PROGRAM FLOATING YOUR BOAT FACING THE...

18

PROGRAM - FLOATING YOUR BOAT - FACING THE PRACTICAL ISSUES OF RECREATIONAL BOAT FINANCING AND RECOVERY

-

Upload

phungkhanh -

Category

Documents

-

view

216 -

download

0

Transcript of PROGRAM FLOATING YOUR BOAT FACING THE...

PROGRAM - FLOATING YOUR BOAT - FACING THE PRACTICAL ISSUES OF RECREATIONAL BOAT

FINANCING AND RECOVERY

C:\Documents and Settings\scleckle\Desktop\Winter Meeting 2011\(11) Personal Property\ABA Winter Personal Property Fin Cover.DOC

American Bar Association

Committee on Consumer Financial Services Personal Property Financing Subcommittee

Winter Meeting – Naples, Florida January 2011

Personal Property Financing Subcommittee Chair: Robert Aitken, Ford Motor Credit Company, Dearborn, MI Vice Chair: Douglas Johnson, Americredit Corp., Fort Worth, TX Vice Chair: Deborah Robertson, McGlinchey Stafford, Albany, NY

Presentation: Floating Your Boat - Facing the practical issues of recreational boat financing and recovery.

We will examine the legal issues presented in the financing and perfection of security interests in personal use boats and their associated equipment. In addition, the unique challenges of watercraft recovery and subsequent sale will be examined.

Speakers:

James Y. Stewart, Kotz, Sangster, Wysocki & Berg, P.C, Birmingham, MI

Ken Cage, International Recovery and Remarketing Group, Orlando, FL

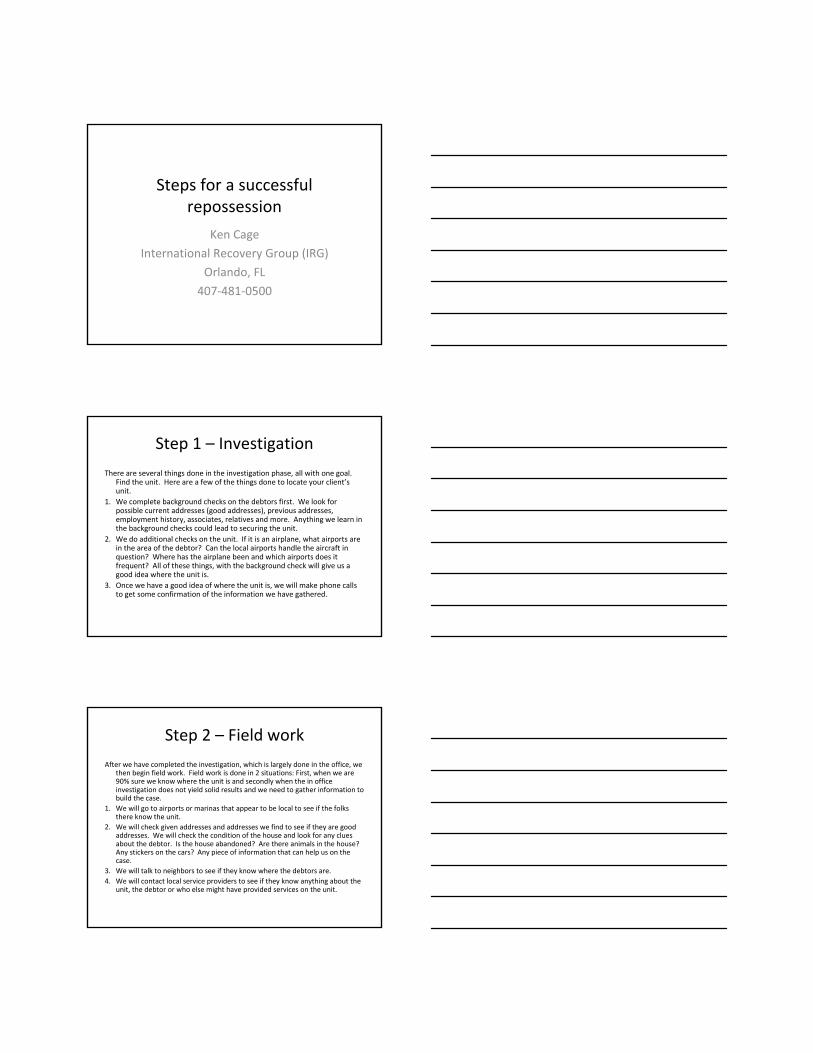

Steps for a successful repossession

Ken Cage

International Recovery Group (IRG)

Orlando, FL

407‐481‐0500

Step 1 – Investigation

There are several things done in the investigation phase, all with one goal. Find the unit. Here are a few of the things done to locate your client’s unit.

1. We complete background checks on the debtors first. We look forpossible current addresses (good addresses), previous addresses,employment history, associates, relatives and more. Anything we learn in the background checks could lead to securing the unit.

