Proposed Acquisition of Wells Fargo’s Share Registration .../media/Files/E/... · (7) The rights...

31

12 July 2017 Proposed Acquisition of Wells Fargo’s Share Registration & Services Business (WFSS) Combining Two Leading Share Registry Businesses

Transcript of Proposed Acquisition of Wells Fargo’s Share Registration .../media/Files/E/... · (7) The rights...

12 July 2017

Proposed Acquisition of Wells Fargo’s Share Registration & Services Business (WFSS)

Combining Two Leading Share Registry Businesses

This presentation comprises the written materials/slides for a presentation concerning the proposed acquisition and rights issue by Equiniti Group PLC (the "Company") (the "Transaction"). The following applies to the

presentation materials following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the presentation materials. In accessing the presentation materials, you

agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such. By attending this presentation you acknowledge and accept

that some or all of the information in this presentation may be inside information and/or price sensitive information. The provisions of applicable securities laws may restrict or prohibit the use and/or disclosure of such

information, and by attending the presentation you agree to comply with such laws.

This document does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any shares in the Company or securities in any other entity nor shall it

or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision in relation thereto. This document does not constitute a recommendation regarding

shares of the Company. The information contained herein is for discussion purposes only and does not purport to contain all information that may be required to evaluate the Company and/or its financial position.

The contents of this presentation are to be kept confidential. The contents of this presentation have not been verified by the Company, Greenhill & Co International LLP, Citigroup Global Markets Limited, or Barclays Bank

PLC (together, the "Banks").

This document is an advertisement and not a prospectus and investors should not subscribe for any shares referred to in this document except on the basis of information in the prospectus expected to be published by the

Company on around September 2017 (the "Prospectus"). Copies of the Prospectus will, following publication, be available from the Company at its registered office. The Prospectus includes a description of risk factors in

relation to an investment in the Company. This presentation contains forward-looking statements that involve substantial risks and uncertainties and actual results and developments may differ materially from those

expressed or implied by these statements or a variety of factors. These forward-looking statements are subject to risks, uncertainties and assumptions about the Company and its subsidiaries and investments, including

those described in the risk factor section of the Prospectus. These forward looking statements speak only as of the date of this presentation and are subject to updating, revision, verification and amendment without

notice and such information may change materially. Neither the Company nor the Banks nor any other person are under an obligation to correct, update or keep current the information contained in this presentation or to

publicly announce or inform you of the result of any revision to the statements made herein except where they would be required to do so under applicable law.

No reliance may be placed for any purposes whatsoever on the information contained in this presentation or on its completeness. No representation or warranty, express or implied, is given by or on behalf of the

Company or the Banks or any of such persons’ directors, officers or employees or any other person as so to the accuracy, completeness or verification of the information or the opinions contained in this document and no

liability is accepted by the Company or the Banks or any of such persons members, directors, officers or employees nor any other person for any loss arising, directly or indirectly from any use of such information or

opinions or otherwise. No statement in this presentation is intended to be nor may be construed as a profit forecast. Persons receiving this document will make all trading and investment decisions in reliance on their own

judgement and not in reliance on any of the Banks and no statement in this presentation should be interpreted to mean that earnings per share for future financial years would necessarily match or exceed the Company’s

historic earnings per share. In addition, the ROIC, synergy and deleveraging statements relate to future actions and circumstances which, by their nature, involve risks, uncertainties and contingencies. As a result, the ROIC,

synergies and deleveraging referred to may not be achieved, or may be achieved later or sooner than estimated, or those achieved could be materially different from those estimated.. None of the Banks or the Company is

providing any such persons with advice on the suitability of the matters set out in this presentation or otherwise providing them with any investment advice or personal recommendations. Any presentations, research or

other information communicated or otherwise made available in this presentation is incidental to the provision of services by the Banks to the Company and is not based on individual circumstances.

The Banks are advising the Company and no one else in connection with the Transaction and will not be responsible to anyone other than the Company for providing the protections afforded to their clients. Prospective

purchasers of securities of the Company are required to make their own independent investigation and appraisal of the business and financial condition of the Company and the nature of the securities of the Company.

Attendees of this presentation should seek their own independent legal, investment and tax advice as they see fit. This document and its contents are confidential and may not be reproduced, redistributed or passed on

directly or indirectly, to any other person or published, in whole or in part, for any purpose. The materials are only addressed and directed at persons in member states of the European Economic Area who are "qualified

investors" within the meaning of Article 2(1)(e) of the Prospectus Directive (Directive 2003/71/EC) ("Qualified Investors"). Within the United Kingdom, this document is intended for distribution in the United Kingdom only

to persons who (i) are Qualified Investors and (ii) who have professional experience in matters relating to investments and/or to high net worth companies falling within Articles 19(5) or 49(2) respectively of the Financial

Services and Markets Act 2000 (Financial Promotion) Order 2005 (or persons to whom it may otherwise be lawfully communicated) and, if permitted by applicable law, is supplied outside the United Kingdom to

professionals or institutions whose ordinary business involves them engaging in investment activities. The information contained in this document is not intended to be viewed by, or distributed or passed on (directly or

indirectly) to, and should not be acted upon by any other class of persons.

