Bespoke Digital Media: Strategies on How to Become a Creative and Profitable Online Presence!

Profitable growth strategies for the next 4 billionLearning from Indian Innovations

www.pwc.com

CFO Conclave24-26 November 2011

Content

• Growth Horizon (s)

• Emerging Middle

• Research Profitable Growth Strategies

- Growth

PwC

- Profit

- Mindset

• Financial Approach

• Relevance for you

Slide 2November 2011CFO Conclave

Growth Horizon(s)

PwCNovember 2011CFO Conclave

Slide 3

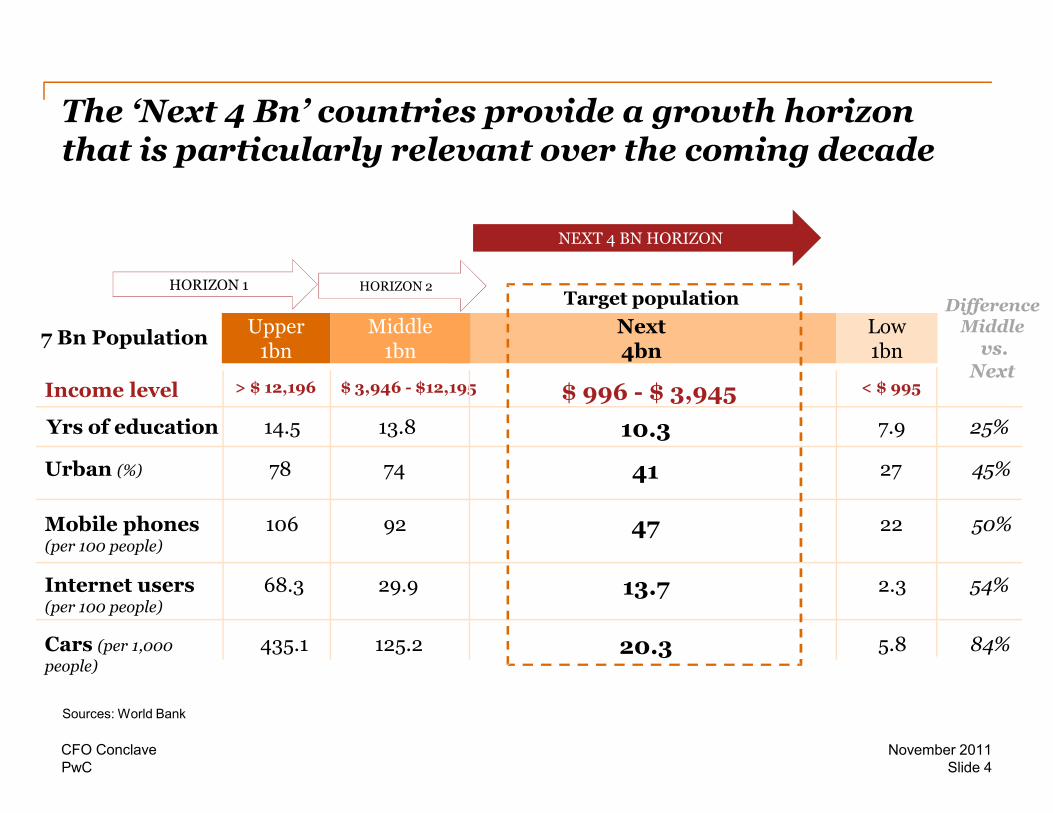

The ‘Next 4 Bn’ countries provide a growth horizon that is particularly relevant over the coming decade

Target population

NEXT 4 BN HORIZON

HORIZON 1 HORIZON 2

Upper 1bn

Next4bn

Low 1bn

7 Bn Population

Income level > $ 12,196 $ 3,946 - $12,195 $ 996 - $ 3,945 < $ 995

Middle 1bn

DifferenceMiddle

vs. Next

PwC

Sources: World Bank

Yrs of education 14.5 13.8 10.3 7.9

Urban (%) 78 74 41 27

Mobile phones (per 100 people)