2. We do additional checks on the unit. If it is an airplane, what airports are in the area of the debtor? Can the local airports handle the aircraft in question? Where has the airplane been and which airports does it frequent? All of these things, with the background check will give us a good idea where the unit is.

3. Once we have a good idea of where the unit is, we will make phone calls to get some confirmation of the information we have gathered.

Step 2 – Field work

After we have completed the investigation, which is largely done in the office, we then begin field work. Field work is done in 2 situations: First, when we are 90% sure we know where the unit is and secondly when the in office investigation does not yield solid results and we need to gather information to build the case.

1. We will go to airports or marinas that appear to be local to see if the folks there know the unit.

2. We will check given addresses and addresses we find to see if they are good addresses. We will check the condition of the house and look for any clues about the debtor. Is the house abandoned? Are there animals in the house? Any stickers on the cars? Any piece of information that can help us on the case.

3. We will talk to neighbors to see if they know where the debtors are.4. We will contact local service providers to see if they know anything about the

unit, the debtor or who else might have provided services on the unit.

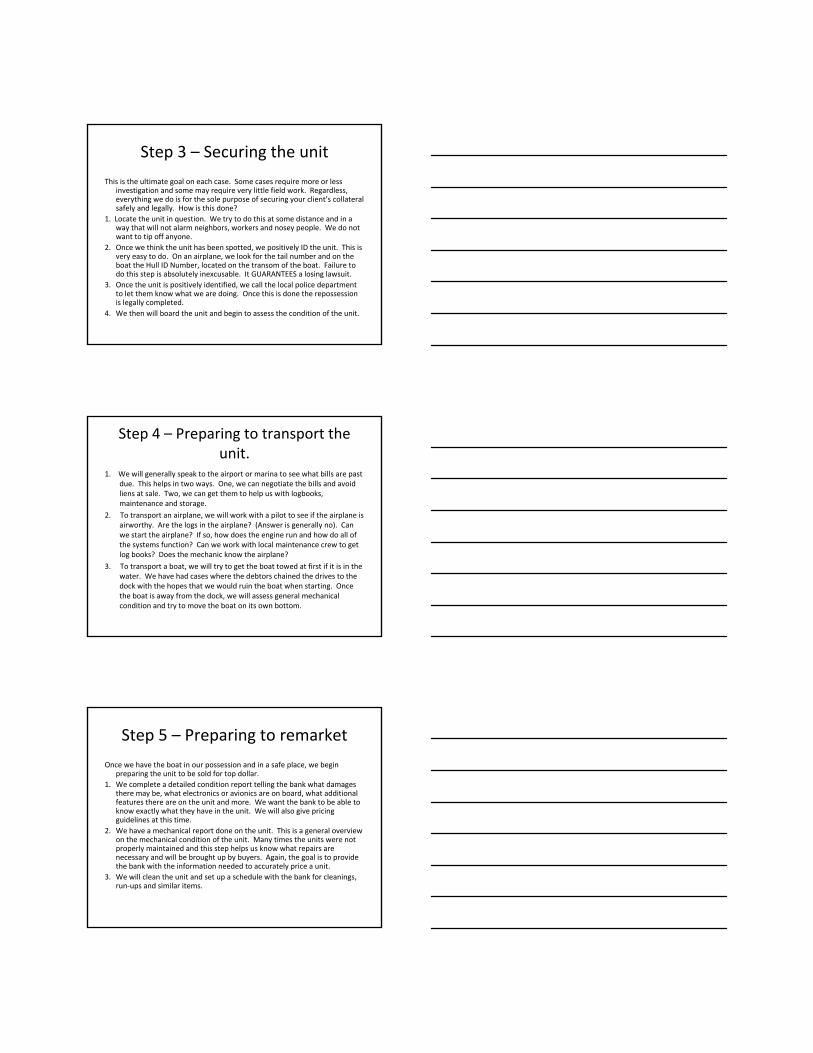

Step 3 – Securing the unit

This is the ultimate goal on each case. Some cases require more or less investigation and some may require very little field work. Regardless, everything we do is for the sole purpose of securing your client’s collateral safely and legally. How is this done?

1. Locate the unit in question. We try to do this at some distance and in a way that will not alarm neighbors, workers and nosey people. We do not want to tip off anyone.

2. Once we think the unit has been spotted, we positively ID the unit. This is very easy to do. On an airplane, we look for the tail number and on the boat the Hull ID Number, located on the transom of the boat. Failure to do this step is absolutely inexcusable. It GUARANTEES a losing lawsuit.

3. Once the unit is positively identified, we call the local police department to let them know what we are doing. Once this is done the repossession is legally completed.

4. We then will board the unit and begin to assess the condition of the unit.

Step 4 – Preparing to transport the unit.

1. We will generally speak to the airport or marina to see what bills are past due. This helps in two ways. One, we can negotiate the bills and avoid liens at sale. Two, we can get them to help us with logbooks, maintenance and storage.

