Proppant Prospects for Industrial Minerals Mike O'Driscoll IMFORMED at SME 2015

66

Proppant prospects for industrial minerals Ceramic proppant supply and demand trends imformed.com Networking and knowledge for the industrial minerals business

-

Upload

mike-odriscoll -

Category

Environment

-

view

412 -

download

11

Transcript of Proppant Prospects for Industrial Minerals Mike O'Driscoll IMFORMED at SME 2015

Proppant prospects for

industrial minerals

Ceramic proppant supply and demand trends

imformed.com

Networking and knowledge for the industrial minerals business

imformed.com

[email protected] ▪ +44 (0)1372 450 679 ▪ mobile +44 (0)7985 986 255

Mike O’Driscoll Ismene Clarke

imformed.com

[email protected] ▪ +44 (0)1372 450 679 ▪ mobile +44 (0)7985 986 255

• Launched in January 2015

• The new source of professional networking opportunities and market research

expertise for the global non-metallic minerals industry

• Focused high profile Forums on specific market areas

• Research and consultancy

• Market briefings

• Training seminars

• Field trips

• Special publications

Outline

1. Hydraulic fracturing

2. Proppants

3. Ceramic proppants (CP) & raw materials

4. Trends and developments

5. Outlook

6. Conclusions

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

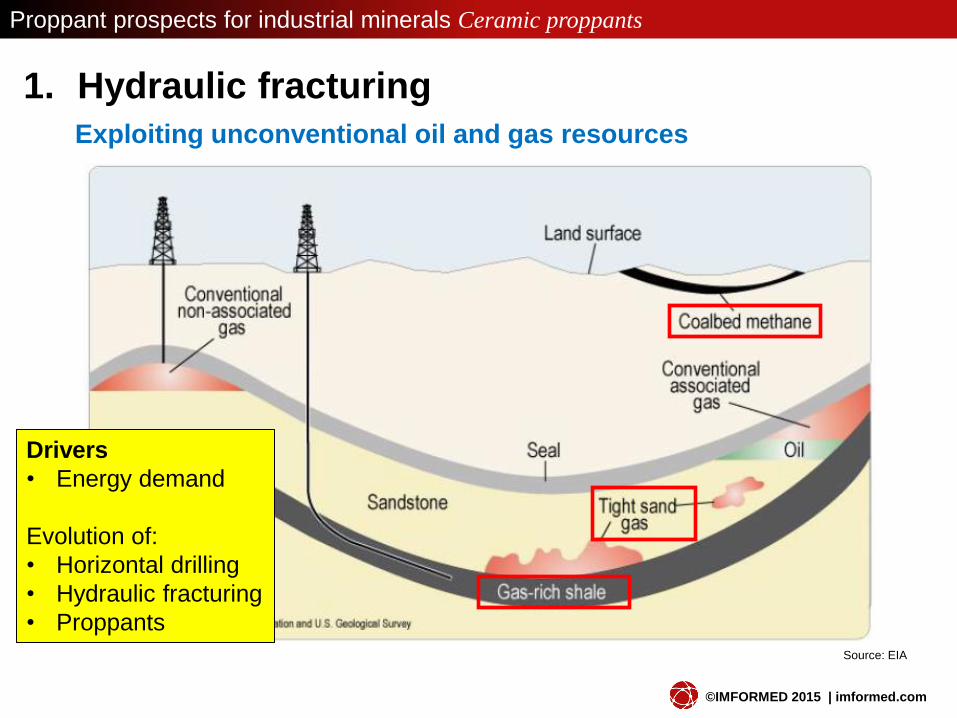

1. Hydraulic fracturing

Exploiting unconventional oil and gas resources

Drivers

• Energy demand

Evolution of:

• Horizontal drilling

• Hydraulic fracturing

• Proppants

Source: EIA

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

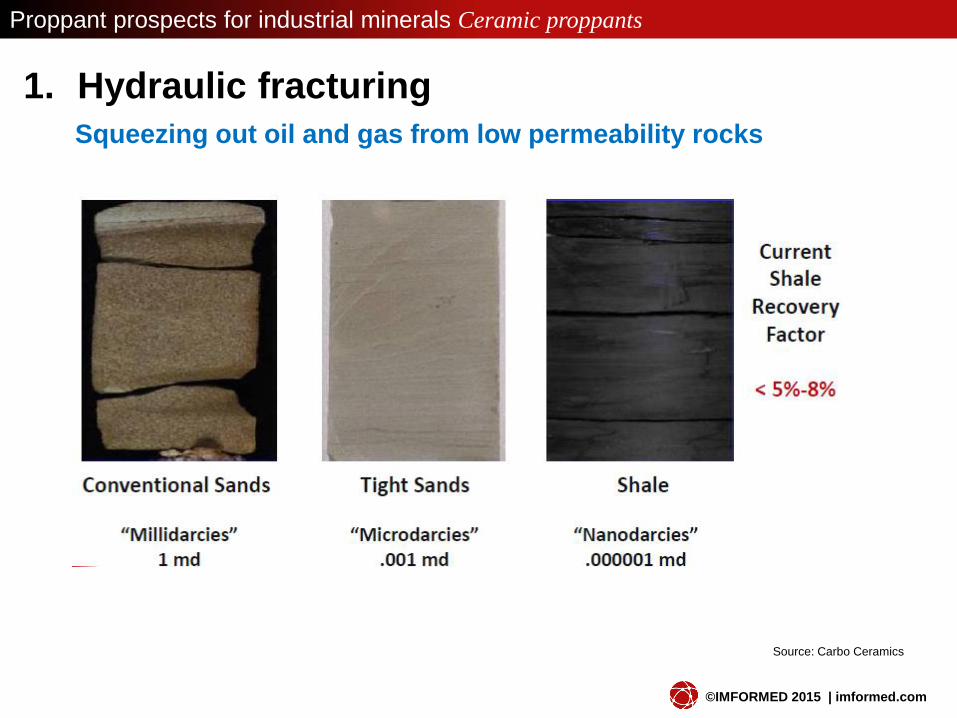

1. Hydraulic fracturing

Squeezing out oil and gas from low permeability rocks

Source: Carbo Ceramics

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

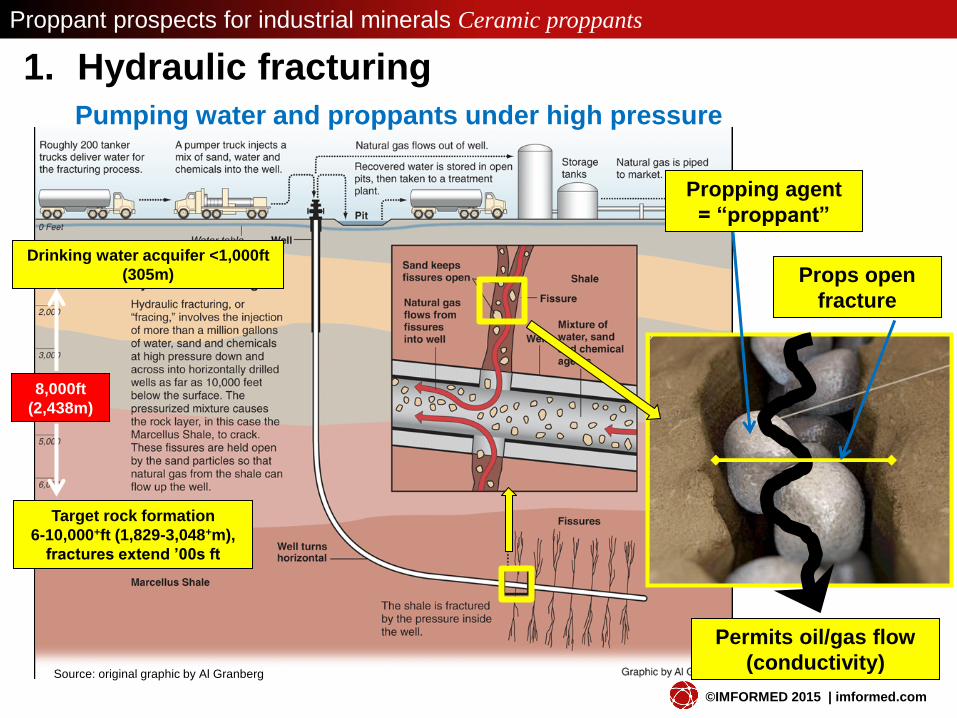

1. Hydraulic fracturing

Pumping water and proppants under high pressure

Propping agent

= “proppant”

Props open

fracture

Permits oil/gas flow

(conductivity)

Drinking water acquifer <1,000ft

(305m)

Target rock formation

6-10,000+ft (1,829-3,048+m),

fractures extend ’00s ft

8,000ft

(2,438m)

Source: original graphic by Al Granberg

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

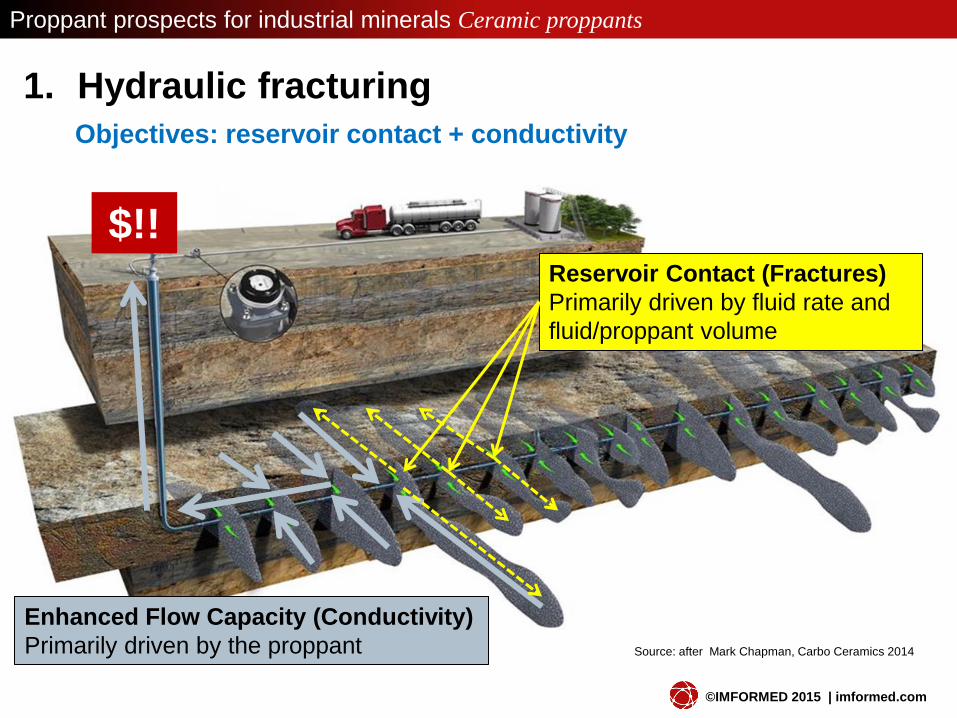

1. Hydraulic fracturing

Objectives: reservoir contact + conductivity

Reservoir Contact (Fractures)

Primarily driven by fluid rate and

fluid/proppant volume

Enhanced Flow Capacity (Conductivity)

Primarily driven by the proppant Source: after Mark Chapman, Carbo Ceramics 2014

$!!

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

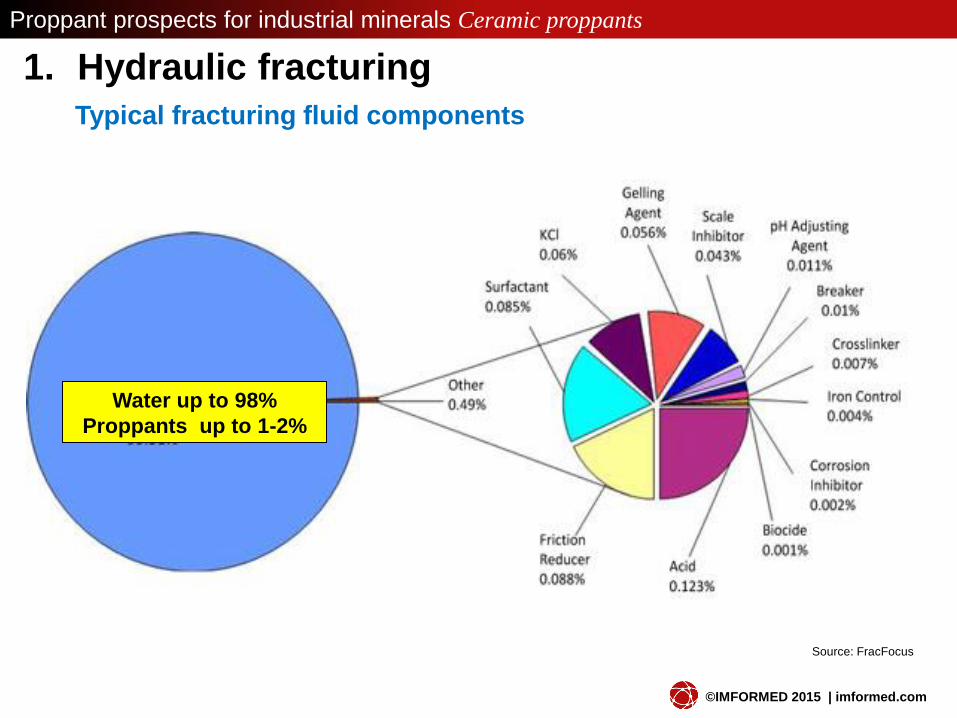

1. Hydraulic fracturing

Typical fracturing fluid components

Source: FracFocus

Water up to 98%

Proppants up to 1-2%

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

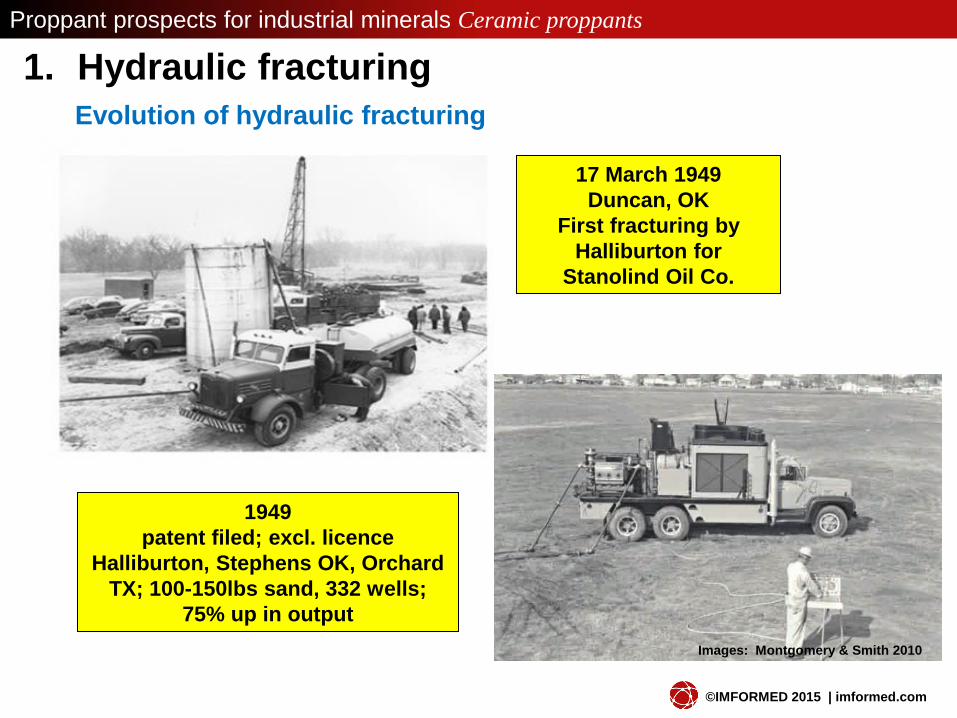

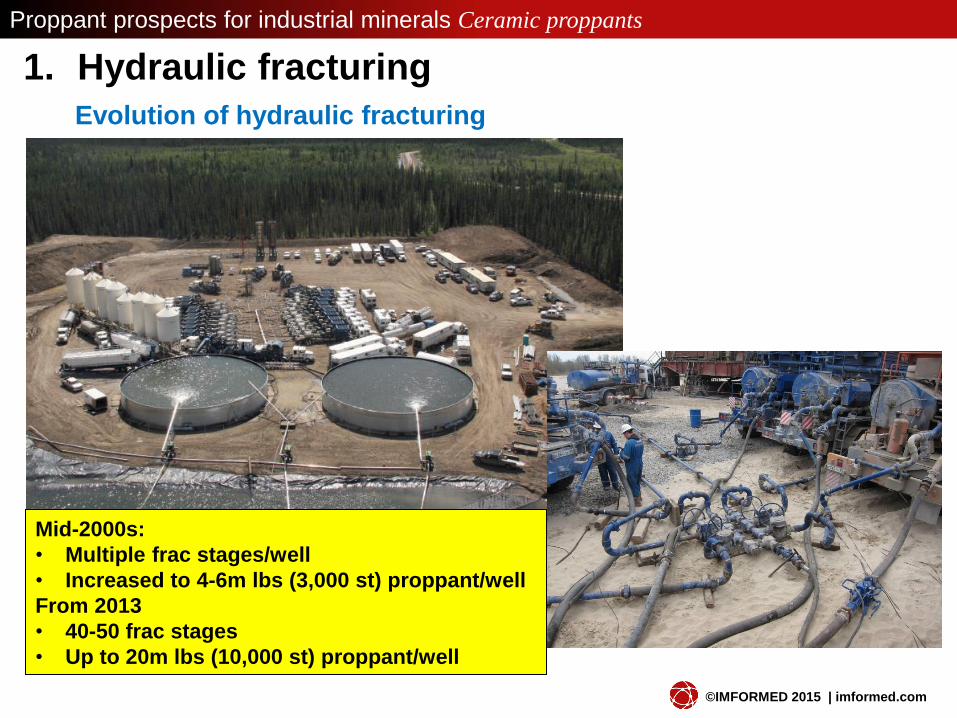

1. Hydraulic fracturing

Evolution of hydraulic fracturing

17 March 1949

Duncan, OK

First fracturing by

Halliburton for

Stanolind Oil Co.

