Product Catalogue International Solar - eupd...

64

Product Catalogue International Solar EuPD Research

Transcript of Product Catalogue International Solar - eupd...

Product Catalogue International SolarEuPD Research

© a

+f

Gm

bH

Product Catalogue International SolarEuPD Research

4 EuPD Research 2011

Content

The Hoehner Research & Consulting Group Value Cycle ....................................... 6

EuPD Research – PV Research & Consulting Services ............................................. 7

1. The Global PV Market .......................................................................................... 9

ManufacturersMonitor© ......................................................................................10

PV Executive News Summary© ..............................................................................12

PV Thin Film Guidebook© 2011 ............................................................................14

Global Off-Grid PV Markets© ...............................................................................16

Potential of Building-Integrated PV 2010 ..........................................................18

2. The European PV Market ..................................................................................... 21

PV Market Matrix© ................................................................................................22

European PV InstallerMonitor© 2011/12 .............................................................24

European PV InverterMonitor© ............................................................................26

PV BrandMonitor© 2011/12 – Europe ...................................................................28

PV Seal ...................................................................................................................30

European PV ModulePriceMonitor© ....................................................................32

PV SalesMonitor© – Germany ...............................................................................34

Dawning of a New Era – Photovoltaics on the Edge of Grid Parity ..................36

PV MarketMonitor© – Germany ...........................................................................38

Regional Market Attractiveness© – Germany ......................................................40

The German Photovoltaic Market 2010 ...............................................................42

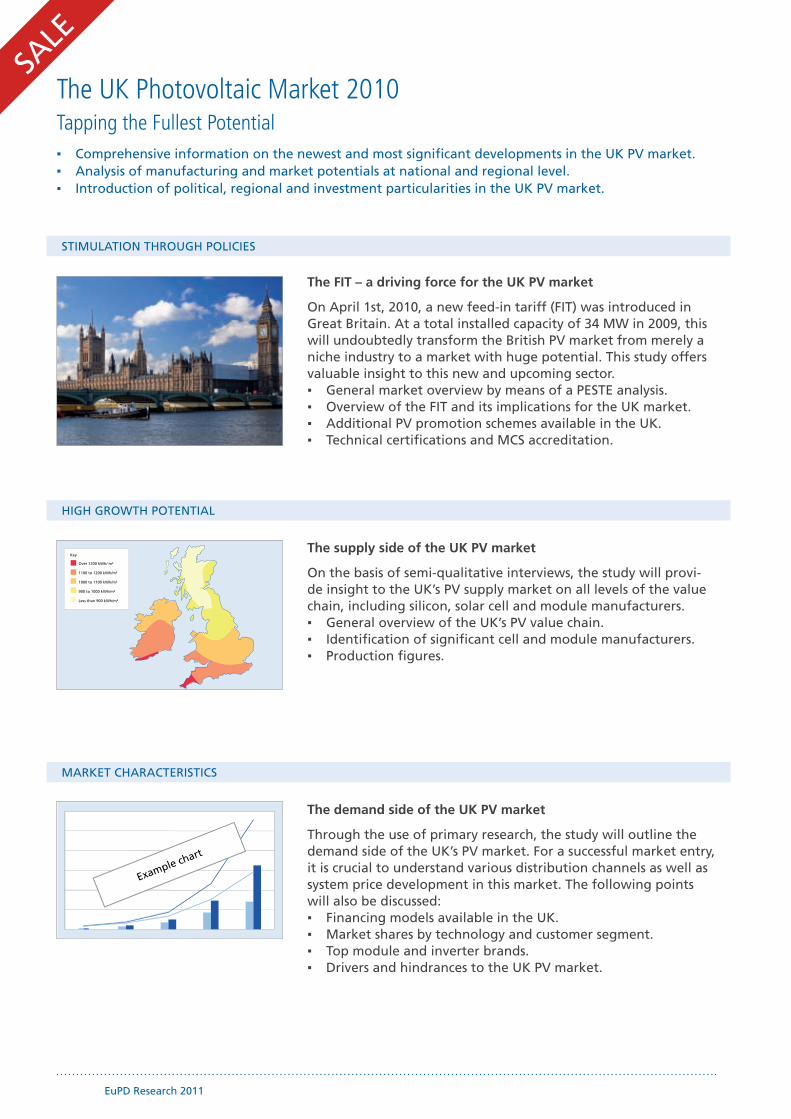

The UK Photovoltaic Market 2010 .......................................................................44

EuPD Research 2011 5

3. The US PV Market ................................................................................................. 47

US PV InstallerMonitor© 2011 ...............................................................................48

US PV BrandMonitor 2011© (East) ........................................................................50

US PV BrandMonitor 2011© (West) .......................................................................52

US PV ModulePriceMonitor© ...............................................................................54

4. The Asian PV Market ............................................................................................ 57

The Indian Photovoltaic Market 2010/11 ............................................................58

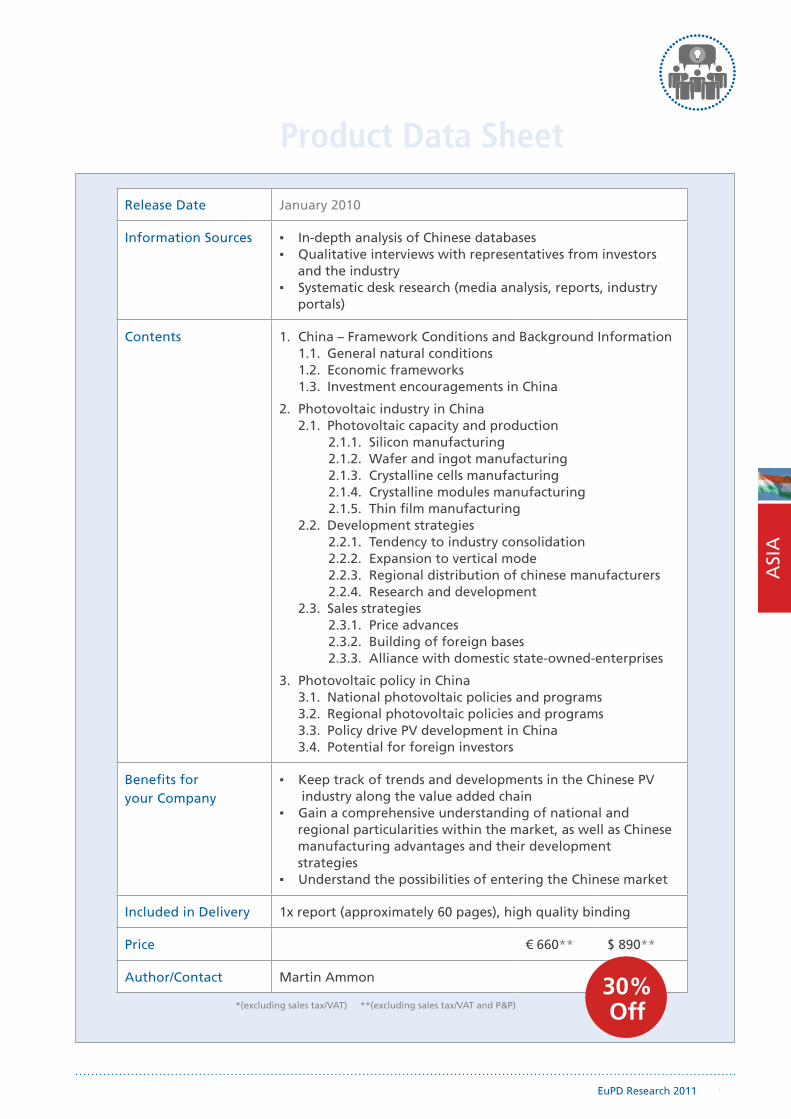

The Chinese PV Market .........................................................................................60

Imprint ....................................................................................................................... 62

6 EuPD Research 2011

The Hoehner Research & Consulting Group Value Cycle

We deliver comprehensive solutions from one source.

By applying an integrated approach, our customers

save time, reduce costs and mitigate risks in new,

highly dynamic markets.

By offering integrated business solutions

we maximize value for money:

Research, Consulting, Communications

Products & Services

Business Drivers

Your Added Value

CustomerYou

Des

ign

D

ialogue Data Research

Co

mm

unications Consulting Training

Ana

lysi

s

Com

pany/Organisation

Cust

omer

s

Co

mpe

titio

n

Market Enviroment

360

| Co

ncep

t

EuPD Research

360 | Consult

>>

>>>>

We maximize our customers value through

Market coverageGlobal approach ▪Local offices ▪Close to market ▪

Industry knowledgeIndustry Experience, high level of ▪

industry specific knowledgePublished more than 100 studies ▪Successfully accomplished ▪

1000+ projects

MethodologyProfound primary data due to ▪

own interview centerReliable secondary data elaborated ▪

on by our analytics divisionProven qualitative and quantitative ▪

market research

SustainabilitySustainable industries in focus ▪Balance between business and ▪

sustainabilityEconomic, ecologic and social ▪

perspectives

PeopleInterdisciplinary team ▪Multi-cultural, skilled, experienced ▪Cross-linked with excellent ▪

and reliable partners

EuPD Research 2011 7

As part of HRCG, EuPD Research provides customers with in-depth PV market research and consulting services. This document presents an overview of the products that EuPD Research currently offers. The catalogue does not include the variety of exclusive research or consulting projects which you can also order from us. The three types of products reflect our strategy of offering our customers various product types according to their requirements, e.g. depth of information, exclusivity and budget.

