Production New

26

Production theory Provides framework for economics of production of firm

-

Upload

abhishek-agarwal -

Category

Documents

-

view

220 -

download

0

Transcript of Production New

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 1/26

Production theory

Provides framework foreconomics of production of

firm

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 2/26

What is production

Production refers to transformation of inputs or resources into outputs of goodsand services

Inputs = resources used in production of goods (fixed and variable)

Output = end result

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 3/26

Basic production decision

1.How much of commodity to produce

2.How much inputs should be used

To answer these questions, the firm

a. Requires engineering data on productionpossibilities

b. Economic data on input and output prices

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 4/26

Production function

Production is a function that transformsinputs into output

Q = f (L, N, K……T)

Factors affecting production are

1.Technology

2.Inputs (land, labour etc)3.Time period (short run vz long run)

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 5/26

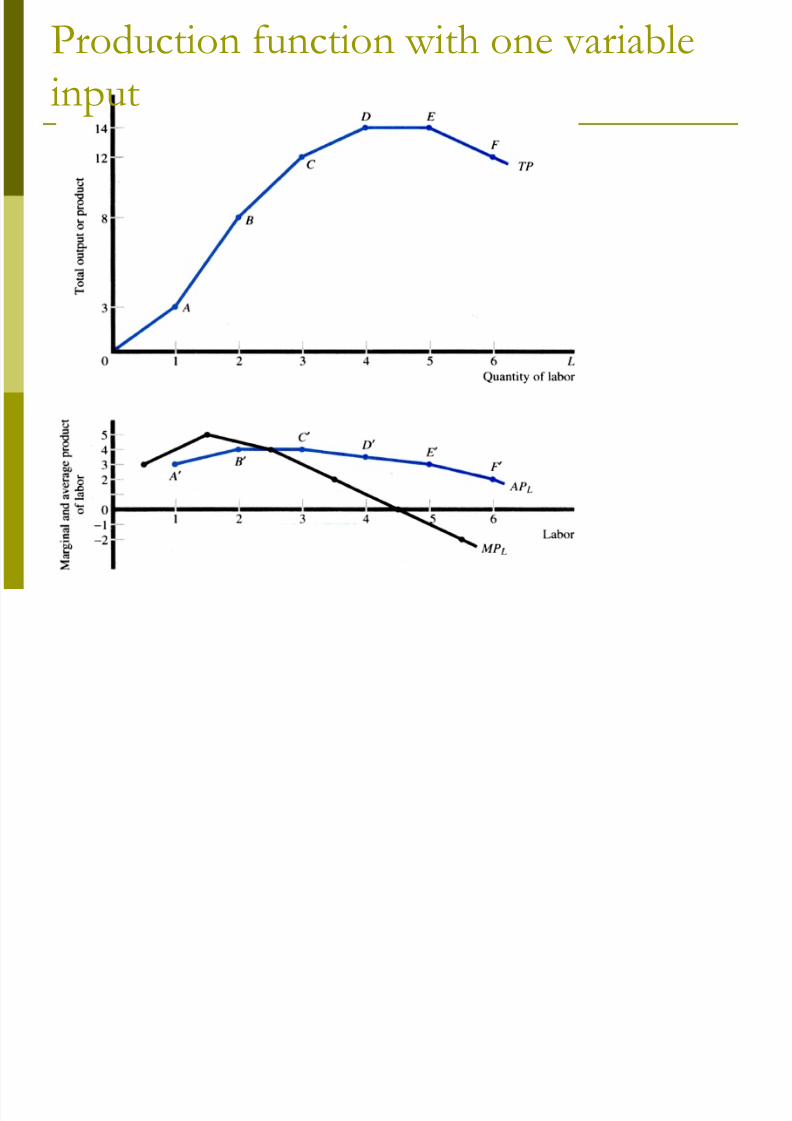

1) Total Product:

3) Marginal Product:

2) Average Product:

TP = Q = f(L)

MPL =

TP

L

APL =TPL

Production function with one variable

input

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 6/26

Concepts of production

Total Product :This is amount of totaloutput produced by a given amount of factor, other factors held constant.

