Pros & Cons of Outsourcing Bus Operations

36

Pros & Cons of Outsourcing Bus Operations Sanjiv N. Sahai i i &C O S d Managing Director & CEO, DIMTS Ltd Urban Mobility Conference Technical Session IV ‐ PPP in Urban Bus Operations and Maintenance Strategies

Transcript of Pros & Cons of Outsourcing Bus Operations

Pros & Cons of Outsourcing Bus Operations

Sanjiv N. Sahai

i i & C O S dManaging Director & CEO, DIMTS Ltd

Urban Mobility Conference Technical Session IV ‐ PPP in Urban Bus Operations and Maintenance Strategies

Structure of the Presentation

• Introduction

• Various Models for Procurement of Bus OperationVarious Models for Procurement of Bus Operation

• Appraisal of Different Models

• Discussion on Gross Cost

2

Trends in the Delhi Bus Market

Modal Split ‐ % of Person Trips (excluding walk trips) in Delhi*(Figures in Percent)

59.8%

41.5%

2000‐01

2007‐08

10.3%

17.2%

5 3% 3 6%

13.9%

21.5%

3 6% 4 1%6.8% 7.9%

3.1%0.0% 0.7%

5.3% 3.6%3.6% 4.1%0.7%

Car Two Wheelers Auto Rickshaw Bus Metro Train (IR) Bicycle Cycle Rickshaws

* Walk‐only trips account for 35% of trips Walk only trips account for 35% of trips

Source: RITES Delhi Traffic and Forecast Study (2008)

3

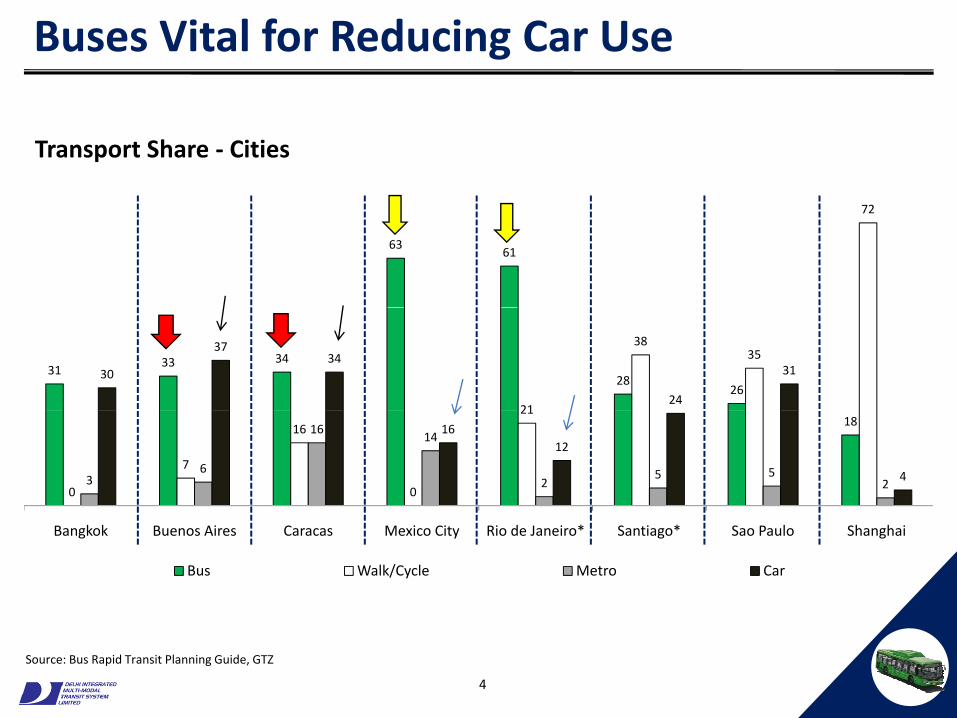

Buses Vital for Reducing Car Use

72

Transport Share ‐ Cities

6361

72

3133 34

2826

21

3835

30

3734

24

31

18

0

7

16

0

21

36

1614

25 5

2

1612

4

Bangkok Buenos Aires Caracas Mexico City Rio de Janeiro* Santiago* Sao Paulo Shanghai

Bus Walk/Cycle Metro Car

4

Source: Bus Rapid Transit Planning Guide, GTZ

Buses in Delhi

Private Stage Carriage ‐ BluelinesDelhi Transport Corporation

• Privately owned

• Fares set by Government

• Reliant on Fare box Revenue

• State owned

• Fares set by Government

• Get Gap‐funding from the Govt Reliant on Fare box Revenue

• 77% of owners have one vehicle

Get Gap funding from the Govt.

