Proposition to improve mobile money services for cash ... to improve mobile money services for cash...

15

Proposition to improve mobile money services for cash transfer interventions (and financial inclusion) Cash Working Group - Goma – October 28 th 2016

-

Upload

phungthien -

Category

Documents

-

view

217 -

download

2

Transcript of Proposition to improve mobile money services for cash ... to improve mobile money services for cash...

Proposition to improve mobile money services for cash transfer interventions (and financial inclusion)

Cash Working Group - Goma – October 28th 2016

CONTENTS

• Who are we?• Mobile money experience on cash transfer and financial inclusion in the World and

DRC• Proposed solutions to make mobile money a viable solution for cash transfer and

financial inclusion• Next steps• Questions

WHO ARE WE?

£50mProgramme

5Bureaux

44core staff

ELAN DRC is a private sector development program that aims to increasethe income of over a million low-income men and women in the DRC by2020.

It provides international expertise and market insight to businesses, financialinstitutions and industry associations, supporting them to innovate and grow.

It is implemented by the consultancy firm Adam Smith International andsupported by the UK government as part of its private sector developmentstrategy in the DRC.

ELAN RDCBranchless banking strategy (mobile money and agency

network)

1. Increased confidence in alternative distribution channels

2. MNOs and financial institutions offer appropriateproducts/services to poor consumers

3. MNOs and financial institutions improve agents quality servicesand expand agents network to serve poor consumers

Main Branchless banking achievements

1. Study on consumer financial needs & behaviour assessment

2. Orange Money agent distribution network training anddevelopment

3. Joined TV and radio educational campaign with Airtel Money ,Tigo cash, M-Pesa and BCC

4. Tigo Cash Women Micro-entrepreneurs Agent network

5. Study on opportunities on mobile money for financialinstitutions

MOBILE MONEY EXPERIENCE ON CASH TRANSFER AND FINANCIAL INCLUSION IN THE WORLD AND DRC

Mobile Money, a pertinent tool for cash transfer intervention and financial inclusion

Observation Proposition Justification for mobile money

Movement in the aid industry to advocatefor a shift away from in-kind aid towardscash transfer programmes as ahumanitarian tool.

Cash transfers rose up to 6% of totalhumanitarian spending in 2015 from 1% in2004.

Cash transfers do not distort local marketsfor goods and services and as such shouldbe closely looked at by MSD programmes.

Increasing recognition of the vital role ofcomplementary interventions (humanitarianaid and market system developmentprograms).

Increase linkages and collaborationbetween humanitarian aid and marketsystems development programs tocreate a favourable environment for mobilemoney to:

1. Enable efficient cash transferinterventions to displaced people in acrisis context;

2. Encourage financial inclusion in a preand post crisis context.

Humanitarian AidExample of successful use of cash transferin Kenya and Somalia.

Financial inclusion271 mobile money services in the worldand 441 millions mobile money accounts in93 countries, 30% being actives (but only11% have more than 1M active users).

Financial inclusion after crisis contextin Malawi, Opportunity International Bankreports that 45% of recipients enrolled inthe Dowa Emergency Cash Transferscheme are still using their bank accountmore than 2 years after the end of theprogramme.