Neither the rights issued in this Transaction (the “Rights”), the new ordinary shares issued upon taking up such Rights (the “New Ordinary Shares”), nor any provisional allotment letters in respect thereof (together with the

Rights and the New Ordinary Shares, the “Securities”) have been and will be registered under the United States Securities Act of 1933 (the “Securities Act”), as amended, or under the applicable securities laws of any state

of the United States or any proving or territory of Canada, Japan, the Republic of South Africa or Australia. Subject to certain exceptions, the Securities may not be offered, sold, taken up, renounced or delivered, directly or

indirectly, within the United States, Canada, Japan, the Republic of South Africa or Australia or in any country, territory or possession where to do so may contravene local securities laws or regulations. The Securities are

being offered and sold outside the United States only in offshore transactions within the meaning of and in accordance with Regulation S under the Securities Act. The offer and sale of the Securities may be made in the

United States only to "qualified institutional buyers" (as defined in Rule 144A under the Securities Act) in reliance on a private placement exemption from the registration requirements of the Securities Act and only in a

manner not requiring registration under the Securities Act. There will be no public offer of the Securities in the United States.

By attending the presentation to which this document relates or by accepting this document, you will be taken to have represented, warranted and undertaken to the Company and the Banks that: (i) you are a Qualified

Investor or, if a resident of or located in the United States, you are a Qualified Institutional Buyer, and (ii) you have read and agree to comply with, and be bound by, the contents of this notice. Private and Confidential For

personal use only and not for distribution.

LEGAL DISCLAIMER

2

AGENDA

Transaction Overview 1

Strategic Rationale 2

Financials, Financing and Timetable 4

US Market Overview 3

3

Transaction Overview

TRANSACTION HIGHLIGHTS

(1) USD/GBP foreign exchange rate of 0.775 used for transaction value, 0.777 used for all other conversions. (2) By number of issuers served, market position by shareholders served is 2nd. (3) Based on non-IFRS financial projections and may be subject to amendment by Equiniti in the prospectus when based on the Business’ projections under IFRS and / or IFRS-consistent accounting policies adopted by Equiniti. (4) This statement is not intended as a profit forecast and should not be interpreted to mean that earnings per share for Equiniti for the current or future financial years would necessarily match or exceed historical published earnings. (5) Adjusted profit to be acquired is after certain management normalisation and other adjustments to reflect the results of WFSS on a standalone basis, see page 18 for details. (6) On an underlying EPS basis. (7) The rights issue will be subject to shareholder approval of the acquisition and other customary conditions, including availability of the new debt facilities. Completion of the acquisition is conditional on shareholders approval.

Acquisition of WFSS for a consideration of $227m (£176m)(1) combining the #1 UK and #3(2) US share registrars

5

Highly compelling strategic and financial rationale 1

• Creates a stronger, more diversified, multi-national group combining local expertise with global reach

WFSS is a proven market leader with significant momentum, organic growth and market share capture 2

• Unique entry point into deep, highly active and concentrated US market

Excellent strategic fit and core competencies correlation with Equiniti 3

• Long-standing relationship and extensive exclusive due diligence process

Expected to be strongly earnings accretive in the first full year of ownership, and double digit earnings accretive by the end of year two(3)(4)(5)(6) 4

• Expected ROIC (post-tax) > WACC in the second full year of ownership(3)(4)(5)

Anticipated synergies of at least $10m (£8m)(1) by the third full year of ownership 5

• Largely driven by migration from WFSS legacy system to Equiniti’s market leading Sirius platform

Funded by existing and new debt facilities and a c.£122m proposed Rights Issue(7) 6