Customized services enable the generation and exploitation of strategic competitive advantages.

Our exclusive research projects are always targeted to your company specific ▪ information requirements.

You, as the client, determine the focus, extent and time frame of the survey. ▪The rights to use the findings are reserved exclusively for you. ▪

A limited number of customers ensure cost-efficient research.Our shared service projects ensure that our clients receive information that is ▪

not made available to everyone whilst sharing the costs for primary research. Where possible, we carry out exclusive analyses specifically for our shared ▪

service customers.

Detailed market surveys and information services for everyone.These products cover different scopes and markets in the field of PV. ▪The products differ with respect to focal points, theoretical bases, market ▪

data or actions recommended. Furthermore, informative news services delivered on a regular basis are also ▪

among our portfolio of products.

Individual requirements, competitive advantages, exclusiveness

EuPD Research – PV Research & Consulting Services

PV RMS – Maximize the value of your research

Our services will be available online via the PV Research Management System (PV RMS) provided by EuPD Research. It allows you to work immediately and flexibly via three online accounts*. This personal online version allows you …

» to have the product immediately at hand upon completion

» to exclusively access the digital version of the productyou ordered, enabling you to… download high resolution pages ▪ immediately make use of the documents, e.g. in presentations ▪ efficiently make use of products in further processes ▪

» to manage your information from anywhere in the world

» to store all relevant EuPD Research services – and your company‘s own research – in one place

» to alleviate communicate with your company’s subsidiaries worldwide

» to train your new employees in a more time-efficient and effective manner with the assistance of a centralized information management system

* You may purchase further accounts upon request.

Exclusive Services

Shared Services

Multi-Client Services

8 EuPD Research 2011

EuPD Research 2011 9

1. The Global PV Market

10 EuPD Research 2011

ADVANCED RESEARCH

MODELING TOOL

COMPANY PROFILING

ManufacturersMonitor© A Dynamic Modeling Tool for Analysis of PV Manufacturers Worldwide

The ManufacturersMonitor is a comprehensive tool that includes data about all manufacturers ▪ active in the PV value chain and forecasts demand and supply scenarios up to 2020.

The tool is delivered in the form of an Excel. ▪It is ownloadable via our PV-RMS online platform. ▪

Detailed company profiles

The Company Profiling Tool generates a detailed profile sheet including all data available for approximately 1,200 companies of all relevant levels of the value chain: silicon, wafer/ingot, cells, crystalline and thin-film modules.

The profile sheet provides general information, value chain pres-ence, latest news, capacity and production data from 2008-2015, financial information such as revenues, investments, EBIT, ASPs and stock performance.

Dynamic Modeling of Market and Manufacturers

This tool makes it possible to view and model the market and ma-nufacturers according to each value chain. In addition to viewing individual capacity and production data according to companies, the demand and supply situation of the whole value chain can be simulated using input variables such as company strength indica-tors and other forecasting conditions.

Analysis via customized options

As an addition, user friendly interfaces along with graphic displays are created that allow precise and one-stop-shop for customized analysis:

by company ▪by region/subregion ▪by value chain ▪by technology ▪by capacity or production level ▪

Japan webadress42

Stocklisted (Stock | Currency1) Asessement: 0

Production:

Vaue Chain Positioning:

C d t e C I G S a -S i µ -S i

Year-over-Year News:

Thin-film

Company47 | Company Information

14.10.2011

Headquarters:

Company Type:

Silicon Ingot Wafer Cell Panel

Poly Mono Poly

Web:

Mono Poly Mono Poly Mono

22.07.2011:PVTECH News: "News sample 1"*

09.06.2011:PV Magazine: "News sample 2.[...]"*

4.07.2011: Xyz PV Lowers Q2 2011 Revenue Guidance. For the second quarter of 2011, news sample 3[…]

EuPD ManufacturerMonitor

0 0Japan 0 0 0 0

Product Data Sheet

EuPD Research 2011 11

Information Sources Annual reports ▪Industrial sector analyses ▪Press reports ▪Telephone interviews ▪PV Executive News Summary ▪

Contents Production capacity covering years 2008 to 2020 ▪ including announced plans

Output covering years 2008 to 2020 ▪Data access on an aggregated level as well as on firm level ▪Output interface according to value chain and ▪

company locationFinancial information ▪Demand and supply situation (2008-2020) ▪Dynamic simulation of market and manufacturer ▪

performance up to 2020

Benefits for your Company

Analyze the entire value chain with a mouse click; from sili- ▪ con to wafers and ingots to crystalline and thin-film modules

Access data on 1,200 manufacturers around the world ▪ – either individually or according to specific criteria – and use it for a competitive analysis

Find information about production capacity and production ▪ either globally or organized according to country

Call up up-to-date data on prognoses from the present ▪ time to 2020

Price Single subscription Twelve month subscription

€ 5,900* € 9,500*

$ 8,100* $ 14,500*

Author/Contact Markus Lohr

Glo

bal

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

12 EuPD Research 2011

BENEFITS

PRODUCT THEME

PRODUCT BACKGROUND

PV Executive News Summary©

Overview of important daily news from global PV markets. ▪Saves time as the five most important news items are highlighted. ▪Biweekly publication of executive summaries. ▪

Product information

The following services are included:Daily monitoring and selection of relevant articles, based on ▪

the photovoltaic market from international online platforms and newsletters.

Classification of articles: company news is categorized accor- ▪ ding to the firms’ level on the value-added chain, other news according to main topics (market, politics, etc.)

Publication on a biweekly basis. ▪Articles in English ensuring a consistent information flow ▪

making it suitable for international companies.

Product objectives

The news overview delivers up-to-date and comprehensive infor-mation about:

International PV companies, new production sites, supply ▪ agreements, mergers and acquisitions, projects and install- ations as well as technological developments.

International PV market and political conditions, e.g. changes ▪ in funding conditions and country installation figures.

ContentsTop five news items ▪News along the value chain ▪Market and political news ▪Miscellaneous ▪

“Executive PV News Summary” will provide your company with decisive competitive advantages:

Continuous tracking of developments in the PV branch. ▪Quick and relevant information about partners. ▪

and competitors.The top 5 news items are highlighted informing about the ▪

most important PV news.Product can be customized according to your company profile. ▪

Source: EuPD Research April 2011

Product Data Sheet

EuPD Research 2011 13

Price Per month Per six months Per year

€ 295* € 1,600* € 3,100*

$390* $2,245* $3,100*

Author/Contact Daniel-Christian Quack

Glo

bal

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

14 EuPD Research 2011

MARKET OUTLOOK 2020

THE PV TECHNOLOGIES RACE & MANUFACTURERS´ STRATEGIC POSITIONING

STATUS QUO ANALYSIS – DEMAND AND SUPPLY UP TO 2011

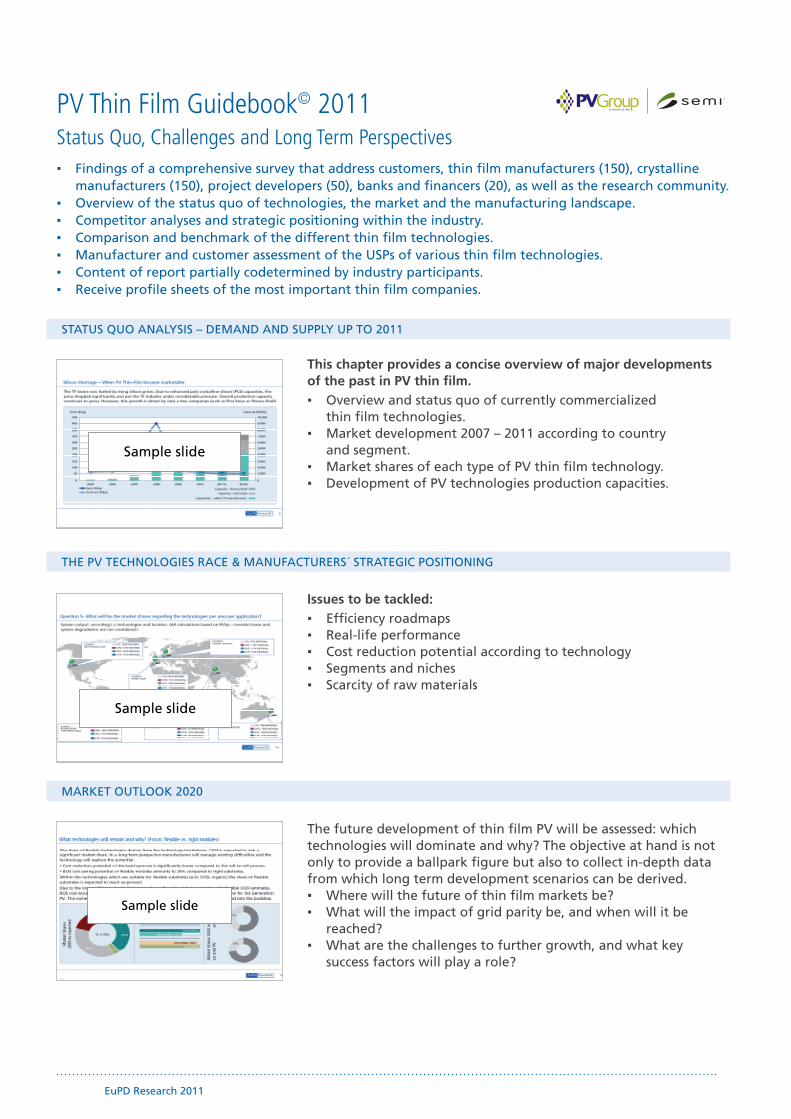

PV Thin Film Guidebook© 2011 Status Quo, Challenges and Long Term Perspectives

Findings of a comprehensive survey that address customers, thin film manufacturers (150), crystalline ▪ manufacturers (150), project developers (50), banks and financers (20), as well as the research community.

