Project Report Stocks Reconciliation Ashok Shalgar IIMP FINAL

95

A PROJECT REPORT ON “THIRD PARTY STOCKS RECONCILIATION OF THE SUB-CONTRACTED PARTS” UNDERTAKEN AT, GENERAL MOTORS (I) PVT. LTD, PUNE. UNDER THE GUIDANCE OF: MR.ANAND PRAKASH, INDIRA INSTITUTE OF MANAGEMENT, PUNE SUBMITED BY: ASHOK SHALGAR, OPERATIONS MANAGEMENT - 2011-13, INDIRA INSTITUTE OF MANAGEMENT, PUNE. PUNE UNIVERSITY SEAT NO. - 00547. IN THE PARTIAL FULFILLMENT OF, 1

description

Supply Chain Management SIP Report

Transcript of Project Report Stocks Reconciliation Ashok Shalgar IIMP FINAL

A

PROJECT REPORT

ON

“THIRD PARTY STOCKS RECONCILIATION

OF THE SUB-CONTRACTED PARTS”

UNDERTAKEN AT,

GENERAL MOTORS (I) PVT. LTD, PUNE.

UNDER THE GUIDANCE OF:

MR.ANAND PRAKASH,

INDIRA INSTITUTE OF MANAGEMENT, PUNE

SUBMITED BY:

ASHOK SHALGAR,

OPERATIONS MANAGEMENT - 2011-13,

INDIRA INSTITUTE OF MANAGEMENT, PUNE.

PUNE UNIVERSITY SEAT NO. - 00547.

IN THE PARTIAL FULFILLMENT OF,

MASTER OF BUSINESS ADMINISTRATION

(M.B.A.)

1

COMPANY CERTIFICATE

2

COLLEGE CERTIFICATE

TO WHOMSOEVER IT MAY CONCERN

This is to certify that Mr. Ashok Vijay Shalgar, a student of ‘Master of Business

Administration – Production & Materials Management’ from Indira Institute of

Management, Pune has done his/her Summer Internship Project at General

Motors India Pvt. Ltd., Pune from 1st Jun’12 to 1st Aug’12.

The project work entitled,

“Third Party stocks Reconciliation of The Sub-Contracted Parts”,

embodies the original work done by him/her during his/her Summer Internship

Project period.

Date:

Place: Pune

Mr. Anand Prakash,

Professor,

Indira Institute of Management, Pune.

3

ACKNOWLEDGEMENT

I would like to express my deep gratitude and sincere thanks to my project guide Mr. Anand

Prakash (Professor – IIMP) for his valuable guidance and unparallel support during the

progress of this project. Without his encouragement & crucial inputs, this project would not

have been possible.

I acknowledge with pleasure my debt to Mr. Avinash Bagul( HOD – Operations Dept.,

MBA- IIMP), who has provided me with important guidelines & supported in the project

work.

I express my heartiest thanks to Dr. Poornima Tapas (HOD – MBA, IIMP) for her guidance

& Support.

I would like to specially thank Mr. Dhiraj Agrawal (Manager, GSC, Power-Train Plant, GM

India) and Mr. Rajiv Gupta (Head, GPSC, Power-Train plant, GM India) for giving me this

opportunity to learn & work in the dynamic environment of the esteemed organization,

General Motors India.

On a more personal note, I would like to express my special thanks to my parents, all my

friends, who directly or indirectly, contributed to the successful completion of this project.

I sincerely thank everyone who was a part of this and helped me in completing this project

successfully.

Sign. :

Name: Ashok Vijay Shalgar

4

CONTENTS

I. LIST OF FIGURES

II. LIST OF TABLES

1.0 INTRODUCTION…………………………………………………………12

1.1 Motivation

1.2 Objectives

1.3 Scope

1.4 Chapterization

2.0 INDUSTRY PROFILE…………………………………………………….16

2.1 Industry Definition

2.2 Products and Services

2.3 History

2.4 Life Cycle

2.5 Major Players & Segmentation

2.6 Market Statistics & Potential

3.0 COMPANY PROFILE ………………………………………………...….20

3.1 General Motors

3.2 Vision & Strategy

3.3 General Motors in India

3.4 Joint Venture of GMIPL with SAIC

3.5 Products in the Indian Market

3.5.1 GM-Chevrolet Products in India

3.5.2 GM-Power-Train /Engine Products

4.0 LITERATURE REVIEW & NEED/PURPOSE OF THE PROJECT….…26

4.1 Definition: Reconciliation

4.1.1 Reconcile

4.1.2 Reconciliation

4.2 Concept of Reconciliation

5

4.3 Purpose of Reconciliation

4.3.1 Supply chain & Supply Chain Management

4.3.1.1 Supply Chain

4.3.1.2 Supply Chain Management

4.3.2 Sub-contracting

4.3.2.1 The Process of Sub-Contracting the Parts to

Suppliers

4.3.3 Flow of Materials during Sub-Contracting

4.3.4 Purpose of Reconciliation

4.4 Types of Reconciliation Methods & General Procedure of

Stocks Reconciliation

4.4.1 Types of Reconciliation Methods

4.4.2 Types of Inventory Systems:

4.4.3 General Procedure of Stocks Reconciliation

4.5 Global Manufacturing System

4.6 Overview of GPSC Department activities in GM India

4.6.1 Study Of Global Purchasing & Supply chain (GPSC) Process

4.6.2 Study of Roles & Responsibilities of Schedulers

5.0 RESEARCH METHODOLOGY…………...……………………………..41

5.1 Methodology for the Third Party Stocks/ Inventory Reconciliation

Process at General Motors India

5.2 Stocks/ Inventory Reconciliation Conducted in GMI Power- Train

Plant

5.2.1 In Detail Procedure of Reconciliation

5.3 Reconciliation Status of the Sub-Contracted Parts

5.3.1 Steps followed in the Reconciliation Process

5.3.2 Status of Reconciliation Part -1

5.3.3 Status of Reconciliation Part -2

6

6.0 RECONCILIATION DISCREPANCY ANALYSIS……………………...55

6.1 Reconciliation – Part 1 Discrepancy Analysis

6.1.1 Data for Reconciliation Discrepancy Analysis

& Reconciliation discrepancies Chart

6.2 Reconciliation Discrepancies Analysis

6.3 Savings & Treatment of the Discrepancies

7.0 SUGGESTIONS & FUTURE SCOPE…………………………………….59

8.0 OTHER ASSIGNMENTS…………………………………………………62

8.1 Short Lead Time (SLT) audit

8.1.1 Internal Audit for GMS –SLT implementation

8.1.2 Action Plan for GMS –SLT implementation

APPENDICES

REFERENCES

7

I. LIST OF FIGURES

Figure 2.1: Indian Auto Industry Market share distribution

Figure 2.2: Indian Auto Industry Market share, Passenger vehicles

Figure 3.1: New GM Business Model

Figure 4.1: Supply Chain activities

Figure 4.2: Principles of the Global Manufacturing System (GMS)

Figure 4.3: 33 Elements of The GMS Principles

Figure 4.4: In-Plant Material Flow Process – Global Purchasing & supply

Chain Dept., General Motors India

Figure 5.1: Methodology – The Third Party Stocks/Inventory Reconciliation

Process

Figure 5.2: Format of Reconciliation data received from Supplier.

Figure 5.3: Format showing the Child part cross verification for Reconciliation

purpose

Figure 5.4: Format showing the Parent part cross verification for

Reconciliation purpose

Figure 5.5: Format for Stocks Balance Sheet for Reconciliation

Figure 5.6: Status – Third Party Stocks Reconciliation-1

Figure 5.7: Status – Third Party Stocks Reconciliation-2

Figure 6.1: Discrepancies reasons Frequency Bar Chart

Figure 7.1: Reconciliation Format ‘in use’

Figure 7.2: Proposed Reconciliation format

8

II. LIST OF TABLES

Table 3.1: GM India Power-Train division products

Table 5.1: List of sub-contracted Parts Reconciliated

Table 6.1: Reconciliation Discrepancies Reasons

Table 6.2: Savings Summary – Third Party Stocks Reconciliation

9

EXECUTIVE SUMMARY

This project is titled as the ‘Third Party Stocks Reconciliation of the Sub-Contracted Parts’ It

covers the Reconciliation of all the sub-contracted parts in the GM-Power-Train division

manufacturing plant. It includes reconciling first the GM’s ERP maintained inventory records

with the supplier’s Book/System maintained Inventory records and then reconciling the

system record with the Actual Physical Inventory of the specific part/s at the Supplier’s end.

The Third Party here stands to be jointly the Finance Dept. of the company & external

Financial Auditing firm which will audit the Reconciliation from Financial point of view.

The project is aimed at Reconciling the Physical Inventory of all the sub-contracted parts at

supplier’s end with the GM ERP system inventory records for the last nine months period so

that there will be an updated inventory record available after resolving all the previous

discrepancies. The process of Reconciliation is studied, analyzed for improvements and

required improvements are suggested so that, in future, the process will be easier, less time

consuming and carried out more frequently to provide the transparent and updated inventory

records. The standardization & Continuous Improvement Principles of Global Manufacturing

system (GMS) are used to improve the Reconciliation process. Another Principle of GMS,

Short Lead Time (SLT) is also studied and Internal Audit for GMS-SLT is co-ordinated

during the Summer Project period.

