Proj of Fm Final

86

1 : Managed by : Gujarat Law Society

Transcript of Proj of Fm Final

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 1/86

1

: Managed by :

Gujarat Law Society

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 2/86

2

Project report on:

Prepared by:- Practical study report on:

Mahindra and Mahindra limited

Prepared by:-

Zinzuwadia charmi c..

S.Y. B.B.A.

Roll no.-320

Submitted To:-

G.L.S. Institute of Business Administrative

´Prof. Swati Modiµ

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 3/86

3

PREFACE

TTr r uuee lleeaar r nniinngg hhaa p p p peennss oouutt oof f eexx p peer r iieennccee aanndd oo b bsseer r vvaattiioonn.. AAnndd f f oor r

mmoor r ee iimm p pr r oovveemmeenntt,, nneeww ttoooollss aanndd tteecchhnniiqquueess hhaavvee b beeeenn ddeevveelloo p peedd ttoo mmeeeett tthhee nneeeeddss oof f mmooddeer r nn b buussiinneessss wwhhiicchh wwoor r k k ss iinn ccoomm p plleexx

eennvviir r oonnmmeenntt.. AAss aa p paar r tt oof f tthhee SS..YY.. BB..BB..AA.. ssyyllllaa b buuss,, p pr r aaccttiiccaall ssttuuddiieess

hheell p p uuss ttoo lliinnk k ccllaassssr r oooomm k k nnoowwlleeddggee wwiitthh p pr r aaccttiiccaall sscceennaar r iioo..

BBuussiinneessss mmaannaaggeemmeenntt iiss aann aaccttiivviittyy iinnvvoollvviinngg p pllaannnniinngg,, ddeecciissiioonn

mmaak k iinngg aanndd mmoosstt iimm p poor r ttaanntt iiss iittss iimm p plleemmeennttaattiioonn tthhr r oouugghh iinntteer r aaccttiioonn

aammoonngg iinnddiivviidduuaallss wwiitthh tthhee hheell p p oof f ddiissccuussssiioonnss aanndd eexxcchhaannggeess oof f iiddeeaass

aanndd eexx p peer r iieenncceess aanndd tthhuuss r r eessuullttss iinnttoo p pr r aaccttiiccaall aa p p p plliiccaattiioonn oof f tthhee aannnnuuaall

r r ee p poor r tt oof f tthhr r eeee ssuucccceessssiivvee yyeeaar r ss wwhhiicchh aar r ee p puutt iinn ttooggeetthheer r iinn aa llooggiiccaall

f f oor r mmaatt..

SSoo ttoo k k nnooww b baassiiccaallllyy hhooww tthhee p pr r oof f eessssiioonnaall mmaannaaggeer r ss wwoor r k k oouutt iinn

iinndduussttr r iieess,, f f iinnaanncciiaall ccoonncceer r nnss ccaann b bee cclleeaar r llyy k k nnoowwnn.. II hhoo p pee tthhiiss p pr r eesseennttaattiioonn wwiillll b bee uusseef f uull ttoo aallll ccoonncceer r nneedd..

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 4/86

4

ACKNOWLEDGEMENT

TThhr r oouugghh tthhiiss aacck k nnoowwlleeddggeemmeenntt,, II eexx p pr r eessss mmyy ggr r aattiittuuddee ttoowwaar r ddss aallll

tthhoossee p peeoo p pllee wwhhoo hheell p peedd mmee iinn p pr r ee p paar r iinngg tthhiiss p pr r oo j jeecctt r r ee p poor r tt wwhhiicchh hhaass

b beeeenn aa ggr r eeaatt lleeaar r nniinngg eexx p peer r iieennccee..

FFiir r sstt oof f aallll II wwoouulldd lliik k ee ttoo tthhaannk k tthhee DDiir r eeccttoor r M M r r . . V V aad d i i B Bhhaai i P P aat t eel l

aanndd ssiinncceer r ee tthhaannk k ss ttoo P P r r oo f f . . S S wwaat t i i M M ood d i i wwhhoo gguuiiddeedd mmee tthhr r oouugghhoouutt tthhee

p pr r oo j jeecctt aanndd aallssoo p pr r oovviiddeedd vvaalluuaa b bllee ssuuggggeessttiioonnss aanndd eennccoouur r aaggeemmeenntt aass

aanndd wwhheenn nneeeeddeedd..

II aamm hheeaar r tt f f uullllyy tthhaannk k f f uull ttoo mmyy ccl l aassssmmaat t eess aannd d mm y y F F aammi i l l y y

mmeemmbbeer r ss wwhhoo wweer r ee ssuu p p p poor r ttiivvee dduur r iinngg tthhee p pr r ee p paar r aattiioonn oof f tthhiiss r r ee p poor r tt..

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 5/86

5

Index1 General information 6

2 Introduction of

company8

3 Introduction of

finanace10

4 Ratio analysis 13

5 Profit &loss a/c 64

6 Balance sheet 65

7 Comparative statement

of p&l a/c66

8 Comparative

statement of balancesheet

68

9 Cash flow 71

10 Director¶s report 72

11 Auditor¶s report 76

12 Conclusion 84

13 Bibilogarphy 85

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 6/86

6

General Information1)Board of directors A.K Nanda

A S Ganguly

Anupam Puri

Deepak S Parekh

M M Murugappan

Nadir B Godrej

Narayanan Vaghul

R K Kulkarni

2)Bankers

Bank of America N.A

Bank of BarodaBank of India

Central Bank

Central Bank of India

HDFC Bank Limited

State Bank of India

Union Bank of India

3)Auditor

Deloitte Haskins & Sells

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 7/86

7

4)Registered Address

Gateway Building,

Apollo Bunder

City:Mumbai

State:Maharashtra

Pincode:400001

Web

Url:http://www.mahindra.com

5)Company Background

Industry Name: Auto - Cars & Jeeps

House Name:M & M Group

Incorporation Date: 02/10/1945

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 8/86

8

A)Introduction of company

The Company was Incorporated and converted into Public Limited in 1955 at

Mumbai. The Company Manufacture Jeep type vehicles, petrol industrial engines,industrial process control instruments and flow meters. Trading in steel and

manufacture of professional grade electronic components.

Jeeps are manufactured under a license and an agreement with Willys Motors Inc.,

Toledo, Ohio, U.S.A., for whom the Company also acts as exclusive distributors

for the whole of India for their entire range of vehicles including utility vans,

cargo/personnel carriers and pick-up trucks.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 9/86

9

B) Brief History& Background

Few groups can identify as closely with India's destiny and

industrial progress as the Mahindra Group. In fact, Mahindra is

like a microcosm of India. Both were born around the same time,

had the same aspirations and both experienced the inevitable

troughs

And crests in the journey towards their goals. And both continue to

march on the path to progress and global recognition.

The birth of Mahindra & Mahindra began when K.C. Mahindra

visited the United States of America as Chairman of the IndiaSupply Mission. He met Barney Roos, inventor of the rugged

'general purpose vehicle' or Jeep and had a flash of inspiration:wouldn't a

vehicle that had proved its invincibility on the battlefields of World

War II be ideal for India's rugged terrain and its kutcha rural roads?

Swift action followed thought. The Mahindra brothers joined hands

with a distinguished gentleman called Ghulam Mohammed. And, onOctober 2

nd, 1945, Mahindra & Mohammed was set up as a franchise

for assembling jeeps from Willys, USA.

Two years later, India became an independent nation and Mahindra

& Mohammed changed its name to Mahindra & Mahindra.

Since then, Mahindra & Mahindra has grown steadily in size and

stature and evolved into a Group that occupies a premier position inalmost all key sectors of the economy. The Group's history is

studded with milestones.

For Mahindra & Mahindra, this translates into many more milestones to

be set up before it rests. If ever.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 10/86

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 11/86

11

Meaning of financial activities:

FFiinnaannccee mmeeaannss mmoonneeyy uusseedd b byy ccoomm p paannyy p pr r oovviiddeedd b byy tthhee

sshhaar r eehhoollddeer r ss oor r b byy llooaannss ii..ee,, iitt iiss aa ssttuuddyy oof f mmoonneeyy mmaannaaggeemmeenntt aanndd

p pr r oovviissiioonn oof f mmoonneeyy wwhheenn iitt iiss r r eeqquuiir r eedd ..

Definition of FinancialManagement:

³³FFiinnaannccee´́ iiss aa wwoor r dd f f r r oomm FFr r eenncchh llaanngguuaaggee.. TThhee mmeeaanniinngg oof f tthhiiss

wwoor r dd iiss eevveer r cchhaannggiinngg.. IInn 1177tthh

cceennttuur r yy tthhee tteer r mm ³³f f iinnaannccee´́ wwaass ccoonnssiiddeer r eedd

aass ³³mmoonneeyylleennddeer r ss´́.. BBuutt nnooww iitt iiss ccoonnssiiddeer r eedd aass ³³f f iinnaanncciiaall

aaddmmiinniissttrraattiioonn´́.. TThhee mmeeaanniinngg aanndd ddeef f iinniittiioonn cchhaannggeess aaccccoor r ddiinngg ttoo cciir r ccuummssttaanncceess..

AAccccoor r ddiinngg ttoo WWhheeeelleerr::

µµFFiinnaanncciiaall MMaannaaggeemmeenntt iiss tthhee b buussiinneessss aaccttiivviittyy wwhhiicchh iiss ccoonncceer r nn

wwiitthh aaccqquuiissiittiioonn aanndd ccoonnsseer r vvaattiioonn oof f ccaa p piittaall f f uunnddss iinn mmeeeettiinngg f f iinnaanncciiaall nneeeeddss aanndd oovveer r aallll oo b b j jeeccttiivveess oof f b buussiinneessss eenntteer r p pr r iissee¶¶..

TThhuuss f f iinnaanncciiaall mmaannaaggeemmeenntt iiss ccoonncceer r nneedd wwiitthh tthhee aaccqquuiissiittiioonn,,

aar r r r aannggeemmeenntt,, iinnvveessttmmeenntt,, ddiissttr r ii b buuttiioonn aanndd ccoonnttr r ooll oovveer r tthhee b buussiinneessss

f f iinnaannccee.. WWhhaatt ssoo eevveer r iiss ddoonnee b byy f f iinnaannccee mmaannaaggeer r iiss k k nnoowwnn aass f f iinnaanncciiaall

mmaannaaggeemmeenntt..

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 12/86

12

A) IMPORTANCE OF FINANCE IN

MODERN WORLD:

WWiitthhoouutt f f iinnaannccee nnoo aaccttiivviittyy iiss p poossssii b bllee.. AAccccoor r ddiinngg ttoo SS..CC..

K K uucchhhhaall ³³MMoonneeyy iiss aa p piivvoott,, aar r oouunndd iitt aallll eeccoonnoommiicc aaccttiivviittiieess aar r ee

cclluusstteer r ́́ .. AAccqquuiissiittiioonn aanndd uuttiilliizzaattiioonn oof f f f iinnaannccee aar r ee tthhee mmaaiinn ccoomm p poonneennttss

oof f f f iinnaanncciiaall mmaannaaggeemmeenntt.. ³³BBuutt uuttiilliizzaattiioonn oof f f f iinnaannccee iinn wwr r oonngg ddiir r eeccttiioonn

wwiillll ddeeccr r eeaassee tthhee p pr r oof f iittaa b biilliittyy aanndd p pr r eessttiiggee oof f uunniitt.. AAnndd eennttiir r ee ssuucccceessss

aanndd p pr r ooggr r eessss oof f b buussiinneessss ddee p peennddss oonn eef f f f eeccttiivvee f f iinnaannccee f f uunnccttiioonnss..

The Importance of finance function can be pointed out as

under:

oo IInn tthhee b buussiinneessss p puur r cchhaassee,, oof f R R aaww mmaatteer r iiaall,, PPllaanntt aanndd MMaacchhiinneer r yy,,

LLaanndd aanndd BBuuiillddiinngg,, b beenneef f iitt oof f sscciieennttiif f iicc p puur r cchhaassee ccaann oonnllyy b bee

oo b bttaaiinneedd oonnllyy iif f f f iinnaannccee f f uunnccttiioonn iiss iiddeeaall..

oo TThhee aaiimm oof f b buussiinneessss iiss ttoo mmaak k ee p pr r oof f iitt p pr r oommootteer r aar r ee aallwwaayyss k k eeee p piinngg

iiddeeaa oof f eexx p paannssiioonn,, f f oor r ggeettttiinngg p pr r oof f iitt..

oo ³³CCuussttoommeerr ssaattiissf f aaccttiioonn iiss oouurr MMoottttoo´́.. IItt iiss ttr r uuee b buutt f f oor r tthhiiss,,

ccuussttoommeer r sseer r vviiccee cceennttr r ee aar r ee r r eeqquuiir r eedd.. IItt iiss vveer r yy cclleeaar r tthhaatt wwiitthhoouutt

f f iinnaannccee f f uunnccttiioonnss tthhee iiddeeaa oof f ccuussttoommeer r sseer r vviiccee cceennttr r ee b beeccoommeess

mmeer r eellyy aa ddr r eeaamm..

TT

hh

uu

ss,,

iinn

b b

uu

ssiinn

eessss,,

f f iinn

aann

ccee

f f uu

nn

ccttiioo

nn

iiss

aann

iimm

p p

oo

r r ttaann

tt

aaccttiivv

iittyy

.

. OOtthheer r aaccttiivviittiieess oof f b buussiinneessss ddee p peenndd oonn f f iinnaanncciiaall mmaatttteer r ss.. TThhaatt iiss

wwhhyy f f iinnaannccee iiss ccoomm p paar r eedd wwiitthh tthhee b blloooodd cciir r ccuullaattiioonn oor r lliif f ee lliinnee oof f

b buussiinneessss aanndd iinndduussttr r yy..

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 13/86

13

4)Ratio analysis

INTRODUCTION

OBJECTIVE:

To understand the information contained in financial statements

with a view to know the strength or weaknesses of the firm and to make

forecast about the future prospects of the firm and thereby enabling the

financial analyst to take different decisions regarding the operations of

the firm.

RATIO ANALYSIS:

Fundamental Analysis has a very broad scope. One aspect looks

at the general (qualitative) factors of a company. The other side

considers tangible and measurable factors (quantitative). This means

crunching and analyzing numbers from the financial statements. If used

in conjunction with other methods, quantitative analysis can produce

excellent results.

MEANING OF RATIO:

A ratio is one figure express in terms of another figure. It is a

mathematical yardstick that measures the relationship two figures, which

are related to each other and mutually interdependent. Ratio is express

by dividing one figure by the other related figure. Thus a ratio is an

expression relating one number to another. It is simply the quotient of two numbers. It can be expressed as a fraction or as a decimal or as a

pure ratio or in absolute figures as ³ so many times´. As accounting ratio

is an expression relating two figures or accounts or two sets of account

heads or group contain in the financial statements.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 14/86

14

ADVANTAGES OF RATIO ANALYSIS

Financial ratios are essentially concerned with the identification of

significant accounting data relationships, which give the decision-maker insights into the financial performance of a company. The advantages of

ratio analysis can be summarized as follows:

Ratios facilitate conducting trend analysis, which is important for

decision

making and forecasting.

Ratio analysis helps in the assessment of the liquidity, operating

efficiency, profitability and solvency of a firm.

Ratio analysis provides a basis for both intra-firm as well as inter-

firm

comparisons.

The comparison of actual ratios with base year ratios or standard ratios helpsthe management analyze the financial performance of the firm

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 15/86

15

LIMITATIONS OF RATIO ANALYSIS

Ratio analysis has its limitations. These limitations are described below:

1] Information problems Ratios require quantitative information for analysis but it is not

decisive about analytical

output .

The figures in a set of accounts are likely to be at least several

months out of

date, and so might not give a proper indication of the company¶s current

financial

position. Where historical cost convention is used, asset valuations in

the balance sheet

could be misleading. Ratios based on this information will not

be very useful for

decision-making.

2]Comparison

of

performance

over

time

When comparing performance over time, there is need to

consider the changes

in price. The movement in performance should be in line with

the changes in

price.

When comparing performance over time, there is need to

consider the changes

in technology. The movement in performance should be in line

with the changes

in technology.

Changes in accounting policy may affect the comparison of

results between different accounting years as misleading.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 16/86

16

When comparing performance over time, there is need to

consider the changes in price. The movement in performance

should be in line with the changes in price.

When comparing performance over time, there is need toconsider the changes in technology. The movement in

performance should be in line with the changes in technology.

Changes in accounting policy may affect the comparison of

results between different accounting years as misleading.

3] Inter-firm comparison

Companies may have different capital structures and to

make comparison of performance when one is all equity

financed and another is a geared company it may not be a good

analysis.

Selective application of government incentives to various

companies may also distort intercompany comparison.

comparing the performance of two enterprises may be

misleading When comparing performance over time, there is need to

consider the changes in price. The movement in performance

should be in line with the changes in price.

When comparing performance over time, there is need to

consider the changes in technology. The movement in

performance should be in line with the changes in technology.

Changes in accounting policy may affect the comparison of results between different accounting years as misleading.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 17/86

17

CCllaassssiif f iiccaattiioonn oof f R R aattiiooss::

AAss p peer r r r eeqquuiir r eemmeenntt oof f vvaar r iioouuss uusseer r ss ((f f oor r ee..gg.. sshhoor r tt tteer r mm ccr r eeddiittoor r ss,,

mmaannaaggeemmeenntt,, iinnvveessttoor r ss)) tthhee r r aattiiooss mmaayy b bee ccllaassssiif f iieedd iinn f f oolllloowwiinngg

ggr r oouu p pss::

PPrroof f iittaabbiilliittyy

R R aattiiooss

LLiiqquuiiddiittyy

R R aattiiooss

LLeevveerraaggee

R R aattiiooss

AAccttiivviittyy R R aattiiooss

GGr r oossss PPr r oof f iitt

R R aattiioo

CCuur r r r eenntt R R aattiiooss DDee b btt EEqquuiittyy

R R aattiioo

SSttoocck k TTuur r nnoovveer r

R R aattiiooss

N Neett PPr r oof f iitt R R aattiioo LLiiqquuiidd R R aattiioo PPr r oo p pr r iieettaar r yy R R aattiioo WWoor r k k iinngg

CCaa p piittaall

TTuur r nnoovveer r R R eettuur r nn oonn sshhaar r ee--

hhoollddeer r ss f f uunndd

CCaa p piittaall GGeeaar r iinngg

R R aattiioo

TToottaall AAsssseettss

TTuur r nnoovveer r

OO p peer r aattiinngg R R aattiioo LLoonngg tteer r mm f f uunnddss

ttoo f f iixxeedd AAsssseettss

BBooook k VVaalluuee PPeer r

SShhaar r ee

EExx p peennsseess R R aattiioo DDee b bttoor r ss R R aattiioo

R R eettuur r nn oonn ccaa p piittaall

eemm p pllooyyeedd

CCr r eeddiittoor r ss R R aattiioo

EEaar r nniinnggss p peer r

sshhaar r ee DDiivviiddeenndd p peer r

sshhaar r ee

PPr r iiccee EEaar r nniinngg

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 18/86

18

PPrroof f iittaabbiilliittyy R R aattiioo ::

aa.. GGrroossss PPrroof f iitt R R aattiioo:: MMeeaanniinngg:: -- TThhiiss r r aattiioo sshhoowwss tthhee r r eellaattiioonnsshhii p p b beettwweeeenn GGr r oossss PPr r oof f iitt aanndd N Neett ssaalleess..