Average Product: This is total outputproduced per unit of factor employed

AP =TP/no. of units of factor employed

Marginal Product: This is addition to totalproduction by employment of extra unit of factor

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 7/26

Law of variable proportions or law of

diminishing returns

As more and more of one factor input isemployed, all other input quantities heldconstant, a point will be reached whereadditional quantities of varying input willyield diminishing marginal contribution tototal product

Short run law

Some factors fixed, other factors variable State of technology fixed and unchanged

Possibility of varying proportion of factors

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 8/26

L Q MPL APL EL

0 0 - - -

1 3 3 3 1

2 8 5 4 1.25

3 12 4 4 1

4 14 2 3.5 0.57

5 14 0 2.8 0

6 12 -2 2 -1

Total, Marginal, and Average Product of Labor, and Output Elasticity

Production function with one variable

input

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 9/26

Production function with one variable

input

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 10/26

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 11/26

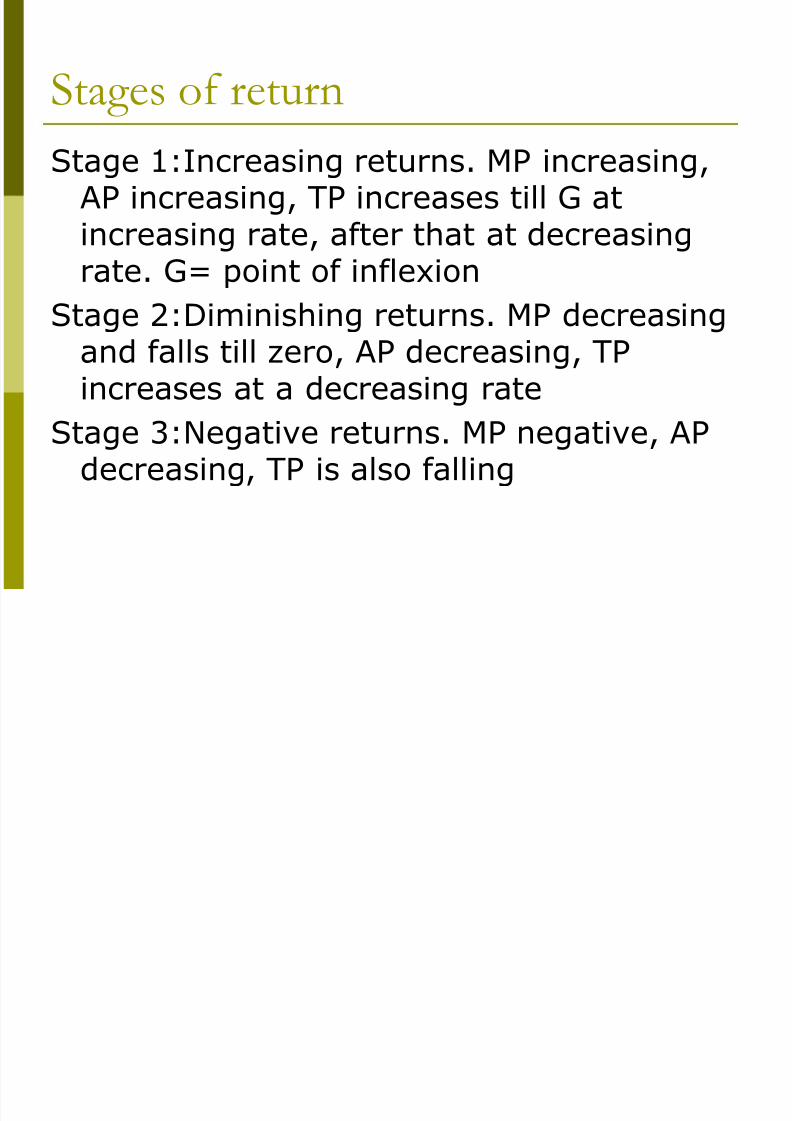

Stages of return

Stage 1:Increasing returns. MP increasing,AP increasing, TP increases till G atincreasing rate, after that at decreasing

rate. G= point of inflexionStage 2:Diminishing returns. MP decreasing

and falls till zero, AP decreasing, TPincreases at a decreasing rate

Stage 3:Negative returns. MP negative, APdecreasing, TP is also falling

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 12/26

Contd..

Stage of operations –stage2

Stage 1 – fixed factor too much forvariable factor. Fixed factor is more

intensively utilised Stage 3- variable factor too much in

relation to fixed factor

Applications – agriculture, studying

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 13/26

Isoquants show combinations of two inputsthat can produce the same level of output.