2. To transport an airplane, we will work with a pilot to see if the airplane is airworthy. Are the logs in the airplane? (Answer is generally no). Can we start the airplane? If so, how does the engine run and how do all of the systems function? Can we work with local maintenance crew to get log books? Does the mechanic know the airplane?

3. To transport a boat, we will try to get the boat towed at first if it is in the water. We have had cases where the debtors chained the drives to the dock with the hopes that we would ruin the boat when starting. Once the boat is away from the dock, we will assess general mechanical condition and try to move the boat on its own bottom.

Step 5 – Preparing to remarket

Once we have the boat in our possession and in a safe place, we begin preparing the unit to be sold for top dollar.

1. We complete a detailed condition report telling the bank what damages there may be, what electronics or avionics are on board, what additional features there are on the unit and more. We want the bank to be able to know exactly what they have in the unit. We will also give pricing guidelines at this time.

2. We have a mechanical report done on the unit. This is a general overview on the mechanical condition of the unit. Many times the units were not properly maintained and this step helps us know what repairs arenecessary and will be brought up by buyers. Again, the goal is to provide the bank with the information needed to accurately price a unit.

3. We will clean the unit and set up a schedule with the bank for cleanings, run‐ups and similar items.

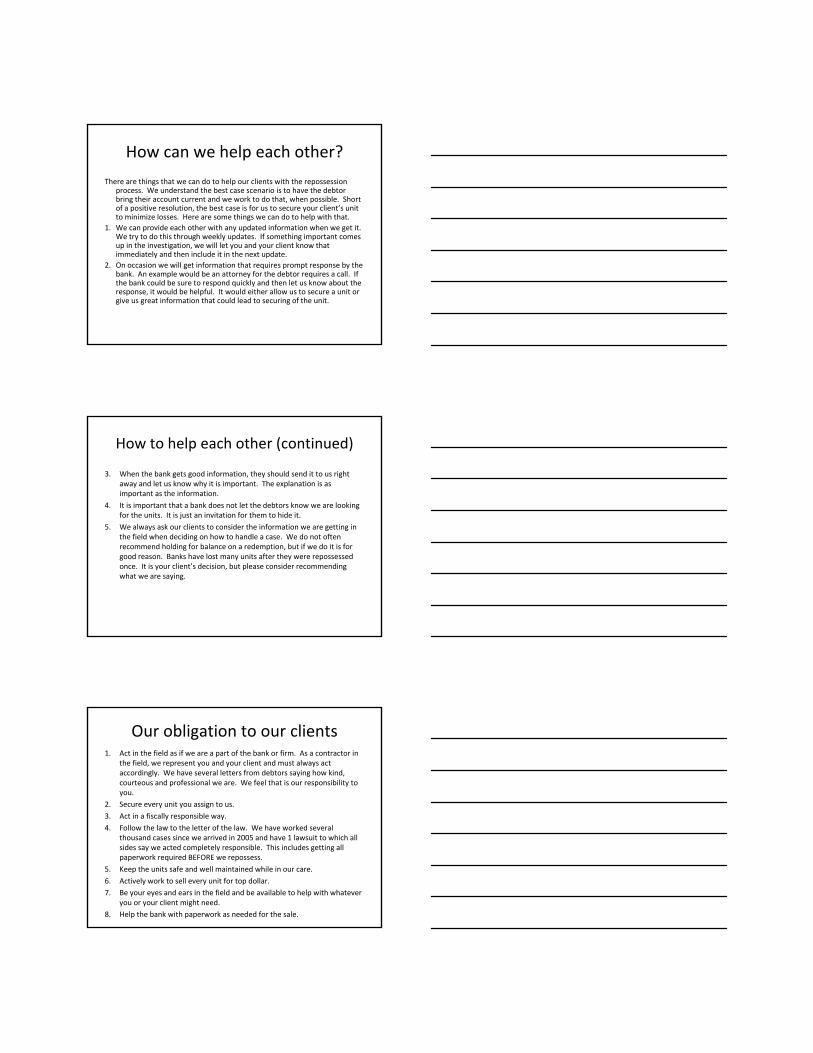

How can we help each other?

There are things that we can do to help our clients with the repossession process. We understand the best case scenario is to have the debtor bring their account current and we work to do that, when possible. Short of a positive resolution, the best case is for us to secure your client’s unit to minimize losses. Here are some things we can do to help with that.

1. We can provide each other with any updated information when we get it. We try to do this through weekly updates. If something important comes up in the investigation, we will let you and your client know that immediately and then include it in the next update.

2. On occasion we will get information that requires prompt response by the bank. An example would be an attorney for the debtor requires a call. If the bank could be sure to respond quickly and then let us know about the response, it would be helpful. It would either allow us to secure a unit or give us great information that could lead to securing of the unit.

