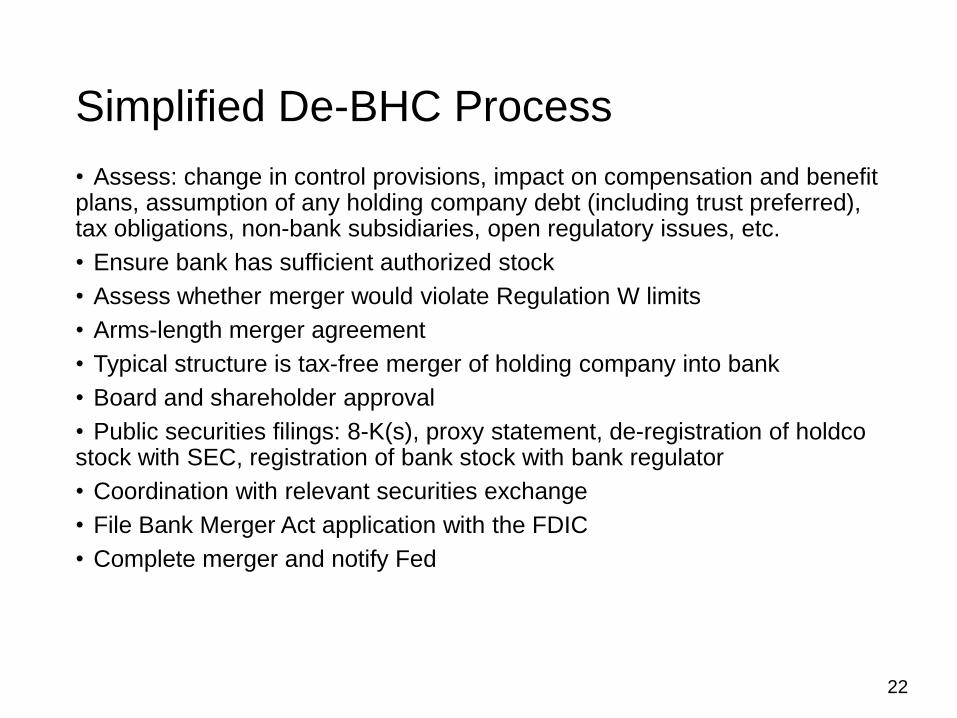

Simplified De-BHC Process

• Assess: change in control provisions, impact on compensation and benefit plans, assumption of any holding company debt (including trust preferred), tax obligations, non-bank subsidiaries, open regulatory issues, etc.

• Ensure bank has sufficient authorized stock

• Assess whether merger would violate Regulation W limits

• Arms-length merger agreement

• Typical structure is tax-free merger of holding company into bank

• Board and shareholder approval

• Public securities filings: 8-K(s), proxy statement, de-registration of holdco stock with SEC, registration of bank stock with bank regulator

• Coordination with relevant securities exchange

• File Bank Merger Act application with the FDIC

• Complete merger and notify Fed

22

M&A and Regulatory Impacts

23

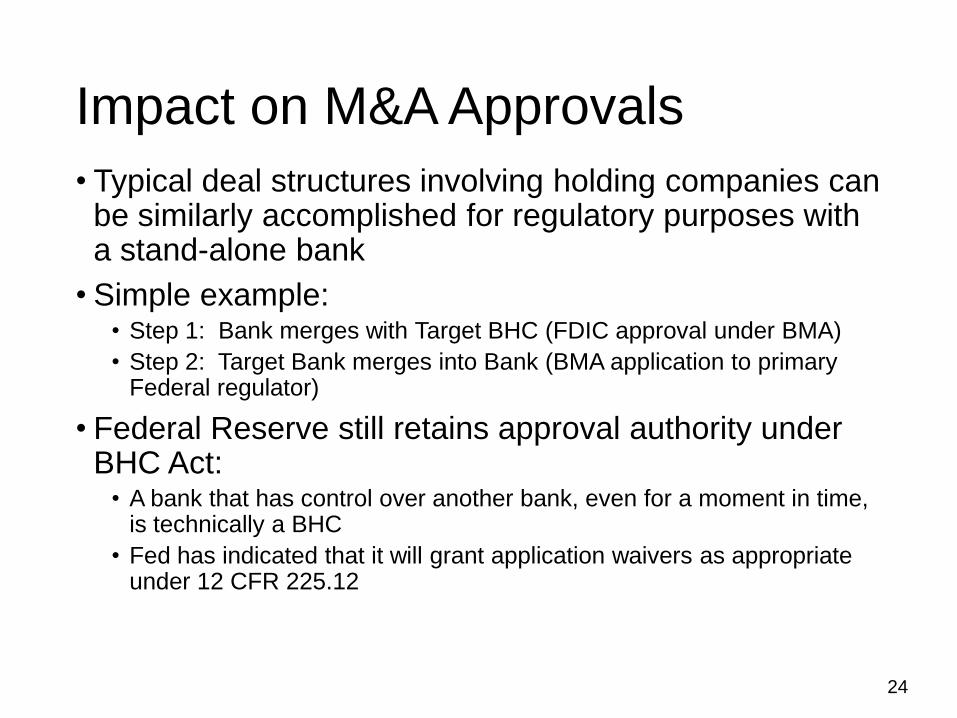

Impact on M&A Approvals

• Typical deal structures involving holding companies can be similarly accomplished for regulatory purposes with a stand-alone bank

• Simple example: • Step 1: Bank merges with Target BHC (FDIC approval under BMA)

• Step 2: Target Bank merges into Bank (BMA application to primary Federal regulator)

• Federal Reserve still retains approval authority under BHC Act:

• A bank that has control over another bank, even for a moment in time, is technically a BHC

• Fed has indicated that it will grant application waivers as appropriate under 12 CFR 225.12

24

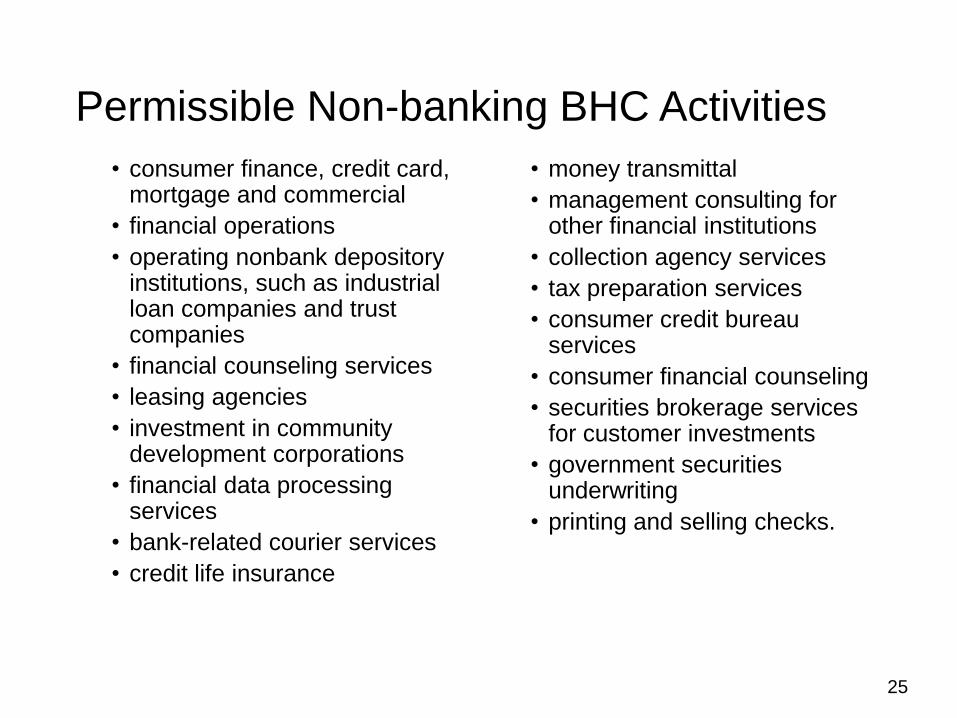

Permissible Non-banking BHC Activities

• consumer finance, credit card, mortgage and commercial

• financial operations

• operating nonbank depository institutions, such as industrial loan companies and trust companies

• financial counseling services

• leasing agencies

• investment in community development corporations

• financial data processing services

• bank-related courier services

• credit life insurance

• money transmittal

• management consulting for other financial institutions

• collection agency services

• tax preparation services

• consumer credit bureau services

• consumer financial counseling

• securities brokerage services for customer investments

• government securities underwriting

• printing and selling checks.

