Prof. H.-J. Lüthi WS Budapest 10.-13..9.2003, 1 Hedging strategy and operational flexibility in the...

23

Prof. H.-J. Lüthi Budapest 10.-13..9.2003, 1 Hedging strategy and operational flexibility in the electricity market Characteristics of the electricity market • Non-storability • Transmission constraints • Very complex contracts • Physical production

-

Upload

ariel-chambers -

Category

Documents

-

view

215 -

download

1

Transcript of Prof. H.-J. Lüthi WS Budapest 10.-13..9.2003, 1 Hedging strategy and operational flexibility in the...

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 1

Hedging strategy and operational flexibility in the electricity market

Characteristics of the electricity market

• Non-storability

• Transmission constraints

• Very complex contracts

• Physical production

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 2

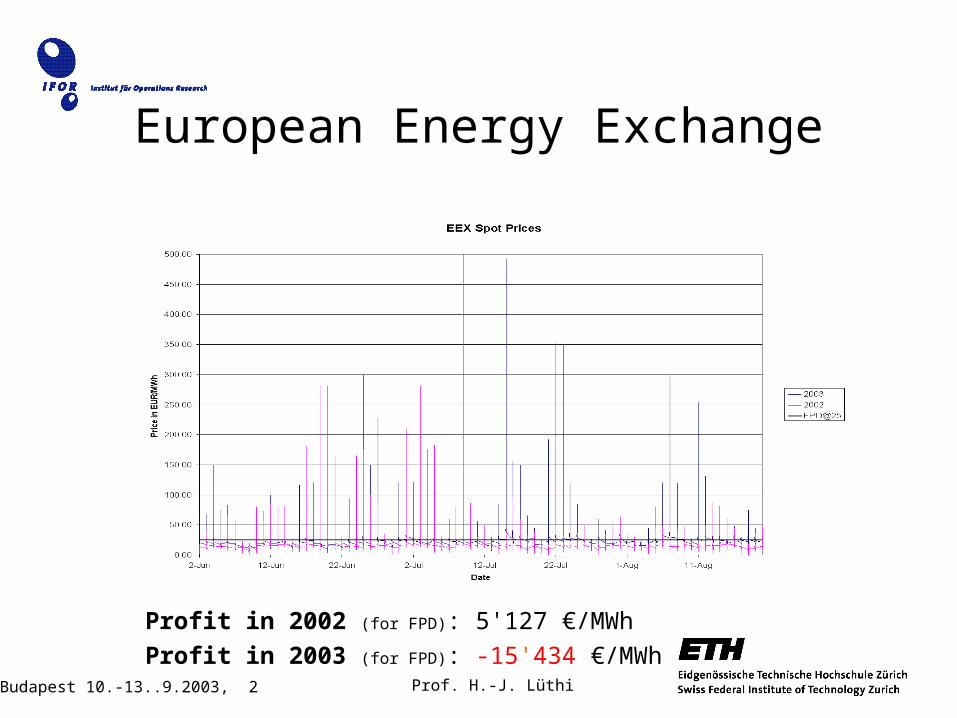

European Energy Exchange

Profit in 2002 (for FPD): 5'127 €/MWh

Profit in 2003 (for FPD): -15'434 €/MWh

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 3

Introduction