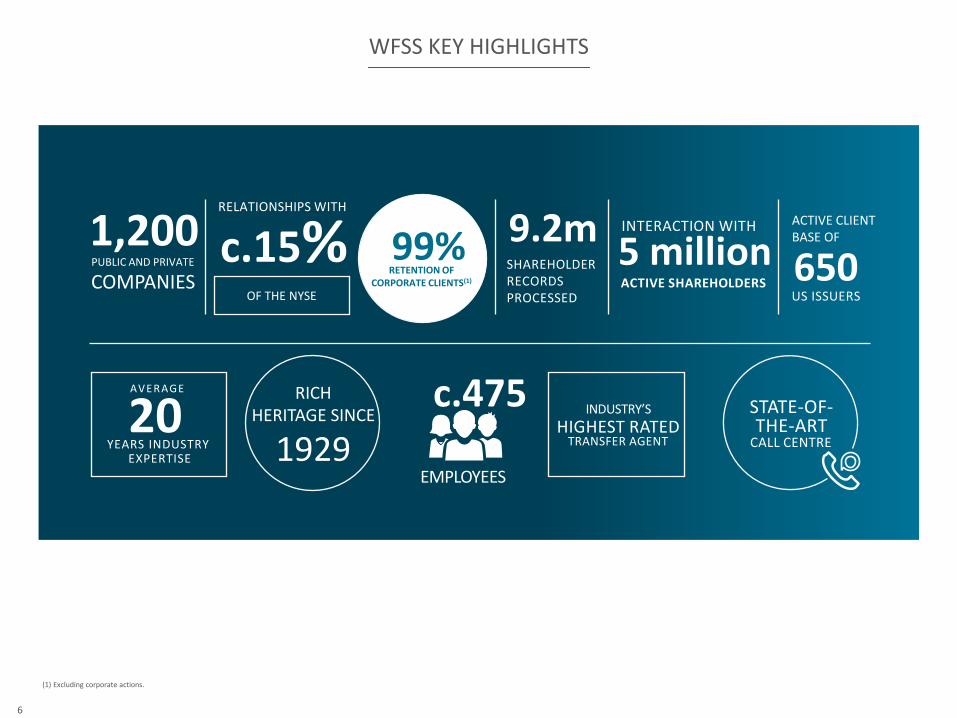

WFSS KEY HIGHLIGHTS

(1) Excluding corporate actions.

1,200 PUBLIC AND PRIVATE

COMPANIES

RELATIONSHIPS WITH

c.15% OF THE NYSE

9.2m SHAREHOLDER RECORDS PROCESSED

99% RETENTION OF

CORPORATE CLIENTS(1)

5 million INTERACTION WITH

RICH HERITAGE SINCE

1929 20 AVERAGE

YEARS INDUSTRY EXPERTISE

c.475

EMPLOYEES

INDUSTRY’S

HIGHEST RATED TRANSFER AGENT

STATE-OF- THE-ART

CALL CENTRE

ACTIVE SHAREHOLDERS 650

ACTIVE CLIENT BASE OF

US ISSUERS

6

Blue chip client base delivering

high profile corporate

actions business

/

A HIGH QUALITY ASSET WITH A STRONG US MARKET POSITION

Strong Equiniti “Value

Proposition” alignment

3 5

Share registry services business of WF since 1929 servicing c.650(1) corporate issuers and 5.0m active US shareholders

1

Leading #3(2) US market position,

with growing market share

(22%)(3)

2

2016A Revenue $104m (£81m) (5)(8)

2016A Adjusted

profits to be acquired $18m

(£14m)(7)(8)

6

(1) Excluding c.600 JP Morgan ADR clients. (2) By number of issuers served, market position by shareholders served is 2nd. (3) By number of shareholders served, market share by issuers served is 10%. (4) 2016 client win. (5) Includes fee income and interest margin. Revenues are as extracted from WFSS management accounts. (6) Client of WFSS pre transaction. (7) Based on non-IFRS financial data and may be subject to amendment by Equiniti in the prospectus when based on Equiniti’s IFRS and / or IFRS-consistent accounting policies. Adjusted profits to be acquired are as extracted from WFSS management accounts adjusted by Equiniti for own assessment of arms length standalone costs. (8) USD/GBP foreign exchange rate of 0.777 used.

Recent client wins driving

strong revenue growth (2014-16

CAGR c.6%)(5)

4

(4) (4)

(6)

(6)

(6)

(6)

/

/

/

7

(6)

18,464

4,8843,583 3,037 2,576 2,434 2,055

1,279 775 512 152

US IND HK CH UK JP AUS GER SG SA NZ

0%

60%

Other

COMBINING TWO LEADING BUSINESSES IN AN INCREASINGLY CONCENTRATED INDUSTRY

Access to the largest market globally

Combining two leading businesses(1)

Source: FactSet, advisor rankings, management. (1) By number of issuers served, UK data is based on FTSE 100 companies.