The Methodology used is based on the standardized Procedure of Reconciliation in GM. First

the existing standard procedure of Reconciliation is studied & Reconciliation is carried out

for the last nine months’ transactions. For some parts, reconciliation is carried out since the

beginning of the transaction i.e. last two years period. The two inventory records i.e. GM-

ERP System record & Physical Inventory record at the supplier’s end, are cross checked &

discrepancies are found. The discrepancies are investigated & evidences are collected. Later

discrepancies are treated accordingly & ERP system adjustments or debit on supplier is done.

The Reconciliation is done in two phases, phase one being Reconciliation up to 31 st March

2012 & Second Phase is from 1st Apr’12 to 29th Jul’12 when Annual Physical Inventory is

carried out.

10

The major findings are in terms of frequency of Reconciliation andmethod of data

collection& treatment used. The Reconciliation was not carried out since the beginning of the

operations of the plant. Previously, only physical stock taking was done in September 2011

but the two system records i.e. GM ERP System & Suppliers Book/System records were not

cross checked. And the reconciled system record was not cross verified with the physical

inventory record at Supplier’s end. So, the discrepancies already existing at that time were

not resolved and carried forward. The format standardized for the Reconciliation Process has

many areas of improvement. One major area is the absence of feedback system. The record

maintained in the books/system for the sub-contracted parts’ transaction needs feedback in

terms of Goods Receipt Note at both the ends. And the system needs to be updated after

every reconciliation process which was not done previously.

A more frequent i.e. monthly Reconciliation is suggested and improvement is suggested in

the formats used for data collection from suppliers & formats for Reconciliation.A feedback

system is incorporated by including the GRN records to be maintained in the data collection

format.After these improvements are done,it will become a self-Reconciling activity apart

fromother benefits like reduction in time & efforts for the same. As an ideal state of

Inventory Management, Perpetual Inventory system is suggested.

The limited time period of two months for the project seems to be limiting factor in exploring

the more possible results from the project work. The complete & timely data availability for

the project work was constrained by the lack of access to the ERP system of the company for

being a project trainee. No cost was allocated separately for the project work which turned

out to be a cost saving project for the company.

The savings in terms of Debit on supplier range between 2% and 18 % of the Invoice value

ranging from Rs. 2,000 to Rs.10, 00,000.

The project has to be mutually benefiting to both the organization & the researcher. In this

project, it helped the organization in completing the long pending activity of Inventory

Reconciliation which is a mandatory norm to comply with the GMS system and bring

transparency in inventory records and financial records. It also helped the researcher in

learning the aspects of Materials Management, Supply Chain Management and

manufacturing processes & practices in the Automobile Industry.

11

1.0 INTRODUCTION

The project is a study as well as the actual working application of The Third Party

Stocks/Inventory Reconciliation Process carried out in the Supply Chain Management of a

World’s leading Automobile firm in the challenging environment of Automobile Industry.

The challenge lies in the fact that a large number of parts go into the manufacturing of an

automobile product i.e.an Automotive vehicle, along with tighter time constraints, for which

an efficient Inventory management is a tough task. Inventory Reconciliation is a part of a

larger function called Materials Management in an organization’s operations. It is an

inevitable part of Materials Management for maintaining up to date records of the Inventory

being utilized by the Organization. Materials are one of the most important resources being

used by a firm as it contributes almost sixty to seventy percent in the total cost of the product,

being manufactured, on an average. The importance of this activity is of great concern to all

the functions like Sales & Marketing, Operations and Finance of a firm. Periodic

Reconciliation of Stocks is a general practice whereas Perpetual Inventory being an ideal

condition in this regard. The Standard Procedure for Reconciliation Process is previously

developed in GMI which is followed as guideline and further additional formats & methods

are used for simplification of the process. Reconciliation is done in two parts, first half being

Reconciliation upto 31st March 2012 & second half is from 31st March 2012 to 29th July

2012.The Nett outcome of this process in terms of final adjustments in the inventory figures

in ERP system & Debit to the suppliers, as applicable,are subjected to thePlanned

Organizational Decisions which we hope will be affected soon after the Annual Physical

Inventory(API) conducted from 29thJuly 2012 to 4th August 2012 across GM India Plants.

1.1Motivation

The Project is completed in the World’s Leading Auto manufacturer General Motors’

manufacturing facility which has its existence in India since a long way back in 1928 with

currently two manufacturing facilities, one at Halol, Gujarat & second at Talegaon, Pune,

Maharashtra. The Power-Train Plant of GM India started its operations on 12th November

2010. Before this, GM had an operative Plant of General Assembly along with the Body

Shop & Paint Shop at its Pune facility since August 2008.

From the beginning of operations at Power-Train Plant, the Stocks Reconciliation was carried

out after ten months since it started the operations. Due to some technical reasons, the

12

previous Reconciliation conducted in September 2012 could not be affected in the ERP

system with due adjustments in the system to bring the System’s stocks & Physical stocks in

agreement. And it remained as just the stock taking process and not the complete Stocks

Reconciliation. So, to keep the inventory records transparent & updated up to date, the Stocks

Reconciliation for its Sub-Contracted parts was vital.This task has been tried to be

accomplished under this project.

1.2 Objectives

a. To study the Third Party Stocks Reconciliation at GM India & overall study of the

Process of Purchasing & Supply Chain Management at GM India

b. To carry out Third Party stocks Reconciliation for the selected parts for specified time

period to bring into agreement the GM ERP system Inventory records & Physical

Inventory at the Supplier’s end.

c. To suggest improvements in the process of Third Party Stocks Reconciliation as a part

of Continuous Improvement (Kaizen)

d. To study Global Manufacturing System - Lean Manufacturing system at GM

i. Study of elements of GMS –Short Lead Time , Audit point of View

ii. Coordinating the SLT Audit for Power-Train plant

1.3 Scope

The project is mainly focused on delivering the successful completion of stocks

Reconciliation of all the sub-contracted parts. The concerned dept. is the Global Supply

Chain, a sub group of the Global Purchasing & Supply Chain Dept. under the Power-Train

division of GM India operations.

Here we will refine the ERP system data available with the company. The data with the

company and the suppliers needs to be cross checked for accuracy. Some corrections are

required in both the data available with both the sources. Finally this corrected data will be

cross checked with the actual Physical Inventory available with supplier/ GM India. The

discrepancies need to be treated.

The discrepancies are either in the form of adjustments in the ERP system records or the

amount of inventory in discrepancy shall be debited to suppliers account. After the

completion of this task, the two inventory records will be in agreement i.e. reconciled.

13

The suggestions will be done on the basis of shortcomings observed in the existing process of

reconciliation. Those will be useful to meet the shortcomings and make the inventory

management & reconciliation process stronger and easier.

The discrepancies may or may not be investigated thoroughly due to the fact that the data is

not investigated for the last nineteen months since the operations of the plant are initiated.

The various adjustments, reversals, cancellations are done at various times in the inventory

records. This will reduce the accuracy of the data being used. Hence we need to rely on the

data available & the investigation possible at this point of time.

The area of work will be limited for the Power-train plant only and to the sub-contracted parts

under consideration. The engine assembly consists of hundreds of parts. We have selected

only the eight sub-contracted parts for reconciliation. The time period is well defined which

is of nine months from the last stock taking up to the Annual Physical Inventory carried out

in the month of July 2012. The cost/Price of the parts is not a limiting factor for the work. As

all the suppliers are located within the boundaries of India, the work will be carried out in

India only.

1.4 Chapterization

The report is made up of total eight chapters.

The first chapter is of Introduction which covers the basic introduction to the task of

reconciliation of inventory, the background of the work, the organizational history related to

the work and purpose, importance in brief. Objectives and scope of work is also explained in

this chapter.

The second chapter is the Industry Profile which deals with the background and current status

of the Indian Automobile Industry in which the organization works. The major players, their

contribution and economical aspects & importance of this industry are explained.

The Third chapter is of Company profile where we can find the details about the

organization, General Motors India. It’s existence and tenure in the country. Current product

offerings and economical statistics of the company are also explained.

The forth chapter is of the Literature Review of the Reconciliation process where the Supply

chain process, Sub-contracting activity & the need /purpose of the project are elaborated. The

general practices adopted in this area are explained to get an overview of what are the

14

practices followed & how is the project work will be guided with respect to the existing work

in this area.

The fifth chapter is the Research Methodology which covers the procedure followed for

reconciliation work. The various steps actually carried out and formats, methods of work are

shown in this chapter.

The sixth chapter is of the analysis of discrepancies found during reconciliation and their

treatment. The monetary savings which are of great importance can be sited here.

The seventh chapter consists of the Suggestions made based on the work carried out during

the project. The future scope of the project is about improvements to be done in existing

processes and practices followed. This will surely enhance the efficiency & effectiveness of

the process of reconciliation.

The eighth chapter explains the other assignments completed during the project period. The

assignments were additional knowledgeable activities under the umbrella of Supply Chain

Management which were helpful in learning the concept & practical aspects of the Supply

Chain management.

15

2.0 INDUSTRY PROFILE

The Indian Automotive sector has a significant place in the country’s economy which

provides about 5 % contribution to the nation’s GDP of $1.78 Trillion and 13 million

employments. It has come a long way since its inception.

(Source: Department of Heavy Industry & Public Enterprises Government of India -

http://www.imaginmor.com)

2.1 Industry Definition

This class consists of units mainly engaged in manufacturing motor vehicles or motor vehicle

engines.