• No performance monitoring

Characteristics of Bus Network in Delhi

• Public Operator (Delhi TransportBus Fleets Size in Delhi – By Operators

• Public Operator (Delhi Transport Corporation) carried approx. 2.2 million passengers on an average per day in 2008.

• Private Operators carried approx. 2 ti th2 times more passengers than Public Operator.

Source: 1.STA as of February 2009

l ( b )2.DTC Operational Statistics (October 2009);3.Delhi Metro – Feeder Service (http://www.delhimetrorail.com/commuters/feeder_bus.html)

6

Public Sector Model ‐ Advantages• Closer authority control over services and fares• Closer authority control over services and fares

• Social and community objectives can be easier to achieve

Off i f t f d fi ht t– Offering free passes to freedom fighters etc.

• More accessible in terms of:

– Geography: serving unremunerative and rural routes

– Time: operating service in early morning & late night

– Fare: offering concessionary passes to students, old persons etc.

• Easy to acquire assets such as new fleet and depot space

• Better paid and trained manpower including drivers etc. permits adequate rest and recuperation

7

Issues with Public Sector Model

P l i i i d i d i k• Poorly incentivized management ‐ perceived risk

• Over staffing and at the same time absenteeism

• No incentive to adhere to performance management system

• Not responsive to customer demand

• Lack of innovation and adaption to changing environment

• Little incentive to control costs as subsidies provided ex‐post with no link to achieving policy objectives

DFID Global Review of Bus Performance “could not find any example where a pure public monopoly

offers a superior alternative to the best designed i i ”

8Source: Halcrow Fox for DfID, May 2000

competitive arrangement”

Productivity Gap

Parameters Particulars Nos.

Average Fleet 3,028 (Nos.)

Buses Average buses on road (Daily) 2,458 (Nos.)

Fleet Utilization (%) 81.18%

Scheduled Trips (Daily) 22 447

TripsScheduled Trips (Daily) 22,447

Operated (Daily) 17,265

Trip Efficiency (%) 76.91%

KmsScheduled Kms (Daily – in Lakhs) 164.31

Actual Kms (Daily – in Lakhs) 125.85

Kms Efficiency (%) 76.59%

9

Source: DTC Operational Statistics (June 2009)

Private Stage Carriage Model ‐ Advantages • No subsidy burden on the govt exchequer• No subsidy burden on the govt. exchequer

• Cost control and higher levels of bus patronage occupancy as payment made per passengerpayment made per passenger