Images: Montgomery & Smith 2010

1949

patent filed; excl. licence

Halliburton, Stephens OK, Orchard

TX; 100-150lbs sand, 332 wells;

75% up in output

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

1. Hydraulic fracturing

Evolution of hydraulic fracturing

Mid-2000s:

• Multiple frac stages/well

• Increased to 4-6m lbs (3,000 st) proppant/well

From 2013

• 40-50 frac stages

• Up to 20m lbs (10,000 st) proppant/well

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

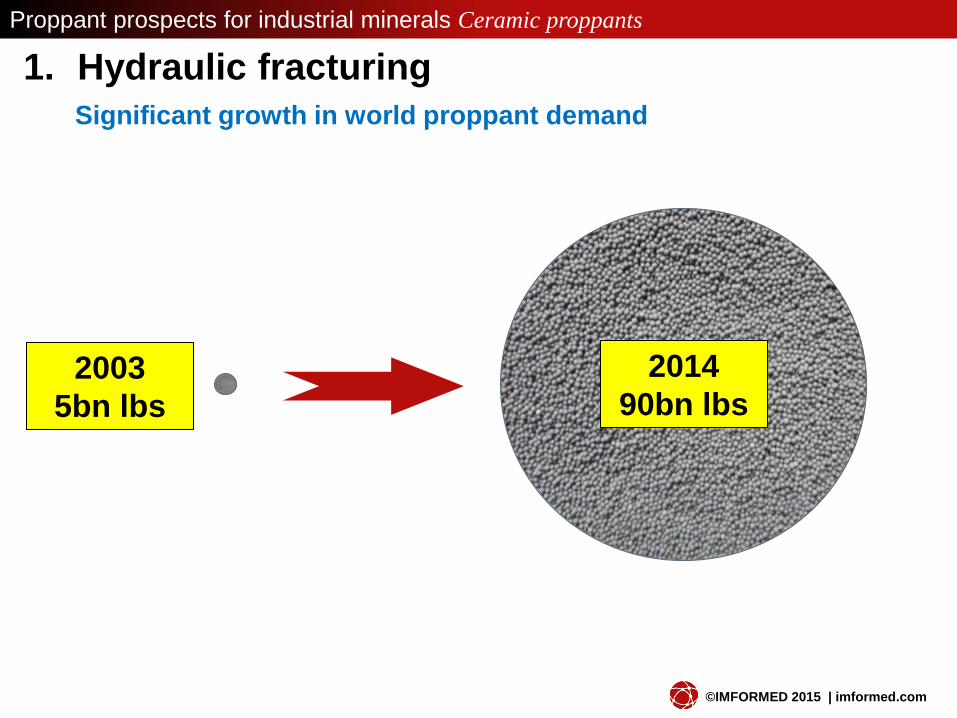

1. Hydraulic fracturing

Significant growth in world proppant demand

2014

90bn lbs 2003

5bn lbs

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

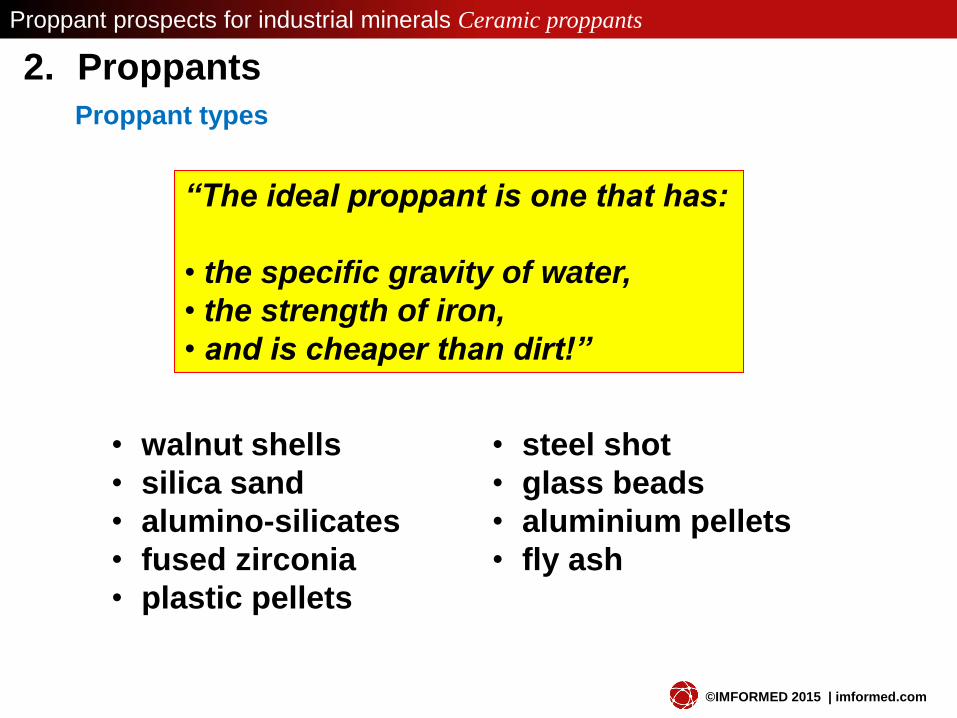

2. Proppants

Proppant types

“The ideal proppant is one that has:

• the specific gravity of water,

• the strength of iron,

• and is cheaper than dirt!”

• walnut shells

• silica sand

• alumino-silicates

• fused zirconia

• plastic pellets

• steel shot

• glass beads

• aluminium pellets

• fly ash

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

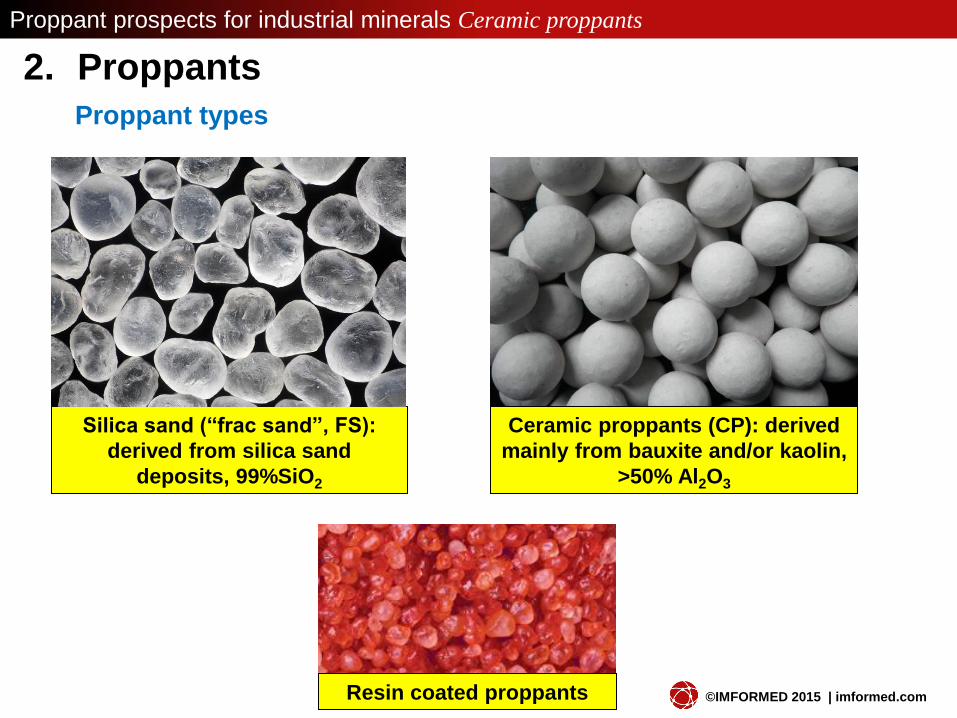

2. Proppants

Proppant types

Silica sand (“frac sand”, FS):

derived from silica sand

deposits, 99%SiO2

Ceramic proppants (CP): derived

mainly from bauxite and/or kaolin,

>50% Al2O3

Resin coated proppants

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

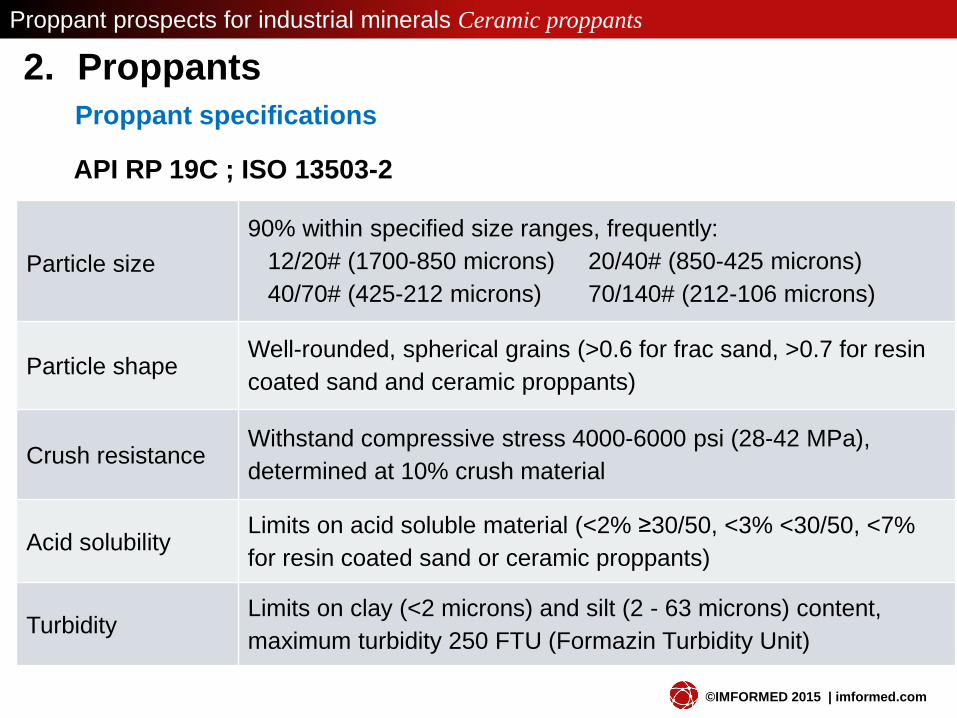

2. Proppants

Proppant specifications

API RP 19C ; ISO 13503-2

Particle size

90% within specified size ranges, frequently:

12/20# (1700-850 microns) 20/40# (850-425 microns)

40/70# (425-212 microns) 70/140# (212-106 microns)

Particle shape Well-rounded, spherical grains (>0.6 for frac sand, >0.7 for resin

coated sand and ceramic proppants)

Crush resistance Withstand compressive stress 4000-6000 psi (28-42 MPa),

determined at 10% crush material

Acid solubility Limits on acid soluble material (<2% ≥30/50, <3% <30/50, <7%

for resin coated sand or ceramic proppants)

Turbidity Limits on clay (<2 microns) and silt (2 - 63 microns) content,

maximum turbidity 250 FTU (Formazin Turbidity Unit)

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

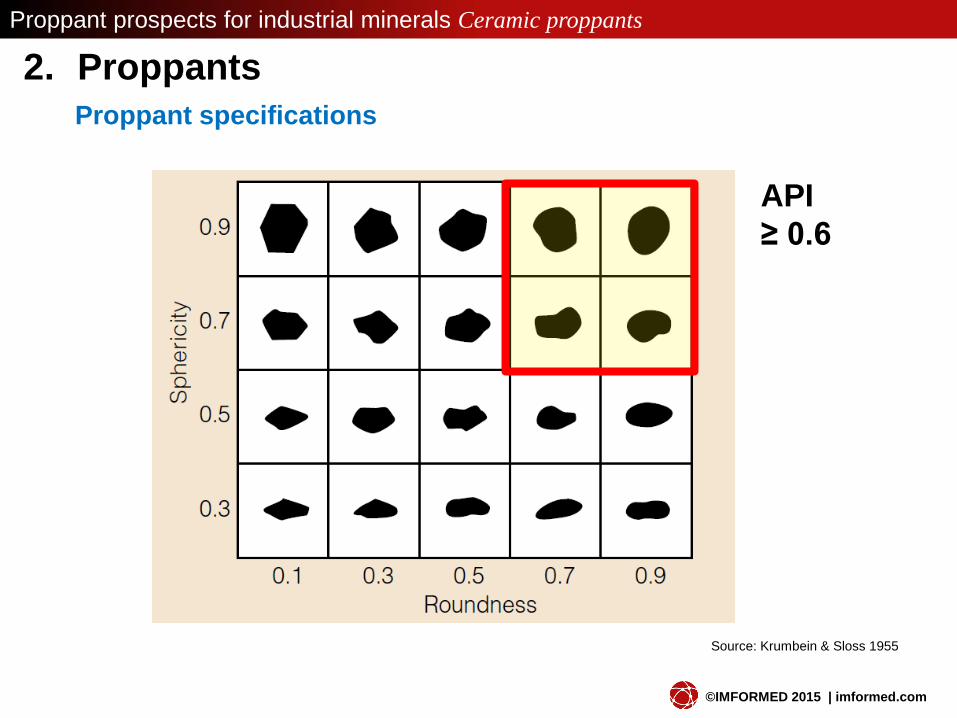

2. Proppants

Proppant specifications

Source: Krumbein & Sloss 1955

API

≥ 0.6

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

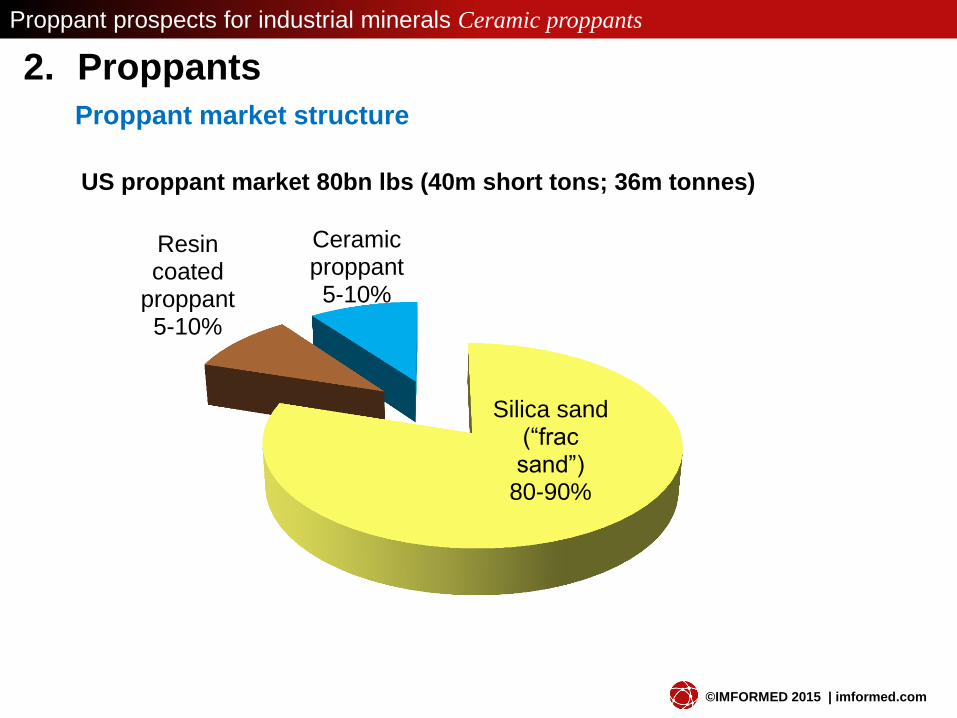

2. Proppants

Proppant market structure

US proppant market 80bn lbs (40m short tons; 36m tonnes)

Silica sand (“frac sand”)