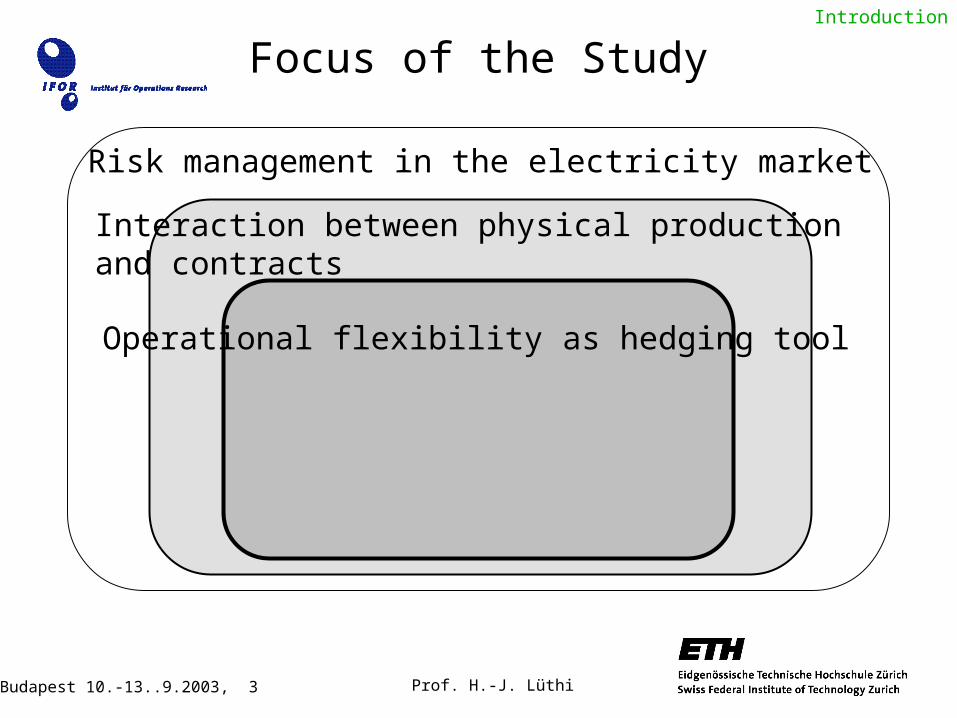

Focus of the Study

Risk management in the electricity market

Interaction between physical production and contracts

Operational flexibility as hedging tool

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 4

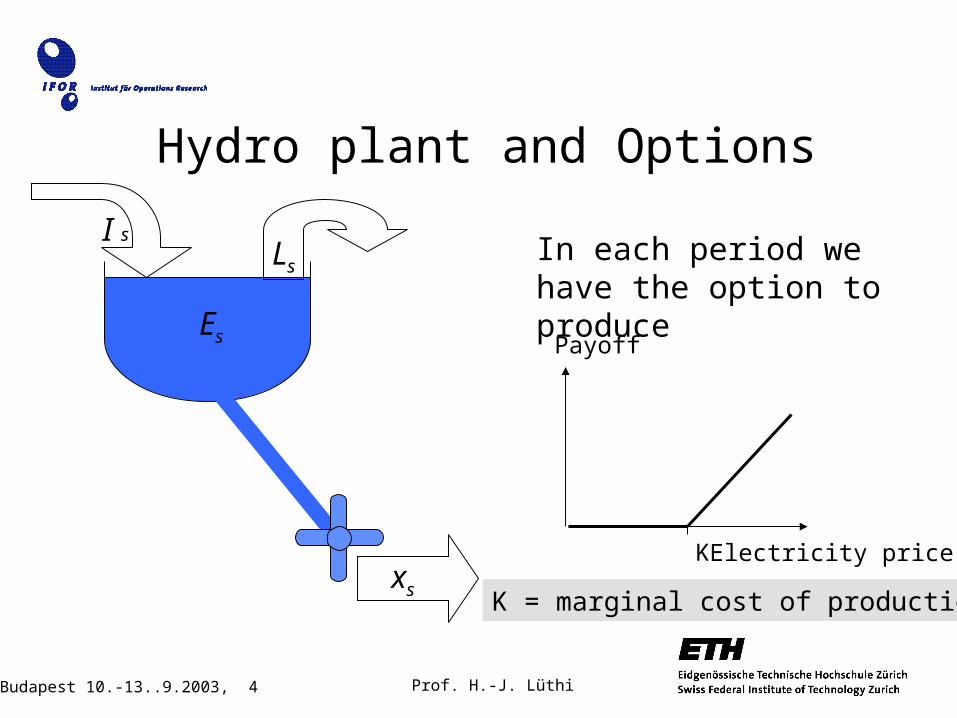

Hydro plant and Options

xs

Es

I sLs

In each period we have the option to produce

Payoff

Electricity price

K = marginal cost of production

K

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 5

• If we produce today the possibility to produce tomorrow will be affected

• In each period we have the option to produce if Es > 0

Time (hourly buckets)

Max capacity, 500MW

Min capacity, -50MW

A series of interdependent options

Storage almost emptyHigh spot prices

Low spot prices

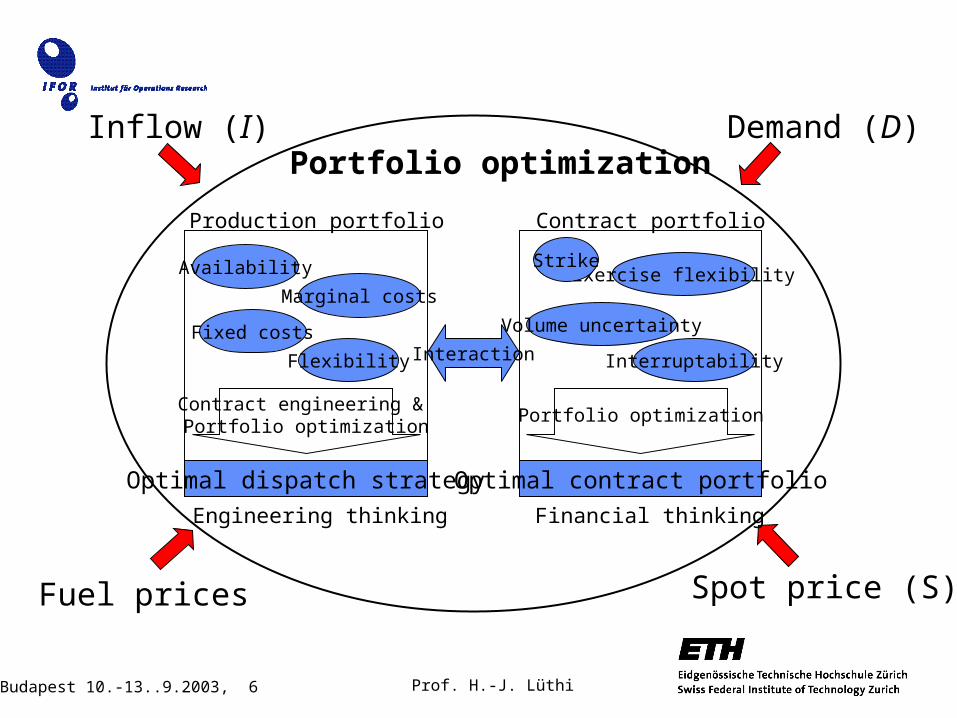

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 6

Portfolio optimization

Production portfolio

Engineering thinking

Marginal costs

Fixed costs

Flexibility

Availability

Contract engineering & Portfolio optimization

Optimal dispatch strategy

Interaction

Inflow (I)