Overview of the status quo of technologies, the market and the manufacturing landscape. ▪Competitor analyses and strategic positioning within the industry. ▪Comparison and benchmark of the different thin film technologies. ▪Manufacturer and customer assessment of the USPs of various thin film technologies. ▪Content of report partially codetermined by industry participants. ▪Receive profile sheets of the most important thin film companies. ▪

This chapter provides a concise overview of major developments of the past in PV thin film.

Overview and status quo of currently commercialized ▪ thin film technologies.

Market development 2007 – 2011 according to country ▪ and segment.

Market shares of each type of PV thin film technology. ▪Development of PV technologies production capacities. ▪

Issues to be tackled:Efficiency roadmaps ▪Real-life performance ▪Cost reduction potential according to technology ▪Segments and niches ▪Scarcity of raw materials ▪

The future development of thin film PV will be assessed: which technologies will dominate and why? The objective at hand is not only to provide a ballpark figure but also to collect in-depth data from which long term development scenarios can be derived.

Where will the future of thin film markets be? ▪What will the impact of grid parity be, and when will it be ▪

reached? What are the challenges to further growth, and what key ▪

success factors will play a role?

Sample slide

Sample slide

Sample slide

Product Data Sheet

EuPD Research 2011 15

Release Date August 2011

Information Sources Quantitative interviews with thin film producers and ▪ market entrants

Qualitative interviews with analysts, academics and other ▪ stakeholders

Systematic desk research (external databases, business ▪ reports, etc.)

EuPD DAT – internal database (developed in over ten years ▪ of industry expertise)

Contents(Subject to change)

Acquire an overview of the status quo of the thin film industryRecent developments regarding supply and demand ▪Mapping of the current manufacturer landscape in the ▪

thin film industry

One industry but several technologies – who will win the race?Identification & analysis of key success factors ▪Technology benchmarks ▪First-hand information and assessments from market participants ▪

Ways to differentiate with increasingly commoditized products Comparison of unique selling positions (USPs) communicated ▪

by various manufacturersGap analysis of customer perception and manufacturer ▪

portrayal of USPsBest practice cases – what can a manufacturer do to achieve a USP ▪

Market outlook 2020 Collection of data and opinions regarding future market ▪

development (insights from Delphi-Survey)Impact assessment of different parities ▪

Special topic & company profiles The role of carbon footprint in PV ▪Profile sheets of the most important thin film companies ▪

Benefits for your company

Provides a comprehensive foundation for strategic decision ▪ making in a setting where thin film manufacturers face tightening global markets and increased competition

Receive profile sheets of the most important thin film companies ▪

Included in Delivery 1x report, high quality binding; a digital version is available on request

Price Standard For Semi Members (proof required)

€ 4,900** € 4,410**

$ 6,950** $ 6,190**

Author/Contact Rob van der Meulen and Juan Pablo Ralón-Fonseca

Glo

bal

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

16 EuPD Research 2011

PROJECT FINANCING AND FUTURE MARKET DEVELOPMENT

MARKET CONDITIONS ON COUNTRY LEVEL

GLOBAL OFF-GRID PV MARKET RATING

Global Off-Grid PV Markets©

In times of an oversupply of PV modules, off-grid PV offers a very promising alternative for market ▪ participants from the PV production and distribution sector.

This Q2/2009 chart report is based on primary research from more than 60 market players from the ▪ distribution and production sector of off-grid PV.

This report gives you comprehensive information on the most promising markets and their most ▪ important participants.

Identification and analysis of the international key regions

At the moment many PV producers are looking for new sales markets. But which are the regions with the biggest potential for off-grid PV? To answer this question EuPD Research carried out a country market rating based on a general market and specific off-grid PV market assessment. Afterwards, an analysis took into account the following aspects:

Current and future significance of electricity generation ▪ technologies.

Distribution of PV system components. ▪Unaided brand awareness of panel, inverter and battery ▪

producers.Important criteria when selecting PV modules and inverters. ▪Price comparison of PV panels and complete systems. ▪

Analysis of market segmentation as well as advantages and dis-advantages of the country markets

Along with the regions, the most relevant country markets within these regions were identified. In order to open up these new sales markets, it is crucial to know the necessary facts about the needs of the relevant customers. Based on the survey of 46 local distributors active in the key regions, learn more about the fol-lowing topics:

Current and future market segmentation regarding ▪ application types, customer groups, system sizes and module technologies.

Drivers and hindrances of the country market. ▪

Illustration of project financing methods and outlook on the further global market

Finally, EuPD Research provides qualitative information on several project financing methods and regarding a successful targeting of different end customer types and active market intermediaries.

The study closes with two scenarios of the further development of the global off-grid PV market until 2020. In a second step, EuPD Research calculated the likely development of the segmen-tation of the global off-grid PV market regarding application types up to 2020.

Total (n=40) Latin America (n=16)

productcharacteristics

delivery time/availability

warranty

service

quality

performance/efficiency

brand/certificates

financial aspects

awareness and experience of supplier/location of supplier

Product Data Sheet

EuPD Research 2011 17

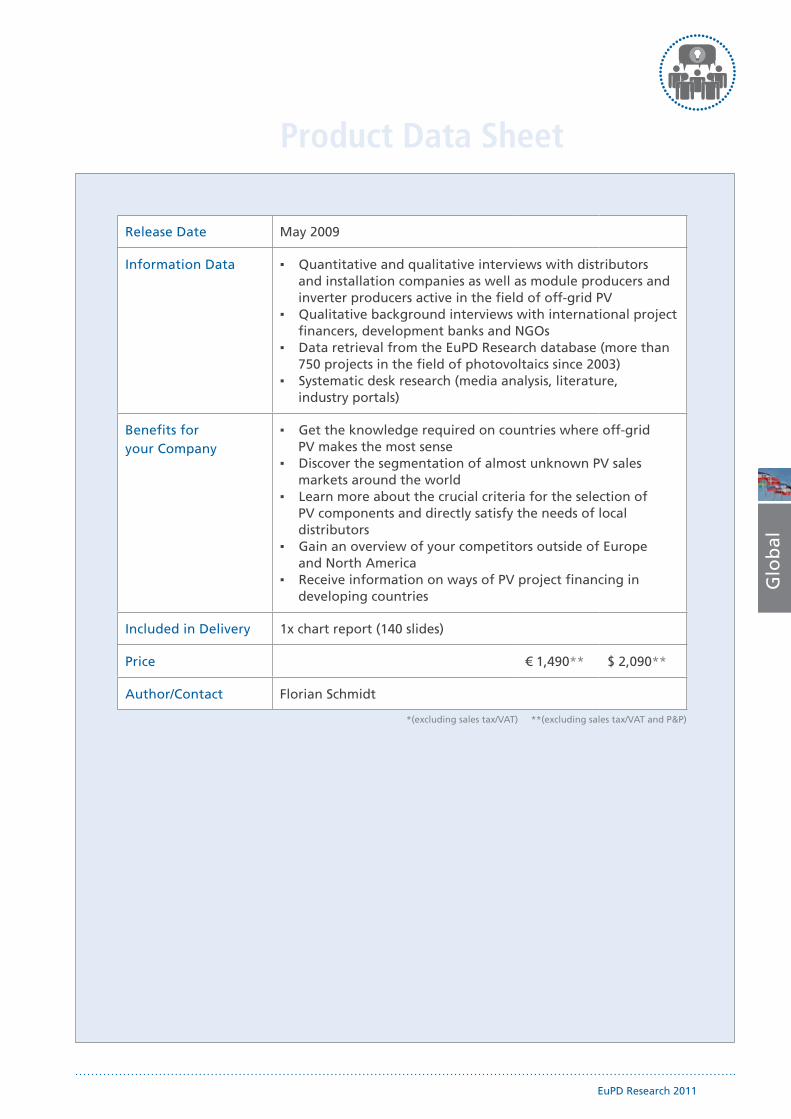

Release Date May 2009

Information Data Quantitative and qualitative interviews with distributors ▪ and installation companies as well as module producers and inverter producers active in the field of off-grid PV