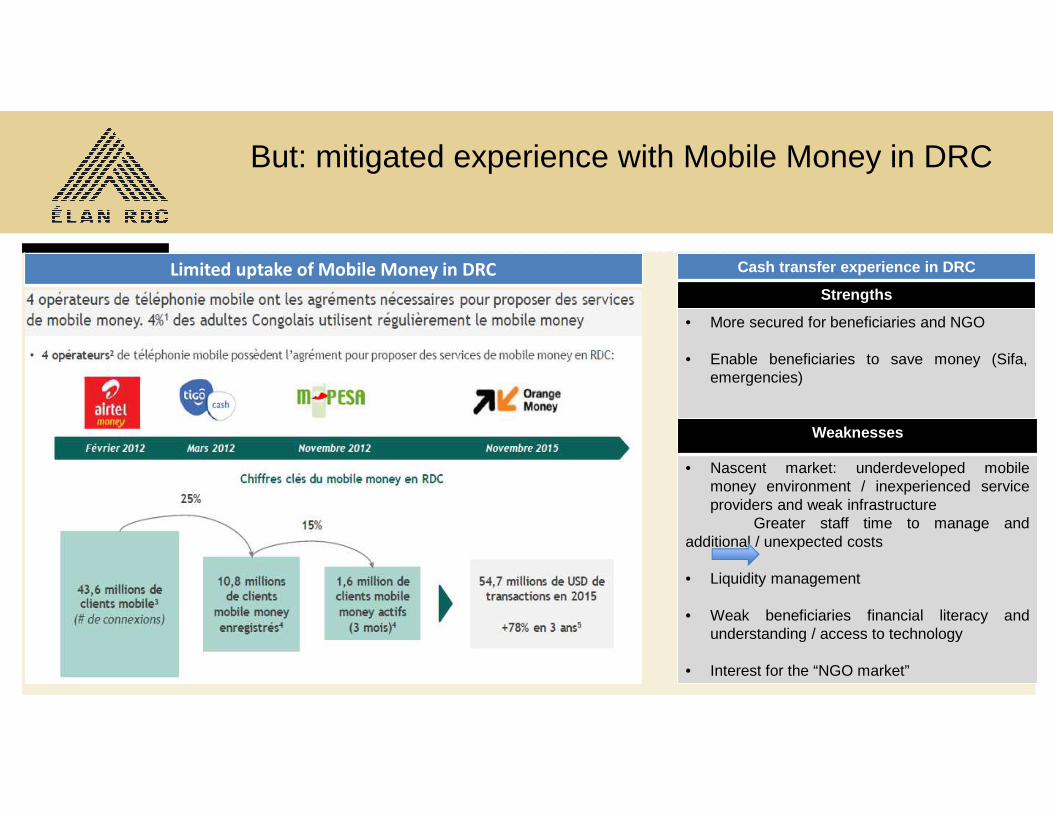

But: mitigated experience with Mobile Money in DRC

Cash transfer experience in DRC

Strengths

• More secured for beneficiaries and NGO

• Enable beneficiaries to save money (Sifa,emergencies)

Weaknesses

• Nascent market: underdeveloped mobilemoney environment / inexperienced serviceproviders and weak infrastructure

Greater staff time to manage andadditional / unexpected costs

• Liquidity management

• Weak beneficiaries financial literacy andunderstanding / access to technology

• Interest for the “NGO market”

Limited uptake of Mobile Money in DRC

HOW TO MAKE MOBILE MONEY A VIABLE OPTION FOR CASH TRANSFER AND FINANCIAL INCLUSION IN DRC?

Ecosystem set Standard mode

TransferAgents

Salary paymentMerchants

Cash deposit

Float replenishing

MM

conversion

Customer

Mobile money provisioningMobile money provisioning

Mobile money service

Ecosystem Set up• Customer education• Distribution network set up

• Select and recruit the agents

• Select and recruit the merchants

• Training modules• Distribution management tools• Select and recruit the IMF

ELAN RDC intervention:• Technical assistance• Training and education

programme development• Co-funding consultant payment

Recommend to bring in a FI as cash partner:• More payment to Merchants and less withdrawal • More Merchants mobile money conversion and less Agent cash replenishment

Payment

Cash out Cash in

Legal, regulatory and compliance framework and

process

Ecosystem setIntervention mode

Agents

Merchants

MM

conversion

Contract sign offFund provisioningNGO

NGO MPESA Account

m-pesa account credited

Bulk payment

Payment

Cash out

Float replenishment

Beneficiary registration and KYC framework

Information/ education, ME, SIM safe keeping and CRM framework

Distribution network set up:• IMF recruitment• Agents/merchant qualification FW• Recruiting Agents/merchants• Training program• Distribution tracking tools

Summary of advantages of the proposed model

Actors Advantages

Local economy

1. Development of the local economy thanks to the creation of a mobile money ecosystem2. Less pressure on cash availability3. Improved security4. Financial inclusion

Beneficiaries

1. Improved security2. Easy access to goods without pressure on cash3. Time saving4. Financial inclusion

NGO

1. Improved security2. Improved transparency3. Time saving4. Reporting5. Reinforced relationship with MNO

MNO1. Reinforced infrastructure2. Reinforced relationship with NGO

Risks and mitigation actions

Risks Mitigation actions Who does? Who pays (tbc)?