Fuel prices

Demand (D)

Spot price (S)

Contract portfolio

Financial thinking

Exercise flexibility

Interruptability

Strike

Volume uncertainty

Optimal contract portfolio

Portfolio optimization

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 7

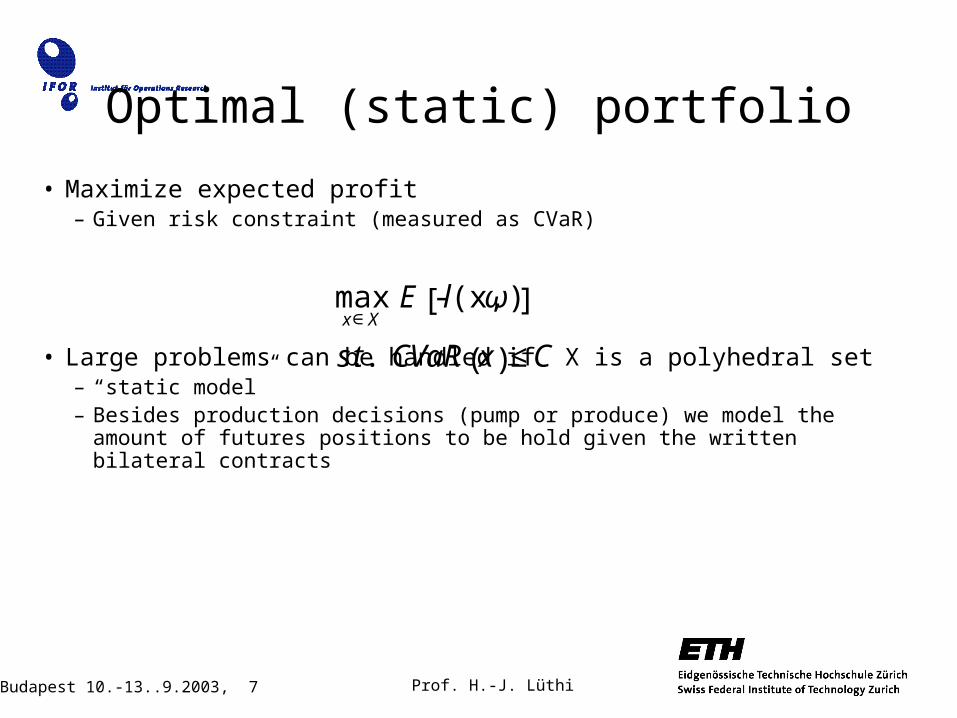

• Maximize expected profit– Given risk constraint (measured as CVaR)

• Large problems can be handled if X is a polyhedral set– “static model”– Besides production decisions (pump or produce) we model the amount of

futures positions to be hold given the written bilateral contracts

Optimal (static) portfolio

€

maxx∈X

E -l(x,ω)[ ]

