PROJECT DEVELOPMENT FACILITY · Web viewTechnical capabilities concerning design, operation and...

83

PROJECT DEVELOPMENT FACILITY CONCEPT FOR PIPELINE ENTRY FINANCING PLAN (US$) GEF ALLOCATION 2.470 Project (estimated) 13.320 Project Co- financing (estimated) 11.350 PDF A* PDF B** 600,160 PDF C Sub-Total GE F PDF 600,1 60 PDF CO-FINANCING (details provided in Part II, Section E – Budget) GEF Agency National Contribution Others 258,000 Sub-Total PDF Co- financing: 258,000 Total PDF Project Financing: 858,160 * Indicate approval date of PDFA ** If supplemental, indicate amount and date of originally approved PDF AGENCY’S PROJECT ID: GEFSEC PROJECT ID: 2683 COUNTRIES: Burundi, Kenya, Malawi, Mozambique, Rwanda, Tanzania, Uganda, Zambia, Zimbabwe PROJECT TITLE: Greening the Tea Industry in East Africa GEF AGENCY: OTHER EXECUTING AGENCY: EATTA ( East African Tea Trade Association) DURATION: 4 years GEF FOCAL AREA: Climate Change GEF OPERATIONAL PROGRAM: OP6: Promoting the Adoption of Renewable Energy by removing barriers and reducing implementation costs. GEF STRATEGIC PRIORITY: SP-3: Power Sector Policy Framework Supporting of Renewable Energy and Energy Efficiency with relevance to SP-1: Transformation of Markets for High Value Products and Processes. ESTIMATED STARTING DATE: PDF-B June 2005; Full Size Project March 2007 ESTIMATED WP ENTRY DATE: OCTOBER 2006 PIPELINE ENTRY DATE: MARCH 2005 1

Transcript of PROJECT DEVELOPMENT FACILITY · Web viewTechnical capabilities concerning design, operation and...

PROJECT DEVELOPMENT FACILITYCONCEPT FOR PIPELINE ENTRY

FINANCING PLAN (US$)GEF ALLOCATION 2.470 Project (estimated) 13.320Project Co-financing (estimated)

11.350

PDF A* PDF B** 600,160PDF C Sub-Total GE F PDF 600,160

PDF CO-FINANCING (details provided in Part II, Section E – Budget)

GEF AgencyNational Contribution Others 258,000Sub-Total PDF Co-financing:

258,000

Total PDF Project Financing:

858,160

* Indicate approval date of PDFA ** If supplemental, indicate amount and date of originally approved PDF

AGENCY’S PROJECT ID: GEFSEC PROJECT ID: 2683COUNTRIES: Burundi, Kenya, Malawi, Mozambique, Rwanda, Tanzania, Uganda, Zambia, ZimbabwePROJECT TITLE: Greening the Tea Industry in East AfricaGEF AGENCY: OTHER EXECUTING AGENCY: EATTA ( East African Tea Trade Association)DURATION: 4 yearsGEF FOCAL AREA: Climate ChangeGEF OPERATIONAL PROGRAM: OP6: Promoting the Adoption of Renewable Energy by removing barriers and reducing implementation costs.

GEF STRATEGIC PRIORITY: SP-3: Power Sector Policy Framework Supporting of Renewable Energy and Energy Efficiency with relevance to SP-1: Transformation of Markets for High Value Products and Processes.

ESTIMATED STARTING DATE: PDF-B June 2005; Full Size Project March 2007ESTIMATED WP ENTRY DATE: OCTOBER 2006PIPELINE ENTRY DATE: MARCH 2005

1

RECORD OF ENDORSEMENT ON BEHALF OF THE GOVERNMENT: (EATTA is in the process of Securing GEF Focal Points Endorsements)Etienne Kayengayene Directeur General of Environment and Land ManagementMinistry of Land Management, Environment and TourismB.P. 631Bujumbura, BurundiTEL: 257 21 3257 / 24 1203FAX: 257 24 1205 / 22 8902

Date: (Month, day, year)

Ratemo W. Micheka Director GeneralNational Environment Management AuthorityPO Box 67839Nairobi Kenya TEL: 254 2 609013FAX : 254 2 608997E-mail: [email protected]

Raphael KabwazaDirector of Environmental AffairsMinistry of Natural Resources and Environmental AffairsLingadzi HousePrivate Bag 394Lilongwe 3, MalawiTEL: (265) 781 111FAX : (265) 783 379E-mail: [email protected]

Francisco Mabjaia Vice-MinisterMinistry for Coordination of Environmental Affairs (MICOA)Rua de Kassuende, 167C.P. 2020 MaputoMozambiqueTEL: (258-1) 495409 / 485265FAX: (258-1) 496108 / 485264

Laurent NkusiMinistre des Terres, de la reinstallation ed de l'EnvironnementBP 3502KigaliRwandaTEL: 250 82628FAX: 250 82629E-mail: [email protected]

Raphael MollelSenior Permanent Secretary Vice President's Office P.O. Box 5380 Dar es Salaam TanzaniaPHONE: (255-22) 2116995FAX : (255-22) 2113856Email: [email protected] 2

Mary MuduuliDeputy Secretary to the TreasuryMinistry of Finance, Planning and Economic DevelopmentFinance Headquarters BuildingPlot 2-12 Appollo Kaggwa RoadPO Box 8147KampalaUgandaTEL: 256 41 234433 FAX : 256 41 250005 E-mail: [email protected]

L.E. KapuluActing Permanent SecretaryMinistry of Tourism, Environment and Natural ResourcesKwacha HouseCairo RoadPO Box 34011Lusaka, Zambia TEL: 260 1 229416FAX : 260 1 229420

Margaret SangaraweMinistry of Environment and Tourism15th Floor, Karigamombe Centre53 Samora Machel AvenueP. Bag 7753 - CAUSEWAY; HarareZimbabweTEL: 263 4 757881

This proposal has been prepared in accordance with GEF policies and procedures and meets the standards of the GEF Project Review Criteria for pipeline approval.

Ahmed DjoghlafAssistant Executive DirectorUNEP/DGEFFax: 254 20 4165

Peerke De BakkerProgramme OfficerUNEP – DGEFTel: ++254-20-623967

Date: March 9, 2005 Email: [email protected]

3

Acronyms and Abbreviations:

ADEME French Agency for Energy and EnvironmentAFREPREN African Energy Policy Research NetworkAREED African Renewable Energy Enterprise DevelopmentCC Climate ChangeCDCF Community Development Carbon FundEATTA East African Tea Trade AssociationERB Energy Regulatory BoardERT Energy for Rural TransformationESCO Energy Service CompanyEUEI European Union Energy Initiative for Poverty Reduction and

Sustainable DevelopmentGEF Global Environment FacilityGEF-KAM Global Environment Facility – Kenya Association of

ManufacturersGHG Greenhouse GasGWh Giga Watt HourGTZ German Agency for Technical CooperationIBRD International Bank for Reconstruction and DevelopmentIPP Independent Power ProducersKPLC Kenya Power & Lighting CompanyKTDA Kenya Tea Development AuthoritykW Kilo WattMHP Mini Hydro ProjectUNFCC United Nations Framework Convention on Climate ChangeUNEP United Nations Environment ProgrammeMOU Memorandum Of UnderstandingMW Mega WattMWH Mega Watt HourNEPAD New Partnership for Africa’s New DevelopmentO.P Operational ProgrammePMO Project Management OfficePV PhotovoltaicsREEEP Renewable Energy and Energy Efficiency PartnershipSADC South African Development CommunitySC Steering CommitteeSTAP Scientific &Technical Advisory PannelTANESCO Tanzania Electrical Servic4e CompanyUNDP United Nations Development ProgrammeUNIDO United Nations Industry development OrganisationZESCO Zambia Electric Service Company

4

PART 1 – PROJECT CONCEPT

A – SUMMARY

Many Eastern and Southern African countries (Ethiopia, Burundi, Kenya, Malawi, Mozambique, Rwanda, Tanzania, Uganda, Zambia, and Zimbabwe) produce tea in bulk for export, generating crucial foreign earnings. Foreign earnings are the ultimate productive use of energy allowing tea communities to become economically strong. The basic processing of tealeaves undertaken at the tea factories requires significant amounts of electrical energy. Currently, in most factories the electrical energy is sourced from, often unreliable, national grids or inefficient and highly polluting and greenhouse gas emitting diesel gensets. Since the tea areas are often remote areas and voltage on the grid may drop causing damage to equipment and preventing the use of some voltage sensitive equipment like compact fluorescent lights. Drought prone countries including most of these have had drought induced power rationing in recent years. Most of these countries have inefficient transmission and distribution systems, high demand and low generation capacities resulting in frequent load shedding. All tea factories have generator sets that are on average in operation for up to 5 % of (factory operation) time. The fuel budgets of tea factories are dependent on increasing international oil prices with negative implications on the competitiveness of the tea produce at the world market.