2.2 Products and Services

The primary activities of this industry are:

1. Motor cars manufacturing

2. Motor vehicle engine manufacturing

The major products and services in this industry are:

1. Passenger motor vehicle manufacturing segment (Passenger Cars, Utility Vehicles &

Multi Purpose Vehicles)

2. Commercial Vehicles (Medium & Heavy and Light Commercial Vehicles)

3. Two Wheelers

4. Three Wheelers

2.3 History

The first car ran on India's roads in 1897. Until the 1930s, cars were imported directly, but in

very small numbers. The automotive industry emerged in India in the 1940s. Mahindra &

Mahindra was established by two brothers as a trading company in 1945, and began assembly

of Jeep CJ-3A utility vehicles under license from Willys. The company soon branched out

into the manufacture of light commercial vehicles (LCVs) and agricultural tractors.

Following the independence, in 1947, the Government of India and the private

sector launched efforts to create an automotive component manufacturing industry to supply

to the automobile industry. However, the growth was relatively slow in the 1950s and 1960s

16

due to nationalisation and the license raj which hampered the Indian private sector. Tata’s

were in Heavy Commercial Vehicles Mfg. whereas Ashok Leyland was another major player

in this segment. Govt. of India formed the joint venture Maruti-Suzuki with Japanese vehicles

manufacturer Suzuki for commercial passenger cars. Following economic liberalization in

India in 1991, the Indian automotive industry has demonstrated sustained growth as a result

of increased competitiveness and relaxed restrictions. Several Indian automobile

manufacturers such as Tata Motors, Maruti Suzuki and Mahindra and Mahindra, expanded

their domestic and international operations. India's robust economic growth led to the further

expansion of its domestic automobile market which has attracted significant India-specific

investment by multinational automobile manufacturers.After a 100 % FDI allowed in the

sector, Today there are almost all the major International Auto manufacturing Players like

Toyota, Volkswagen, General Motors, Ford, Honda, Hyundai, Daimler, BMW present in

India with their Manufacturing plants which supply to the Domestic demand as well as

Export the vehicles to the World Market.

(Source: "Timeline: India's automotive industry". BBC News. 3 April 2007. Archived from

the original on 2 January 2009. )

2.4 Life Cycle

The life cycle stage of the Indian Auto Industry is ‘growth’.

The Life Cycle stage is so called because of following reasons:

1. The market for manufacturing motor vehicles is consistently increasing.

2. The products manufactured by this industry are profitable.

3. Companies have been consistently opening new plants and employing over the past

five years.

4. Japanese and European manufacturers of motor vehicles have entered the market.

5. Industry value added has been rising, along with the rise in GDP.

2.5 Major Players & Segmentation

The Indian automobile Industry has following major segments:

1. Passenger Vehicles ( 15.07 % Market Share)

2. Commercial Vehicles (4.66%)

3. Three Wheelers (2.95%)

4. Two Wheelers (77.32 %) (Source : SIAM data – www.siamindia.com)

17

Figure 2.1 : Indian Auto Industry Market share distribution

The Major Players in the Indian Automobile sector are

1. Tata Motors

Market Share: Commercial Vehicles 63.94%, Passenger Vehicles 13.10 %

2. Maruti Suzuki India

Market Share: Passenger Vehicles 36.60 %

3. Hyundai Motors India

Market Share: Passenger Vehicles 14.61%

4. Mahindra & Mahindra

Market Share: Commercial Vehicles 10.01%, Passenger Vehicles 11.26%,

Three Wheelers 1.31%

5. Ashok Leyland

Market Share: Commercial Vehicles 22%

Others being Toyota, General Motors, Volkswagen, Ford, BMW, HM, Hero Honda,

Bajaj,TVS etc. (Source: Economic Times –14th Sept’12 publication)

Figure 2.2: Indian Auto Industry Market share, Passenger vehicles

18

The figure 2.2 shows the market shares of the various Auto manufacturers in the passenger

vehicles segment for the two consecutive years and respective variations. Maruti Suzuki, in

spite of being the market leader, has lost a big amount of market share and other players are

gaining the same at the same time. The competition has become tougher and some other

reasons like shut down at the Maruti Suzuki’s Manesar plant has given other companies to

excel in the share.

2.6 Market Statistics& Potential

Indian Auto Industry is

The Largest three wheeler market in the world

2nd largest two wheeler market in the world

10th largest passenger car market in the world

4th largest tractor market in the world

5th largest commercial vehicle market in the world

5th largest bus & truck market in the world. (source: www.oica.net )

The turnover of Indian Auto Industry is about $ 36 Billion.

It manufactures over 11 million vehicles and exports about 1.5 million each year.

The growth rate of the industry has been on an average of 17% for last few years.

The industry provides direct and indirect employment to 13.1 million people.

About 91% of the vehicles sold are used by households and only about 9% for commercial

purposes.

India's share is about 3.28% of the world Passenger & commercial vehicle production with

2.6 million units a year in 2011.

The Global Production is 77 million passenger and commercial vehicles.

India's automotive exports constitute only about 0.3% of global automotive trade.

The contribution in the nation’s GDP is expected to grow around 10 % by 2016. Indian

passenger car market will have a growth rate of about 12 percent per annum over the next

few years to reach the production of 5.1 million units by the year 2015 and turnover of $122-

$159 in the year 2016 and 25 million additional employments. Experts state that in the year

2050, India will top the car volumes of all the nations of the world with about 611 million

cars running on its roads.

(Source: Dept of Heavy Industry & Public Enterprises Govt. of India- www.imaginmor.com)

19

3.0 COMPANY PROFILE

3.1 General Motors:

General Motors was found in 1908 in Flint, Michigan, U.S.A. by William C. Durant. The

company has its global headquarters in Detroit and employs approximately 2, 02,000 people

all over the world. It does business in 120 countries and, together with its strategic partners,

produces cars and trucks in 31 countries. GM’s highest sales are reported from China,

followed by the United States, Brazil, the United Kingdom, Germany, Canada, and Russia.

The company includes a total of 13 brands - Baojun, Buick, Cadillac, Chevrolet, FAW,

GMC, Daewoo (car division), Holden, Isuzu, Jiefang, Opel, Vauxhall, and Wuling – under its

umbrella.

Over the past few years, GM has suffered several setbacks, including the declaration of

bankruptcy in June 2009 and an eventual split. A “New GM” emerged in 2009 with the

support of the US government. The new company was listed on the New York Stock

Exchange in November 2010. As part of the reorganization, the company phased out two of

its brands - Pontiac and Goodwrench - and adopted a new brand identity. It also received

loans from European governments in 2009, and reduced its stake in European operations.

Operations in other parts of the world were not affected by the bankruptcy and continued as

before. (Source: "History of General Motors, Company profile". – www.gm.com)

The company has generated total revenue of $ 150 Billion in the year 2011-12 with net profit

of $ 7.58 Billion. Total unit sales of the company stood at maximum in the industry i.e. 9.025

million units sold worldwide, corresponding to 11.9% market share of the global motor

vehicle industry which makes GM the number one manufacturer in auto sector.

(Source: GM Press Release ,January 20th 2012. "GM global sales up 7.6% in 2011 to 9.026M

vehicles; China and US largest markets". Green Car Congress. )

3.2 Vision & Strategy

The GM is focused on a single global vision:

“To design, build and sell the world’s best vehicles.”

“ To be the world leader in transportation products and related services.

We will earn our customer’s enthusiasm through continuous improvements driven by the

integrity, teamwork and innovation of GM people.”

20

This powers the development of world-class products that are winning in the marketplace,

and is helping to transform the business and fortify the balance sheet of GM.

Figure 3.1: New GM Business Model

(Source: www.gm.com)

Here’s how GM brings the insight, drive and vision of its business model to the market every

day to yield positive results for its investors, employees and customers worldwide:

1. Design

Focusing on core brands; leveraging global resources to create the most compelling vehicles

and technologies, leading in the research and development of advanced technologies to

reinvent the future of transportation.

2. Build

Optimizing its global footprint to cost-effectively develop best-in-segment vehicles.

Maximizing the efficiencies of operating its facilities in an environmentally and socially-

responsible manner.

3. Sell

Maximizing revenues with a focused brand strategy; delivering world-class vehicles to the

marketplace that offer its customers higher residual value, with lower incentives and

appropriate pricing.

21

4. Reinvest

Consistently reinvesting cash and profits into vehicle and technology development at

strategic points in the business cycle. Putting its financial strength to work to ensure the

economic viability of the company.

3.3 General Motors in India:

General Motors India has its headquarters in Gurgaon, Haryana, and has two assembly plants

(in Talagaon, Maharashtra and Halol, Gujarat) with a combined production capacity of

385,000 vehicles per year.

It also has a technical centre in Bangalore which focuses on research and development,

vehicle engineering activities, purchasing and financial support services, and vehicle engine

and transmission design.

The company first started doing business in India in 1928, assembling Chevrolet cars, trucks

and buses, but ceased operations in the country in 1954. It continued its tie-up with Hindustan

Motors to build Bedford trucks, Vauxhall cars, Allison Transmissions and off-road

equipment.

In 1994, General Motors India Private Limited (GMIPL) was formed as a 50-50 joint venture

between GM and Hindustan Motors. GMIPL started out producing and selling Opel vehicles,

and was bought over completely by GM in 1999. Till 2003, the company continued to

produce Opel cars at its Halol facility. Later, it switched to producing Chevrolet vehicles at

the same plant.