Qualitative background interviews with international project ▪ financers, development banks and NGOs

Data retrieval from the EuPD Research database (more than ▪ 750 projects in the field of photovoltaics since 2003)

Systematic desk research (media analysis, literature, ▪ industry portals)

Benefits for your Company

Get the knowledge required on countries where off-grid ▪ PV makes the most sense

Discover the segmentation of almost unknown PV sales ▪ markets around the world

Learn more about the crucial criteria for the selection of ▪ PV components and directly satisfy the needs of local distributors

Gain an overview of your competitors outside of Europe ▪ and North America

Receive information on ways of PV project financing in ▪ developing countries

Included in Delivery 1x chart report (140 slides)

Price € 1,490** $ 2,090**

Author/Contact Florian Schmidt

Glo

bal

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

18 EuPD Research 2011

MARKET INTERMEDIARIES/END CUSTOMERS

SUPPLY OF BIPV PRODUCTS

MARKET ANALYSIS

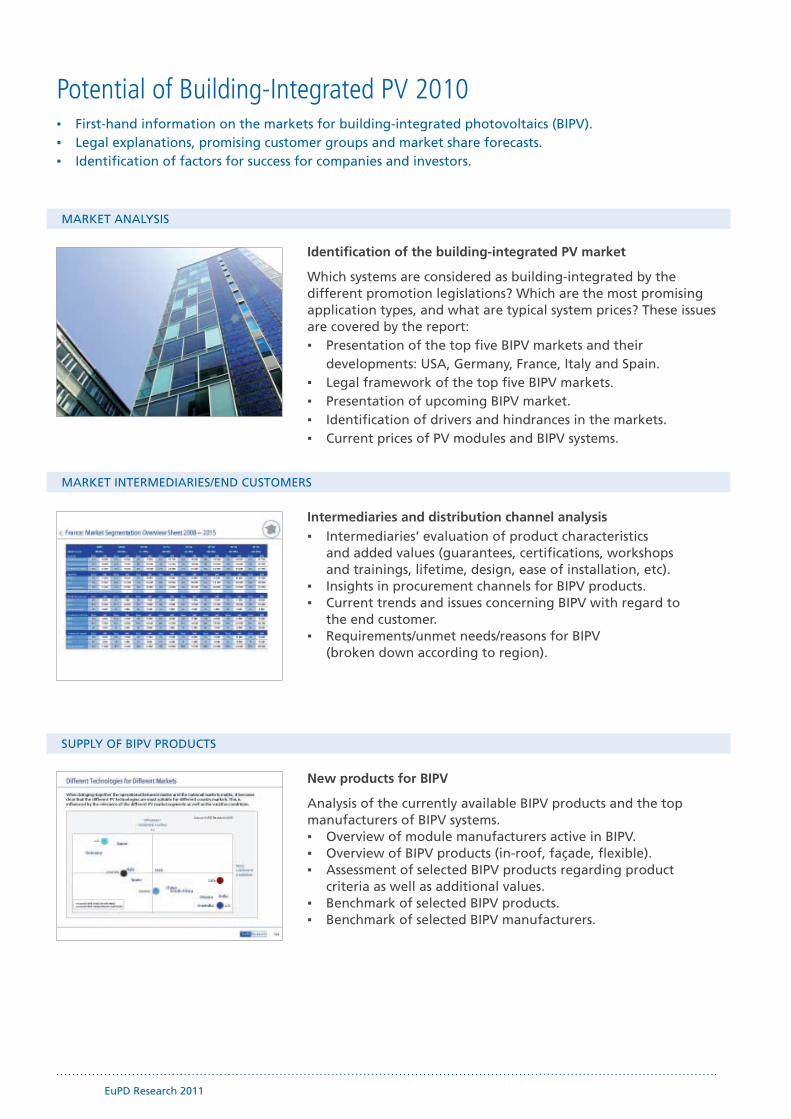

Potential of Building-Integrated PV 2010First-hand information on the markets for building-integrated photovoltaics (BIPV). ▪Legal explanations, promising customer groups and market share forecasts. ▪Identification of factors for success for companies and investors. ▪

Identification of the building-integrated PV market

Which systems are considered as building-integrated by the different promotion legislations? Which are the most promising application types, and what are typical system prices? These issues are covered by the report:

Presentation of the top five BIPV markets and their ▪ developments: USA, Germany, France, Italy and Spain.

Legal framework of the top five BIPV markets. ▪Presentation of upcoming BIPV market. ▪Identification of drivers and hindrances in the markets. ▪Current prices of PV modules and BIPV systems. ▪

Intermediaries and distribution channel analysisIntermediaries’ evaluation of product characteristics ▪

and added values (guarantees, certifications, workshops and trainings, lifetime, design, ease of installation, etc).

Insights in procurement channels for BIPV products. ▪Current trends and issues concerning BIPV with regard to ▪

the end customer.Requirements/unmet needs/reasons for BIPV ▪

(broken down according to region).

New products for BIPV

Analysis of the currently available BIPV products and the top manufacturers of BIPV systems.

Overview of module manufacturers active in BIPV. ▪Overview of BIPV products (in-roof, façade, flexible). ▪Assessment of selected BIPV products regarding product ▪

criteria as well as additional values.Benchmark of selected BIPV products. ▪Benchmark of selected BIPV manufacturers. ▪

Product Data Sheet

EuPD Research 2011 19

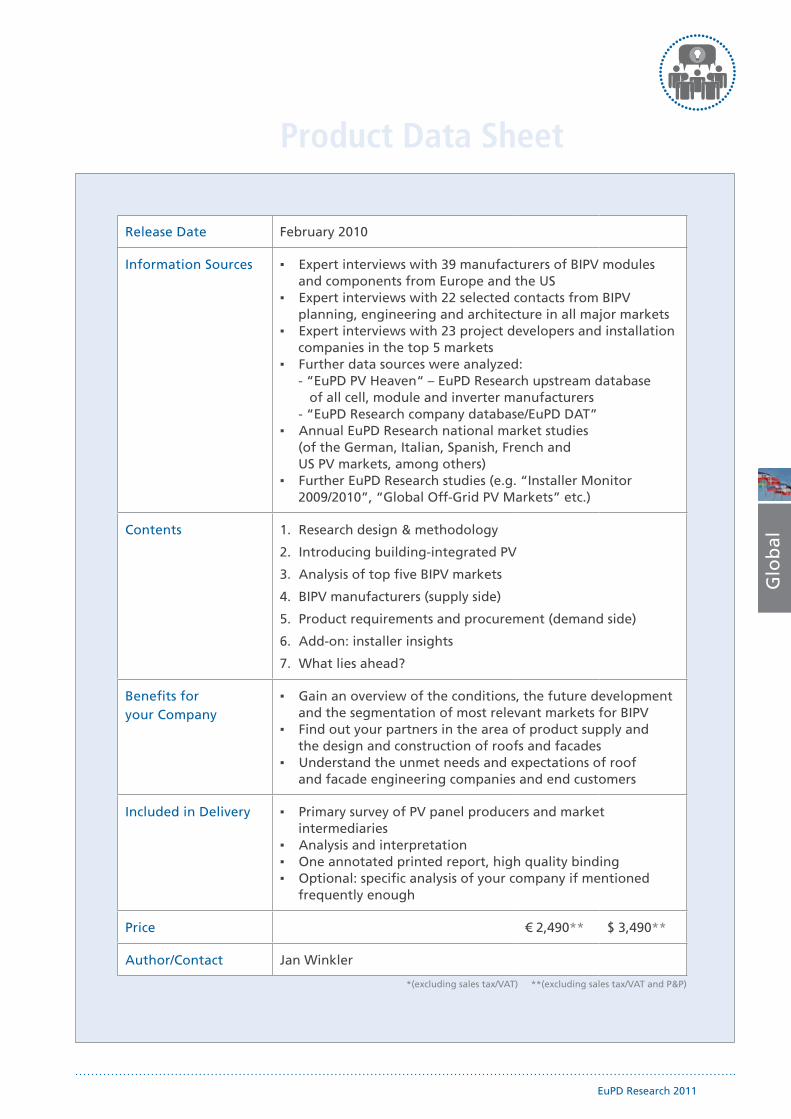

Release Date February 2010

Information Sources Expert interviews with 39 manufacturers of BIPV modules ▪ and components from Europe and the US

Expert interviews with 22 selected contacts from BIPV ▪ planning, engineering and architecture in all major markets

Expert interviews with 23 project developers and installation ▪ companies in the top 5 markets

Further data sources were analyzed: ▪ - “EuPD PV Heaven“ – EuPD Research upstream database of all cell, module and inverter manufacturers - “EuPD Research company database/EuPD DAT”

Annual EuPD Research national market studies ▪ (of the German, Italian, Spanish, French and US PV markets, among others)

Further EuPD Research studies (e.g. “Installer Monitor ▪ 2009/2010”, “Global Off-Grid PV Markets” etc.)

Contents Research design & methodology1.