How to help each other (continued)

3. When the bank gets good information, they should send it to us right away and let us know why it is important. The explanation is asimportant as the information.

4. It is important that a bank does not let the debtors know we are looking for the units. It is just an invitation for them to hide it.

5. We always ask our clients to consider the information we are getting in the field when deciding on how to handle a case. We do not often recommend holding for balance on a redemption, but if we do it is for good reason. Banks have lost many units after they were repossessed once. It is your client’s decision, but please consider recommending what we are saying.

Our obligation to our clients1. Act in the field as if we are a part of the bank or firm. As a contractor in

the field, we represent you and your client and must always act accordingly. We have several letters from debtors saying how kind, courteous and professional we are. We feel that is our responsibility to you.

2. Secure every unit you assign to us.

3. Act in a fiscally responsible way.

4. Follow the law to the letter of the law. We have worked severalthousand cases since we arrived in 2005 and have 1 lawsuit to which all sides say we acted completely responsible. This includes getting all paperwork required BEFORE we repossess.

5. Keep the units safe and well maintained while in our care.

6. Actively work to sell every unit for top dollar.7. Be your eyes and ears in the field and be available to help with whatever

you or your client might need.8. Help the bank with paperwork as needed for the sale.

Conclusion

In conclusion, please consider repossession as an alternative for airplanes, boats and other specialty assets. It is an efficient and cost effective alternative to consider.

1/13/2011

1

American Bar Association American Bar Association Consumer Financial Services Committee MeetingConsumer Financial Services Committee MeetingJanuary 10, 2011January 10, 2011LaPlaya Beach & Golf ResortLaPlaya Beach & Golf ResortNaples, FloridaNaples, Florida

By: James Y. Stewart

I. Recreational Boating HistoryYacht

Pleasure onlyGenerally over 30 feetS ll l ll f d bSmaller vessels are usually referred to as boats

I. Recreational Boating History Yacht Financing

Prior to 1960 very limitedAdditional collateral Unsecured basisUnsecured basis

During 1960’s and 1970’s specialized yacht financing divisions beganState titling laws passedBegan utilizing federal system

1/13/2011

2

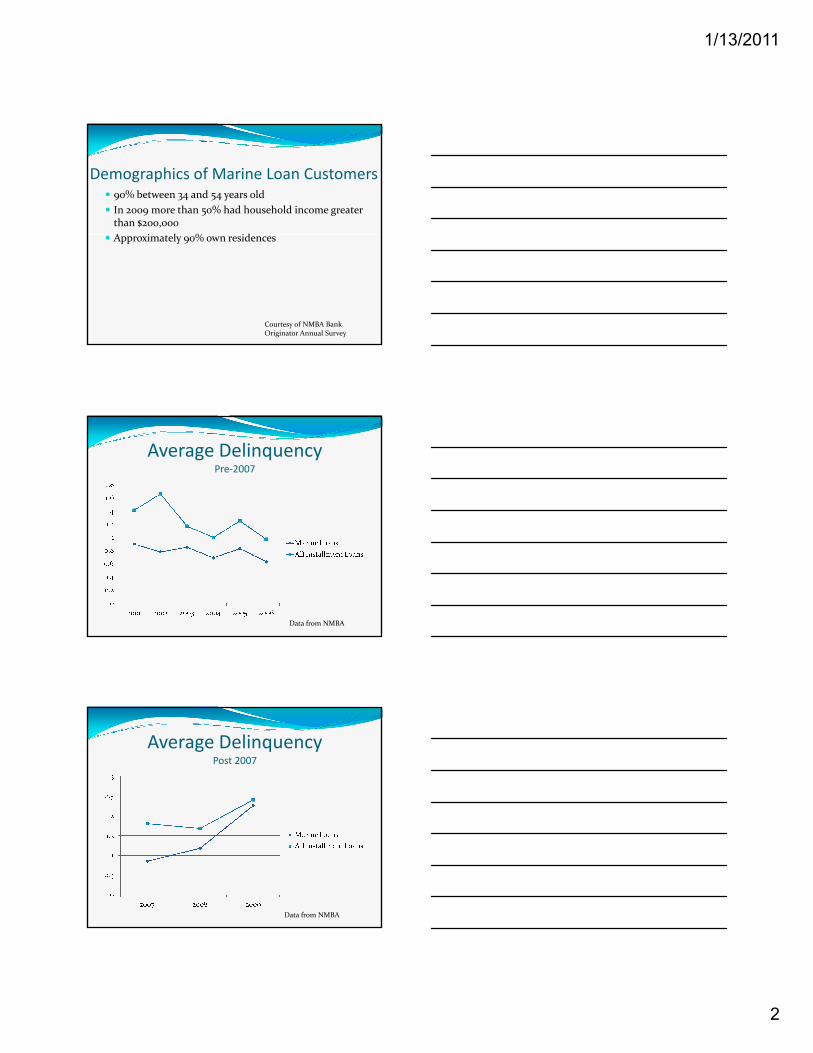

Demographics of Marine Loan Customers 90% between 34 and 54 years oldIn 2009 more than 50% had household income greater than $200,000A i l % id Approximately 90% own residences