Slow start up Preparation plan ELAN / MPESA / NGO

“Entrée en relation” / contract signatureDevelopment of transparent procedures andprocesses to be communicated to NGOs

ELAN / MPESA with thesupport of NGOs

ELAN / MPESA

Mpesa accounts opening forbeneficiaries (KYC)

NGO bears the risk and open accounts on behalf ofbeneficiaries

ELAN / MPESA / NGO NGO

Quality of the distribution network(agents/merchants)

Improvement of distribution management proceduresand training of agents / merchants

ELAN / MPESA ELAN / MPESA

Merchants’ lack of understanding oftechnology and interest in MM

Development of training tools + trainingIncentive systemBusiness case for merchants

ELAN / MPESA / NGOELAN / MPESA / NGO

Unavailability of mobile phones andburden on vendors

MPesa lends phones to merchants MPESA MPESA

Beneficiaries’ lack of understanding oftechnology and customer protection

Development of training and CRM tools (leaflets,posters etc…)Training of beneficiaries

ELAN / MPESA / NGO ELAN / MPESA / NGO

MFI’s lack of understanding of theprocess

Development of transparent proceduresBusiness case for MFI

ELAN / MPESA ELAN / MPESA

Identification of the pilot area(s) NGO proposes most likely affected areas NGO

NEXT STEPS

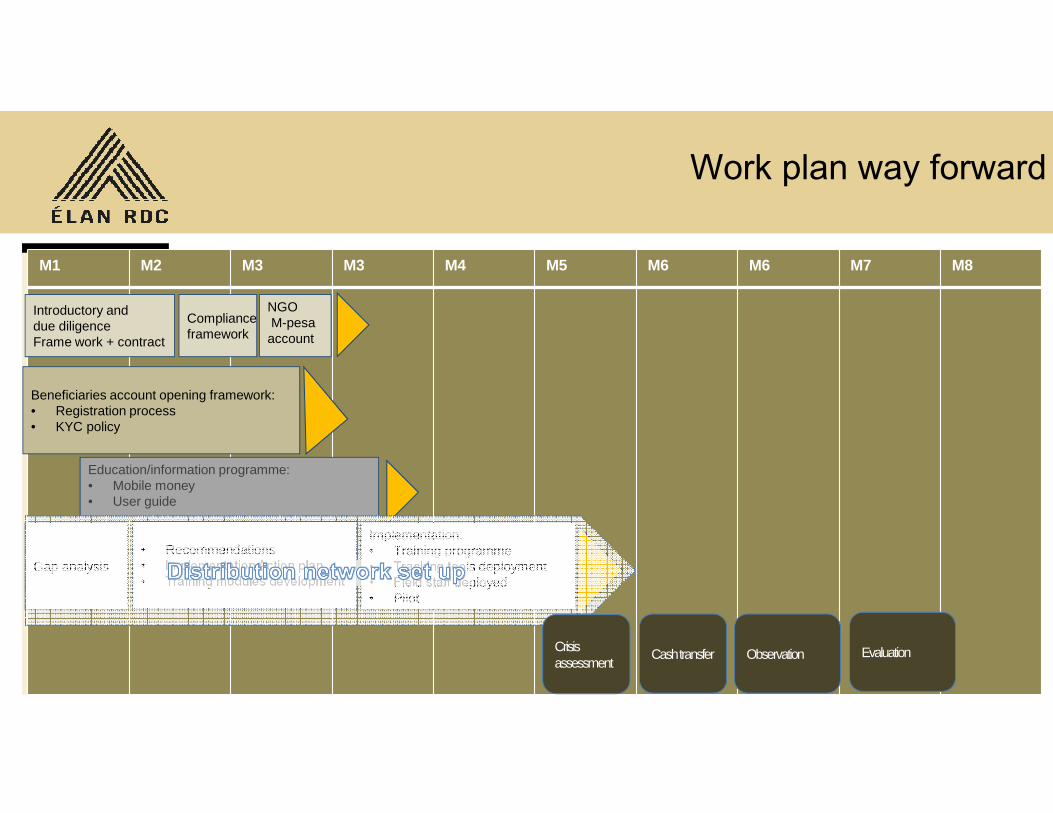

Work plan way forward

M1 M2 M3 M3 M4 M5 M6 M6 M7 M8

Introductory and due diligence Frame work + contract

Compliance framework

NGOM-pesa account

Beneficiaries account opening framework:• Registration process• KYC policy

Education/information programme:• Mobile money• User guide

Gap analysis• Recommendations• Implementation Action plan• Training modules development

Implementation:• Training programme• Tracking tools deployment• Field staff deployed• Pilot

Crisisassessment

Cashtransfer Observation Evaluation

QUESTIONS / DISCUSSION