Introducing building-integrated PV2.

Analysis of top five BIPV markets3.

BIPV manufacturers (supply side)4.

Product requirements and procurement (demand side)5.

Add-on: installer insights6.

What lies ahead?7.

Benefits for your Company

Gain an overview of the conditions, the future development ▪ and the segmentation of most relevant markets for BIPV

Find out your partners in the area of product supply and ▪ the design and construction of roofs and facades

Understand the unmet needs and expectations of roof ▪ and facade engineering companies and end customers

Included in Delivery Primary survey of PV panel producers and market ▪ intermediaries

Analysis and interpretation ▪One annotated printed report, high quality binding ▪Optional: specific analysis of your company if mentioned ▪

frequently enough

Price € 2,490** $ 3,490**

Author/Contact Jan Winkler

Glo

bal

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

20 EuPD Research 2011

EuPD Research 2011 21

2. The European PV Market

22 EuPD Research 2011

BACKGROUND

OBJECTIVES

ADVANTAGES

PV Market Matrix©

Dynamic tool to evaluate and compare PV country markets according to their appeal and investment risk. ▪Data aggregation guarantees reduction of complexity and compact information for decision maker level. ▪Quarterly updates ensure up-to-date information on changing investment conditions. ▪

Challenges for PV investments

Despite the strong growth of the European PV market, invest-ment decisions regarding PV have become more difficult. Also, the dynamic and volatility of PV market development has incre-ased. Reasons for this range from decreasing political support as grid parity approaches to major bureaucratic barriers.

Therefore, investing in PV requires both a sound understanding of the respective country markets as well as the capability of in-terpreting these insights with respect to individual needs.

Consideration of individual investment profiles

Feed-in-tariff

Country risk

Investment freedom

electricity prices (comm. & priv.)

Development of electricity prices

LCOE of PV systems / grid-parity

Profitability of net-metering

PV feed-in-tariff & irradiation

Irradiation

Availability of green certificates

Existence of green certificates

Independence from PV subsidies

General country conditions/risks

PV market sustainability

Stability of PV subsidy scheme

Grid capacity

Bureaucracy

PV market volume 2009, 2010, 2011

Grid capacity

Date of implementation

Perceived stability/instability

Price guarantee

General level of bureaucracy & corruption

Degree of bureaucracy in relevant segments

Perceived intensity of bureaucracy

Regional level of bureaucratic hurdles

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

Feed-in-tariff

Country risk

Investment freedom

electricity prices (comm. & priv.)

Development of electricity prices

LCOE of PV systems / grid-parity

Profitability of net-metering

PV feed-in-tariff & irradiation

Irradiation

Availability of green certificates

Existence of green certificates

Independence from PV subsidies

General country conditions/risks

PV market sustainability

Stability of PV subsidy scheme

Grid capacity

Bureaucracy

PV market volume 2009, 2010, 2011

Grid capacity

Date of implementation

Perceived stability/instability

Price guarantee

General level of bureaucracy & corruption

Degree of bureaucracy in relevant segments

Perceived intensity of bureaucracy

Regional level of bureaucratic hurdles

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

0 100

Systematic market analysis and evaluation option

The understanding of PV country markets requires knowledge of fundamental market data and relevant market trends. Thus, the “PV Market Matrix” provides:

an extensive database with quantitative information on more ▪ than 20 criteria relevant for determining the appeal and risk of investing in 30 European PV markets.

differentiation according to market segments (residential, ▪ commercial, open-space).

a quarterly update of these criteria. ▪the possibility to weight these criteria according to the indivi ▪

dual investment profile.

Reduced complexity of analyzed PV investment factors

The results of the individual weighting of the relevant criteria can be displayed in the “PV Market Matrix” from a “risk” and “profit” perspective.

Individual country rankings per mouse-click facilitate the ▪ optimal allocation of resources.

An ideal starting point for the elaboration of strategic options ▪ in finding the right target markets for PV investments.

Screenshots – Weighting the Overall Dimensions and Interpreting the Results

Consideration of individual investment profiles

Product Data Sheet

EuPD Research 2011 23

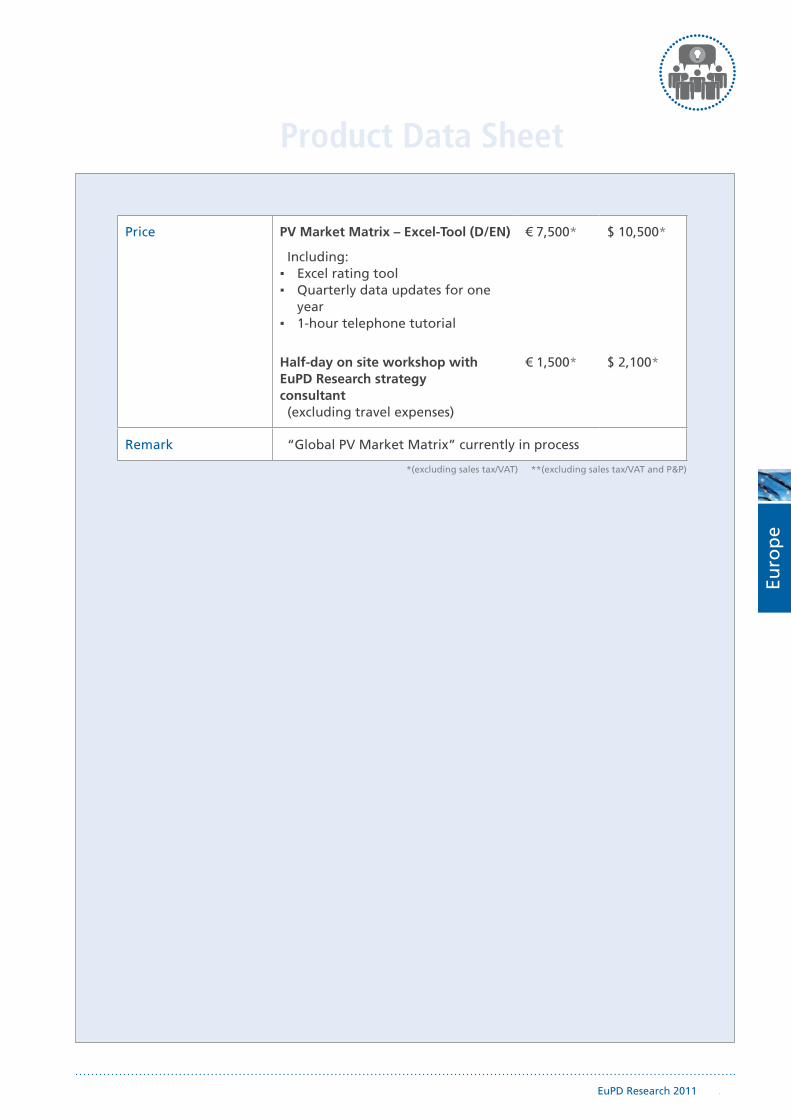

Price PV Market Matrix – Excel-Tool (D/EN)

Including:Excel rating tool ▪Quarterly data updates for one ▪year1-hour telephone tutorial ▪

Half-day on site workshop with EuPD Research strategy consultant (excluding travel expenses)

€ 7,500*

€ 1,500*

$ 10,500*

$ 2,100*

Remark “Global PV Market Matrix” currently in process

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

24 EuPD Research 2011

TURBULENT MARKET SITUATION IN KEY EUROPEAN PV MARKETS

GROWING IMPORTANCE OF EFFECTIVE AND EFFICIENT BRAND MANAGEMENT

THE NECESSITY OF BUILDING AND ExTENDING EFFECTIVE SALES CHANNELS

European PV InstallerMonitor© 2011/12 Procurement Management | Brand Significance | Sales Strategies

Receive comprehensive information on procurement management and distribution strategies from ▪ PV market intermediaries in the key European PV markets, Germany, Italy, France, Spain as well as UK, Belgium and Greece (optional).

Learn how installers, the gatekeepers to the end customer, perceive your brand. ▪Utilize markets insights to improve your current market situation as well as to identify promising ▪

business opportunities for the future.

Feed-in tariffs have been either cut or largely modified in all core European markets. As a result, market consolidation and compe-titive rivalry are on the increase. In order to remain successful in this challenging market situation, it is necessary to be up-to-date on the framework conditions and market figures of the key Euro-pean PV markets. Therefore, the study includes:

A detailed overview of framework conditions. ▪A display of market development and segmentation figures. ▪An identification of promising application types/customer ▪

groups etc.

The study will help you to increase or improve your sales channel activities. An insight into the procurement activities of installers is provided in order to support and secure this. Furthermore, both distribution activities and supplier strategies will be analyzed in detail. Amongst others, the following points will be covered:

Procurement channels. ▪Market positioning of the most important PV suppliers. ▪Distribution ranges of top PV module and inverter manufac- ▪

turers, as well as of top wholesalers.