OObb j jeeccttiivvee:: -- TThhee mmaaiinn OO b b j jeeccttiivvee oof f ccoomm p puuttiinngg tthhiiss r r aattiioo iiss ttoo f f iinndd

oouutt tthhee eef f f f iicciieennccyy wwiitthh wwhhiicchh p pr r oodduuccttiioonn oor r p puur r cchhaassee oo p peer r aattiioonn aar r ee

ccaar r r r iieedd oonn..

Components: - There are 2 components of this ratio which are as

under:

Gross profit is the excess of net sales over cost of cost sold

i.e. Net sales (-) cost of goods sold.Cost of goods sold =

Opening stock + Net purchase (purchase ±purchase return)

+ Direct Expenses (purchase related expenses) - Closing

stock.Net sales which is gross sales (both cash and credit)

± Sales return.

CCaallccuullaattiioonn::--

This ratio is calculated by dividing the gross profit by

net sales. It is expressed as percentage. In the form of a

formula this ratio may be expressed as under:

y Formula: -

Gross Profit = Gross Profit * 100

Net Sales

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 19/86

19

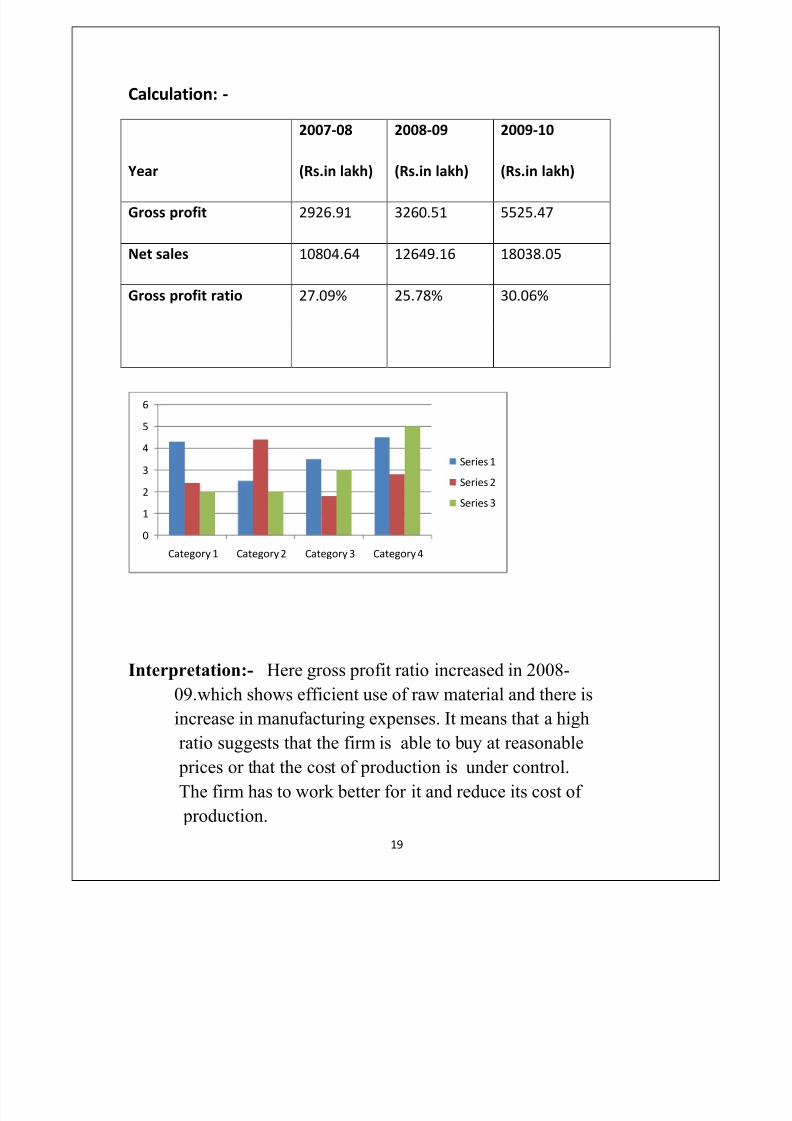

Calculation: -

Year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Gross profit 2926.91 3260.51 5525.47

Net sales 10804.64 12649.16 18038.05

Gross profit ratio 27.09% 25.78% 30.06%

Interpretation:- Here gross profit ratio increased in 2008-

09

.which shows efficient use of raw material and there isincrease in manufacturing expenses. It means that a high

ratio suggests that the firm is able to buy at reasonable

prices or that the cost of production is under control.

The firm has to work better for it and reduce its cost of

production.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 20/86

20

b. Net Profit Ratio: Meaning:-

This ratio measures the relationship between net profit

& net sales.

Objective:-

The main objective of computing this ratio is to find the

overall profitability due to various factors such as

operational efficiency, trading on equity etc.

Components:-

There are two components of this ratio which are as

under:

1. Net Profit

2. Net Sales

Calculation:-

This ratio is calculated by dividing the next profit by net

sales. It is expressed as percentage. In the form of a

formula this ratio may be expressed as under:

Formula: -

Net Profit Ratio = Net Profit * 100

Net Sales

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 21/86

21

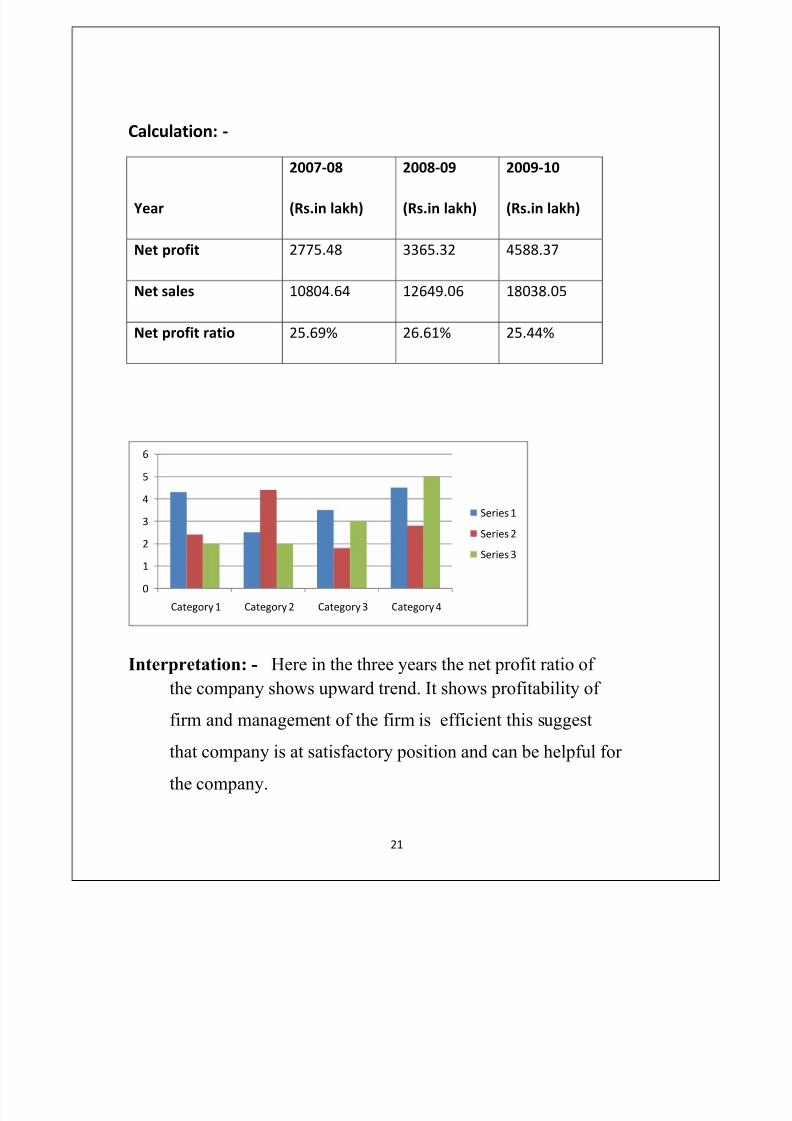

Calculation: -

Year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Net profit 2775.48 3365.32 4588.37

Net sales 10804.64 12649.06 18038.05

Net profit ratio 25.69% 26.61% 25.44%

Interpretation: - Here in the three years the net profit ratio of

the company shows upward trend. It shows profitability of

firm and management of the firm is efficient this suggest

that company is at satisfactory position and can be helpful for

the company.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 22/86

22

c.Return on Shareholder¶s Fund:

Meaning:-

This ratio measures a relationship between net profit after interest, tax and preference dividend and equity shareholder¶s

funds.

Objective:-

The objective of calculating this ratio is to find out how

efficiently the funds supplies by the equity shareholder¶s have

been used.

Components:-

There are two components of this ratio they are as under:

1. Net Profit after Interest, Tax & Preference dividend

2. Equity Shareholder¶s Fund which means Equity Share Capital +

Reserves & Surplus ± Fictitious Assets

Calculation:-

This ratio is computed by dividing the net profit after interest &

tax and preference dividend by equity shareholder¶s fund. It is

expressed as percentage. In the form of a formula this ratio may

be expressed as under:

Formula: -

Return on Eq. sh. holders fund = Profit after tax *100

Equity share holders fund

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 23/86

23

Calculation:-

Year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Net profit(PAT) 1136.37 836.78 2087.75

Shareholders fund 4332.54 5255.53 7818.76

Returns 26.20% 15.94% 26.69%

Interpretation: -

Return on equity share holder fund was 1136.37%in 2007-08 which

decreased 836.78% and again increased to 2087.75% it indicates that

fund which is provided by the owners have been not used properly by

the firm which can be unsatisfactory for the company in the future.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 24/86

24

c. Operating Ratio: Meaning:-

This ratio measures a relationship between operating cost and

net sales.

Objective:-

The main objective of computing this ratio is to find out the

operating efficiency with which production or purchase &

selling operations are carried on.

Components:-

There are two components of this ratio which are as under:

A. Cost of Goods Sold

B. Other Operating expenses

Ex. Administrative expenses, selling & distribution expenses,

interest on short term loans, discount allowed and bed debts, netsales (Gross Sales ± Sales Return).

Calculation:-

This ratio is calculated by dividing the operating cost by net

sales. This ratio is expressed as percentage. In the form of a

formula this ratio may be expressed as under:

Operating Ratio =

*100

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 25/86

25

Calculation:

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Cogs 7906.04 9463.68 12529.20

Operating exp 2296.97 2612.49 3134.29

Net sales 10804.64 12649.06 18038.05

Operating ratio 94.43% 95.47% 86.84%

Interpretation:-

This ratio indicates an average operating cost incurred on sales

of goods worth rs. 100. Lower the ratio, greater is the operating

profit to cover the operating expense to pay dividend and to

create reserves & vice-versa.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 26/86

26

d. Expenses Ratio: Meaning:-

This ratio measures the relationship between different types of

ratio with expenses & net sales.

Objective:-

The main objective of computing different types of expenses the

incurrence of different types of expenses.

Components:-

There are two components of this ratio which are as under:

1. Different type of expenses

2. Net Sales

Calculation:-

This ratio is calculated by dividing different types of expenses

by the net sales. This ratio is expressed as a percentage. In the

form of a formula this ratio may be expressed as under:

Expense Ratio =

×100

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 27/86

27

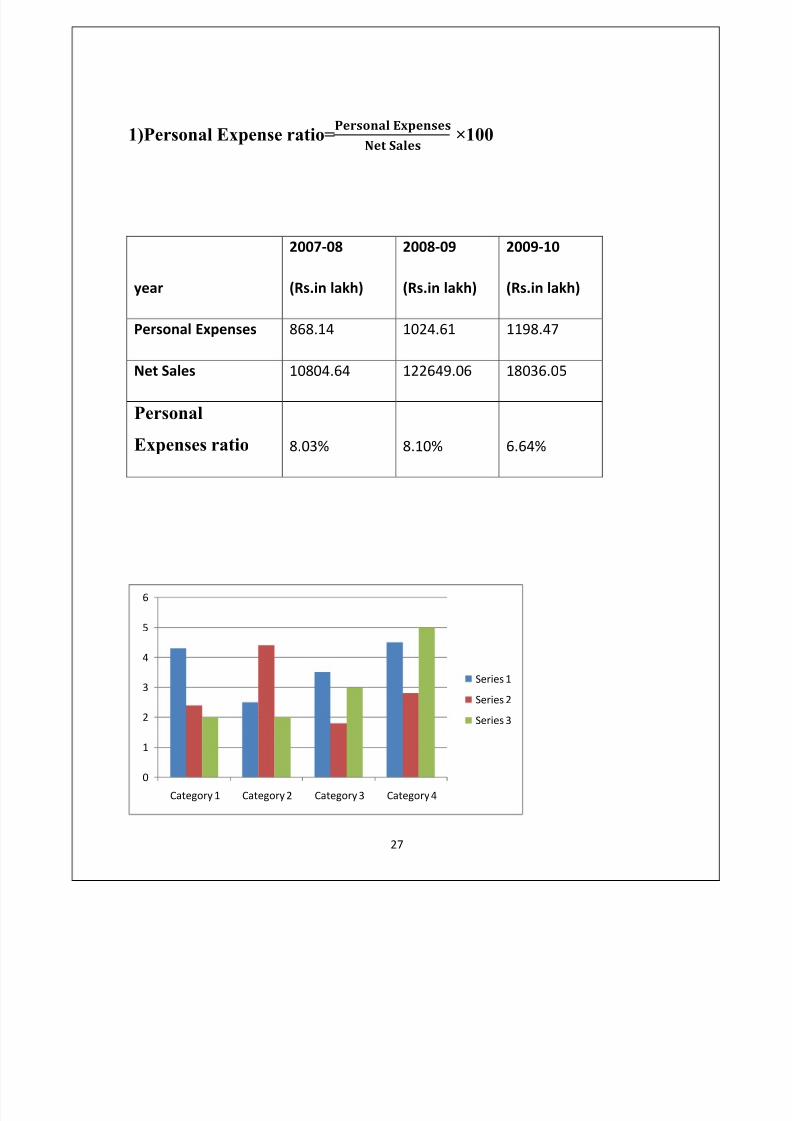

1)Personal Expense ratio=

×100

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Personal Expenses 868.14 1024.61 1198.47

Net Sales 10804.64 122649.06 18036.05

Personal

Expenses ratio 8.03% 8.10% 6.64%

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 28/86

28

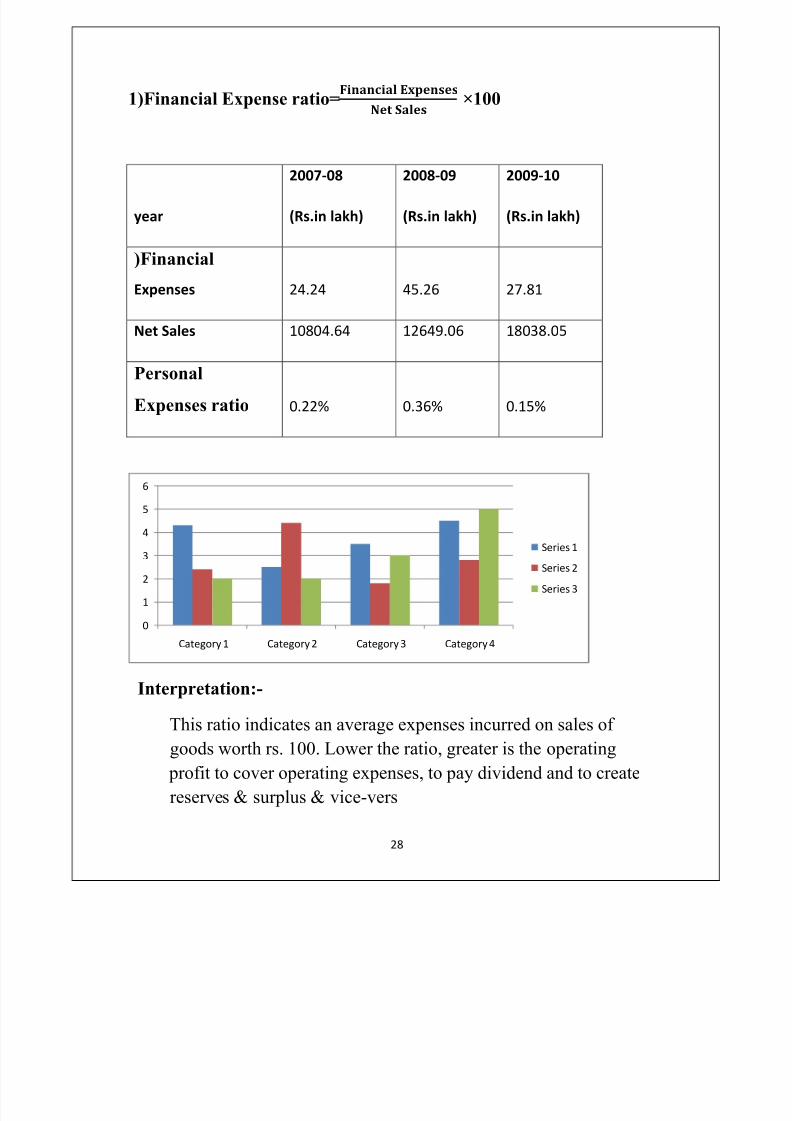

1)Financial Expense ratio=

×100

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

)Financial

Expenses 24.24 45.26 27.81

Net Sales 10804.64 12649.06 18038.05

Personal

Expenses ratio 0.22% 0.36% 0.15%

Interpretation:-

This ratio indicates an average expenses incurred on sales of

goods worth rs. 100. Lower the ratio, greater is the operating

profit to cover operating expenses, to pay dividend and to create

reserves & surplus & vice-vers

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 29/86

29

e. Return on Capital Employee:

Meaning:-

This ratio measures a relationship between not profit before

interest & tax and capital employed.