106 92 47 22

Internet users (per 100 people)

68.3 29.9 13.7 2.3

Cars (per 1,000 people)

435.1 125.2 20.3 5.8

25%

45%

50%

54%

84%

November 2011Slide 4

CFO Conclave

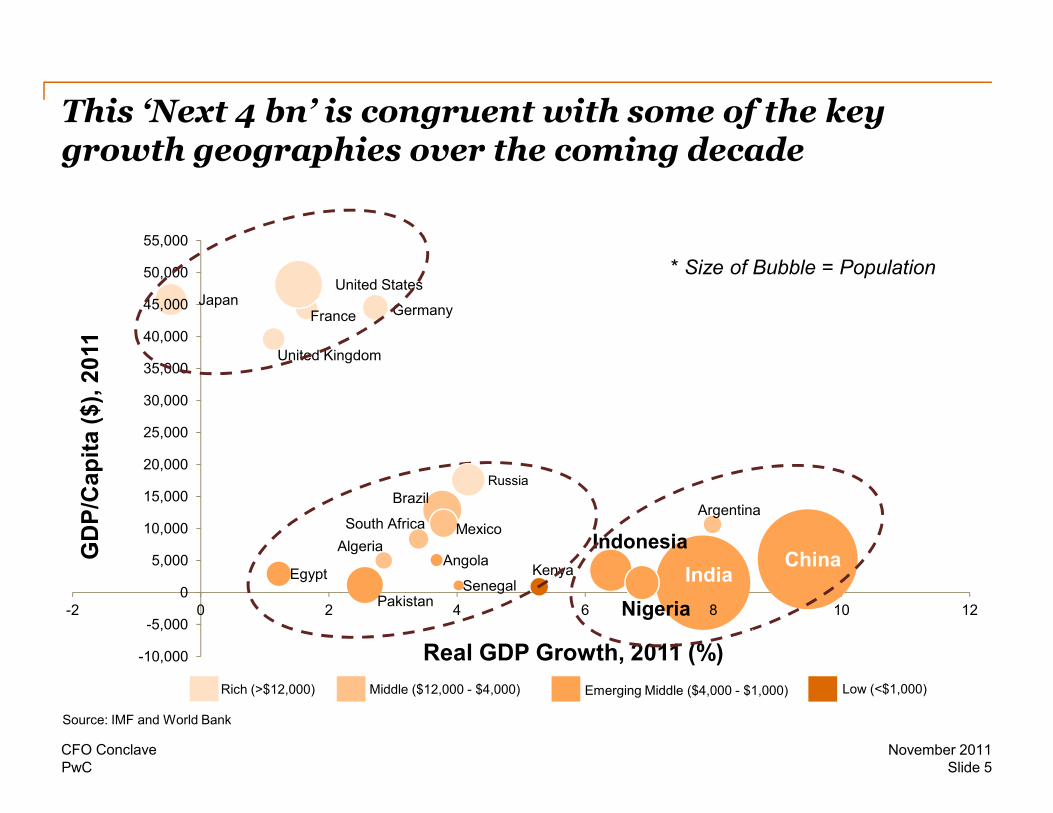

France GermanyJapan

United Kingdom

United States

30,000

35,000

40,000

45,000

50,000

55,000

GDP/Capita ($), 2011

* Size of Bubble = Population

This ‘Next 4 bn’ is congruent with some of the key growth geographies over the coming decade

PwC

AlgeriaAngola

ArgentinaBrazil

ChinaEgypt India

Indonesia

Kenya

Mexico

NigeriaPakistanSenegal

South Africa

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

-2 0 2 4 6 8 10 12

GDP/Capita ($), 2011

Real GDP Growth, 2011 (%)

Middle ($12,000 - $4,000) Emerging Middle ($4,000 - $1,000) Low (<$1,000) Rich (>$12,000)