It appears that whenever tea is grown, the rainfall and hilly terrain guarantee that there will be a hydro potential somewhere near the tea processing plant. In some cases this potential is already used, but in most cases the tea manufacturers rely on the grid and some diesel gen-sets for back up purposes. Since few tea factories have taken up small hydro, a project is proposed to systematically remove barriers regionally (see discussion on barriers in subsequent section).

The umbrella organization engaging in the entire Tea Sector in all countries mentioned is the East African Tea Trade Association (EATTA). EATTA is the proponent of the proposal, as well as the initiator and facilitator of the project. Through its network, it shall be instrumental in liaison with national tea agencies and individual tea factories, support overall data collection, and provide support to consultative workshops and training sessions in various countries.

Through a number of (pre) feasibility studies, some six pilot mini-hydro projects are to be developed, preferably with a rural community electrification component piggy-backed to the mini-hydro project development. All stages of such a project development (pre-feasibility, feasibility including detailed design, tendering, actual construction and commissioning, operation and maintenance) will form a solid training ground for tea sector engineers as well as civil engineers from national consulting/engineering firms. Hands-on training should build sufficient technical capacity that will enable the realization of future mini-hydro systems tapping local expertise. Socioeconomic impacts and environmental assessments would be included at feasibility and completion stages.

In addition the project aims to accelerate the shift from grid and diesel gensets to hydro through the creation of special financing window for tea manufacturers with conducive terms

5

and conditions offered to all EATTA member countries, in order to provide a long lasting incentive for such a shift.

This initiative aims to improve both energy supply security and lower tea production costs by reducing dependency on fossil fuels, consumed by generator sets, and shifting from grid power to hydropower generated in close proximity to the tea factories. The project will have the global environmental benefit of reducing Greenhouse Gas (GHG) emissions and contribute to poverty alleviation through employment and local productive uses. The specific objectives are to: facilitate generation of electricity from decentralized hydropower; improve the reliability and quality of energy service to the tea factories and hence lower factory production costs; while providing access of electricity to households and public and community facilities within close proximity to the tea factories. The benefit to the utilities will be grid reinforcement and reduce any fossil fuel generated electricity in the main grid. The concept is to blend a commercial activity (tea processing) and its energy requirements with the social and developmental dimension of rural electrification in a sustainable manner.

B – COUNTRY OWNERSHIP

1. COUNTRY ELIGIBILITYAs per requisite all of the participating countries (EATTA members) have to be a signatory to the United Nations Framework Convention on Climate Change (UNFCCC). All countries considered have signed and ratified the convention. A summary is provided in Table 01.

Table 01: UNFCCC RatificationsCountry Date Of Signature Date Of RatificationEthiopia 10 June 1992 05 April 1994Kenya 12 June 1992 30/August 1994Tanzania 12 June 1992 17 April 1996Uganda 13 June 1992 08 September 1993Malawi 10 June 1992 21 April 1994Zimbabwe 12 June 1992 03 November 1992Rwanda 10 June 1992 18 August 1995Zambia 11 June 1992 28 May 1993Mozambique 12 June 1992 25 August 1995Burundi 11 June 1992 06 January 1997

2. COUNTRY DRIVEN-NESS

During the conceptual stage of project formulation, a discussion was held between UNEP and the Board of the EATTA (see Appendix C – mission report and Appendix D – minutes EATTA Board). The Board expressed keen interest and decided to support and facilitate data collection during the stage of project formulation.

Over the last 10 years, structural power sector reforms were implemented in the region. Independent power producers are now able to officially generate power (see Table 02). However, it appears that in general the tariffs offered for electric power by third parties does not provide much of an incentive. A more conducive climate for power development starts with a tariff structure.

6

Today, tariff related issues form an obstacle for Independent Power Producers (IPP) to supply (excess) electric power to the grid. Rates for the transfer of electric power, acceptable to both the utility and the (third party) power generator are a pre-requisite for future development of IPPs. An alternative would be that individual companies (tea factories or IPPs) in cooperation with local community organisations both generate and distribute power to nearby residents and communities. This last approach would entail concession licensing, different tariffication and revenue collection by the IPP.

Table 02: Status of Power Sector ReformStatus of Power Reform SectorReform Policy

New/Amended Electricity Act

Regulation Agency

Licenses Issued

Access to Grid Granted

Private Sector Participation

Ethiopia Implemented Implemented Implemented No No PendingKenya Implemented Implemented Implemented Implemented Implemented ImplementedMalawi Implemented Implemented Implemented Implemented Implemented PendingMozambique Implemented Implemented Pending Pending Implemented PendingTanzania Implemented Pending Pending Implemented No ImplementedUganda Implemented Implemented Implemented Pending Pending ImplementedZambia Implemented Implemented Implemented Implemented Implemented ImplementedZimbabwe Implemented Pending Pending Pending Pending PendingBurundi No No No No No NoRwanda Implemented Pending Implemented Pending Pending Pending

Energy policies in all EATTA member states were reviewed for their commitment to the development of mini hydro and private sector involvement:

Ethiopia:

Energy Policy of the Transitional Government of Ethiopia (2004) states the following paragraphs in support of the development of small hydro projects:

4.7.1 To ensure the compatibility of energy resources developed and utilization with ecological and environmentally sound policies.

4.10. To create conducive environment for the participation of the private sector in the development of energy sources.

5.0 Priority of the Policy: 5.1 High priority of hydro-power resource development as hydrological resources are one

of Ethiopia’s most abundant and energy forms.5.3.1 To pay due and close attention to ecological and environmental issues during the

development of energy projects.

Burundi: In the national communication for UNFCCC, Burundi states it has decided to take 3 potential options to reduce GHG:

1) Increase access rate to modern energy such as hydro electricity and renewable energy;2) Supply of energy of sufficient quality and quantity for industry and cottage industry

while improving the supply security for both electricity and petrol products;3) Meeting domestic requirements while safeguarding the environment.

7

To attain these objectives, the government will rehabilitate and extend the existing electricity network, plan hydropower plants and promote technologies that save wood fuel as well as promote renewable energy. The biggest constraint is the lack of finance for the sector’s program. The government will adopt measures to reduce the cost of certain equipment to provide greater access to industries and households.

Furthermore the national communications talk about increasing energy efficiency in the manufacturing industry and energy efficiency (thermal power) in breweries and tea processing plants in order to reduce consumption of fossil fuel and biomass.

For decentralized electrification of public infrastructure both solar PV and small (“pico”) hydropower plants are envisioned, as this will contribute to a reduction in GHG emissions.

Kenya:

The Draft National Energy Policy of 2004 is clear on encouraging mini hydro and private sector involvement:

6.4 Rural Energy: The government will encourage and promote private sector initiatives in entering the renewable energy market. The government recognizes the side of development partners in finding specific programs and will continue to seek their support especially in areas less attractive to the private sector. Furthermore the government will allocate resources to complement self-help groups and private sector efforts in rural energy supplies.

6.5.2 Fiscal policies: The government in recognition of the need to lower the electricity tariffs will grant a 15 year income tax holiday for hydroelectric projects whose installed capacity will not be less than 50 MW; 10 years for projects between 20 MW and 7 years for those below 20 MW but not less than 1 MW. (Note: the project obvious has a task in the formulation of incentives for small-scale power generation, or lumping together a number of mini hydro in one project). For the rest 6.5.2 specifies the duty and tax-free procurement of plant, equipment and related accessories for generation and transmission; exempt public electricity supplies from income tax (up to a certain extent). Tax holiday system is to be reviewed in a new Energy Policy.

6.7 Legal and Regulatory framework: Specifies ERB to license electric power producers with ERB as a one stop office for facilitating permits and licenses; enabling renewable energy systems and not exceeding 3 MW to operate in any area without license irrespective of any other existing distribution license. The National Energy Policy would make it mandatory for a licensed public electricity supplier operating in an area where power generation is being undertaken by parties other than those with agreements or arrangements with such public electricity suppliers to buy such power on terms approved by ERB (note: obviously the project will have a role to play in discussions with ERB).

Note (March 2005): The newly published Sessional Paper on Energy spells and Kenya’s new energy policies: Whereas before the limit was set at 1mw (and obligatory hybrid-a reflection of a national lack of confidence is renewable energy technologies), the new threshold is set as a ceiling of 3MW and below (and not hybrid) for power generation that has no large needs to be licensed by the Ministry of Energy. Provided tariffs are approved by the Energy Regulatory Board, Large power producers can now access customers directly. For hydro projects clearing from the water authority and environmental Management Agency (Environmental Impact

8

assessment and regular audits) remain compulsory. Environmental safety Standards for transmission are under preparation wheres before it was required to follow KPLC prudent practices, now a new grid code allows for independent mini grids.