Objective:-

The objective of calculating this ratio is to find out how

efficiently the long term fund supplied by the creditors &

shareholders has been used.

Components:-

There are two Components of this ratio which are as under:

1. Net Profit Before Interest & Tax

2. Capital Employed Which Refers to Long Term Fund Supplied

by the long term creditors & shareholders.

It comprises the long term debts & shareholder¶s fund.

Calculation:-

This ratio is calculated by dividing the net profit before interest

& tax by capital employed. This is expressed as percentage. In

the form of a formula this ratio may be expressed as under:

Return on Capital Employed =

× 100

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 30/86

30

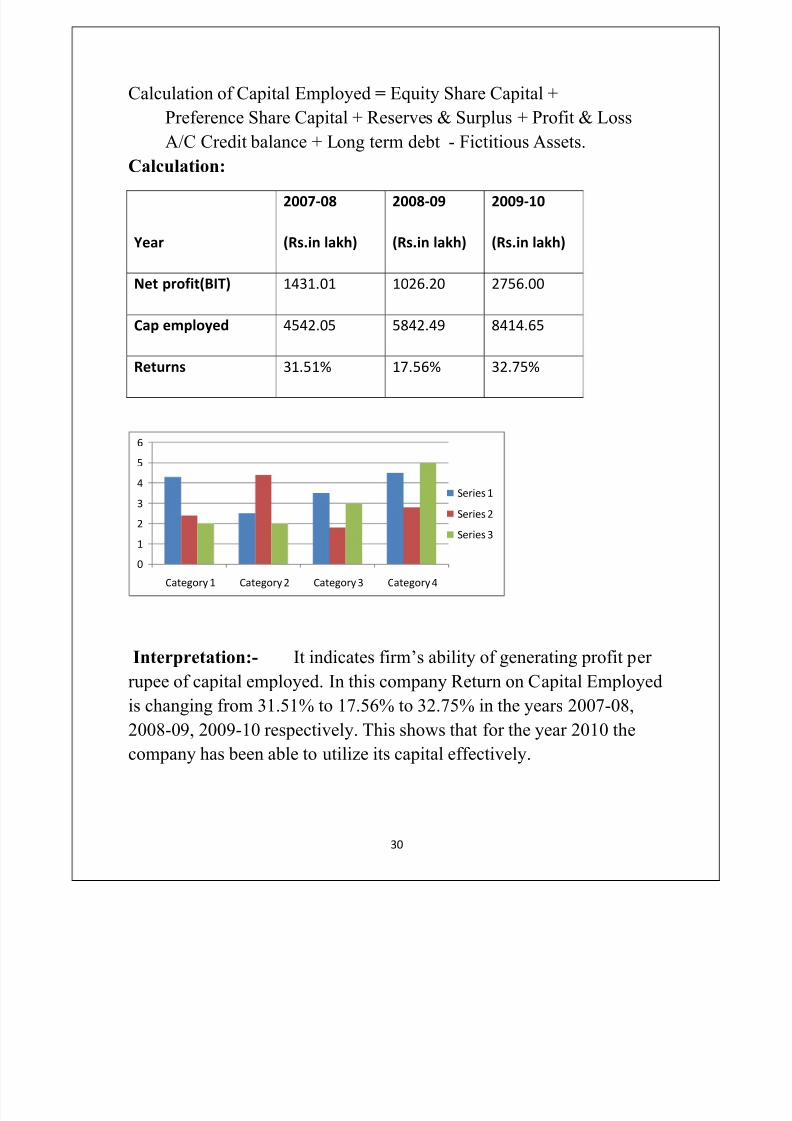

Calculation of Capital Employed = Equity Share Capital +

Preference Share Capital + Reserves & Surplus + Profit & Loss

A/C Credit balance + Long term debt - Fictitious Assets.

Calculation:

Year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Net profit(BIT) 1431.01 1026.20 2756.00

Cap employed 4542.05 5842.49 8414.65

Returns 31.51% 17.56% 32.75%

Interpretation:- It indicates firm¶s ability of generating profit per

rupee of capital employed. In this company Return on Capital Employed

is changing from 31.51% to 17.56% to 32.75% in the years 2007-08,

2008-09, 2009-10 respectively. This shows that for the year 2010 the

company has been able to utilize its capital effectively.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 31/86

31

Earning per share :

Meaning:-

This ratio measures the earnings available to an equityshareholder on a per share basis.

Objective:-

The objective of computing this ratio is to find out the

profitability of the firm on per equity share basis.

Components:-

There are two components of this ratio which are as under:

1. Net Profit after Interest, Tax & Preference dividend

2. No. of equity Shares

Calculation:-

This ratio is calculated by regarding the net profit after interest,

tax and preference dividend by the no. of equity shares. It is

expressed as absolute figure. In the form of a formula this ratio

may be expressed as under:

Formula: -

Earning per share = net profit preference divideNo. of equity shares

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 32/86

32

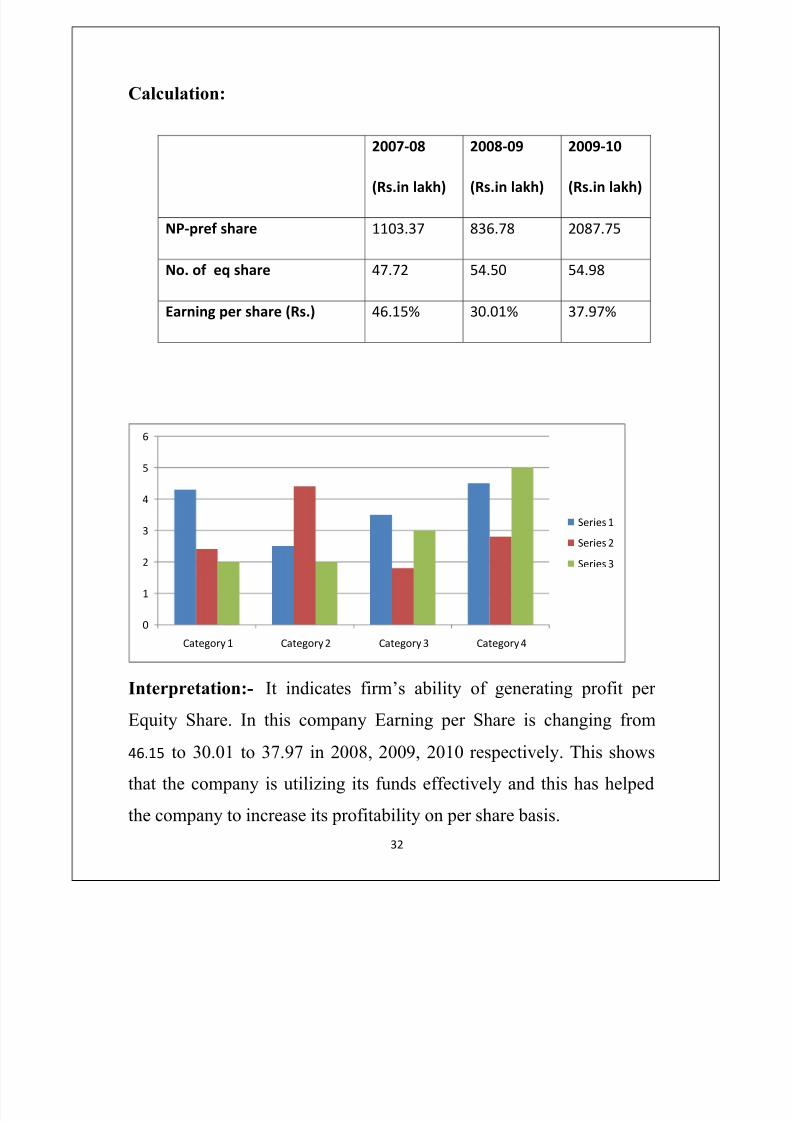

Calculation:

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

NP-pref share 1103.37 836.78 2087.75

No. of eq share 47.72 54.50 54.98

Earning per share (Rs.) 46.15% 30.01% 37.97%

Interpretation:- It indicates firm¶s ability of generating profit per

Equity Share. In this company Earning per Share is changing from

46.15 to 30.01 to 37.97 in 2008, 2009, 2010 respectively. This shows

that the company is utilizing its funds effectively and this has helped

the company to increase its profitability on per share basis.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 33/86

33

Dividend per share:

Meaning:-

This ratio measures relationship between dividend and no. of equity

shares.

Objective:-

The objective of computing this ratio is to find out net distributed

profit

after interest, tax and preference dividend to equity shareholders.

Components:-

There are two components of this ratio which are as under:

1. Dividend paid to equity shareholders

2. No. of equity shares

Calculation:-

This ratio is calculated by dividing dividend paid to equity

shareholders by no. of equity shares. It is expressed as absolute

figure. In the form of a formula this ratio can be expressed as

under:

Formula: -

Dividend per share = total dividend declared

No. of shares

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 34/86

34

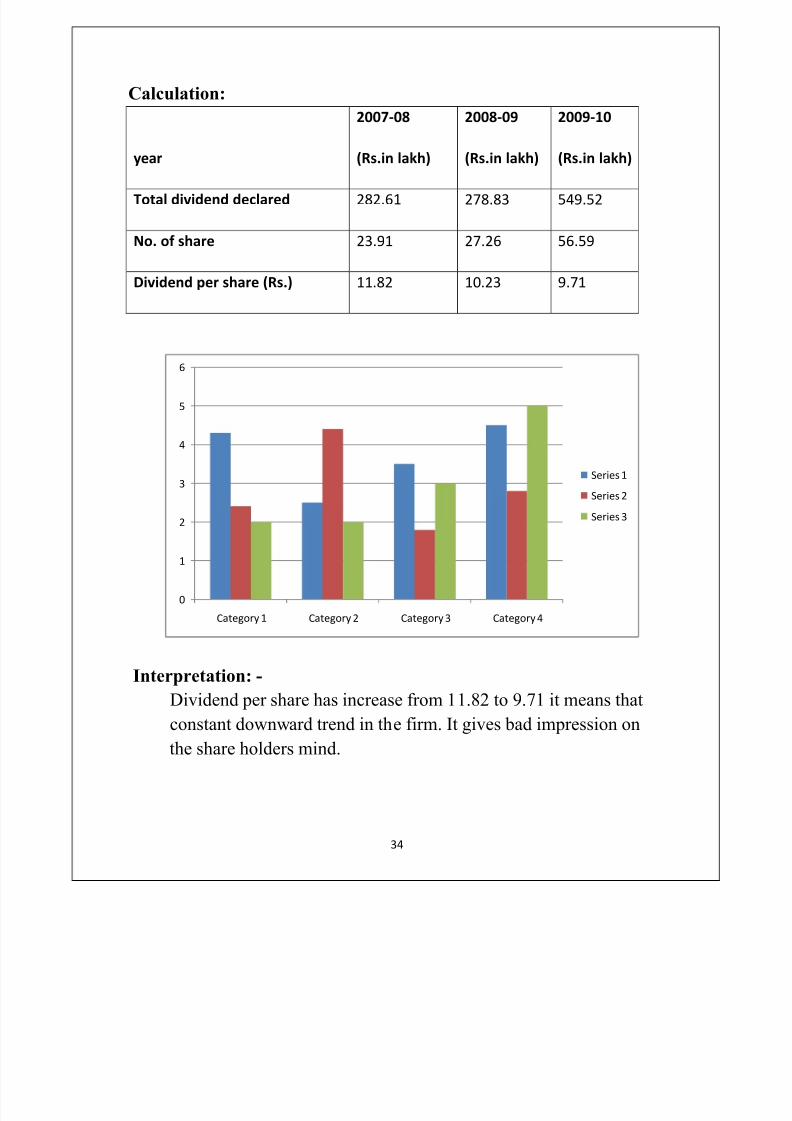

Calculation:

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Total dividend declared 282.61 278.83 549.52

No. of share 23.91 27.26 56.59

Dividend per share (Rs.) 11.82 10.23 9.71

Interpretation: -

Dividend per share has increase from 11.82 to 9.71 it means thatconstant downward trend in the firm. It gives bad impression on

the share holders mind.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 35/86

35

f. Price earning ratio: Meaning:-

This ratio measures relationship between market value of equityshares & earning per share.

Objective:-

The objective of computing this ratio is to find out expected

return on investment in equity shares.

Components:-

There are two components of this ratio which are as under:

1. Market price per equity share

2. Earnings per share

Calculation:-

This ratio is calculated by dividing market price per equity share

by earning per share. It is expressed has an absolute this figure.

In the form of a formula this ratio may be expressed as under:

Formula: -

Price earning ratio = market value per share

Earning per share

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 36/86

36

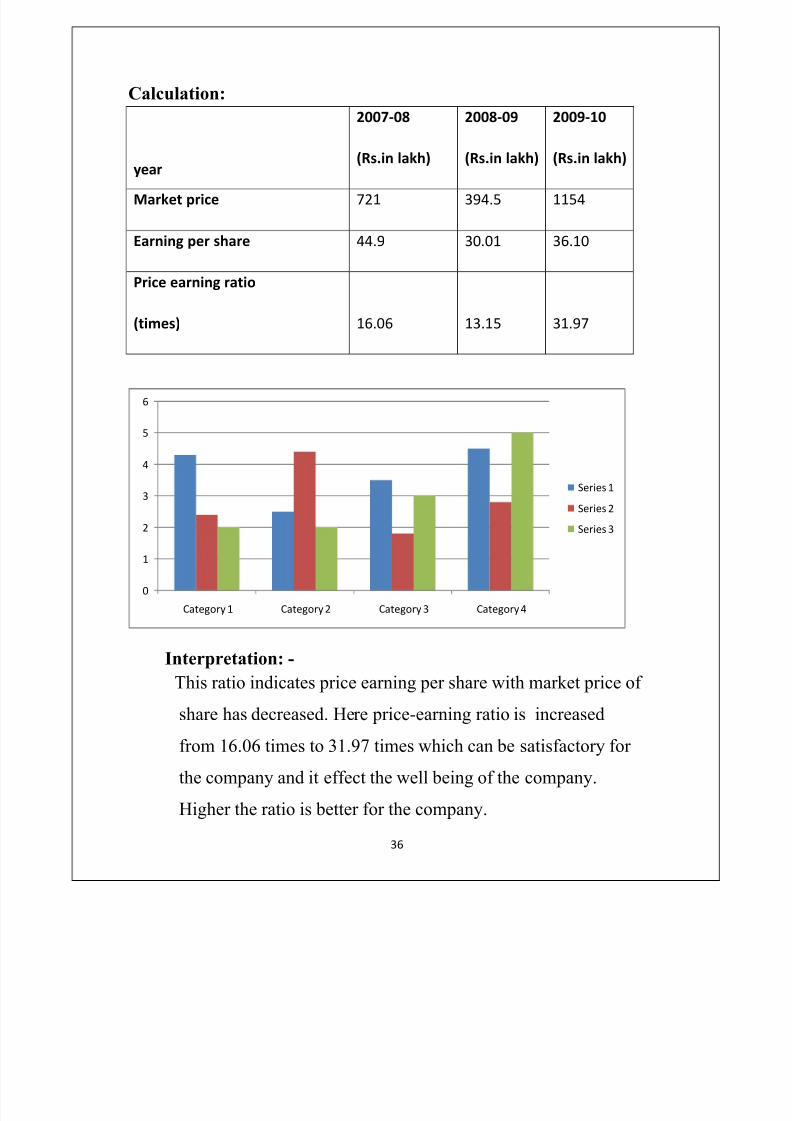

Calculation:

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Market price 721 394.5 1154

Earning per share 44.9 30.01 36.10

Price earning ratio

(times) 16.06 13.15 31.97

Interpretation: -

This ratio indicates price earning per share with market price of

share has decreased. Here price-earning ratio is increased

from 16.06 times to 31.97 times which can be satisfactory for

the company and it effect the well being of the company.

Higher the ratio is better for the company.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 37/86

37

Liquidity Ratio:

a. Current ratio:

Meaning:-

This ratio establishes a relationship between current assets &

current liabilities.

Objective:-

The objective of computing this ratio is to find the ability of

the firm to meet its short term obligation & to reflect the

short term financial strength or solvency of the firm.

Components:-

There are two components of this ratio which are as under:

1. Current Assets: Current Assets means the assets which are convertible in too cash

within a year & include the following:

y Cash balance, Marketable securities, Bills Receivables(less

provisions), Prepaid expenses, advanced payment of tax,

Bank balance, Debtors(less provisions), Stock of all types

(raw-materials, work in progress, Finished goods), Short termloans and advances(debit balance), Incomes due but not

received.

The provision for bed debt & or bills is deducted from the total

amount of trade.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 38/86

38

2. Current Liabilities: A current liability means the liabilities which are the expected to

be matured within a year and include the following.

y Creditors, Bills payable, short term loans & advances,

Provision for taxation, Bank overdraft, and income received

in advances, unclaimed dividend.

Calculation:-

This ratio is calculated by dividing the current assets by current

liabilities. This ratio is usually express as pure ratio.

Ex. 2:1

A form of a formula this ratio may be express as under.