80-90%

Resin coated

proppant 5-10%

Ceramic proppant 5-10%

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

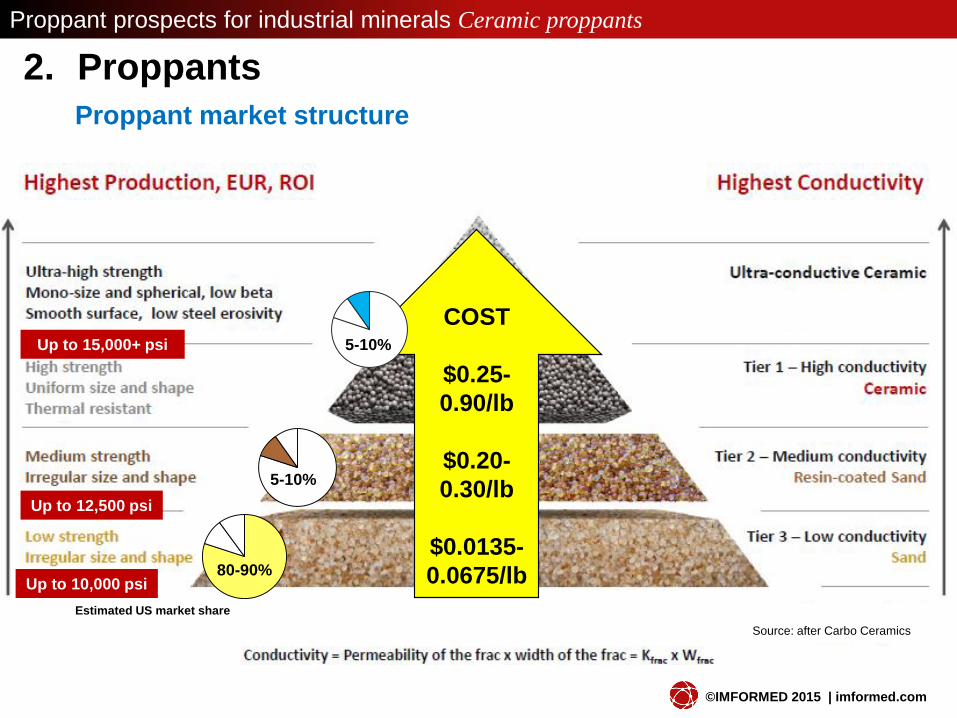

2. Proppants

Proppant market structure

Source: after Carbo Ceramics

COST

$0.25-

0.90/lb

$0.20-

0.30/lb

$0.0135-

0.0675/lb 80-90%

5-10%

5-10%

Estimated US market share

Up to 10,000 psi

Up to 12,500 psi

Up to 15,000+ psi

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

2. Proppants

Selection criteria

• Proppant properties

Strength

Shape

Size

Durability

• Proppant availability

Supply source, quality, and cost

• Fracture treatment

eg. fluid system required, slickwater vs cross-linked fluids and

impact on proppant size

• Conductivity requirements

Desired conductivity

Cost vs benefit, ie. proppant cost set against oil recovery

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

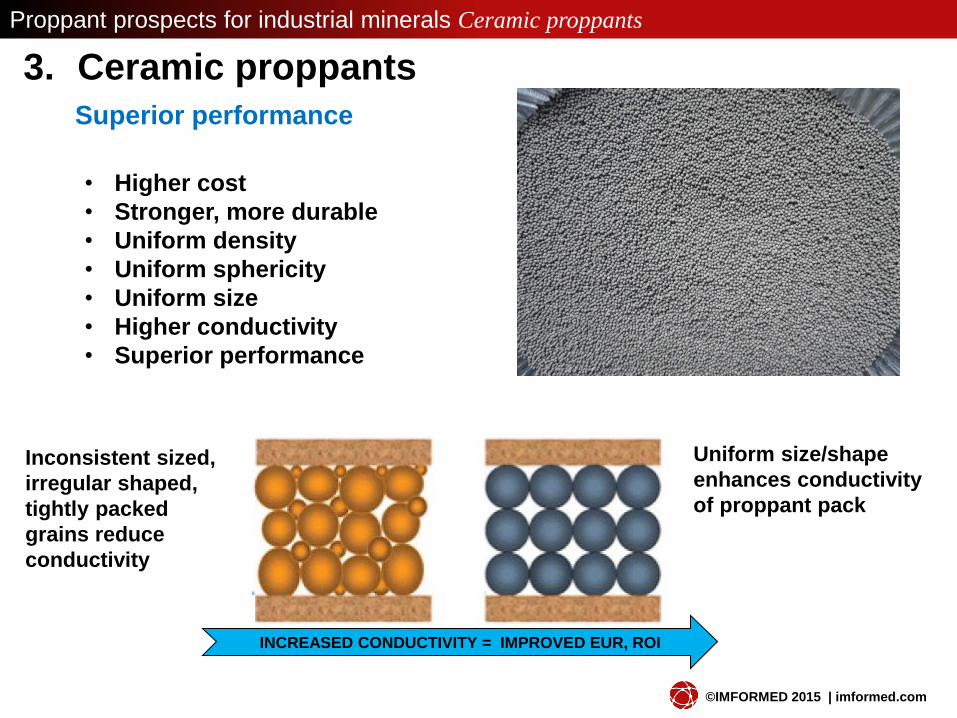

3. Ceramic proppants

Superior performance

Uniform size/shape

enhances conductivity

of proppant pack

Inconsistent sized,

irregular shaped,

tightly packed

grains reduce

conductivity

INCREASED CONDUCTIVITY = IMPROVED EUR, ROI

• Higher cost

• Stronger, more durable

• Uniform density

• Uniform sphericity

• Uniform size

• Higher conductivity

• Superior performance

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

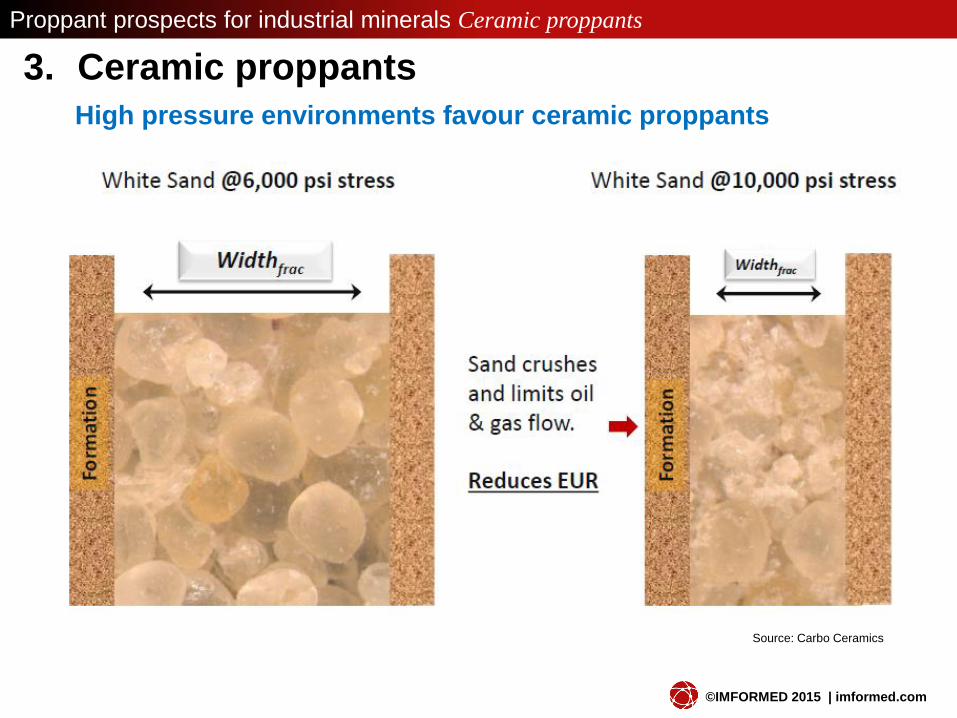

3. Ceramic proppants

High pressure environments favour ceramic proppants

Source: Carbo Ceramics

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

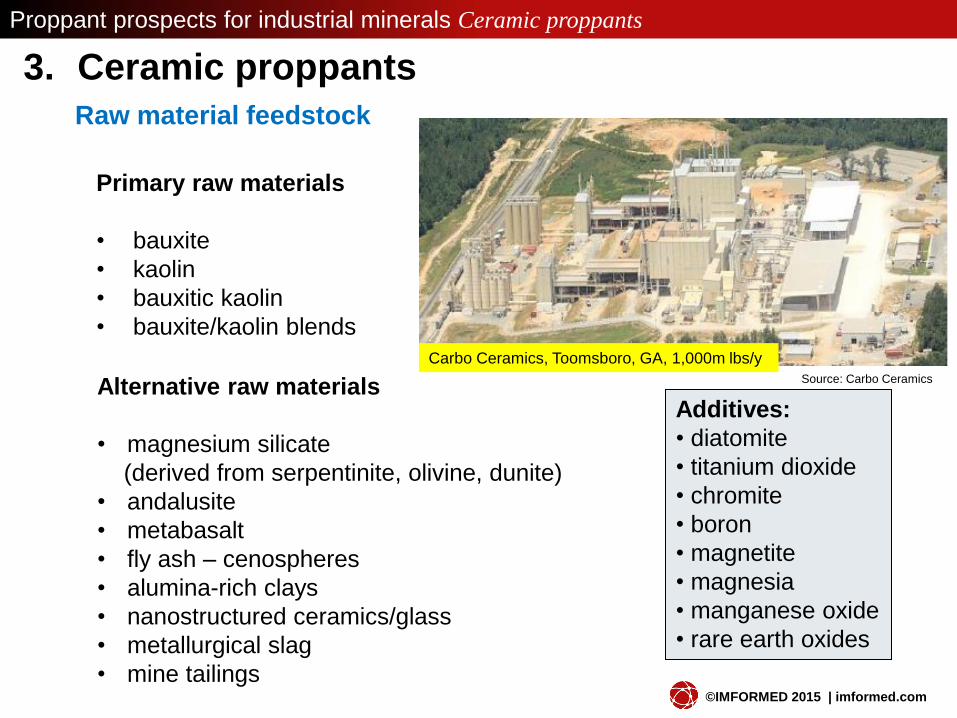

3. Ceramic proppants

Raw material feedstock

Primary raw materials

• bauxite

• kaolin

• bauxitic kaolin

• bauxite/kaolin blends

Additives:

• diatomite

• titanium dioxide

• chromite

• boron

• magnetite

• magnesia

• manganese oxide

• rare earth oxides

Alternative raw materials

• magnesium silicate

(derived from serpentinite, olivine, dunite)

• andalusite

• metabasalt

• fly ash – cenospheres

• alumina-rich clays

• nanostructured ceramics/glass

• metallurgical slag

• mine tailings

Source: Carbo Ceramics

Carbo Ceramics, Toomsboro, GA, 1,000m lbs/y

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

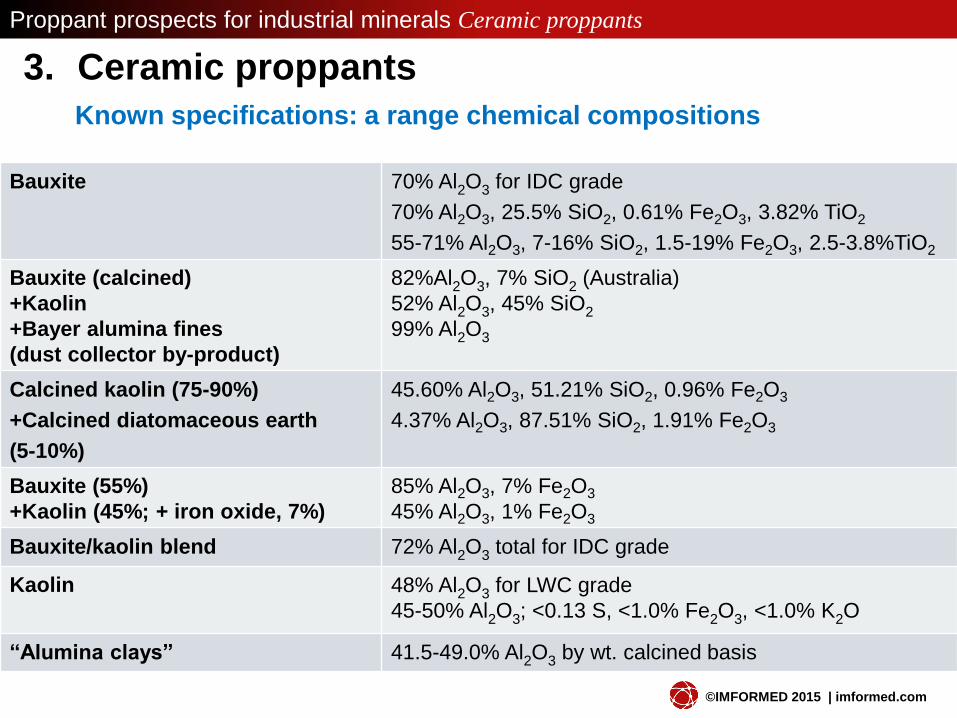

Bauxite 70% Al2O3 for IDC grade

70% Al2O3, 25.5% SiO2, 0.61% Fe2O3, 3.82% TiO2

55-71% Al2O3, 7-16% SiO2, 1.5-19% Fe2O3, 2.5-3.8%TiO2

Bauxite (calcined)

+Kaolin

+Bayer alumina fines

(dust collector by-product)

82%Al2O3, 7% SiO2 (Australia)

52% Al2O3, 45% SiO2

99% Al2O3

Calcined kaolin (75-90%)

+Calcined diatomaceous earth

(5-10%)

45.60% Al2O3, 51.21% SiO2, 0.96% Fe2O3

4.37% Al2O3, 87.51% SiO2, 1.91% Fe2O3

Bauxite (55%)

+Kaolin (45%; + iron oxide, 7%)

85% Al2O3, 7% Fe2O3

45% Al2O3, 1% Fe2O3

Bauxite/kaolin blend 72% Al2O3 total for IDC grade

Kaolin 48% Al2O3 for LWC grade

45-50% Al2O3; <0.13 S, <1.0% Fe2O3, <1.0% K2O

“Alumina clays” 41.5-49.0% Al2O3 by wt. calcined basis

3. Ceramic proppants

Known specifications: a range chemical compositions

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

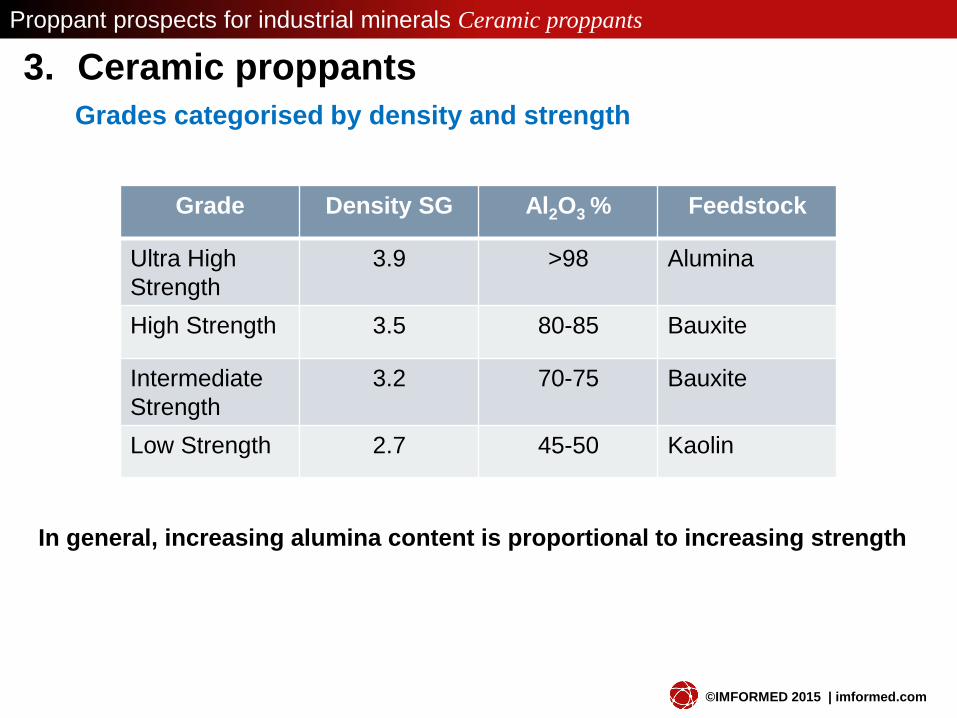

3. Ceramic proppants

Grades categorised by density and strength

Grade Density SG Al2O3 % Feedstock

Ultra High

Strength

3.9 >98 Alumina

High Strength 3.5 80-85 Bauxite

Intermediate

Strength

3.2 70-75 Bauxite

Low Strength 2.7 45-50 Kaolin

In general, increasing alumina content is proportional to increasing strength

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

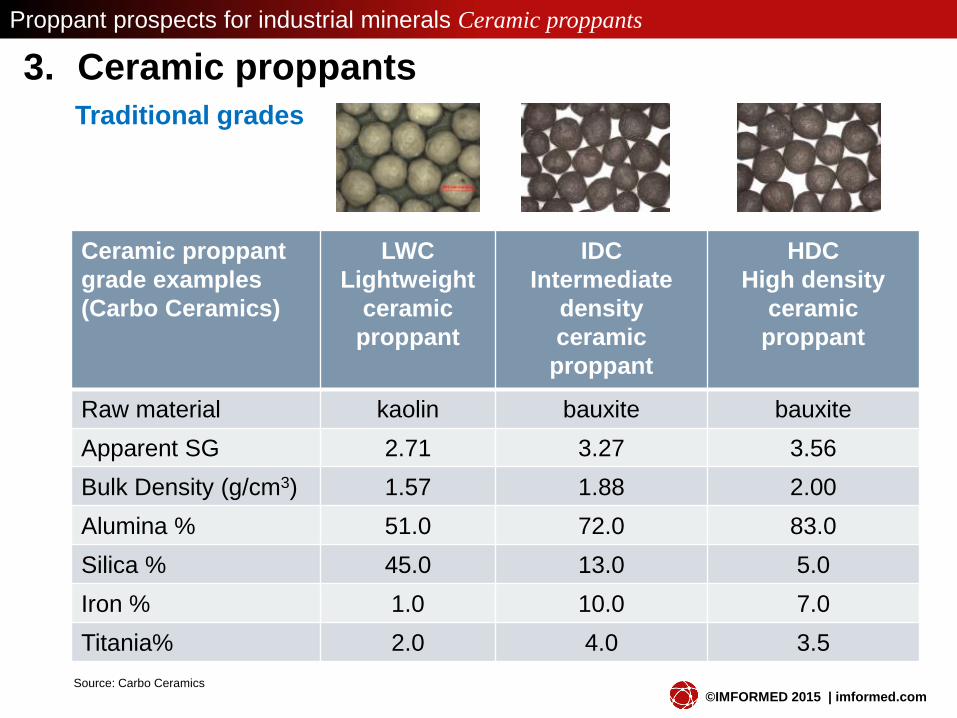

3. Ceramic proppants

Traditional grades

Ceramic proppant

grade examples

(Carbo Ceramics)