6.14.2 Other Renewables: The government recognizes that most of the renewable energy sources; solar, wind, small hydros, co-generation, biogas and municipal waste energy have potential for the creation of opportunities and employment generation. In order to encourage private sector participation in harnessing these sources of energy the government will therefore pursue the following policy strategies: Collection of hydrological data and undertaking of pre-feasibility and feasibility studies

on small hydro; Packaging and dissemination of information on renewable energy systems to create

investor and consumer awareness and community based pilot projects; Review of Electric Power Act 1997 to facilitate rural electrification base don supply on a

limited scale using renewable energy technologies; Allowing duty free importation of renewable energy hardware as to promote widespread

usage; Provision of tax incentive to both users and producers of renewable energy technologies

and related accessories based on the degree of maturity and market presentation; Encouraging financial institutions to provide credit facilities for up to a maximum period

of 7 years to consumers and entrepreneurs through fiscal incentives; Enforcing protection of the catchment areas.

Malawi:

The White Paper on Energy Policy for Malawi – 2001 mentions the following:

2.2.2 Specific Policy Goals: Create an enabling environment for investment, private enterprise, competition and operational efficiency with minimum adverse effects on wealth and environment; Promote wide spread efficient use of suitable at affordable new and renewable energy

among rural, per-urban and urban population.

Being aware that past rural electrification efforts were inadequate, the government now is (3.1.6) “ committed to providing and supporting rural electrification as a means of poverty reduction and will intensify public sector investment to accelerate electrification activities in rural and peri-urban areas,” while “ensuring the establishment of a dedicated funding mechanism and establishing an appropriate regulatory and legal framework to support arrangements for rural electrification.”

In 3.3.4. the Government of Malawi pledged to “increase access to and efficient use of sustainable new and renewable energy among the Malawi population,” and make sure that (3.4.1) “ duties and taxes on renewable are not re-introduced”. In addition the government will “ensure appropriate financing mechanisms and credit schemes using existing financial institutions.”

Mozambique:

The Renewable Energy sub-sector in Mozambique is rather new. The overall energy policy strategy aims to create “a proper viable climate in order to attract all stakeholders and key

9

players that could promote the renewable sub-sector”. There exists some ideas to start work in mini and micro hydro but there is a general lack of information on such systems and the related costs. Source: Transcript of presentation of Regional REEEP meeting, Southern Africa July 20-22, 2003, Johannesberg.

Rwanda:

The Enhanced Structural Adjustment Facility Policy Framework makes mention of Rwanda’s priorities in the energy sector:

The objective of the government in the energy sector are to expand and diversify energy supplies at competitive costs, promote the efficient utilization of Rwanda’s energy resources, and minimize the potential adverse environmental impacts. The immediate priorities in the energy sector are to (i) rehabilitate key power facilities; (ii) restructure and privatize the part of ELECTROGAZ that supplies and distributes electricity and gas so as to improve its operational efficiency; (iii) build capacity for policy development and investment planning in key sub-sectors such as gas, hydropower, petroleum products, rural electrification, and (iv) promote the regeneration of forest resources damaged during the emergencies in the country.

The government is preparing a strategic and regulatory framework to address both urban and rural energy needs and to encourage private sector energy provision and distribution. This strategy will emphasize the efficient use of sustainable energy sources based on natural resources.

Tanzania:

Tanzania recently revised the national energy policy to accommodate power sector reforms, promote renewables and advance rural electrification. Under the power sector-restructuring program, independent power producers can generate power and sell to TANESCO. An important strategic objective in the national policy is to reduce fossil fuel dependency through increased use of renewables and improving energy efficiency. Some renewable energy and rural electrification projects have been implemented with assistance from various agencies. However most of the past efforts have been targeted at households and not at the rural industrial sector.

The National Energy Policy, 2003: The government of Tanzania is aware that renewable energy resources so far have remained under utilized (1.1.2. Energy situation) while “electricity needs to be made available for economic activities in rural areas, rural townships and commercial centers. Rural electrification is therefore a case of long-term national interest and a pre-requisite for a balanced social economic growth for all in Tanzania”.

Policy Statement 35: Introduce appropriate rural energy development, financial, legal, and administrative institutions.Policy Statement 36: Establish norms, codes of practice, guidelines and standards for renewable energy technologies, to facilitate the creation of an enabling environment for sustainable development of renewable energy sources. Policy Statement 38: Ensure inclusion of environmental considerations in all renewable energy planning and implementation and enhance co-generation with other relevant stakeholders.Policy Statement 39: Support research and development of renewable energy technologies.

10

Policy Statement 43: Support research and development of rural energyPolicy Statement 45: Promote entrepreneurship and private initiatives in the production and marketing of products and services for rural and renewable energyPolicy Statement 46: Ensure continued electrification of rural economic centers and make electricity accessible and affordable to low income customers.Policy statement 47: Facilitate increased availability of energy services including grid and non- grid electrification to rural areas.

Uganda:

The Energy Policy for Uganda (2002) states that: Realizing (in 1.2.4) that the Uganda is endowed with a variety of renewable energy sources that include hydrological resources “ with only a meager fraction of the country’s renewable energy potential being exploited, Uganda aims to develop the use of renewable energy resources for both single and large scale applications”. In 4.2.3: The Government has spelled out a number of strategies ranging from dissemination of technologies, including renewables in school curriculum, setting of standards, facilitating financing schemes, etc.

Zambia:

The National Energy Policy of 1994 of Zambia mentions: 1.3.5 Mini hydro is identified as one of the renewable energy resources that is greatly under utilized.2.6 New and renewable sources of energy:

2.6.1 Promote NRSE technological development2.6.2 Promote wider application of NRSE technologies 2.6.3 Promote information dissemination2.6.4 Promote education and training

Zimbabwe:

AFREPREN Occasional Paper 20: Zimbabwe’s Policy on Energy Services for the Urban Poor – Proceedings of a National Policy Workshop: There is a “Renewable” Sector in the Department of Energy that is to facilitate renewable energy policies, strategies and action plans, promote renewable energy technologies, coordinate actions, disseminate projects. The draft energy policy has tried to address that the “economically viable new and renewable sources of energy technologies are to be encouraged and promoted. Support (initiation, coordination and monitoring) is given to research efforts in order to establish the viability of NRSE technologies. The strategy regarding NRSE is to identify appropriate alternative energy technologies and sources and to promote the commercialization of viable technologies”. The policy also highlights the removal of import duties and other taxes to reduce investment cost of NRSE technologies.

C – PROGRAM AND POLICY CONFORMITY

1. PROGRAM DESIGNATION AND CONFORMITY

Hydro projects in general support the global environmental objective of reduction of GHG emissions by replacing current or planned thermal power generation.

11

Operational Program O.P.6: “Promoting the Adoption of Renewable Energy by Removing Barriers and Reducing Implementation Costs”.

The central activity is the promotion of mini hydro to meet electric power needs of the energy-hungry tea processing plants.

However, it is inconceivable to use the current and actual power consumption of a tea factory as a given fact in the subsequent dimensioning of a (renewable) power supply system: that will have to start with a proper energy audit determining what potential there is for energy saving (equipment and staggering of production processes). Only after that a proper power supply design can be made. Therefore, also O.P. 5 “Removing barriers to energy conservation and energy efficiency” is directly relevant to the proposed project.

Strategic Priorities:

Promoting the research to invest in mini hyro to meet its captive power needs, and promoting the use of excess hydro potential for rural electrification are classified under SP-3: “Power Sector Policy Framework Supportive of Renewable Energy and Energy Efficiency”

In addition, introducing mini-hydro to sustain the power requirements of tea processing plants is conform SP 1:

“The Transformation of Markets for High Volume Products”.

The proposed utilization of hydropower in every particular project would directly lead to income generation with the tea factories productively using the renewable energy sources (SP 4 –“productive uses of renewable energy”).

