Project Report Unit Link Plans

90

OBJECTIVES This study has been undertaken to know about the UNIT LINKS PLANS OF HDFC SLIC .The major objectives are: 1. T o know abo ut comp any hist ory and org aniza tion structure. 2. Provide an overview of unit linked plans of HDFC standard life insurance company ltd. 3. T o make a comparative performance of unit linked plans. 4. T o find the improvement area s in unit li nked pla ns. 1

-

Upload

shah-faisal -

Category

Documents

-

view

226 -

download

0

Transcript of Project Report Unit Link Plans

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 1/90

OBJECTIVES

This study has been undertaken to know about the UNIT

LINKS PLANS OF HDFC SLIC .The major objectives are:

1. To know about company history and organization

structure.

2. Provide an overview of unit linked plans of HDFC

standard life insurance company ltd.

3. To make a comparative performance of unit linked plans.

4. To find the improvement areas in unit linked plans.

1

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 2/90

METHODOLOGY

Information is collected through secondary data and some

discussions were also held with employees of HDFC SLIC to

know about the insurance plans.

In order to have a detailed insight into the insurance schemes

of HDFC SLIC. Literature on insurance plans and framework

certain leading schemes were for study to develop a

framework for study.

2

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 3/90

3

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 4/90

INTRODUCTION

Insurance is basically risk management device. The losses to assets

resulting from natural calamities like fire; flood, earthquake, accident etc.

are met out of the common pool contributed by large number of persons

who are exposed to similar risks. This contribution of many is used to pay

the looses suffered by unfortunate few. However the basic principle is that

loss should occur as a result of natural calamities or unexpected events,

which are beyond the human control. Secondly insured person should not

make any gains out of insurance.

It is natural to think of insurance of physical assets such as motor car

insurance or fire insurance but often be forget that creator all these assets is

the human being whose effort have gone along way in building up to assets.

In that scene human life is a unique income generating assets. Unlike physical assets, which decrease with the passage of time, the individual

become more experienced and mature as he advances in age. This raises his

earning capacity and the purpose of life insurance is to protect the income

to individual and provide financial security to his family, which is

dependent on his income in the event of his pre-mature death. The

individual also himself also needs financial security for the old age or on his

becoming permanently disabled when his income will stop. Insurance also

has an element of saving in certain cases.

Insurance is rupees 400 billion business in India and yet its spread in

the country is relatively thin. Insurance as a concept has not being able to

make headway in India. Presently LIC enjoys a monopoly in Life Insurance

business while GIC enjoys it in general insurance business. There has been

4

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 5/90

very little option before the customer to decide the insurer. A successful

passage of the IRA bill has clear the way of private sector operators in

collaboration with their overseas partners. It is likely to bring in a more

professional and focused approach. More over the foreign players would

bring sophisticated actuarial techniques with them, which would facilitate

the insurer to effectively price the product. It is very important that the

trained marketing professionals who are able to communicate specific

features of the policy should sell the policy. In the next millennium all

these activities would play a crucial role in the overall development and

maturity of the insurance industry.

DEFINITION GENERAL DEFINITION: -

In the words of John Magee, “Insurance is a plan by which

large numbers of people associate themselves and transfers to the shoulders

Of all risks that attach to individuals”

FUNDAMENTAL DEFINITION: -

In the words of D S Hansell, “Insurance may be defined as a

social device providing financial compensation for the effects of

misfortune, the payments being made from the accumulated contributions

of all participating in the scheme.”

5

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 6/90

CONTRACTUAL DEFINITION: -

In the words of justice Tindall “Insurance is a contract in

which a sum of money is paid to the assured as consideration of insurer’s

incurring the risk of paying a large sum upon a given contingency.

CHARACTERISTICS OF INSURANCE

• Sharing of risk

• Co-operative device

• Evaluation of risk

• Payment on happening of special event

• The amount of payment depends on the nature of losses incurred

NEED OF THE LIFE INSURANCE: -

The original, basic intention of life insurance is to provide for

one’s family and perhaps others in the event of death. Originally, polices were

to provide for short periods of time, covering temporary risk situations, such as

sea voyages. As life insurance became more established. It was realized what a

useful tool it was in a number of situations, including:

6

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 7/90

1. Temporary needs/ threats:

The original purpose of Life Insurance remains an important element,

namely providing for replacement of income on death etc.

2. Regular Saving:

Providing one’s family and oneself, as a medium to long term exercise

(through a series of regular payment of premiums). This has become more

relevant in recent times as people seek financial independence from their

family.

3. Investment:

Put simply, the building up of saving while safeguarding it from ravages

of inflation. Unlike regular saving products are traditionally lump sum

investments, where the individual makes are one time payment.

4. Retirement:

Provision for one’s on later years has become increasingly necessary,

especially in changing culture and social environment. One can buy a

suitable insurance policy, which will provide periodical payments in one’s

old age.

7

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 8/90

BENEFITS:

1. It is superior to traditional saving machine

As well as providing a secure vehicle to build up saving etc. it

provides piece of mind to the policy holder. In the event

ultimately death, of say the main earner in the family, the policy

will pay out guaranteed sum assured, which is likely to be

significantly more then the total premiums paid. With more

traditional saving vehicles, such as fixed deposits, the only return

would be the amount invested plus any interested accrued.

2. It encourages saving and forces thrift:

Once an insurance contract has been entered into, the insured has

an obligation to continue paying premiums, until the end of the

term of policy, otherwise the policy will lapse. In other words, it

becomes compulsory for the insure to save regularly and spend

wisely. In contrast savings held in a deposit account can be

accessed or stop easily.

3. It provides easy settlement and protection against creditors

Once a person appointed for receiving the benefits or a transfer of

rights is made (assignment), a claim under the life insurance

contract can be settled easily. In addition, creditors have no right

to any mommies by the insurer, where the policy is written under

trust. Under the married woman’s act the money available from

the policy forms a kind of trust which creditors can not claim on.

8

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 9/90

4. It can be encased and facilities borrowing:

Sum contracts may allow the policy can be surrendered for a cash

amount, if policy holder is not in a position to pay the premium.

A loan, against certain policy, can be taken for a temporary period

to tide over the difficulty. Presence of life insurance policy

facilitates credit for personal or commercial loans as it can be

offered as collateral security.

5. Tax relief :

The policy holder obtains income tax rebates by paying the insurance

premium. The specified form of saving which enjoys a tax rebate u/s

88 of the income tax act. Include Life Insurance premiums and

contribution to a recognized PF etc.

GOVT. ROLE:

============

Govt. keen to reduce the dependency on the state via private pension

provisions. They have a choice between using compulsion and incentives. Most

of the govt. chooses the later method. Tax relief is guaranteed in the pension

plants and is extremely generous, reflecting the value that the govt. and the

society and large place on the provision of retirement benefits. Tax treatments

of the benefit vary by country and by benefits.

In India, the proceeds of gratuity and provident fund are tax free in the

hand of the members. In UK, a certain amount of the proceeds can be taken as

tax lump sum and reminder as taxable income. Benefits due on withdrawal

9

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 10/90

from schemes are generally taxed unless they are transferred to another scheme

or approved pension plan.

ROLE OF LIFE INSURANCE

========================

Role 1: Life Insurance as “investment”

Insurance is an attractive option for investment. While most people

recognize the tax hedging and tax saving potential of life insurance, many are

not aware of its advantages as an investment option as well as. Insurance

products yield more compared to regular investment option as this is besides

the added incentives (read bonuses) offered by insurers.

You can not compare an insurance product with other investment

schemes for simple reason that it offers financial protection from risks,

something that is the missing in non- insurance products.