LWC

Lightweight

ceramic

proppant

IDC

Intermediate

density

ceramic

proppant

HDC

High density

ceramic

proppant

Raw material kaolin bauxite bauxite

Apparent SG 2.71 3.27 3.56

Bulk Density (g/cm3) 1.57 1.88 2.00

Alumina % 51.0 72.0 83.0

Silica % 45.0 13.0 5.0

Iron % 1.0 10.0 7.0

Titania% 2.0 4.0 3.5

Source: Carbo Ceramics

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

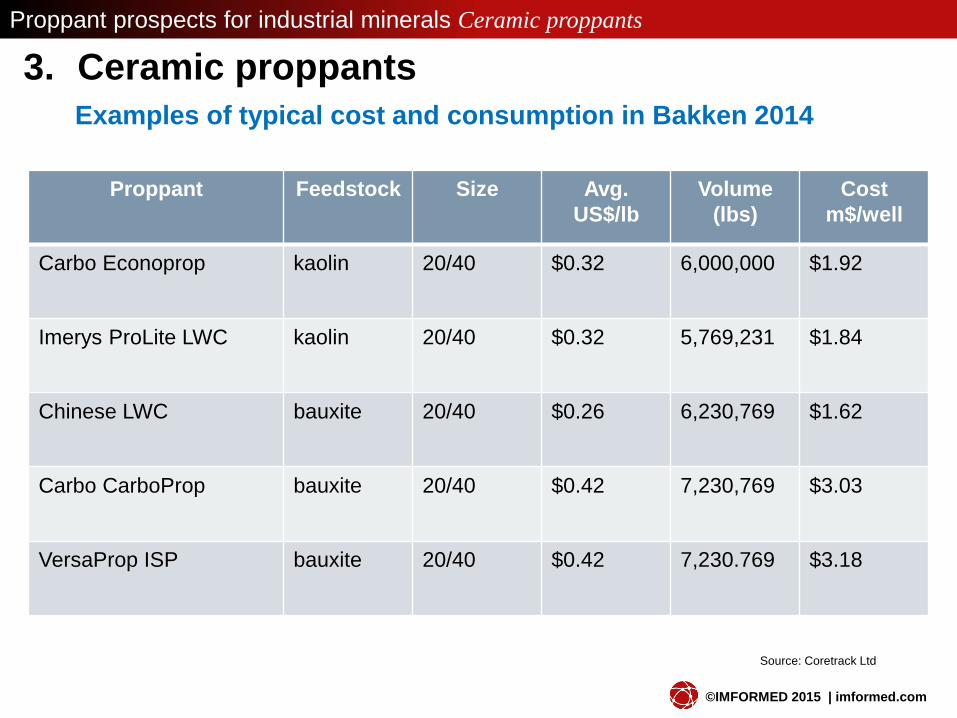

Proppant Feedstock Size Avg.

US$/lb

Volume

(lbs)

Cost

m$/well

Carbo Econoprop kaolin 20/40 $0.32 6,000,000 $1.92

Imerys ProLite LWC kaolin 20/40 $0.32 5,769,231 $1.84

Chinese LWC bauxite 20/40 $0.26 6,230,769 $1.62

Carbo CarboProp bauxite 20/40 $0.42 7,230,769 $3.03

VersaProp ISP bauxite 20/40 $0.42 7,230.769 $3.18

3. Ceramic proppants

Examples of typical cost and consumption in Bakken 2014

Source: Coretrack Ltd

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

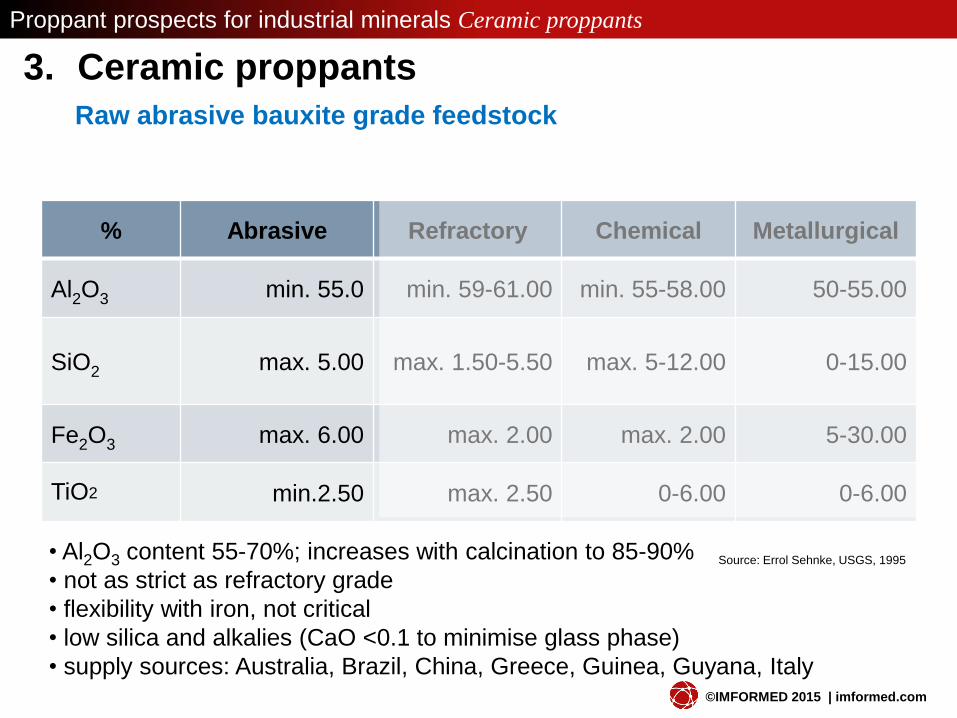

3. Ceramic proppants

Raw abrasive bauxite grade feedstock

% Abrasive Refractory Chemical Metallurgical

Al2O3 min. 55.0 min. 59-61.00 min. 55-58.00 50-55.00

SiO2 max. 5.00 max. 1.50-5.50 max. 5-12.00 0-15.00

Fe2O3 max. 6.00 max. 2.00 max. 2.00 5-30.00

TiO2 min.2.50 max. 2.50 0-6.00 0-6.00

Source: Errol Sehnke, USGS, 1995 • Al2O3 content 55-70%; increases with calcination to 85-90%

• not as strict as refractory grade

• flexibility with iron, not critical

• low silica and alkalies (CaO <0.1 to minimise glass phase)

• supply sources: Australia, Brazil, China, Greece, Guinea, Guyana, Italy

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

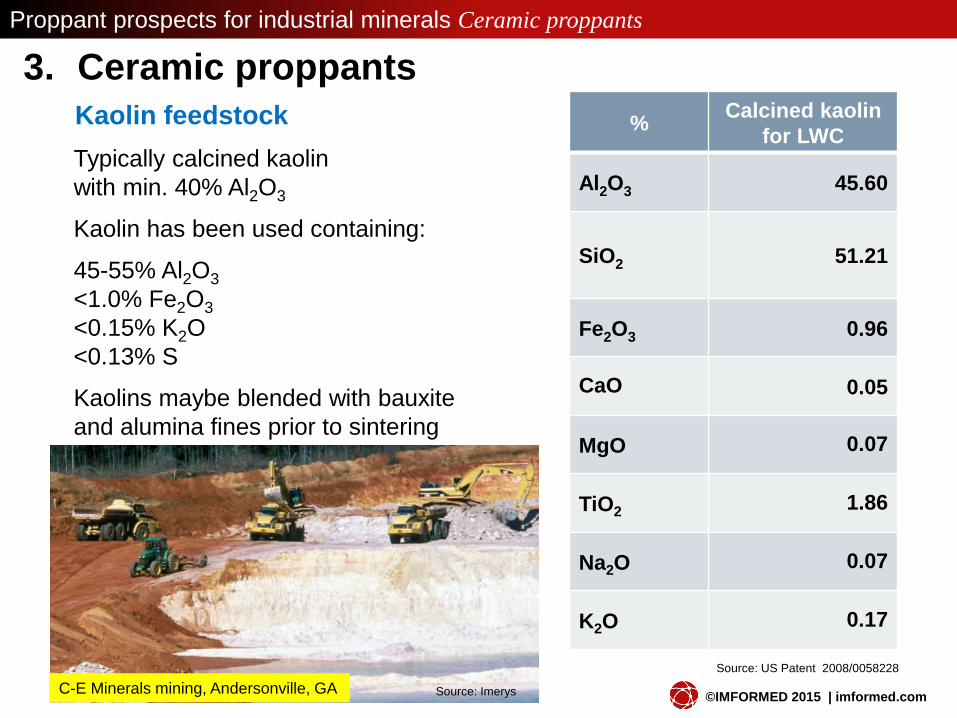

3. Ceramic proppants

Kaolin feedstock % Calcined kaolin

for LWC

Al2O3 45.60

SiO2 51.21

Fe2O3 0.96

CaO 0.05

MgO 0.07

TiO2 1.86

Na2O 0.07

K2O 0.17

Typically calcined kaolin

with min. 40% Al2O3

Kaolin has been used containing:

45-55% Al2O3

<1.0% Fe2O3

<0.15% K2O

<0.13% S

Kaolins maybe blended with bauxite

and alumina fines prior to sintering

Source: US Patent 2008/0058228

Source: Imerys C-E Minerals mining, Andersonville, GA

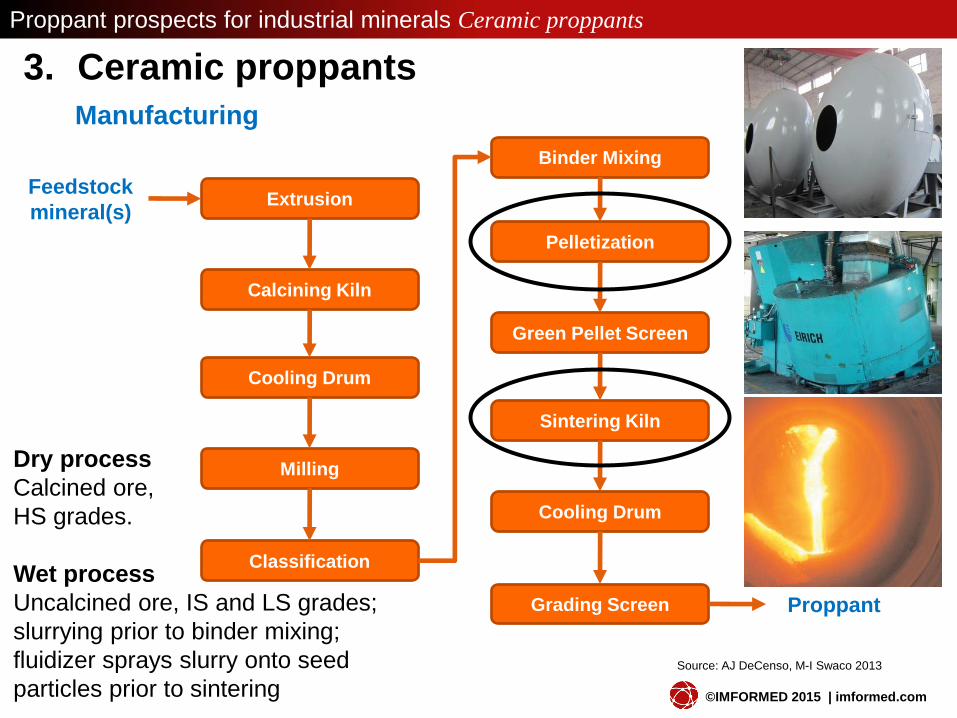

Extrusion

Calcining Kiln

Cooling Drum

Milling

Classification

Binder Mixing

Pelletization

Green Pellet Screen

Sintering Kiln

Cooling Drum

Grading Screen

Feedstock

mineral(s)

Proppant

Source: AJ DeCenso, M-I Swaco 2013

Dry process

Calcined ore,

HS grades.

Wet process

Uncalcined ore, IS and LS grades;

slurrying prior to binder mixing;

fluidizer sprays slurry onto seed

particles prior to sintering

Proppant prospects for industrial minerals Ceramic proppants

3. Ceramic proppants

Manufacturing

©IMFORMED 2015 | imformed.com

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

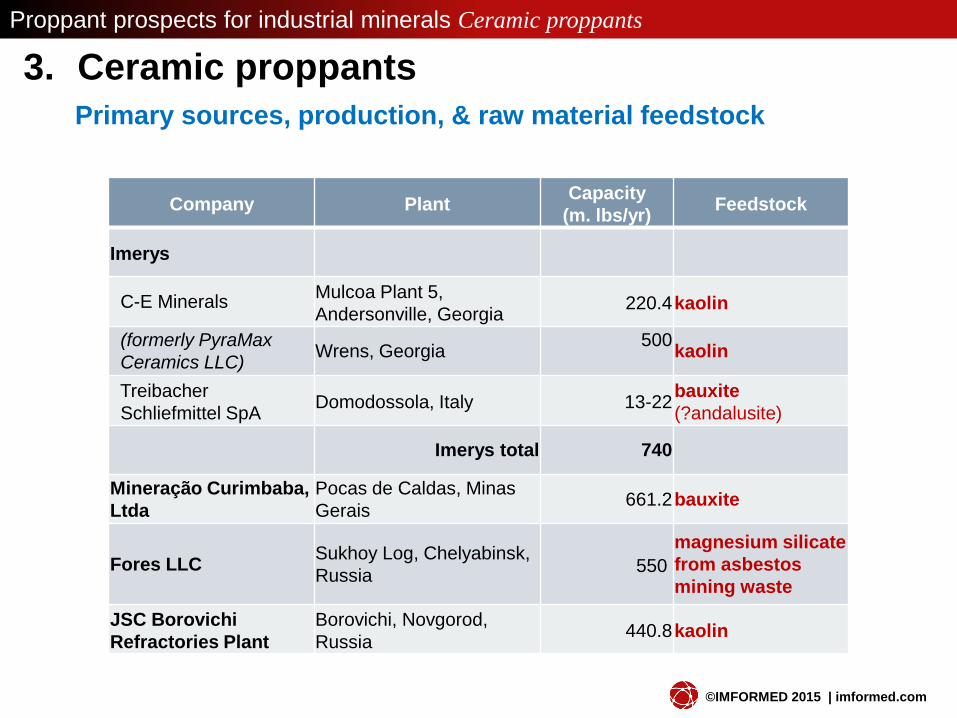

3. Ceramic proppants

Primary sources, production, & raw material feedstock

Company Plant Capacity

(m. lbs/yr) Feedstock

Carbo Ceramics Inc.

Carbo Ceramics Inc. Eufaula, Alabama 275 kaolin

McIntyre, Georgia 275 kaolin & bauxite

Toomsboro, Georgia 1,000 kaolin

Millen, Georgia 250

(+250 Q3 2015) kaolin & bauxite

Carbo Ceramics (China)

Co. Ltd Luoyang, Henan, China 100 kaolin & bauxite

Carbo Ceramics Eurasia Kopeysk, Chelyabinsk,

Russia 100 bauxite

Carbo total 2,000

Saint-Gobain Proppants

Saint-Gobain Proppants Fort Smith, Arkansas 180-200+ bauxite

Bryant, Saline, Arkansas 330 bauxite

closed 2011 Puerto Ordaz, Venezuela 110.2 bauxite

Saint-Gobain Proppants

(Guanghan) Co. Ltd Guanghan, Sichuan, China 198.4 bauxite

S-G total 730

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

3. Ceramic proppants

Primary sources, production, & raw material feedstock

Company Plant Capacity

(m. lbs/yr) Feedstock

Imerys

C-E Minerals Mulcoa Plant 5,

Andersonville, Georgia 220.4 kaolin

(formerly PyraMax

Ceramics LLC) Wrens, Georgia

500

kaolin

Treibacher

Schliefmittel SpA Domodossola, Italy 13-22

bauxite

(?andalusite)

Imerys total 740

Mineração Curimbaba,

Ltda

Pocas de Caldas, Minas

Gerais 661.2 bauxite

Fores LLC Sukhoy Log, Chelyabinsk,

Russia 550

magnesium silicate

from asbestos

mining waste

JSC Borovichi

Refractories Plant

Borovichi, Novgorod,

Russia 440.8 kaolin

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

3. Ceramic proppants

China: leading producer, modernising

• Total production capacity est. 10bn lbs/y.

Production est. <50%.