GM is the sixth largest passenger cars manufacturer in India with a Market Share of 3.4 % as

of August 2012. (source: www. http://business.mapsofindia.com)

3.4 Joint Venture of GMIPL with SAIC

In December 2009, Chinese auto company Shanghai Automotive Industry Corporation

(SAIC) bought a 50 percent stake in GM India. The new joint venture company is called

General Motors SAIC Investment Limited (GMSIL) and is the sixth largest automobile

manufacturing company in the country after Maruti Suzuki, Hyundai, Tata

Motors & Mahindra and Toyota. (source: www. http://business.mapsofindia.com)

22

3.5 Products in the Indian Market

General Motors India has many products in its portfolio which are accepted as value for

money by the Indian Market. Following are the Products and their specifications.

3.5.1 GM-Chevrolet Products in India

The GM currently manufactures & sells its Chevrolet brand products in India. Since 2003, it

has launched eleven products in various categories from small car, sedan to SUV.

Some other brands like GM corvette are also launched by the company to attract the premium

segment customers.

Following is the list of various GM Chevrolet brand models and their technical specifications

& Prices which explains the segment, Price range in which GM India operates.

In the near future GM India plans to launch the vehicles in Hatchback, Multi Utility Vehicles

and Notchback segments which will enhance its product portfolio to capture two digit market

share from the current 3.4 % share.

1 Chevrolet CorvetteSpecs ValuesEngine 6.2 L V8Max Torque 424 Nm @ 4600 rpmMax. Power 430 hp @ 5900 rpmTransmission 6-Speed AutomaticFuel Type PetrolPrice 50 Lacs

2 Chevrolet CaptivaEngine 2.2 LMax Torque 320 Nm @ 2000 rpmMax. Power 150 PS @ 4000 rpmTransmission 5 Speed ATFuel Type PetrolPrice 18 -20 Lacs

3 Chevrolet CruzeEngine 1.8L I-4Max Torque 326 Nm @ 2600 rpmMax. Power 138 bhp @ 4400 rpmTransmission 5-Speed ManualFuel Type PetrolPrice 11.25-15.25 Lacs

23

4 Chevrolet Optra MagnumEngine 1.6 L VGISMax Torque 148 Nm @ 4000 rpmMax. Power 104 PS @ 5800 rpmTransmission 5-Speed ManualFuel Type PetrolPrice 7.30-9.99 Lacs

5 Chevrolet TaveraEngine 2.5L Direct Injection Turbo DieselMax Torque 186 Nm @ 1800 rpmMax. Power 80 PS @ 3900 rpmTransmission 5-ManualFuel Type PetrolPrice 6.50-10.15 Lacs

6 Chevrolet Optra SRVEngine 1.6 L VGISMax Torque 140 Nm @ 4500 rpmMax. Power 101 PS @ 5800 rpmTransmission ManualFuel Type PetrolPrice 7.31-7.87 Lacs

7 Chevrolet AveoEngine 1.4LMax Torque 127 Nm @ 3400 rpmMax. Power 94 PS @ 6200 rpmTransmission 5 Speed ManualFuel Type PetrolPrice 5.97-7.42 Lacs

8 Chevrolet Beat DieselEngine 1.0 L Smartech EngineMax Torque 150 Nm @ 1750 rpmMax. Power 58.5 PS @ 4000 rpmTransmission 5- Speed ManualFuel Type DieselPrice 4.29-5.73 Lacs

9 Chevrolet Aveo U-VAEngine 1.2 L I-4Max Torque 110 Nm @ 4400 rpmMax. Power 76 PS @ 5500 rpmTransmission 5 Speed ManualFuel Type PetrolPrice 3.99-5.49 Lacs

( Source : www.carwale.com)

24

10 Chevrolet Beat PetrolEngine 1.0 L S-TEC II 16VMax Torque 108 Nm @ 4400 rpmMax. Power 79 bhp @ 6200 rpmTransmission 5-Speed ManualFuel Type PetrolPrice 3.42-4.92 Lacs

11 Chevrolet SparkEngine 1.0 L Max Torque 90 Nm @ 4200 rpmMax. Power 63 PS @ 5400 rpmTransmission ManualFuel Type PetrolPrice 3.19-4.23 Lacs

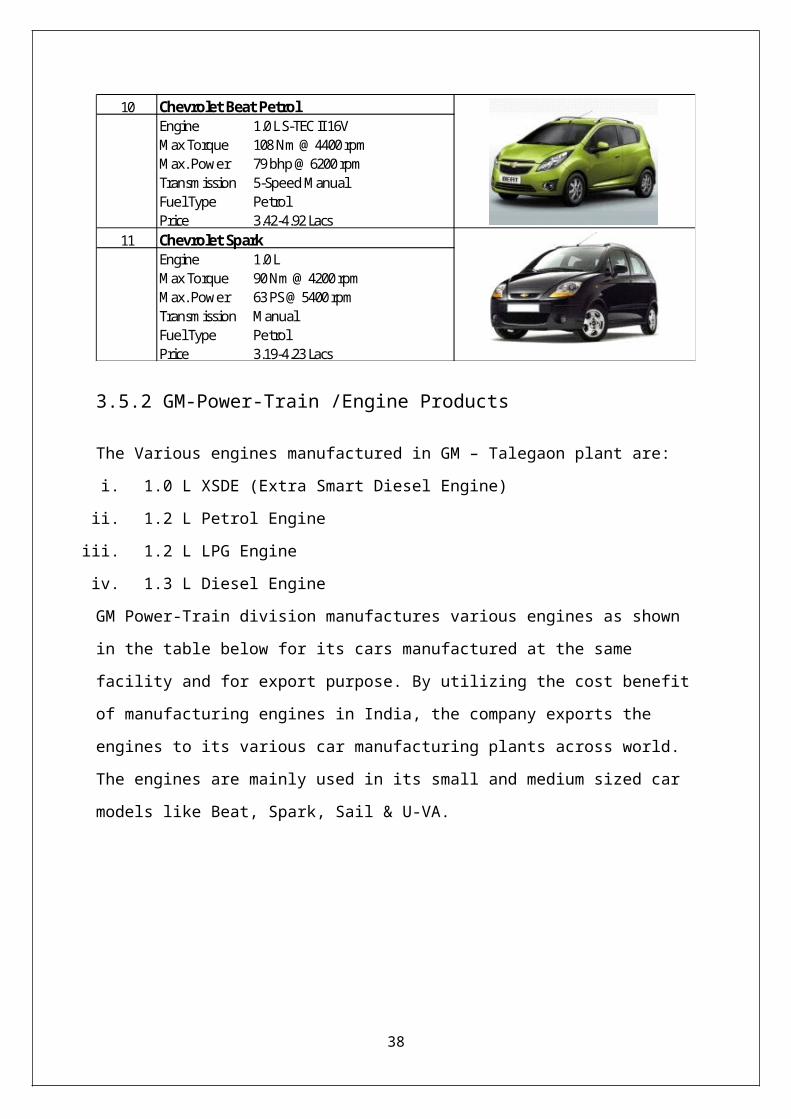

3.5.2 GM-Power-Train /Engine Products

The Various engines manufactured in GM – Talegaon plant are:

i. 1.0 L XSDE (Extra Smart Diesel Engine)

ii. 1.2 L Petrol Engine

iii. 1.2 L LPG Engine

iv. 1.3 L Diesel Engine

GM Power-Train division manufactures various engines as shown in the table below for its

cars manufactured at the same facility and for export purpose. By utilizing the cost benefit of

manufacturing engines in India, the company exports the engines to its various car

manufacturing plants across world. The engines are mainly used in its small and medium

sized car models like Beat, Spark, Sail & U-VA.

Sr No Engine name Type C.C Drive Vehicle application Models

1 XSDE (Xtra Smart Diesel Engine) Diesel 1L FWD Beat,Spark Diesel

2BDOHC (Base Double Over Head Cam )

Petrol (GAS), LPG

1.2 L FWD Beat, Spark Petrol

3NGS SDE (New Generation System - Small Diesel Engine)

Diesel 1.3L FWDU-VA Diesel,

Sail Diesel

4NGS BDHOC (New Generation System -Base Double Over Head Cam )

Petrol (GAS),LPG

1.2 L FWDU-VA Petrol, Sail

Petrol

5 CN 100 SDE (Small Diesel Engine) Diesel 1.3L RWD Enjoy (Diesel) Enjoy (Future)

General Motors India Pvt. Ltd. Talegaon POWERTRAIN Engine Series

Beat, Spark

Sail (U-VA)Hatch back, Sail Notch

back (Future)

Table 3.1: GM India Power-Train division products (Source: GM India database)

25

4.0 LITERATURE REVIEW & NEED/PURPOSE OF THE

PROJECT

4.1 Definition: Reconciliation

4.1.1 Reconcile:

To bring (two or more different aims, points of views etc.) into agreement.

4.1.2 Reconciliation:

Item by item examination of two related sets of figures obtained from different sources.

Most commonly, this term is applied to bank reconciliationof stocks/funds. In the same

manner, it is applicable to Stocks/Inventory in case of Supply Chain Management (SCM).

In our study of the Inventory Reconciliation of Sub-Contracted parts, the two different

sources of data are the physical Inventory count at the Supplier’s end & the ERP System

maintained inventory record for the same supplier.

4.2 Concept of Reconciliation:

In general, The Reconciliation is the process of :

Item by item Examination of two sets of figures where

1. The sets of figures collected are related in the same context e.g. in SCM, the

dispatch & receipt ofMaterial between two parties

2. The source of sets of figures will be different. i.e. The data about dispatch of

material from sender & receipt of material by the receiver.