Source: IMF and World Bank

Russia

November 2011Slide 5

CFO Conclave

Emerging Middle

PwCNovember 2011CFO Conclave

Slide 6

India’s Population Distribution (millions) 1.19 Bn 1.36 Bn

Re Household ($*/day per capita)

Classification

> 8.5 L, ($10) Upper Middle

+

3–8.5 L, ($5-$10) Middle 300

190

2021 (Projection)

170

80

2010 (%)

14%

23%

Within India, a 600 million strong ‘emerging middle’ is the focus of our research

PwC

3–8.5 L, ($5-$10) Middle

1.5 – 3 L, ($1.7-$5) Emerging middle

<1.5 L, (<$1.7) Low290

570

300

460

470

170

Sources: PWC Analysis, NCAER (National Centre for Applied Economic Research), CMI.

All figures are reported at 2010 constant prices

42%

21%

November 2011Slide 7

CFO Conclave

Remarks by Sanjeev Kumar, CFO of Coca-Cola India

1 Relevance of this market for Coke

2 Opportunities & Challenges

PwCNovember 2011

Slide 8CFO Conclave

Research Profitable Growth Strategies

PwCNovember 2011CFO Conclave

Slide 9

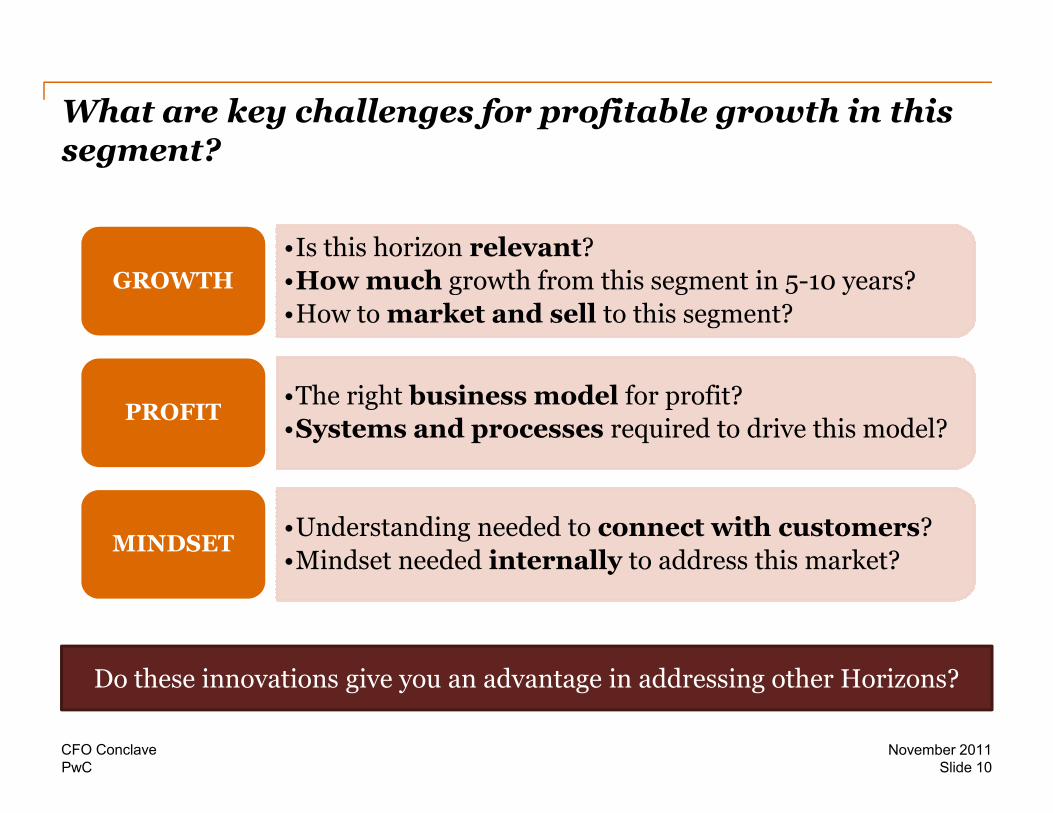

What are key challenges for profitable growth in this segment?