On the basis of a large number of quantitative interviews, the study will provide a detailed impression of installer brand awa-reness and recognition in all sales markets subject to analysis. This will allow your company to successfully adjust its marketing strategies and brand management. For instance, the following essential aspects will be looked at:

Assessment of brand status, value and loyalty. ▪Reasons for selecting or not selecting a PV brand. ▪Benchmark of most important PV suppliers. ▪

Ab

ove

ave

rag

e im

po

rtan

ceB

elo

w a

vera

ge

imp

ort

ance

+30%

-30%

PriceTechnology Availability Prior experience Brand image

Price Technology Availability Prior experience Brand image

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

Ab

ove

ave

rag

e im

po

rtan

ceB

elo

w a

vera

ge

imp

ort

ance

+30%

-30%

PriceTechnology Availability Prior experience Brand image

Price Technology Availability Prior experience Brand image

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

BRAND

Sample chart

Sample chart

Sample chart

Product Data Sheet

EuPD Research 2011 25

Information Sources Standard package: Approx. 750 quantitative interviews with ▪ PV installers from Germany, Italy, France and Spain

Extended package (optional): UK, Belgium, Greece ▪Systematic desk research (external databases, business ▪

reports, etc.)EuPD DAT – internal database (quarterly EuPD studies, EuPD ▪

market reports, etc.)

Contents General Introduction I. BackgroundII. ContentsIII. Theoretical CommentsIV. Research Design V. Description of the Sample

Part I. – Germany A. Market AnalysisB. Procurement Management C. Market Penetration: Supplier Positioning D. Brand Management: Awareness and Image

Part II. – Spain A.-D. (as shown in Part I.)

Part III. – ItalyA.-D. (as shown in Part I.)

Part IV. – FranceA.-D. (as shown in Part I.)

Country Comparison

Benefits for your Company

Become part of an exclusive client group which receives ▪ comprehensive market knowledge at an attractive price

Fully understand installer attitudes, requirements and ex- ▪ pectations of PV components and supplier services based on the survey results

Identify the most promising sales markets and customer ▪ segments based on a detailed country comparison in order to increase sales margin

Included in Delivery Standard package: 1x report, high quality binding, digital ePaper and 1x Excel table reportExtended package: 1x seperate report for each country market

Price Standard packageExtended package: Standard packa-ge plus (Price depends on number of countries)

€ 14,900**€ 4,500 to € 7,500**

$ 22,900**$ 6,300 to $ 10,500**

Author/Contact René Mund and Stefano Reccia

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

26 EuPD Research 2011

SALES CHANNEL ARCHITECTURE

PRODUCT FEATURES AND SUCCESS FACTORS

VALUE OF BRAND MANAGEMENT

European PV InverterMonitor©

Recognize the main players in the most important European PV markets (Germany, Italy and France). ▪ This helps you to navigate within this fast moving industry.

Focus on downstream data in order to leverage your sales activities. ▪Receive comprehensive primary data-based information on the PV inverter market. ▪Understand installer behavior and dynamics in the market for an increasingly important system ▪

component. Learn how installers, the gatekeeper to the end customer, perceive different brands. ▪

The study will help you to extend and improve your sales channel activities. An insight into the procurement activities of installers is provided in order to support and secure this.

Furthermore, both distribution activities and supplier strategies will be analyzed in detail. Amongst others, installer procurement channels, distribution ranges of top PV inverter manufacturers as well as the market penetration of the most important PV inverter suppliers will be covered.

On the basis of more than 400 quantitative interviews, the study will provide a detailed impression of installer brand awareness and recognition. This will support your company in improving its marketing strategies and brand management.

The analyses include assessment of brand status, brand value and loyalty as well as the reasons for selecting or not selecting a spe-cific PV inverter brand. Furthermore a benchmark of most impor-tant PV inverter suppliers will be given. Brands covered include SMA, Fonius, Solarmax, Kaco, Danfoss or Mastervolt.

A substancial part of the report will cover the subject of product features required by the installer:

What are the features most desired by the installers? ▪Which technological developments have to be considered? ▪Which technological features are required? ▪The study will provide an overview with regard to current ▪

and future product characteristics of interest.This will provide you with additional knowledge to more ▪

accurately meet your customer requirements.

Source: EuPD Research 2010

Siemens (n=11)

SMA (n=201)

Schüco (n=9)

Mastervolt (n=9)

Kostal (n=24)

PowerOne (n=13)

Fronius (n=75)

Sunways (n=15)

Solarmax (n=31)

Kaco (n=41)

Danfoss (n=31)

Exclusive: no other thin-film module brands in installer's portfolio (proportion = 100%)Dominator: brand dominates installer's portfolio (proportion ≥ 50%) Complementary: brand influences the portfolio without dominating (proportion between 25% and 50%)Space-filler: brand has an inferior position in the installer's portfolio (proportion between 0% and 25%)

Source: EuPD Research 2010

Siemens (n=11)

SMA (n=201)

Schüco (n=9)

Mastervolt (n=9)

Kostal (n=24)

PowerOne (n=13)

Fronius (n=75)

Sunways (n=15)

Solarmax (n=31)

Kaco (n=41)

Danfoss (n=31)

Exclusive: no other thin-film module brands in installer's portfolio (proportion = 100%)Dominator: brand dominates installer's portfolio (proportion ≥ 50%) Complementary: brand influences the portfolio without dominating (proportion between 25% and 50%)Space-filler: brand has an inferior position in the installer's portfolio (proportion between 0% and 25%)

Exclusive: no other thin-film module brands in installer's portfolio (proportion = 100%)Dominator: brand dominates installer's portfolio (proportion ≥ 50%) Complementary: brand influences the portfolio without dominating (proportion between 25% and 50%)Space-filler: brand has an inferior position in the installer's portfolio (proportion between 0% and 25%)

Sample chart

Source: EuPD Research 2010

2008: n=245

2007: n=257

2009: n=249

2010: n=237

< 0%

> 0%

Market shares

> 6%

> 4% – 6%

0% – 4%

= 0%

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Company 1 48.3% 54.4% 54.8% 52.6% -2.2% SolarWorld 2.5% 1.0% 0.4% 0.6% 0.2%

Company 2 17.1% 14.7% 16.2% 9.8% -6.4% Refu 0.0% 0.0% 0.5% 0.5% 0.0%

Company 3 10.9% 8.4% 6.6% 7.8% 1.2% IBC Solar 0.0% 0.7% 0.8% 0.5% -0.3%

Company 4 3.2% 3.6% 2.5% 4.8% 2.3% Steca 0.0% 0.3% 0.4% 0.4% 0.0%

Company 5 0.0% 0.6% 1.5% 3.3% 1.8% Diehl 0.4% 0.2% 0.7% 0.4% -0.4%

Company 6 0.0% 2.2% 2.8% 2.9% 0.1% Conergy 1.0% 0.1% 0.3% 0.4% 0.1%

Company 7 0.0% 0.0% 1.5% 2.7% 1.2% Mitsubishi 0.0% 0.0% 0.0% 0.2% 0.2%

Company 8 1.6% 0.9% 0.5% 2.2% 1.7% AEG 0.0% 0.0% 0.1% 0.2% 0.1%

Company 9 0.0% 3.3% 1.5% 1.9% 0.4% Aixcon 0.0% 0.0% 0.0% 0.2% 0.2%

Company 10 2.0% 1.1% 0.4% 1.8% 1.4% Voltwerk 0.0% 0.0% 0.0% 0.2% 0.2%

Company 11 2.0% 1.8% 1.8% 1.8% 0.0% Other 10.8% 5.9% 6.5% 4.0%

Company 12 0.2% 0.7% 0.1% 0.8% 0.7%

Source: EuPD Research 2010

2008: n=245

2007: n=257

2009: n=249

2010: n=237

< 0%

> 0%

Market shares

> 6%

> 4% – 6%

0% – 4%

= 0%

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Company 1 48.3% 54.4% 54.8% 52.6% -2.2% SolarWorld 2.5% 1.0% 0.4% 0.6% 0.2%

Company 2 17.1% 14.7% 16.2% 9.8% -6.4% Refu 0.0% 0.0% 0.5% 0.5% 0.0%

Company 3 10.9% 8.4% 6.6% 7.8% 1.2% IBC Solar 0.0% 0.7% 0.8% 0.5% -0.3%

Company 4 3.2% 3.6% 2.5% 4.8% 2.3% Steca 0.0% 0.3% 0.4% 0.4% 0.0%

Company 5 0.0% 0.6% 1.5% 3.3% 1.8% Diehl 0.4% 0.2% 0.7% 0.4% -0.4%

Company 6 0.0% 2.2% 2.8% 2.9% 0.1% Conergy 1.0% 0.1% 0.3% 0.4% 0.1%

Company 7 0.0% 0.0% 1.5% 2.7% 1.2% Mitsubishi 0.0% 0.0% 0.0% 0.2% 0.2%

Company 8 1.6% 0.9% 0.5% 2.2% 1.7% AEG 0.0% 0.0% 0.1% 0.2% 0.1%

Company 9 0.0% 3.3% 1.5% 1.9% 0.4% Aixcon 0.0% 0.0% 0.0% 0.2% 0.2%

Company 10 2.0% 1.1% 0.4% 1.8% 1.4% Voltwerk 0.0% 0.0% 0.0% 0.2% 0.2%

Company 11 2.0% 1.8% 1.8% 1.8% 0.0% Other 10.8% 5.9% 6.5% 4.0%

Company 12 0.2% 0.7% 0.1% 0.8% 0.7%

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Company 1 48.3% 54.4% 54.8% 52.6% -2.2% SolarWorld 2.5% 1.0% 0.4% 0.6% 0.2%