Formula: -

Current ratio = Current asset

Current liabilities

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 39/86

39

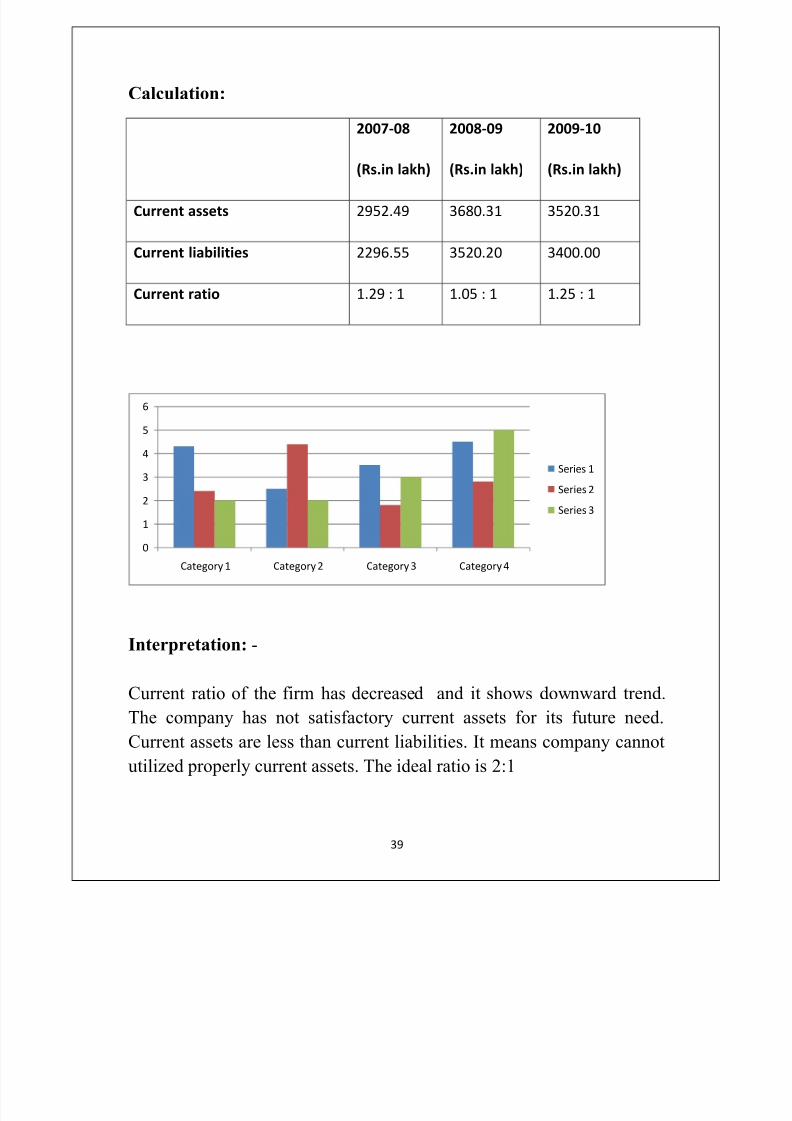

Calculation:

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Current assets 2952.49 3680.31 3520.31

Current liabilities 2296.55 3520.20 3400.00

Current ratio 1.29 : 1 1.05 : 1 1.25 : 1

Interpretation: -

Current ratio of the firm has decreased and it shows downward trend.The company has not satisfactory current assets for its future need.

Current assets are less than current liabilities. It means company cannot

utilized properly current assets. The ideal ratio is 2:1

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 40/86

40

b. Liquid Ratio(Quick Ratio/Acid Test Ratio):

Meaning:-

This ratio establishes the relationship between quick assets and

liquid liabilities.

Objective:-

The objective of calculating this ratio is to find out the ability of

the firm to meet its short term obligations as and when due

without relying upon the realization of stock.

Components:-

There are two components of this ratio which are as under:1. Quick assets/Liquid assets:

Which means those assets which can be converted short noticed

without a loss of value. They are:

y Cash balance, Marketable securities, Bills receivable,

Bankbalance & debtors.

2. Liquid Liabilities:

Liquid Liabilities = Current liabilities ± Bank over DraftCalculation:-

This ratio is calculated by dividing by the liquid assets by liquid

liabilities. This ratio is usually express as a pure ratio.

Ex. 1:1

In the form of a formula this ratio may be expressed as under:

Formula: -

Liquid ratio = Current asset - stock

Current liability-bank overdraft

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 41/86

41

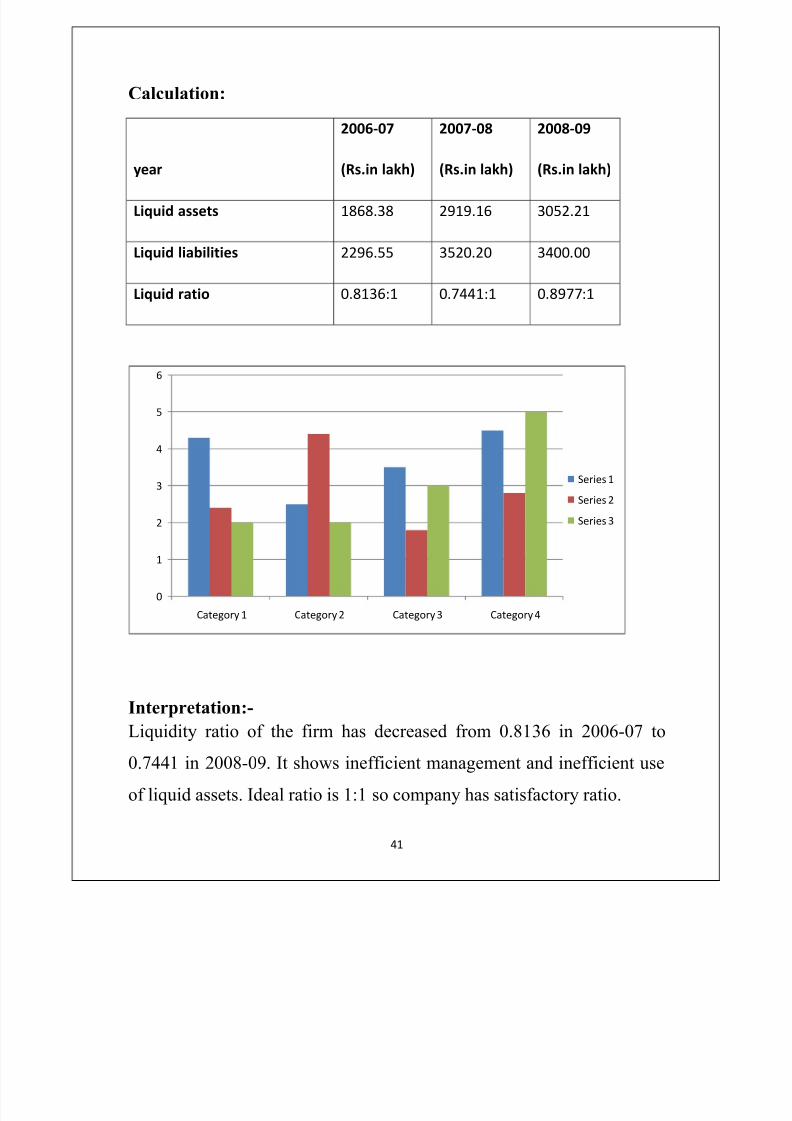

Calculation:

year

2006-07

(Rs.in lakh)

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

Liquid assets 1868.38 2919.16 3052.21

Liquid liabilities 2296.55 3520.20 3400.00

Liquid ratio 0.8136:1 0.7441:1 0.8977:1

Interpretation:-

Liquidity ratio of the firm has decreased from 0.8136 in 2006-07 to

0.7441 in 2008-09. It shows inefficient management and inefficient use

of liquid assets. Ideal ratio is 1:1 so company has satisfactory ratio.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series

3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 42/86

42

Activity Ratio:

Introduction:

This ratio measures the effectiveness with which a firm uses its

available resources. These ratios are also called turnover ratios since

they indicate the speed with which the resources are converted in to

sales. Usually the following activity ratios are calculated.

1. Stock Turnover Ratio

2. Working Capital Turnover Ratio

3. Total Assets Turnover Ratio

4. Book Value per Share Ratio

5. Debtors Ratio

6. Creditors Ratio

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 43/86

43

Stock turnover

ratio

Meaning:

This ratio establishes a relationship between costs of goods sold

(COGS)And average inventory.

Objective:

The objective of computing this ratio is to find out the efficiency

with which the inventory is utilized.

Components:

There are two components of this ratio they are as under:

1. Cost of Goods Sold which is calculated as under

y Opening stock + Net purchases + Direct expenses ± Closing

stock

Or

COGS = Net Sales ± Gross Profit

2. Average Inventory or Average Stock

3. Calculation: This ratio is calculation by dividing the cost of goods sold by

average inventory. This ratio is usually expressed as number of times.

Formula: -

Stock turnover ratio = cost of goods sold

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 44/86

44

Average inventory

Calculation: -

year

2006-07

(Rs.in lakh)

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

Cost of goods sold 7906.04 9463.68 12529.97

Average inventories 981.30 1072.39 1124.71

Stock turnover ratio (times) 8.66 8.82 8.82

Interpretation:

This ratios signifies that the average stock is turned over eight times

during the year. If figure for cost of sales are not available, then the ratiomay be calculated on the basis of sales. The ratio is very important in

judging the ability of management with which it can move the stock.

The higher the turnover ratio the more profitability the business would

be. Thus,a firm should have neither a very high nor a very low stock

turnover ratio.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 45/86

45

Working capital

turn

over

ratio

Meaning:-

This ratio establishes a relationship between net sales &

working capital.

Objective:-

The objective of computing this ratio is to find out the efficiency

with which the working capital is utilized.

Components:-

There are two components of this ratio which are as under:

1. Net Sales which means Gross Profit ± Sales Return

2. Working Capital which means Current Assets ± Current Liabilities

Calculation:-

This ratio is calculated by dividing the net profit by the working

capital. This ratio is usually expressed as no. of times. In the

form of a formula this ratio may be expressed as under.

Formula: -

Working Capital Turnover ratio =

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 46/86

46

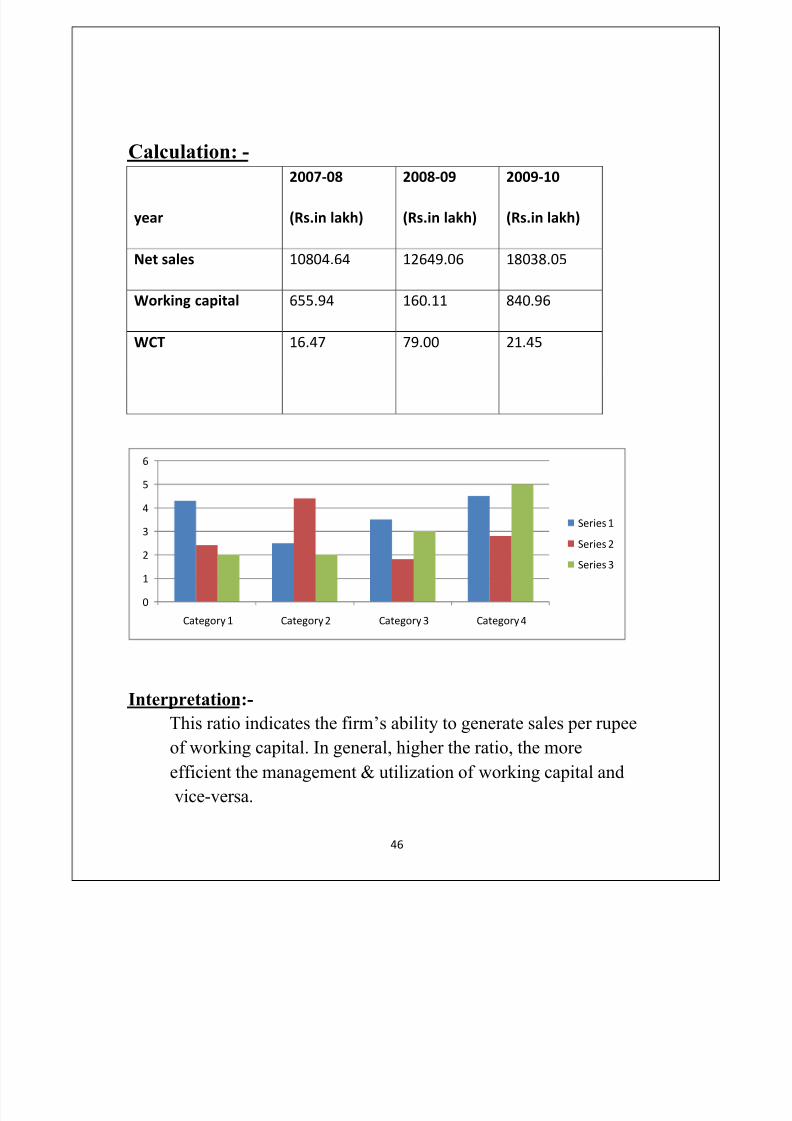

Calculation: -

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Net sales 10804.64 12649.06 18038.05

Working capital 655.94 160.11 840.96

WCT 16.47 79.00 21.45

Interpretation:- This ratio indicates the firm¶s ability to generate sales per rupee

of working capital. In general, higher the ratio, the more

efficient the management & utilization of working capital and

vice-versa.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 47/86

47

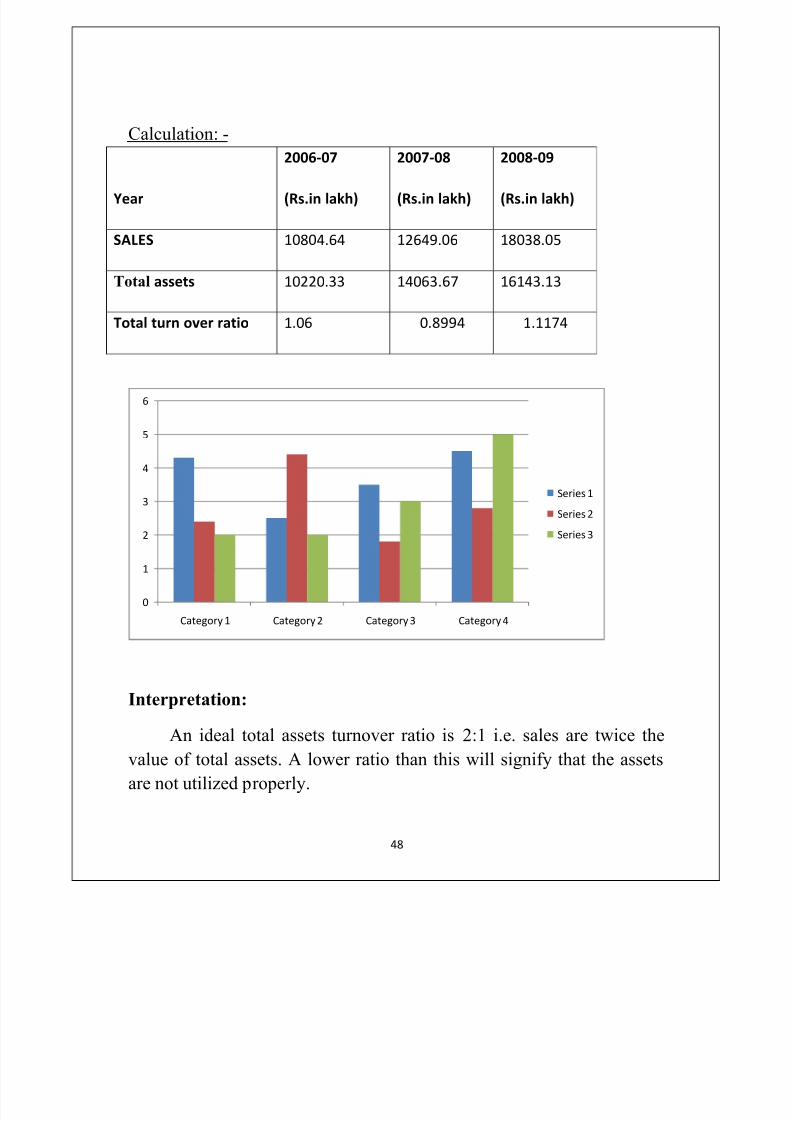

Total Turnover Ratio

Meaning:

This ratio measures the overall performance or activity of the

business enterprise.

Objective:

The objective of calculating this ratio is to point out the efficiency

or inefficiency in the use of total assets.

Components:

There are two components of this ratio which

1. Net Sales2. Total Assets

Calculation:

This ratio is calculated by dividing net sales by total assets.

Total Assets Turnover Ratio =

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 48/86

48

Calculation: -

Year

2006-07

(Rs.in lakh)

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

SALES 10804.64 12649.06 18038.05

Total assets 10220.33 14063.67 16143.13

Total turn over ratio 1.06 0.8994 1.1174

Interpretation:

An ideal total assets turnover ratio is 2:1 i.e. sales are twice the

value of total assets. A lower ratio than this will signify that the assets

are not utilized properly.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 49/86

49

Book Value Per Share

Meaning:

This ratio establishes relationship between equity share capital &

reserves and surplus with no. of shares.

Objective:

The objective of computing this ratio is to find out the proportion

of share capital & reserves & surplus with no. of equity shares.

Components:

There are two components of this ratio

1. Equity share capital & reserves and surplus

2. No. of equity shares

Calculation:

This ratio is computed by dividing equity share capital & reserves

& surplus by no. of equity shares. It is expressed as an absolute figure.

Book Value per Share Ratio =

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 50/86

50

Calculation: -

Year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Eq. shares+Resrves &

surplus 4350.07 5262.08 7826.77

No. of eq shares 23.91 27.26 56.89

Book valueper share 181.94 193.03 138.31

Interpretation:

In general higher the ratio better it is because this ratio measures

relationship between share capital and reserves & surplus with no. of

equity shares. In the most of the companies the amount of equity share

capital remains constant & the value of reserves & surplus charges.

Whenever company has high amount of profits, the value of reserves &

surplus will increase. Therefore higher book value per share means high

amount of profitability.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 51/86

51

Debtors Ratio

Meaning:

This ratio establishes a relationship between debtors and bills

receivables with average daily credit sales.

Objective:

The objectives of computing this ratio is to find out the efficiency

with the trade debtors are managed.

Components:

There are two components of this ratio

1. Debtors and Bills receivable

2. Net Credit Sales

Calculation:

This ratio is calculated by dividing debtors and bills receivables by

net credit sales. This ratio is usually expressed as X no. of times (days).