25

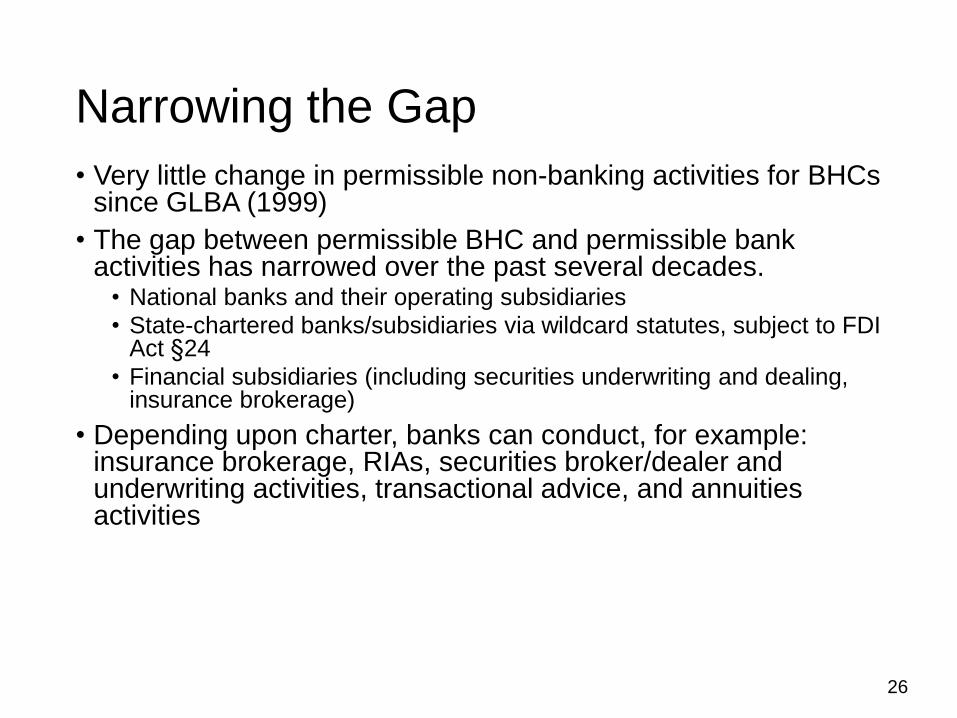

Narrowing the Gap

• Very little change in permissible non-banking activities for BHCs since GLBA (1999)

• The gap between permissible BHC and permissible bank activities has narrowed over the past several decades.

• National banks and their operating subsidiaries

• State-chartered banks/subsidiaries via wildcard statutes, subject to FDI Act §24

• Financial subsidiaries (including securities underwriting and dealing, insurance brokerage)

• Depending upon charter, banks can conduct, for example: insurance brokerage, RIAs, securities broker/dealer and underwriting activities, transactional advice, and annuities activities

26

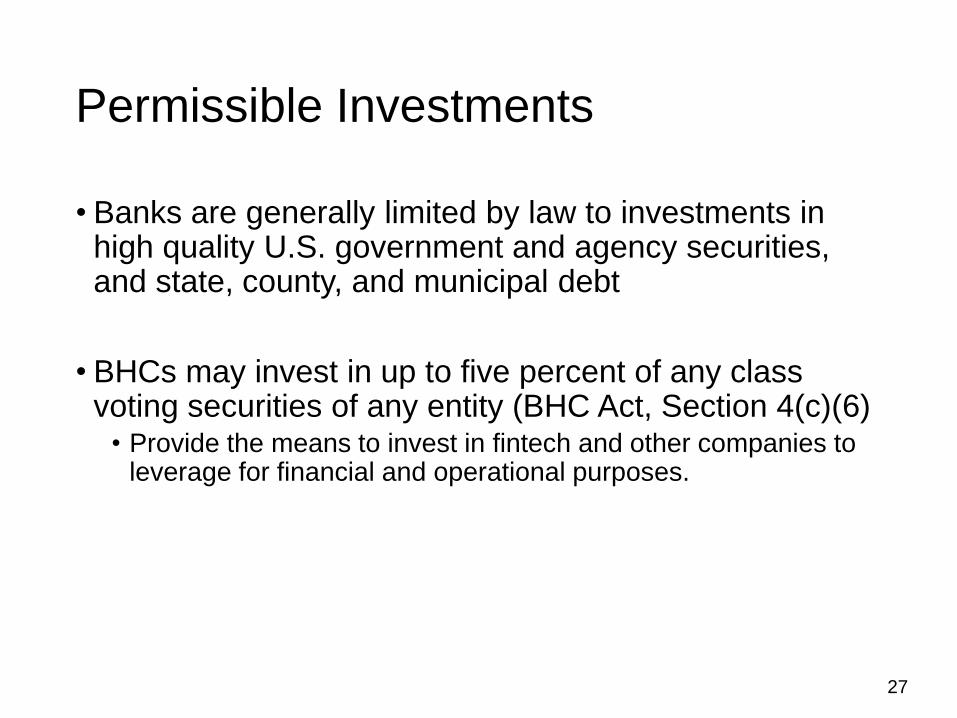

Permissible Investments

• Banks are generally limited by law to investments in high quality U.S. government and agency securities, and state, county, and municipal debt

• BHCs may invest in up to five percent of any class voting securities of any entity (BHC Act, Section 4(c)(6)

• Provide the means to invest in fintech and other companies to leverage for financial and operational purposes.

27

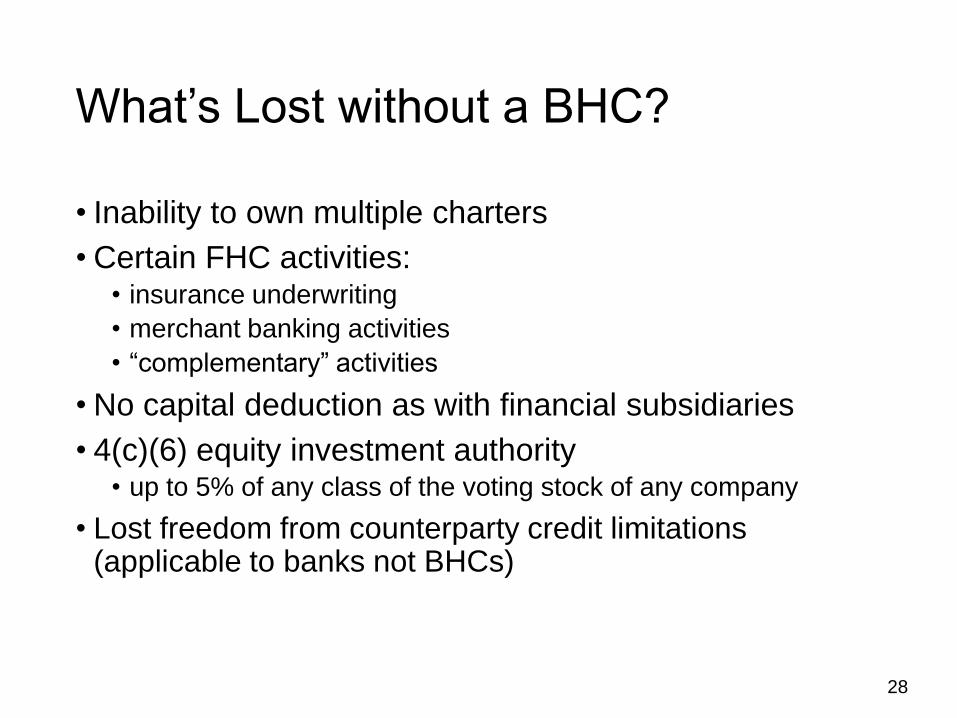

What’s Lost without a BHC?

• Inability to own multiple charters

• Certain FHC activities: • insurance underwriting

• merchant banking activities

• “complementary” activities

• No capital deduction as with financial subsidiaries

• 4(c)(6) equity investment authority • up to 5% of any class of the voting stock of any company

• Lost freedom from counterparty credit limitations (applicable to banks not BHCs)

28

Savings and Loan Holding Companies

• Unique scheme from BHCs, but convergence under Federal

Reserve authority

• SLHCs may engage in:

• Generally, anything permitted to a BHC

• Generally, anything permitted to a financial holding company (if so qualified)

• Certain other exempt activities under HOLA

• Grandfathered unitary SLHCs may engage in commercial activities

• Grandfathered multiple SLHCs have additional authority

• Thrifts have distinct non-banking authority

• Federal Savings Associations cannot own financial subsidiaries

29

23A/23B and Regulation W

• The merger of an affiliate (BHC) into the bank is a “purchase of assets” (and therefore a “covered transaction”) if the bank assumes any liabilities of the affiliate or pays any other form of consideration in the transaction.