0%

60%

WFSS Other

8

STRONG PRODUCT ALIGNMENT AND CROSS SELL OPPORTUNITY

WFSS

Cross & Up-sell Opportunities

EQPAYMASTER EQINVEST

REGISTRATION SERVICES / CORPORATE ACTIONS

FINANCIAL CRIME PENSION SOLUTIONS INVESTMENT ADMINISTRATION

BUSINESS TO BUSINESS DIRECT TO CONSUMER

Boardroom RegTech B2B2C Direct to Investors

REGISTRATION SERVICES / CORPORATE ACTIONS

INVESTMENT PLAN SERVICES

EMPLOYEE SERVICES

BEREAVEMENT SERVICES

CUSTOMER COMPLAINTS

CREDIT SERVICING

DIGITISATION

DATA

CYBER & INFORMATION SECURITY

DATA SOLUTIONS

REWARDS & BENEFITS

PAYROLL

LIFE & PENSIONS

EXECUTIVE & EMPLOYEE SHARE DEALING

INTERNATIONAL PAYMENTS

9

STRONG RELATIONSHIP WITH WELLS FARGO AND DEEP CARVE-OUT EXPERIENCE

Strong reciprocal relationship with Wells Fargo

Integration plan and carve out experience

• TSA and commercial relationship

• Direct alignment of client characteristics

• Wells Fargo as supplier:

• Financial services

• Transaction banking

• Custodial services

• Stockbroking solutions

• Print & Mail services

• Equiniti as supplier:

• Transfer agent services

• Registrar services

• Equiniti as customer:

• Holding of cash deposits with Wells Fargo

• Proven blueprint from Lloyds carve out

• Todd May, Executive Vice President and Head of WFSS, is to be a direct report to Equiniti CEO

• Equiniti has an excellent track record of integration

• Equiniti has extensive carve out experience:

• Equiniti / Lloyds – 2007/8

• Nat West Stockbrokers CES / RBS – 2011

• My CSP / HMG – 2012

• Xafinity / Equiniti – 2012

• Killik Employee Services / Killik – 2013

• JPM Corporate Dealing Services / JPM – 2014

• Selftrade / Societe Generale – 2014

• The transition project will be overseen by senior Equiniti personnel who oversaw Equiniti’s carve-out from Lloyds TSB:

• Helps ensure a seamless integration process and rapid realisation of synergies

10

Strategic Rationale

STRATEGIC RATIONALE

Transforms Equiniti into a multi-national share registration business with immediate scale benefits 1

• Direct opportunities to target new “big-ticket” global and dual listed registry clients and provide multi-national solutions

• c.18,000 US listed corporates vs. c.2,500 in the UK

• High levels of US corporate finance activity

Core competency correlation between Equiniti & WFSS 3

• Focus on client / customer “value proposition” and culture of providing market leading service

• Similarities to Equiniti / Lloyds carve out in 2007/8

• WFSS is extremely well known to Equiniti through the Global Share Alliance (GSA)

WFSS has a strong track record of organic growth and market share capture 2

• c.650 clients including: J.P. Morgan, Wells Fargo, General Electric, and Berkshire Hathaway

• Client revenue growth of c.6%(1) over 2014A-2016A

• #3 position in share registration services in the US market(2)

• Strong client fidelity

(1) Fee income. CAGR. Revenues are as extracted from WFSS management accounts (2) By number of issuers served.

12

STRATEGIC RATIONALE (CONT’D)

Significant value from integration of Equiniti’s state-of-the-art Sirius platform to the US share registry market 4

• Equiniti intends to migrate WFSS onto Equiniti’s market leading Sirius platform (Equiniti registration database and workflow solution)

• Initial work on WFSS indicates high levels of cross functionality

• Migration to be key driver of operational excellence

Significant cross-selling (revenue synergies) opportunities 6

• Software capabilities including KYC, financial crime, fraud analytics, asset tracing, financial services remediation and complaints

• Additional distribution channel for transfer agent related services: proxy solicitation, investor relations, multi-national offerings and share plans

• Revenue synergies identified represent incremental upside and are not required to underpin transaction rationale

Significant cost synergy opportunity 5

• Initial cost synergy assessment indicates at least $10m (c.£8m)(1) synergies achievable by 2020

• Principal technology and operational synergies identified

• Integration outline agreed

(1) USD/GBP foreign exchange rate of 0.777 used.

13

US Market Overview

Industry Overview

US SHAREHOLDER SERVICES INDUSTRY OVERVIEW

#3 Market Share by Number of Issuers Served (2016)

Shareholder Services – Client Loyalty(1) Shareholder Services – Client Satisfaction(1)

62

52 52 50 52

WFSS Competitor A Competitor B Competitor C Competitor D

2016

Source: Audit Analytics, Bloomberg, Group 5, FactSet, equity research.

(1) Based on Group 5 survey results; represents net promoter score based on range from -100 to +100 based upon the percent of promoter and detractor scores.

95

93

91 90

89

WFSS Competitor A Competitor B Competitor C Competitor D

2016

• The US shareholder services industry is mature and highly concentrated, with the top 3 participants accounting for ~80% of total market share

• Consolidation continues to be a long-term trend

#2 Market Share by Number of Shareholders Served (2016)

62% 22%

8% 7% 1%

Computershare WFSSAST BroadridgeOther

48%

31%

10%

4% 7%

Computershare ASTWFSS BroadridgeOther

15

BLUE CHIP CLIENT BASE IS DEMONSTRATING MOMENTUM AND WILL CREATE OPPORTUNITIES FOR EQUINITI

Blue chip client base Demonstrating strong momentum Financial services clients

• JP Morgan ADR

• General Electric

• Procter & Gamble

• Southern Company Services

• Johnson Controls

• Exelon

• Adient

• PG & E Corp.