Infect, the premium you pay for a investment against risk. Thus, before

comparing with other scheme, you must accept that a part of total amount

invested in life insurance goes towards providing for the risk cover, while the

rest is used for savings.

In life insurance, unlike non-products, you get maturity benefits on

survival at the end of the term. In other words, if you take a life insurance

policy for 20 years and survive the term the amount investor as premium in the

policy will come back to you with added returns. In the unfortunate event of

10

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 11/90

death within the tenure of the policy, the family of the deceased will receive the

sum assured.

Now, let us compare insurance as an investment options. If you invest

Rs. 10000/- in PPF, year money grows to Rs. 10950 at 9.5% interest over a

year. But in this case, the access to your funds will be limited. One can

withdraw 50% of the initial deposit only after four years.

The sane amount of Rs. 10000/- can give you an insurance cover of up

to approximately Rs. 5 to 12 lacks. (Depending upon the plan, age and medical

condition of life insure etc.) And this amount can become immediately

available to the nominee of the policy holder on death. Thus insurance is a

unique investment avenue that delivers sound returns in addition to protection.

Role 2: Life Insurance as “Risk Cover”

First and foremost, insurance is about risk cover and protection –

financial protection, to be more precise-to help out last once unpredictable

losses. Designed to safe guard against losses suffered on account of an

unforeseen events. Insurance provide you with that uniqueness sense of

security that no other form of investment provides. By buying life insurance,

you buy peace of mind and are prepared to face any financial demand that

would hit the family incase of an untimely demise.

To provide such protection, insurance firms collect contributions for

many people who face the same risk. A loss claim is paid out of the total

premium collected by the insurance companies, who act as trustees to the

monies.

Insurance also provides a safeguard in the case of accident or a drop in

income after retirement. An accident or disability can be devastating and an

11

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 12/90

insurance policy can lend timely support to the family in such time. It also

comes as a great help when you retire, in case untoward incident happens

during the term in the policy.

With the entry of private sector player in insurance, you have a wide

range of products and services to choose from. Further, many of these can be

further customized to fit individual/group specific needs considering the

amount you have to pay now; it’s worth buying some extra sleep.

ROLE 3: Life Insurance as “Tax Planning”

Insurance serves as an excellent tax saving mechanism too. The Govt. of

India has offered tax incentives to life insurance products in order to facilitate

the flow of funds into productive assets. U/S 88 of Income Tax Act 1961, an

individual is entitled to rebate 20% on the annual premium payable on his/her

life and life of his/her children or adult children. The rebate is reducible from

tax payable by a individual or Hindu undivided family. This rebate is can be

availed up to a maximum of Rs 12000/- on payment of yearly premium of Rs

60000/- a year, you can buy anything upward of Rs 100000/- in sum assured.

This means that you get Rs 12000/- tax benefit. This rebate is deductible from

the tax payable by an individual or a Hindu undivided family.

12

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 13/90

THE EVALUATION OF INSURANCE INDUSTRY IN INDIA:

Life Insurance in its modern form is a western concept. The Indian

insurance industry is as old as it is in other part of the world. Although life

insurance business has been taking shape for the last 300 years, it came to India

with the arrival of Europeans. First Life Insurance Company was established in

1818 as Oriental Insurance Company, mainly to provide for widows of

Europeans. The companies that follow mainly catered to Europeans and

charged extra premium on Indian Lives. The first insurance company insuring

Indian Lives at standard rates was BOMBAY MUTUAL LIFE INSURANCE

COMPANY which was formed in 1870. This was also the year when 1st

Insurance act was passed by the British Parliament. The years subsequent to the

Swadeshi movement saw the emergence of several insurance companies. At the

end of the year 1955 there were 245 insurance companies. All the insurance

companies were nationalized in 1956 and brought under one umbrella- LIFE

INSURANCE CORPORATION OF INDIA (LIC) which enjoyed a monopoly

of the Life Insurance business until near the end of 2000. By enacting the

IRDA act 1999, the Govt of India effectively ended LIC’s monopoly and

opened the doors for private Insurance companies.

13

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 14/90

14

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 15/90

COMPANY PROFILE

INTRODUCTION

Founded in 1977, HDFC is today the market leader in housing finance in India

and has extended financial assistance to more than 15 lacks homes. HDFC

has more than 110 offices in India presently. It has also one international

office in Dubai and 3 more services associate in Kuwait, Qatar and sultanate

of OMAN. HDFC’s assets base amount to over 15,000 crore. Its financial

strength is reflected in highest safety rating of ‘FAAA’ and ‘MAAA’ awarded by

CRISIL and ICRA – two of India’s leading credit rating agency respectively, for

the last 6 year consecutively. It has a depositor base of over 11 lacks

customer and a deposit agents force of over 46,000 of the total deposit, 73%

are sourced from individual and trust depositors, which demonstrates the

tremendous confidence that retail investors have in the company.

HDFC- promoted companies have emerged to meet the

investors and customers needs. HDFC bank for commercial banking, HDFC

Mutual Fund for mutual fund products, to be followed very shortly by HDFC

Standard Life Insurance Company for the life insurance and pension products.

Being an institution that is strongly committed to the highest

standards of quality and excellence, HDFC has won several accolades in the

past few years. One such award is the “ Ramakrishnan Bajaj National Quality

Award “ for the year 1999. this award was instituted to award recognition to

Indian companies for business excellence and quality achievement. HDFC is

the only company so far to receive this award in the service category.

HDFC Standard Life Insurance Company Ltd. is one of India’s leading private

life insurance companies, which offers a range of individual and group

insurance solutions. It is a joint venture between Housing Development

15

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 16/90

Finance Corporation Limited (HDFC Ltd.), India’s leading housing finance

institution and one of the subsidiaries of Standard Life plc, leading providers

of financial services in the United Kingdom. Both the promoters are well

known for their ethical dealings and financial strength and are thus committed

to being a long-term player in the life insurance industry – all-important factors

to consider when choosing your insurer.

Our key strengths

Financial Expertise

As a joint venture of leading financial services groups, HDFC Standard Life

has the financial expertise required to manage your long-term investments

safely and efficiently.

Range of Solutions

We have a range of individual and group solutions, which can be easily

customized to specific needs. Our group solutions have been designed to

offer you complete flexibility combined with a low charging structure.

Track Record so far

our cumulative premium income, including the first year premiums and

renewal premiums is Rs. 1532.21 Cores Apr-Mar 2005 - 06.

We have covered over 1.6 million individuals out of which over 5,00,000 lives

have been covered through our group business tie-ups.

16

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 17/90

History

The Standard Life Assurance Company ("Standard Life") was established in

1825 and the first Standard Life Assurance Company Act was passed by

Parliament in 1832. Standard Life was reincorporated as a mutual assurance

company in 1925.

The Standard Life group originally operated only through branches or

agencies of the mutual company in the United Kingdom and certain other

countries. Its Canadian branch was founded in 1833 and its Irish operations in

1838. This largely remained the structure of the group until 1996, when it

opened a branch in Frankfurt, Germany with the aim of exporting its UK life

assurance and pensions operating model to capitalize on the opportunities

presented by EC Directive 92/96/EEC (the “Third Life Directive”) and offer a

product range in that market with features which local providers were unable

to offer. In the 1990s, the group also sought to diversify its operations into

areas, which complemented its core life assurance and pensions business,

with the intention of positioning itself as a broad range financial services

provider.

Banking, Healthcare & Investments -

The group set up Standard Life Bank, its UK mortgage and retail savings

banking subsidiary, in 1998 and Standard Life Investments, which had

previously been the in-house investment management unit of the group’s life

assurance and pensions business, was separated into a distinct legal entity in

the same year, with the aim of establishing it as an independent investment

management business providing services to both the group and third party

retail and institutional clients. The group acquired Prime Health Limited

(subsequently renamed Standard Life Healthcare) in the United Kingdom in

2000. Standard Life Healthcare expanded in March 2006 with the acquisition

17

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 18/90

of the PMI business of First Assist.