s.t. CVaR x( )≤C

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 8

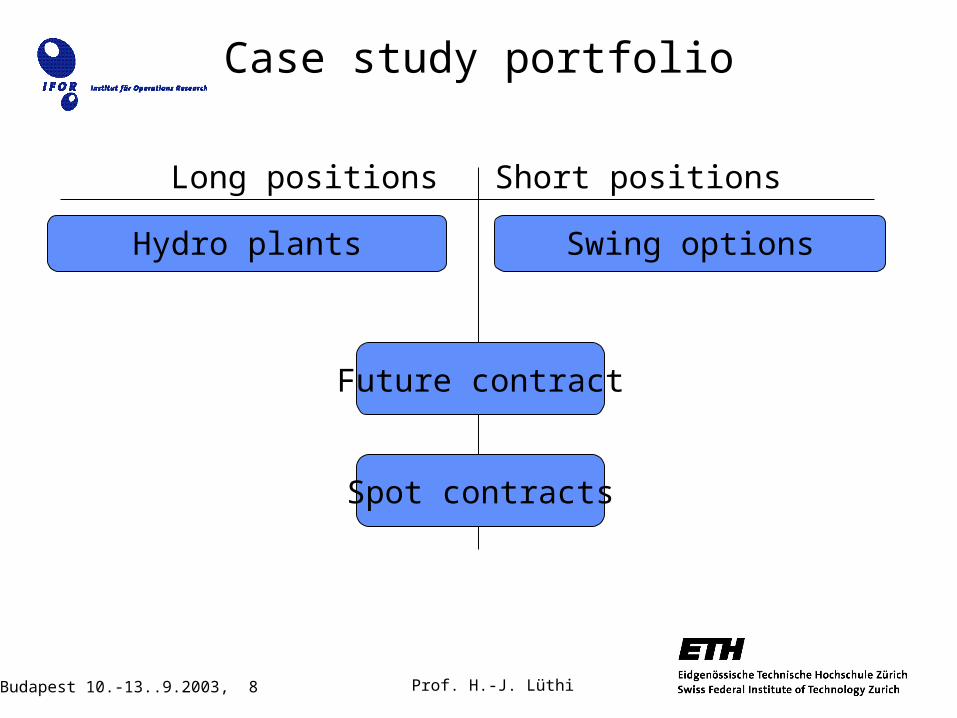

Case study portfolio

Long positions Short positions

Hydro plants Swing options

Future contract

Spot contracts

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 9

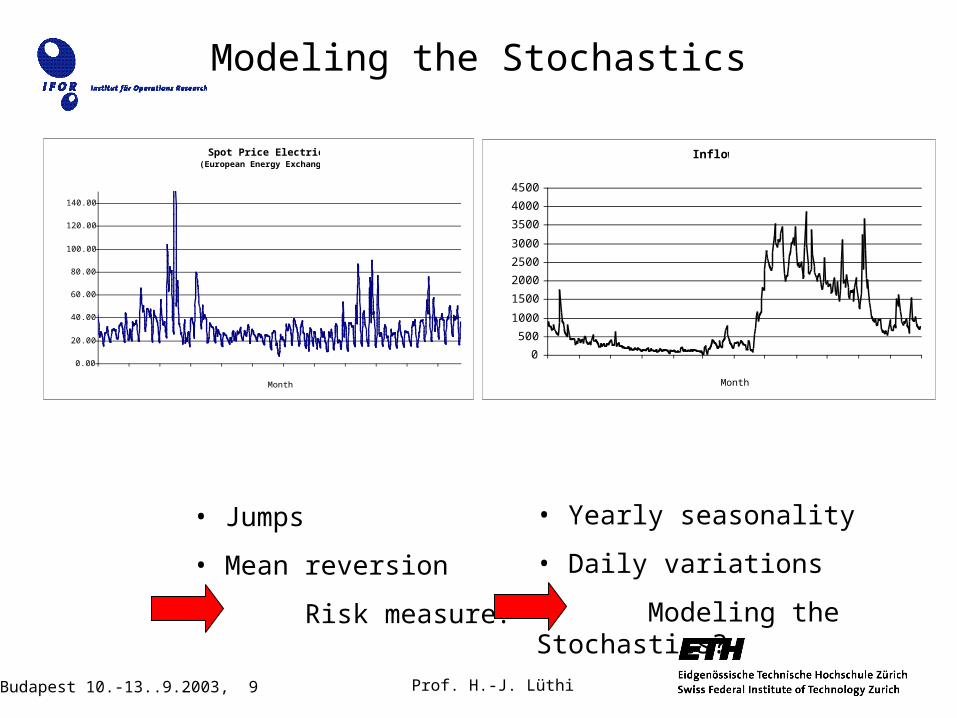

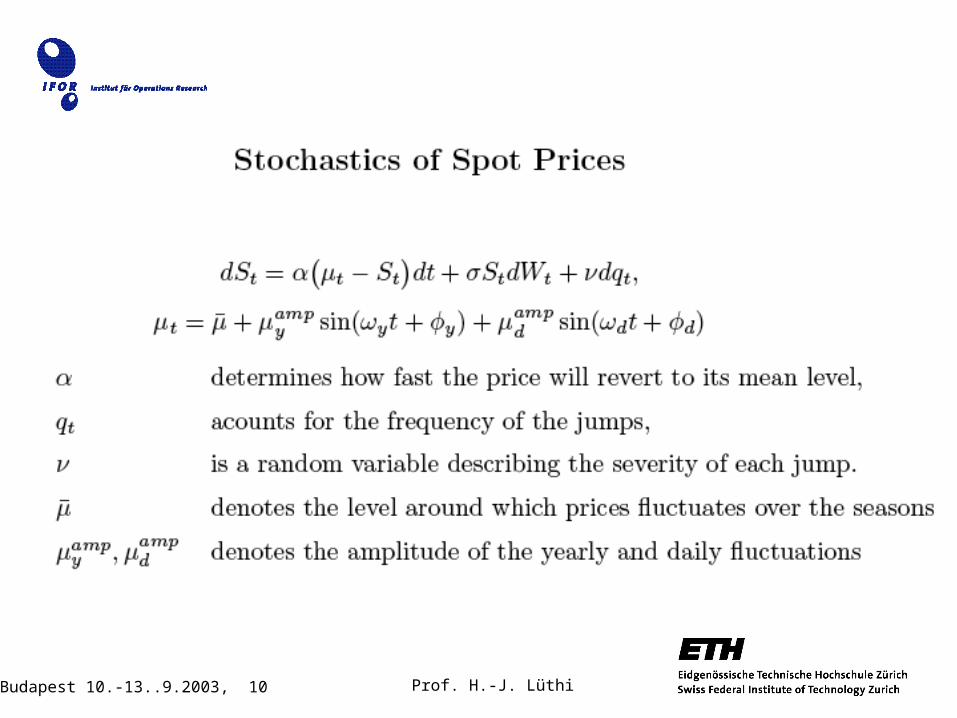

Modeling the Stochastics

• Jumps

• Mean reversion

Risk measure?