10

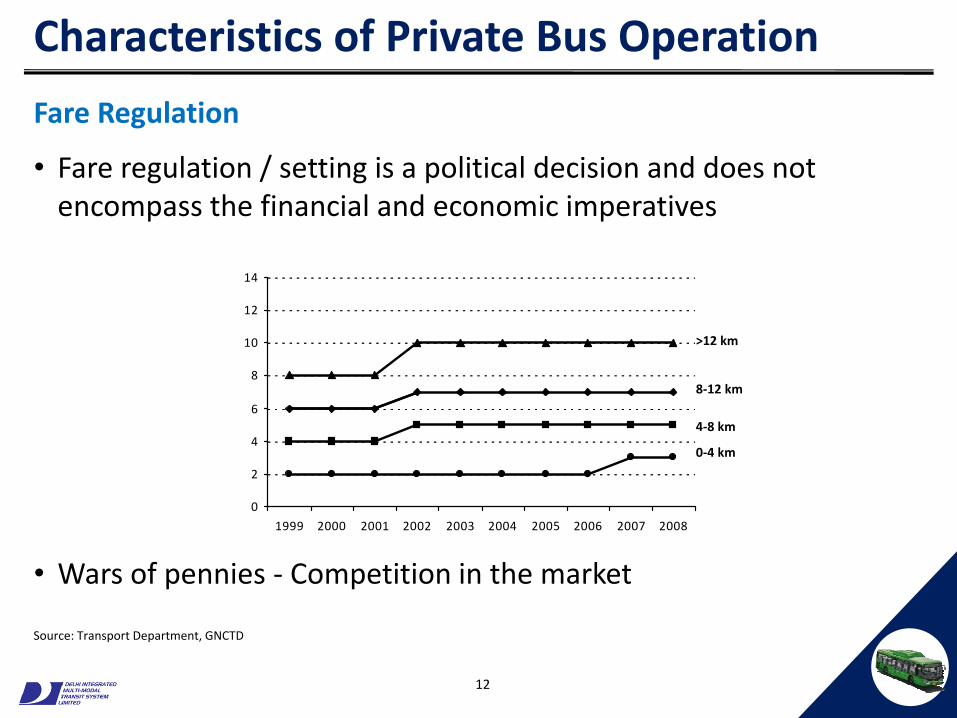

Characteristics of Private Bus Operation

O hi

Distribution of Blueline Fleet Size by Size of Operator

Ownership Pattern

76.3%

eet

e of

Bus

Fle

14.4%

4.1% 1.8% 1.3% 0.9% 0.2% 0.2% 0.3% 0.5%

Shar

e

1 2 3 4 5 6 8 9 10 18

Size of Operator (No. of Buses)

11

Source: STA, Delhi (October 2007)

Characteristics of Private Bus Operation

l i

• Fare regulation / setting is a political decision and does not encompass the financial and economic imperatives

Fare Regulation

encompass the financial and economic imperatives

12

14

6

8

10

12

8‐12 km

>12 km

0

2

4

6

0‐4 km

4‐8 km

• Wars of pennies ‐ Competition in the market

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

12

Source: Transport Department, GNCTD

Issues in Private Bus Operation

• 49% of bus routes are non‐operational

• Lack of network benefits

• Undesirable driving practices

– Accidents and traffic violations

– Predation by incumbents or cartelizationPredation by incumbents or cartelization

• Unreliable bus service ‐ absence of bus route/schedule informationroute/schedule information

• Under investment

13

Regulatory Burden ‐ Permit Conditions

• There are more than 51 permit conditions which private operator needs to comply The cost of compliance is high so violation isneeds to comply. The cost of compliance is high so violation is likely

• In case of violation of permit condition, buses are moved off theIn case of violation of permit condition, buses are moved off the road by the authority

– The operators face 100% revenue risk as most of the operators are single bus owners

– Passengers also faced inconvenience due to withdrawal of iservices

14

Strategic Objectives

Wh ki d f b i d d?What kind of bus service do we need?

• Effective, economic, efficient and safeA hi h lit ff d bl bli t t i– A high quality, affordable public transport service

– Mitigate safety risk – competition for the market, not in the market – Minimum scale required to ensure appropriate management skills– Clear contractual obligations and responsibilities– Maintain service levels on existing routes, extend coverage– Provide comfortable and clean environmentProvide comfortable and clean environment

• Ensure flexibility for the future– Current route network is not rationalised or optimisedCurrent route network is not rationalised or optimised– Need scope to redeploy resources to respond to shifts in demand– Ability to respond to demographic changes and economic growth

C bili d h i l li ( f )– Capability to accommodate changes in regulatory policy (e.g. fares)

15

Risk Allocation

• Appropriate allocation of risk

– High cost associated with attempts to transfer uncontrolled riskg p

– Where does control lie?

– Recognise information gaps and asymmetry

• Sponsor’s dilemma . . .

the greater the extent of attempted risk transfer

the fewer the likely bidders

the greater the potential costs

16

Contract Types

Net Cost

– Full transfer of revenue risk?

Sh d i k?

Gross Cost

– Resource contract

No transfer of revenue risk– or Shared risk?

– Or Minimum revenue guarantee?