When the two different sets of data are collected from the two parties, it will be considered as

the data collected from different sources, which can be further reconciled.

The two records of the inventory i.e. physical Inventory count at the Supplier’s end & the

ERP System maintained inventory record for the same supplier, at the predetermined date are

collected and cross checked for discrepancies. If no discrepancies are found, a Reconciliation

Note is prepared and approved.

If some discrepancies are found, they are investigated, reasons are found for the same. And

the difference is eliminated by appropriate adjustment in the system with required approvals

or debit on supplier. In detail Reconciliation process is explained in the latter part.

26

4.3Purpose of Reconciliation

Purpose of Stocks/ Inventory Reconciliation in Supply Chain Management

(SCM):

Inventory reconciliation is very important when the parts are sub-contracted to the vendors &

there is a flow of material to and fro the Suppliers. To understand the need of reconciliation

for Sub-Contracted parts it is mandatory to understand the Supply Chain & Sub-Contracting

Process in it.

4.3.1 Supply chain & Supply Chain Management

4.3.1.1 Supply Chain

A supply chain is a system of organizations, people, technology, activities, information and

resources involved in moving a product or service from supplier to customer.

It isreferred to as the logistics network of facilities i.e. Suppliers, manufacturers, warehouses,

distribution centers & retail outlets and the inventory in the form of Raw materials, Work-in-

process (WIP) inventory & Finished productsthat flow between the facilities.

There are majorly three types of flow that take place in a Supply chain

i. Material

ii. Information

iii. Finances

4.3.1.2 Supply Chain Management:

A set of approaches used to efficiently integrate Suppliers, Manufacturers, Warehouses &

Distribution centers So that the product is produced and distributed in the right quantities, to

the right locations and at the right time so as the System-wide costs are minimized

andService level requirements are satisfied.

So the function of a Supply Chain Management is to Integrate;

i. Suppliers

ii. Manufacturers

iii. Warehouses

iv. Distribution System

27

So that the product is produced & distributed in

i. In the right quantities

ii. To the right locations and

iii. At the right time

With the objective to achieve is

i. System-wide costs are minimized and

ii. Service level requirements are satisfied

Figure below shows the overall structure, integration & flow of Material, information &

Finances in a Supply Chain.

Figure 4.1: Supply Chain activities (Source: http://www.supplychainmanagement.in)

4.3.2Sub-contracting

The practice of assigning part of the obligations and tasks under a contract to another party

known as a subcontractor.Subcontracting is especially prevalent in areas where complex

projects are the norm, such as construction and information technology. Subcontractors are

hired by the project's general contractor, who continues to have overall responsibility for

project completion and execution within its stipulated parameters and deadlines.

In Automotive manufacturing, where large number of parts go into the final assembly of a

vehicle , it’s a smart & obvious move to sub-contract some items to the suppliers to achieve

28

Plan Source Make Deliver Buy

cost, time and quality obligations. In this process, The Original Equipment Manufacturer

(OEM) is the Customer & the service providing vendors are the suppliers. The OEM supplies

some parts & receives the parts in theform of sub-assembly or assembly.

4.3.2.1The Process of Sub-Contracting the Parts to Suppliers:

In Supply Chain Management(SCM) certain parts needs to be sub contracted to the vendors

for various purposes i.e. machining, sub-assembly, Assembly.

The various organizations Sub-Contract some parts/ Sub-Assemblies in their products

because of various reasons like:

1. Optimum Capital utilization in manufacturing of only critical parts& assemblies and

rest of the parts can be Sub-contracted to the vendors/Suppliers.

2. Special Purpose Machines / Capabilities available with certain vendors which may

need large Capital investment or high complexity & monitoring. Such parts

manufacturing & processing is delegated to the Vendors.

3. Convenience in terms of nearness from the Delivery point. E.g. Some companies

utilize the facilities of vendors who are located nearer from the harbours, Air ports or

Delivery points to optimize the delivery time & cost.

4. Some tooling development at particular vendor after modifications in his(Vendor’s)

existing facility will be cost effective for the company instead of fresh capital infusion

in buying new tooling.

5. Reduce Risk by delegating the manufacturing. This is in context of some rescheduling

of projects/ orders. The risk of non-utilization of inventory, manpower & capital will

be distributed between the Customer (the firm who Sub-Contracts) & Supplier firms.

6. Outsourcing is a better option for certain one time or less frequent activities where the

facilities of suppliers can be utilized intermittently by the Customer firm.

7. Some parts can be manufactured by certain vendors in smaller batches with high cost

efficiency.

8. The special high skilled manpower can provide required services to the customer firm

whenever required. This is applicable where it is not feasible to maintain such

manpower on continuous basis by the Customer firm due to one or more reasons.

29

4.3.3 Flow of Materials during Sub-Contracting:

While Sub-Contracting the parts manufacturing or Services to the vendors, there is a

continuous transaction of materials between Supplier & the Customer firm in following

manner -

1. The material which goes from Customer firm to the supplier as sub-contracted items

are called child part & the part which are returned by the supplier firm to the customer

firm are called parent parts.

2. The child parts material is issued by the customer firm to the supplier when required

for sub-assembly, assembly or processing and

3. After processing, the parent parts are returned to the Customer firm with the sub-

assembly or assembly.

4. The transactions are maintained in the books and/or systems.

5. The respective financial transactions are maintained in the Supplier’s Accounts.

6. The inventory moves from Customer firm to Supplier firm in computerized systems.

7. The child parts are credited to the supplier’s account when it is issued to him & they

are debited from Supplier’s account when it is returned along with the parent part by

the supplier.

8. The inventory accounts are maintained and updated as the inventory moves between

the two firms.

4.3.4 Purpose of Reconciliation:

In ideal condition, there should be hundred percent perfection in maintaining the inventories

between the customer & supplier firm’s accounts. But there are certain cases where this

system of inventory accounting is disturbed. Following are the reasons which can be

responsible for them.

1. Some items are scheduled for dispatch by the customer firm but the dispatch is

cancelled due to some reasons. The system entry is done initially but physically the

material doesn’t move.

2. The order is re-planned as per the updated requirement after entering the order details

in the system. But the previous system entry is not discarded.

30

3. When the parent parts are rejected at the Customers end, the child parts should be

credited to suppliers account along with the parent parts credit. But only the parent

part is credited and child part inventory accounts get disturbed.

4. Manual errors contribute a large part in this regard. The manual errors can be of the

following types :

i. Entering a wrong invoice number or other details i.e. quantity, date or Supplier

name while making an entry in the Material shipping or receiving register.

ii. Making a mistake while making an entry in the system when updating the system

with the manual register of Material Shipping or Receiving.

iii. At Supplier’s end the same mistake can take place which creates difficulty while

reconciling the invoice numbers.

iv. The invoice copies are not entered at all in the register. So such entries are not

found while reconciling the inventory.

v. The invoice hard copies are lost, some times before the entry is made in the

register and the system.

5. Theft is another reason to reconcile inventory. If there is theft occurring in the

warehouse, the system maintained inventory will be higher than the physically

available inventory which will show a wrong figure and cause stock-out condition on

the assembly line. This will hamper production & supply of goods.

6. Damage of parts during transit or during handling. The damaged parts if not treated

accordingly in the system record will show a wrong picture regarding receipt &

delivery of child parts and Parent parts respectively.

7. The damaged parts or short supply needs to be updated in the system timely to

maintain a true record of inventory.

8. Inventory reconciliation can affect a company’s tax liability. Taxes can be accessed

on the unsold balance of inventory based on the company’s accounting information.

Inaccurate balances can result in companies having to pay more money in taxes from

faulty inventory information. Additionally, paying taxes on damaged, obsolete, or

otherwise unsellable goods results in more money lost from poor inventory figures.

The main purpose of reconciling the inventory is to maintain the system & physical inventory

numbers in harmony. The most important aspect of this is to be able to get the updated

information of inventory as and when required.

31

The matched figures between system & physical record allow,

1. Materials Manager to plan the movement of Inventory in and out of the factory may

be in terms of Raw material, WIP and Finished Goods.

2. The sales personnel to know if enough inventory exists to meet company orders /

Customer Requirements.

3. Plant personnel can know if enough raw material& WIP inventory is on hand to meet

production needs.

4. The Finance Personnel can plan the funds accordingly for the purchase of material

etc.

4.4 Types of Reconciliation Methods & General Procedureof Stocks

Reconciliation

4.4.1Types of Reconciliation Methods

Inventory reconciliation involves mainly two steps:

1. Physical Inventory

2. Accounting Inventory

1. Physical Inventory:

The steps including in Physical Inventory are:

i. Physical Count of the Inventory in the warehouse

ii. Taking a written inventory record and

iii. Comparing it to the actual goods in the company’s warehouses.

iv. Counting obsolete and damaged products.

2. Accounting Inventory :

Reconciliation steps on the accounting side include

i. Verification that all inventory purchases are posted,

ii. Entering adjustments from the physical count and

iii. Analyzing the dollar differences between months.

32

4.4.2 Types of Inventory Systems:

There are two types of inventory systems common in business:

1. Periodic Inventory System and

2. Perpetual Inventory System.

Both involve tasks or activities that relate to the physical and accounting methods of

inventory reconciliation which are as explained ahead.

1. Periodic Inventory System:

This system is somewhat easier, as it only requires for the recording of financial inventory

information on a monthly, quarterly, or annual basis. For example, the general ledger will

include a starting figure for the quarter. Accountants will add the total inventory purchases

for this time period, deduct sales and adjustments, and then present a final figure on the

company’s balance sheet.