Standard Life Asia Limited/Joint ventures -

The group’s Hong Kong subsidiary, Standard Life Asia Limited (“SL Asia”),

was incorporated in 1999 as a joint venture and became a wholly-owned

subsidiary of Standard Life in 2002. The group’s operations in Hong Kong

were established to give the group a presence in the Far East from which it

could expand into China. The group’s joint ventures in India with Housing

Development Finance Corporation Limited (“HDFC”) were incorporated in

2000 (in relation to the life assurance and pensions joint venture) and 2003 (in

relation to the investment management joint venture). The group’s joint

venture in China with Tianjin Economic Development Area General Company

(“TEDA”) became operational in 2003.

Standard Life International Limited -

The group also incorporated Standard Life International Limited (“SLIL”) in

2005 for the purposes of providing the group with an offshore vehicle, based

in Ireland, through which it could sell tax-efficient investment products into the

United Kingdom. Sales of these products commenced in 2006.

Service company

Following the group’s strategic review in 2004, the group established a

service company structure for the provision of central corporate services to

the group’s business units. Standard Life Employee Services Limited

(“SLESL”) supplies a wide range of central services to the rest of the group,

including IT, facilities, legal and human resources services, and employs staff

working in the group’s UK and Irish operations (other than SLI, SLB and SLH,

which employ their staff directly). This service company structure was created

18

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 19/90

to enable Standard Life to comply with regulatory restrictions on the provision

of non-insurance services and to exploit group-wide synergies.

Demutualization of Standard Life

On 31 May 2006, Standard Life's voting members voted in favor of the

Special Resolution for the demutualization of The Standard Life Assurance

Company and the flotation of Standard Life plc on the London Stock

Exchange.

19

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 20/90

STANDARD LIFE ASSURANCE COMPANY (SLAC):

Founded in 1952, Standard Life has been at the for front of the

UK Insurance industry for 176 years by combining sound financial judgment

with integrity and reliability. The kingdom, Ireland, Spain, Germany and some

more with representative office in Hong-Kong and China.

One of the most recent successes was the launch of standard

Life Bank on 1

st

January 1998. In less than 20 months, the bank collected Rs.28,000 crore in deposit. The introduction of its innovative mortgage product in

Jan. 1999 had an immediate impact on the UK market, accounting for 11% of

all new lending within the first operational tear. The current loans outstanding

amount to Rs. 43,300 crore.

Standard Life has total assets of Rs. 55,000 crore and new

premium income last year 33,000 crore. Its UK investment portfolio account

for approximately 2% of all shares listed in the London Stock Exchange. Its

one of the new Insurance companies in the world to receive AAA rating from

two of the leading international credit rating agencies. Moody’s and Standard’s

And Poor’s. The latter described Standard Life’s ability to meet its claim

obligations as overwhelming under a variety of economic conditions.

Not surprisingly, Standard Life is rated as one of the few

strongest companies in the world, in financial terms. The quality and value

standard Life brings to this venture are immense. The company’s reputation in

UK market remains unrivalled. Besides being voted ‘Company of the ears for

overall service, for the third consecutive year. Standard Life was recently

voted ‘Company f the decade’ by independent brokers.

20

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 21/90

THE PARTNERSHIPS: -

HDFC and Standard discussions about possible

joint venture, to enter the life Insurance Life first commenced market, in Jan.

1995. it was clear from the outset that both companies shared similar values

and beliefs and a strong relationship quickly formed. In oct. 1995 the

companies signed a 3 year joint venture agreement.

Around this time standard Life purchased a 5% stake in HDFC ,

further strengthening the relationship.

A small project team was set up in UK and India and set about

preparatory work. Among other things, the team conducted market research,

looked at possible information technology, documented high level business

process maps and set about preparing the first project plan.

The next three years were filled uncertainty, due to change in

Govt. and both ongoing delays in getting the insurance bill passed in

parliament. Despite this both companies remained firmly committed to

venture.

In Oct. 1998, the joint venture agreement was renewed and additional

resources made available. Around this time Standard Life purchased 2% of

Infrastructure Development Finance Company Ltd. (IDFC) Standard Life also

started to use the services of the HDFC Treasury department to advise them

upon their investments in India.

One of many success stories over the last few tears has been

the actuarial student program. The program was designed to identify high

21

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 22/90

caliber individuals who would be sponsored by Standard Life to study for their

actuarial qualification in the UK.

The new company has 1 Indian actuary and 5 actuarial students

in the team, with a further 2 students undergoing training in the UK. Both

parents companies strongly believe the program will benefit the new company

in the years to come and are firmly committed to it. Towards the end of 1999,

the opening of the market looked very promising and both companies agreed

the time was right to move the operation to the next level. Therefore, in Jan.

2000 and expect team from the UK joined a hand picked team from HDFC to

form the core project team, based in Mumbai.

Around this time Standard Life purchased a further 5% stake in

HDFC and a 5% stake in HDFC bank.

In further development standard Life to participate in the Assets

Management Company promoted by HDFC to enter the mutual fund market.

The Mutual Fund market was launched on 20 th July 2000 and

one on the 10th Nov. 2000 assets under the management reached Rs. 1,063

crores.

The company was incorporated on 14th Aug 2000 under thename of HDFC Standard Life Insurance Company Limited.

The ambition of the company from as afr back as Oct. 1995 was

to be first private company to reenter the Life Insurance market in India. On

23rd of Oct. 2000 , this ambition was realized when HDFC standard Life

Insurance Company Limited were only Life company to be grated a certificate

of registration.

22

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 23/90

HDFC are main shareholders in HDFC standard Life Insurance

Company Limited with 81.4% while standard Life own 18.6 given Standard

Life’s existing investment in the HDFC Group, this is max. Investment allowed

under current regulations.

FACTS AND FIGURES

Standard Life

Standard Life provides an extensive range of products and services which is

aimed at meeting the financial requirements of our customers throughout their

lives. Our product range is known for its breadth and design, as well as for the

innovative features we have built into a number of those products.

Standard Life is a leading pension’s provider in the UK, and we were voted

the Best Pension Provider at the Money Marketing Awards in 2006.

Standard Life is recognized for the high quality of its customer service, in

particular for providing a service that is consistent, reliable and responsive.

We received recognition for this in 2005 when we were voted a 5 star provider

at the Financial Adviser Service Awards for the 10th year running.

Standard Life has been looking after its customers for over 180 years. More

on Standard Life's history.

Standard Life has operations in the United Kingdom, Canada, Germany, the

Republic of Ireland, Hong Kong, India and China.

The Standard Life group of companies also includes:

• Standard Life Investments, an investment manager with a reputation

for delivering strong investment performance, which had approximately

£124.8 billion of funds under management*1

23

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 24/90

• Standard Life Bank, offering a range of mortgages and savings

products, which managed approximately £10.6 billion of mortgages*2

• Standard Life Healthcare, which offers private medical insurance and

with the recent acquisition of First Assist is one of the largest such

insurers in the UK.

*1 as at 31/03/2006

*2 as at 31/12/2005. Statements contained in this website regarding past

trends, performance or activities should not be taken as a representation or

indication that such trends, performance or activities will continue in the

future.