•Is this horizon relevant?

•How much growth from this segment in 5-10 years?

•How to market and sell to this segment?

GROWTH

•The right business model for profit?PROFIT

PwC

•The right business model for profit?

•Systems and processes required to drive this model?PROFIT

•Understanding needed to connect with customers?

•Mindset needed internally to address this market?MINDSET

Do these innovations give you an advantage in addressing other Horizons?

November 2011Slide 10

CFO Conclave

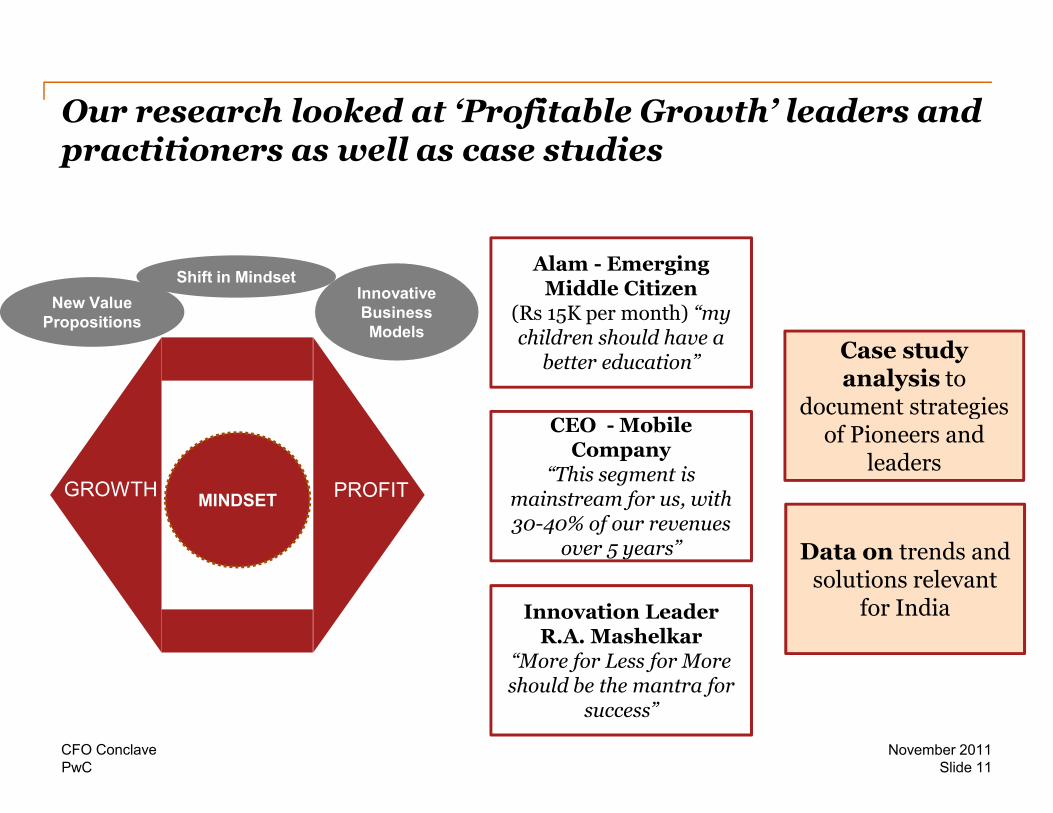

Our research looked at ‘Profitable Growth’ leaders and practitioners as well as case studies

Innovative Business Models

Shift in Mindset

New Value Propositions

Alam - Emerging Middle Citizen

(Rs 15K per month) “my children should have a better education”

Case study analysis to

document strategies

PwC

MINDSETGROWTH PROFIT

CEO - Mobile Company

“This segment is mainstream for us, with 30-40% of our revenues

over 5 years”