Firms will only use combinations of twoinputs that are in the economic region ofproduction, which is defined by the portionof each isoquant that is negatively sloped.

Production with two variable inputs

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 14/26

Isoquant

An isoquant is a curve representingvarious combinations of 2 inputs thatproduce the same level of output

ISO+QUANT= same + quantity

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 15/26

Isoquants

Production with two variable inputs

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 16/26

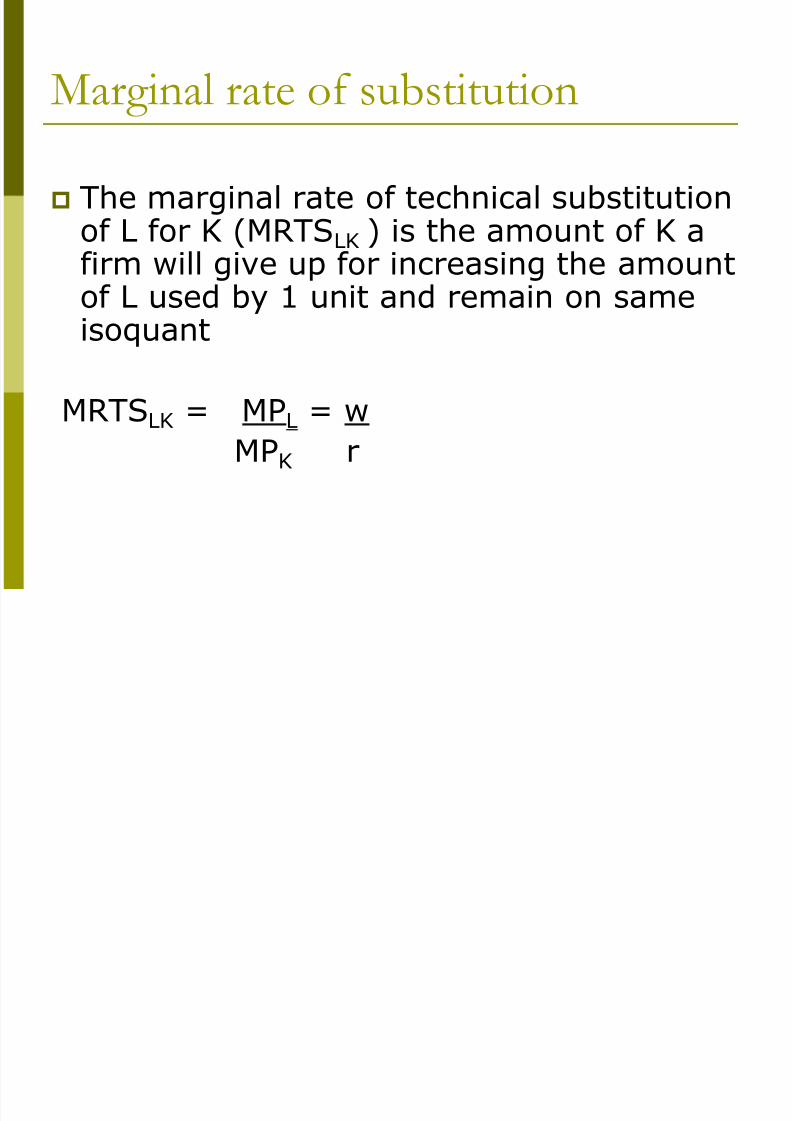

Marginal Rate of Technical Substitution

MRTS = K/ L = MPL /MPK

Production with two variable inputs

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 17/26

Marginal rate of substitution

The marginal rate of technical substitutionof L for K (MRTSLK ) is the amount of K a

firm will give up for increasing the amountof L used by 1 unit and remain on sameisoquant

MRTSLK = MPL = wMPK r

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 18/26

Production With Two

Variable InputsMRTS = (-2.5/1) = 2.5

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 19/26

Isocost lines represent all combinations oftwo inputs that a firm can purchase with

the same total cost.