Customer statistics

Customers Statistics

Worldwide customers Approximately 7 million

Customers in the UK Over 5 million

With profits members worldwide 2.4 million

Standard Life people

Full-time equivalent 15 November 200331 December 2003

31December

2005

Worldwide 13,295 11,324 10,405

In the United Kingdom(UK)

10,174 8,223 7,454

24

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 25/90

THE FOLLOWING COMPANIES HAS THE REST OF THE MARKET

SHARE OF THE INSURANCE INDUSTRY.

NAME OF THE PLAYER

(%)

MARKET SHARE

LIC 82.3

ICICI PRUDENTIAL 5.63

BIRLA SUN LIFE 2.56

BAJA ALLIANZ 2.03

SBI LIFE 1.80

HDFC STANDARD 1.36

TATA AIG 1.29

MAX NEW YORK 0.90

AVIVA 0.79

OM KOTAK MAHINDRA 0.51ING VYASA 0.37

AMP SANMAR 0.26

METLIFE 0.21

25

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 26/90

26

82.3

5.63

2.562.03 1.8

1.361.29

0.90.79

0.510.37

0.260.21

0

10

20

30

40

50

60

70

80

90

MARKET SHARE

LIC

ICICI PRUDENTIAL

BIRLA SUN LIFE

BAJA ALLIANZ

SBI LIFE

HDFC STANDARD

TATA AIG

MAX NEW YORK

AVIVA

OM KOTAK MAHINDRA

ING VYASA

AMP SANMAR

METLIFE

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 27/90

There are many types of Life Insurance but they generally fall into

two categories:

1. Term Insurance

2. Permanent Insurance

1. Term Insurance:

It provides protection for a specific period of time. It pays a benefit only

if one dies during the term. Some term insurance

policies can be renewed when you reach the end of the term, which can

be from one to 30 years. The premium rates increase at each renewal

date. Many policies require that you present evidence of insurability at

renewal to qualify for the lowest rates.The following points can help you determine if term insurance best suits

your needs.

Advantages Disadvantages

• Initial premiums generally are lower than

those for permanent insurance, allowing

you to buy higher levels of coverage at a

younger age when the need for protection

often is greatest.

• It’s good for covering needs that will

disappear in time, such as mortgages or

car loans.

• Premiums increase as you grow older.

• Coverage may terminate at the end of the

term or become too expensive to continue.

• The policy generally doesn’t offer cash value

or paid-up insurance.

27

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 28/90

HDFC and Standard Life first came together for a possible joint venture, to

enter the Life Insurance market, in January 1995. It was clear from the outset

that both companies shared similar values and beliefs and a strong

relationship quickly formed. In October 1995 the companies signed a 3 year

joint venture agreement.

Around this time Standard Life purchased a 5% stake in HDFC, further

strengthening the relationship.

The next three years were filled with uncertainty, due to changes in

government and ongoing delays in getting the IRDA (Insurance Regulatory

and Development authority) Act passed in parliament. Despite this both

companies remained firmly committed to the venture.

In October 1998, the joint venture agreement was renewed and additional

resource made available. Around this time Standard Life purchased 2% of

Infrastructure Development Finance Company Ltd. (IDFC). Standard Life also

started to use the services of the HDFC Treasury department to advise them

upon their investments in India.

Towards the end of 1999, the opening of the market looked very promising

and both companies agreed the time was right to move the operation to the

next level. Therefore, in January 2000 an expert team from the UK joined a

hand picked team from HDFC to form the core project team, based in

Mumbai.

Around this time Standard Life purchased a further 5% stake in HDFC and a

5% stake in HDFC Bank.

In a further development Standard Life agreed to participate in the Asset

Management Company promoted by HDFC to enter the mutual fund market.

The Mutual Fund was launched on 20th July 2000.

28

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 29/90

INCORPORATION OF HDFC STANDARD LIFE INSURANCE COMPANY LIMITED:

The company was incorporated on 14th August 2000 under the name of

HDFC Standard Life Insurance Company Limited.

Our ambition from as far back as October 1995 was to be the first private

company to re-enter the life insurance market in India. On the 23rd of October

2000, this ambition was realized when HDFC Standard Life was the only life

company to be granted a certificate of registration.

HDFC are the main shareholders in HDFC Standard Life, with 81.4%, while

Standard Life owns 18.6%. Given Standard Life's existing investment in the

HDFC Group, this is the maximum investment allowed under current

regulations.

HDFC and Standard Life have a long and close relationship built upon shared

values and trust. The ambition of HDFC Standard Life is to mirror the success

of the parent companies and be the yardstick by which all other insurance

company's in India are measured.

MISSION

We aim to be the top new life insurance company in the market.

This doe’s not just mean being the largest or the most productive company in

the market; rather it is a combination of several things like-

• Customer service of the highest order

• Value for money for customers

• Professionalism in carrying out business

• Innovative products to cater to different needs of different customers

• Use of technology to improve service standards

• Increasing market share

29

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 30/90

VALUES

• SECURITY: Providing long term financial security to our policy holders will

be our constant endeavor. We will be do this by offering life insurance and

pension products.

• TRUST: We appreciate the trust placed by our policy holders in us. Hence,

we will aim to manage their investments very carefully and live up to this

trust.

• INNOVATION: Recognizing the different needs of our customers, we will

be offering a range of innovative products to meet these needs.

Our mission is to be the best new life insurance company in India and these

are the values that will guide us in this.

30

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 31/90

A REVISION OF THE CONCEPT OF UNIT LINKED

Unit Linked Policies Are Unbundled

Unbundling means the factors which affect the final benefits payable

can be seen explicitly by the customer. This means that the customer

can see how the expenses, the cost of risk benefits and investment

growth are delivering their final benefit.

Unit-Linked Policies Make use of Unit Linked Funds

• The Unit-linked policies the customer’s money is managed in

what we call as the unit linked funds.

• The value of the policy is linked to the value of the net assets

(assets less liabilities) of the fund.

• Unlike some with profits policies the entire investment risk is

borne by the customer.

• At HDFC Standard Life, the client has a choice of funds in which

to invest.

• Our unit linked funds have different investment objectives and

give the customer the opportunity to be exposed to different types

of assets.

• As a result, the customer can choose his fund according to his

attitude to risk and desire of investment return.

31

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 32/90

Unit-Linked Policies Have Explicit Charges:• With all insurance products we allow for the expenses, the cost of

benefits incurred and a profit margin to the company.

• In HDFC standard life’s unit-linked policies the customer sees the

charges being deducted explicitly from their policy in respect to

these expenses.

• Some of these charges are charges deducted from the premium

and some are deducted from the fund.

The charges on a unit linked plan of HDFC Standard Life:

The charges under this policy are deducted to provide for the benefits

and the administration provided by HDFC standard life charges when

taken together, are among the lowest in the industry and are structured

to the give the better returns over the long term.

Investment Content Charge: This is a premium based charge. After

deducting this charge from the premiums, the remainder is invested to

buy units. The following table shows how much is used to buy units.

This percentage is called the investment content Rate.

INVESTMENTCONTENT RATE (ICR)

1st

& 2nd

years 3rd

year

Regular

Premiums

Up to 200000 73.00% 99.00%

From 200000 to

50000080.00% 99.00%

From 500000 to

100000085.00% 99.00%

Above 1000000 90.00% 99.00%

Additional single premiums 97.50% 99.00%

32

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 33/90

Other Charges Explanation

8Reduced ICR • A reduced percentage of the policy holder’s

premium is added to the fund.

• These charges are intended to cover the

marketing distribution (including

commission) and some other administrative

costs relating to the policy.

Fund Management

Charge (FMC)

• Deducted as a percentage of the customer’s

fund on a daily basis.

• These are intended to cover the ongoing

costs of managing the investments of the

policy.

• The daily unit price already includes a low

fund management charge of 0.80% per

annum of the fund’s value.• In the long term, the key to building great

maturity values is low FMC.