– No transfer of revenue risk

– Revenue paid to Government

Revenue

Profit

Revenue

Profit

Cost

Funding Support

Govt Operator

Cost

Revenue

Funding

Support

Govt OperatorGovt Operator Govt Operator

17

Contract Types

Production (Cost) risk borne by

Authority Operator

Gross CostManagement

Contract

born

e by

AuthorityGross CostContract

(cost plus)Gross Cost

with passengervolume/revenue

venu

e ri

sk volume/revenue

incentive

Net Costwith shared

i k

Rev

Operator Net Cost

revenue risk

18

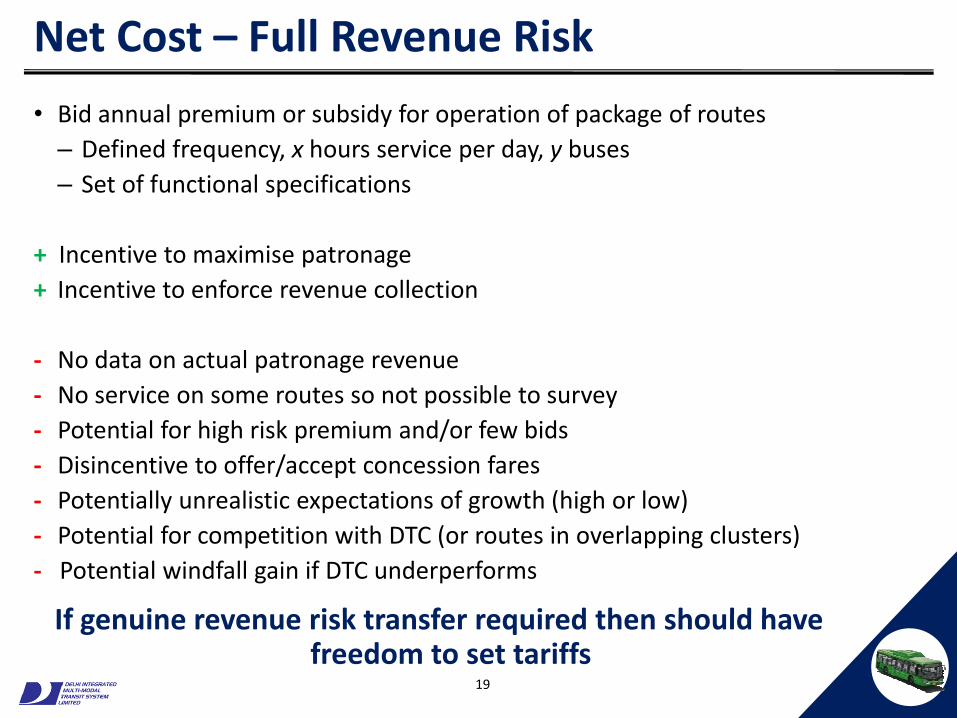

Net Cost – Full Revenue Risk

• Bid annual premium or subsidy for operation of package of routes – Defined frequency, x hours service per day, y buses– Set of functional specifications

+ Incentive to maximise patronage+ Incentive to enforce revenue collection

‐ No data on actual patronage revenue ‐ No service on some routes so not possible to survey‐ Potential for high risk premium and/or few bids ‐ Disincentive to offer/accept concession fares‐ Potentially unrealistic expectations of growth (high or low)y p g ( g )‐ Potential for competition with DTC (or routes in overlapping clusters)‐ Potential windfall gain if DTC underperforms

If genuine revenue risk transfer required then should haveIf genuine revenue risk transfer required then should have freedom to set tariffs

19

Net Cost 2 – SRR and MRG

• Bid annual premium or subsidy for operation of package of routes• Define expected revenues each year

• Shared Revenue Risk (SRR)– Any shortfall in revenue partially compensated by Government

A id i h d i h G– Any upside revenue gain shared with Government

• Minimum Revenue Guarantee (MRG)– All shortfall compensated by Government– All upside to operator

• Similar pros/cons to Net Cost with full revenue risk except:+ Reduces potential risk premium in bid+ Reduces incentive for competition with DTC

20

Gross Cost – No revenue risk

• Resource contract with fare collection on behalf of Government

• Tender for defined package of service schedules and functional specifications

• Define costs by type of bus for base bid

• Defined rates for marginal service increments

• Fare collection and revenue protection separately outsourced

+ Flexibility to add routes, change frequency, redeploy resources

+ Fares and ticketing policy revised at will

/+ Full acceptance of all ticket types including concession fares/passes

+ Payments related to type of bus (quality of service) provided

+ Reduced cost of finance due to secure income stream (from Government)

‐ No incentive to maximise patronage (or pick up)