C wL rK

C wK L

r r

C Total Cost

( )w Wage Rate of Labor L

( )r Cost of Capital K

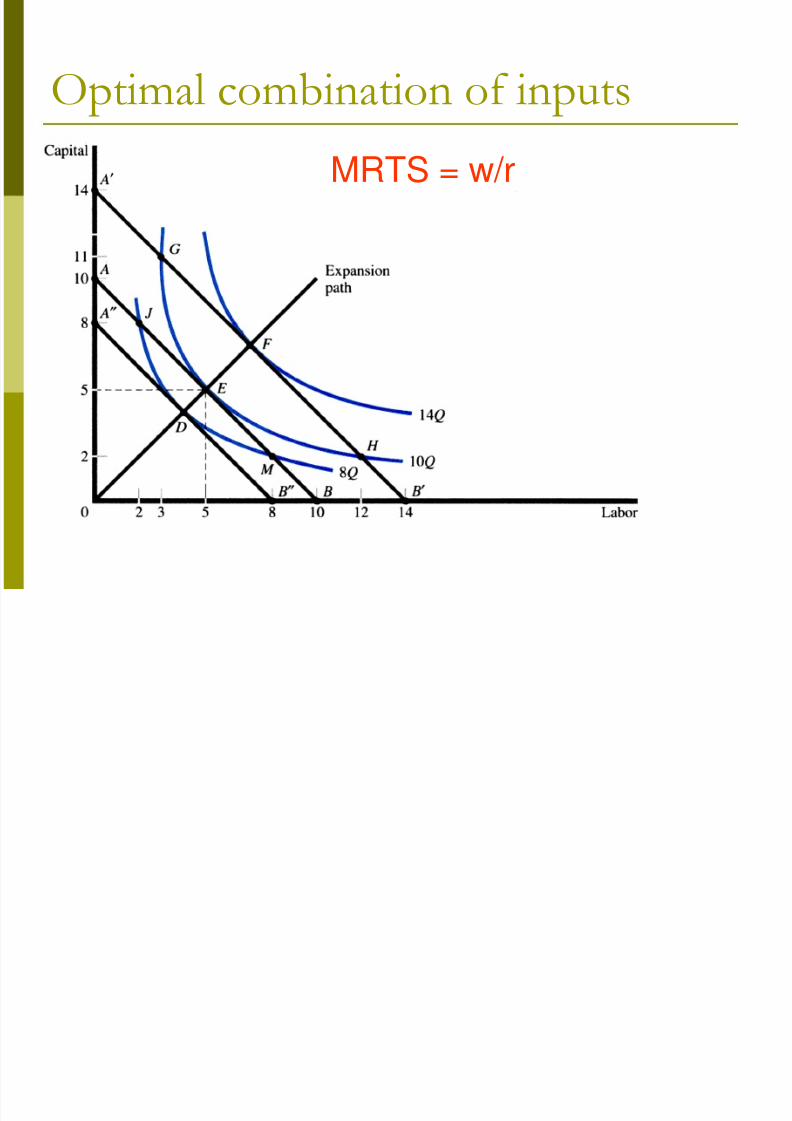

Optimal combination of inputs

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 20/26

Isocost

An isocost shows all differentcombinations of labor and capital that afirm can purchase, given the total outlay

(TO) of firm and factor prices.

The slope of an isocost is – Pl.

Pk

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 21/26

Producer’s equilibrium

An producer is in equilibrium when hemaximises output for total outlay.

i.produces given output at minimum cost

ii. Produces maximum output at given level

of cost

Equilibrium = isocost tangent to isoquant

Here, MRTS lk = MPl /MPk = w/r

i.e.At equilibrium, MPl = MPk

Pl Pk

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 22/26

MRTS = w/r

Optimal combination of inputs

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 23/26

Production Function Q = f(L, K)

Q = f(hL, hK)

If = h, then f has constant returns to scale.

If > h, then f has increasing returns to scale.

If < h, the f has decreasing returns to scale.

Returns to Scale- Change in all inputs

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 24/26

Stages of return – Returns to scale

The percentage increase in output when all inputsvary in same proportion is known as returns toscale

1.Constant returns to scale – Output increases insame proportion as increase in input

2.Increasing returns to scale-Output increases bygreater proportion as increase in input

3. Decreasing returns to scale – Output increasesby lesser proportion as increase in input

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 25/26

ConstantReturns to

Scale

IncreasingReturns to

Scale

DecreasingReturns to

Scale

Returns to Scale

8/3/2019 Production New

http://slidepdf.com/reader/full/production-new 26/26

Reasons

Causes of increasing returns

Specialisation in large scale production. Insome industries, small scale production is

not possible

Causes of decreasing returns

Coordination and control maybe difficult.Information maybe lost or distorted whentransmitted