• Yearly seasonality

• Daily variations

Modeling the Stochastics?

Inflow

0

500

1000

1500

2000

2500

3000

3500

4000

4500

O N D J F M A M J J A S

Month

Inflow (in m

3/s)

Spot Price Electricity (European Energy Exchange)

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

O N D J F M A M J J A S

Month

Spot Price (in Euro/MWh)

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 10

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 11

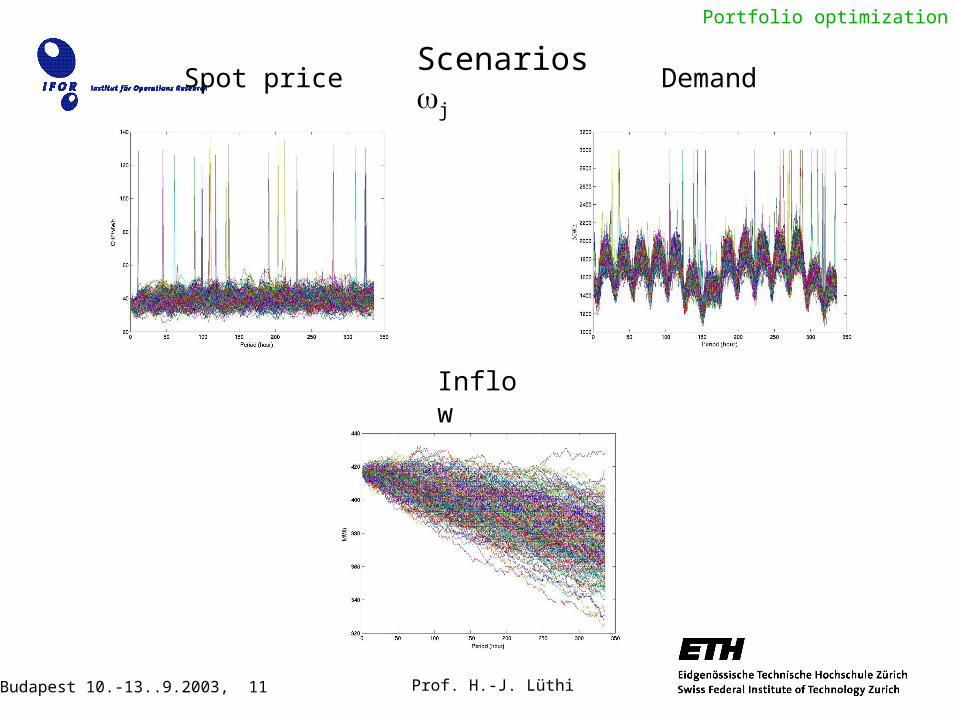

Portfolio optimization

Spot price

Inflow

DemandScenarios j

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 12

Notations in Period s

xs

Es

I sLs

xs Production / Pumping

Is Inflow

Es Waterlevel

Ls Spill-over

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 13

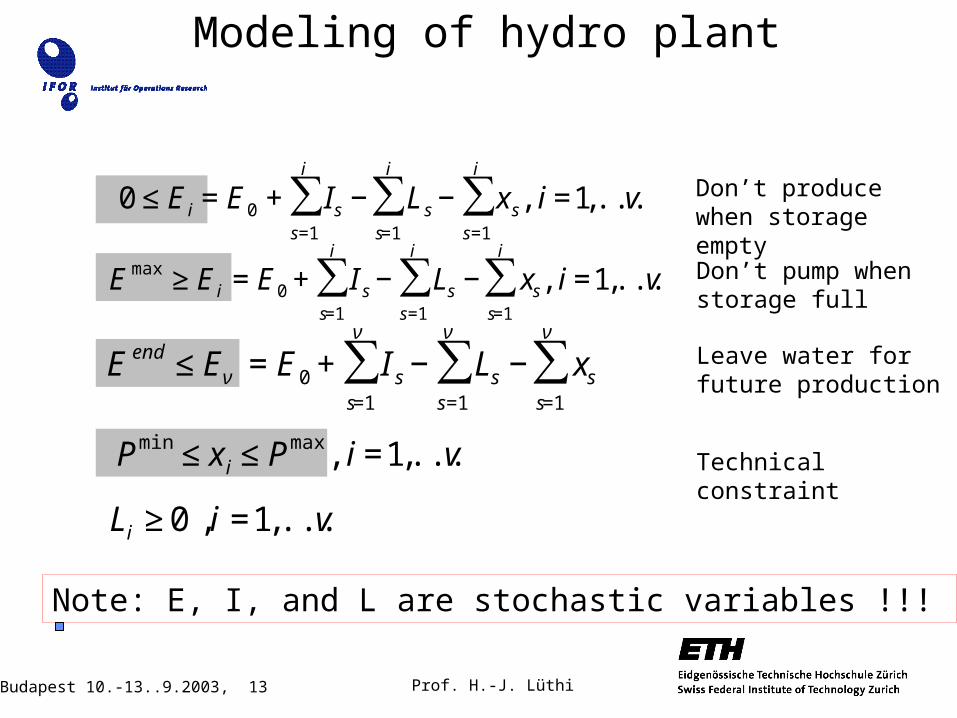

Modeling of hydro plant

Li ≥0 ,i =1,...,v

€

0≤Ei =E0 + Is − Lss=1

i

∑ − xs, i=1,...,vs=1

i

∑s=1

i

∑

€

Emax≥Ei =E0 + I s− Lss=1

i

∑ − xss=1

i

∑s=1

i

∑ , i=1,...,v

€

Pmin ≤xi ≤Pmax, i=1,...,v

€

E end≤Eν =E0 + I s− Lss=1

ν

∑ − xss=1

ν

∑s=1

ν

∑

Don’t produce when storage empty

Don’t pump when storage full

Leave water for future production

Technical constraint

Note: E, I, and L are stochastic variables !!!