Physical inventory counts under the periodic method are typically quarterly or annual. More

frequent counts may be necessary if theft occurs, or if a significant number of inventory

products continually wind up damaged going through the company’s processes.

2. Perpetual inventory System:

This method records and reconciles inventory information after each purchase, sale, or

adjustment to the general ledger account. Inventory reconciliation under the perpetual method

is much more accurate than the periodic system. Companies with individual or unique

inventory products will often use the perpetual system because of the large variety of goods

within the company’s warehouse. Physical inventory counts are often annual, although cycle

counts may be more frequent. Cycle counts help maintain records on a weekly basis to ensure

significant adjustments are not made to the company’s general ledger at one time.

In our study & subsequent reconciliation practice, the reconciliation is carried out under the

Periodic Inventory system where the Annual Physical Inventory(API) has been conducted

after ten months.

The system data is prepared and the Physical Inventory figures will be collected & compared

for action either an adjustment in the system or Debit to the Supplier.

33

4.4.3 General Procedure of Stocks Reconciliation:

The reconciliation is mandatory everywhere whenever there is flow of material. Every type of

industry handles certain type of material. The physical count of stocks is checked periodically

for its match with the Book Records for purposes discussed previously. Though it be FMCG

sector or Pharmaceutical sector or any other manufacturing sector, if there is flow of material,

Reconciliation of inventory has a vital place. There are certain steps that you should follow

during the reconciliation of inventory.

In particular, you should consider following any or all of these steps:

1. Recount the inventory:

It is entirely possible that someone incorrectly counted the inventory. If so, have a

different person count it again (since the first counter could make the same counting

mistake a second time). Further, if the physical count appears to be significantly lower

than the book balance, it is quite possible that there is more inventory in a second

location - so look around for a second cache of inventory. Recounting is the most

likely reason for a variance, so consider this step first.

2. Match the units of measure:

Are the units of measure used for the count and the book balance the same? One

might be in individual units (known as "eaches"), while the other might be in dozens,

or boxes, or pounds, or kilograms. If you have already conducted a recount and there

is still a difference that is orders of magnitude apart, it is quite likely that the units of

measure are the problem.

3. Verify the part number:

It is possible that you are misreading the part number of the item on the shelf, or

guessing at its identification because there is no part number at all. If so, get a second

opinion from an experienced warehouse staff person, or compare the item to the

descriptions in the item master records. Another option is to look for some other item

for which there is a unit count variance in the opposite direction - that could be the

part number that you are looking for.

4. Look for missing paperwork:

This is an unfortunately large source of inventory reconciliation issues. The unit count

in the inventory records may be incorrect because a transaction has occurred, but no

one has yet logged it. This is a massive issue for cycle counters, who may have to root

around for un-entered paperwork of this sort before they feel comfortable in making

34

an adjusting entry to the inventory records. Other examples of this problem are

receipts that have not yet been entered (so the inventory record is too low) or

issuances from the warehouse to the production area that have not been entered (so the

inventory record is too high).

5. Examine scrap:

Scrap can arise anywhere in a company (especially production), and the staff may

easily overlook its proper recordation in the accounting records. If you see a modest

variance where the inventory records are always just a small amount higher than the

physical count, this is a likely cause.

6. Investigate possible customer ownership:

If you have no record of an inventory item at all in the accounting records, there may

be a very good reason for it, which is that the company does not own it -

a customer does. This is especially common when the company remodels or enhances

products for its customers.

7. Investigate possible supplier ownership:

To follow up on the last item, it is also possible that you have items in stock that are

on consignment from a supplier, and which are therefore owned by the supplier. This

is most common in a retail environment, and highly unlikely anywhere else.

8. Investigate Back-flushing records:

If your company uses Back-flushing to alter inventory records (where you relieve

inventory based on the number of finished goods produced), then the bill of

materials and the finished goods production numbers had better both be in excellent

condition, or the reconciliation process will be painful. Back-flushing is not

recommended unless your manufacturing record keeping is superb.

9. Accept the variance:

If all forms of investigation fail, then you really have no choice but to alter the

inventory record to match the physical count. It is possible that some other error will

eventually be found that explains the discrepancy, but for now you cannot leave a

variance; when in doubt, the physical count is correct.

35

4.5 Global Manufacturing System (GMS)

GMS is a set of standards which describe the what, why and how to organize manufacturing

operations in GM in order to eliminate waste. Within GMS, waste is defined as “anything

that the customers are not willing to pay for.” Elimination of waste is the only way to survive

as a company.

The structure of GMS is organized around five principles –

1. People Involvement

2. Continuous Improvement

3. Standardization

4. Short Lead Time (SLT)

5. Built in Quality

1. People Involvement

GM recognizes its employees as the most valuable resource, and will provide the support

necessary to allow all the people to work in a motivated, empowered and particular way.

2. Standardization

A dynamic process by which the work is documented, followed and performed according to

core standards, terminology, principles, methods, and processes to achieve a common base

from which to improve.

3. Built-in Quality

Quality expectations are achieved in each process to ensure defects are not passed on to the

following process.

4. Short Lead Time

Reduce the time from the placement of an order by the final customer to the delivery of the

product and receipt of payment. There are three types of lead time:

i. Total Lead Time

ii. Product Development Lead Time and

iii. Process Lead Time.

5. Continuous Improvement

GM fosters an attitude which nurtures change and supports all employees in improving their

own jobs and environment for the continuous improvement of the company.

36

Within each of these five principles are several unique operating concepts named “Elements”

which define particular ways to accomplish a particular part of all the manufacturing effort.

In total, there are 33 Elements, each one belonging to one of the 5 Principles. The most

important thing to understand about the Principles and Elements is that it takes ALL of them

to form GMS.

Figure 4.2: Principles of the Global Manufacturing System (GMS)

Figure 4.3: 33 Elements of The GMS Principles (Source: GMS Tri-fold, GM India)

37

The GMS is implemented at all the manufacturing facilities & offices of General Motors. It is

implemented at GMI’s newly formed Power Train division manufacturing facility &it’s

offices at Talegaon, Pune from Day one.

4.6 Overview of GPSC Department activities in GM India

4.6.1 Study Of Global Purchasing & Supply chain (GPSC) Process:

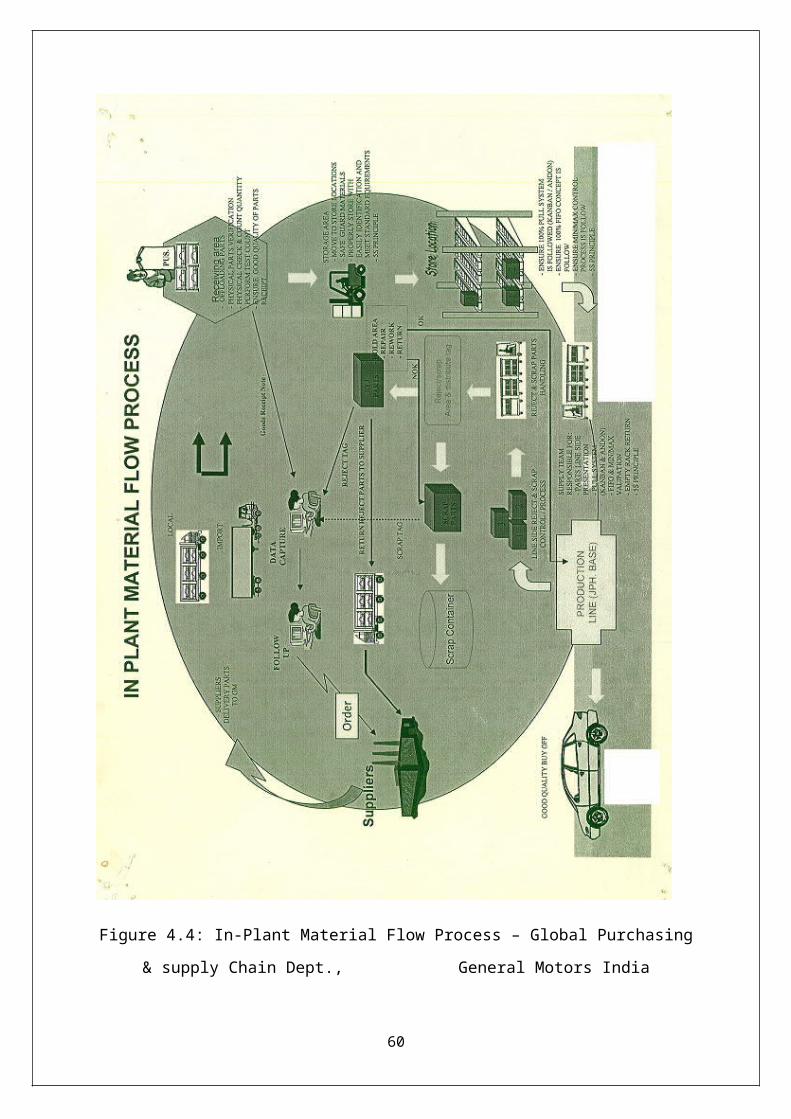

The chart below shows the Process Map of the whole GPSC - activities carried out in the GM

India Power-Train Plant which can be explained as below:

1. Data Capture center captures the data for new material requirement and generates

Purchase Orders

2. The Follow up team follows up & tracks the dispatches of the material from Supplier

& their movement in Transit as per the schedules of material

3. The Goods Supplied by the Suppliers is received & Goods Received Note is Prepared.

The GRN data flows to the Data Capture center

4. The material is stored in the Storage area at the appropriate Storage Locations. There

the Identification of material, 5 S application & safety of the material is taken care of.