Company 2 17.1% 14.7% 16.2% 9.8% -6.4% Refu 0.0% 0.0% 0.5% 0.5% 0.0%

Company 3 10.9% 8.4% 6.6% 7.8% 1.2% IBC Solar 0.0% 0.7% 0.8% 0.5% -0.3%

Company 4 3.2% 3.6% 2.5% 4.8% 2.3% Steca 0.0% 0.3% 0.4% 0.4% 0.0%

Company 5 0.0% 0.6% 1.5% 3.3% 1.8% Diehl 0.4% 0.2% 0.7% 0.4% -0.4%

Company 6 0.0% 2.2% 2.8% 2.9% 0.1% Conergy 1.0% 0.1% 0.3% 0.4% 0.1%

Company 7 0.0% 0.0% 1.5% 2.7% 1.2% Mitsubishi 0.0% 0.0% 0.0% 0.2% 0.2%

Company 8 1.6% 0.9% 0.5% 2.2% 1.7% AEG 0.0%

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Dis

trib

uti

on

ran

ge

2007

Dis

trib

uti

on

ran

ge

2008

Dis

trib

uti

on

ran

ge

2009

Dis

trib

uti

on

ran

ge

2010

abso

lute

ch

ang

ein

co

mp

aris

on

to 2

009

Company 1 48.3% 54.4% 54.8% 52.6% -2.2% SolarWorld 2.5% 1.0% 0.4% 0.6% 0.2%

Company 2 17.1% 14.7% 16.2% 9.8% -6.4% Refu 0.0% 0.0% 0.5% 0.5% 0.0%

Company 3 10.9% 8.4% 6.6% 7.8% 1.2% IBC Solar 0.0% 0.7% 0.8% 0.5% -0.3%

Company 4 3.2% 3.6% 2.5% 4.8% 2.3% Steca 0.0% 0.3% 0.4% 0.4% 0.0%

Company 5 0.0% 0.6% 1.5% 3.3% 1.8% Diehl 0.4% 0.2% 0.7% 0.4% -0.4%

Company 6 0.0% 2.2% 2.8% 2.9% 0.1% Conergy 1.0% 0.1% 0.3% 0.4% 0.1%

Company 7 0.0% 0.0% 1.5% 2.7% 1.2% Mitsubishi 0.0% 0.0% 0.0% 0.2% 0.2%

Company 8 1.6% 0.9% 0.5% 2.2% 1.7% AEG 0.0% 0.0% 0.1% 0.2% 0.1%

Company 9 0.0% 3.3% 1.5% 1.9% 0.4% Aixcon 0.0% 0.0% 0.0% 0.2% 0.2%

Company 10 2.0% 1.1% 0.4% 1.8% 1.4% Voltwerk 0.0% 0.0% 0.0% 0.2% 0.2%

Company 11 2.0% 1.8% 1.8% 1.8% 0.0% Other 10.8% 5.9% 6.5% 4.0%

Company 12 0.2% 0.7% 0.1% 0.8% 0.7%

0.0% 0.1% 0.2% 0.1%

Company 9 0.0% 3.3% 1.5% 1.9% 0.4% Aixcon 0.0% 0.0% 0.0% 0.2% 0.2%

Company 10 2.0% 1.1% 0.4% 1.8% 1.4% Voltwerk 0.0% 0.0% 0.0% 0.2% 0.2%

Company 11 2.0% 1.8% 1.8% 1.8% 0.0% Other 10.8% 5.9% 6.5% 4.0%

Company 12 0.2% 0.7% 0.1% 0.8% 0.7%

Sample chart

“How important you consider the following control and MV connection features?”

Product features

Bi-directional communication

VAR support

Remote VAR control

Anti-Islanding

Total ## ## ## ##

Static and dynamic VAR control

2.33

##

Frequency response

3.002.672.75 2.002.38

Over and under voltage protection

2.13 2.502.501.67 2.002.14

2.33 3.252.401.75 2.472.43

2.22 3.252.832.00 2.292.46

1.75 3.002.672.33 2.152.26

1.71 2.002.331.33 2.132.00

1.44 2.502.331.751.92 1.93

very important1 42 important 3 of average relevance of less relevance not important at all5 (mean values)

“How important you consider the following control and MV connection features?”

Product features

Bi-directional communication

VAR support

Remote VAR control

Anti-Islanding

Total ## ## ## ##

Static and dynamic VAR control

2.33

##

Frequency response

3.002.672.75 2.002.38

Over and under voltage protection

2.13 2.502.501.67 2.002.14

2.33 3.252.401.75 2.472.43

2.22 3.252.832.00 2.292.46

1.75 3.002.672.33 2.152.26

1.71 2.002.331.33 2.132.00

1.44 2.502.331.751.92 1.93

very important1 42 important 3 of average relevance of less relevance not important at all5 (mean values)

Sample chart

EuPD Research 2011 27

Product Data Sheet

Information Sources Quantitative interviews with installation companies in the ▪ key European PV markets

Systematic desk research (external databases, business ▪ reports, etc.)

EuPD DAT – internal market & industry database ▪

Contents(Subject to change)

Executive SummaryPart I. – Industry Overview ▪Part II. – Brand Awareness ▪Part III. – Procurement Behavior ▪Part IV. – Price Development ▪Part V. – Product Characteristics ▪Part VI. – Conclusion ▪

Benefits for your Company

Receive helpful information in order to develop innovative ▪ marketing strategies

Realize the dynamics of this rapidly changing industry to ▪ gain a competitive advantage

Better understand customer attitudes, requirements and ▪ expectations with regard to PV inverters

Leverage your sales efforts by efficiently targeting customer ▪ expectations in order to increase sales margin

Included in Delivery 1x report, high quality binding

Price € 4,950** $ 6,900**

Author/Contact Stefan Pietzsch

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

28 EuPD Research 2011

BRAND AWARENESS

PRICE SITUATION AND FUTURE TRENDS

NEW: FORECAST SCENARIO OF MODULE PRICE DEVELOPMENT

PV BrandMonitor© 2011/12 – Europe Analysis of brand awareness enjoyed by solar manufacturers in the German photovoltaic market. ▪Additional important European Markets (Italy, France and UK) will be analyzed for the first time this year ▪Compare the position of your company brand with that of your competitors. ▪Results based on more than 1,000 quantitative interviews in Germany and 500 interviews each in the ▪

other countries conducted in autumn 2011.

Analysis of the brand and brand awareness

The value of a brand is not anchored within a company but rather it is reflected in the minds of consumers. With a very high market share, private end consumers constitute the most impor-tant consumer group in the European countries surveyed.

The PV BrandMonitor analyzes the brand awareness and asso-ciations that individuals have with solar manufacturers using a survey of the population.

Survey contents

EuPD Research has been conducting surveys on this topic every year since 2006 among 1,000 German citizens aged 18 and up.

The analysis provides answers to the following questions: ▪Do citizens know the brand names of solar products? ▪If they do, where did they get their information from? ▪What characteristics do they associate with the individual ▪

brands?What role does the brand play in purchase decisions? ▪

Price situation and developmentFor the analysis, the participants will be divided into Nielsen ▪

regions in Germany or regions in the other countries.The dataset will be weighted on the basis of age and sex ▪

variations within the regions towards comparable specifica- tions of the Federal Statistical Office Annual Book (Germany).

The data has been analyzed by means of univariate and ▪ bivariate procedures using SPSS.

Divisio n of the Sam p le into Niel sen Re gions

EuPD Research 2011 29

Product Data Sheet

Release Date January 2012

Information Sources Representative, nationwide random sample ▪CATI-survey of persons aged 18 years and older ▪Survey by the last-birthday-method within a household ▪1,000 questionnaires answered in Germany, 500 each in Italy, ▪

France and UKSurvey period: November/December 2011 ▪

Contents Basic Version:

Background of the Study 1.

Objectives, Method and Sample 2.

Composition of the Sample3.

Owner and Planner of a Solar Plant4.

Attitude and Reception Analysis5.

Brand Analysis 6.

Conclusion 7.

Exclusive Version:

If your company is mentioned more than 30 times, an exclusive analysis of your brand name can be conducted in comparison to other well-known solar brands.