2. PROJECT DESIGN

2 A) Background and Context Fresh tealeaves are processed in tea processing plants. This process requires substantial amounts of both electric power (for lighting, cutting, transport, sieving, etc.) and thermal power (for drying). Tea factories in the entire region have persistently faced problems with the supply reliability as well as the cost of electric power while the fluctuating cost of fossil fuel oil for back-up generator sets and boilers/furnaces may spell the difference between a year of profit or loss. For African tea to remain competitive on the world market, cost cutting in the production and processing is necessary. From the perspective of the Global Environment Facility the interest in addressing the concern of the tea sector basically has an environmental dimension: The processing of the tealeaves requires enormous amounts of both electrical and thermal power. Thermal power, in large amounts is needed in the ovens. The sea fermentation process is stopped instantly by injecting the relatively humid curled tea leaves in a high temperature oven where it is flash dried. This process required large bailers. To a large extent power for tea processing is sourced from (imported) fossil fuels (diesel, furnace oil) or the grid while in many cases alternative (renewable and therefore less polluting) sources can be found nearby. Small hydro-power (in terms of both price and performance) will be competitive with more conventional power supply options. Typically the tea factory might enjoy a low bulk tariff, and suffer early disconnection in case of grid weakness. Diesel backup electricity could easily be triple the cost of small hydro with relatively low capital cost but high fuel cost

12

(including transport). A more rational generation of power with overall lowest cost would be local small hydro production to reinforce the main grid and eliminate the diesel consumption. Since the small hydro cannot “save” the main grid, control systems should be installed to isolate the minigrid in case of main grid failure. Using renewable energy sources in meeting the energy requirements of tea plants may be a new and attractive selling point to Western markets giving an entire new meaning to the word “green” tea.

However a number of obstacles obstructing the massive introduction of these environmentally friendly options do exist:

Financial Weakness: The recent surge of world energy prices certainly must provide extra motivation to shift away from fossil fuel but at the very instant such sudden high prices only weaken the overall performance of every tea factory. To date no financial incentives are available that would make the choice for a future power supply any easier;

Captive Power Generation Awareness: To date most factories rely for the bulk of their electric power requirements on the (national) utility. Expensive generator sets are commonly used for back-up services only. The concept of generating your own base load is generally relatively new in the region. In addition and varying per country, there may exist legal obstacles to captive power generation (especially when actual generation occurs outside the tea factory, utilizing national /natural resources such as water in rivers:

Lack of Technical Capacity: Technical expertise in the development of small-scale (mini) hydro projects is short throughout the region. Support is needed in the entire process of a proper feasibility study that (has to) include topographic and soil surveys as well as a detailed engineering design and costing. Although some achievements of the metal sector of the region should not be ignored, actual manufacturing capability for mini hydro equipment (ranging from 100-1000 kW) are non-existent. The proposed project aims to address all the aforementioned obstacles through the creation of a special financing window, provide technical assistance to actual projects while building technical capacities hands-on, promote and facilitate captive power generation (and local distribution, if feasible) and disseminate experiences with small scale hydro in the region and beyond. The proposed project would promote clear prospects for the development of a local manufacturing industry for a number of electro mechanical system components in the mini hydro sector. Such local manufacturing capabilities would facilitate the development of additional (e.g. community-based) decentralized power generation projects in the region.

Policy Framework issues: The sale of relatively small quantities of bulk power or the option of creating a ESCO that generates and sells power to tea factories and local communities; tea factories distributing electric power to nearby communities; securing water rights that will prevent water extraction upstream (e.g. for irrigation purposes) are all issues that need to be addressed prior and during actual project implementation.

Hydro Electric Power

The correlation between tea plantations and hydro potential (in Africa) has been briefly explored during the period of writing the concept. Simply because of availability of data, the situation in Kenya was analyzed. Rainfall data were superimposed on a map of the Kenya tea plantations. Clearly tea is grown in those areas with the highest yearly precipitation. In Central Kenya, this rainfall is caused by orographic lifting caused by coastal air being forced to higher altitudes by Mount Kenya and the Aberdares Range. Tea is grown in areas with modest temperatures; both heat and cold (frost) would prohibit tea growing. Both flat (low) areas and

13

high altitudes have temperature extremes. In addition, the presence of water (water has a relatively high heat capacity) has a strong moderating effect on local temperatures. In short, the hilly and mountainous areas of Kenya are rather wet, thus providing the right conditions for tea growing as well as sufficient water to assure local hydro potential. This observation appears to be holding true for most tea growing areas in the Eastern Africa region, possibly with a small exception for tea growing at rather flat areas of Tanzania.

Not surprisingly considering the logistics involved, tea factories are always near tea growing areas. It follows that where there are tea factories, there must be also a hydro potential. Only a few private tea plantations/factories in the region have installed any hydro equipment to meet their private power needs. The proposed project study aims to identify hydro potential near all tea factories in the region. Such micro hydro plants with sizes between 300 kW and 1 MW should and could first of all meet the power needs of these tea factories in an environmentally friendly way.

The tea factories typically cover areas with 2-5 km radii from the processing plant. Clusters of tea factories with each factory no more than some 5-6 km from the next can be identified in various tea growing areas. In order to increase power supply security, such clusters of mini hydro plants could be interconnected. A cluster development of mini hydros may have another positive impact: Because of the number of power plants involved, design, mobilization of contractors, electro-mechanic equipment and installation, training, stocks of spare parts, etc may all be at reduced costs, thus making a cluster development even more attractive to technology providers and each individual project cheaper. The opposite may also exist. In some areas one particular site may have sufficient hydro potential to connect a number of tea factories. Should potential hydro electricity exceed the electricity requirements of both tea factory and nearby communities, such excess power could be used to even thermal power requirements of tea leave drying.

Thermal Energy

Tea factories either use wood fuel (self grown or purchased) or fossil fuel for heat applications. Solar water heaters could also contribute minimally to the high temperature requirements of the flush drying process. It is roughly estimated that each 4 hectares of tea plantation require approximately 1 hectare of woodlot in order to cover the thermal power requirements of the tea processing plant. Most tea estates appear to have sufficient wood plantations to cover their own needs. On the other hand it appears that KTDA factories, cooperatively owned by small holder tea farmers commonly are faced to meet (part of) their thermal needs by furnace oil. A number of tea factories already have nurseries for seedlings of fast growing tree varieties to be distributed to tea farmers and to be planted on marginal land (e.g. too steep for tea growing). In a number of cases wood fuel production is not adequate to cover the year round thermal energy needs of a factory and possibly sustainable production woodlots may have to be developed in addition. Fast as well as slow growing tree species should be considered in order to assure biodiverse plantations. Depending on the location, and if and when available in considerable and recurrent amounts, other biomass residues (e.g. coffee, sugar industries) can be considered to (partly) meet the thermal power requirements. A small survey conducted in collaboration with EATTA during the time of actual proposal preparation clearly showed that most tea factories do not depend on fossil fuel (furnace oil) to meet their thermal energy requirements. Most factories appear to have their own wood lots as main source, while some purchase wood fuel from tea farmers and/or other sources.

14

Depending on the actual location, houses of tea farmers, but also schools, clinics etc. may or may not yet be electrified. While the tea factory will be the dominant productive use, tea farmers and the communities could diversify their earnings through other activities. Depending on the area, communities just around processing plants have remained unelectrified. It may possibly be an option to use such small hydro plants in addition to cover the demand of the tea factory itself as well as meet residential, social and possibly even commercial demand for electric power in the tea farming area. This will make such a mini hydro1 option commercially, socially and politically a very attractive option.

During the actual phase of project formulation, 3 French experts executed a field mission to a cluster of 7 tea factories managed by the Kenya Tea Development Agency (KTDA). This field mission is part of a pre-feasibility study on small hydro potential for tea factories, a partnership between the previously mentioned KTDA and the French Agency for Energy and Environment (ADEME). Besides the collection of field data (for load forecasts, settlement structures of nearby communities, etc), also the hydro potential was assessed based on surveys, maps and 20 years of river flow data. For 7 tea factories in one single area the demand would roughly amount to 7 x 500 kW = 3.5 MW. The mission returned with an indication that the area could easily produce 10 MW for at least 60 % of the time, with 3 extra sites of 300 –700 kW in reserve. Autonomous power generation for the tea factory is possible in a number of cases. Excess power would indeed be available for rural electrification for power sales for the grid. See appendix F for a short summary of the findings.

Rural Electrification

The status of electrification of communities around tea processing plants appears to be varying per country and per location. Whereas the tea factory may primarily want to consider meeting its industrial power needs, tea farmers and tea factory workers in general will be keen on realizing access to electric power. Especially if the tea factory is cooperatively owned (all the tea factories of the Kenya Tea Development Agency are owned by tea farmers cooperatives) the prime interest of the individual tea farmer may not be the IRR of a small hydro plant but the household connection to electricity. The opportunities of an added electrification compound may lend itself to the establishment of public-private partnerships (tea factory/utility), the creation of an Energy Service Company (ESCO), or a tea factory venturing into power generation and sales (IPP) or even as distribution with a mini-grid to nearby communities. Such an initiative may count on possible external support from new initiatives such as the EUEI (European Union Energy Initiative for Poverty Reduction and Sustainable Development).