Innovation LeaderR.A. Mashelkar

“More for Less for More should be the mantra for

success”

document strategies of Pioneers and

leaders

Data on trends and solutions relevant

for India

November 2011Slide 11

CFO Conclave

The Indian emerging middle class will constitute a $1 Trillion economy by 2021 with a young, largely rural base

Significant

$ 1 Trillion economy

• Double from now• 30% of Indian economy

DEMOGRAPHICS

PwC

Significant demographic shift and aspiration for

change

Young and Rural

Rapid Change

• Median age < 30 yrs• ~ 70% Rural

• Food less important• Ceremonies, Education etc.

November 2011Slide 12

CFO Conclave

Aspiration Tradeoffs

Understand the very different aspirations,

influencers, and tradeoffs of this segment

Position product and Design Product or

GROWTH

Growth requires understanding unique aspirations positioning and customization for this segment

PwC

Platform Customization

Beyond Cost Position

Design product and services with a few key features, but tailoring it for diversity

Position product and services beyond cost,

pricing beyond functional considerations

Design Product or Service with the specific needs of

this market

November 2011Slide 13

CFO Conclave

Ecosystem Collaboration

Extract value by creating an ecosystem, collaborate with the unorganized sector

Have a modular design, Create a scalable

PROFIT

Profit requires scale thinking, collaboration and use of technology with offline interventions

PwC

Smart Reach

Modular Scale

Cluster marketing and distribution, create local financing mechanism,

enable through technology and offline

Have a modular design, aggregate local demand and think scale from the

beginning

Create a scalable business through collaboration, Technology and

offline

November 2011Slide 14

CFO Conclave

Trusted

Endorsement

Build the brand with aspiration in mind, but using word of mouth to

drive awareness

Drive this business with

Create trust with this segment and

MINDSET

A mindset that creates trust in a unique way backed by performance measures and disruptive thinking

PwC

Disruptive

AND

Values & Metrics

Disruptive changes required in this model alongside

‘AND thinking’

Drive this business with broader values and

incubate it with different metrics

this segment and drive business by measures and disruptive thinking

November 2011Slide 15

CFO Conclave

Idea cellular took a path that consolidated its position in this market before moving up

“Targeted Emerging Middle”