• The Southern Company

2016 Business wins

• Medtronic, Inc.

• Medtronic, plc

• Kraft Heinz

• Hewlett Packard

• Honeywell

• Kraft Foods

• NCR Corporation

• Occidental Petroleum

• Talen Energy

2015 Business wins

18

10

10

8

6

5

Regional Banks

InvestmentManagers &

Trusts

Insurance &Savings

InvestmentBanks & Major

Banks

FinancialConglomerates

FinancialServices

Example

• CMS Energy

• Concur Technologies

• Target Corporation

• Select Income REIT

• Praxair

• CDK Global

• ITT

• Ventas

• Michaels Companies

• Eastman Chemical

2014 Business wins

0.0

0.2

0.4

0.6

0.8

1.0

2014 2015 2016

Mill

ion

s

Shareowners Converted (m)

16

Financials, Financing and Timetable

• At least $10m (c.£8m) of run rate cost synergies by the third full year of ownership, with 50% achieved in the second full year of ownership

• Key areas of cost synergies:

• Migration from Wells Fargo legacy system to Equiniti’s market leading Sirius platform is expected to optimise data management and operational workflow

• Operational cost efficiencies through introducing Equiniti’s best in class practices to WFSS’ back office function

• In addition, significant cross-selling opportunities driven by Equiniti’s proprietary technology solutions, digital products and new share registrar related services to WFSS’ clients

• Expected cost to achieve of approximately $26m (c.£20m), with majority (c.60%) incurred during 2018 through a combination of carve out, dual running and programme related costs

• Expected capex requirement of approximately $28m (c.£22m), with majority (c.80%) incurred during 2018 to implement a standalone IT infrastructure and transition to the Sirius IT platform

• One off transaction costs of approximately £17m including advisory, debt and equity issuance costs

• WFSS possesses its own P&L which is maintained within the Wells Fargo accounting system

• Direct revenue and expenses reported alongside group recharges

• Summary financials therefore do not reflect WFSS’ results on a fully standalone basis

• Management have made a number of adjustments to estimate the results on a standalone basis. These adjustments include:

• Removal of Wells Fargo corporate overhead cost allocations and costs associated with shared IT platforms

• Deduction of internal revenue share

• Addition of estimated standalone entity costs

WFSS ADJUSTED SUMMARY FINANCIALS, SYNERGIES & PHASING

$m FY2016 2014-16A

CAGR

Revenue - Fee income - Interest income(3)

104.3 96.6 7.6

c.6%

Adjusted profits to be acquired

- Margin

18.4 17.7%

--

WFSS Adjusted Summary Financials(1)(2)

(1) Based on non-IFRS financial data and may be subject to amendment by Equiniti in the prospectus when based on Equiniti’s IFRS and / or IFRS-consistent accounting policies. (2) Revenues are as extracted from WFSS management accounts. Adjusted profits to be acquired are as extracted from WFSS management accounts adjusted by Equiniti for own assessment of arms length standalone costs. (3) c.$900m in client cash balances. (4) USD/GBP foreign exchange rate of 0.777 used.

Acquisition of WFSS expected to Deliver Significant Synergies(1)(4)