Administration

Charges

• A charge of Rs. 15 per month is charges to

cover regular administration costs.

• HDFC SL make the charge by canceling units

in each of the funds customer have chosen, in

the proportion customer have chosen.Policy Fee • A fixed monetary deduction done from the

customer’s fund on a monthly basis.

• This charge is taken to cover the ongoing

costs of administration of the policy and for

any renewal commissions.

Risk Charges • Deducted from the customer’s fund on a

monthly basis.

33

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 34/90

• To cover the cost of the lie cover, critical

illness or accidental death depending on the

options the customer has chosen.

• Every month HDFC SL customers make a

charge for providing customer with the death

or critical illness cover they have selected.

• The amount of the charge taken each month

depends on customer age.

Miscellaneous

However you may come across other charges, which are used by other

companies elsewhere in the market. Here are few examples:

Surrender Charges

• Are applied when a policy is surrendered.

• They are used to recover costs and lost profits.

• On cancellation or surrender of the policy before 3 years of

regular premiums have been paid.

• The company will make a charge of 25% of the outstanding

premiums due for the remainder of this 3 year period.

Switch or Redirection Charges

• These cover the additional administration costs associated with

switching investments between funds and redirecting premiums.

• Companies also sometimes use them to discourage excessively

frequent switches are premium redirections.

• Premium alterations include stopping and restarting the regular

premium after 3 years.

34

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 35/90

• The Co. HDFC SL does not charge for any of these options

currently.

• The HDFC SL reserves the right to introduce such charges after

approval from the IRDA.

Additional points to note:

• Expense charges and insurance benefit charges may or ma not

be guaranteed.

• Sometimes a maximum guaranteed charge is stated, but actual

charges are lower.

• The client is not allowed has negative number of units in any fund

of the plan.

EFFECT OF CHARGES

What Is The True Cost Of Charges?

This will depend on the level and type of charges that the company

levies. Firstly customer must be aware of these, as all charges will

affect the final value of the fund. However, they must also be aware of

the effect of these charges.

• It is not meaningful to look at one single charge in isolation. All

charges must be considered as a complete package. It is the

combined effect of all of the charges, which will affect the final

benefits payable.

The following example illustrates the relative effect of charges on an

HDFC Standard Life Unit Linked Endowment and a similar plan

available elsewhere in the market but with a different charging structure.

35

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 36/90

Take the case of a man aged 30 buying a unit linked endowment. The

charge assumptions are as follows:

HDFC STANDARD

LIFE

OTHER

Investment content

1st year

2nd year

3rd year

73%

73%

99%

85%

96%

96%

Fund Management

Charges

0.80%` 1.00% pa

Monthly Service Charges RS. 15 Rs. 60

HDFC Standard Life mortality has been used for both. The charges for

risk benefits are insignificant in comparison to the other charges.

Assuming IRDA projection rate of 10% pa, if this customer was to pay

Rs. 10,000 premium annually for 10 years, his fund will have frowned

but charges will have been deducted. A sum assured of Rs. 100000 has

been used.

At this term and for this size of premium, the effect of the lower initial

ICR on the HDFC Standard Life is greater, as we would expect.

However, the impact of the higher FMC and higher service charge

means that the HDFC Standard Life plan does in fact give a better

illustrative maturity value.

What happens if we increase the premium?

Take an annual premium of Rs. 100000 with a sum assured of Rs.

1000000.

36

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 37/90

What is immediately apparent is that the service charge is now relatively

insignificant for both companies. The monetary amount deducted for the

reduced ICR and the FMC will be much greater for bigger premium

policies but the service charge is fixed regardless of the premium and

therefore has little impact in this example. As a result, the illustrative

maturity value for this size of premium over a 10 year term is broadly

similar for both companies.

This is just a 10 year plan. HDFC Standard Life products have been

designed with the long term in mind – they are aimed at customers

looking to make long-term savings. We will now extend this same policy

to 30 years.

It is apparent that over the long term, the fund management charge has

the greatest impact on the customer’s fund. The reduced ICR is still

visible but the effect is not as rest as the FMC. Although there was only

a 0.2% difference in the FMC, this has been large enough to result in a

better illustrative maturity value under the HDFC Standard Life plan.

What does this example show us?

It shows that each type of charge affects the growth of the fund in

different ways. Mainly depending on the size of premiums and term. It

also means that we can not look at each charge individually – we have

to look at the complete package.

ALLOCATION OF UNITS

• The day on which units are allocated will be governed by unit

allocation rules.

37

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 38/90

• These rules will specify which day’s unit prices are used for

requested made on a specific day and time.

• For the first premium, allocation rules will apply to the day and

time on which the policy is issued.

• For subsequent premiums and premium top-ups, the allocation

rules will apply to the date and time at which we receive the

intimation and the cheque.

WHY BUY A UNIT LINKED PLAN

• A unit – linked plan offers the benefits of market – linked returns.

• It give flexibility in

o Premium paying g

o Withdrawals

o Protective elements.

• They enable to have ale are, transparent picture of their

investments.

• They allow adapting the level of investment risk according to the

changing risk profile.

38

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 39/90

DESIGN OF AN UNIT LINKED PLAN

The product specification would include (where relevant):

CLASS OF PRODUCT

• The technical class of product – e.g. whole, endowment, pension.

• Versions available – single life, joint life (first death, last survivor),

and business.

• Premium options – single, regular, flexible.

• Allowable insurance benefit add-ons.

39

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 40/90

INVESTMENTS

• Fund links available and investment objectives of each fund.

• Investment guarantees (or lack of investment guarantees)

• Methods and frequency of unit pricing

• The investment accounting and management system to be used.

MARKETING AND DISTRIBUTION

• The distribution channels through which the product is available.

• Variations of product design by distribution channels, if any.

• The initial and renewal commission payable rules

• Capabilities of illustration system to be used.

• Marketing material to be available.

• Training and qualification standards of anti linked insurance

intermediaries.

ADMINISTRATION

• Business processing rules – new and ongoing business.

• Policy and endorsement wordings.

• Cash processing rules – allocation of cast to policies, late

processing rules.

• Permitted policy changes (by the insurer and by the client)

• Availability of loans and / or partial withdrawals and the rules for

administering them

• Non-forfeiture provisions.

40

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 41/90

PRICING

This means the level and type of charges that the insurer can take

under the policy. The types of charge, which can be levied, are initial

charges, surrender charges, renewal charges, fund management

charges, and switch or redirection charges. In addition, charges are

taken for add-on benefits if the premium for such benefits is not

included in the total premium payable.

INITIAL CHARGES

Initial charges are intended to cover the marketing, distribution and

other new business costs relating to the policy. There are many different

variations of initial charges, but essentially, whatever method is used;

the effect is that less money is actually allocated to the policy than is

received from the client for a period of time. Some possible way of

doing this are:

• Allocate no money to the policy for a period of months.

• Allocate only a proportion of each premium to the policy for a

period of months.

• Allocate money received in the early months of a policy to units

that have a higher fund management charge than thesepurchases by later premiums.

In the event of the policy being surrendered, the future excess fund

management charges, in excess of the regular charges that would have

been levied on these units, are levied at the point of surrender. As such,

the excess fund management charges will be received regardless of

whether the policy runs its full term or not, and only the amount of

41

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 42/90

money required to purchase the units net of the excess fund

management charges needs to be allocated to the policy.

ADD-ON BENEFITS CHARGES

These are usually calculated using a current cost method (unless the

premium for add-on benefits is included in the total premium). This

means that risk premium rate are applied each month the sum at risk

under each benefit. Any charge over and above the pure risk premium

charge will help offset expenses.