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 14

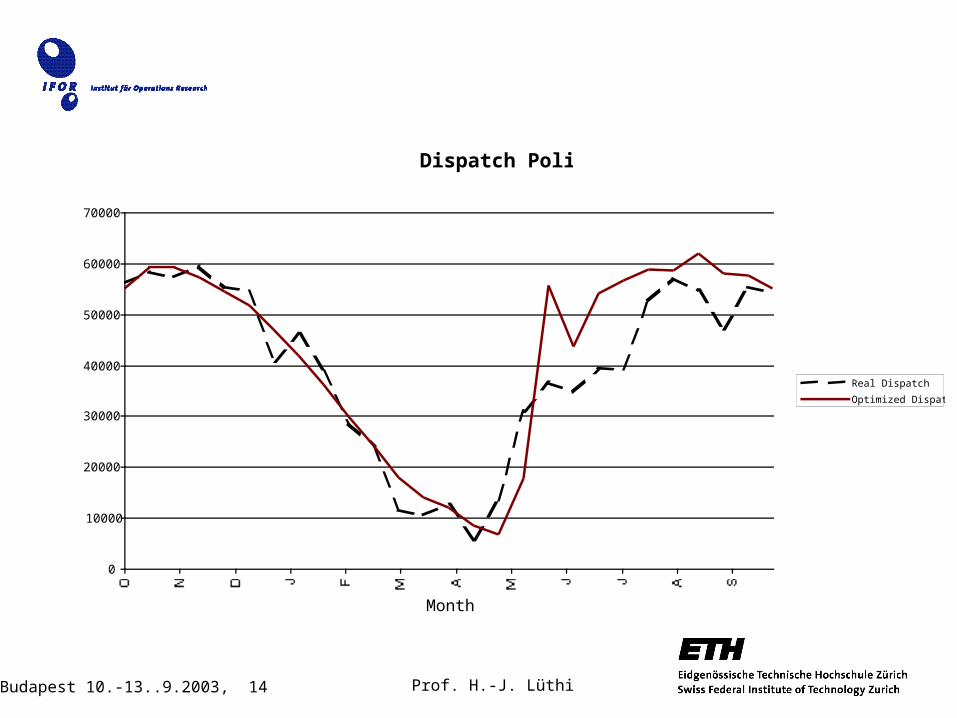

Dispatch Policy

0

10000

20000

30000

40000

50000

60000

70000

Month

Water Level

Real Dispatch

Optimized Dispatch

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 15

Dynamic Dispatch

• Dispatch responds to observations of uncertainties

– Spot-price S

– Aggregated Inflow up to time t: I

– Demand

• Corresponds to an exercise-frontier in American options

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 16

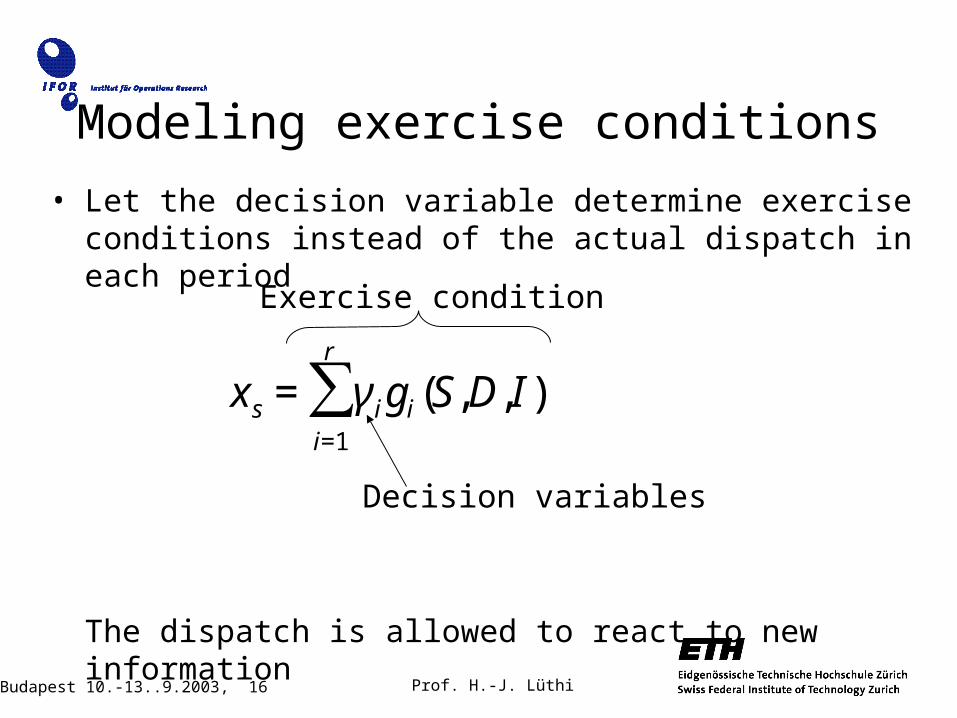

Modeling exercise conditions

• Let the decision variable determine exercise conditions instead of the actual dispatch in each period

The dispatch is allowed to react to new information

€

xs = γigi S,D,I( )i=1

r

∑

Decision variables

Exercise condition