• Export market boomed from 2001,

peaked in 2011 at >1m tonnes;

40-50% of output; mostly to USA

• ~100 plants producing ceramic proppants

10% >220m lbs/y

20% 132-220m lbs/y

70% <110m lbs/y

• Feedstock is bauxite (except Carbo Ceramics plant also uses kaolin)

• Located close to bauxite resources: Henan, Guizhou, Shanxi, and Sichuan

• Major players:

Producers >441m lbs/y:

Gongyi Tianxiang Ceramic Proppant Co. Ltd

Hebei Haihua Petroleum Proppants Ltd

Xinmi Wanli Industry Development Co. Ltd.

• Addressing quality and inefficiency issues

Companies investing in modern capacity

Xinmi Wanli Industry Development Co. Ltd

Yangquan Changqing Petroleum Fracturing

Propping Agents Co. Ltd

Luoyang Maide Ceramics Co. Ltd

Yixing Orient Petroleum Proppant Co. Ltd

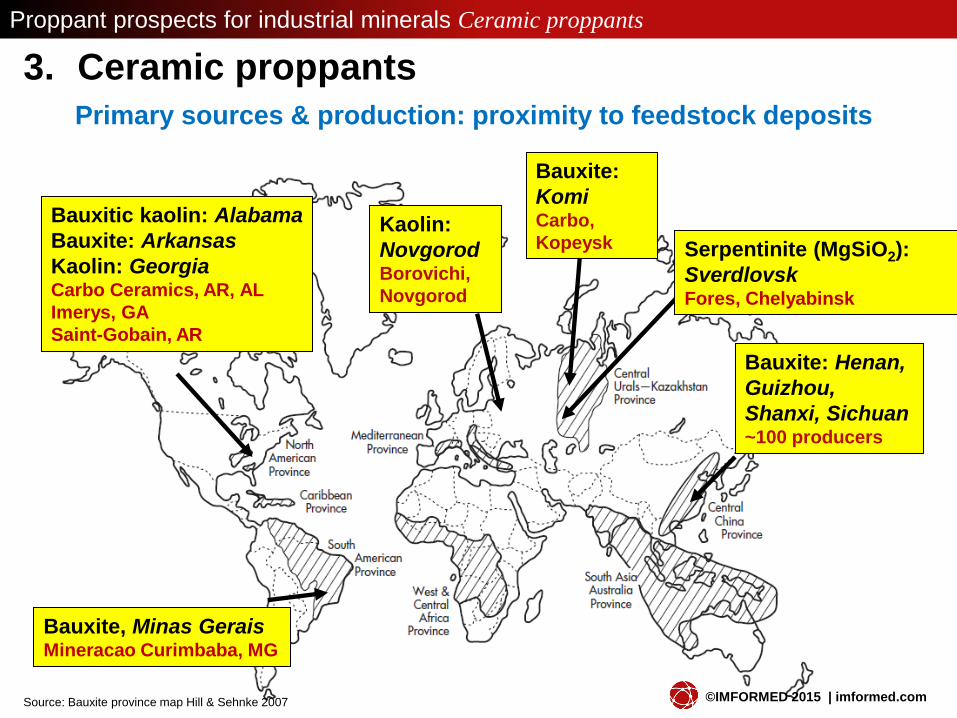

Source: Bauxite province map Hill & Sehnke 2007

Bauxitic kaolin: Alabama

Bauxite: Arkansas

Kaolin: Georgia Carbo Ceramics, AR, AL

Imerys, GA

Saint-Gobain, AR

Bauxite, Minas Gerais Mineracao Curimbaba, MG

Bauxite: Henan,

Guizhou,

Shanxi, Sichuan ~100 producers

Kaolin:

Novgorod Borovichi,

Novgorod

Serpentinite (MgSiO2):

Sverdlovsk Fores, Chelyabinsk

Bauxite:

Komi Carbo,

Kopeysk

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

3. Ceramic proppants

Primary sources & production: proximity to feedstock deposits

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

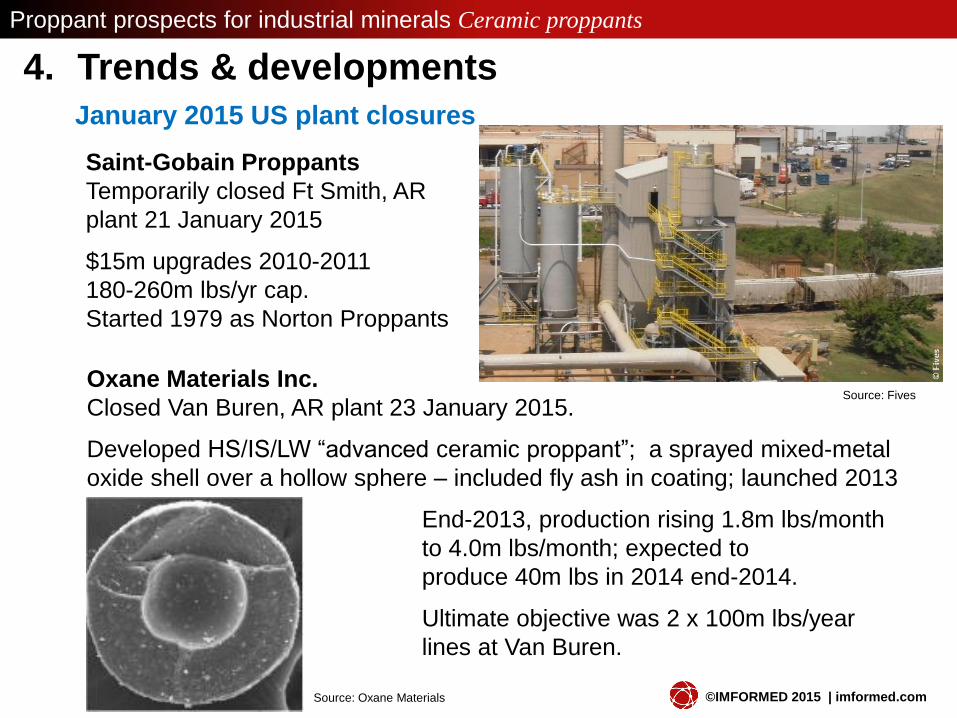

4. Trends & developments

January 2015 US plant closures

Saint-Gobain Proppants

Temporarily closed Ft Smith, AR

plant 21 January 2015

$15m upgrades 2010-2011

180-260m lbs/yr cap.

Started 1979 as Norton Proppants

Oxane Materials Inc.

Closed Van Buren, AR plant 23 January 2015.

Developed HS/IS/LW “advanced ceramic proppant”; a sprayed mixed-metal

oxide shell over a hollow sphere – included fly ash in coating; launched 2013

End-2013, production rising 1.8m lbs/month

to 4.0m lbs/month; expected to

produce 40m lbs in 2014 end-2014.

Ultimate objective was 2 x 100m lbs/year

lines at Van Buren.

Source: Fives

Source: Oxane Materials

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

4. Trends & developments

Expansions and investments

Curimbaba Group, Brazil

Oil price impact has placed on hold

planned 70,000 tpa (154.2m lbs/yr)

expansion with new plant originally

scheduled end-2015/early 2016

Source: Sintex

Prime Meridian/Hallmark Minerals

Prime Meridian Resources Corp., Canada LOI for 55% stake in

Hallmark Minerals (I) Pvt. Ltd, India

Aims to add 25,000 tpa (55m lbs/yr) to 10,000 tpa (22m lbs/yr) plant using

bauxite/clay blends.

Carbo Ceramics Inc.

Deferred completion of Millen Line 2

(250m lbs) until Q3 2015/2016

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

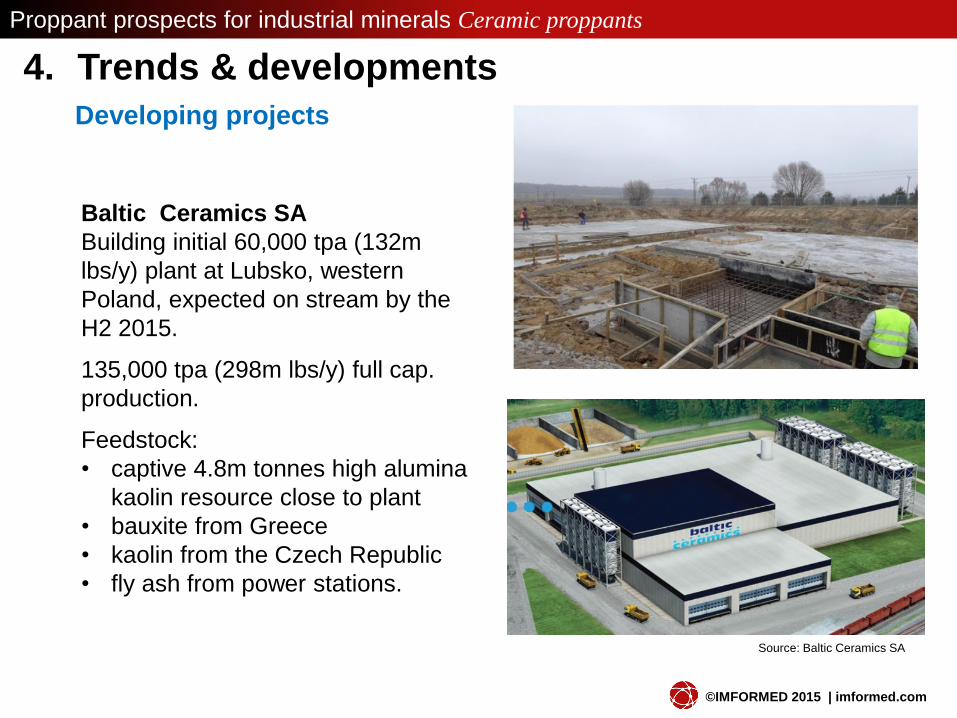

4. Trends & developments

Developing projects

Baltic Ceramics SA

Building initial 60,000 tpa (132m

lbs/y) plant at Lubsko, western

Poland, expected on stream by the

H2 2015.

135,000 tpa (298m lbs/y) full cap.

production.

Feedstock:

• captive 4.8m tonnes high alumina

kaolin resource close to plant

• bauxite from Greece

• kaolin from the Czech Republic

• fly ash from power stations.

Source: Baltic Ceramics SA

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

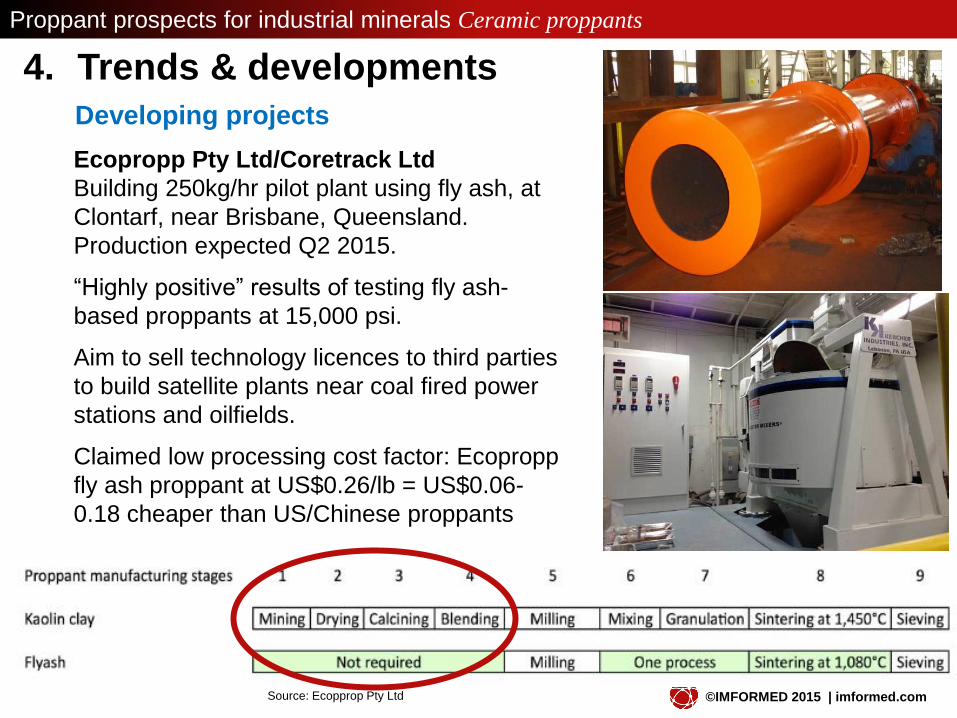

4. Trends & developments

Developing projects

Ecopropp Pty Ltd/Coretrack Ltd

Building 250kg/hr pilot plant using fly ash, at

Clontarf, near Brisbane, Queensland.

Production expected Q2 2015.

“Highly positive” results of testing fly ash-

based proppants at 15,000 psi.

Aim to sell technology licences to third parties

to build satellite plants near coal fired power

stations and oilfields.

Claimed low processing cost factor: Ecopropp

fly ash proppant at US$0.26/lb = US$0.06-

0.18 cheaper than US/Chinese proppants

Source: Ecopprop Pty Ltd

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

4. Trends & developments

Developing feedstock projects

Latin Resources Ltd

Developing the Guadalopito heavy minerals project 25km from Chimbote,

northern Peru. Seeking j-v partners.

Contains estimated 14-16m tonnes andalusite; 15m tpa conventional dredge

mining operation envisaged to yield 155,000 tpa andalusite.

Envisage proppant potential with andalusite blended with kaolin or other.

First Bauxite Corp.

Developing Bonasika bauxite deposit

60km south-west of Georgetown,

Guyana.

Evaluating revised plan for bauxite

mining and beneficiation in Guyana;

150,000 tpa calcining and sintering

plant in south Louisiana aimed at

ceramic proppant and refractory

makets. Source: First Bauxite Corp.

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

4. Trends & developments

Developing projects: Where did they go?

Shamrock Proppants LLC

In 2013, acquired Mid America Brick & Structural Clay Products plant, Mexico, MO.

Planning started 2013 2x 36.8 tph rotary kilns Wellsville, MO.

Feedstock: own kaolin resource (affiliated with Christy Minerals Inc.)

Applied Minerals Inc.

October 2013 agreement with OPF to

formulate ceramic proppants based on

halloysite clay from AMI’s developing

Dragon Mine, Utah.

March 2014 clay process plant

commissioned

Brownwood Clay Holdings LLC

Since 2011, developing with OPF Enterprises LLC a deposit in Brownwood, TX,

reportedly >10m s.tons inferred resource of “proppant grade clay”.

March 2014 secured property for plant build in Brownwood, but no construction

expected for “a couple more years”.

Source: Applied Minerals Inc.

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

4. Trends & developments

Developing projects: Bubbling under?

Kaolin AD, Bulgaria: kaolin Pasek Minerales, Spain: dunite

Source: Pasek Minerales

Source: Kaolin AD

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

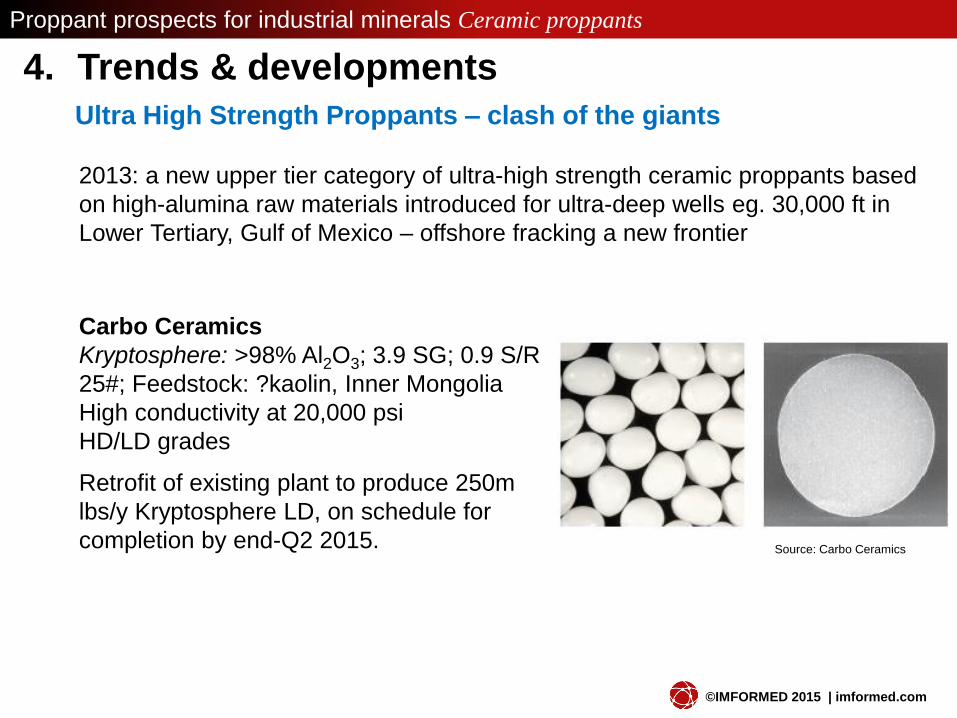

4. Trends & developments

Ultra High Strength Proppants – clash of the giants

2013: a new upper tier category of ultra-high strength ceramic proppants based

on high-alumina raw materials introduced for ultra-deep wells eg. 30,000 ft in

Lower Tertiary, Gulf of Mexico – offshore fracking a new frontier

Carbo Ceramics

Kryptosphere: >98% Al2O3; 3.9 SG; 0.9 S/R

25#; Feedstock: ?kaolin, Inner Mongolia

High conductivity at 20,000 psi

HD/LD grades

Retrofit of existing plant to produce 250m

lbs/y Kryptosphere LD, on schedule for

completion by end-Q2 2015. Source: Carbo Ceramics

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

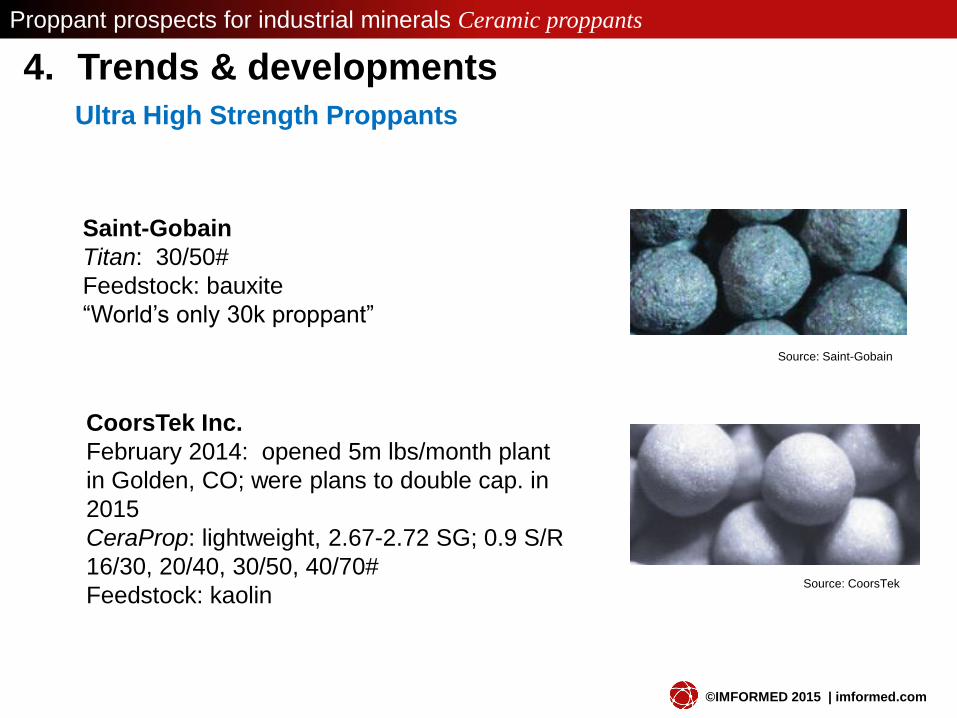

4. Trends & developments

Ultra High Strength Proppants

CoorsTek Inc.