18

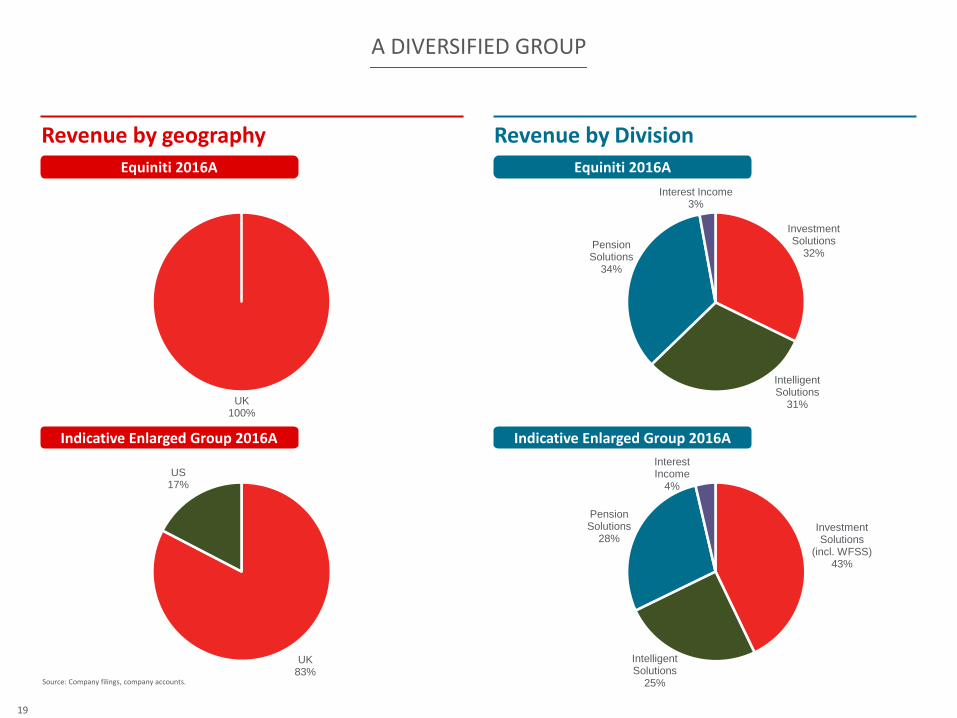

UK83%

US17%

A DIVERSIFIED GROUP

Revenue by geography Revenue by Division

Indicative Enlarged Group 2016A Indicative Enlarged Group 2016A

Investment Solutions

(incl. WFSS)43%

Intelligent Solutions

25%

PensionSolutions

28%

Interest Income

4%

Equiniti 2016A Equiniti 2016A

Investment Solutions

32%

Intelligent Solutions

31%

PensionSolutions

34%

Interest Income3%

UK100%

Source: Company filings, company accounts.

19

ACQUISITION FINANCING AND INDICATIVE TIMETABLE

• Cash element financed by a mixture of debt and equity

• c.$155m (c.£120m)(1) (underwritten) debt facilities

• c.$160m (c.£122m)(1)(2) Rights Issue (standby underwriting)

• The transaction is well funded, with the group adding $60m of working capital facilities to provide ample funding to support the integration of WFSS and future growth

• Pro-forma Enlarged Group leverage is expected to be broadly in line with the current group level (depending on the completion date)

• Clear deleveraging profile to Equiniti’s 2-2.5x medium term objective by the end of the second full year of ownership(3)(4)(5)

Acquisition Financing

• Transaction Announcement – July 2017

• Application for regulatory licenses – July 2017

• Equiniti interim results – 28 July 2017

• Prospectus / Circular published and posted to shareholders –September 2017

• Proposed EGM to approve the Acquisition – September 2017

• Expected launch of the Rights Issue – September 2017

• Expected completion of the Rights Issue – October 2017

• Regulatory approvals, carve out completion and anti-trust clearances – November 2017

• Expected completion of the Acquisition – Q4 2017 / Q1 2018

Indicative Timetable

(1) USD/GBP foreign exchange rate of 0.777 used. (2) The rights issue will be subject to shareholder approval of the acquisition and other customary conditions, including availability of the new debt facilities. Completion of the acquisition is conditional on shareholders approval. (3) Based on non-IFRS financial projections and may be subject to amendment by Equiniti in the prospectus when based on the Business’ projections under IFRS and / or IFRS-consistent accounting policies adopted by Equiniti. (4) This statement is not intended as a profit forecast and should not be interpreted to mean that earnings per share for Equiniti for the current or future financial years would necessarily match or exceed historical published earnings. (5) Adjusted profit to be acquired is stated after certain management normalisation and other adjustments to reflect the results of WFSS on a standalone basis, see page 18 for details.

20

SUMMARY

Transformational acquisition combining the #1 UK and #3(1) US share registrars to create a multi-national share registration and services business spanning the world’s deepest capital markets

Value enhancing transformational acquisition, consistent with Equiniti’s stated strategy, which is expected to create a stronger, more diversified multi-national group

Proven market leader with significant momentum, organic growth and market share capture

Significant cost and revenue synergies identified with clear pathway to capture

Extremely compelling commercial and financial rationale

Expected to be strongly earnings accretive in the first full year of ownership, with double digit EPS accretion in the second full year of ownership(2)(3)(4)

Excellent strategic fit and core competencies correlation with Equiniti

Expected to exceed WACC in second full year of ownership(2)(3)

(1) By number of issuers served. (2) Based on non-IFRS financial projections and may be subject to amendment by Equiniti in the prospectus when based on the Business’ projections under IFRS and / or IFRS-consistent accounting policies adopted by Equiniti. (3) Adjusted profit to be acquired is stated after certain management normalisation and other adjustments to reflect the results of WFSS on a standalone basis, see page 18 for details. (4) On an underlying EPS basis.