• Therefore, the merger is subject to the quantitative limits under Regulation W

• Bank subsidiaries are not affiliates, unless “financial subsidiaries”

• But, 10% quantitative limit does not apply to financial subsidiaries

• Special valuation rules for contribution of financial subs or new investment

• Relief from Regulation W limits on transactions with affiliates can be a material consideration

30

Regulatory Reporting

• Without a BHC, the bank no longer files (as applicable, with frequency depending upon size and other characteristics):

• FR Y-9C, Consolidated Financial Statements of Bank Holding Companies

• FR Y-9LP/SP, Parent Company Only Financial Statements

• FR Y-11/FR Y-11S, Financial Statements of U.S. Nonbank Subsidiaries of U.S. Bank Holding Companies

• FR Y-6, Annual Report of Bank Holding Companies

• FR Y-10, Report of Changes in Organizational Structure (unless a state member bank, or regarding foreign activities of national banks)

31

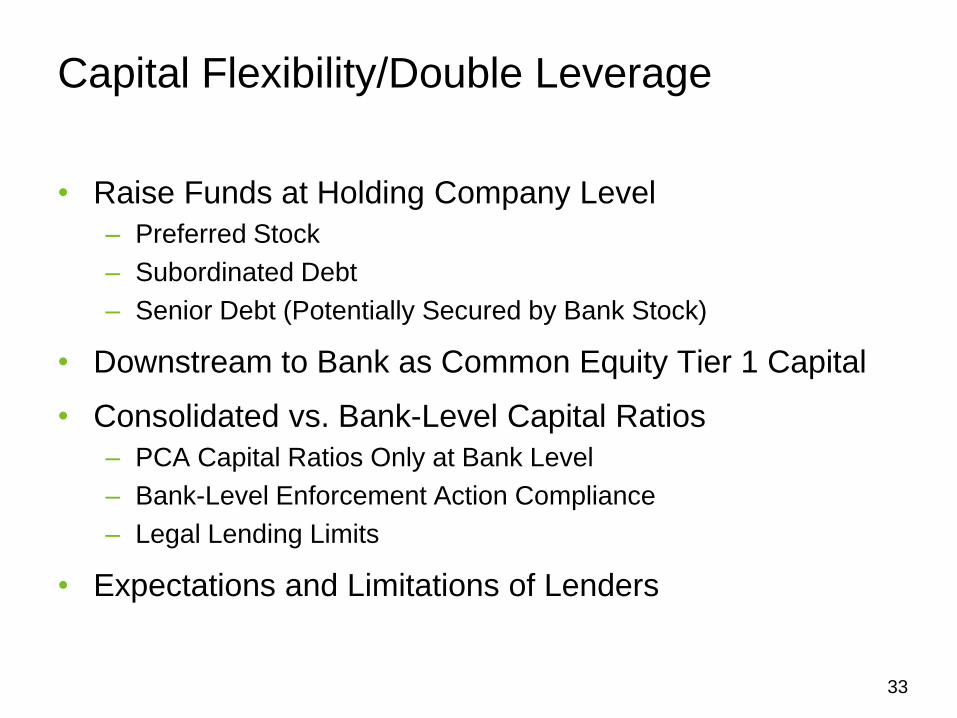

Capital Flexibility

32

• Raise Funds at Holding Company Level

– Preferred Stock

– Subordinated Debt

– Senior Debt (Potentially Secured by Bank Stock)