Tea and Small Hydro in the EATTA Member States

The “Greening of the Tea Industry in Eastern Africa” concept was brought by EATTA to the attention of its Board during an official Board Meeting on July 31, 2004 (see Appendix C mission report). The EATTA’s official reaction in the minutes of the meeting (see Appendix D, minutes of the EATTA Board Meeting) is that the tea industry would welcome such an initiative.

The situation of both tea production and (potential for) hydro-power generation will be briefly discussed for each of the EATTA member states.

1 The term “mini hydro” is here used for hydro applications with capacities between 100 and 1,000 kW

15

Burundi

Total quantity of made tea in 2003 was 7,400 tons with 5,500 tons sold through Mombassa for export. Increase of production (up to 10,000 tons) and lowering of production costs are seen as the biggest challenges. Today, there are 5 tea factories operating in Burundi. The Office du The Burundi is currently in the process of creating farmers associations.

In 1995 hydro-power provided virtually 100 % of all electric power in Burundi. In 1996 a set of standby diesel units with a capacity of 5.5 MW was installed. In 1997 the country had 43 MW of installed electrical capacity of which 32 MW was installed in hydro-power projects, which is an estimated 10 % of the technically and economically feasible potential. Some 27 small hydro plants (defined as plants up to 1 MW) are currently in operation in Burundi with a total capacity of approximately 3 MW. It is not certain how many of these small schemes are actually in operation today.

Kenya

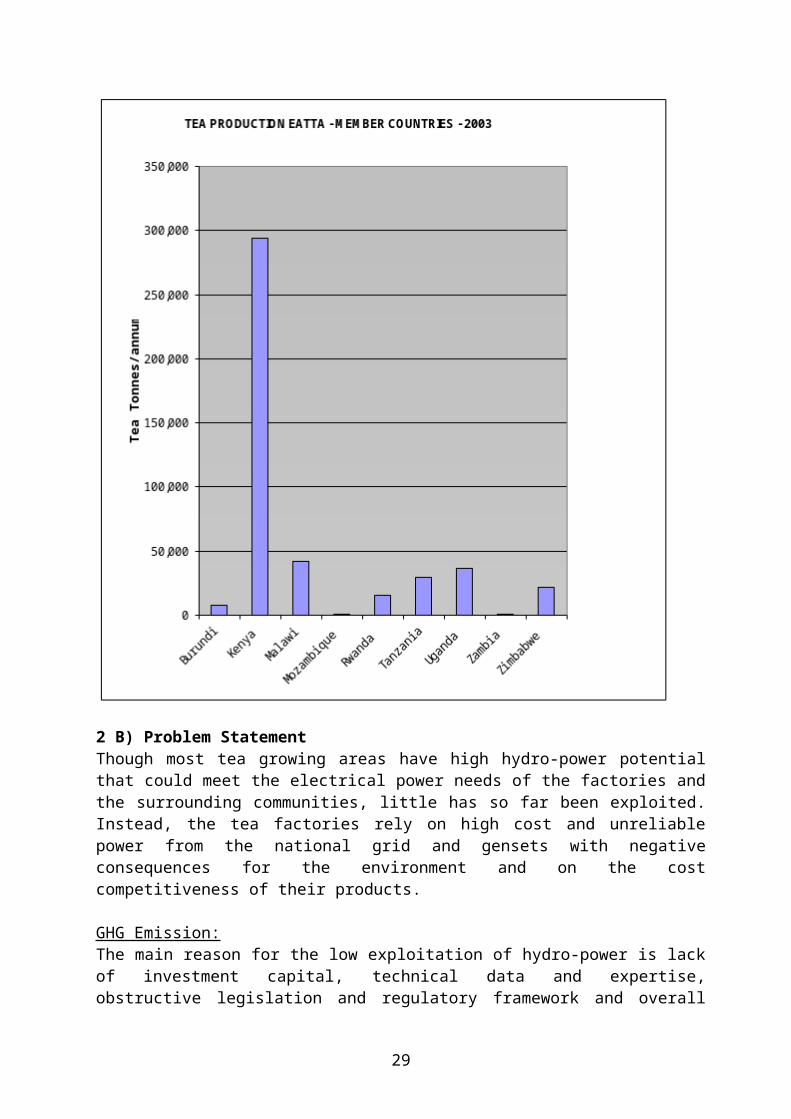

Total tea production in Kenya amounted to 293,632 tons with 217,063 tons sold through the Mombassa auction for export. Kenya has a total number of 95 operational tea factories.

Kenya’s energy policy emphasizes the need for sustainable energy supplies in adequate quantities at effective costs, so as to achieve national development goals. The policy also emphasizes delivery of quality energy services so as to ensure that Kenya will continue to attract investments in those economic activities of which energy inputs are basic to production at competitive prices.Kenya has made significant progress in reflecting electricity tariffs to long run marginal cost, restructuring the power sector, opening the power generation market to private investment, and reforming the sector’s legal and regulatory environment. Specific progress achieved under the reform program includes:

a. Unbundling of power generation, transmission and distribution activities on one hand and incorporation and commercialization on the other hand;

b. Entrance of IPPs;c. Elimination of government subsidies to the sector with possibly the exception of

those to rural electrification;d. Amendment of the Electricity Act which ascended in 1998 to legislate private

sector participation and the establishment of an independent regulator.

Malawi

Total tea production increased in 2003 to 41,965 tons with only 5 % (2,262 tons) sold through the Mombasa Auction. Malawi has all together 23 tea factories

The hydro-power resources of Malawi have not yet been described in detail but the potential of a number of major rivers and sites has been identified. A figure of 6,000 GWh/year of technically feasible potential is cited by the small hydro website. There is some 220 MW of hydro capacity in operation. The total plant capacity of 240 MW is threatened by serious siltation. There is only one 4.5 MW small hydro plant in operation in Wowve. In addition, there is the 600 kW Zomba micro hydro-electric plant.

16

Mozambique

Dry weather conditions, difficulties with the availability of spare parts, transportation and finance restricted the tea output to 1,122 tons with only 788 tons sold through Mombasa.Mozambique has 7 tea factories in operation.

A large hydro capacity is already developed on the Zambezi River (Cahora Bassa) with power exported to neighboring countries. Mini/micro hydro for decentralized electrification is not yet developed.

Rwanda

Total tea production in 2003 was 15,484 tons while 9,457 tons were auctioned through Mombasa. Rwanda’s development of the tea sector is hampered by low quality, inconsistent manufacturing and high transport costs. There are 10 tea factories in Rwanda.

Rwanda has a total hydro electric potential of approximately 100 MW nearly a third of which has been developed at four small hydro electric stations and a number of independent micro-hydro electric stations. Only 5 % of Rwanda’s population has access to the national power grid. One of the main challenges of the new government is to address the crippling power shortage that forced widespread power rationing. The national utility (Electrogaz) is trying to bridge the short fall by using emergency diesel generators, which are slowly coming on line.

Tanzania

In the year 2003/4 Tanzania produced 29,751 tons of tea. A total of 14,571 tons was auctioned through Mombassa. All in all there are 18 tea factories in Tanzania. Access to reliable electricity remains rather poor. Though rural electrification has been pursued since 1961, only about 1% of the rural population has access. While the reform aimed at privatizing TANESCO might improve the overall national electrification situation, it is unlikely to have significant impact on the power situation in tea factories mainly due to the technical limitations of the infrastructure and disperse nature of the factories.

The tea zones are expected to have a sufficient but yet untapped hydroelectric potential.The small hydro potential in Tanzania is said to be attractive. With hydro electric power development estimated to be 3,800 MW of which only roughly 382 MW has been exploited, Tanzania should be open to increased investments in its hydropower sector. Moreover, with large isolated rural communities unable to access the national grid, the government of Tanzania placed rural electrification high on its agenda.

Uganda

The total tea output in 2003 rose slightly to 36,293 tons with the bulk (34,494 tons) sold through Mombassa for export. 27 tea factories are currently operating in Uganda; 3 tea factories (in Masaka) are currently being rehabilitated.

Uganda has developed a rural electrification strategy that aims to increase access to 10 % by 2010. The strategy supports use of renewable energy and provides for subsidies to level the playing field. The country’s electrification level remains rather low with only about 5 % of the

17

total population having access to electricity and less than 1 % of the rural population. Though new generating facilities were installed since 2000, the availability especially in rural areas remains poor. The tea factories rely on a grid that experiences frequent blackouts.

Uganda enacted the electricity act in 1999. This act removed the monopoly power of Uganda Electricity Board allowing for independent generation and hence paving way for the entry of IPPs. In addition an electricity regulatory board has been established. The government is in the process of concessioning, distribution and transmission to increase role of the private sector. A rural electrification fund which will partially subsidize capital investments to facilitate improved access in rural areas has also been established.