1 4

2 5

3 6

21

Questions & Answers

Appendix

Business Overview

• WFSS provides stock transfer agent, corporate actions, and investment plan services to 1,200+ public and private companies(1)

• 5 million active shareholder accounts

• Founded in 1929 and headquartered in Mendota Heights, Minnesota

• Additional personnel located in New York City, Arizona and India

WFSS OVERVIEW

Service Offerings Align Directly to Equiniti

Value to Shareholders

1. Accessible, helpful service online, by mail or over the phone

2. Easy and secure online tools to deliver account management

3. Resources and controls focusing on security and privacy

4. WFSS does not bill per call, creating incentive to care for shareowners’ needs on the first contact

WFSS’ Product Mix(2)

Plan Services • Direct Stock Purchase Plan • Dividend Reimbursement • Employee Plans • Dividend Reinvestment

Transfer Agent • Book-entry Recordkeeping • Certificate Issuance • Shareowner Inquiries • Abandoned Property

Corporate Actions • Exchange Agent • Tender Agent • Spin Offs • Paying Agent

Annual Meeting • Proxy tabulation • Inspector of election • Notice and access

(1) Number of clients served includes 600+ ADR clients from JP Morgan.

(2) Net of pass through revenues.

P Equiniti EQ Boardroom service provision.

P P

P P

Client

Share Registration Services

76%

Corporate Actions16%

Interest Income 8%

24

Overall Satisfaction

CONSISTENTLY SCORES BEST-IN-CLASS SATISFACTION RATINGS

Issuer Service

• WFSS has the highest client loyalty

• This year’s score is 10 points above the closest competitor

• Issuer loyalty is most influenced by satisfaction with service from account management

• Specifically Account Support’s ability to keep clients updated

Data Security Shareholder Service

Market Leader in Shareholder Services(1)

95

89 90

93

WFSS 1 2 3

Competitors

99

91 93

92

1 2 3

97

89

94

91

1 2 3

87

81

86

81

1 2 3

62

50 52 50

Competitors

WFSS is the Industry’s Highest Rated Transfer Agent

1 2 3

Competitors Competitors Competitors

(1) Based on Group 5 survey results; represents net promoter score based on range from -100 to +100 based upon the percent of promoter and detractor scores.

WFSS WFSS WFSS

WFSS

25

American International Group, Inc. Automatic Data Processing Inc. CBS Corporation Comcast Corporation Gannett Co. Inc. MSG Networks Inc. McCormick PPL The Travelers Companies, Inc. T Rowe Price United States Steel Corporation General Electric Company

WFSS SERVES MANY OF AMERICA’S MOST RESPECTED BLUE-CHIP CORPORATES

Midwest

3M Company Alliant Energy Corporation Bemis Company ConAgra Brands, Inc. Berkshire Hathaway

ConAgra Foods, Inc. DTE Energy Company Eli Lilly & Company Exelon Corporation General Mills, Inc.

Johnson Controls International plc Medtronic plc Mondelez International, Inc. Rockwell Collins, Inc. The Allstate Corporation

The Kroger Co. The Proctor and Gamble The Sherwin-Williams Company Walgreens Boots Alliance, Inc.

Northeast

Southeast

Darden Restaurants, Inc. Delta Air Lines, Inc. Dollar General Corporation Entergy Corporation HCA Holdings, Inc. NCR Corporation Ryder system, Inc. SCANA Corporation The Southern Company Tech Data Corporation

West

Apache Corporation Cabot Oil & Gas Corporation Comerica Incorporated Edison International Enterprise Products Partners L.P. Hewlett-Packard Company Hewlett Packard Enterprise Company Occidental Petroleum Corporation Janus Capital Group, Inc. PACCAR Inc. Pacific Gas and Electric Company Schnitzer Steel Industries Inc. Southwest Airlines Co. The Charles Schwab Corporation The Gap, Inc. Viad Corp. VISA, Inc. Wells Fargo & Company Williams-Sonoma, Inc.

26

Paying Agent US$28 billion

Berkshire Hathaway and

3G Capital Acquisition of

H.J. Heinz 2013

Paying Agent US$49.9 billion

Medtronic

Acquisition of Covidien

2015

Paying Agent US$55 billion

H.J. Heinz

Acquisition of Kraft Foods Group

2015

Paying Agent US$17.7 billion

Altice Acquisition of Cablevision Systems

Corporation 2016

Paying Agent US$5.2 billion

Level 3 Communications

Acquisition of TW Telecom

2014

Paying Agent US$12.7 billion

CVS Health Corp.

Acquisition of Omnicare Inc.

2015

Paying Agent US$4.9 billion

Duke Energy Acquisition

of Piedmont Natural Gas

2016

Paying Agent US$6.8 billion

Exelon Corporation

Acquisition of Pepco Holdings, Inc.

2016

Paying Agent US$8.3 billion

SAP

Acquisition of Concur Technologies

2014

Paying Agent US$12.8 billion

UnitedHealth Group

Acquisition of Catamaran Inc.