5. The material in storage is inspected before it is used. The Inspection test passed

material moves ahead in special locations to be further used for Production.

6. The material failing to pass inspection test is sent to Hold area. Here the material can

be treated in three ways,

i. Repair & send for location of inspection test passed material.

ii. Rework &send for location of inspection test passed material.

iii. Return to the Supplier or reject

7. The material ready for Production moves to Production area & further Production

takes place.

8. The Line side rejects during the Production & after Production are again sent to Hold

area where they are treated for correction and sent back to use or rejected.

9. The Quality test passed final product is sent for Sale to the Customers.

10. The Rejected parts are treated in following ways,

i. Return the material to the Supplier after preparing the Reject Tag by Data

Capture center.

ii. Scrap the material after Preparing Scrap Tag by the Data Capture center.

38

Figure 4.4: In-Plant Material Flow Process – Global Purchasing & supply Chain Dept.,

General Motors India

39

4.6.2 Study of Roles & Responsibilities of Schedulers:

The reconciliation of the Sub-contracted parts being a responsibility of Scheduling team,

there was an opportunity to study the activities carried out by the Schedulers in the Global

Supply Chain group of GPSC. A summary of the activities studied during the project period

is given below:

The roles and responsibilities of a scheduler are as following:

1. To ensure that the scheduled supply quantities are sufficient to cover daily Schedule.

2. To ensure the material flow is being maintained or to take appropriate action &

escalate the issues.

3. To ensure that the suppliers supply the material as per schedules

4. To ensure that the shipments are followed by the Suppliers and monitor & co-ordinate

the activity

5. Monitoring inventory status in system & it’s compliance with physical inventory

6. To Verify receipts of material in ERP system and respective packing details

7. To Performs physical inventory of parts as required

8. To Analyze and correct discrepancies in the balances of supply & inventory

9. To ensure reduction in inventory levels

10. Make corrections in the system as and when required

11. To Maintains supplier contact information

12. To Report problem parts or suppliers, status to schedule, recovery plans

13. To Coordinate for part changes and communicate to suppliers

14. To Support Production activities including new launch activities

15. To Verify that the contracts are current and request the GM purchasing team to renew

expired or expiring contracts

16. To Verify the cumulative yearly shipments match with supplies and reconciles

differences

40

5.0 RESEARCH METHODOLOGY –

Third Party Stocks/Inventory Reconciliation at GM India Power-Train Plant

In GM India, Power Train Plant, the Reconciliation Process has been standardized when the

plant became operative. This process is finalized on the basis of the guidelines from Global

Manufacturing System (GMS) standardization concept.

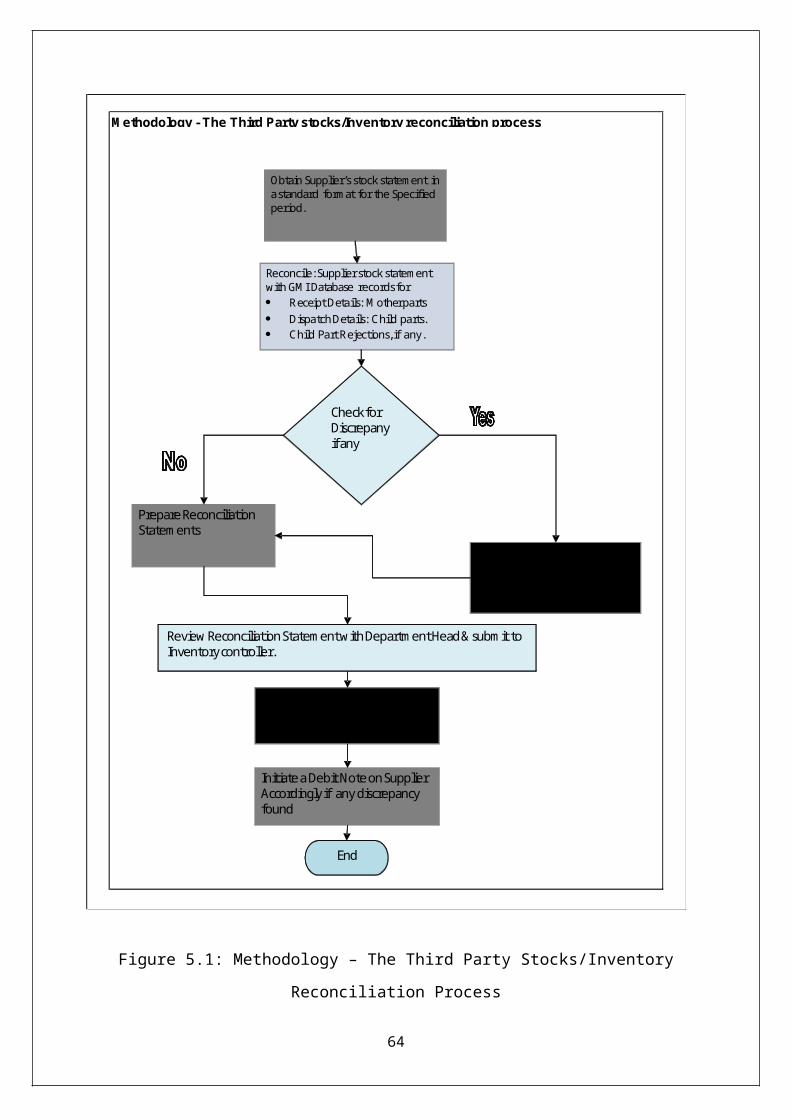

5.1 Methodology for the Third Party Stocks/ Inventory Reconciliation Process

at GMI

Following is the methodology to be followed for Third Party Stocks/Inventory Reconciliation

in GMI.

Methodology for Third Party stocks Reconciliation :

1. Obtain Supplier’s stock statement in a standard format for the Specified period.

2. Reconcile: Supplier statement with GMI database records for Mother Parts receipts,

Child parts dispatches, Child Part Rejections, if any.

3. Obtain Supplier’s Reconciliation Statement in a standard format for the Specified

period in case of discrepancy else review reconciliation statement with department

Head & submit to inventory controller.

4. After finance approval post the discrepancy if any in ERP system.

5. Raise the debit note on supplier in case any discrepancy found at supplier end.

6. Once in a year the stock at supplier end will be taken in presence of GM employee.

41

Methodology - The Third Party stocks/Inventory reconciliation process

Reconcile: Supplier stock statement with GMI Database records for Receipt Details: Mother parts

Dispatch Details: Child parts. Child Part Rejections, if any.

Obtain Supplier’s stock statement in a standard format for the Specified period.

Check for Discrepany if any

Obtain Supplier’s Reconciliation Statement in a standard format for the Specified period.

Prepare Reconciliation Statements

Review Reconciliation Statement with Department Head & submit to Inventory controller.

After finance approval post the variance/ discrepancies in ERP

Initiate a Debit Note on Supplier Accordingly if any discrepancy found

End

Figure 5.1: Methodology – The Third Party Stocks/Inventory Reconciliation Process

42

5.2 Stocks/ Inventory Reconciliation Conducted in GMI Power-train

Plant:

This project covers the actual Stocks / Inventory Reconciliation Conducted for the Sub-

Contracted parts in Power Train Plant of General Motors India.

Following are the various steps followed as per the methodology shownabove to carry on

Reconciliation of the Inventory for the Eight Selected Sub-Contracted parts.

These parts are used in the assembly of Petrol, Diesel & LPG engines manufactured at GMI

Power-Train Plant in Talegaon, Pune, India.

List of Parts Reconciliated:

The table below shows the Nine Sub-Contracted Parts:

List of Sub-Contracted Parts Reconciliated

Child Stud Parent BracketChild Stud Parent Bracket assemblyChild BracketParent Fuel Rail Child Sensor Parent Manifold AssemblyChild NutParent BracketChild Switch AssemblyParent Housing Assembly Child Raw Cylinder BlockParent Cylinder Block Engine (Partial Machining)Child Crank Case Assy. (Bed Plate)Parent Bed PlateChild Sensor Assembly Parent Manifold Assy

Sr. No

Vendor Name

1

8 MARK IV

4 Magneti Marelli Motherson Auto Systems

Part Name

7.1 SHRINIWAS ENGINEERING AUTO COMPONENT PVT. LTD.

7.2 SHRINIWAS ENGINEERING AUTO COMPONENT PVT. LTD.

5 MEHTA ENTERPRISES

6

Part Type

ENDURANCE SYSTEMS (INDIA) PVT LTD

2 CONTINENTAL ENGINES LIMITED

UFI Filters India pvt Ltd

3 CIKAUTXO TAURUS FLEXIBLES PVT LTD

Table 5.1: List of sub-contracted Parts reconciliated

43

5.2.1 In Detail Procedure of Reconciliation

The Procedure adopted for Reconciliation can be elaborated as given below:

Step I : Obtain Supplier’s statement in a standard format for the Specified Period .

1. The various suppliers are provided with a standard format to maintain the data of all

the receipts& dispatches of sub-contracted parts from GM India.

2. All the Supplier’s maintain the data on daily basis & communicate the same to GMI

monthly.