Courtesy of NMBA Bank Originator Annual Survey

Average DelinquencyPre‐2007

Data from NMBA

Average DelinquencyPost 2007

Data from NMBA

1/13/2011

3

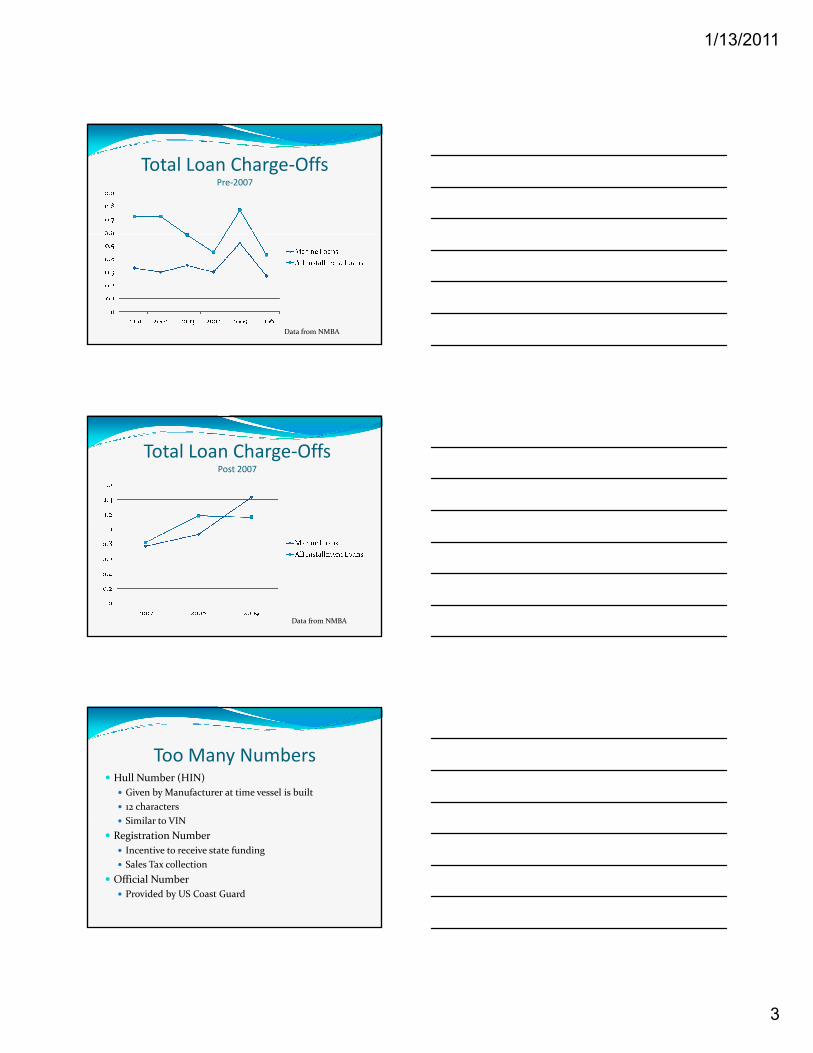

Total Loan Charge‐OffsPre‐2007

Data from NMBA

Total Loan Charge‐OffsPost 2007

Data from NMBA

Too Many NumbersHull Number (HIN)

Given by Manufacturer at time vessel is built12 characters Si il VINSimilar to VIN