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 17

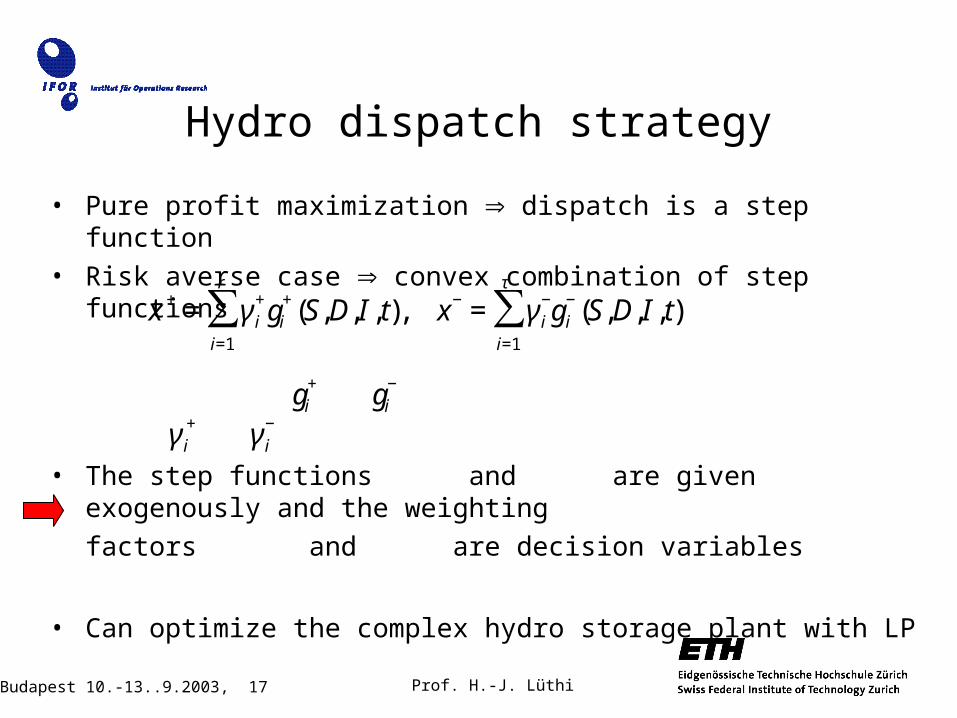

• Pure profit maximization dispatch is a step function

• Risk averse case convex combination of step functions

• The step functions and are given exogenously and the weighting

factors and are decision variables

• Can optimize the complex hydro storage plant with LP

Hydro dispatch strategy

€

gi+

€

gi−

€

γi+

€

γi−

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 18

Portfolio optimization & hedging strategy

Dispatch strategy

Tight risk constraint (low C)No risk constraint (high C)

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 19

Hedging strategy

• Uncertain demand is risky

• Cannot hedge with standardized contracts

• Operational flexibility to hedge against volume risk

What is the operational flexibility worth?