‐ No incentive for revenue protectionNo incentive for revenue protection

21

Government Contractual Obligations

Gross Cost

• Guaranteed on time paymentsp y

• Provide for inflation indexation on quarterly or annual basis

• Provision of depots

and for Net Cost

• DTC to run in accordance with unified timetable

22

Bid Parameters

• Cost to operate a defined schedule for a set of services = base bid

• Specified outputs:

– Bus‐kmsb b t}– Bus hours

– Minimum peak buses in service

by bus type}

23

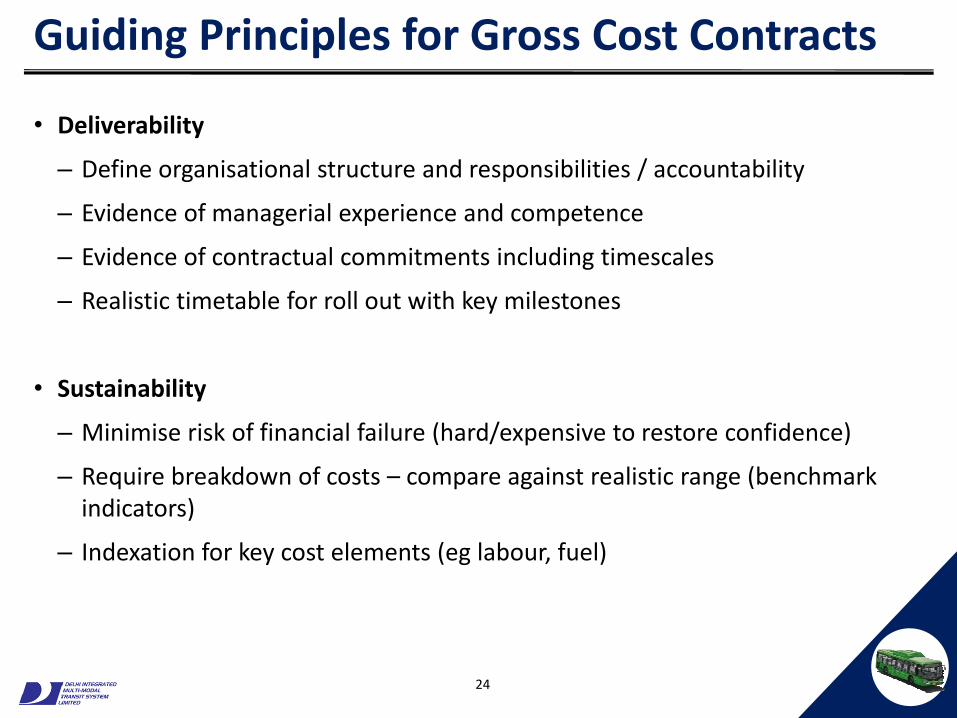

Guiding Principles for Gross Cost Contracts

• Deliverability

– Define organisational structure and responsibilities / accountability

E id f i l i d– Evidence of managerial experience and competence

– Evidence of contractual commitments including timescales

– Realistic timetable for roll out with key milestonesRealistic timetable for roll out with key milestones

• Sustainability

– Minimise risk of financial failure (hard/expensive to restore confidence)

– Require breakdown of costs – compare against realistic range (benchmark indicators)indicators)

– Indexation for key cost elements (eg labour, fuel)

24

Comparator Models

• The value for money can be assessed by comparing the various

bids with a public sector comparator (PSC) or ideally an “efficientbids with a public sector comparator (PSC) or ideally an efficient

operator” model

• DIMTS has relevant data for DTC and hypothetical private operator.