• Downstream to Bank as Common Equity Tier 1 Capital

• Consolidated vs. Bank-Level Capital Ratios

– PCA Capital Ratios Only at Bank Level

– Bank-Level Enforcement Action Compliance

– Legal Lending Limits

• Expectations and Limitations of Lenders

Capital Flexibility/Double Leverage

33

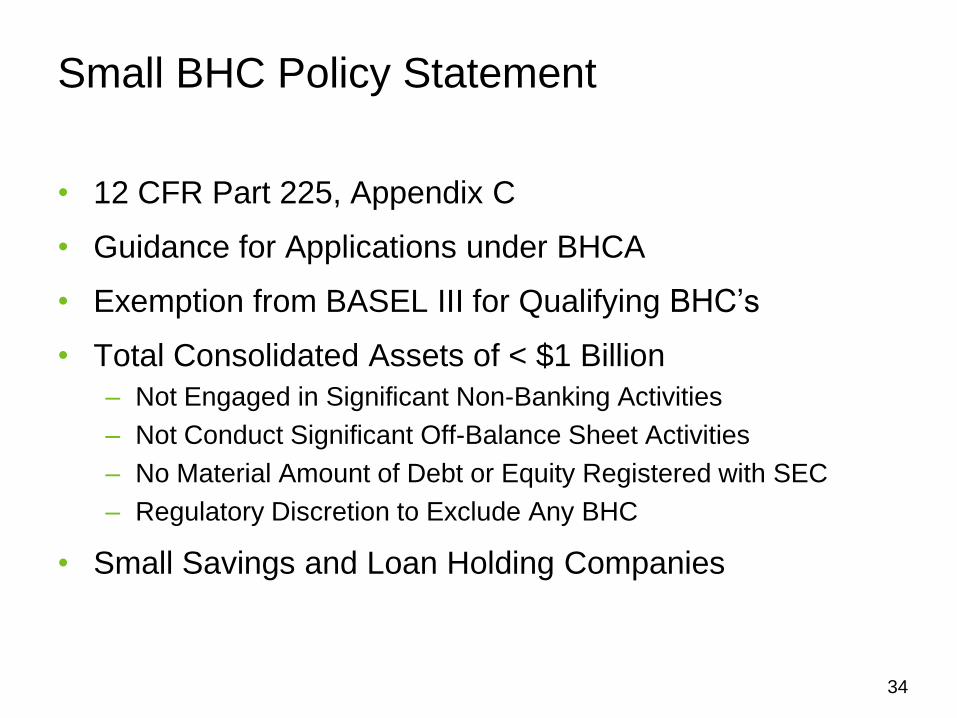

• 12 CFR Part 225, Appendix C

• Guidance for Applications under BHCA

• Exemption from BASEL III for Qualifying BHC’s

• Total Consolidated Assets of < $1 Billion

– Not Engaged in Significant Non-Banking Activities

– Not Conduct Significant Off-Balance Sheet Activities

– No Material Amount of Debt or Equity Registered with SEC

– Regulatory Discretion to Exclude Any BHC

• Small Savings and Loan Holding Companies

Small BHC Policy Statement

34

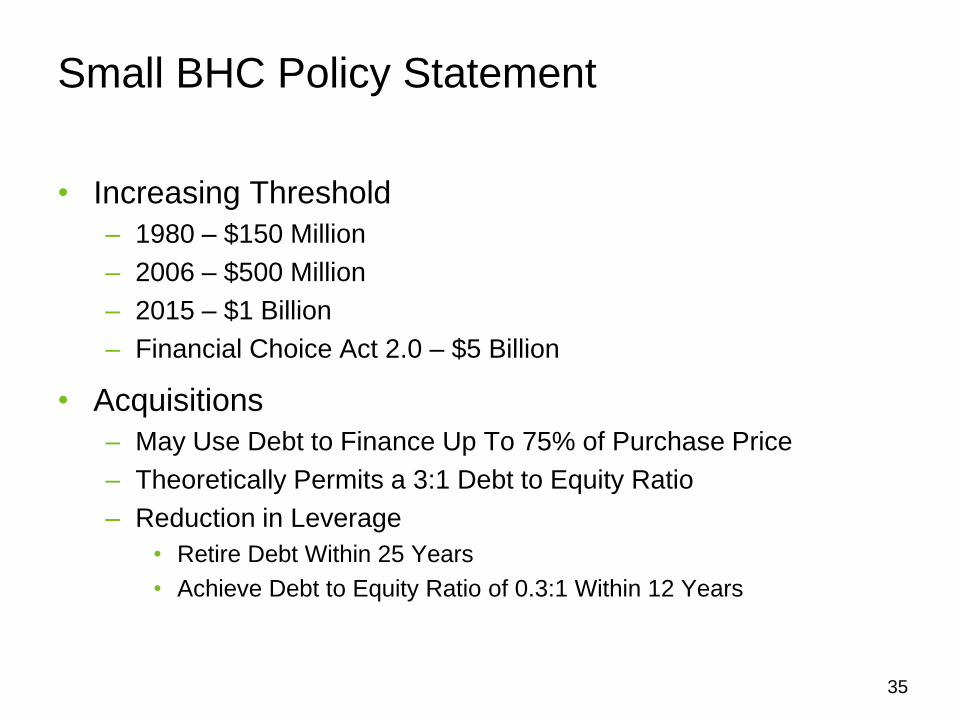

• Increasing Threshold

– 1980 – $150 Million

– 2006 – $500 Million

– 2015 – $1 Billion

– Financial Choice Act 2.0 – $5 Billion

• Acquisitions

– May Use Debt to Finance Up To 75% of Purchase Price

– Theoretically Permits a 3:1 Debt to Equity Ratio

– Reduction in Leverage

• Retire Debt Within 25 Years

• Achieve Debt to Equity Ratio of 0.3:1 Within 12 Years

Small BHC Policy Statement

35

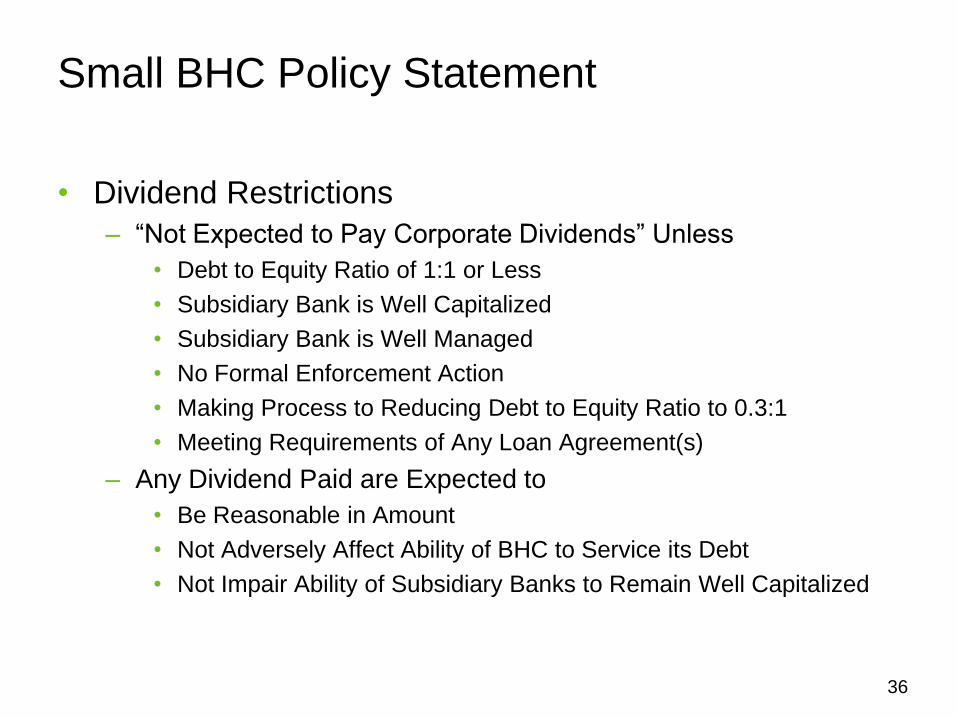

• Dividend Restrictions

– “Not Expected to Pay Corporate Dividends” Unless

• Debt to Equity Ratio of 1:1 or Less

• Subsidiary Bank is Well Capitalized

• Subsidiary Bank is Well Managed

• No Formal Enforcement Action

• Making Process to Reducing Debt to Equity Ratio to 0.3:1

• Meeting Requirements of Any Loan Agreement(s)