CHOOSING A CHARGING STRUCTURE

The pattern of expenses incurred for a life insurance policy will always

be high acquisition costs followed by much lower but steadily increasing

renewal costs. There will also usually be a high initial commission

followed by a much lower renewal commission. Ideally, therefore, the

charging structure should match this incidence of expenses with a high

initial charge followed by a much lower level of renewal charges. For

marketing reasons, this may be unacceptable and the insurer may have

to either recoup initial expenses over a period of time by taking charges

that (Significantly) exceed there renewal expenses or disguise the high

initial charges. It was this latter approach that gave rise to the concept

of initial units (units that have a high fund management charge.

The alternative approach of taking higher renewal charges makes the

insurer vulnerable to early lapses, particularly if no surrender penalty is

applied. Taking charges more evenly can be accomplished in a variety

of ways, but the main ones are:

42

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 43/90

• A high bid/offer spread.

• An allocation rate of (significantly) less than 100%. This may be

increased after a period of years to 100% or more and can be

marketed as a loyalty bonus.

• An investment fee (often expressed as a percentage of the

premium)

This is effectively an additional bid/offer spread.

• A high fund management fee on all units. This could be reduced

after a period of years (for example by allocating bonus units) to

bring the fund management charge into line with the market

more.

These can be used either in isolation or in combination.

43

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 44/90

DESIGN OF THE UNIT LINKED PLANS OF HDFC STANDARD LIFE

HDFC Standard life has the following unit linked plans

1. Unit Linked Endowment Plat

2. Unit Linked Young Star Plan

3. Unit Linked Pension Plan

FEATURES OF THESE PLANS ARE GIVEN BELOW:

UNIT LINKED ENDOWMENT ASSURANCE

INTRODUCTION

The unit linked endowment plan is an insurance policy that is designed

to pay a lump sum on maturity or on earlier death. The Unit Linked

Endowment Plan also gives the option of additional protection against

the six common critical illnesses, as well as additional protection if

death is as the result of an accident.

Your premiums are invested in units of the investment fund of your

choice, based on the prevailing unit price. On maturity you receive the

value of your units. On death (or critical illness, if chosen) you receive

the greater of the value of your units and your selected basic sum

assured.

FLEXIBILITY IN PREMIUMS PAYMENT

The You agree to pay a level premium regularly, either quarterly, half-

yearly or annually, throughout the term of the policy. The minimum

premium amount is Rs. 10,000 each year.

To facilitate increased investment, we allow additional single premium

top-ups at any time. The minimum single premium top-up is Rs. 5,000

44

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 45/90

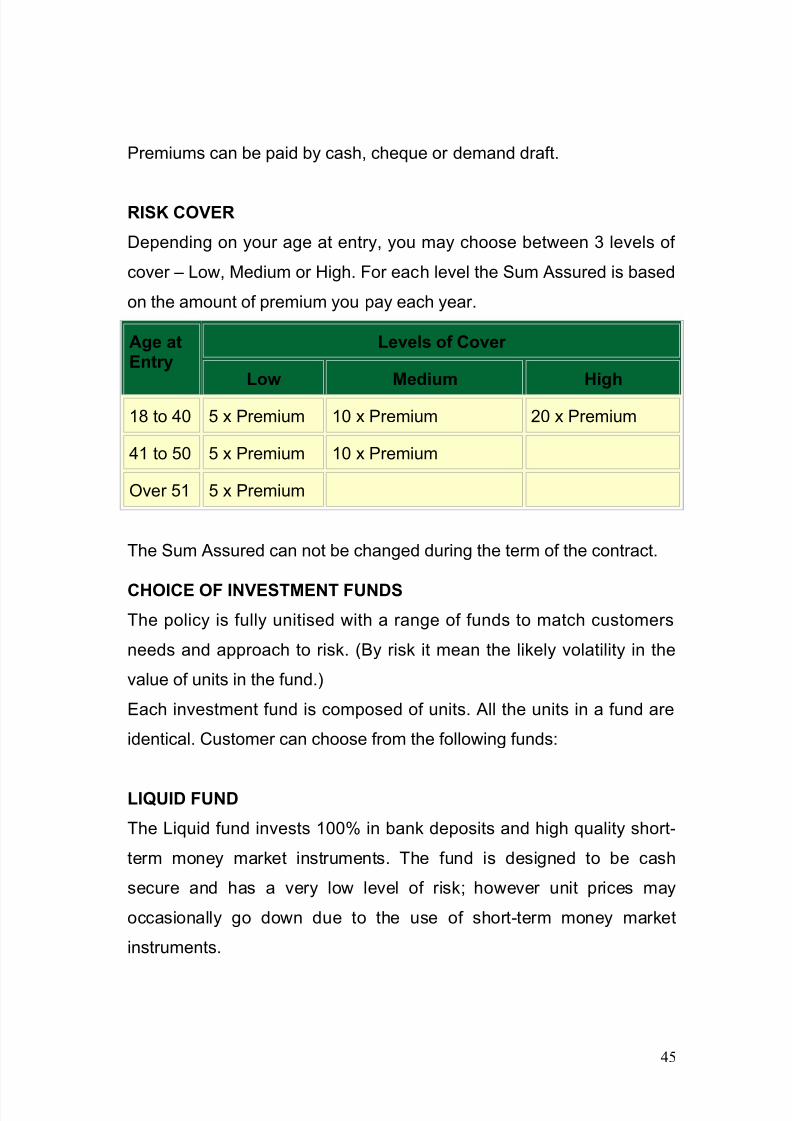

Premiums can be paid by cash, cheque or demand draft.

RISK COVER

Depending on your age at entry, you may choose between 3 levels of

cover – Low, Medium or High. For each level the Sum Assured is based

on the amount of premium you pay each year.

Age atEntry

Levels of Cover

Low Medium High

18 to 40 5 x Premium 10 x Premium 20 x Premium

41 to 50 5 x Premium 10 x Premium

Over 51 5 x Premium

The Sum Assured can not be changed during the term of the contract.

CHOICE OF INVESTMENT FUNDS

The policy is fully unitised with a range of funds to match customers

needs and approach to risk. (By risk it mean the likely volatility in the

value of units in the fund.)

Each investment fund is composed of units. All the units in a fund are

identical. Customer can choose from the following funds:

LIQUID FUND

The Liquid fund invests 100% in bank deposits and high quality short-

term money market instruments. The fund is designed to be cash

secure and has a very low level of risk; however unit prices may

occasionally go down due to the use of short-term money market

instruments.