Debtors Ratio =

×365

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 52/86

52

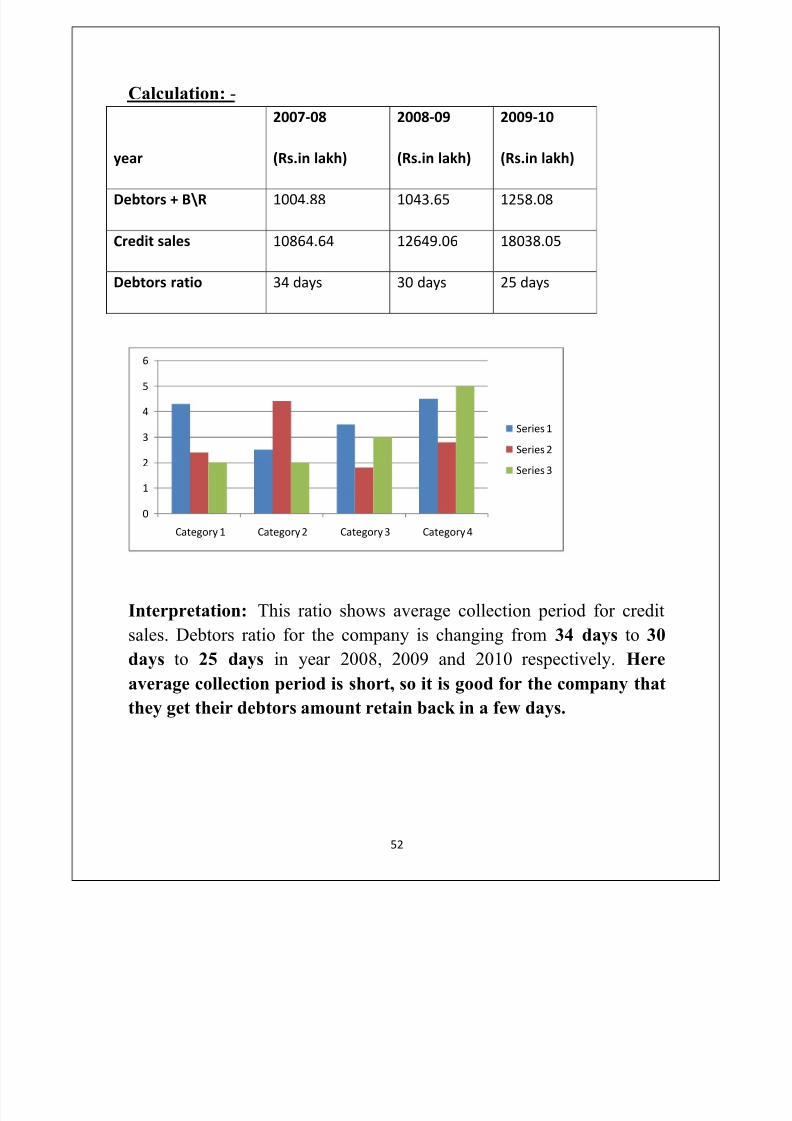

Calculation: -

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Debtors + B\R 1004.88 1043.65 1258.08

Credit sales 10864.64 12649.06 18038.05

Debtors ratio 34 days 30 days 25 days

Interpretation: This ratio shows average collection period for credit

sales. Debtors ratio for the company is changing from 34 days to 30

days to 25 days in year 2008, 2009 and 2010 respectively. Here

average collection period is short, so it is good for the company that

they get their debtors amount retain back in a few days.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 53/86

53

Creditors ratio

Meaning:

This ratio establishes a relationship between creditors and bills

payable and average daily credit purchases.

Objective:

The objective of computing this ratio is to determine the efficiency

with which creditors are managed.

Components:

There are two components of this ratio

1. Creditors and Bills Payable

2. Net Credit Purchases

Calculation:

This ratio is calculated by dividing the creditors and Bills Payables

by Net credit purchases. This ratio is usually expressed as X no. of times

(days).

Formula: -

Creditors ratio = Creditors + bills payable

Credit purchase

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 54/86

54

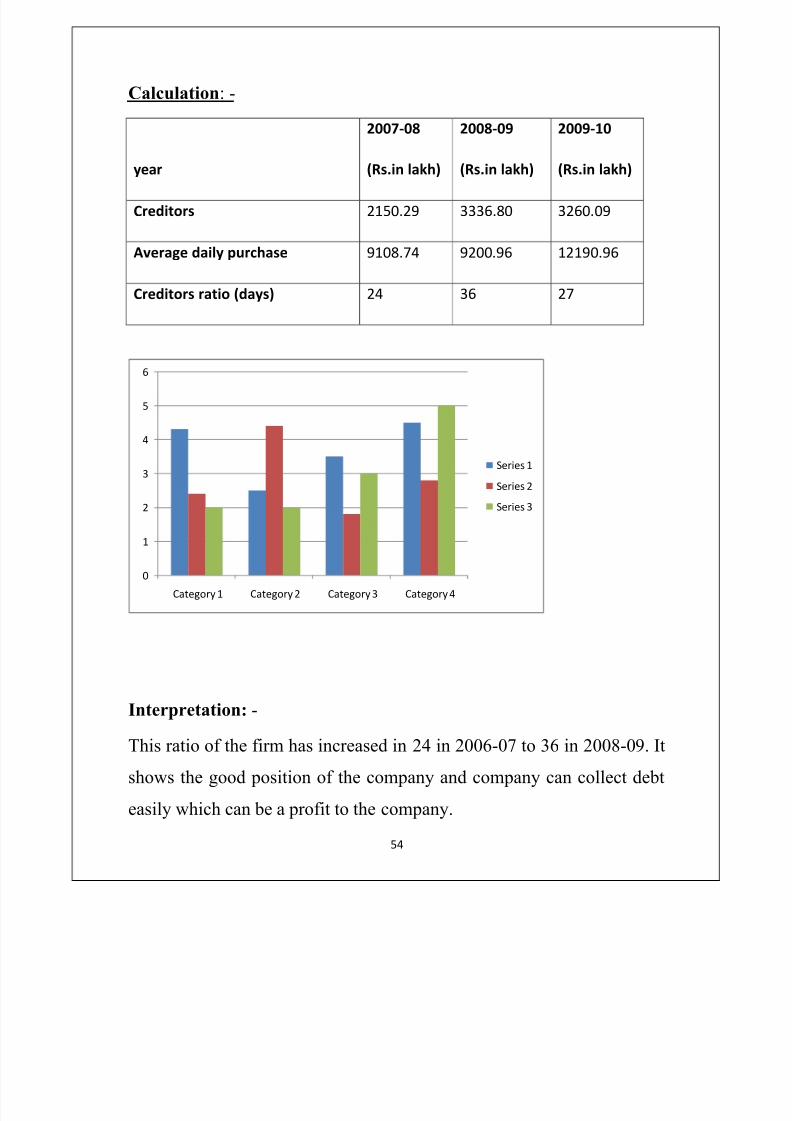

Calculation: -

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Creditors 2150.29 3336.80 3260.09

Average daily purchase 9108.74 9200.96 12190.96

Creditors ratio (days) 24 36 27

Interpretation: -

This ratio of the firm has increased in 24 in 2006-07 to 36 in 2008-09. It

shows the good position of the company and company can collect debt

easily which can be a profit to the company.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 55/86

55

Leverage Ratio

Capital Structure Ratio (Capital Gearing Ratio)

Meaning:

Capital structure of a company consist of a verity of securities

Ex. Equity share & preference share which satisfy its share capitalrequirements while by other securities such as debentures, warrants etc.

the company satisfies its access requirement of long term capital &

borrowed capital, leverage ratios are calculated. Sum of the leverage

ratios are as under.

1. Debt equity ratio

2. Proprietary ratio

3. Capital Gearing ratio

4. Long term funds to fixed assets ratio

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 56/86

56

Debt Equity Ratio

Meaning:

This ratio establishes a relationship between long term debts &

shareholders funds.

Objective:

The objective of computing this ratio is to find out the relative

proportion of debt & equity in financing the assets of a firm.

Components:

There are two components of this ratio which are as under:

1. Long term debt which means all types of secured and unsecured

loans.

Ex. Debtors, Loans from financial institution

2. Shareholder¶s funds which means equity share capital +

Preference share capital + Reserves & surplus ± Fictitious

Assets

Calculation:

This ratio is calculated by dividing the long term debts of the firm

by shareholder¶s fund. This ratio is usually expressed as a pure ratio.

Ex. 2:1

Debt Equity Ratio =

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 57/86

57

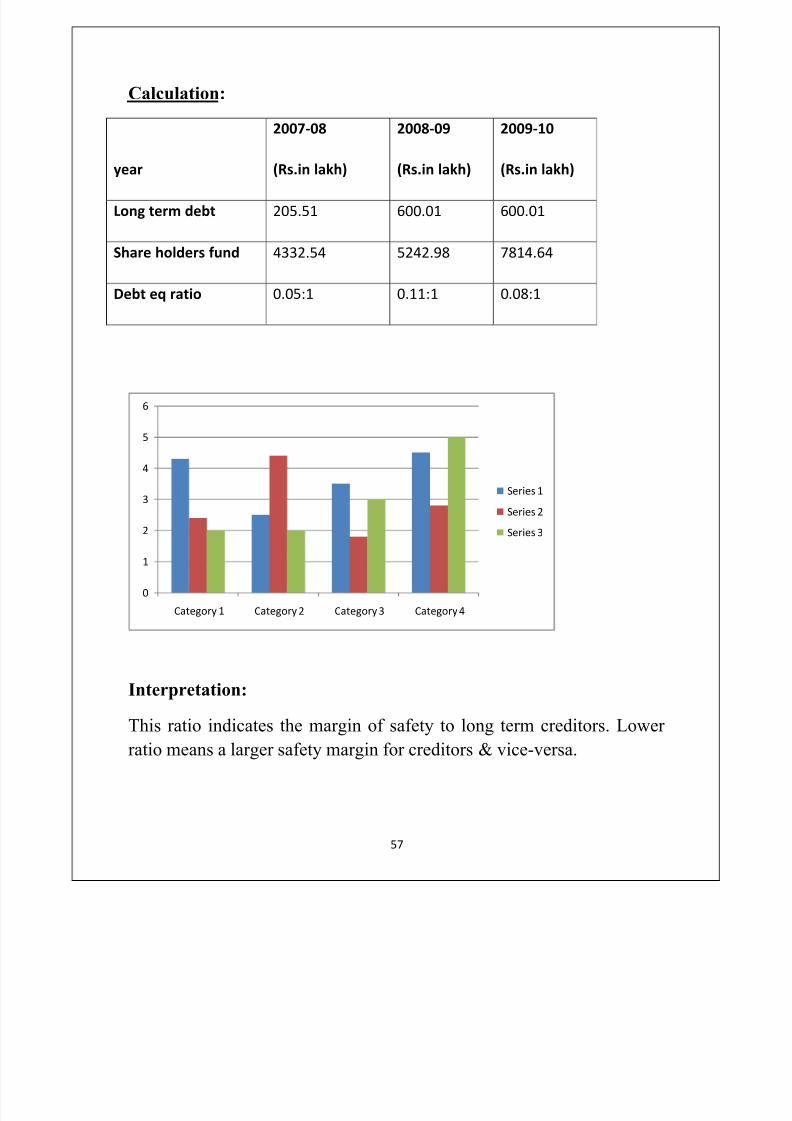

Calculation:

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Long term debt 205.51 600.01 600.01

Share holders fund 4332.54 5242.98 7814.64

Debt eq ratio 0.05:1 0.11:1 0.08:1

Interpretation:

This ratio indicates the margin of safety to long term creditors. Lower

ratio means a larger safety margin for creditors & vice-versa.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 58/86

58

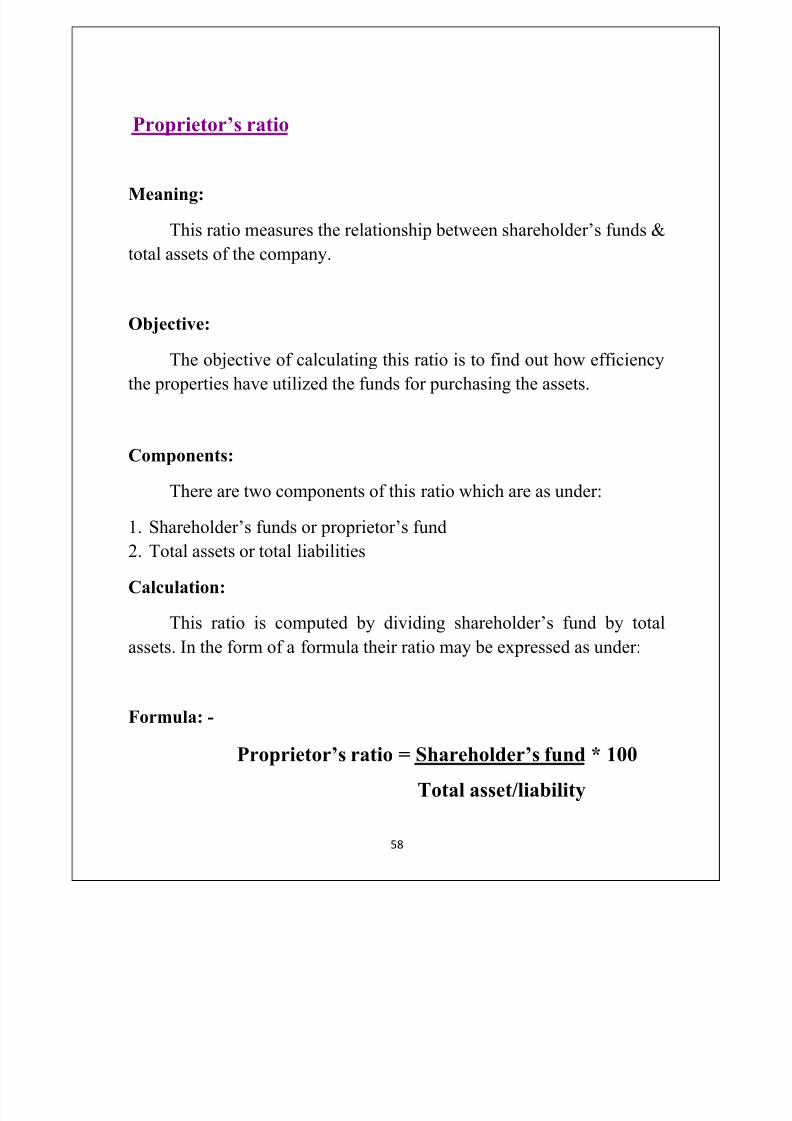

Proprietor¶s ratio

Meaning:

This ratio measures the relationship between shareholder¶s funds &

total assets of the company.

Objective:

The objective of calculating this ratio is to find out how efficiency

the properties have utilized the funds for purchasing the assets.

Components:

There are two components of this ratio which are as under:

1. Shareholder¶s funds or proprietor¶s fund2. Total assets or total liabilities

Calculation:

This ratio is computed by dividing shareholder¶s fund by total

assets. In the form of a formula their ratio may be expressed as under:

Formula: -

Proprietor¶s ratio = Shareholder¶s fund * 100

Total asset/liability

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 59/86

59

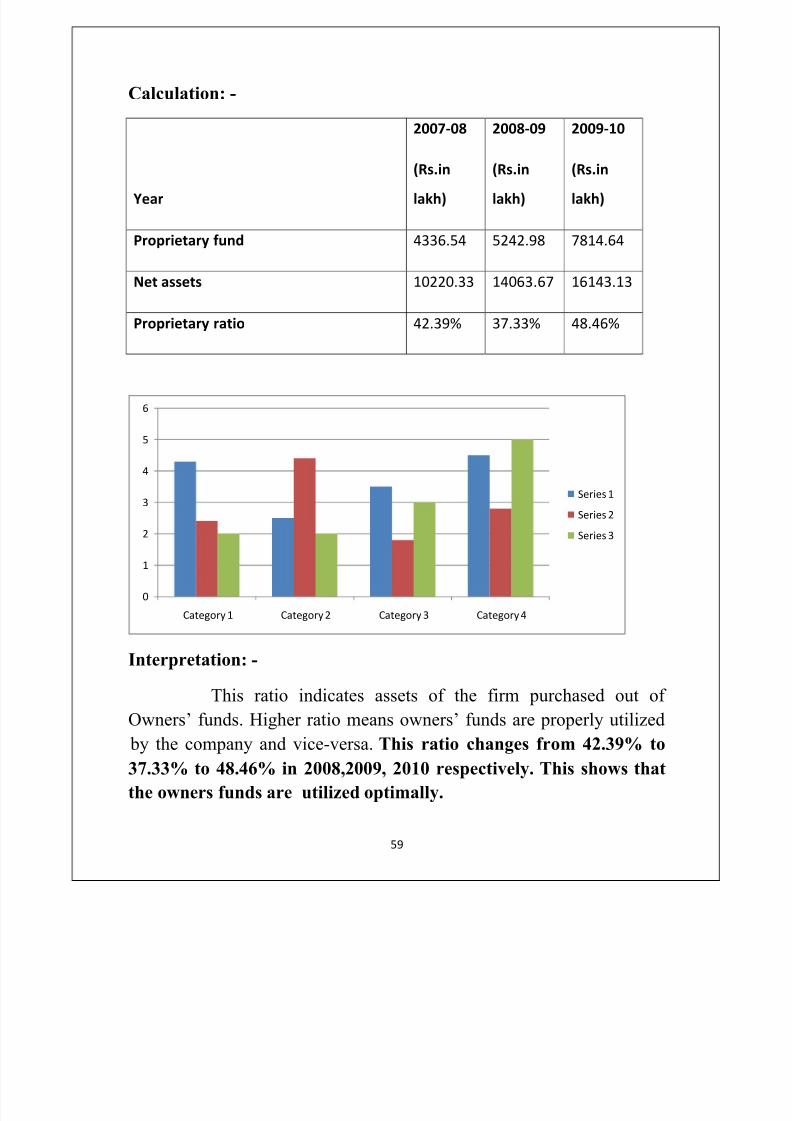

Calculation: -

Year

2007-08

(Rs.inlakh)

2008-09

(Rs.inlakh)

2009-10

(Rs.inlakh)

Proprietary fund 4336.54 5242.98 7814.64

Net assets 10220.33 14063.67 16143.13

Proprietary ratio 42.39% 37.33% 48.46%

Interpretation: -

This ratio indicates assets of the firm purchased out of Owners¶ funds. Higher ratio means owners¶ funds are properly utilized

by the company and vice-versa. This ratio changes from 42.39% to

37.33% to 48.46% in 2008,2009, 2010 respectively. This shows that

the owners funds are utilized optimally.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 60/86

60

Capital Gearing Ratio

Meaning:

This ratio measures a relationship between equity shares capitaland fixed interest bearing capital.