Registration NumberIncentive to receive state fundingSales Tax collection

Official NumberProvided by US Coast Guard

1/13/2011

4

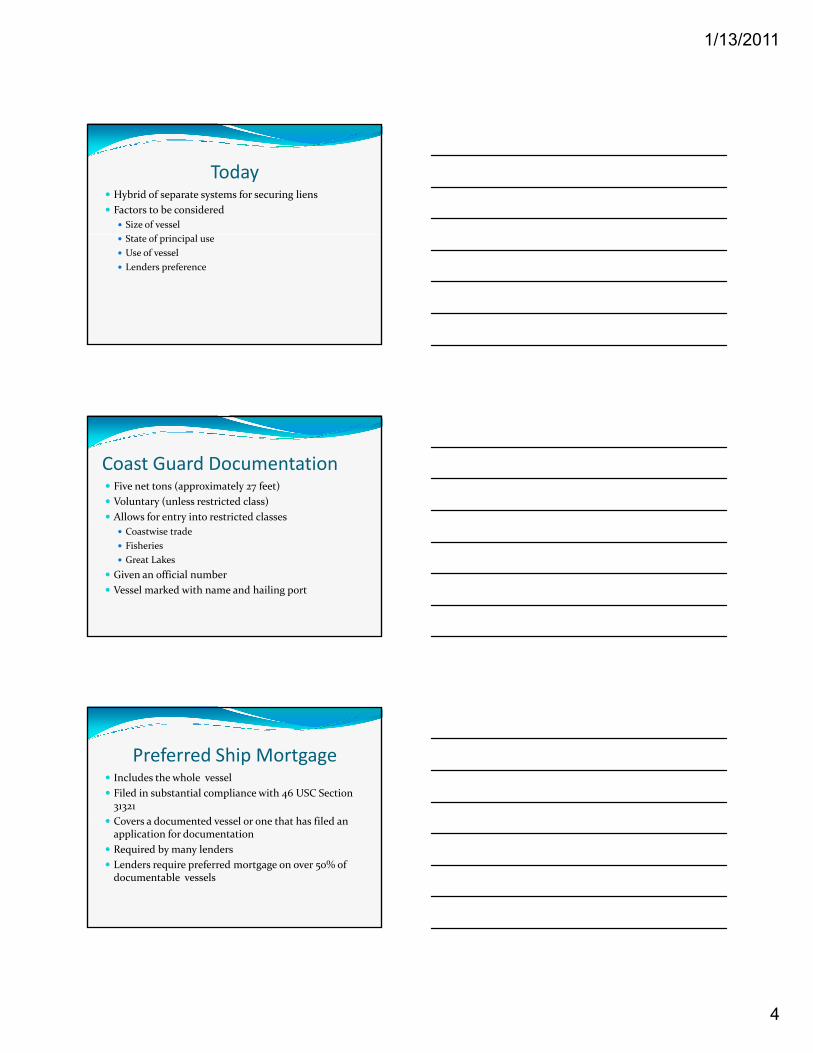

TodayHybrid of separate systems for securing liens Factors to be considered

Size of vesselState of principal useUse of vesselLenders preference

Coast Guard DocumentationFive net tons (approximately 27 feet)Voluntary (unless restricted class)Allows for entry into restricted classes

Coastwise tradeFisheriesGreat Lakes

Given an official numberVessel marked with name and hailing port

Preferred Ship MortgageIncludes the whole vesselFiled in substantial compliance with 46 USC Section 31321C d d l h h fil d Covers a documented vessel or one that has filed an application for documentationRequired by many lendersLenders require preferred mortgage on over 50% of documentable vessels

1/13/2011

5

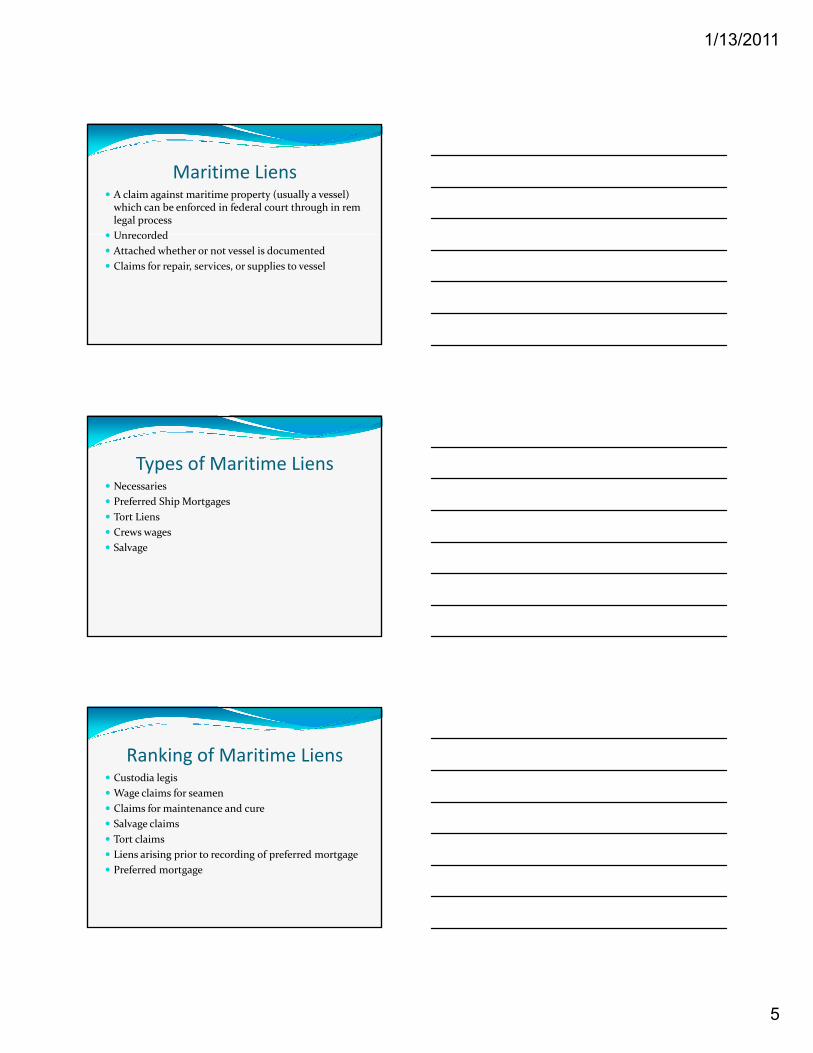

Maritime LiensA claim against maritime property (usually a vessel) which can be enforced in federal court through in rem legal process UnrecordedUnrecordedAttached whether or not vessel is documentedClaims for repair, services, or supplies to vessel