• Smaller town licences to start the

business

PROFITABLE GROWTH FRAMEWORK

80

2010

PwC

business

• Customized for rural and low-

income consumers

• Distribution network of 1,520

branded service centers

• Strength to Move up

Source: PwC analysis, primary research

460

470

170

November 2011Slide 16

CFO Conclave

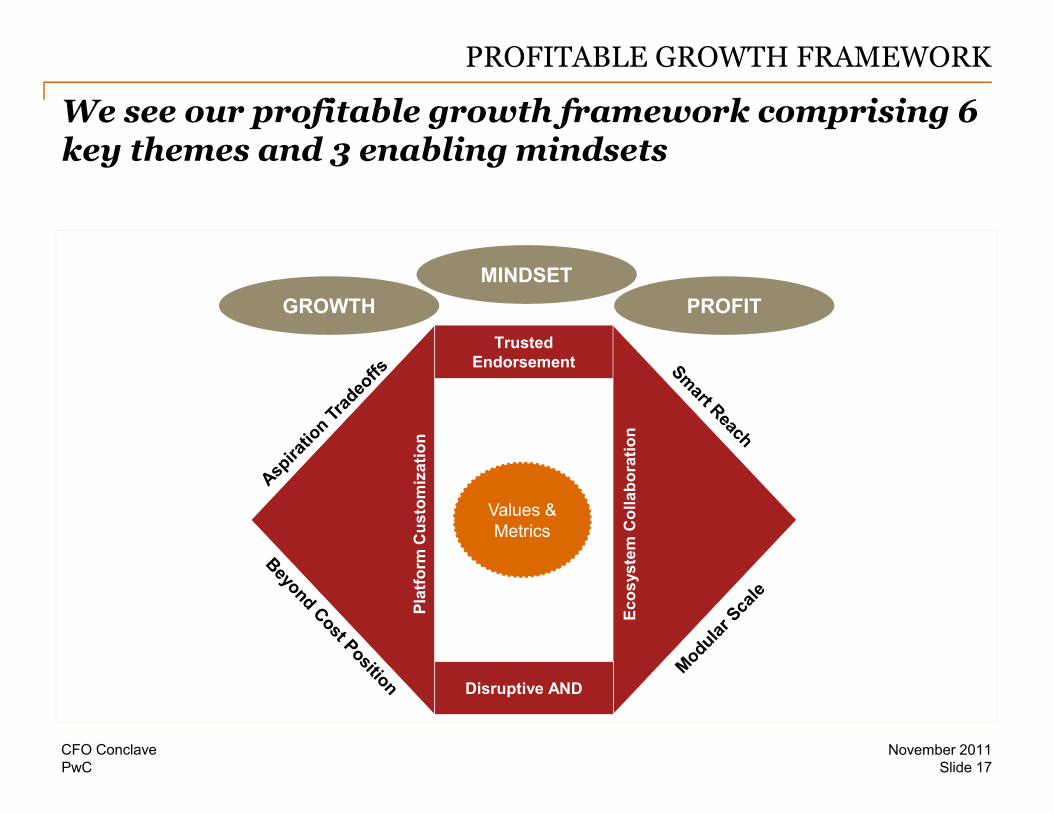

We see our profitable growth framework comprising 6 key themes and 3 enabling mindsets

PROFITABLE GROWTH FRAMEWORK

Trusted Endorsement

PROFIT

MINDSET

GROWTH

PwC

Ecosystem Collaboration

Values & Metrics

Disruptive AND

Platform

Customization

November 2011Slide 17

CFO Conclave

Financial Approach

PwCNovember 2011CFO Conclave

Slide 18

Financial approach in one case followed a different approach in the Adoption, Acceleration and Steady State

Adoption Acceleration Steady Phase

Revenue

COGS

PwC

Source PwC Analysis

Gross Margin

SG&A

Operating Margins

Asset Investment

Asset Turnover

ROCE

November 2011Slide 19

CFO Conclave

Relevance for you

PwCNovember 2011CFO Conclave

Slide 20

900

1,200

1,500

HORIZON 1 HORIZON 2

2

Population

(Millions)

Resulting innovations can be used to address other horizons

NEXT 4 BN HORIZON

PwC

0

300

600 3 1

Population

(Millions)

Source: PWC Analysis, World bank, IMF

November 2011Slide 21

CFO Conclave

Where are you in this journey? Where are your different businesses?

Next Steps Not Present Entering Steady State NewHorizon

Assess X X

Organizational Situation

PwC

Design X

Construct X

Implement X

Operate & Review

X

November 2011Slide 22

CFO Conclave

How do you create profitable growth in this Horizon?

Demographics and growth:• Opportunity and Growth• Consumer trends• Lateral research Aspiration Tradeoffs:

Beyond Cost Position/ Mass Customization/ Disruptive AND: • Consumers Strategy• Pricing and Market positioning• Innovation strategyTrusted endorsements:• Branding and Messaging

POTENTIAL

ENTRY STRATEGY

DESIGN &ASSESS &

PwC

Aspiration Tradeoffs:• Competition and Substitutes

Modular scale • Value Chain DesignSmart Reach • Sales and Distribution• Alliances

• Finance and Regulatory• Quality Control• Operations Management• Training, Recruitment, HR

OPERATING MODEL

STEADY STATE/NEW HORIZON

DESIGN &CONSTRUCT

CONSTRUCT &

IMPLEMENT

OPERATE &REVIEW

ASSESS &DESIGN

November 2011Slide 23

CFO Conclave

Thank you!

© 2011 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India), which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.