45

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 46/90

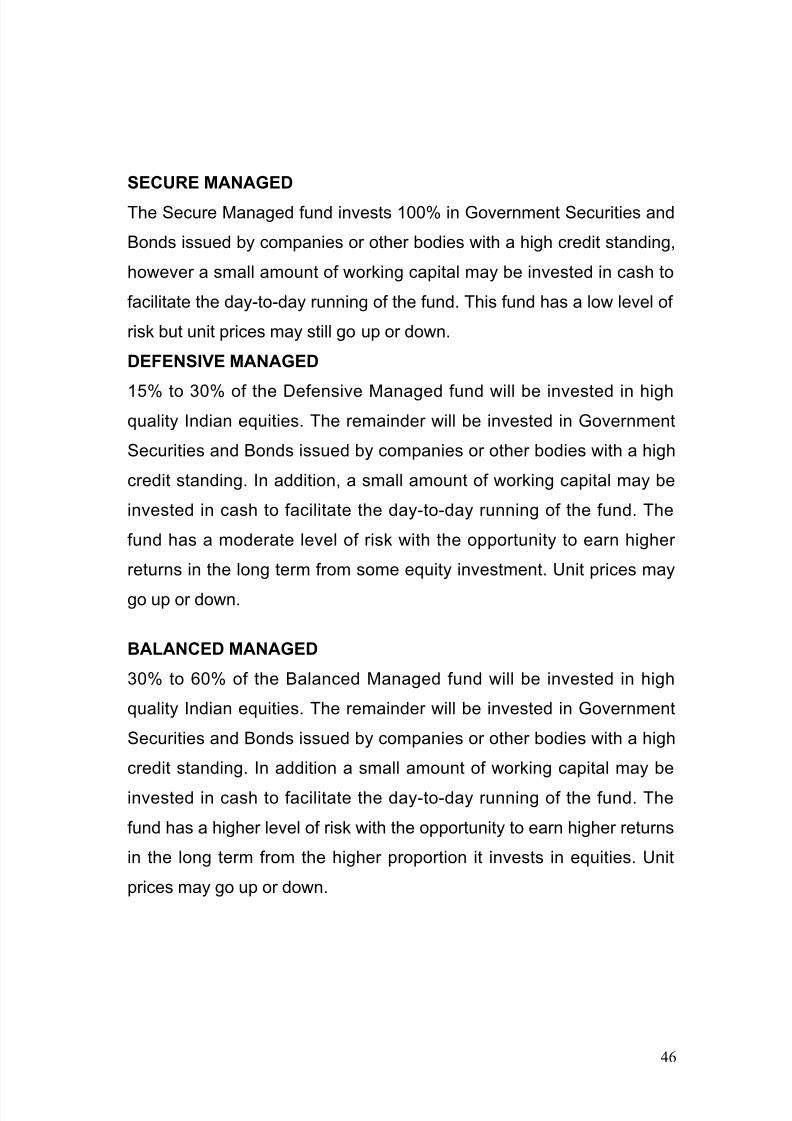

SECURE MANAGED

The Secure Managed fund invests 100% in Government Securities and

Bonds issued by companies or other bodies with a high credit standing,

however a small amount of working capital may be invested in cash to

facilitate the day-to-day running of the fund. This fund has a low level of

risk but unit prices may still go up or down.

DEFENSIVE MANAGED

15% to 30% of the Defensive Managed fund will be invested in high

quality Indian equities. The remainder will be invested in Government

Securities and Bonds issued by companies or other bodies with a high

credit standing. In addition, a small amount of working capital may be

invested in cash to facilitate the day-to-day running of the fund. The

fund has a moderate level of risk with the opportunity to earn higher

returns in the long term from some equity investment. Unit prices may

go up or down.

BALANCED MANAGED

30% to 60% of the Balanced Managed fund will be invested in high

quality Indian equities. The remainder will be invested in Government

Securities and Bonds issued by companies or other bodies with a high

credit standing. In addition a small amount of working capital may be

invested in cash to facilitate the day-to-day running of the fund. The

fund has a higher level of risk with the opportunity to earn higher returns

in the long term from the higher proportion it invests in equities. Unit

prices may go up or down.

46

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 47/90

EQUITY MANAGED FUND

0% to 40% of the equity managed fund will be invested in Govt.

securities & bonds. The remainder will be invested high class

Indian equities. Further increased exposure to equities to give a

greater long term return. A smaller bond holding will aid

diversification and provide a little stability.

GROWTH FUND

The Growth fund invests 100% in high quality Indian equities. In

addition a small amount of working capital may be invested in cash to

facilitate the day-to-day running of the fund. The fund has a higher level

of risk with the opportunity to earn higher returns in the long term from

the investment in equities. Unit prices may go up or down.

The past performance of any of the funds is not necessarily an

indication of future performance.

There are no investment guarantees on the returns of unit linked funds.

None of the funds participate in the profits of HDFC Standard Life

Insurance Company Limited or any of its policyholder funds.

Customer can switch your existing investments from any endowment

unit linked fund to another endowment unit linked fund. Person can also

give us a premium redirection instruction to redirect future premiums to

different endowment unit linked funds.

47

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 48/90

BENEFITS OFFERED

There are 4 different options available to choose from:

1. Life Option

On death within the policy term, the greater of the Sum Assured

and the value of the unit-linked fund will be paid to your nominee.

On survival to the end of the policy term the value of the unit

linked fund will be paid to you.

2. Life and Health Option

On death or earlier diagnosis of any one of six common critical

illnesses within the policy term, the greater of the Sum Assured

and the value of the unit-linked fund will be paid to your nominee.

On survival to the end of the policy term the value of the unit-

linked fund will be paid to you.

The illnesses covered under this option are cancer, coronary

artery by pass graft surgery, heart attack, kidney failure, major

organ transplant (as recipient) and stroke.

3. Extra Life Option

This option pays the same benefits as the Life Option but, should

death occur within the policy term as the result of an accident, an

extra benefit equal to the Sum Assured will be paid.

4. Extra Life and Health Option

This option pays the same benefits as the Life and Health Option

but, should death occur within the policy term as the result of an

accident, an extra benefit equal to the Sum Assured will be paid.

48

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 49/90

AGE AND TERM LIMITS

The age and term limits for taking out a Unit Linked Endowment Plan

are: (years)

MinimumTerm

MaximumTerm

MinimumAge atEntry

MaximumAge atEntry

MaximumAge atExpiry

Life 10 30 18 60 75

Life andHealth

10 30 18 55 65

Extra Life 10 30 18 55 70

Extra Lifeand Health

10 30 18 55 65

Can customer alter the level of my premiums?

Regular premiums can be increased at any time. If needed, the

policyholder can reduce the regular premium levels (even to zero ie the

policy is converted to pay up status) provided:

• 3 years of regular premiums have been paid

• The monetary value of the unit holding across all funds is at least Rs

15,000.

What happens if, policy surrendered?

The policyholder can surrender the policy at any point of time during the

contract term. The amount payable will be the unitised fund value after

applying additional surrender charges mentioned below.

49

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 50/90

When person can access his money?

You can make lump sum withdrawals from you funds provided the fund

balance after withdrawal and charges does not fall below the Sum

Assured. The minimum withdrawal amount is Rs. 10,000.

What happens if, customer stop paying premiums?

This product has a grace period of 15 days for the payment of each

premium after the initial premium.

If customer stops paying premiums, before you have paid 3 years of

annual premiums, we will cancel you policy and return to you the value

of your unitised fund, less cancellation charges.

If, after three years, you are unable to pay the premiums, you have the

option to make the policy paid-up, provided the policy has accumulated

sufficient policy value. Currently, this amount will be Rs. 15,000.

If you make your policy paid up you will continue to be protected

according to the benefits you selected. To provide this cover, we will

continue to collect our usual charges on each monthly charge date. It is

important to note that if no further premiums are paid, this may reduce

the value of your fund over time, or even exhaust it completely.

A paid-up policy can be reinstated to premium paying status at any pointof time in the future.

If the fund value of a paid-up policy falls below Rs. 15,000 we will

cancel the policy and return to you the fund value, less cancellation

charges.

50

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 51/90

CHARGES

We will deduct charges from the policy to cover our costs.

A percentage of each premium is invested to buy units, this percentage

is called the Investment Content Rate.

The rates are as follows:

Premium paid Investment Content Rate (ICR)

Regular - Year 1 73%

Regular - Year 2 73%

Regular - Year 3+ 99%

Regular Premium Increases 99%

Single Premium Top-Up 99%

The unit price each day will include a fund management charge. This

charge is 0.80% of the fund value per annum taken on a daily basis.

A flat fee of Rs 15 per month will be deducted by cancellation of units on

each monthly charge date. This will be proportioned across funds

according to the fund holdings at the time of cancellation of units.