25

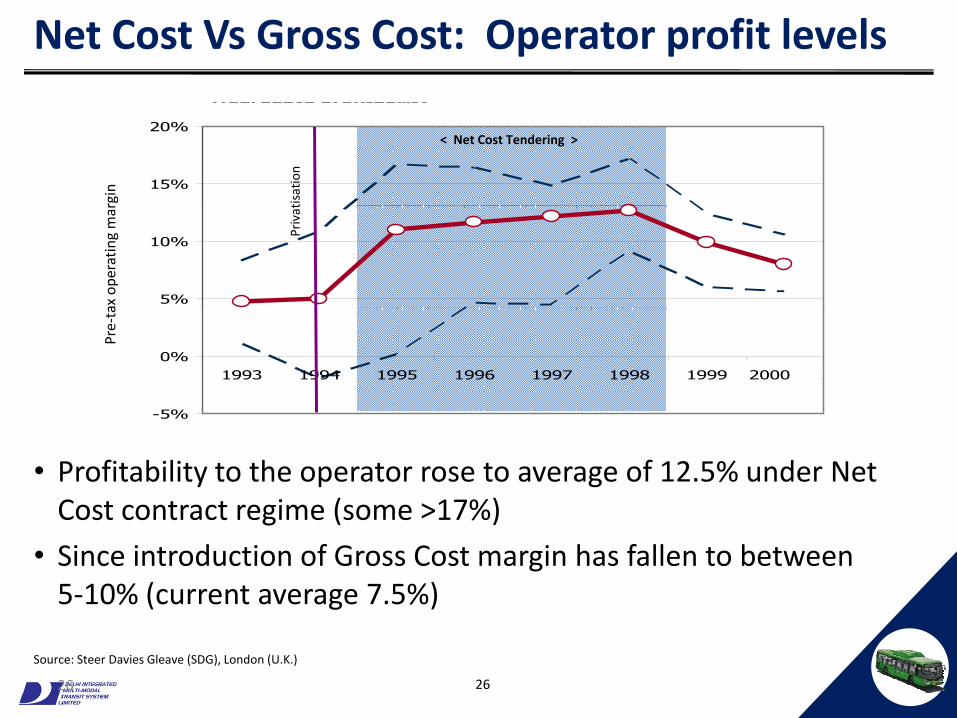

Net Cost Vs Gross Cost: Operator profit levelsAggregate profitabilityAggregate profitability (weighted by Contracted Peak Vehicles)

15%

20%

tisat

ion

< Net Cost Tendering >

rgin

5%

10%

Priv

at

ax o

pera

ting

mar

5%

0%1993 1994 1995 1996 1997 1998 1999 2000 est

Pre‐

ta

-5%

• Profitability to the operator rose to average of 12.5% under Net Cost contract regime (some >17%)Cost contract regime (some >17%)

• Since introduction of Gross Cost margin has fallen to between 5‐10% (current average 7.5%)

26 26

Source: Steer Davies Gleave (SDG), London (U.K.)