The 10-year Energy for Rural Transformation (ERT) project being implemented by the World Bank aims at developing rural energy and information technology so that they make a significant contribution to bringing about rural transformation. Notably emphasis is given to PV though micro-hydro and cogeneration will also be supported. One of the initial Cogen project that has been earmarked for support under the ERT is the Kakira sugar company. The ERT will consider provision of support on case-by-case basis and hence could be a partner for development of micro-hydro at the tea factories.

Zambia

The total production in 2003 amounted to 1,125 tons of tea and 310 tons auctioned through Mombassa for export. There is an effort to increase the area under tea production. Currently, there is only one tea processing plant in Zambia (Kawambwa tea factory). There is no organization/agency representing the tea sector.

Hydro represents 99.8 % of all power produced by the national utility ZESCO, with more capacity available than can be absorbed nationally or exported. UNIDO is currently in the process of developing three sites of micro hydro plants to energize small mini grids for rural development.

Zimbabwe

In the year 2003, total tea production was 21,993 tons with a mere 567 tons sold through the Mombassa auction. Most tea is exported to neighboring countries (Kenya, Botswana, South Africa, Zambia) or locally consumed. Currently there is a serious manpower shortage especially in tea plucking (Mozambican workers returning home because of harsh economic conditions in Zimbabwe). There are 6 tea factories in Zimbabwe. Today only one factory is associated with the EATTA.

The gross theoretical hydro-power potential is 18,500 GWh/year, and the technical potential is estimated at some 17,500 GWh/year. About 19 % of this technically feasible potential has so far been exploited. A small number of mini/micro hydro plants are in operation. The small hydro website mentions three with a total capacity of less than 1 MW.

Summary Tea Production 2003:

Table 03 provides a quick overview of the overall tea production in the region. Purely seen from the point of view numbers of tea factories as well as quantity of tea produced, it is

18

obvious that Kenya is by far the largest producer and has probably the largest associated mini-hydro project potential.

Table 03: Tea Production EATTA – Member Countries

19

2 B) Problem StatementThough most tea growing areas have high hydro-power potential that could meet the electrical power needs of the factories and the surrounding communities, little has so far been exploited. Instead, the tea factories rely on high cost and unreliable power from the national grid and gensets with negative consequences for the environment and on the cost competitiveness of their products.

GHG Emission:The main reason for the low exploitation of hydro-power is lack of investment capital, technical data and expertise, obstructive legislation and regulatory framework and overall awareness of the potential long term benefits. In many cases there is no legal provision for or incentives for distributing power to communities within the environ of a privately owned generating facility. Seen from a National Energy Sector perspective, the shift from grid power to auto-generated hydropower will free capacity that can readily be absorbed for other purposes considering that in all countries rural power consumption is often not met and in all cases is growing. This will

20

everywhere result in the need for additional power plants. Tea factories are always located in rural areas; shifting from grid-based power to hydro will basically avoid or delay the need for additional (fossil fuelled) power plants, thus lowering projected GHG emissions that would otherwise have been produced. In addition, a hydro based power supply that is more reliable than the grid (in terms of both quality and quantity) will reduce the need for back-up generator sets to operate: Already now load shedding is common, forcing the tea factories to start their back-up power supplies (at least some 5 % of all real time, factory owned generators are in operation), and in times of acute power shortages even much more. Such power outages, short as sometimes they may be, occur frequently (2-3 times per day). Shifting back and forth between grid and gen-sets causes financial losses much larger than 5 %. Estimates are that losses of up to 15 % are incurred by unreliable power supply. 2 C) What would happen without GEF? - Baseline scenarioIn the baseline scenario the tea factories will continue to rely on unreliable grid electricity and diesel gensets for electrical power. This will have both local and global implications. Combustion of bunker fuels and operation of diesel gensets generate GHGs. In most countries the overall national generation capacity is lower than demand. Hence continued used grid electricity in tea factories that could potentially use alternative generation sources deprives service provision to the many without access. As such it curtails possibilities for switching from traditional to modern fuels as well as embarking on income generating opportunities: Freeing grid based generation capacity will postpone near-future (fossil based) generation expansion plans.

With the current sharp increase of fossil fuel prices, which eventually will also lead to higher electricity tariffs, it is only logical to expect that tea industries are gradually forced to consider alternative options. The prospect of individual tea factories venturing into mini-hydro without proper technical support is therefore real: Improper analysis of flow data, sub-standard design, civil works, equipment and installations will all lead to rapid disappointment with the technology, effectively preventing any further development.

2 D) What would happen with GEF? - Alternative scenarioThe proposed Mini Hydro Program should support a region-wide shift of tea processing plants away from grid and fossil fuels to Hydro, there where it is both economically justifiable and environmentally benign. Depending on the location of other tea factories in one single area, a cluster development of mini hydro plants might be an option to further reduce costs. Adding a rural electrification component of nearby areas for commercial/social purposes is always worth considering in the case of excess power generation. Power might be available for other purposes after production hours. Periods of high tea leave production (in which double production shifts are necessary -(day & night) will always coincide with periods of high water discharge in rivers (rainy seasons) and (thus) extra available generation potential. Energy efficiency of current operations will always need to be evaluated first in order to come to optimal designs. Converting tea factories to (mainly) operate on hydro should start with a careful analysis of power requirements and actual consumption. In some cases a more staggered production process may reduce (peak) power demand; in other cases the use of more energy efficient electro-motors may substantially reduce daily power consumption. An energy audit in every factory should actually precede any local hydropower initiative and therefore be part of any (pre) feasibility study.

21

In a number of cases, potentially more hydro power can be generated than the tea factory (-ies) will actually need. The primary objective of the tea factory will be to develop sufficient power for its own needs, and at all times. Excess power for rural electrification purposes can be realized by “overdimensioning” the mini hydro plant and taking local commercial, social and residential loads into consideration. Should tariffs for (small scale) power sales to the grid (utility) be acceptable, excess power could also be injected into nearby MV lines. Such rural electrification efforts will quite logically have an impact on the economic and financial feasibility of the proposed projects.

Public Awareness and Climate Change:

Introducing small hydro power plants to meet local energy needs of both tea factory (the majority of the population in these area depend directly or indirectly at the tea sector) as well as all the power requirements will directly instill a sense of responsibility of such communities for the energy source; the local river (flow). The importance of continuous water flow (even against backdrop of possibly reduced rainfall due to climate change) will force both industry and population to preserve or even improve water retention in upstream watershed areas and actively protect such areas.

Objective:

The objective of the proposed Mini Hydro Program is to promote investment in small hydro power through a reduction of the electrical energy costs in the tea processing industries in countries covered by the East African Tea Trade Association and meanwhile increasing power supply for rural electrification as well as power reliability and reducing Greenhouse Gas emissions through removal of barriers related to financial weakness, lack of technical awareness and capacity as well as all obstacles related to power sector policy frameworks.

Specific Objectives:

To provide financial and technical assistance that facilitates the switch from grid-based electricity as main power source to Mini Hydro as locally available alternative;

To facilitate access to electrical power for communities adjacent to tea factories and/or Mini Hydro Plants.

Outcomes:

a. A specific project-oriented financing scheme that encourages mini-hydro development in East Africa is created;

b. Mini hydro projects for tea processing industry in EATTA countries developed and implemented;

c. Technical capabilities concerning design, operation and maintenance of mini-hydro electrical power systems enhanced within the tea sector and civil engineering sector of each participating country.

d. Quality standards for mini hydro design, installation and maintenance and operation have been set for all EATTA countries.

e. Awareness on potential for (mini) hydro as technically viable, economically feasible and environmentally friendly alternative to current (conventional) practices has been raised;

22

f. A regulatory framework for power generation and distribution of (mini-hydro) power has been established in all participating EATTA countries (water rights, generation and distribution licenses and tariffs);

g. Households, commercial and social establishments in unelectrified communities near tea processing plants have been connected to the plants’ mini hydropower supply;

h. Regional increase in local manufacturing of mini-hydro system components;i. One or more models for electric service provision to tea factories (and communities- if

relevant) are established.j. Communities aware of the value of well preserved watershed catchment areas

upstream.

Specific Outputs:

6 Mini hydro demonstration projects established in at least 3 EATTA member countries; preferably with an attached rural-electrification component2;

Partnership between EATTA and UNEP has been established (MOU); Up to 5 extra pre-feasibility studies for promising mini-hydro sites have been prepared; Project financing mechanism established (dedicated financing window for project

development including incentives); EATTA project facilitation skills enhanced & project implementation committee

operational.