February 2014: opened 5m lbs/month plant

in Golden, CO; were plans to double cap. in

2015

CeraProp: lightweight, 2.67-2.72 SG; 0.9 S/R

16/30, 20/40, 30/50, 40/70#

Feedstock: kaolin

Saint-Gobain

Titan: 30/50#

Feedstock: bauxite

“World’s only 30k proppant”

Source: CoorsTek

Source: Saint-Gobain

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

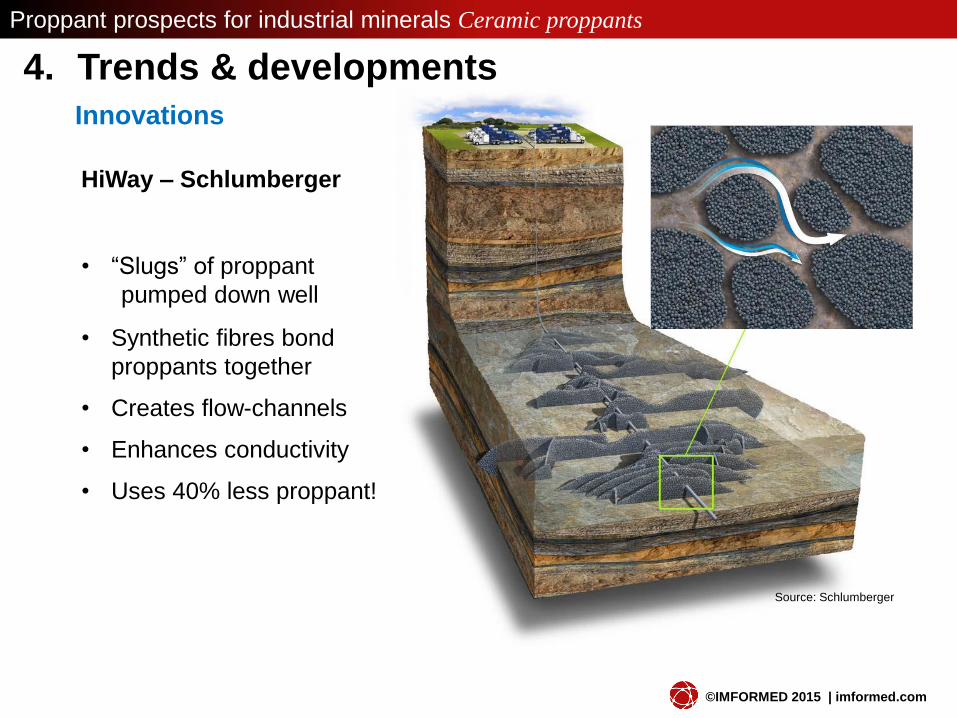

4. Trends & developments

Innovations

HiWay – Schlumberger

• “Slugs” of proppant

pumped down well

• Synthetic fibres bond

proppants together

• Creates flow-channels

• Enhances conductivity

• Uses 40% less proppant!

Source: Schlumberger

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

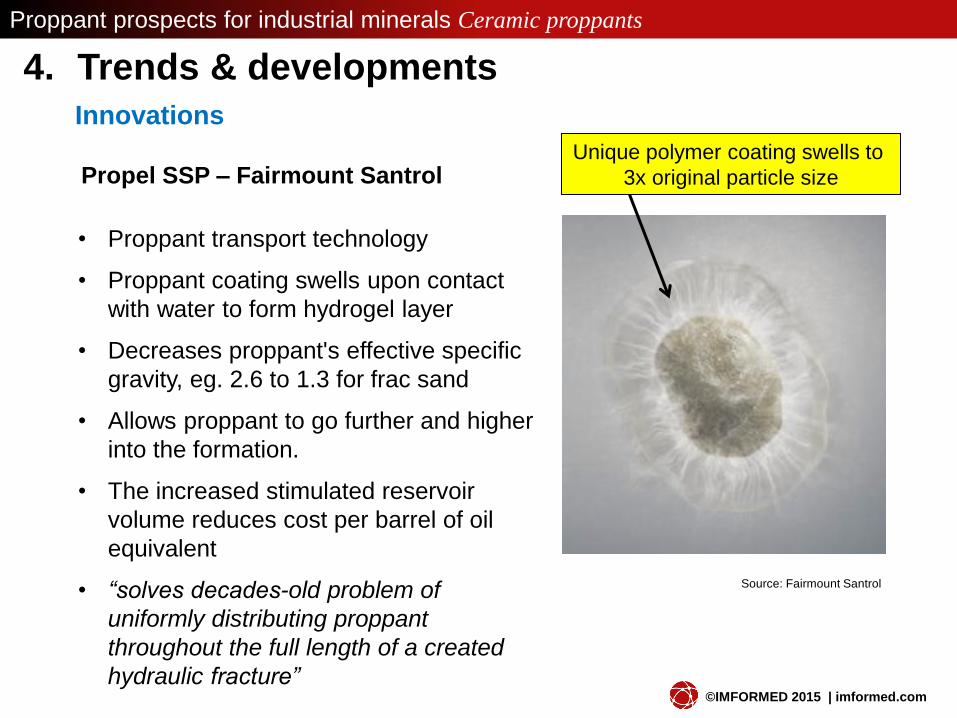

4. Trends & developments

Innovations

Propel SSP – Fairmount Santrol

• Proppant transport technology

• Proppant coating swells upon contact

with water to form hydrogel layer

• Decreases proppant's effective specific

gravity, eg. 2.6 to 1.3 for frac sand

• Allows proppant to go further and higher

into the formation.

• The increased stimulated reservoir

volume reduces cost per barrel of oil

equivalent

• “solves decades-old problem of

uniformly distributing proppant

throughout the full length of a created

hydraulic fracture”

Unique polymer coating swells to

3x original particle size

Source: Fairmount Santrol

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

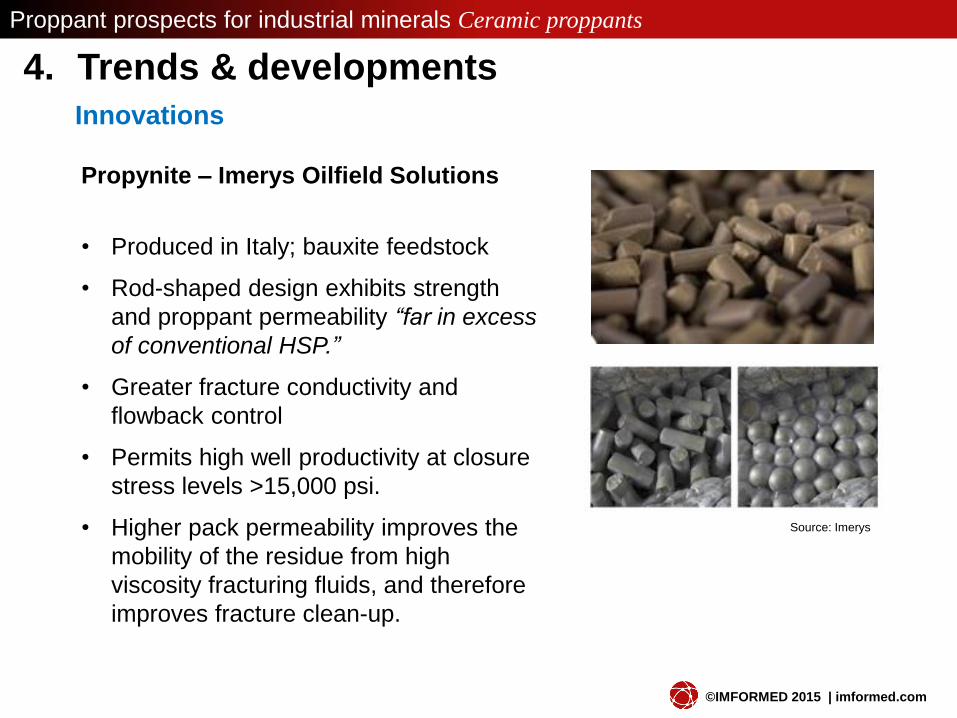

4. Trends & developments

Innovations

Propynite – Imerys Oilfield Solutions

• Produced in Italy; bauxite feedstock

• Rod-shaped design exhibits strength

and proppant permeability “far in excess

of conventional HSP.”

• Greater fracture conductivity and

flowback control

• Permits high well productivity at closure

stress levels >15,000 psi.

• Higher pack permeability improves the

mobility of the residue from high

viscosity fracturing fluids, and therefore

improves fracture clean-up.

Source: Imerys

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

4. Trends & developments

Innovations

In-situ proppant formation – Oil Chem Technologies

• fracturing fluid itself forms the proppant

• little or no material is carried back to be treated or disposed of

• size of proppant can range <1mm - >20 mm by modifying fracturing fluid

composition.

• No polymer is required to suspend the proppant, hence no breakers are

required

• proppants are perfectly spherical particles with hardness equal or

exceeding conventional proppants.

• Highly permeable solid masses can also be formed within the fracture

using hydraulic fluids containing no solids.

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

4. Trends & developments

Proppant application: trend to using more frac sand

• 2013-14 E&P practice of using higher volumes of frac sand, and only “tailing

in” ceramic proppants

• In softer, ductile formations like Eagle Ford, Permian, rock wraps around

proppant reducing conductivity – solution to overload with proppants to plug

short, wide fractures = using more lower cost FS rather than CP

• Major players switched to FS-only in Eagle Ford: EOG, Pioneer, Anadarko,

ConocoPhillips

• EOG also intensive FS use in Bakken wells increased productivity

• Q2 2014; Rosetta Resources Inc. revised completion design in Eagle Ford

by increasing FS volumes against CP volumes = cost savings $0.5m/well or

250-500m lbs CP

• But after initial high well productivity, it declines steeply soon after, therefore

perhaps only a short term solution – CP will always outperform FS

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

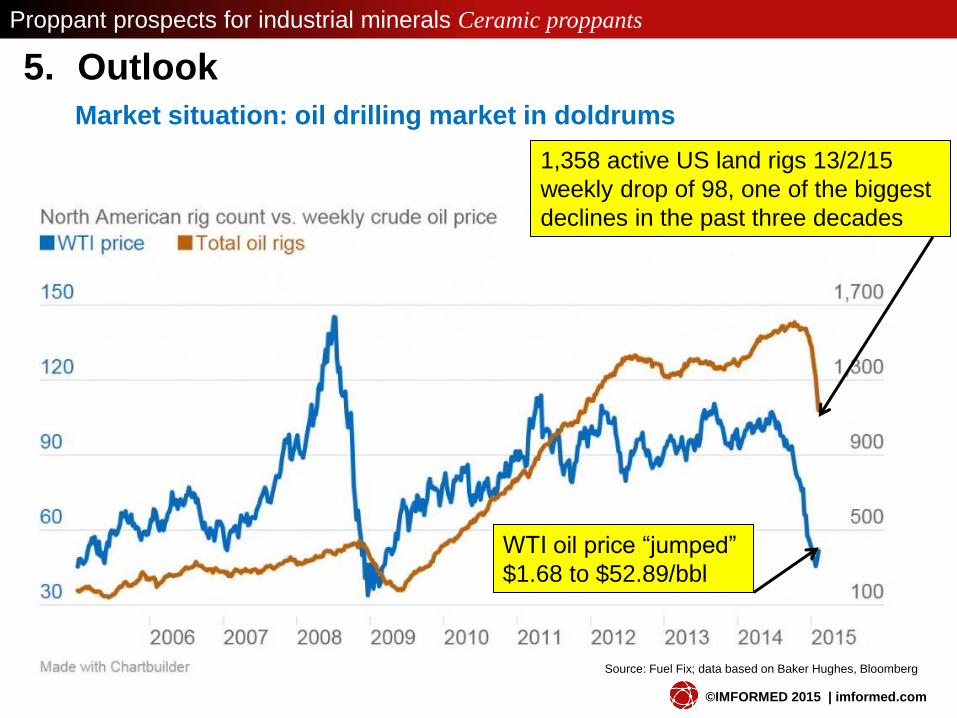

1,358 active US land rigs 13/2/15

weekly drop of 98, one of the biggest

declines in the past three decades

Source: Fuel Fix; data based on Baker Hughes, Bloomberg

5. Outlook

Market situation: oil drilling market in doldrums

WTI oil price “jumped”

$1.68 to $52.89/bbl

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

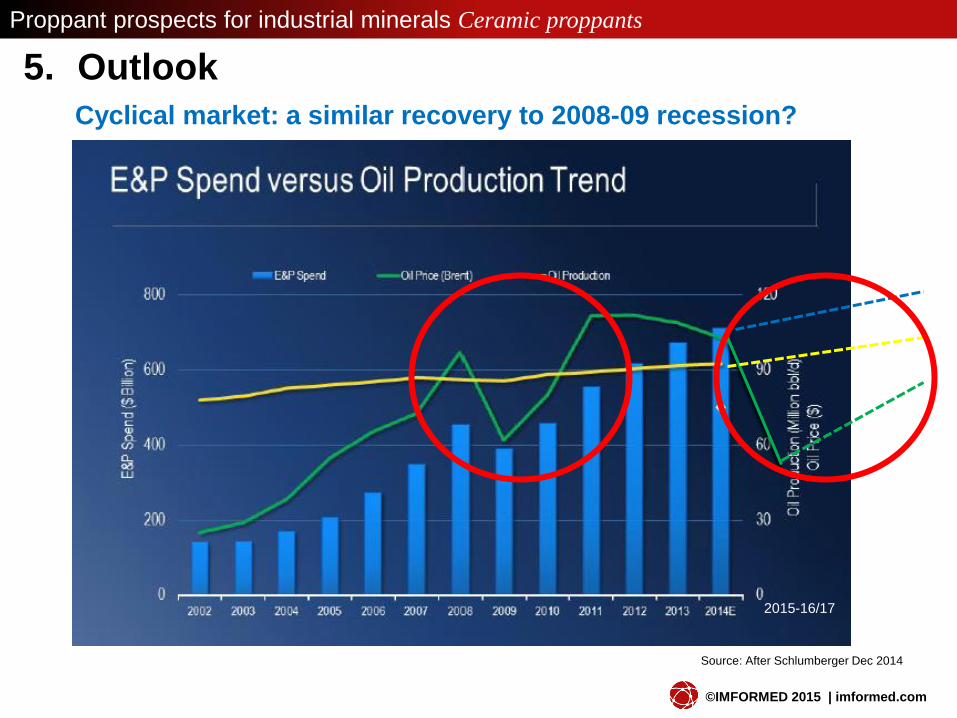

5. Outlook

Cyclical market: a similar recovery to 2008-09 recession?