2015

Paying Agent US$12 billion

Southern Company Acquisition of AGL

Resources 2016

Exchange Agent US$16.5 billion

Johnson Controls Merger with Tyco

International 2016

WFSS’ EXPERIENCE AND CAPABILITIES ACROSS CORPORATE ACTION SOLUTIONS, IPOS, SPIN-OFFS & SPLIT-OFFS

Select M&A Transactions

Timken Co.

Spin-off of TimkenSteel Corp.

July 2014

Honeywell

Spin-off of AdvanSix Inc

Sept 2016

ADP

Spin-off of CDK Global Oct 2014

Procter and Gamble

Split-off of Coty

Sept 2016

Mondelez International

Spin-off of Kraft Foods Group, Inc.

Oct 2012

Tyco Int’l to Pentair, Ltd.

Spin-off of The ADT Corp.

Sept 2012

CBS Outdoor

US$560 million

April 2014

Virgin America, Inc.

US$306 million

Nov 2014

Univar Inc.

US$770 million

Jun 2015

Aimmune Therapeutics

US$160 million

Aug 2015

InfraREIT, Inc.

US$460 million

Jan 2015

ONEOK

Spin-off of ONE Gas Inc.

Jan 2014

Hewlett-Packard Spin-off of

Hewlett-Packard Enterprises Nov 2015

ConAgra Foods, Inc.

Spin-off of Lamb Weston

Nov 2016

Select Split-Off Transactions

Select IPO Transactions

27

CONTINUED OPPORTUNITY

Developing the Platform

Leveraging benefits

Achieving best practice

CONTINUED TO EXPAND SERVICE OFFERING

Acquired Xafinity (pensions business) expanding into pensions

Increased focus on adjacent technology plays

Began major government activity

REDEFINED CORE BUSINESS

Strategy redefined

Cemented ambition of becoming leading UK provider of tech- driven solutions for regulated, complex business processes

Redesigned organization and enhanced top management team

Significant new capabilities delivered

2007 2008 2009 2010 2011 2012 2013 2015 2014

THE FUTURE

Setup of Lloyds stock

registrar

Source: Management information.

SEPARATION AND CARVE-OUT FROM LLOYDS TSB

Significant investment in technology and infrastructure to establish standalone business focused on shareholder services

Established strategy to broaden BPO service offering leveraging customer base

Expanded through M&A into adjacencies strengthening core share registration and share plans business

EVOLUTION OF EQUINITI SINCE 2007

1957 2016

Equiniti IPO

2017

28

67

8692

0

20

40

60

80

100

2014A 2015A 2016A

291

369 383

0

100

200

300

400

500

2014A 2015A 2016A

29.6%

8.7%

FTSE Small Cap

SIGNIFICANT SHAREHOLDER RETURNS & GROWTH

Note: (1) Pre-exceptional items. Source: Factset.

£m £m

Equiniti enjoys strong shareholder support based on its good performance since IPO

Total shareholder return since Oct-15 IPO Total shareholder return in last six months

Sales performance (2014-16A) EBITDA performance(1) (2014-16A)

62.3%

27.6%

FTSE Small Cap

29

Ann. date

Relevant carve-out transactions

Business activities TSA New platform

build / implementation

Platform details

May-07 Lloyds Registrars and other businesses – carve-out from Lloyds Bank

Share registrar, employee share plans, share dealing and pensions administration

£60m build of ‘Sirius’ platform, and subsequent migration of clients completed within 18 months of transaction close. Sirius underpins the share registration and employee share plans business of Equiniti

Sep-11 NatWest Stockbrokers CES carve-out from RBS Group

Executive share dealing

New platform build delivered inside 12 month TSA timeframe and successful migration

Apr-12 MyCSP carve-out from Govt.

Pensions administration

Established new private sector enterprise, including implementation of new pensions administration platform

Nov-12 Xafinity Consulting carve-out from Equiniti

Pensions advisory

Equiniti shared services support functions supported the business under a TSA (this covered IT, Finance, HR, Payroll and Premises)

Oct-13 Killik Employee Services from Killik Group

Share plans administration

Acquisition of new executive share plans platform and carve-out from Killik Group

Jun-14 Selftrade from Societe Generale

Retail trading platform

Carve-out from Societe Generale subsidiary, Boursorama, and re-platform onto EQ new build solution

Jul-14 JP Morgan Corporate Dealing Services from JP Morgan

Executive share dealing

Carve-out from JP Morgan and transfer of book of business onto Equiniti platform

EQUINITI’S CARVE-OUT EXPERIENCE

We have extensive experience of this type of transaction with an understanding of the issues and need to take a measured approach to integration as well as the importance of a long-term relationship with the vendor

30

Thank You