Types of Maritime LiensNecessariesPreferred Ship MortgagesTort LiensCrews wagesSalvage

Ranking of Maritime LiensCustodia legisWage claims for seamenClaims for maintenance and cureSalvage claimsTort claimsLiens arising prior to recording of preferred mortgagePreferred mortgage

1/13/2011

6

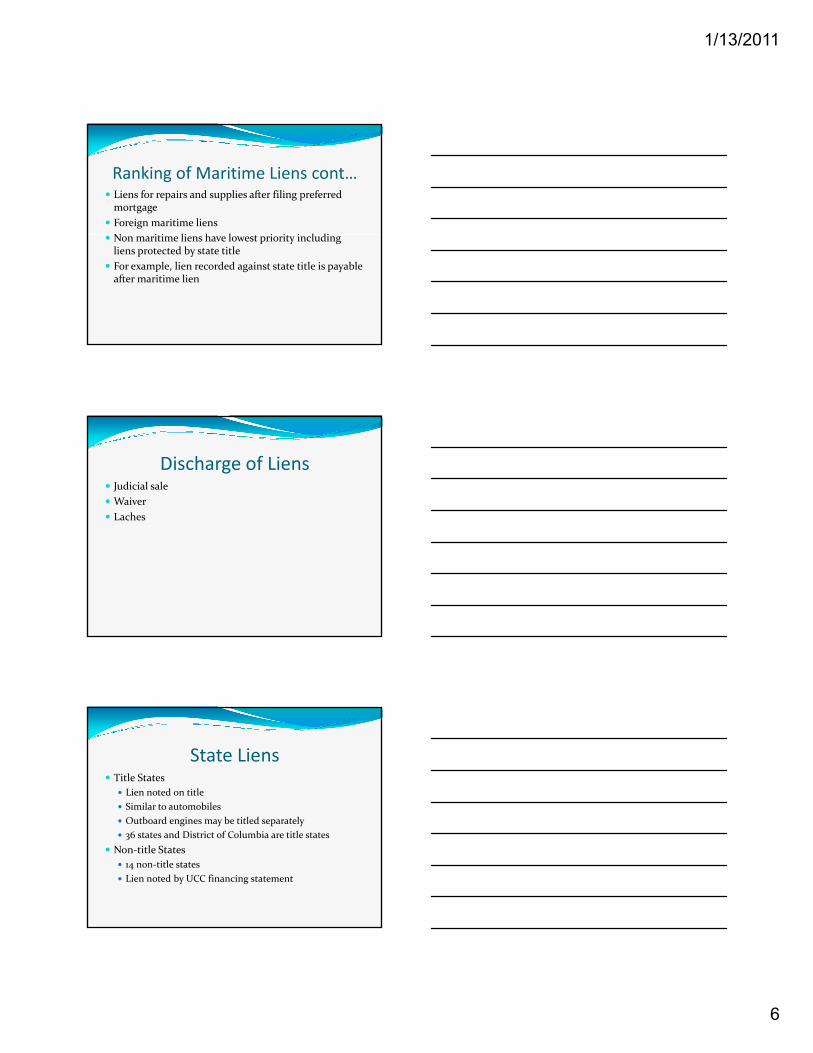

Ranking of Maritime Liens cont…Liens for repairs and supplies after filing preferred mortgageForeign maritime liensN i i li h l i i i l di Non maritime liens have lowest priority including liens protected by state titleFor example, lien recorded against state title is payable after maritime lien

Discharge of LiensJudicial saleWaiverLaches

State LiensTitle States

Lien noted on titleSimilar to automobiles O b d i b i l d l Outboard engines may be titled separately 36 states and District of Columbia are title states