Objectives:

The objective of computing this ratio is to find out the proportion

between fixed interest bearing capital & equity share capital.

Components:

There are two components of this ratio which are as under:

1. Fixed interest bearing capital (preference share capital,

debenture, long term loan)

2. Equity share capital

Calculation:

This ratio is calculated by dividing fixed increased bearing capital

by equity share capital. This ratio is expressed as a pure ratio. In the

form of a formula this ratio may be expressed as under:

Capital Gearing Ratio =

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 61/86

61

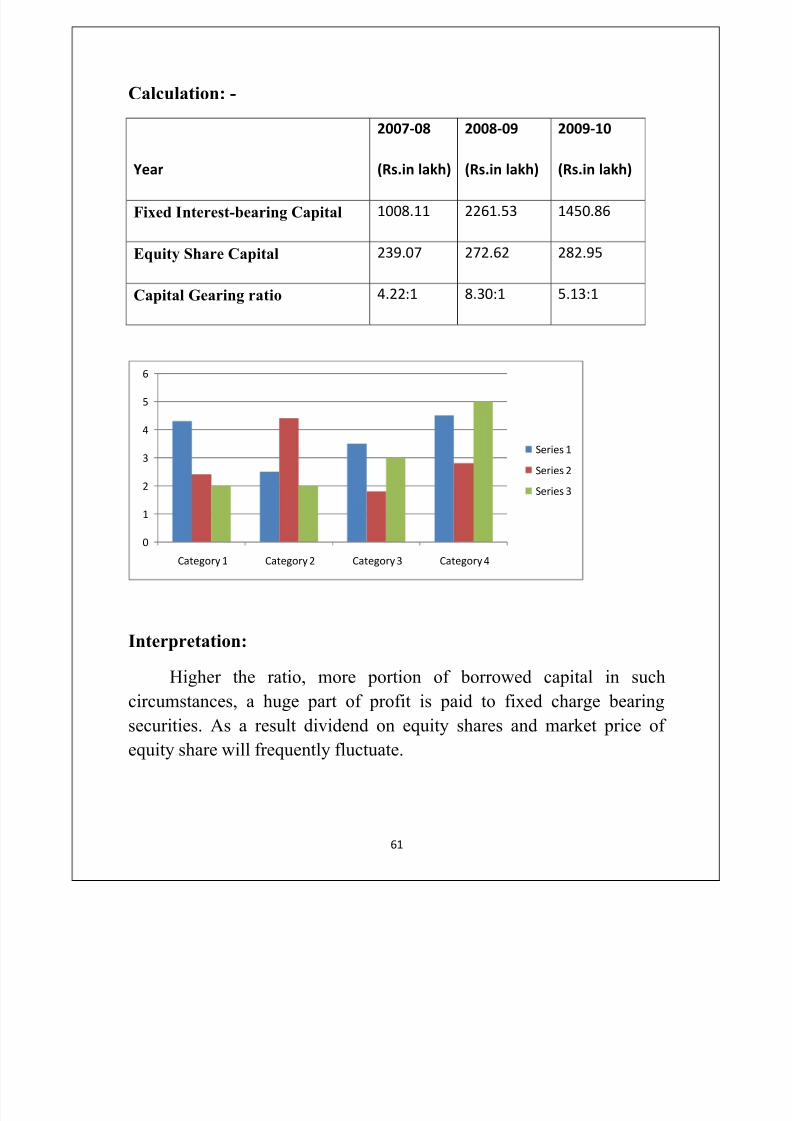

Calculation: -

Year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Fixed Interest-bearing Capital 1008.11 2261.53 1450.86

Equity Share Capital 239.07 272.62 282.95

Capital Gearing ratio 4.22:1 8.30:1 5.13:1

Interpretation:

Higher the ratio, more portion of borrowed capital in such

circumstances, a huge part of profit is paid to fixed charge bearingsecurities. As a result dividend on equity shares and market price of

equity share will frequently fluctuate.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 62/86

62

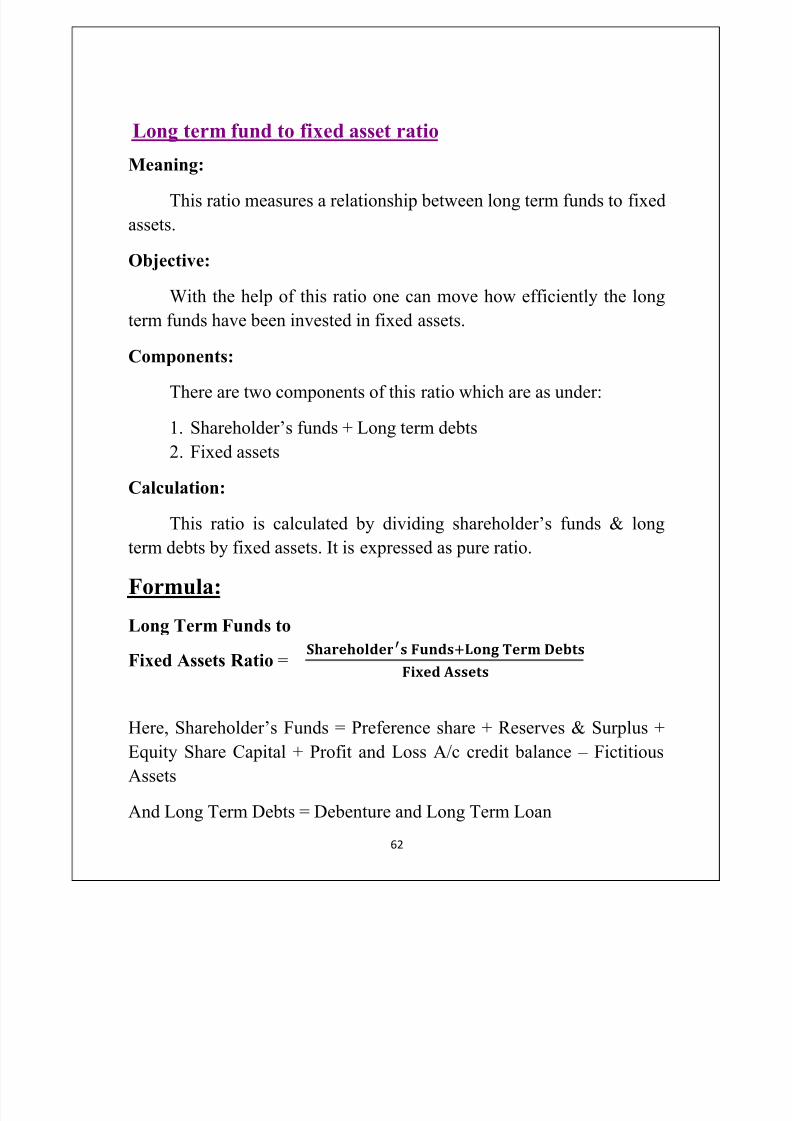

Long term fund to fixed asset ratio

Meaning:

This ratio measures a relationship between long term funds to fixed

assets.

Objective:

With the help of this ratio one can move how efficiently the long

term funds have been invested in fixed assets.

Components:

There are two components of this ratio which are as under:

1. Shareholder¶s funds + Long term debts

2. Fixed assets

Calculation:

This ratio is calculated by dividing shareholder¶s funds & longterm debts by fixed assets. It is expressed as pure ratio.

Formula:

Long Term Funds to

Fixed Assets Ratio =

Here, Shareholder¶s Funds = Preference share + Reserves & Surplus +

Equity Share Capital + Profit and Loss A/c credit balance ± Fictitious

Assets

And Long Term Debts = Debenture and Long Term Loan

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 63/86

63

Calculation: -

year

2007-08

(Rs.in lakh)

2008-09

(Rs.in lakh)

2009-10

(Rs.in lakh)

Long term funds 2587.06 4052.76 2880.15

Fixed assets 2360.09 3216.33 3707.72

Long term funds to fixed ratio 1.096:1 1.26:1 0.78:1

Interpretation: -

Long-term ratio decreased from 1.096 to 1.26. It has shown fall inthe ratio. The fixed assets should always be acquired out of long-term

funds, meaning thereby that this ratio should not be less than 100. The

company has not achieved a good ratio as it shows a downward trend.

0

1

2

3

4

5

6

Category 1 Category 2 Category 3 Category 4

Series 1

Series 2

Series 3

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 64/86

64

Common Size Analysis

Ratio analysis is a part another useful way of analyzing financial

statement is to convert them into common size statement by expressing

absolute rupee amounts into percentages. When this method is pursued

the income statement exhibits each expense item or group of expense.

Items as a percentage of net sales and net sales are taken at 100 percent.

Similarly, each individual asset and liability respectively statement are

prepared. His ways are referred to as common size statement.

5) Common Size Statement of Profit & Loss Account

Particular

Amount in Corer % of Sales

2007-08 2008-09 2009-10 07-08 08-09 09-10

Sales 10804.64 12649.0618038.0

5100 100 100

(-)C.O.G.S. 7906.04 9463.68 12529.20 73.17 74.82 69.46

GP 5525.47 3260.51 2926.91 51.14 25.78 16.23

(-) Admini.

Exp.8612.23 10298.84 13544.68 79.71 81.42 75.09

(-) Selling

Exp.1608.96 1777.34 2161.74 14.89 14.05 11.98

(-)FinancialExp. 262.9 336.77 398.59 2.57 2.66 2.21

Net Profit

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 65/86

65

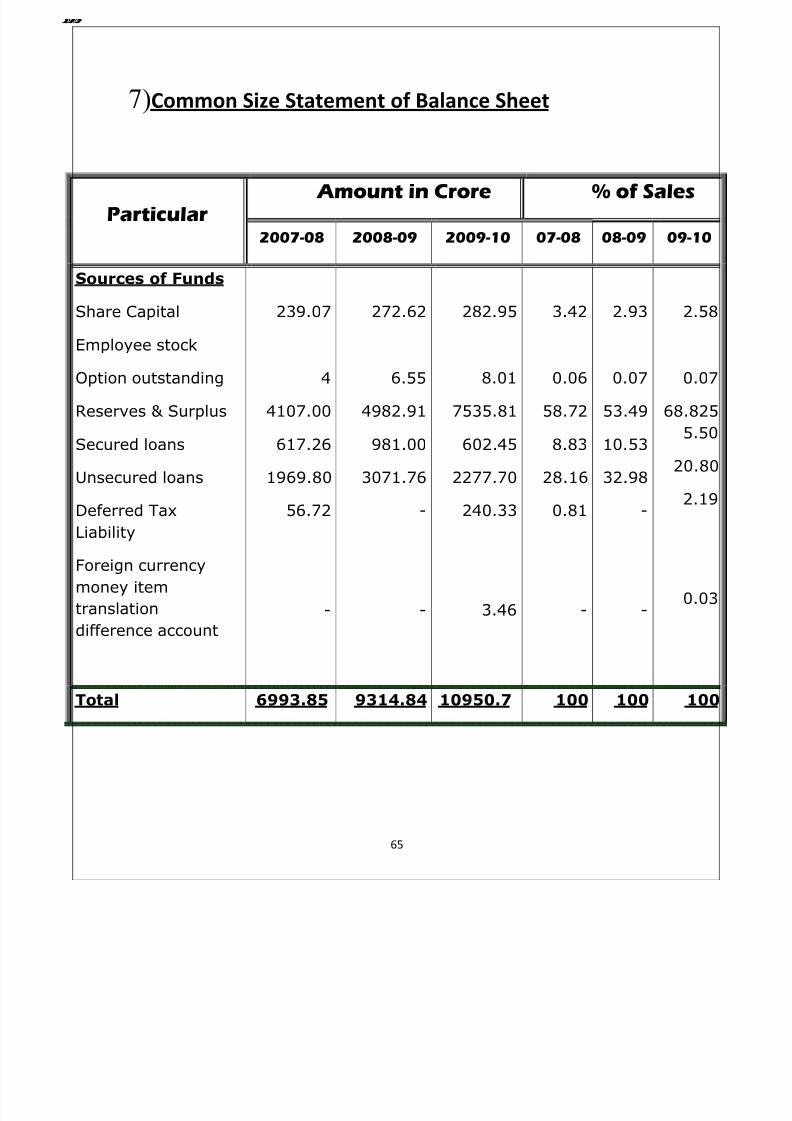

7)Common Size Statement of Balance Sheet

Particular

Amount in Crore % of Sales

2007-08 2008-09 2009-10 07-08 08-09 09-10

Sources of Funds

Share Capital

Employee stock

Option outstanding

Reserves & Surplus

Secured loans

Unsecured loans

Deferred Tax

Liability

Foreign currency

money item

translation

difference account

239.07

4

4107.00

617.26

1969.80

56.72

-

272.62

6.55

4982.91

981.00

3071.76

-

-

282.95

8.01

7535.81

602.45

2277.70

240.33

3.46

3.42

0.06

58.72

8.83

28.16

0.81

-

2.93

0.07

53.49

10.53

32.98

-

-

2.5

0.0

68.82

5.5

20.8

2.1

0.0

Total 6993.85 9314.84 10950.7 100 100 10

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 66/86

66

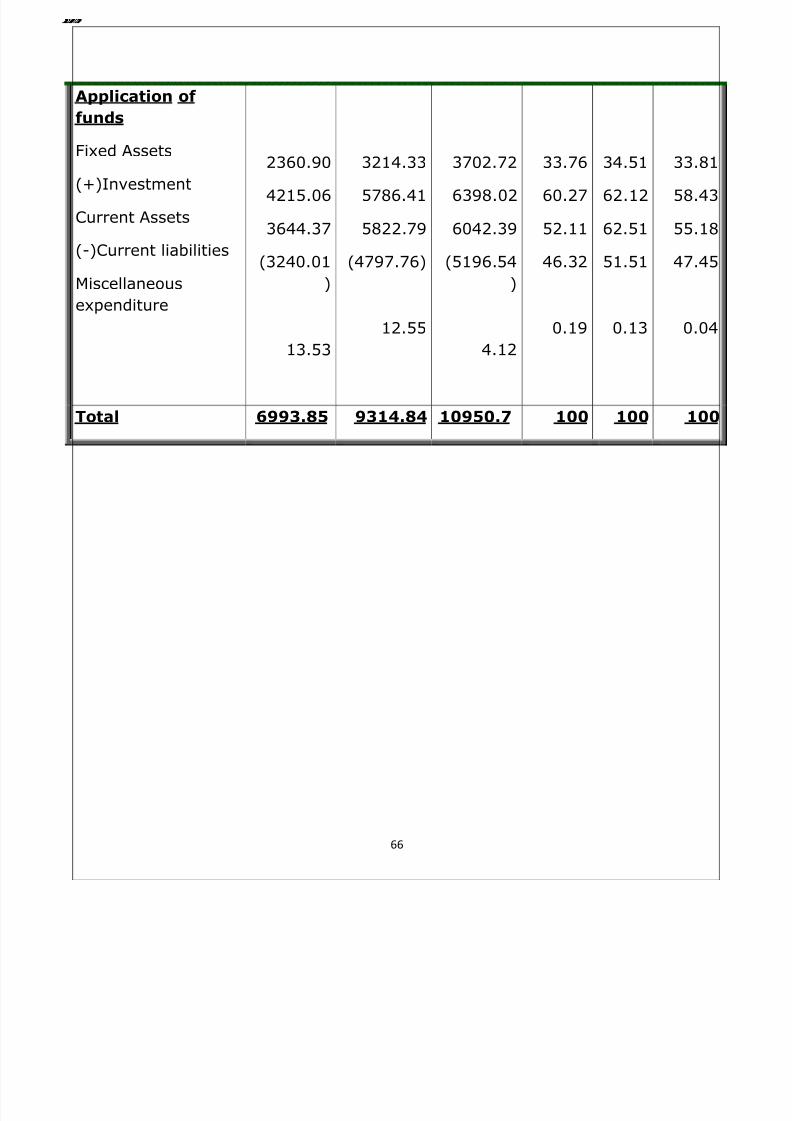

Application of

funds

Fixed Assets

(+)Investment

Current Assets

(-)Current liabilities

Miscellaneous

expenditure

2360.90

4215.06

3644.37

(3240.01

)

13.53

3214.33

5786.41

5822.79

(4797.76)

12.55

3702.72

6398.02

6042.39

(5196.54

)

4.12

33.76

60.27

52.11

46.32

0.19

34.51

62.12

62.51

51.51

0.13

33.8

58.4

55.1

47.4

0.0

Total 6993.85 9314.84 10950.7 100 100 10

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 67/86

67

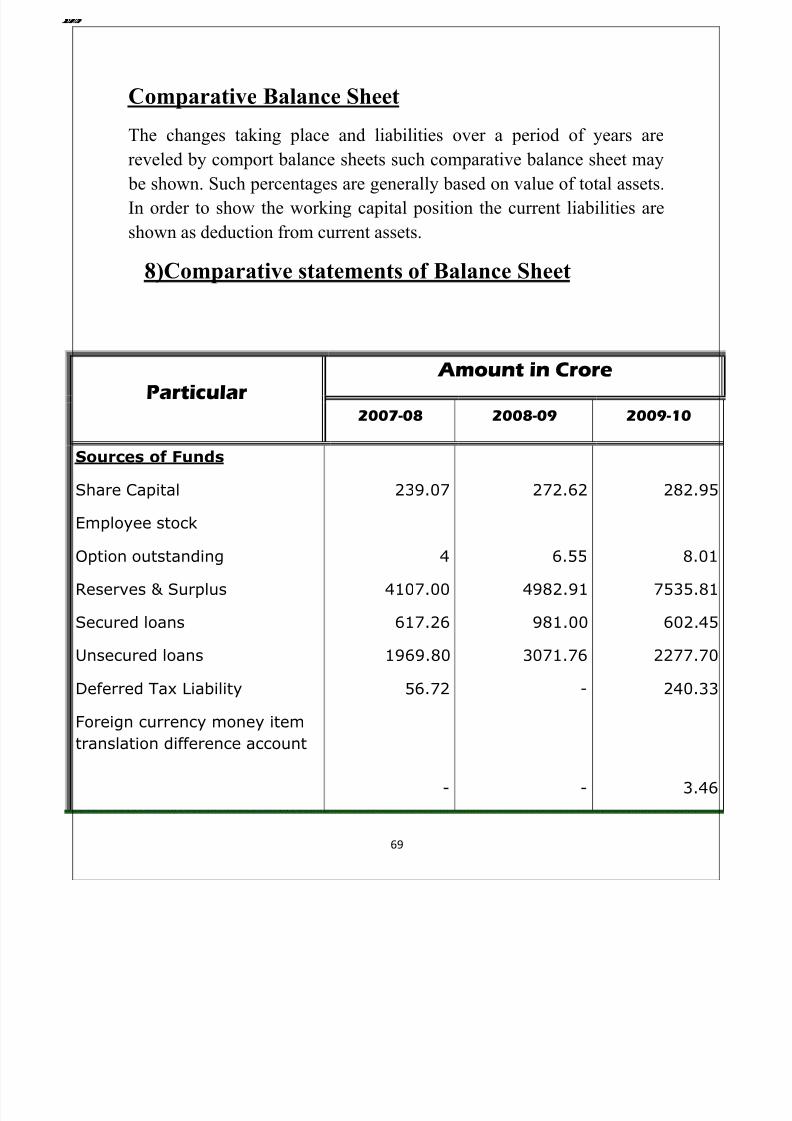

Comparative Statement Analysis

A simple method of tracing periodic changes in the financial performance of a company is to comparative statements. Comparative

financial statements will contain items at least for two periods. Changes

increases or decreases in income statement and balance sheet over

period can be shown on two ways:

(1) Aggregate Changes

(2) Proportional Changes

Aggregate changes can be indicated by drawing special column for

aggregate amount or percentage or both of increase or decrease. Relative

or prepositional, changes, and other hand are shown by recording

percentage calculation in relation to a common base in special columns.For example in the case of profit and loss statement, sales figure is

assumed to be shown. Such percentages are generally based on value of

total assets. In order to show the working capital position the current

liabilities are shown as deduction from current assets.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 68/86

68

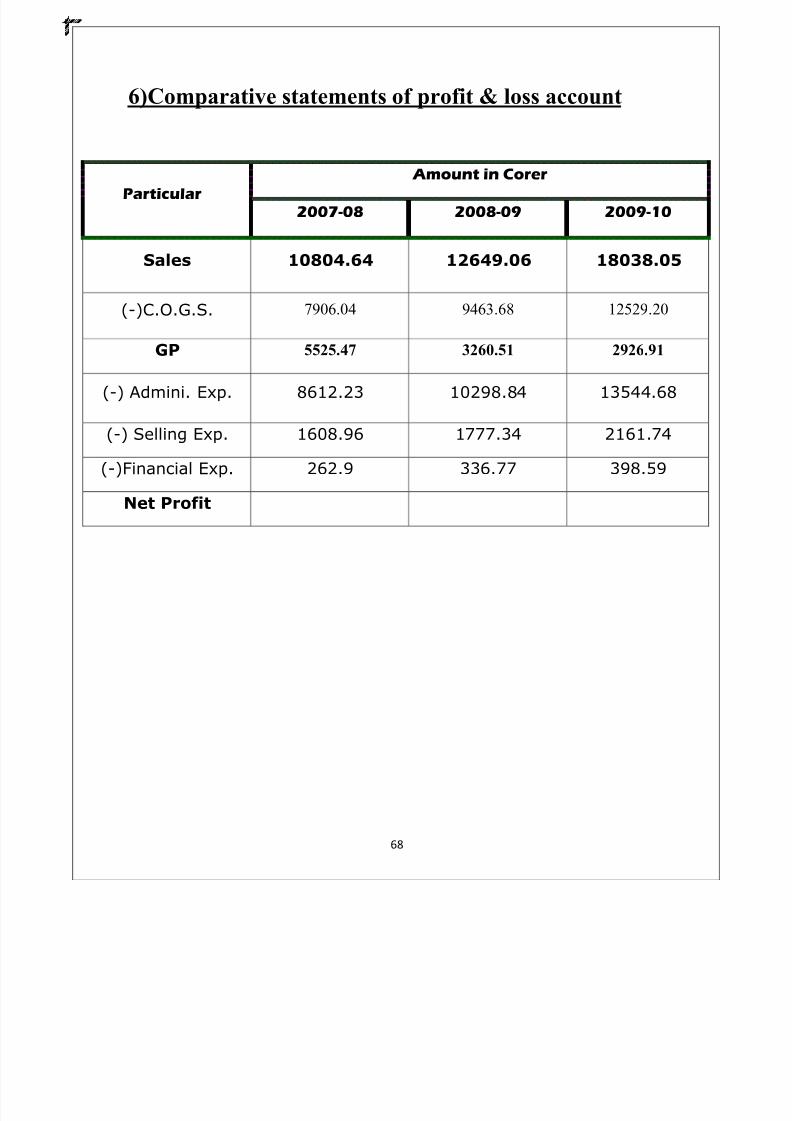

6)Comparative statements of profit & loss account

Particular Amount in Corer

2007-08 2008-09 2009-10

Sales 10804.64 12649.06 18038.05

(-)C.O.G.S. 7906.04 9463.68 12529.20

GP 5525.47 3260.51 2926.91

(-) Admini. Exp. 8612.23 10298.84 13544.68

(-) Selling Exp. 1608.96 1777.34 2161.74

(-)Financial Exp. 262.9 336.77 398.59

Net Profit

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 69/86

69

Comparative Balance Sheet

The changes taking place and liabilities over a period of years are

reveled by comport balance sheets such comparative balance sheet may

be shown. Such percentages are generally based on value of total assets.

In order to show the working capital position the current liabilities are

shown as deduction from current assets.

8)Comparative statements of Balance Sheet

Particular

Amount in Crore

2007-08 2008-09 2009-10

Sources of Funds

Share Capital

Employee stock

Option outstanding

Reserves & Surplus

Secured loans

Unsecured loans

Deferred Tax Liability

Foreign currency money item

translation difference account

239.07

4

4107.00

617.26

1969.80

56.72

-

272.62

6.55

4982.91

981.00

3071.76

-

-

282.9

8.0

7535.8

602.4

2277.7

240.3

3.4

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 70/86

70

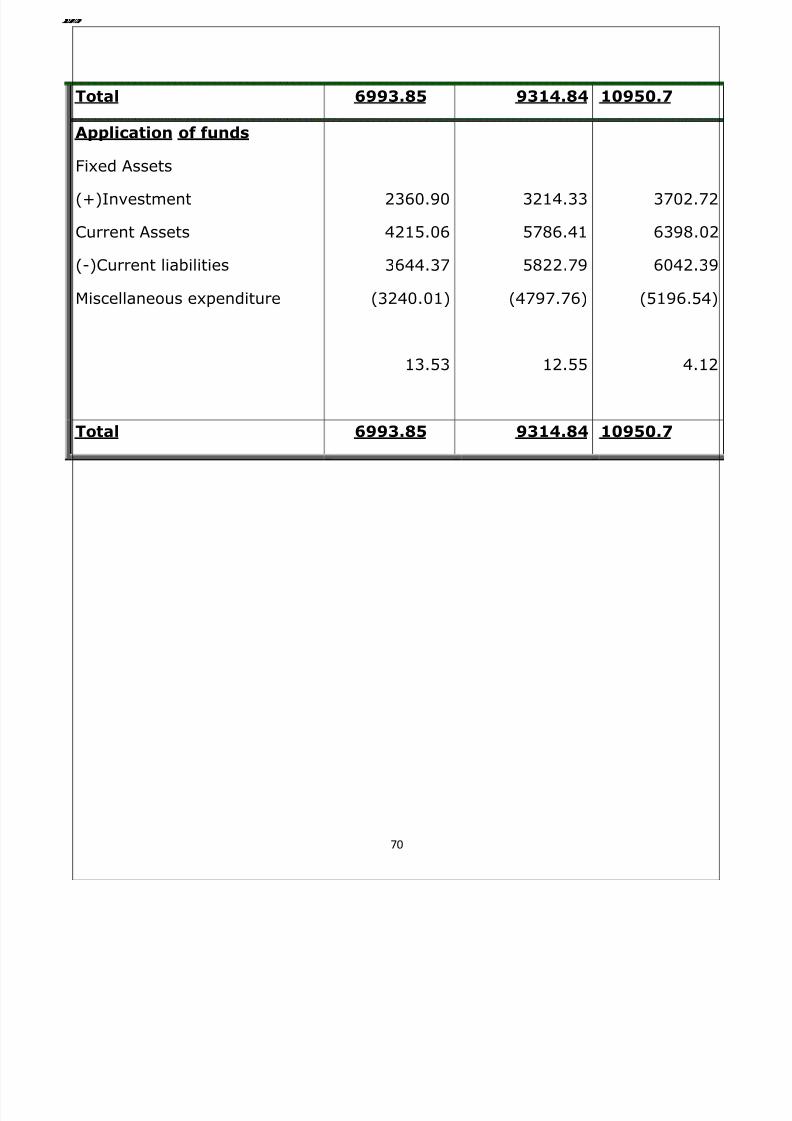

Total 6993.85 9314.84 10950.7

Application of funds

Fixed Assets

(+)Investment

Current Assets

(-)Current liabilities

Miscellaneous expenditure

2360.90

4215.06

3644.37

(3240.01)

13.53

3214.33

5786.41

5822.79

(4797.76)

12.55

3702.7

6398.0

6042.3

(5196.54

4.1

Total 6993.85 9314.84 10950.7

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 71/86

71

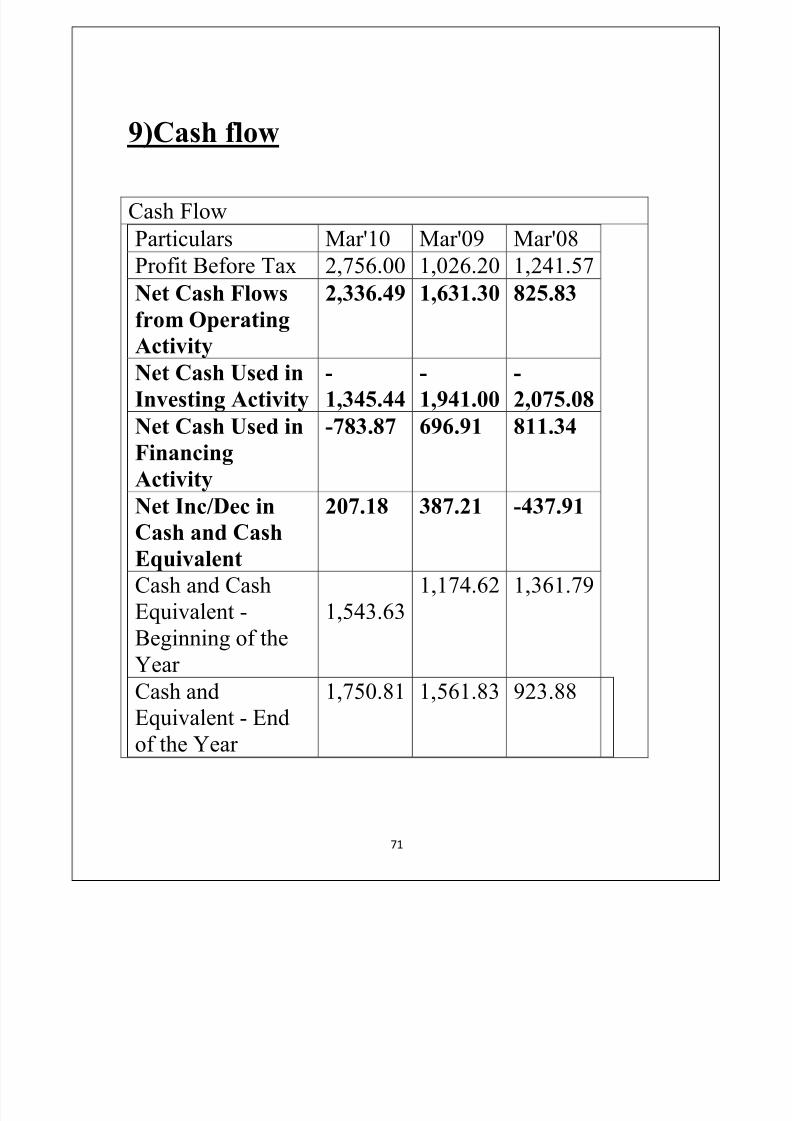

9)Cash flow

Cash Flow

Particulars Mar'10 Mar'09 Mar'08

Profit Before Tax 2,756.00 1,026.20 1,241.57

Net Cash Flows

from Operating

Activity

2,336.49 1,631.30 825.83

Net Cash Used in

Investing Activity

-

1,345.44

-

1,941.00

-

2,075.08

Net Cash Used in

Financing

Activity

-783.87 696.91 811.34

Net Inc/Dec in

Cash and Cash

Equivalent

207.18 387.21 -437.91

Cash and Cash

Equivalent -

Beginning of the

Year

1,543.63

1,174.62 1,361.79

Cash andEquivalent - End

of the Year

1,75

0.81 1,56

1.83 923

.88

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 72/86

72

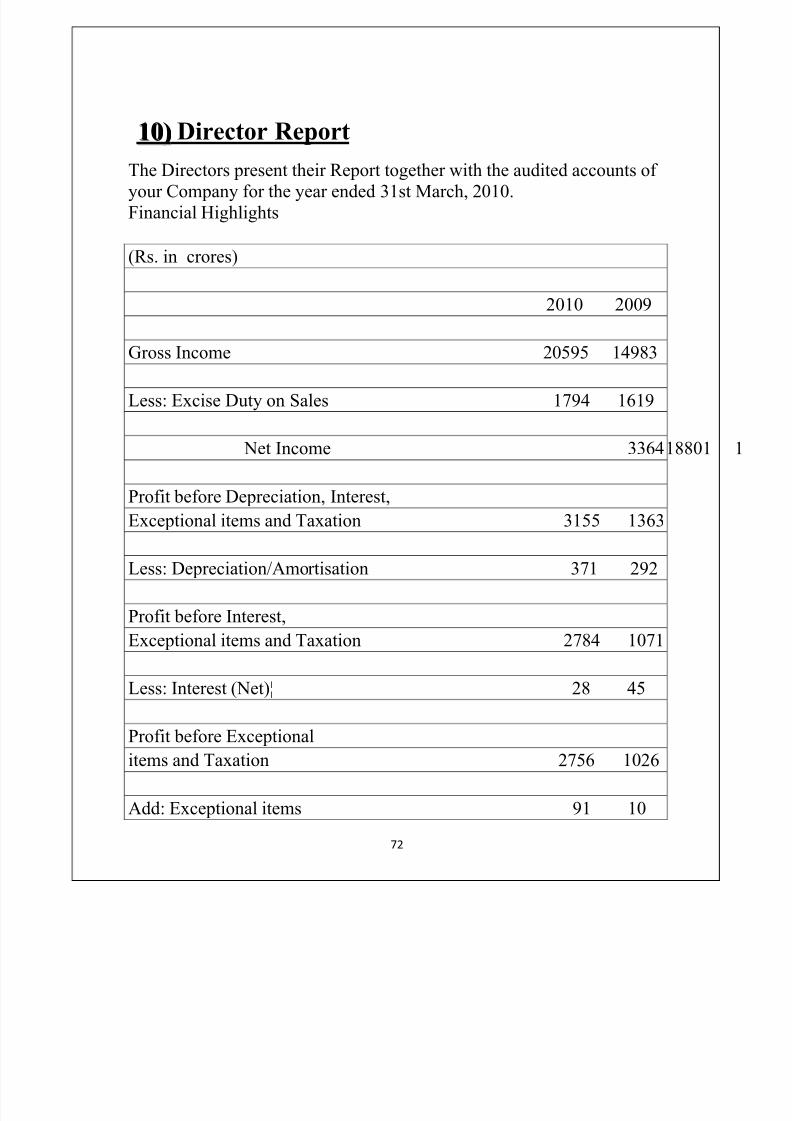

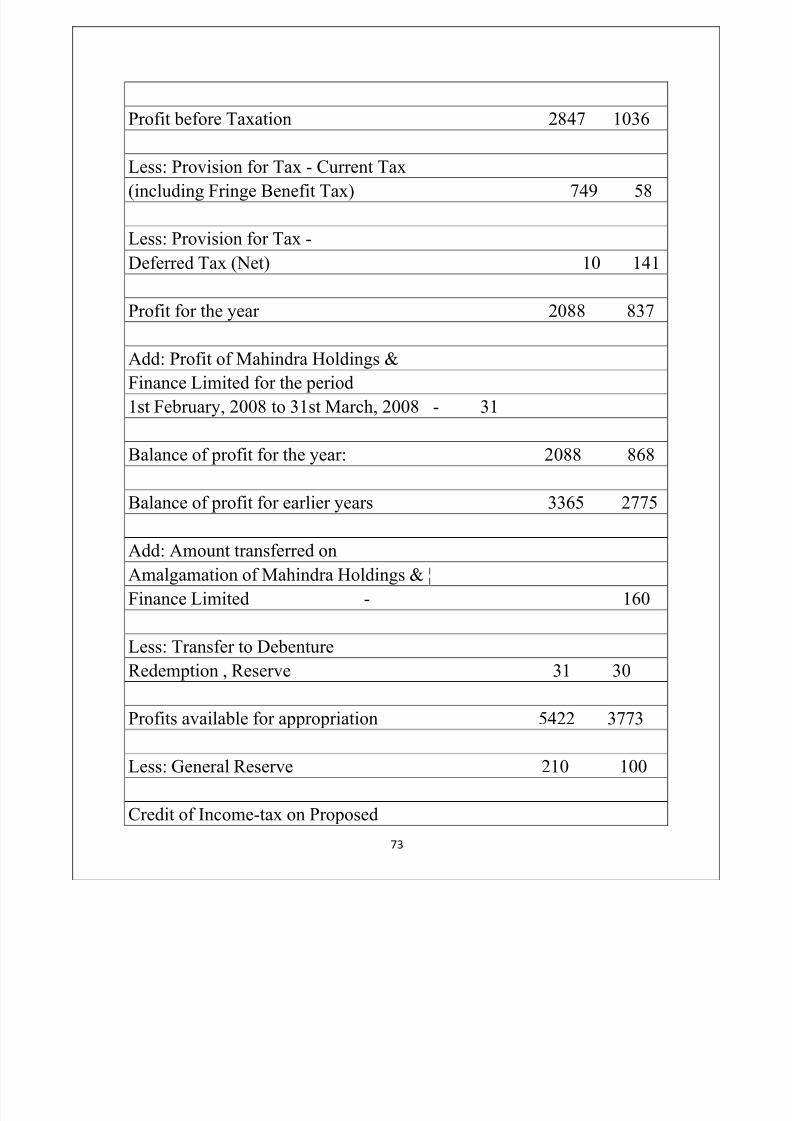

1100)) Director Report

The Directors present their Report together with the audited accounts of your Company for the year ended 31st March, 2010.