– Any Dividend Paid are Expected to

• Be Reasonable in Amount

• Not Adversely Affect Ability of BHC to Service its Debt

• Not Impair Ability of Subsidiary Banks to Remain Well Capitalized

Small BHC Policy Statement

36

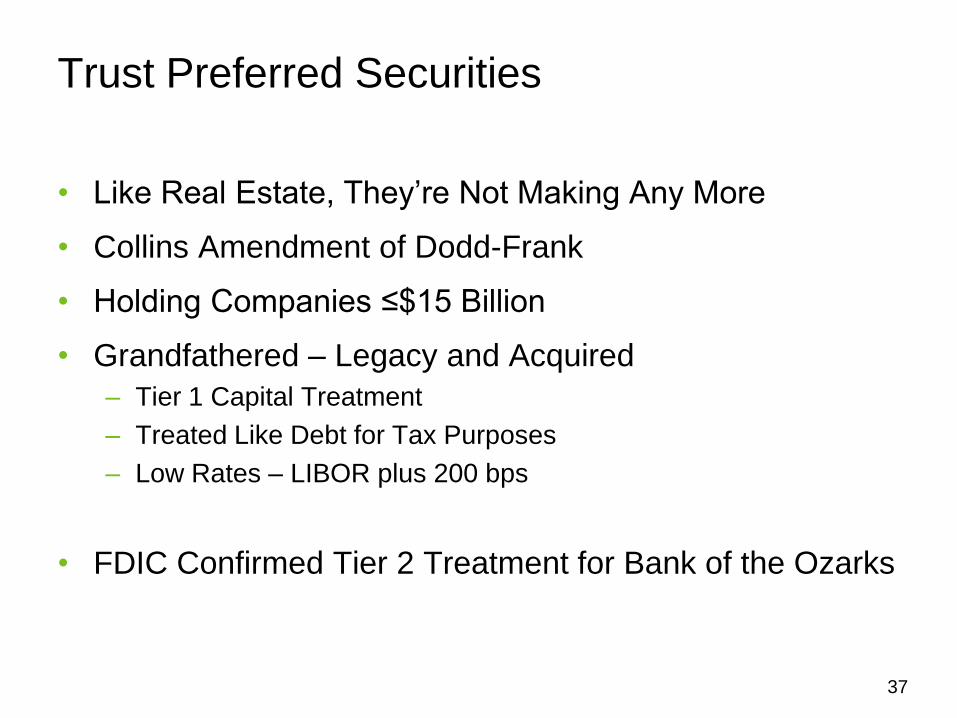

• Like Real Estate, They’re Not Making Any More

• Collins Amendment of Dodd-Frank

• Holding Companies ≤$15 Billion

• Grandfathered – Legacy and Acquired

– Tier 1 Capital Treatment

– Treated Like Debt for Tax Purposes

– Low Rates – LIBOR plus 200 bps

• FDIC Confirmed Tier 2 Treatment for Bank of the Ozarks

Trust Preferred Securities

37

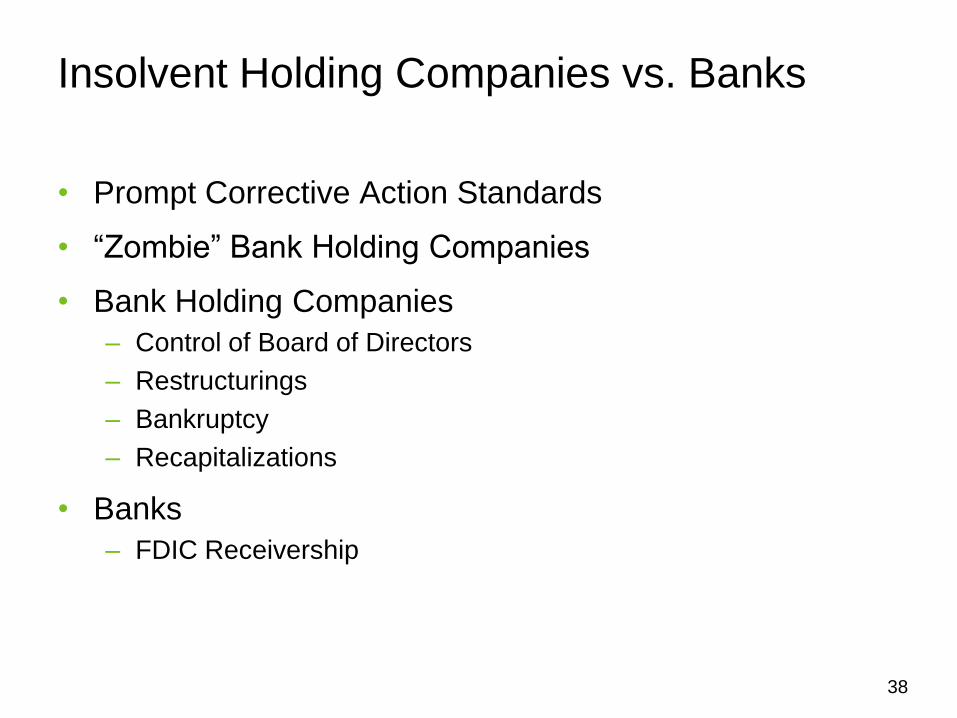

• Prompt Corrective Action Standards

• “Zombie” Bank Holding Companies

• Bank Holding Companies

– Control of Board of Directors

– Restructurings

– Bankruptcy

– Recapitalizations

• Banks

– FDIC Receivership

Insolvent Holding Companies vs. Banks

38

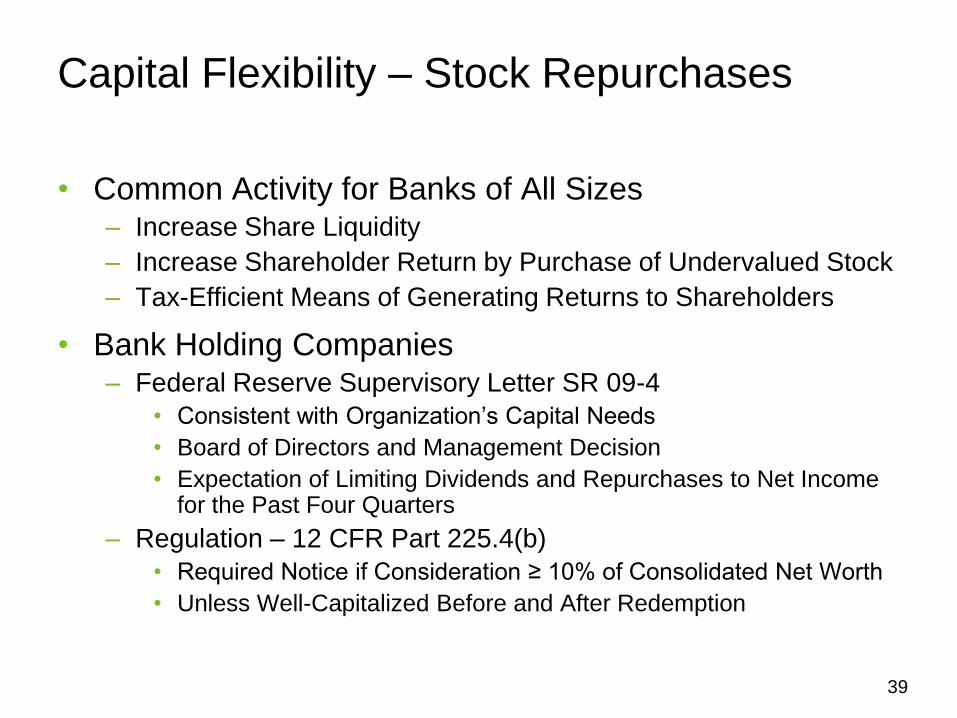

• Common Activity for Banks of All Sizes – Increase Share Liquidity

– Increase Shareholder Return by Purchase of Undervalued Stock

– Tax-Efficient Means of Generating Returns to Shareholders

• Bank Holding Companies – Federal Reserve Supervisory Letter SR 09-4

• Consistent with Organization’s Capital Needs

• Board of Directors and Management Decision

• Expectation of Limiting Dividends and Repurchases to Net Income for the Past Four Quarters

– Regulation – 12 CFR Part 225.4(b)

• Required Notice if Consideration ≥ 10% of Consolidated Net Worth

• Unless Well-Capitalized Before and After Redemption

Capital Flexibility – Stock Repurchases

39

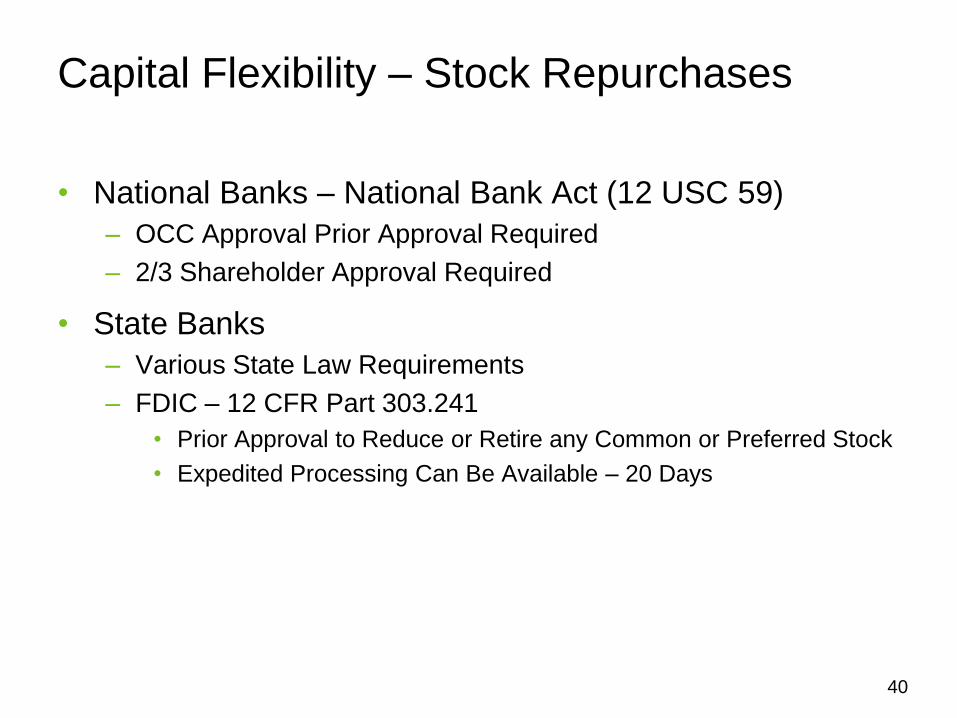

• National Banks – National Bank Act (12 USC 59)