Non‐title States14 non‐title statesLien noted by UCC financing statement

1/13/2011

7

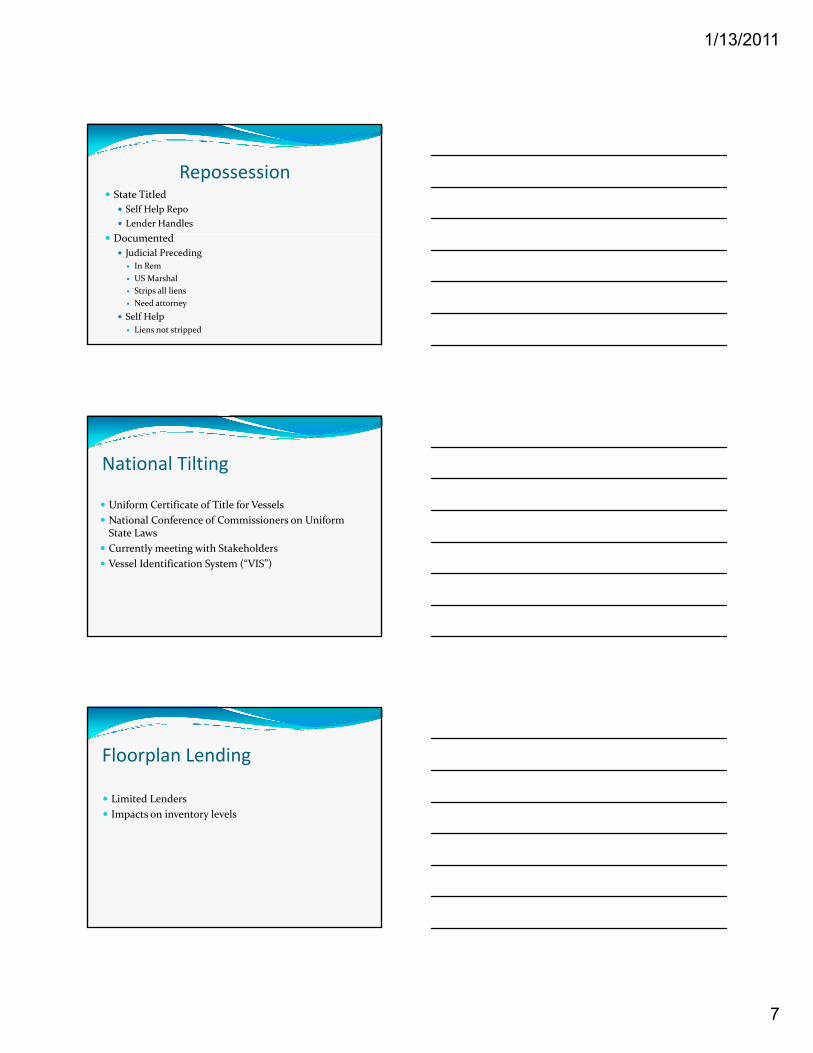

RepossessionState Titled

Self Help RepoLender Handles

D d Documented Judicial Preceding

In RemUS MarshalStrips all liensNeed attorney

Self HelpLiens not stripped

National Tilting

Uniform Certificate of Title for VesselsNational Conference of Commissioners on Uniform State LawsCurrently meeting with StakeholdersVessel Identification System (“VIS”)

Floorplan Lending

Limited LendersImpacts on inventory levelsp y

1/13/2011

8

James Y. StewartKotz Sangster Wysocki and Berg, PC300 Park Avenue, Suite 265Birmingham, Michigan 48009

C:\Documents and Settings\scleckle\Desktop\Winter Meeting 2011\(11) Personal Property\Personal Prop Bios.doc

James Y. Stewart Kotz, Sangster, Wysocki and Berg, P.C Birmingham, Michigan Mr. Stewart is a shareholder at Kotz Sangster. His practice areas include general corporate and business law; formation of corporations and joint ventures; mergers and acquisitions; contracts; shareholder agreements; commercial law; and real estate. He has more than twenty-five years of experience in recreational boating and maritime law. Mr. Stewart is specifically experienced in yacht financing, vessel documentation and the foreclosure of maritime liens. He has vast experience in the perfection and collection of maritime liens including preferred ships mortgages. Mr. Stewart is a frequent speaker on issues relating to recreational boating and maritime lending. He serves as general counsel to the Michigan Boating Industries Association and the National Marine Bankers Association.

C:\Documents and Settings\scleckle\Desktop\Winter Meeting 2011\(11) Personal Property\Personal Prop Bios.doc

Ken Cage President of Operations International Recovery and Remarketing Group

Ken has 20+ years in the banking and collections industry with prestigious firms such as JP Morgan and DaimlerChrysler Financial Services and has vast experience in skip tracing and investigation within the finance sector. This experience allows Ken to understand the needs of banking, financial and legal clientele while utilizing his investigation and recovery skills to provide the highest quality service.

Since joining IRG in 2005, Ken has been involved in thousands of repossessions and investigations on all types of specialty assets. Ken has repossessed units in all 50 states, as well as several foreign countries. Ken has been a guest speaker for the International Superyacht Society and been the focus of many news stories for newspaper, magazines and television all over the world. Ken is a licensed Repossession Agent, Private Investigator and Yacht Broker.

Ken has been a member of many organizations related to the investigation field including American Society of Industrial Security, the International Society of Healthcare Safety and Security, the National Association of Chiefs of Police, Aircraft Owners & Pilots Association (AOPA), National Aircraft Finance Association (NAFA), International Association of Marine Investigators (IAMI) and the National Marine Banking Association