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 20

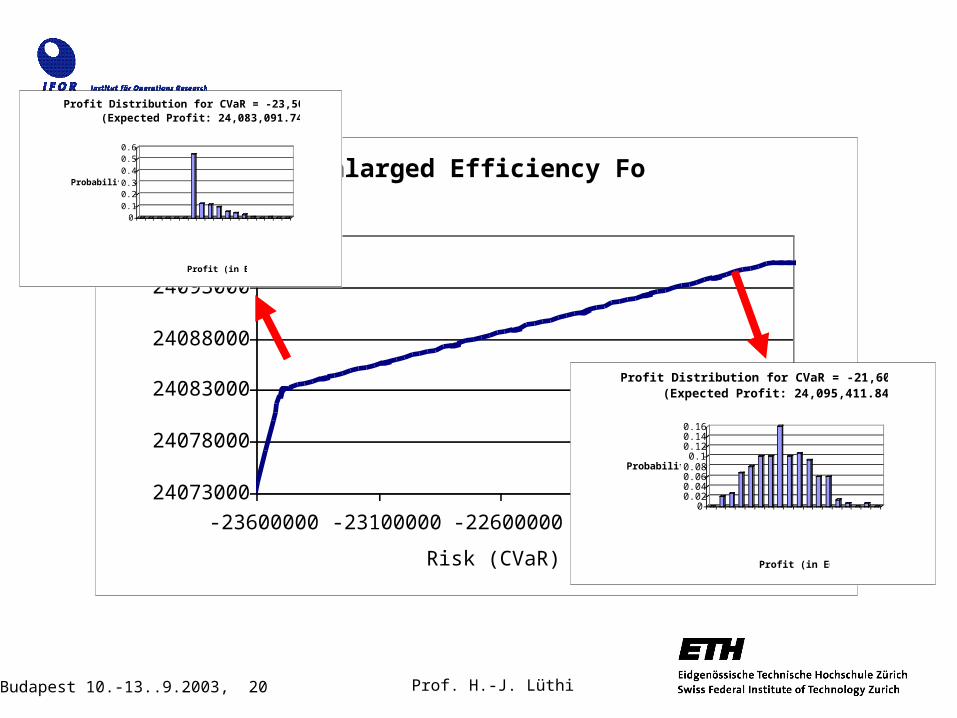

Enlarged Efficiency Fontier

24073000

24078000

24083000

24088000

24093000

24098000

-23600000 -23100000 -22600000 -22100000 -21600000

Risk (CVaR) [in Euro]

Profit (in Euro)

00.10.20.30.40.50.6

Probability

21,400,00022,200,00023,000,00023,800,00024,600,00025,400,00026,200,00027,000,00027,800,000

Profit (in Euro)

Profit Distribution for CVaR = -23,500,000 Euro(Expected Profit: 24,083,091.74)

00.020.040.060.080.1

0.120.140.16

Probability

21,400,00022,200,00023,000,00023,800,00024,600,00025,400,00026,200,00027,000,00027,800,000

Profit (in Euro)

Profit Distribution for CVaR = -21,600,000 Euro(Expected Profit: 24,095,411.84)

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 21

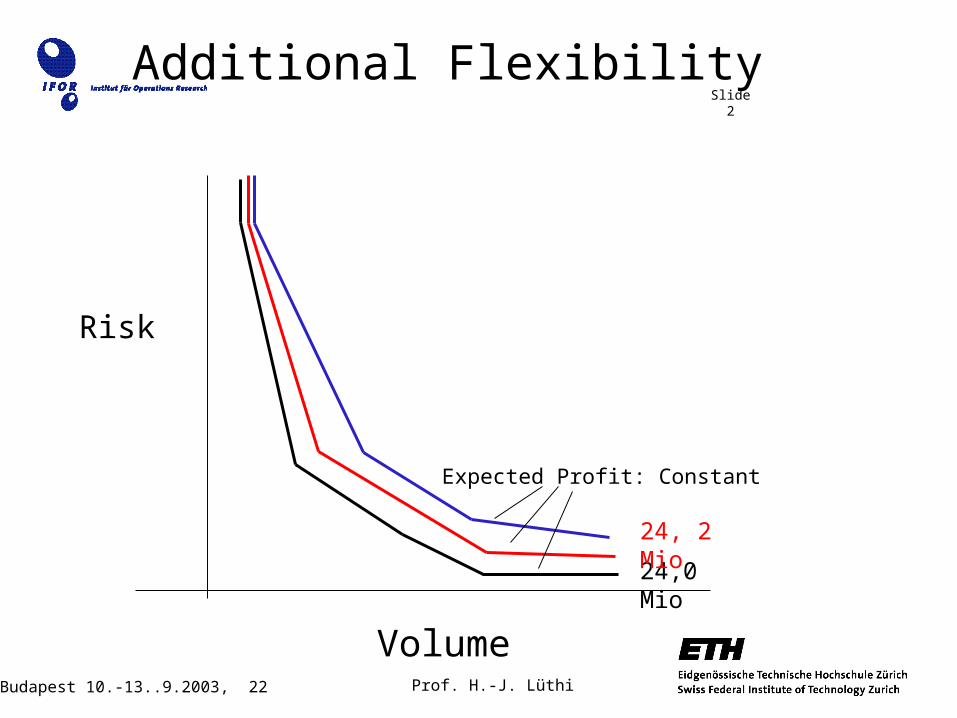

Additional FlexibilitySlide

1

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 22

Additional Flexibility

Expected Profit: Constant

Slide 2

Volume

Risk

24,0 Mio

24, 2 Mio

Prof. H.-J. LüthiWS Budapest 10.-13..9.2003, 23

• Guidance on how to dispatch hydro storage plants under risk / return considerations.

• Not just identify but actually quantify operational flexibility with regard to handle uncertainty.

• Perceive uncertainty as a challenge to flexibility instead of a threat.

• Identified an important value driver in hydro storage plants (and flexible plants in general).

Achievements