3. For Reconciliation purpose , a consolidated data for the last six months was invited.

4. The Format of Reconciliation Data are as shown below:

i. The Format of Child Part receipt from GM to Supplier:

Format - Receipt of Child Part from GM to SupplierVendor Code

Vendor NamePart No. Part NameChild Part receipt from GM to Supplier Source : Supplier Data

Sr.No. Inv.No. Date Qty.1

2

3

4

5

6

7

8

9

10

Total

Nomenclature : 1. Inv.No. : GM Invoice number for Child Part dispatch from GM to Vendor 2. Date : Date of Invoice3. Qty. : Quantity of material (Child Parts) Dispatched.

44

- Suppliers maintain the Reconciliation data in the form of Child Part receipt data &

parent part dispatch data.

- The invoice number which is maintained on the above format sheet is important to

reconcile the child parts dispatched from GM to suppliers.

- This invoice number is generated by GM and the same invoice number can be found

in GM child part data.

ii. The format for Parent/Mother part dispatch from Supplier to GM:

Format : Mother Part dispatch from Vendor to GMVendor Cd

Vendor Part No. Part Name

Source : Supplier Data Mother Part dispatch from Vendor to GM

Sr.No. Invoice No. Qty. Date12345678910

Total

Nomenclature : 1. Invoice.No. : Vendor Invoice number for Parent Part dispatch from Vendor to GM 2. Date : Date of Invoice3. Qty. : Quantity of material (Parent/Mother Parts) Dispatched.

Dispatch from Supplier to GM

- As like child part , the suppliers maintain their Parent part dispatch details to GM.

- The invoice number maintained in above format is also recorded in GM records when

this material is received at GM.

45

- This invoice number is cross verified with GM data invoice numbers to reconcile the

parent part details.

Sr. No. RGP RGP DT Inv. No. Qty. Despatch

DateRemark about Mtl.

ReceiptSr. No. Inv. No. Qty. Invoice Date

1 if RGP material if Invoice matrl 12 23 34 45 56 67 78 89 9

10 10

Total Qty Receipt 0

Opening Stock as on 01.01.2012 ATotal Invoice Qty. BTotal Dispatch Qty. CBalance Qty. as per records D D = A + B - C

Total Qty Dispatch

Reciept(Invoice) Details of Child Parts from GMI (PT) to Supplier Dispatch Details of Parent Part from Supplier to GMI (PT)

Child part Number & name: Parent Part Number & Name:

GMIPowertrain

Figure 5.2: Format of Reconciliation data received from Supplier.

Step II : Reconcile: Supplier statement with GMI Database/ERP records for

Mother Parts receipts,Child parts dispatches, Child Part Rejections, if

any.

Step II.I - Collection of Data from GM ERP for the respective part & Supplier .

1. In the similar manner, the data available in GM ERP System is obtained & structured

in a standard format.

2. Data of all the vendors is collected from the system & structured in the format to

compare the two sets of data for reconciliation purpose.

3. The formats used at GM’s end for structuring the data to be compared with that of

Supplier’s are as shown :

46

i. Format for Child Part dispatch from GM to supplier

Format - Child Part Supply from GM to VendorVendor NameVendor CodePart No. Part Name Child Part Supply from GM to VendorSource of Data : GM ERP session / manual Record.

Sr.No. QUANTITY SHP DATE SHIP NO INVOICE NO12345678910

Total

Nomenclature : 1. Quantity : Qty. of material Dispatched from GM to Vendor2. SHP DATE : Shipment date on which Shipment made to Vendor3. SHIP NO. : Shipper Cut number in ERP for the Shipment4. Invoice No. : The GM System generated Invoice number for the said shipment.

47

ii. Format for Parent /mother Part receipt from Supplier to GM

Format : Mother Part receipt from Vendor to GMVendor Cd

Vendor Part No. Part NameParent Part Receipt from Supplier to GM Source : GM ERP Data

Sr.No. DOC_ID QTY SHIP_DT SID/Inv.No. PO_NBR

1

2

3

4

5

6

7

8

9

10

Total

Nomenclature : 1. DOC_ID : Document ID for the receipt of material2. QTY : Parent parts Quantity received from Vendor 3. SHIP_DT : Shipment date for the Parent parts shipped from Supplier4. SID : Supplier ID ( SID) = Vendor Invoice no. for the shipment5. PO_NBR : Purchase Order NBR for the dispatch of Material

Step II.II – Compare the two sets of Data

1. The Two sets of data collected from GM System & Supplier are compared.

2. A format for this comparison is as shown below.

3. The child part dispatch from GM to Supplier & receipt of those child parts are

compared against Invoice numbers generated by the GM.

4. The Supplier generates the invoices for the Parent parts dispatch which are compared

against the Invoice details maintained by GM. The comparison is made on the basis of

Invoice numbers of the supplier in this case.

48

5. A summary of the two types of data is created with previous opening stock, fresh

receipts of material, fresh Dispatches of material & the available stock at Supplier and

GM end.

6. The formats used for the above mentioned comparisons & Summary are as given :

Child Part Reconciliation _R2Vendor Cd : Vendor : Part No. : Part Name :Reco Period : Source : ERP Records & SHIPPING RECORD Source : Supplier data

Sr.No. QTY SHP DATE SHIP NO INVOICE NO Invoice Check Sr.No. Invoice No. Qty. Date1 w TRUE 1 w2 x TRUE 2 x3 y TRUE 3 y4 z TRUE 4 z

Total 0 Total 0

Figure 5.3: Format showing the Child part cross verification for Reconciliation purpose

Parent Part Reconciliation R2Vendor CdSupplier Part No. Part Name Reco Period :

Source : Supplier Data Source : GM receipt data - ERP records Mother Part

Sr.No. Invoice No. Qty. Date Inv. Check Sr.No. DOC_ID SHIP_DT QTY SID/Invoice No. QTY Check1 101 288 TRUE 1 288 101 TRUE2 102 192 TRUE 2 192 102 TRUE3 103 192 TRUE 3 192 103 TRUE4 104 180 TRUE 4 180 104 TRUE5 105 288 TRUE 5 288 105 TRUE6 106 336 TRUE 6 336 106 TRUE7 107 336 TRUE 7 336 107 TRUE8 108 24 TRUE 8 24 108 TRUE9 109 288 TRUE 9 288 109 TRUE10 110 336 TRUE 10 336 110 TRUE

Total 2460 Total 2460

Figure 5.4: Format showing the Parent part cross verification for Reconciliation purpose

7. The above collected data is summarized in the form of a Balances summary with

following contents in it :

i. Opening Balance as on starting date of Reconciliation period

ii. Child Part Supply(in GM Record) or Receipt (in Supplier Record)

49

iii. Parent Part Supply (in Supplier Record) & Receipt (in GM Record).

iv. Closing Balance as on last date of the Reconciliation Period.

v. The Format of Balance Summary is as shown below :

Format : Stocks Balance Summary Sheet for ReconciliationRecocniliation Period : 31st Mar' 12 to 29th Jul'12

Supplier Data GM System Data DifferenceOpening stock(stock with Supplier)as on 31st Mar'12

a1Opening stock in GM System as on 31st Mar'12

a2 = (a2 - a1 )

Child Part Recieved during the period b1Child Part Dispatched during the period

b2 = (b2 - b1)

Parent Part Dispatched during The period c1Parent Part Recieved during The period

c2 = (c2 - c1 )

Closing stock as on 29th Jul'12 ( stock with Supplier)

d1Closing stock as on 29th Jul'12 in GM system

d2 = (d2 - d1)

where d1 = a1 + b1 -c1 where d2 = a2 + b2 -c2

Figure 5.5 Format for Stocks Balance Sheet for Reconciliation

Step II.III Find Discrepancies if any.

The Discrepancies are found in two inter-dependent ways,

II.III.iFinding Discrepancy between Supplier System & Documents Record & GM

System &Documents Record

II.III.ii Finding Discrepancy between Supplier Physical Inventory Declaration & GM

System data

II.III.i Finding Discrepancy between Supplier System & Documents Record and

GM System & Documents Record

1. The first step in finding discrepancies is to find them between Supplier’s

computerized systems & manually maintained Document Records & GM System and

document records.

2. The advantage of finding discrepancies between Supplier Doc. Records & GM system

data is that we can compare the two sets of data in documents & try to eliminate the

discrepancies before the Physical count of inventory. This saves the time of

reconciliation after Physical Inventory count. This is the major tool of finding &

eliminating the discrepancies between the two records.

3. The above explained formats & Method is used for finding the non-matching entries

in the two sets of data. Such entries are separated & evidences are collected for them.

4. The evidences are collected in the form of :

50

i. The Invoice hard/Soft copy.

ii. Goods Receipt Note (GRN) number & hard/soft copy.

iii.Other Proof Of Delivery (POD) from GM to Supplier or Supplier to GM, like LR

( Loading Receipt)

iv. System generated reference number of transaction if any.

5. After Collection of evidences, the discrepancy is shared with the other party & data of

both the parties are updated accordingly. This action eliminates the discrepancy.

6. The discrepancies for which the evidences cannot be collected are discarded with due

intimation of the respective party.

After the discrepancies are eliminated, this data becomes the Final system data

which can be compared with the physical count of the Inventory.

II.III.ii Finding Discrepancies between Supplier Physical Inventory Declaration

&Final System Data

1. Here the actual Physical Inventory count takes place first.

2. As Periodic Inventory system is being followed at GM India, the physical inventory

count is carried out at the end of July 2012.

3. The refined final System data which is agreed between GM and Supplier system will

be compared with the Physical Count figures for discrepancy.