Financial Highlights

(Rs. in crores)

2010 2009

Gross Income 20595 14983

Less: Excise Duty on Sales 1794 1619

Net Income 18803364

Profit before Depreciation, Interest,

Exceptional items and Taxation 3155 1363

Less: Depreciation/Amortisation 371 292

Profit before Interest,

Exceptional items and Taxation 2784 1071

Less: Interest (Net)¦ 28 45

Profit before Exceptional

items and Taxation 2756 1026

Add: Exceptional items 91 10

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 73/86

73

Profit before Taxation 2847 1036

Less: Provision for Tax - Current Tax(including Fringe Benefit Tax) 749 58

Less: Provision for Tax -

Deferred Tax (Net) 10 141

Profit for the year 2088 837

Add: Profit of Mahindra Holdings &

Finance Limited for the period

1st February, 2008 to 31st March, 2008 - 31

Balance of profit for the year: 2088 868

Balance of profit for earlier years 3365 2775

Add: Amount transferred on

Amalgamation of Mahindra Holdings & ¦

Finance Limited - 160

Less: Transfer to Debenture

Redemption , Reserve 31 30

Profits available for appropriation 5422 3773

Less: General Reserve 210 100

Credit of Income-tax on Proposed

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 74/86

74

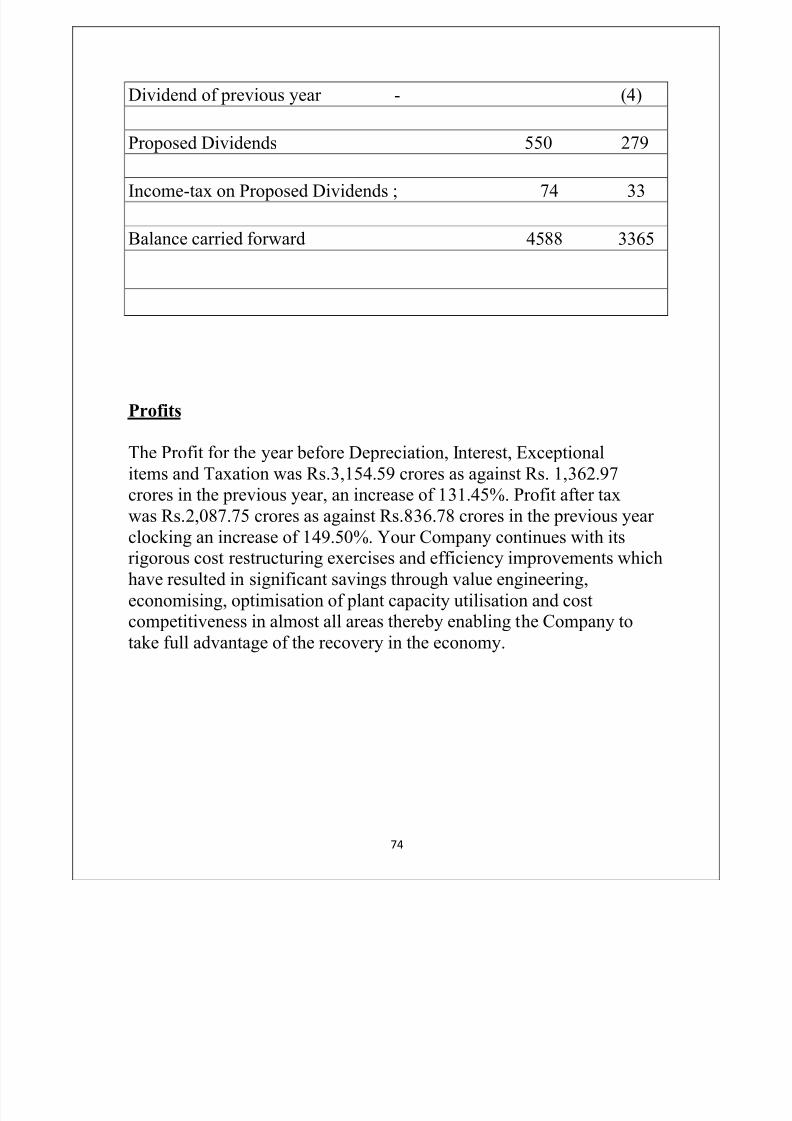

Dividend of previous year - (4)

Proposed Dividends 550 279

Income-tax on Proposed Dividends ; 74 33

Balance carried forward 4588 3365

Profits

The Profit for the year before Depreciation, Interest, Exceptional

items and Taxation was Rs.3,154.59 crores as against Rs. 1,362.97

crores in the previous year, an increase of 131.45%. Profit after tax

was Rs.2,087.75 crores as against Rs.836.78 crores in the previous year

clocking an increase of 149.50%. Your Company continues with itsrigorous cost restructuring exercises and efficiency improvements which

have resulted in significant savings through value engineering,

economising, optimisation of plant capacity utilisation and costcompetitiveness in almost all areas thereby enabling the Company to

take full advantage of the recovery in the economy.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 75/86

75

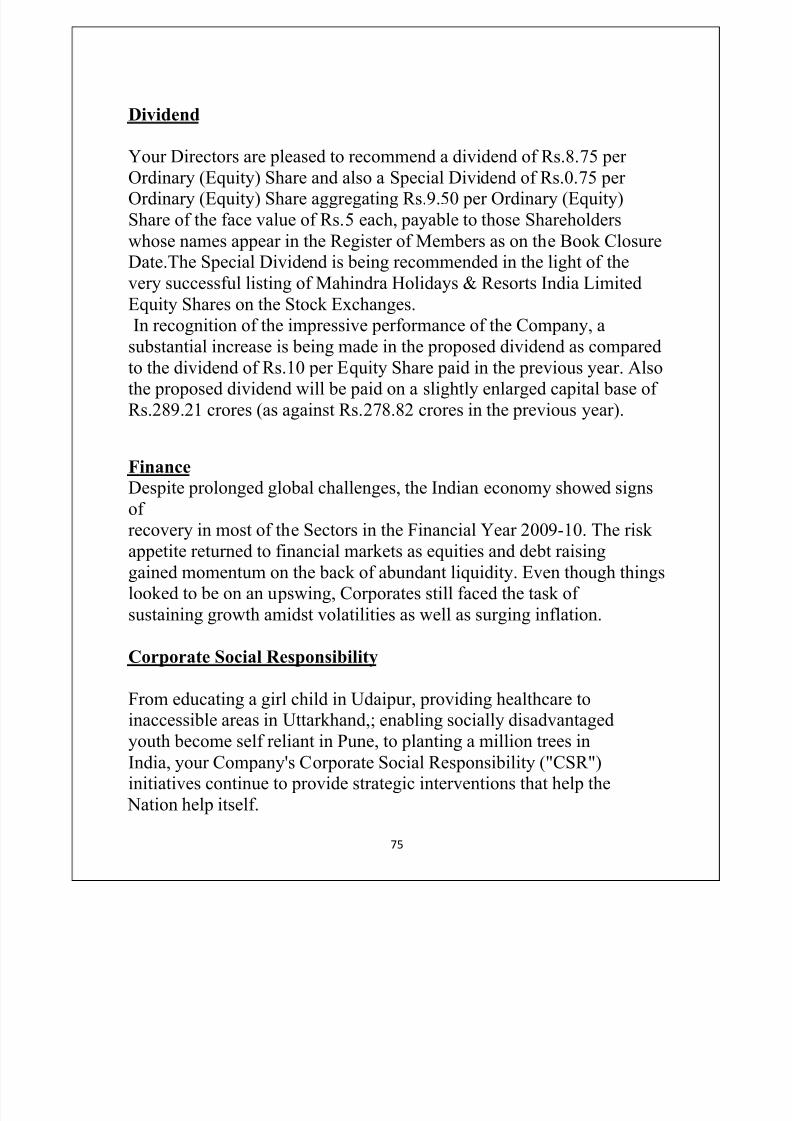

Dividend

Your Directors are pleased to recommend a dividend of Rs.8.75 per

Ordinary (Equity) Share and also a Special Dividend of Rs.0.75 per Ordinary (Equity) Share aggregating Rs.9.50 per Ordinary (Equity)

Share of the face value of Rs.5 each, payable to those Shareholders

whose names appear in the Register of Members as on the Book ClosureDate.The Special Dividend is being recommended in the light of the

very successful listing of Mahindra Holidays & Resorts India Limited

Equity Shares on the Stock Exchanges.

In recognition of the impressive performance of the Company, a

substantial increase is being made in the proposed dividend as comparedto the dividend of Rs.10 per Equity Share paid in the previous year. Also

the proposed dividend will be paid on a slightly enlarged capital base of

Rs.289.21 crores (as against Rs.278.82 crores in the previous year).

Finance

Despite prolonged global challenges, the Indian economy showed signs

of

recovery in most of the Sectors in the Financial Year 2009-10. The risk appetite returned to financial markets as equities and debt raising

gained momentum on the back of abundant liquidity. Even though things

looked to be on an upswing, Corporates still faced the task of

sustaining growth amidst volatilities as well as surging inflation.

Corporate Social Responsibility

From educating a girl child in Udaipur, providing healthcare toinaccessible areas in Uttarkhand,; enabling socially disadvantaged

youth become self reliant in Pune, to planting a million trees in

India, your Company's Corporate Social Responsibility ("CSR")initiatives continue to provide strategic interventions that help the

Nation help itself.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 76/86

76

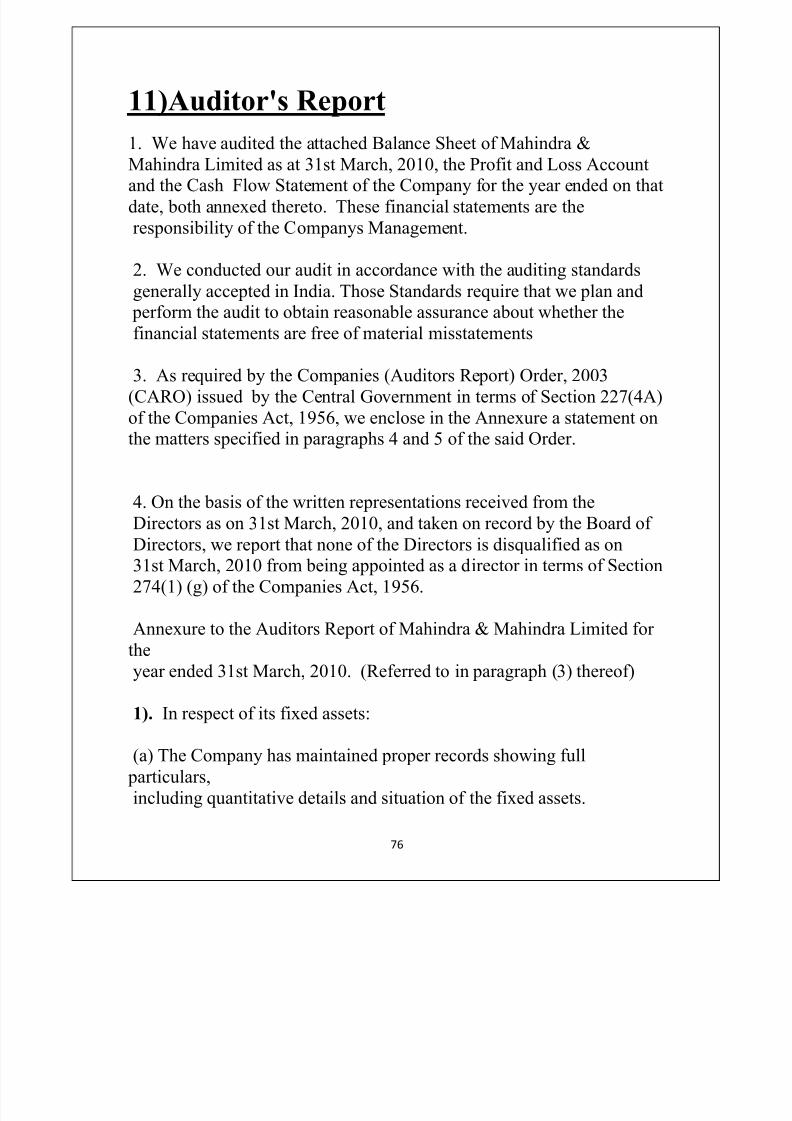

11)Auditor's Report

1. We have audited the attached Balance Sheet of Mahindra &

Mahindra Limited as at 31st March, 2010, the Profit and Loss Accountand the Cash Flow Statement of the Company for the year ended on that

date, both annexed thereto. These financial statements are the

responsibility of the Companys Management.

2. We conducted our audit in accordance with the auditing standards

generally accepted in India. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the

financial statements are free of material misstatements

3. As required by the Companies (Auditors Report) Order, 2003

(CARO) issued by the Central Government in terms of Section 227(4A)

of the Companies Act, 1956, we enclose in the Annexure a statement onthe matters specified in paragraphs 4 and 5 of the said Order.

4. On the basis of the written representations received from the

Directors as on 31st March, 2010, and taken on record by the Board of Directors, we report that none of the Directors is disqualified as on

31st March, 2010 from being appointed as a director in terms of Section

274(1) (g) of the Companies Act, 1956.

Annexure to the Auditors Report of Mahindra & Mahindra Limited for

the

year ended 31st March, 2010. (Referred to in paragraph (3) thereof)

1). In respect of its fixed assets:

(a) The Company has maintained proper records showing full

particulars,

including quantitative details and situation of the fixed assets.

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 77/86

77

(b) The fixed assets disposed off during the year, in our opinion, donot constitute a substantial part of the fixed assets of the Company

and such disposal has, in our opinion, not affected the going concern

status of the Company.

2). In respect of its inventory:

(a) As explained to us, the inventories were physically verified during

the year by the Management at reasonable intervals.

(b) In our opinion and according to the information and explanation

given to us, the procedures of physical verification of inventoriesfollowed by the Management were reasonable and adequate in relation

to the size of the Company and the nature of its business.

3). The Company has neither granted nor taken any loans, secured or

unsecured, to/from companies, firms or other parties listed in the

Register maintained under Section 301 of the Companies Act, 1956.

4). In respect of contracts or arrangements entered in the Register maintained in pursuance of Section 301 of the Companies Act, 1956, to

the best of our knowledge and belief and according to the information

and explanations given to us:

(a) The particulars of contracts or arrangements referred to Section

301 that needed to be entered in the Register maintained under the said

Section have been so entered.

(b) Where each of such transaction is in excess of Rs.5 lakhs in

respect of any party, having regard to the explanations that some of

the items purchased are of special nature and suitable alternative

sources are not readily available for obtaining comparable quotations,

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 78/86

78

the transactions have been mad at prices which are prima facie

reasonable having regard to the prevailing market prices at therelevant time.

5). In our opinion, the Company has an adequate internal audit systemcommensurate with the size and the nature of its business.

6). We have broadly reviewed the books of account maintained by theCompany pursuant to the rules made by the Central Government for the

maintenance of cost records under Section 209(1) (d) of the Companies

Act, 1956 in respect of manufacture of motor vehicles and tractors and

are of the opinion that prima facie the prescribed accounts and records

have been made and maintained.

7). According to the information and explanations given to us in

respect of statutory dues:

(a) The Company has generally been regular in depositing undisputed

dues, including Provident Fund, Investor Education and Protection

Fund, Employees State Insurance, Income-tax, Sales Tax, Wealth Tax,Service Tax, Value Added Tax, Customs Duty, Excise Duty, Cess and

other material statutory dues applicable to it with the appropriate

authorities.

(b) There were no undisputed amounts payable in respect of Income-

tax, Wealth Tax, Customs Duty, Excise Duty, Cess and other material

statutory dues in arrears as at 31st March, 2010 for a period of more

than six months from the date they became payable.

Significant Accounting Policies

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 79/86

79

ACCOUNTING CONVENTION.

The financial statements are prepared under the historical cost

convention, on an accrual basis, in accordance with generally

accepted accounting principles and applicable accounting standards

as notified under the Companies Rules 2006.

USE OF ESTIMATES

The preparation and presentation of financial starements in

conformity with generally accepted accounting principles requires

making of estimates and assumptions that affect the reported amounts

of assets and liabilities and disclosures of contingent assets and

liabilities at the date of the financial statements and the reportedamounts of revenues and expenses during the reporting year.

Differences between the actual results and estimates are recognized in

the year in which the results are known/materialized.

REVENUE RECOGNITION

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 80/86

80

Sale of products are recognized when risk and rewards of ownership

of the products are passed onto the customers, which is generally on

the dispatch of goods. Sales are exclusive of sales tax. License Fee is

accounted based on terms of contract. Interest income is recognizedon time proportion basis.

FIXED ASSETS AND DEPR ICIATION/ AMOR TIZATION

Fixed assets are stated at cost of acquisition less accumulated

depreciation and impairment, if any. Cost is inclusive of freight,

duties, taxes and other directly attributable cost incurred to bring the

assets their working condition for intended use. Depreciation is

charged using straight-line method based on the useful lives of the

fixed assets as estimated by the management as specified below or the

rates specified in accordance with the provisions of Schedule XIV of

the Companies Act 1956 whichever is higher.

Buildings - 20 to 30 years

Plant & Machinery- 5-18 years

Furniture & Fixtures- 10-15 years

Office equipments- 1-5 years

Moulds & Dyes - 1-3 years

Vehicles - 4-8 years

Depreciation is charged on a pro-rata basis for assets purchased/sold

during the year. Individual fixed assets costing less than ` 5000 are

8/8/2019 Proj of Fm Final

http://slidepdf.com/reader/full/proj-of-fm-final 81/86

81

depreciated in full, in the year of purchase. Cost of lease hold land is

amortized over the period of the lease or management estimates

whichever is lower.

INVENTOR IES

Inventories consist of raw and packing materials, stores and spares, work

in progress and finished goods. Inventories are valued at lower of cost

and net realizable value. Cost of Inventories is determined on weighted

average basis.

BORROWING COST