Approaches in Other Cities

City Contract Type

London UK Gross cost Route based

Copenhagen DK Gross cost Area basedCopenhagen DK Gross cost Area based

Stockholm SE Gross cost Area based

Adelaide AU Gross cost Area based

Bogota CO Gross cost Corridor based

Santiago CL Gross cost Area based

27

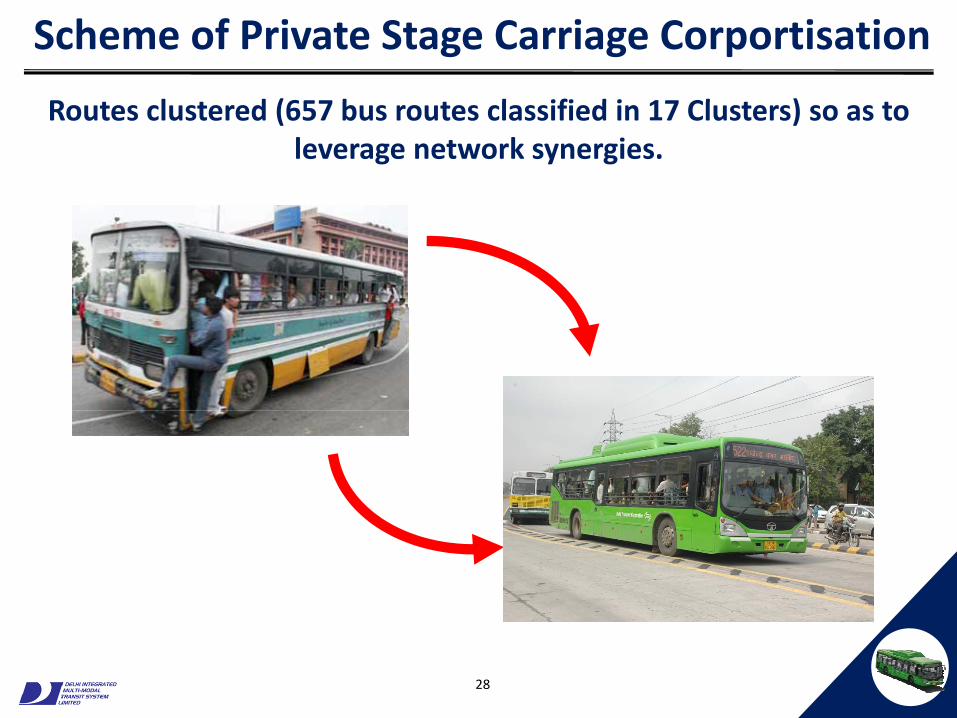

Scheme of Private Stage Carriage Corportisation

R t l t d (657 b t l ifi d i 17 Cl t ) tRoutes clustered (657 bus routes classified in 17 Clusters) so as to leverage network synergies.

28

Role of Integrated Mechanism – DIMTS

• Monitor compliance of the Performance Standards by bus

operators

• Process and impose performance adjustment (PA) for

non‐performance on bus operatorsp p

• Enforcement and monitoring of Unified Time Tables (UTT)

• Monitoring aspects that impact customer service

• Data collection, analysis and monitoring of cluster‐wise operation,Data collection, analysis and monitoring of cluster wise operation,

along with route rationalization

29

Performance Management System

A performance incentive system will be implemented to reward or

penalize the operator on the basis of the quality of service

delivered

• Reliability and Frequency

delivered.

• Reliability and Frequency

• Safety

• Quality such as cleanliness etcQuality such as cleanliness etc.

30

Role of Technology in Performance Monitoring

There is a strong reliance upon modern location technology and

intelligent transport systems to monitor operator performance.

• Automatic Vehicle Location Tracking System (AVLTS)

• Operating Control Centre (OCC) with ITS capability• Operating Control Centre (OCC) with ITS capability

• Automatic Fare Collection System (AFCS)

Application & Map rendering Server (4)

Multiple Cellular (GSM) Networks (2)

Device in the bus

GPS Satellites

HTTP

Communication Hub Gateway Server (3)

PIS A li ti

Database Servers

Map Database

Firewall

PIS Application Server (6)

PIS App Database

(5)

(7)

(1)

Bus Prediction display at stop (8)(7) stop (8)

31

Supported by Systematic Checking

There is also a strong need to assess the other quality

parameters, through daily routine checks and periodic surveys.

• Driver Quality Monitoring (DQM)

• Engineering Quality Checking

Source: www.thestar.com

32

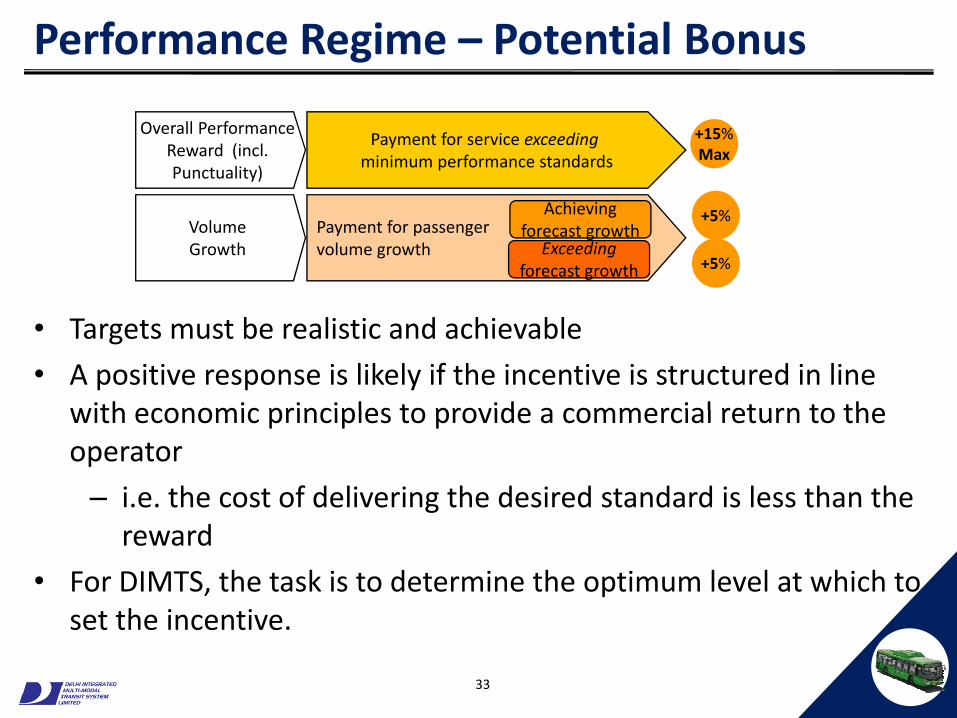

Performance Regime – Potential Bonus

Payment for service exceedingminimum performance standards

Overall Performance Reward (incl. Punctuality)