– OCC Approval Prior Approval Required

– 2/3 Shareholder Approval Required

• State Banks

– Various State Law Requirements

– FDIC – 12 CFR Part 303.241

• Prior Approval to Reduce or Retire any Common or Preferred Stock

• Expedited Processing Can Be Available – 20 Days

Capital Flexibility – Stock Repurchases

40

Corporate Governance

41

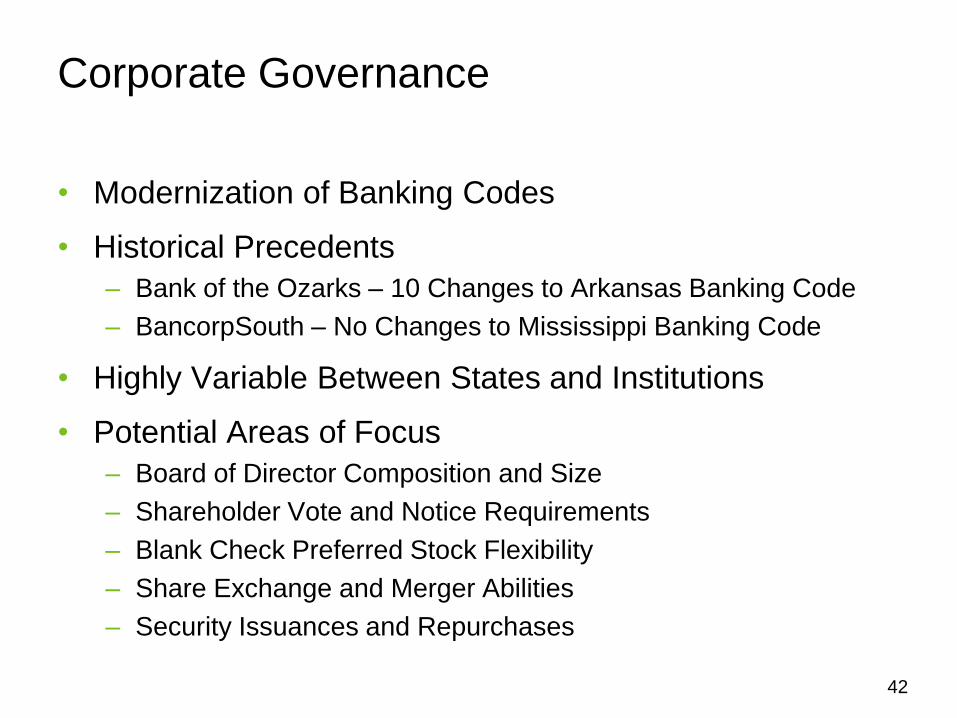

• Modernization of Banking Codes

• Historical Precedents

– Bank of the Ozarks – 10 Changes to Arkansas Banking Code

– BancorpSouth – No Changes to Mississippi Banking Code

• Highly Variable Between States and Institutions

• Potential Areas of Focus

– Board of Director Composition and Size

– Shareholder Vote and Notice Requirements

– Blank Check Preferred Stock Flexibility

– Share Exchange and Merger Abilities

– Security Issuances and Repurchases

Corporate Governance

42

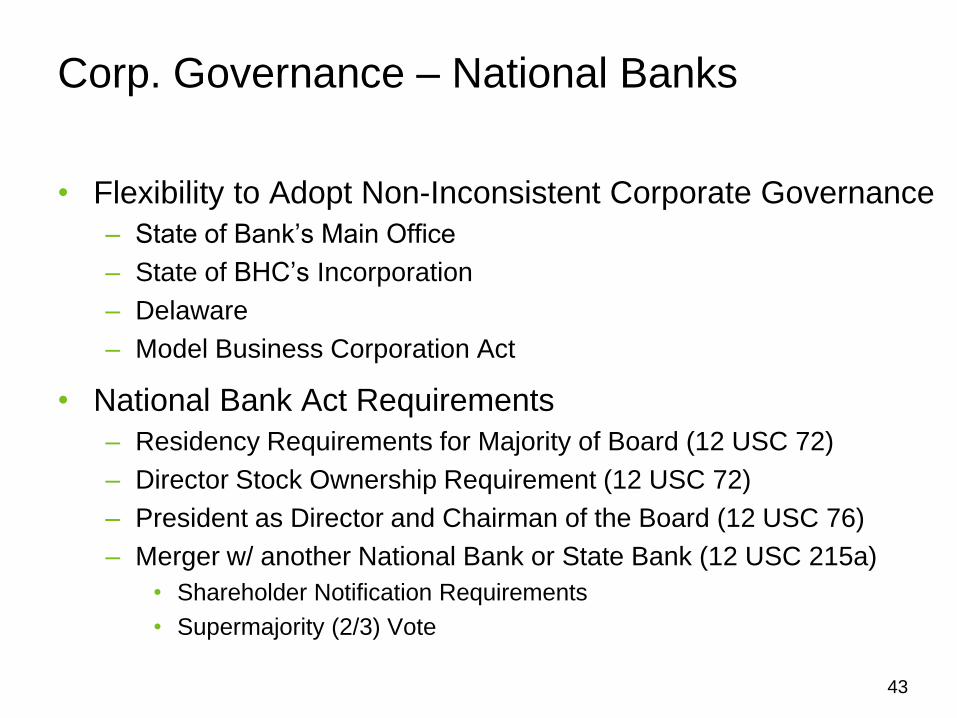

• Flexibility to Adopt Non-Inconsistent Corporate Governance

– State of Bank’s Main Office

– State of BHC’s Incorporation

– Delaware

– Model Business Corporation Act

• National Bank Act Requirements

– Residency Requirements for Majority of Board (12 USC 72)

– Director Stock Ownership Requirement (12 USC 72)

– President as Director and Chairman of the Board (12 USC 76)

– Merger w/ another National Bank or State Bank (12 USC 215a)