Source: After Schlumberger Dec 2014

2015-16/17

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

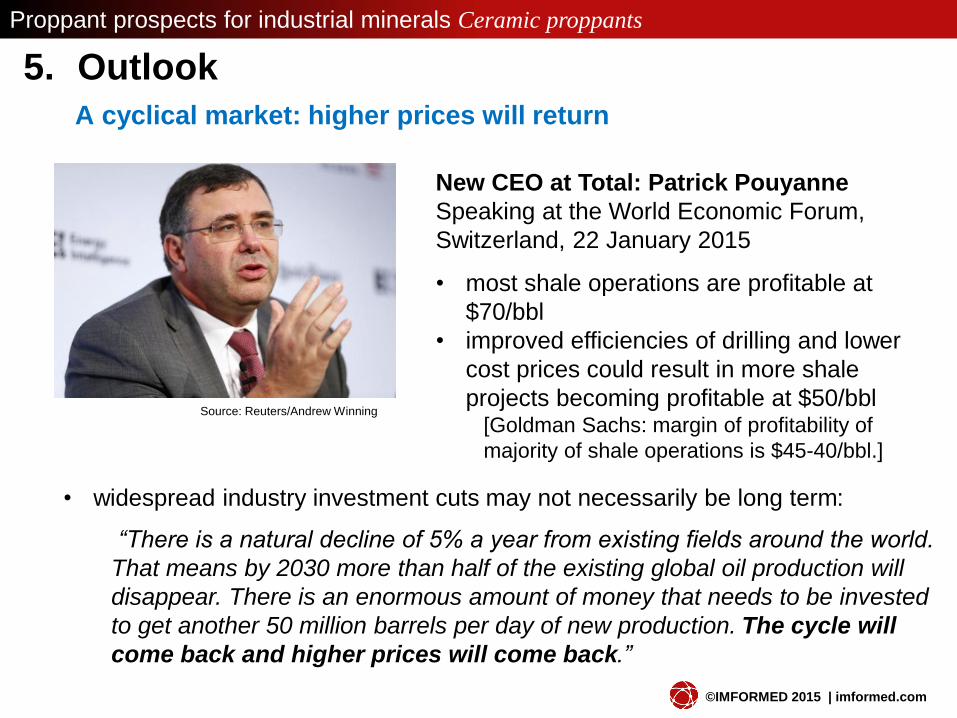

• most shale operations are profitable at

$70/bbl

• improved efficiencies of drilling and lower

cost prices could result in more shale

projects becoming profitable at $50/bbl [Goldman Sachs: margin of profitability of

majority of shale operations is $45-40/bbl.]

New CEO at Total: Patrick Pouyanne

Speaking at the World Economic Forum,

Switzerland, 22 January 2015

5. Outlook

A cyclical market: higher prices will return

• widespread industry investment cuts may not necessarily be long term:

“There is a natural decline of 5% a year from existing fields around the world.

That means by 2030 more than half of the existing global oil production will

disappear. There is an enormous amount of money that needs to be invested

to get another 50 million barrels per day of new production. The cycle will

come back and higher prices will come back.”

Source: Reuters/Andrew Winning

Proppant prospects for industrial minerals Ceramic proppants

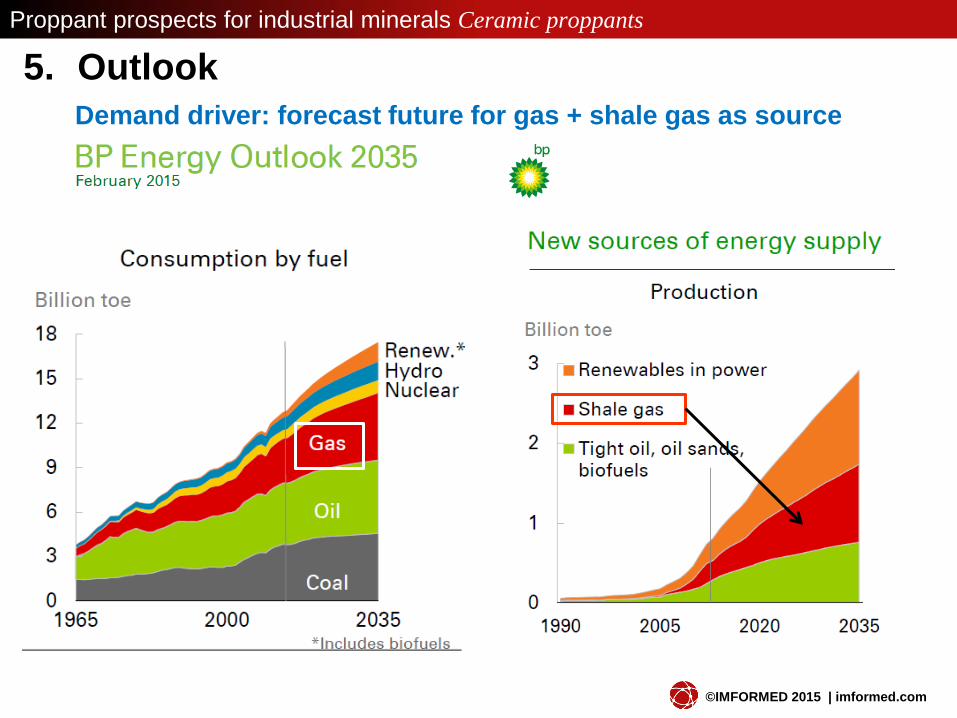

5. Outlook

Demand driver: forecast future for gas + shale gas as source

©IMFORMED 2015 | imformed.com

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

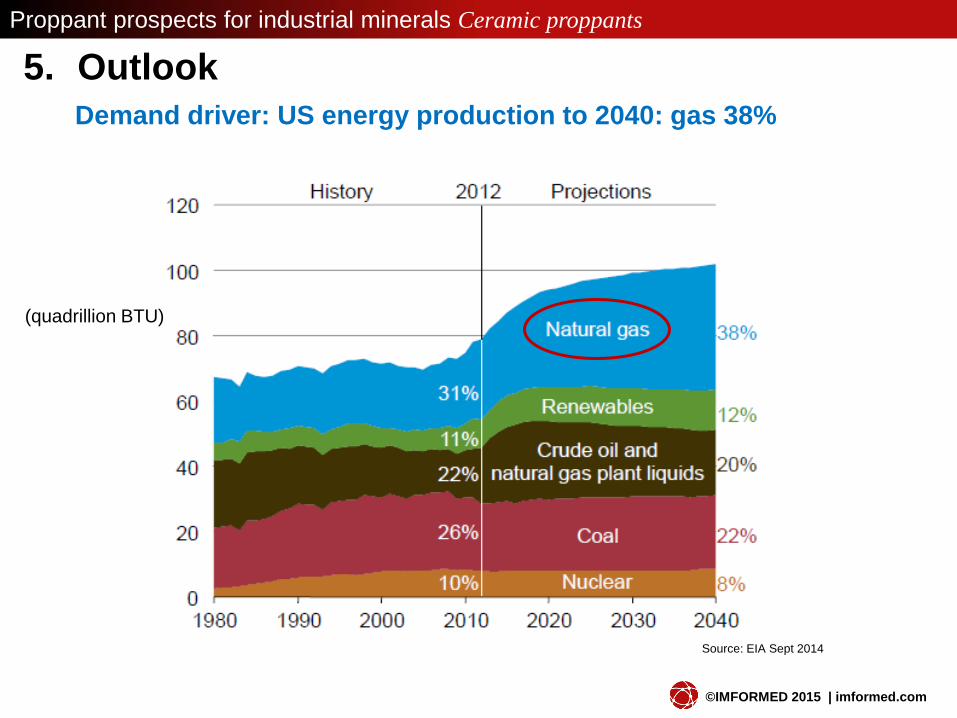

5. Outlook

Demand driver: US energy production to 2040: gas 38%

Source: EIA Sept 2014

(quadrillion BTU)

China

USA

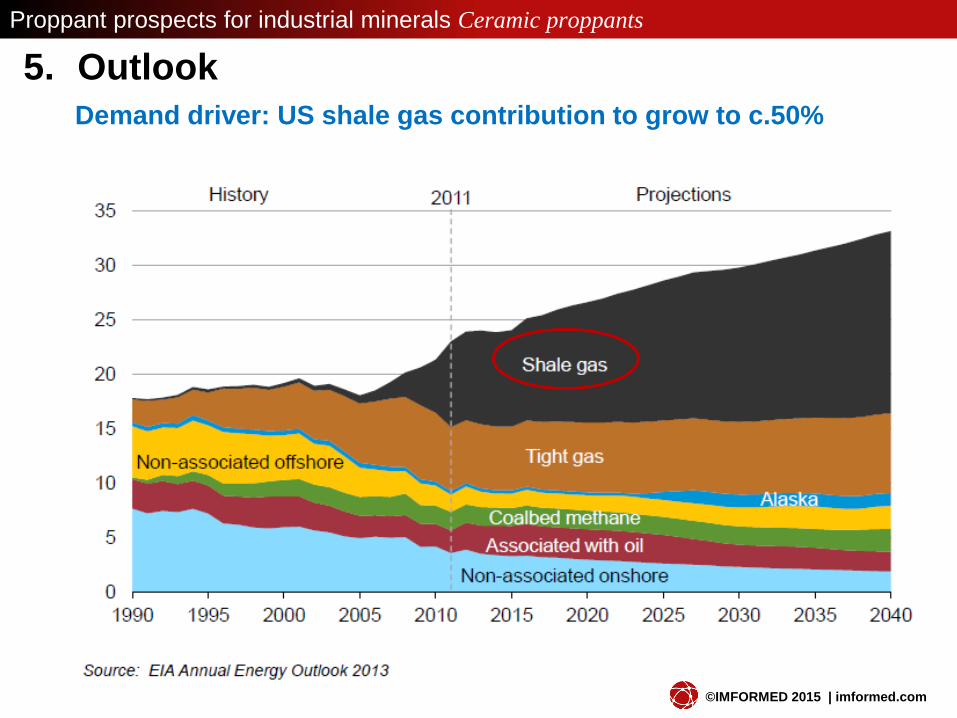

5. Outlook

Demand driver: US shale gas contribution to grow to c.50%

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

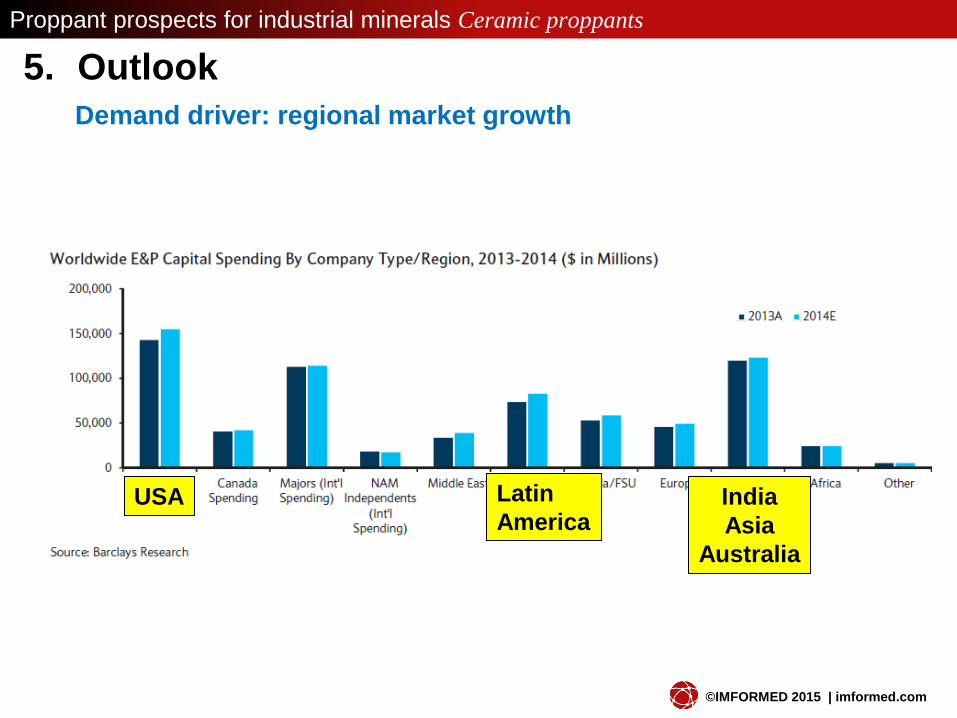

China

USA USA Latin

America India

Asia

Australia

Proppant prospects for industrial minerals Ceramic proppants

5. Outlook

Demand driver: regional market growth

©IMFORMED 2015 | imformed.com

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

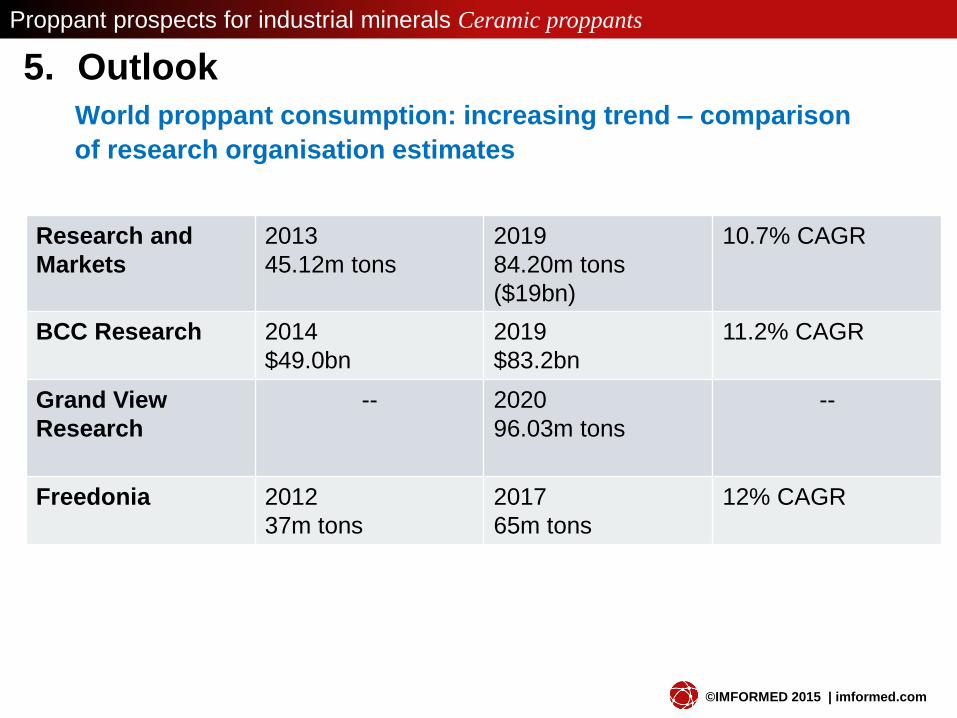

5. Outlook

World proppant consumption: increasing trend – comparison

of research organisation estimates

Research and

Markets

2013

45.12m tons

2019

84.20m tons

($19bn)

10.7% CAGR

BCC Research 2014

$49.0bn

2019

$83.2bn

11.2% CAGR

Grand View

Research

-- 2020

96.03m tons

--

Freedonia 2012

37m tons

2017

65m tons

12% CAGR

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

5. Outlook

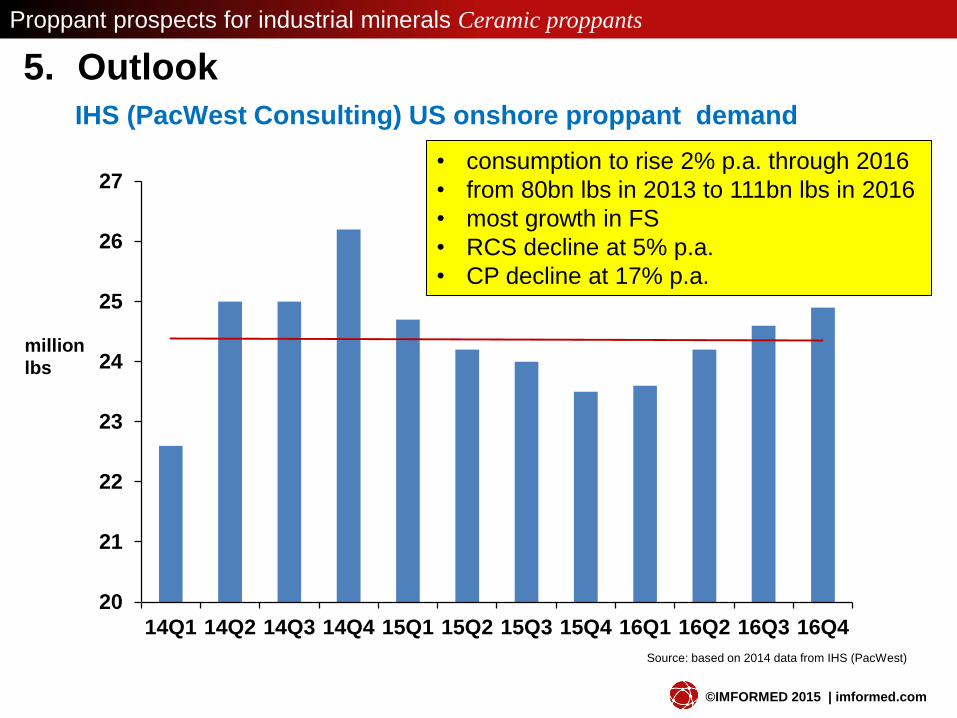

IHS (PacWest Consulting) US onshore proppant demand

20

21

22

23

24

25

26

27

14Q1 14Q2 14Q3 14Q4 15Q1 15Q2 15Q3 15Q4 16Q1 16Q2 16Q3 16Q4

Source: based on 2014 data from IHS (PacWest)

million

lbs

• consumption to rise 2% p.a. through 2016

• from 80bn lbs in 2013 to 111bn lbs in 2016

• most growth in FS

• RCS decline at 5% p.a.