Risk benefits (for death sum assured, critical illness, and accidental

death) will be charged for by cancelling units on each monthly charge

date, based on the person’s age at that time.

We charge neither for premium redirections nor for switches but we may

do so in the future.

We do not charge for altering the regular premium amount (including

making a policy paid-up and reinstating a paid-up policy), but we may

do so in the future.

51

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 52/90

On cancellation of the policy before 3 years of regular premiums have

been paid, we will charge 25% of the outstanding premiums due during

this 3-year period.

ALTERATION TO CHARGES

No changes can be made to our current charges without prior approval

from the Insurance Regulatory and Development Authority.

In any case, the fund management charge will not exceed 2% per

annum.

EXCLUSIONS

No benefit will be paid if the death has occurred directly or indirectly as

a result of suicide within one year from the date of first being covered

under the policy.

We will not pay health benefits if the critical illness has occurred within 6

months of the start of the contract.

We may not pay health benefits if we do not receive a duly completed

claim form within 26 weeks of the illness, disability, operation or other

circumstances giving rise to the claim.

We will not pay health benefits if the critical illness is caused directly or

indirectly by any of the following:

•

Intentionally self-inflicted injury or attempted suicide, irrespective of mental condition.

• Alcohol or solvent abuse, or the taking of drugs except under the

direction of a registered medical practitioner.

• War, invasion, hostilities (whether war is declared or not), civil war,

rebellion, revolution or taking part in a riot or civil commotion.

• Taking part in any flying activity, other than as a passenger in a

commercially licensed aircraft.

52

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 53/90

• Taking part in any act of a criminal nature.

• Pregnancy or childbirth or complications arising there from.

We will not pay accidental death benefit if death occurs after 90

days from the date of the accident.

We will not pay accidental death benefit if death is caused directly or

indirectly from any of the following:

• Suicide within one year of the Date of Commencement or the date of

issue of the Policy, if later

• Alcohol or solvent abuse, or the taking of drugs except under the

direction of a registered medical practitioner.

• Taking part or practicing for any hazardous hobby, pursuit or race

unless previously agreed to by us in writing

• War, invasion, hostilities (whether war is declared or not), civil war,

rebellion, revolution or taking part in a riot or civil commotion.

• Taking part in any flying activity, other than as a passenger in a

commercially licensed aircraft.

• Taking part in any act of a criminal nature.

GENERAL INFORMATION

UNIT PRICES

53

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 54/90

We will set the unit price of a fund by dividing the value of the assets in

the fund at the valuation time by the number of units in existence for the

fund. The resulting price will be rounded to the nearest Rs. 0.0001. The

value of the assets will be calculated as the Market or Fair Value of the

fund’s Investments plus Current Assets (including accrued income) less

Current Liabilities and Provisions (including accrued expenses).

PROHIBITION OF REBATES

Section 41 of the Insurance Act, 1938 states:

1. No person shall allow or offer to allow, either directly or indirectly, as

an inducement to any person to take out or renew or continue an

insurance in respect of any kind of risk relating to lives or property in

India, any rebate of the whole or part of the commission payable or

any rebate of the premium shown on the policy, nor shall any person

taking out or renewing or continuing a policy accept any rebate,

except such rebate as may be allowed in accordance with the

published prospectuses or tables of the insurer.

2. Any person making default in complying with the provisions of this

section shall be punishable with fine which may extend to five

hundred rupees.

TAX BENEFITSPremiums paid under this plan are eligible for tax benefits under Section

88 of the Income Tax Act, 1961.

54

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 55/90

UNIT LINKED YOUNG STAR PLAN

INTRODUCTION

HDFC Unit Linked Young Star Plan is designed to provide a lump sum

to the child at maturity. It also provides financial security to the child in

the future, even in case of the insured parent's unfortunate death during

the policy term. The Unit Linked Young Star Plan also gives the option

of additional protection against the six common critical illnesses.

Your premiums are invested in units of the investment funds of your

choice, based on the prevailing unit prices. On maturity the value of the

units will be paid. On death (or critical illness, if chosen) the selected

basic sum assured is paid, and the policy continues until maturity.

Following a valid death or critical illness claim, we will pay the future

premiums (at the level originally chosen at inception) into your policy, as

and when they would have fallen due.

PREMIUMS

You agree to pay a level premium regularly, either quarterly, half-yearly

or annually, throughout the term of the policy. The minimum premium

amount is Rs. 10,000 each year.

To facilitate increased investment, we allow additional single premium

top-ups at any time. The minimum single premium top-up is Rs. 5,000

Premiums can be paid by cash, cheque or demand draft.

55

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 56/90

FUNDS AND INVESTMENT

The policy is fully unitised with a range of funds to match your needs

and approach to risk. (By risk we mean the likely volatility in the value of

units in the fund.) Each investment fund is composed of units. All the

units in a fund are identical. You can choose from the following funds:

Liquid fund

The Liquid fund invests 100% in bank deposits and high quality short-

term money market instruments. The fund is designed to be cash

secure and has a very low level of risk; however unit prices may

occasionally go down due to the use of short-term money market

instruments. At inception, investments up to 20% can be allocated to

this fund.

Secure Managed

The Secure Managed fund invests 100% in Government Securities and

Bonds issued by companies or other bodies with a high credit standing,

however a small amount of working capital may be invested in cash to

facilitate the day-to-day running of the fund. This fund has a low level of

risk but unit prices may still go up or down.

Defensive Managed

15% to 30% of the Defensive Managed fund will be invested in high

quality Indian equities. The remainder will be invested in Government

Securities and Bonds issued by companies or other bodies with a high

credit standing. In addition, a small amount of working capital may be

invested in cash to facilitate the day-to-day running of the fund. The

56

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 57/90

fund has a moderate level of risk with the opportunity to earn higher

returns in the long term from some equity investment. Unit prices may

go up or down.

Balanced Managed

30% to 60% of the Balanced Managed fund will be invested in high

quality Indian equities. The remainder will be invested in Government

Securities and Bonds issued by companies or other bodies with a high

credit standing. In addition a small amount of working capital may be

invested in cash to facilitate the day-to-day running of the fund. The

fund has a higher level of risk with the opportunity to earn higher returns

in the long term from the higher proportion it invests in equities. Unit

prices may go up or down.

EQUITY MANAGED FUND

0% to 40% of the equity managed fund will be invested in Govt.

Securities & bonds. The remainder will be invested high class

Indian equities. Further increased exposure to equities to give a

Greater long term return. A smaller bond holding will aid

Diversification and provide a little stability.

Growth fund

The Growth fund invests 100% in high quality Indian equities. In

addition a small amount of working capital may be invested in cash to

facilitate the day-to-day running of the fund. The fund has a higher level

of risk with the opportunity to earn higher returns in the long term from

the investment in equities. Unit prices may go up or down.

57

8/14/2019 Project Report Unit Link Plans

http://slidepdf.com/reader/full/project-report-unit-link-plans 58/90

The past performance of any of the funds is not necessarily an

indication of future performance.

There are no investment guarantees on the returns of unit linked funds.

None of the funds participate in the profits of HDFC Standard Life

Insurance Company Limited or any of its policyholder funds.

RISK COVER

You can switch your existing investments from your any of your unit

linked funds, to any other available unit linked fund. You can also give

us a premium redirection instruction to redirect future premiums to

different unit linked funds.

Benefits

There are 2 different options available:

1. Life Option

This option consists of a Maturity Benefit and a Death Benefit.

• The Maturity Benefit will pay the value of the unit-linked fund at the

end of the policy term.

• The Death Benefit will pay the basic Sum Assured on death of the

life assured during the policy term. Following payment of this benefit,

no further premiums are due from the policyholder.

• Following a valid death claim, we will pay future premiums on your