• Shareholder Notification Requirements

• Supermajority (2/3) Vote

Corp. Governance – National Banks

43

Shareholder Regulation

44

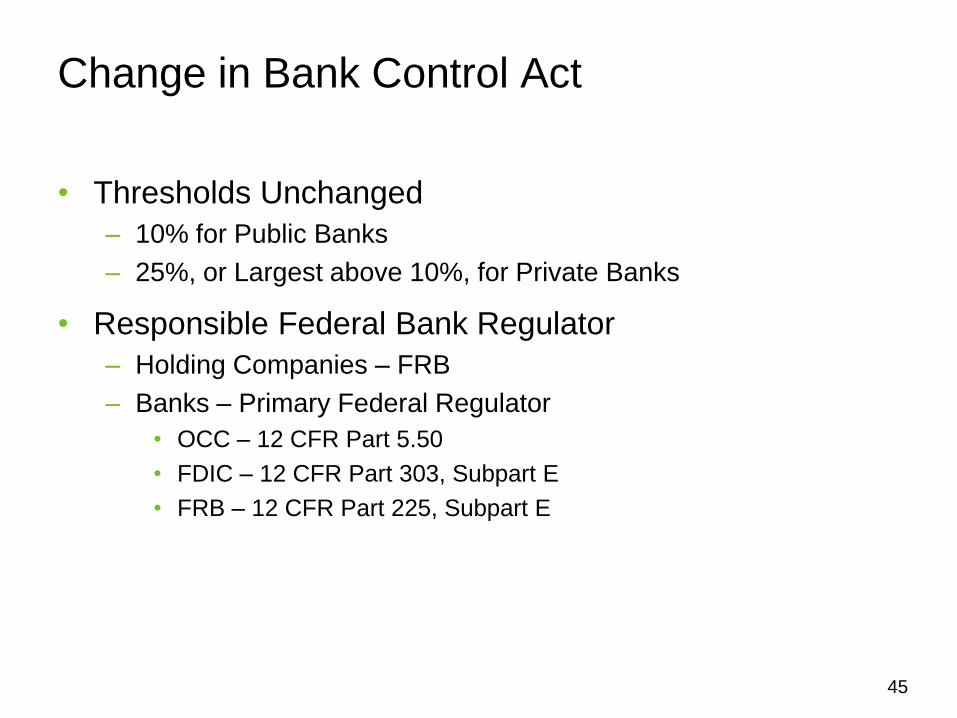

• Thresholds Unchanged

– 10% for Public Banks

– 25%, or Largest above 10%, for Private Banks

• Responsible Federal Bank Regulator

– Holding Companies – FRB

– Banks – Primary Federal Regulator

• OCC – 12 CFR Part 5.50

• FDIC – 12 CFR Part 303, Subpart E

• FRB – 12 CFR Part 225, Subpart E

Change in Bank Control Act

45

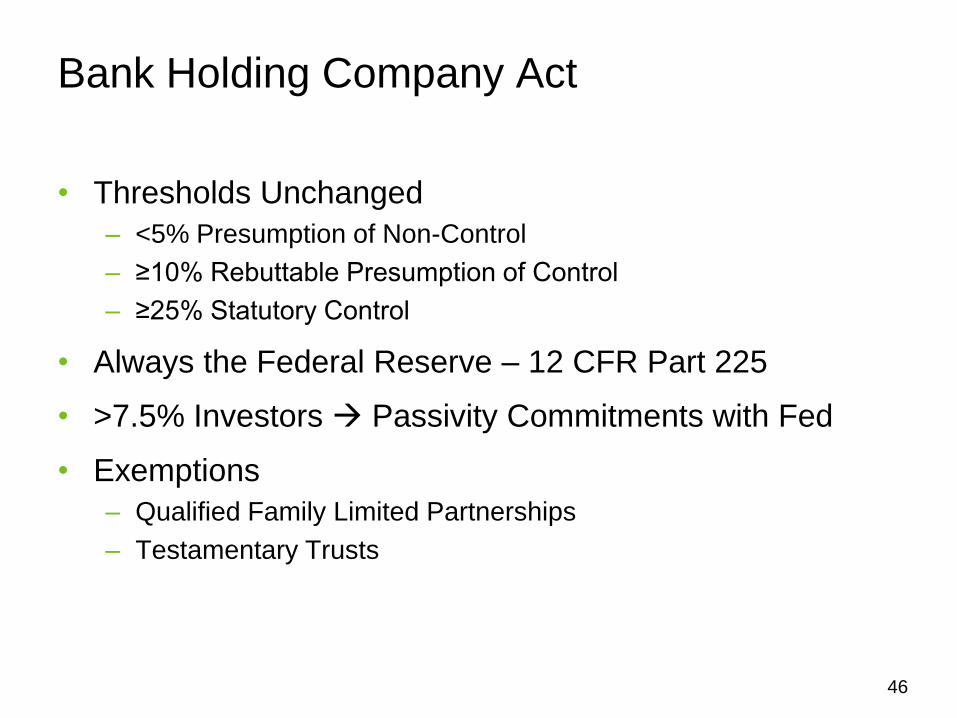

• Thresholds Unchanged

– <5% Presumption of Non-Control

– ≥10% Rebuttable Presumption of Control

– ≥25% Statutory Control

• Always the Federal Reserve – 12 CFR Part 225

• >7.5% Investors Passivity Commitments with Fed

• Exemptions

– Qualified Family Limited Partnerships

– Testamentary Trusts

Bank Holding Company Act

46

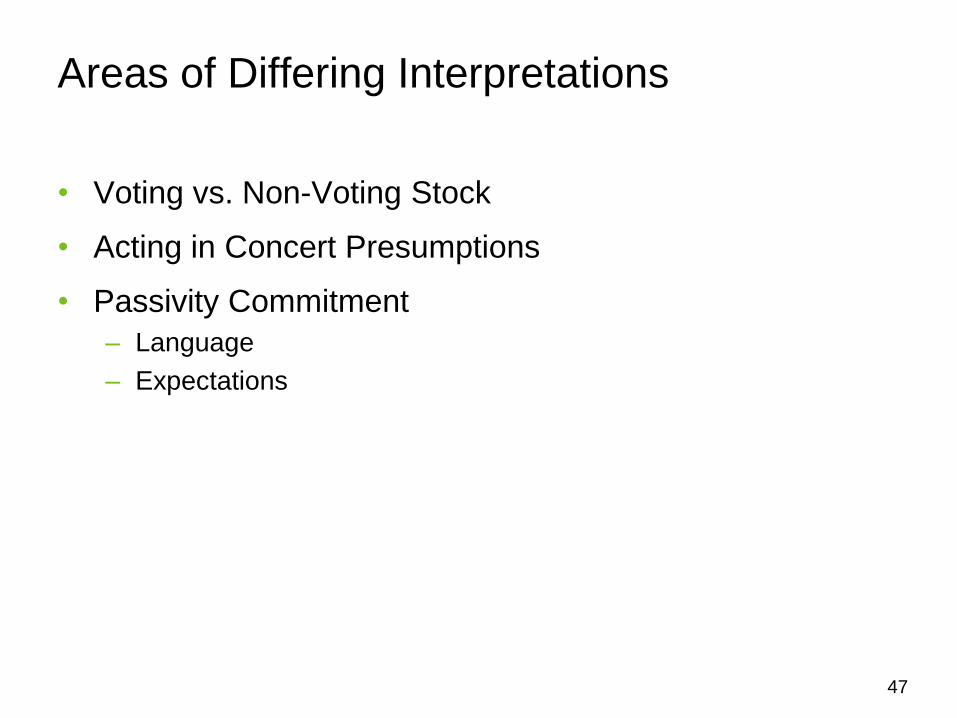

• Voting vs. Non-Voting Stock

• Acting in Concert Presumptions

• Passivity Commitment

– Language

– Expectations

Areas of Differing Interpretations

47

Securities Offerings and

Securities Reporting

48

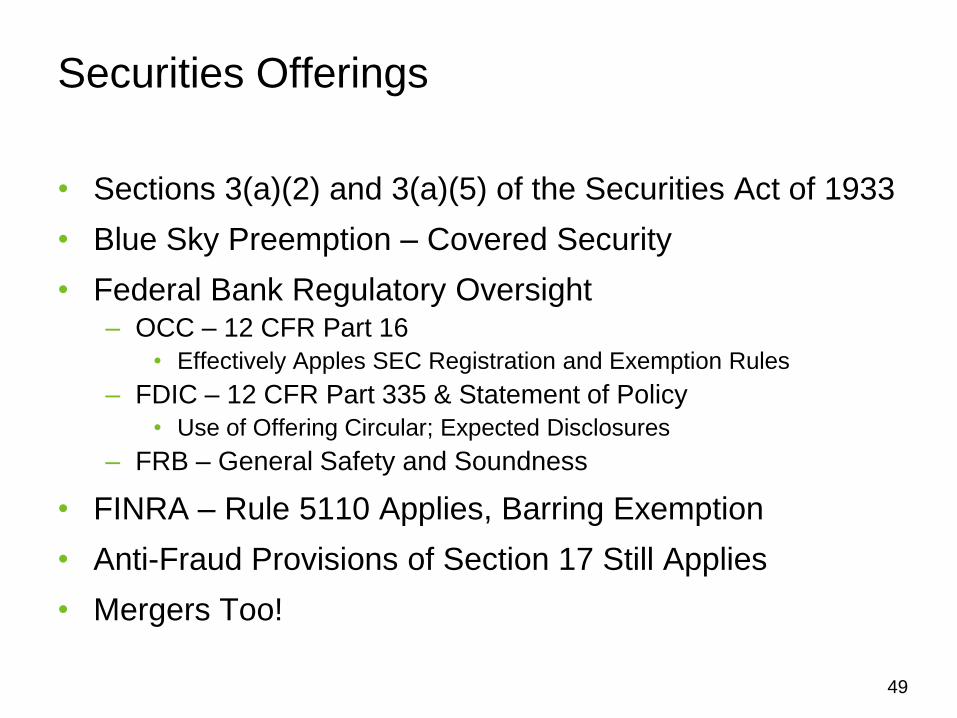

• Sections 3(a)(2) and 3(a)(5) of the Securities Act of 1933

• Blue Sky Preemption – Covered Security

• Federal Bank Regulatory Oversight – OCC – 12 CFR Part 16

• Effectively Apples SEC Registration and Exemption Rules

– FDIC – 12 CFR Part 335 & Statement of Policy

• Use of Offering Circular; Expected Disclosures

– FRB – General Safety and Soundness

• FINRA – Rule 5110 Applies, Barring Exemption

• Anti-Fraud Provisions of Section 17 Still Applies

• Mergers Too!

Securities Offerings

49

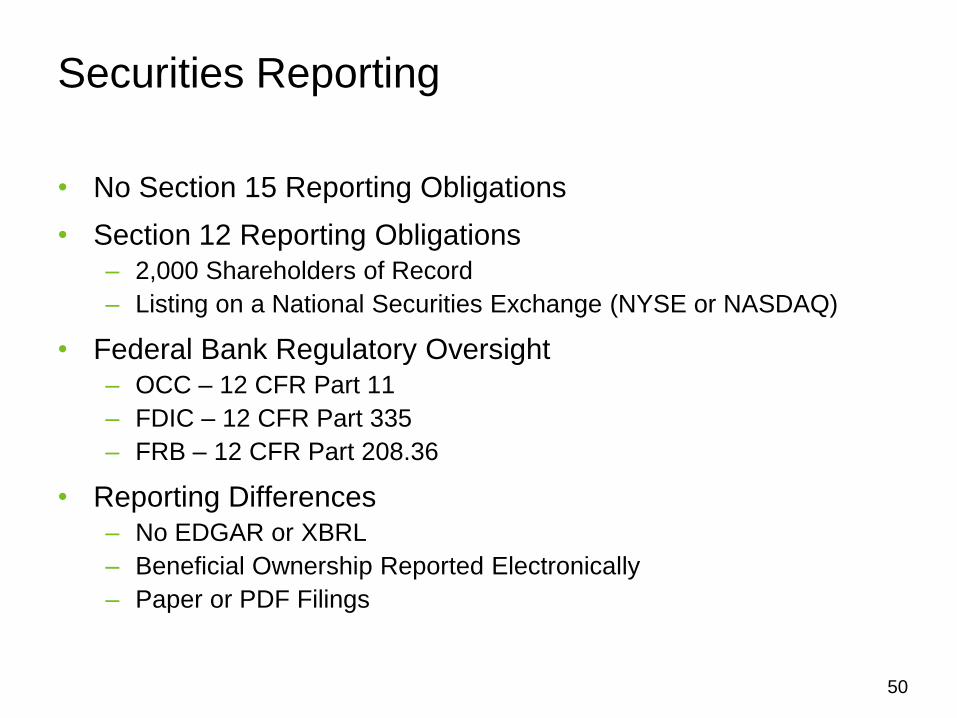

• No Section 15 Reporting Obligations

• Section 12 Reporting Obligations

– 2,000 Shareholders of Record

– Listing on a National Securities Exchange (NYSE or NASDAQ)