Considering the relevance of the tea sector in every EATTA country, it is obvious that the opportunities for replication vary per country.

GHG Emission Reduction:

At this preliminary stage it is not clear what hydro-potential is available, and /or should be developed. It is assumed that on average 500 kW per tea factory shall be installed to meet power requirements of the tea factory and of nearby communities.

For 6 demo-projects: 6 x 500 kW (rate capacity) x 0.6 (assumed load factor, taking non productive nights, low community loads into consideration) x 24 hrs/day x 365 days/annum = 15,768 MWH/annum. Assuming this 6 x 500 kW will now or in the near future replace diesel powered electricity generation, using IPCC emission factor for diesel of 1,019 ton CO2 MWH this would result in a mitigation of some 16,000 tons of CO2. There are all together 150 tea factories in the EATTA region. Should it be possible to develop hydropower installations at a modest 50 tea processing plants of each 500 kW, CO2 emission reductions would amount to 130,000 ton.

In some case the hydro potential might be substantially larger than the demand of the tea factory. Pre feasibility study results for a cluster of tea processing plants in the Aberdares (Kenya) indicate that there might even be more than sufficient power not only to meet power requirements of tea factory and community. In that case, it may even be considered to use (excess) electricity for thermal purposes (tea leave drying), thus substituting furnace oil or wood fuel.

2 Considering volume of tea production and number of tea factories, the potential for mini-hyrdro project replication will be highest in Kenya, Malawi, Tanzania and Uganda. However, technical training workshops and support shall be made available to all EATTA members.

23

3. SUSTAINABILITY (INCLUDING FINANCIAL SUSTAINABILITY)

The power supply systems will be owned by the respective tea factories, as these factories will have directly contributed funds for acquisition. Though support will be provided to such factories through the project, this would only cover the incremental costs of barrier removal. By investing in these systems the tea factories will reduce their energy costs and the savings accrued will be available for system maintenance. In addition the project aims to provide technical training on operation and maintenance to local individuals. Hence these technicians will be available to provide these services beyond the project lifetime. The objective is not to create an engineering /consulting branch within EATTA. By then mini-hydro projects in the tea industry as well as beyond (community based hydro) should have gained sufficient momentum with the technical expertise (and possibly even local manufacturing of system components) available in sufficient amounts.

The productive uses at the tea factories and local diversification activities will provide the revenue stream to achieve financial sustainability. Also a specific financing window for tea based mini hydro projects is envisioned to last for an extended period.

4. REPLICABILITY

Through supporting the establishment of a favorable financing mechanism, the project will enable investments of hydro for all tea factories in EATTA member countries. Given the fact that on of the key barriers is investment finance, availability of this low cost finance will encourage many tea factories to invest in the technology. The project will also establish an awareness raising system within EATTA, which will vigorously and continuously engage with the tea factories and inform them of the financing opportunities as well as the economic and environmental implications of adopting hydro technology. It is expected that the partnership established between UNEP and EATTA would foster into the longer term, beyond the project period and hence UNEP would continue raising awareness within the EATTA and its members and hence facilitate replication.

There are close to 150 tea factories in the East African Region. Based in a preliminary survey most factories appear to be aware of nearby hydro potential. In addition there might be other industries in the small hydro potential areas such as creameries. Using the small hydro for tea processing as an example, other industries may consider shifting to small hydropower. Unmet power demands do exit in all of the unelectrified areas of a country (typically less than 10% of the rural areas in East Africa have remained unelctrified. Assuming the tea industry can provide momentum to mini/micro hydro development in East Africa (resource assessments, project implementation, training, local manufacturing of system (compounds) a spin off might be in the field of community based small hydro for rural development (small industries, domestic, hospitals, schools) thus adding to the overall replicabilty.

5. STAKEHOLDER INVOLVEMENT/ITENDED BENEFICIARIES

The EATTA is the principal proponent and stakeholder especially in the PDF-B project phase. The EATTA board members were informed of the project proposal by its Secretary and their opinion was sought with the aim of providing feedback to UNEP-GEF. As a follow up to these consultations, a draft concept note was circulated by EATTA to its board members and later presented at a board meeting. During the meeting the board members were also individually consulted with the aim of establishing their interest and commitment (see Appendix C, D and

24

H). Detailed information on status of EATTA, management structure and Small Hydro Program Implementation is attached in Appendix L.

Individual tea companies have also been met and the project discussed further. These companies have also presented views and sought clarifications on the project.Not only have EATTA board members explicitly indicated support and interest in the project, but so also several individual tea companies as potential investors

D – FINANCING

1. FINANCING PLANAt this stage of project development it is envisioned that the project aims to realize some 6 mini hydro projects as demonstration projects for tea factories, preferably with a complementary rural electrification scheme (independent mini grid for local distribution or a distribution net owned and operated by a national utility). At this stage, proposed full project budget is indicative only. Duration of the project set at 4 years.

Actual financing shall very much depend on the nature of the mini hydro project:

Table 04:End –Use Financing

Isolated Mini Hydro Tea Factory Tea FactoryTea Factory & Community Tea Factory, Utility, Cooperative, ESCO? Tea

factory as IPP?Grid connected Mini Hydro

Tea Factory Tea Factory

Tea Factory & Community Tea Factory, Utility, Cooperative, ESCO? Tea Factory as IPP?

Sources of finance will likewise vary with the nature of the project: A power supply exclusively for the tea factory may have a relatively high profitability: Financing shall be the main responsibility of the tea factory itself. Should however power be generated for rural electrification purposes, the profitability might be substantially lower while other social and commercial development interests are being served. At this stage (March 05) two parties have indicated strong interest in participation: The African Development Bank: A financing window for Hydro Power in tea industries is to be considered through the private sector window of the AfDB. A rural electrification (through a possible private/public partnership) is of great interest not only to the AfDB but also to the German GTZ in combination with the EUEI (European Union Energy Initiative for Poverty Alleviation and Sustainable Development.

25

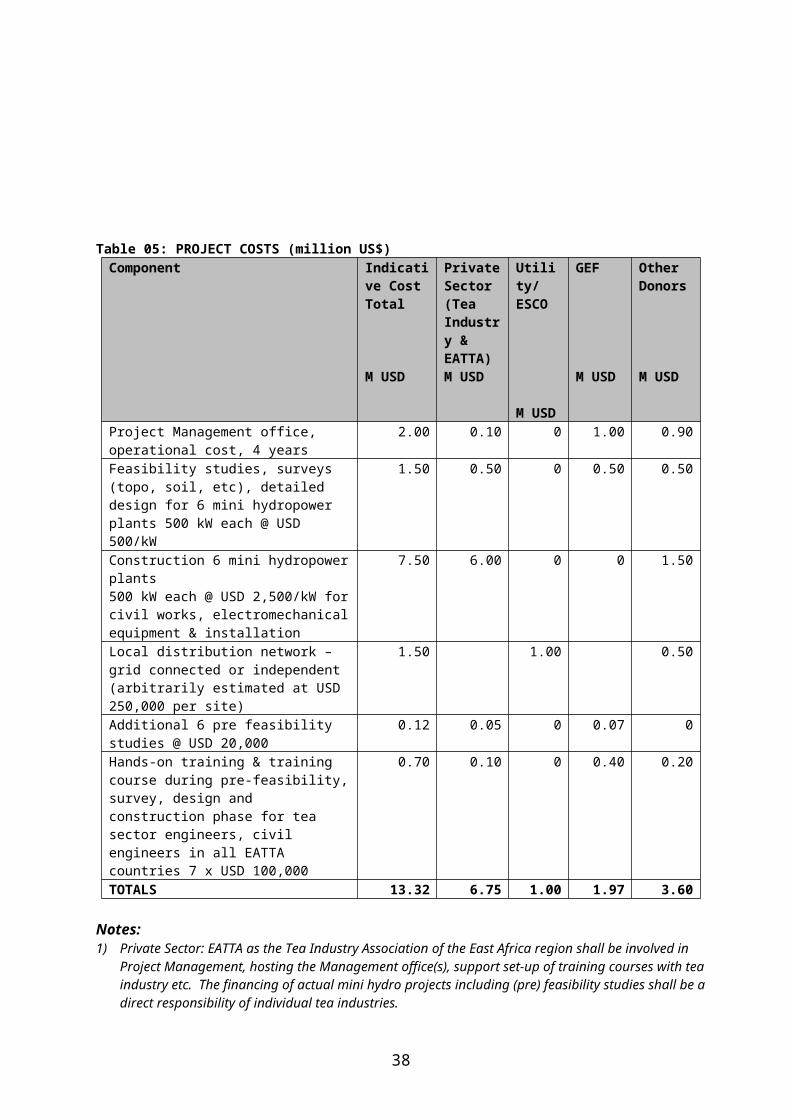

Table 05: PROJECT COSTS (million US$)Component Indicative

Cost Total

M USD

Private Sector (Tea Industry & EATTA)M USD

Utility/ESCO

M USD

GEF

M USD

Other Donors

M USD

Project Management office, operational cost, 4 years

2.00 0.10 0 1.00 0.90

Feasibility studies, surveys (topo, soil, etc), detailed design for 6 mini hydropower plants 500 kW each @ USD 500/kW