+15%Max

A hi iPayment for passenger volume growth

VolumeGrowth

Achievingforecast growth

Exceedingforecast growth

+5%

+5%

• Targets must be realistic and achievable

• A positive response is likely if the incentive is structured in line with economic principles to provide a commercial return to thewith economic principles to provide a commercial return to the operator

– i.e. the cost of delivering the desired standard is less than the greward

• For DIMTS, the task is to determine the optimum level at which to set the incentive

33

set the incentive.

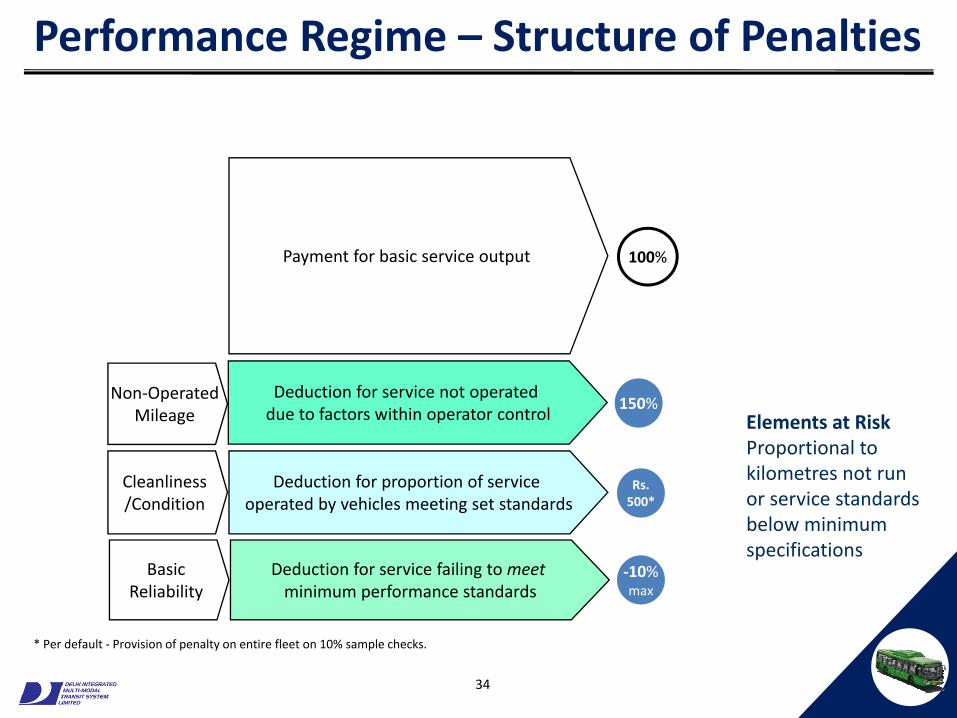

Performance Regime – Structure of Penalties

Payment for basic service output 100%

Non‐OperatedMil

Deduction for service not operated d t f t ithi t t l

150%

Deduction for proportion of service operated by vehicles meeting set standards

Cleanliness/Condition

Mileage

Rs.500*

Elements at RiskProportional to kilometres not run or service standards

due to factors within operator control

p y g

Deduction for service failing to meet minimum performance standards

BasicReliability

‐10%max

below minimum specifications

34

* Per default ‐ Provision of penalty on entire fleet on 10% sample checks.

Challenges

• Political will to ‘stay the course’ of reform

• Institutional capability to plan, monitor and manage

• Data collection and sophisticated information management to maintain consistent quality

• Subsidy dependent y p

• Reliant on technology to reduce revenue leakage

35

Thank youThank you

36

![The Pros and Cons of Hiring IT Outsourcing Services [Infographic]](https://static.fdocuments.in/doc/165x107/58cf8d671a28ab65538b47f5/the-pros-and-cons-of-hiring-it-outsourcing-services-infographic.jpg)