• Federal Bank Regulatory Oversight

– OCC – 12 CFR Part 11

– FDIC – 12 CFR Part 335

– FRB – 12 CFR Part 208.36

• Reporting Differences

– No EDGAR or XBRL

– Beneficial Ownership Reported Electronically

– Paper or PDF Filings

Securities Reporting

50

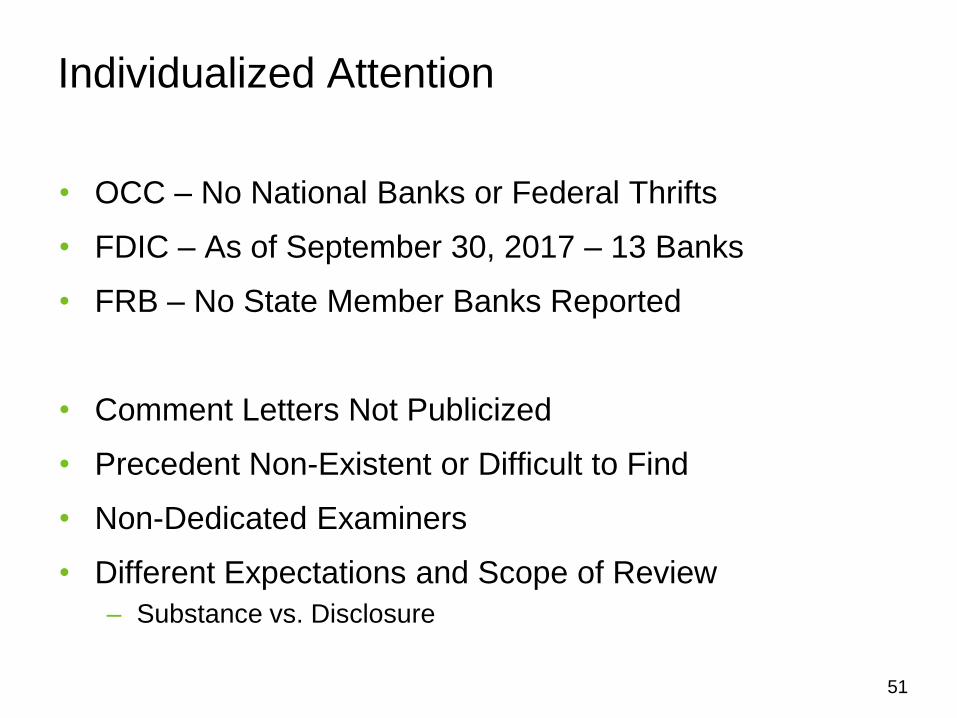

• OCC – No National Banks or Federal Thrifts

• FDIC – As of September 30, 2017 – 13 Banks

• FRB – No State Member Banks Reported

• Comment Letters Not Publicized

• Precedent Non-Existent or Difficult to Find

• Non-Dedicated Examiners

• Different Expectations and Scope of Review

– Substance vs. Disclosure

Individualized Attention

51

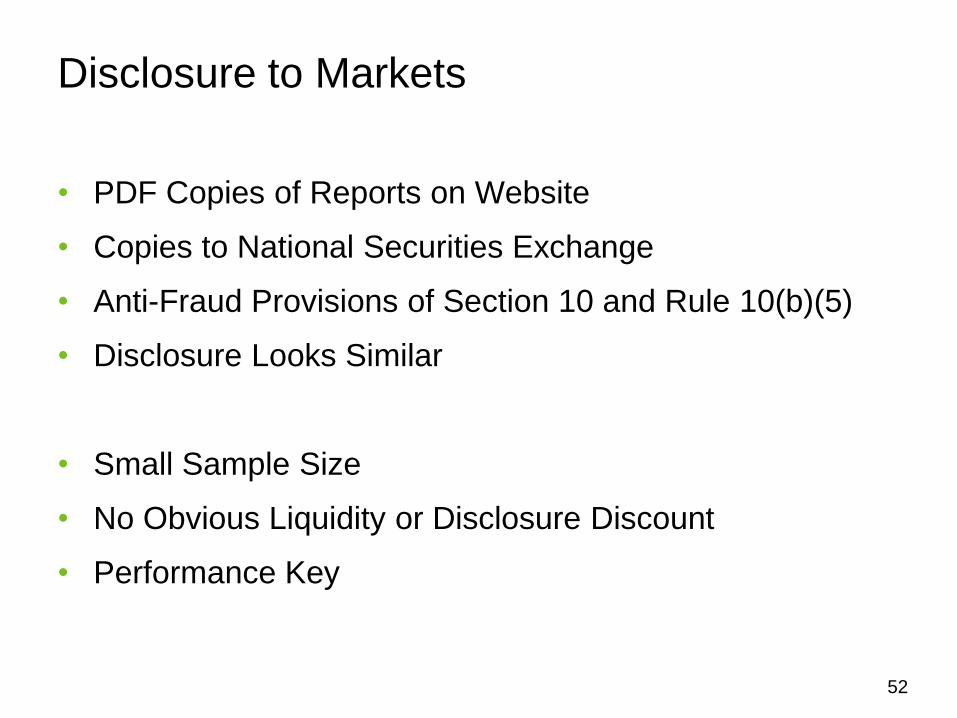

• PDF Copies of Reports on Website

• Copies to National Securities Exchange

• Anti-Fraud Provisions of Section 10 and Rule 10(b)(5)

• Disclosure Looks Similar

• Small Sample Size

• No Obvious Liquidity or Disclosure Discount

• Performance Key

Disclosure to Markets

52

Summary and Conclusion

53

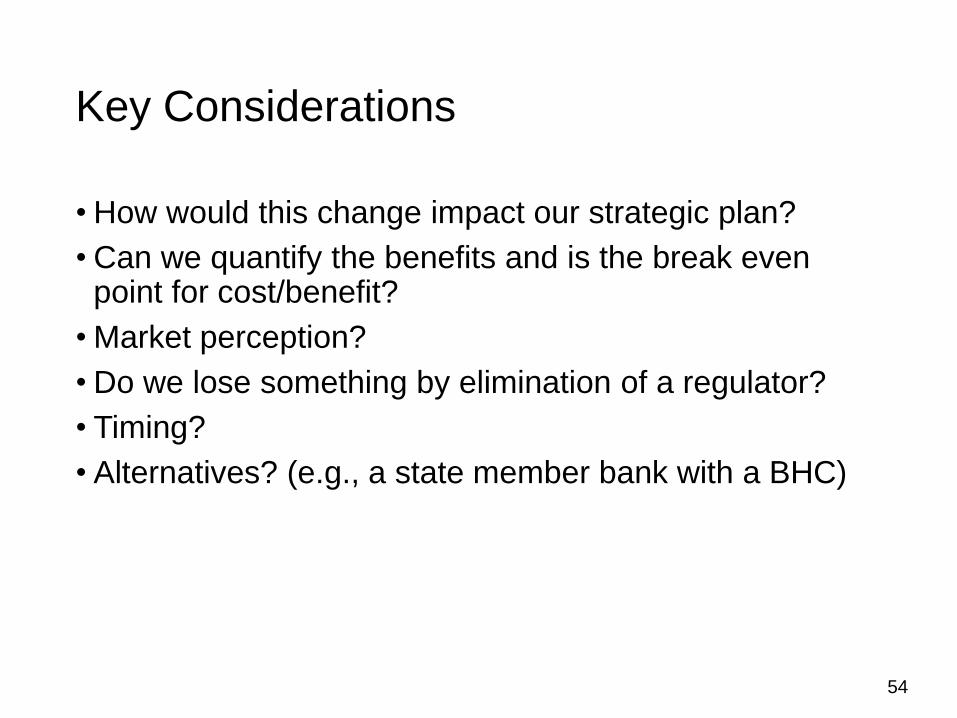

Key Considerations

• How would this change impact our strategic plan?

• Can we quantify the benefits and is the break even point for cost/benefit?

• Market perception?

• Do we lose something by elimination of a regulator?

• Timing?

• Alternatives? (e.g., a state member bank with a BHC)

54

Robert Klingler

Bryan Cave LLP

(404) 572-6810

www.BankBryanCave.com

@RobertKlingler

The Bank Account

Cliff Stanford

Alston & Bird

(404) 881-7833

Questions??

55