1.50 0.50 0 0.50 0.50

Construction 6 mini hydropower plants 500 kW each @ USD 2,500/kW for civil works, electromechanical equipment & installation

7.50 6.00 0 0 1.50

Local distribution network – grid connected or independent (arbitrarily estimated at USD 250,000 per site)

1.50 1.00 0.50

Additional 6 pre feasibility studies @ USD 20,000

0.12 0.05 0 0.07 0

Hands-on training & training course during pre-feasibility, survey, design and construction phase for tea sector engineers, civil engineers in all EATTA countries 7 x USD 100,000

0.70 0.10 0 0.40 0.20

TOTALS 13.32 6.75 1.00 1.97 3.60

Notes:1) Private Sector: EATTA as the Tea Industry Association of the East Africa region shall be involved in Project

Management, hosting the Management office(s), support set-up of training courses with tea industry etc. The financing of actual mini hydro projects including (pre) feasibility studies shall be a direct responsibility of individual tea industries.

2) Utility: Assuming local distribution networks can be financed through intervention from government/utility.3) Other donors: Some other agencies have expressed interest in the concept including ADEME4) Project Management Office manned by both International and national experts/staff. Some experts on part-

time basis. The core team is to manage the project and execute all tasks of the Full Size Project, coordinating all phases of realization of power plants, setting up financing schemes, organization of training courses, etc.

5) Feasibility studies including topo surveys, soil analyses etc, as well as detailed design will serve as hands on training ground for engineers from the tea sector as well as civil engineers. Training courses/workshops will be organized in every country to disseminate experiences, theory, practical solutions etc.

6) Construction of 6 Mini Hydro Plants: The average size has been set at 500 kW per mini hydro plant. For civil works, electro mechanical equipment and installation an amount of USD 2,500 per kW has been reserved.

7) During implementation of the Full Size Project another 6 pre-feasibility studies shall be undertaken for hands-on training purposes, it shall aim to determine whether additional prospects exist for future mini hydro project development.

8) Training courses and Workshops to be organized for Management Staff and Engineers in the Tea Sector and Engineering business should take participants through all stages of a mini hydro project development cycle. Possibly in a number of countries with sufficient industrial base additional workshops/training can be undertaken with the metal manufacturing/engineering sector on local production of mini hydro equipment.

9) Rural Electrification: The rural electrification component is an add-on to te actual commercial hydro power-development for meeting tea factory energy demands. The development of public-private partnerships for rural electrification should generate intrest from various parties. The EUEI may consider active participation in terms of project finance as well as technical support in actual project realization.

26

2. CO-FINANCING Some organizations have expressed interest in participation in this project. The draft proposal shall be used to seek interest and commitment from additional donor organizations.

3 IMPLEMENTATION/EXECUTION ARRANGEMENTS

Program Management Structure

The East Africa Tea Trade Association is based in the port of Mombasa, Kenya. The EATTA operates the Tea Auction of Mombasa for all East African tea. It is engaged in Tea Warehousing and Brokerage. These are its core activities. For a complete overview please refer to appendix G. Members of the EATTA are either engaged in the processing of tea leaves into tea or in the tea trade. Members of EATTA are located in all countries that produce tea in the region: Burundi, Kenya, Malawi, Rwanda, Tanzania, Uganda, Zambia, and Zimbabwe. In some cases individual tea manufacturers are EATTA members, in other cases entire groups or associations are registered as single members. Example: In Kenya, the KTDA – Kenya Tea Development Agency – with 56 tea factories is classified as one single member. The EATTA liaises with various National Authorities on behalf of its members. Up to this day, the EATTA has not (ever) been engaged in any projects that bears any similarity with the proposed “Greening the Tea Industry in East Africa”. It is proposed that UNEP (as Implementing Agency) collaborates with the EATTA (as Executing Agency) in the realization of the proposed tea factory based hydro project. A Steering Committee shall consist of representatives of the tea manufacturers, as represented in the EATTA – Board, but only of those countries that actually will participate in the execution of the Full Size Projects (actual demo project realized).

EATTA shall host a Project Management Office, in which (international) experts shall work on all the tasks defined, creating an enabling environment for mini-hydro development in tea factories, rural electrification, hydro pre-feasibility and feasibility studies including detailed design, training of technical staff in Civil Engineering and Electrical Engineering sector as well as tea factory technical staff and liaise with Ministry of Energy /Industry etc. and national utilities. After the PDF-B a number of tea factories shall be invited for actual demo project mini hydro power plant implementation. In that moment these shall be direct linkages between the EATTA Project Management Office and the individual tea factory. Hands-on training sessions shall be considered with the entire national tea sector as well as civil engineering/electrical engineering sectors (industry associations, consulting/engineering firms etc). The PDF-B experts are invited to design these procedures and linkages in detail.

27

28

E – INSTITUTIONAL COORDINATION AND SUPPORT

1) CORE COMMITMENTS AND LINKAGES

NEPADNEPAD recognizes that energy plays a critical role in the development process, first as a domestic necessity but also as a factor of production whose cost directly affects prices of goods and other services, and the competitiveness of enterprises. In view of the fact that small market sizes and low purchasing power have been the main barriers to universal access to modern energy for development, NEPAD recognizes that the “business as usual” approach will not meet Africa’s energy demand, and adopted a partnership strategy to promote development of the African energy infrastructure. With its aim of addressing Africa-wide electricity problems, this Cogen initiative clearly falls within the NEPAD agenda.

The objectives for the Energy Sector under NEPAD, as stated in the NEPAD document are: To increase Africans’ access to reliable and affordable commercial energy supply from 10

to 35 per cent or more within 20 years; To improve the reliability and lower cost of energy supply to productive activities in order

to enable economic growth of 6 per cent per annum; To rationalize the territorial distribution of existing and unevenly allocated energy

resources; To strive to develop the abundant solar resources; To reverse environmental degradation that is associated with the use of traditional fuels in

rural areas; To exploit and develop the hydropower potential of the river basins of Africa; To integrate and transmission grids and gas pipelines so as to facilitate cross-border energy

flows; To reform and harmonize petroleum regulations and legislation on the continent.

The NEPAD document identifies actions that need to be taken to address these objectives: the establishment of an African Forum for Utility Regulation and regional regulatory associations; the establishment of a task force to recommend priorities and implementation strategies for regional projects, including hydropower generation, transmission grids and gas pipelines; the establishment of a task team to accelerate the development of energy supply to low-income housing; and broadening the scope of the program for biomass energy conservation from the Southern African Development Community (SADC) to the rest of the continent.

NEPAD has drawn up a short-term Action Plan, which identifies its priorities in the Energy Sector. The Summary Action Plan (STAP) provides a wide range of activities, some in more detail, than others. It comprises of 23 energy projects; 7 power systems projects, 3 gas/oil projects, 4 studies, 3 capacity building projects, and 6 facilitation projects. This STAP is being revised and a medium term action plan is being developed. The proposed “Greening the Tea Industry in East Africa” initiative fits within the overall theme of facilitation projects.

GEF Activities in related Sectors:

Table 05 provides an overview of activities that only very randomly will touch on the proposed “Greening of the Tea Industry in Eastern Africa”. This proposed concept is basically to be considered a private sector development with attached to it a rural electrification component wherever relevant and feasible. In addition, excess electricity might be absorbed by national

29

electric power utilities. As such, all private sector reform aspects that deal with the regulatory framework of IPP licensing of power generation and distribution as well as firm/non firm power tariffication are of direct relevance to this project. Technology-wise, as well as implementation-wise, there appears to be no overlap with other existing projects/programs.

Table 07: Relevant GEF related projects in Southern/Eastern Africa (July 2004)Country Project Name Project

TypeImplementing Agency

Approval Date Relevance/Comments

Mozambique Energy Reform and Access Project

Full Size IBRD- The World Bank

Dec 07, 2001 Encourages Renewable Energy Investments in solar, wind, micro hydro and possibly biomass gasification. Phase I to remove barriers. Actually tea hydro projects will fit the objectives.

Zambia Renewable energy-based electricity generations for Isolated mini-grids

Full Size UNEP May 21, 2004 This project is to focus on community based hydro-developments.