• CP decline at 17% p.a.

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

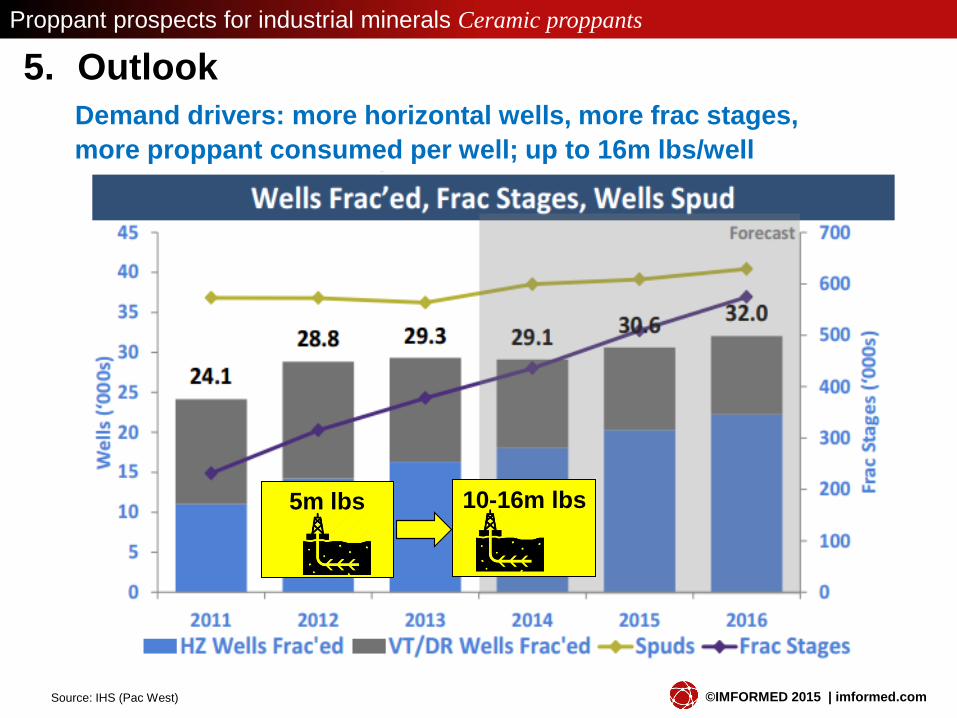

5. Outlook

Demand drivers: more horizontal wells, more frac stages,

more proppant consumed per well; up to 16m lbs/well

Source: IHS (Pac West)

5m lbs

10-16m lbs

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

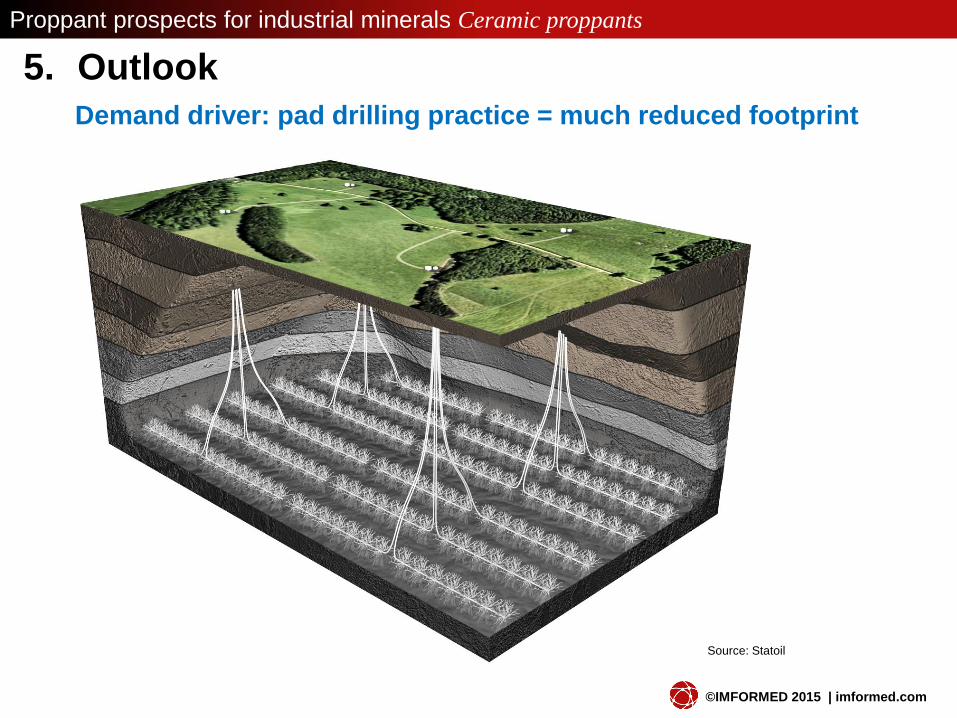

5. Outlook

Demand driver: pad drilling practice = much reduced footprint

Source: Statoil

Proppant prospects for industrial minerals Ceramic proppants

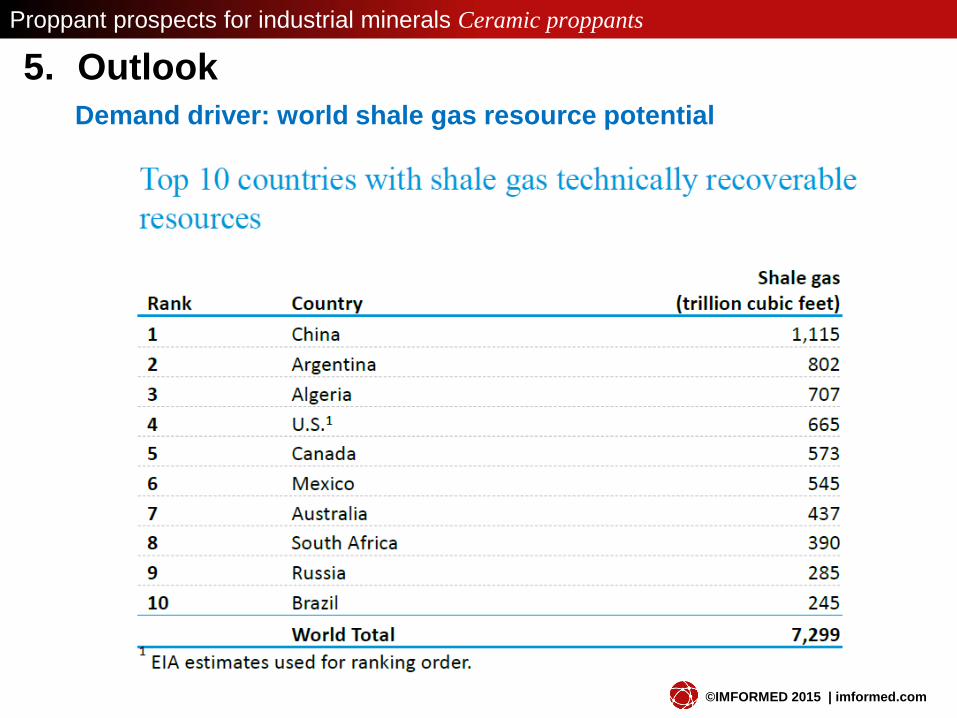

5. Outlook

Demand driver: world shale gas resource potential

©IMFORMED 2015 | imformed.com

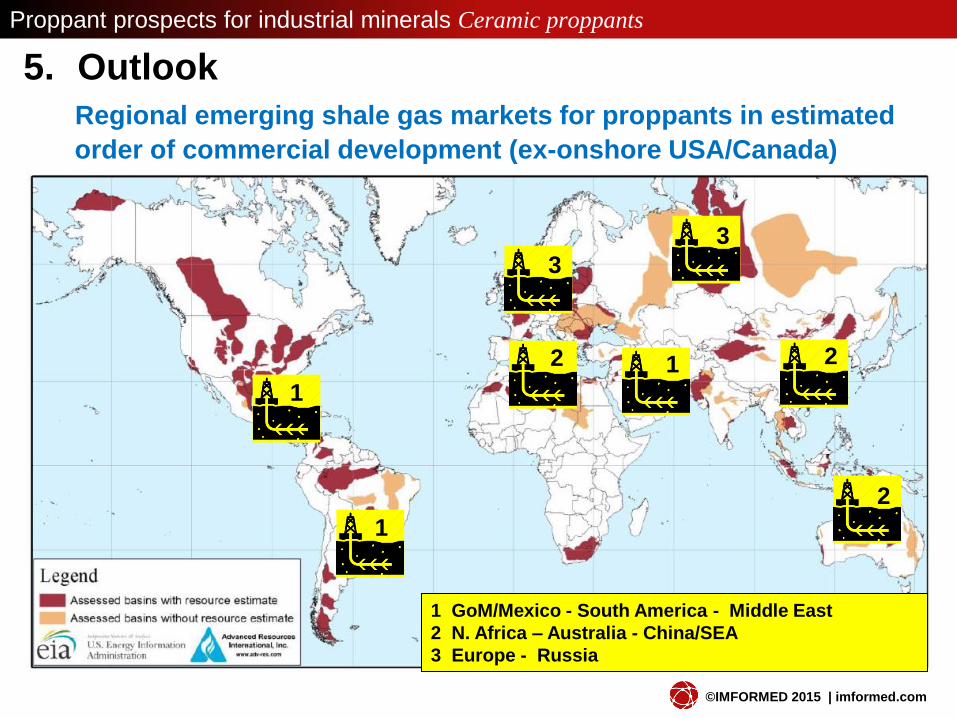

5. Outlook

Regional emerging shale gas markets for proppants in estimated

order of commercial development (ex-onshore USA/Canada)

Proppant prospects for industrial minerals Ceramic proppants

1

1

1

2

2 2

3

3

1 GoM/Mexico - South America - Middle East

2 N. Africa – Australia - China/SEA

3 Europe - Russia

©IMFORMED 2015 | imformed.com

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

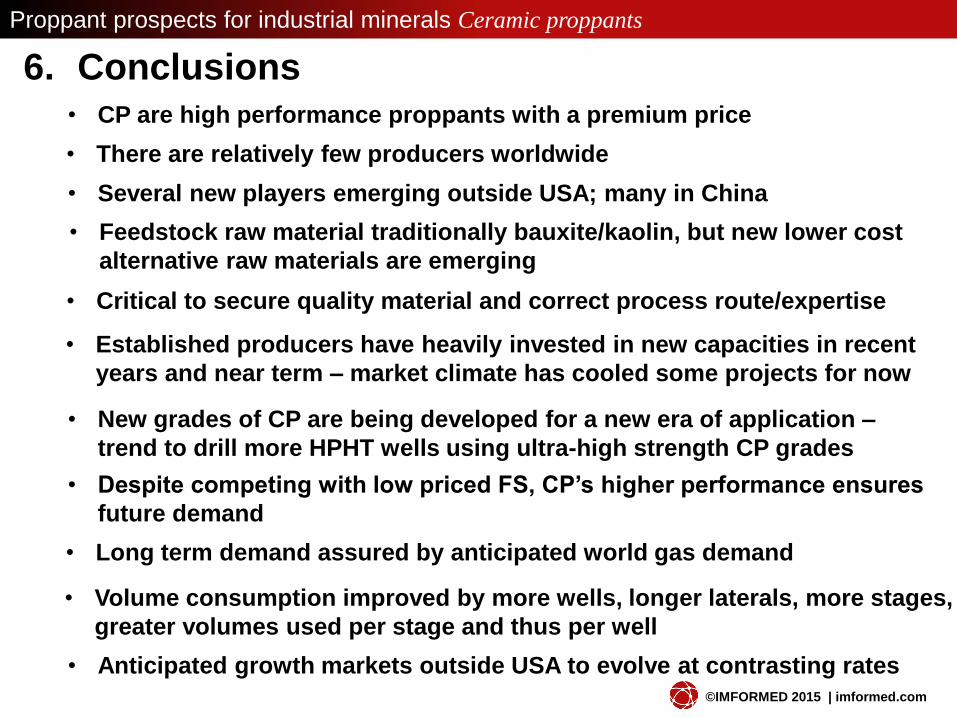

6. Conclusions • CP are high performance proppants with a premium price

• There are relatively few producers worldwide

• Feedstock raw material traditionally bauxite/kaolin, but new lower cost

alternative raw materials are emerging

• Critical to secure quality material and correct process route/expertise

• Several new players emerging outside USA; many in China

• Established producers have heavily invested in new capacities in recent

years and near term – market climate has cooled some projects for now

• New grades of CP are being developed for a new era of application –

trend to drill more HPHT wells using ultra-high strength CP grades

• Despite competing with low priced FS, CP’s higher performance ensures

future demand

• Long term demand assured by anticipated world gas demand

• Volume consumption improved by more wells, longer laterals, more stages,

greater volumes used per stage and thus per well

• Anticipated growth markets outside USA to evolve at contrasting rates

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

6. Conclusions • CP are high performance proppants with a premium price

• There are relatively few producers worldwide

• Feedstock raw material traditionally bauxite/kaolin, but new lower cost

alternative raw materials are emerging

• Critical to secure quality material and correct process route/expertise

• Several new players emerging outside USA; many in China

• Established producers have heavily invested in new capacities in recent

years and near term – market climate has cooled these projects for now

• New grades of CP are being developed for a new era of application –

trend to drill more HTHP wells

• Despite competing with “dirt” (FS), CP’s high performance ensures future

demand

• Long term demand assured by anticipated world gas demand

• Volume consumption improved by more wells, longer laterals, more stages,

greater volumes used per stage and thus well

• Anticipated growth markets outside USA

Proppant

prospects for

industrial

minerals…are

good!

Proppant prospects for industrial minerals Ceramic proppants

©IMFORMED 2015 | imformed.com

Sponsors Media

Partner

Proppant prospects for industrial minerals Ceramic proppants

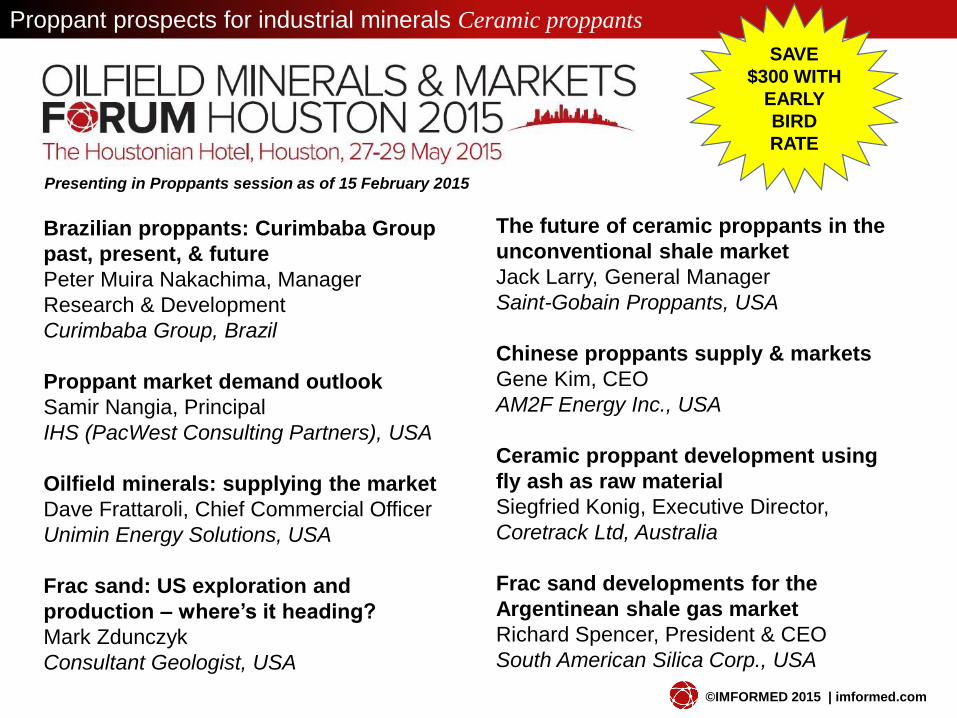

Brazilian proppants: Curimbaba Group

past, present, & future

Peter Muira Nakachima, Manager

Research & Development

Curimbaba Group, Brazil

Proppant market demand outlook

Samir Nangia, Principal

IHS (PacWest Consulting Partners), USA

Oilfield minerals: supplying the market

Dave Frattaroli, Chief Commercial Officer

Unimin Energy Solutions, USA

Frac sand: US exploration and

production – where’s it heading?

Mark Zdunczyk

Consultant Geologist, USA

©IMFORMED 2015 | imformed.com

The future of ceramic proppants in the

unconventional shale market

Jack Larry, General Manager

Saint-Gobain Proppants, USA

Chinese proppants supply & markets

Gene Kim, CEO

AM2F Energy Inc., USA

Ceramic proppant development using

fly ash as raw material

Siegfried Konig, Executive Director,

Coretrack Ltd, Australia

Frac sand developments for the

Argentinean shale gas market

Richard Spencer, President & CEO

South American Silica Corp., USA

SAVE

$300 WITH

EARLY

BIRD

RATE

Presenting in Proppants session as of 15 February 2015

Thank you for your attention.

If you have any questions or comments,

or would like more information, please contact me.

Proppant prospects for industrial minerals Ceramic proppants

imformed.com

[email protected] | +44 (0)1372 450 679 | mobile +44 (0)7985 986 255