1. Individual Solar Brand Analysis (brand awareness in different subgroups, associations with your brand and illustration of different attributes)

2. Regional Analysis (comparison of brand awareness on a regional level)

Benefits for your Company

Compare the position of your company brand to that of ▪ your competitors

Monitor the success of your advertising ▪Advertise on the channels that end customers use to inform ▪

themselves about solar energyAdjust your advertising messages to suit the consumer types ▪

identifiedLearn more about the end customer attitudes toward ▪

certain energy topicsDesign your brand image on the basis of the status quo ▪Better assess the positioning of your competitors ▪

Included in Delivery Printed annotated report (min. 50 pages), high quality binding

Price Basic version per country Exclusive version per country

€ 5,500** € 9,500**

$ 8,900** $ 14,900**

Author/Contact Richard Peikert

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

30 EuPD Research 2011

THE EUPD RESEARCH PV SEAL | SUCCESSFUL BRAND MANAGEMENT

MULTIPLE BENEFITS FOR YOU AND YOUR CUSTOMERS

VALUE COMBINATION OF THE TWO EUPD RESEARCH FLAGSHIP PRODUCTS

PV Seal 2011/12Module and inverter producers profi t by differentiating themselves from their competitors. ▪The PV Seal increases credibility and create trust among end customers and business partners. ▪Digital PV Seal for direct use in all online and print media plus creation of an offi cial seal certifi cate. ▪

For brand management to be successful, a brand should be independent and possess differentiating functional or emotional characteristics in order to be desirable. Only then does it have its own specifi c signature making it distinguishable and recogniz-able. Based on more than ten years of research, EuPD Research has developed an evaluation model to emphasize the aspects of successful brand management – the basis of the PV Seal.

So far awards in the photovoltaic branch have focused only on the technical aspects of the various module and inverter manufacturers. Currently, there is no seal representative of the attitudes of quali-fi ed installers and end customers to the brands they buy. EuPD Research took this as an an impetus to create the PV seal which combines the results from the PV InstallerMonitor and the PV BrandMonitor relevant for brand differentiation.

Manufacturers of PV panels and inverters benefi t from the ▪ results of our independent analyses, increase credibility and create trust among end customers and business partners. As the seal can be integrated fl exibly into any marketing strategy, companies receive a multi-purpose design element to differentiate themselves from their competitors. The accompanying communications material contributes signifi - cantly to brand perception.

Market intermediaries can use the “Top Brand PV” seal to ▪ differentiate their portfolios from the competition. This enables cost-effi cient marketing measures, at no extra cost for your intermediaries.�

End customers can use the seal for the reduction of uncer- ▪ tainty in the buying process as it can be easily understood by end customers.

PV Seal

Image

Brand Awareness

CoherentIndependent

Results

Free Benefits for Intermediaries

Holistic

Approach

EuPD Research PV Seal

Communications

Support

Distinguishing Features

Strengthens Corporate Identity

Differentiation

EuPD Research – Shared Services

PV InstallerMonitor©

EuPD Research – Shared Services

PV InstallerMonitor

EuPD Research – Multi Client Services

PV BrandMonitor©

EuPD Research 2011 31

Product Data Sheet

Euro

pe

Information Sources PV InstallerMonitor®

PV BrandMonitor®

Included Delivery PV Seal 2011/12 (EPS, JPG, GIF or PNG) for direct use online ▪ and in print media

Only available for the Top 20 PV brands and to participants ▪ of the PV InstallerMonitor and the PV BrandMonitor

Creation of an official seal certificate to be given to ▪ intermediaries (PDF)

Press release to the EuPD journalist network ▪Info-Mail to be sent to over 10,000 relevant intermediaries ▪

in the most important PV marketsBrand mentioned in the EuPD Research Corporate Newsletter, ▪

with more than 4,000 recipients from all levels of the PV value chain

Country Options: Germany (Italy, France, and UK are to be offered soon)

Price For use until 31/12/2012 € 10,000** $ 13,990**

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

32 EuPD Research 2011

PRODUCT AND APPLICATION

PRICE SITUATION AND FUTURE TRENDS

NEW: FORECAST SCENARIO OF MODULE PRICE DEVELOPMENT

European PV ModulePriceMonitor©

Quarterly panel research to measure the price of PV modules and PV systems in Germany, Spain, ▪ Italy and France.

Display of price climate based on the current pricing situation and the expected development ▪ and forecast.

Module prices of the most installed brands for the three different module technologies. ▪

Composition of the European PV ModulePriceMonitor

As part of an exclusive customer group you will be able to access the results of the quarterly Europe-wide survey on PV installers at a preferential price. The goal of this product is to collect specific information on price developments in the most important Euro-pean PV markets (GER, IT, FR, ES). It includes:

Relative shares and purchase prices of the three module ▪ technologies.

Current system sales prices for rooftop PV systems. ▪Actual module prices of the most used brands and country ▪

of origin (by headquarter) for the three different module technologies.

Analysis of price differences between certain groups of ▪ installers (e.g. grouped by different customer groups).

Method and advantages of the forecast scenario

A panel of installers, who can provide reliable statements on price development considering their product portfolios and sales volumes, will be asked in every quarter about the future trend of prices of crystalline and thin film modules:

There will be a short-term (3 month) price forecast for three ▪ different module technologies in Eurocent.

Price changes can be compared to current prices, and a pro- ▪ gressive price forecast can be developed.

Price forecasts will reveal information about the installers’ ▪ perception of prices and will give market players the possibi- lity to react to short term changes.

Price situation and development

To determine a sustainable price policy, it is important for every company active in the PV market to observe the price develop-ments of the most significant photovoltaic markets:

Price levels and expectations for the different technologies. ▪Net purchase prices and price development for the three ▪

different module types (mono, polycrystalline and thin film).Price index for panel technologies. ▪Current system sales prices for rooftop PV systems (sales price ▪

for systems 3-10 kWp, 30-50 kWp, 300 kWp, 1,000 kWp open- space), plus cost breakdown for system <30 kWp.

Nominal interest rate regarding capital return. ▪

2.07

3.172.91

2.582.15

1.5 €

2.0 €

2.5 €

3.0 €

3.5 €

4.0 €

Source: EuPD Research 11/2009

Ger

man

y

Spai

n

Ital

y

2.04

2.53

3.242.92

2.25

1.5 €2.0 €2.5 €3.0 €3.5 €4.0 €

2.01

2.392.80

3.053.27

1.5 €2.0 €2.5 €3.0 €3.5 €4.0 €

2.80

3.863.33 3.26

2.66

1.5 €2.0 €2.5 €3.0 €3.5 €4.0 €

Fran

ce

Q2 2009 Q3 2009 Q1 2010 Q4 2009 Q2 2010

22.007722.1155

22.004422..2255

22.0011

2..39

2.8022.6666

* example figures

Domestic

No name manufacturer

brand Foreign brand

ES

FR

IT

GER

98,4%

93,6%

87,1%86,5%

85,5%

89,7%88,6%

95,1%

90,1%

86,6%

89,5% 87,5%

89,5%91,1%

86,6%87,5%

88,2%

95,3%

90,6%89,3%

90,6%

93,6%93,6%94,3%

100,0%

80%

85%

90%

95%

100%

105%

Bezug Q2 2006 3. Quartal 2006 4. Quartal 2006 1. Quartal 2007 2. Quartal 2007 3. Quartal 2007 4. Quartal 2007 1. Quartal 2008 2. Quartal 2008 3. Quartal 2008

monokristalline Module polykristalline Module Dünnschicht-Module Start: 2. Quartal 2006 = 100%

Quelle: EuPD Research 08/2008

Preisindex PV-Module

%

93,6%

89,7%%88,6%

90,1%

86,6%

89,5% 87,5%

89,5%91,1%

93,6%93,6%994,,3%

1. Quartal 2007 2. Quartal 2007 3. Quartal 2007 4. Quartal 2007

Für das 3. Quartal 2006 sind keine Angaben verfügbar

Module technology price index (weighted by technology shares)

3.7003.800

3.9003.9004.1344.158

4.392 4.373

4.8504.800

5.100 5.200

0 €

1.000 €

2.000 €

3.000 €

4.000 €

5.000 €

6.000 €

7.000 €

2. Quartal 2008 3. Quartal 2008 2. Quartal 2008 3. Quartal 2008

Minimum Mittelwert Maximum

Quelle: EuPD Research 08/2008

Wie hoch ist derzeit der Systempreis für eine PV-Aufdachanlage pro kWp?

Anlage unter 10 kWp Anlage zwischen 10 und 100 kWp

n = 100

System price development andcomparison of prices by different sizes

41,2 44,039,1 39,8 37,1 39,8 38,3 39,0

52,7 49,853,8 51,5 53,8 49,2 52,0 52,6

6,2 6,2 7,0 8,8 9,1 11,0 9,7 8,4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

4. Quartal 2006 1. Quartal 2007 2. Quartal 2007 3. Quartal 2007 4. Quartal 2007 1. Quartal 2008 2. Quartal 2008 3. Quartal 2008

monokristalline Module polykristalline Module Dünnschicht-Module

Quelle: EuPD Research 08/2008

Entwicklung der Anteile der PV-Modultechnologien an der installierten Leistung im Quartalsvergleich

n = 100

Development of technology shares41,2 44,0

39,1 39,8 37,1 39,8 38,3 39,0

52,7 49,853,8 51,5 53,8 49,2 52,0 52,6

6,2 6,2 7,0 8,8 9,1 11,0 9,7 8,4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

4. Quartal 2006 1. Quartal 2007 2. Quartal 2007 3. Quartal 2007 4. Quartal 2007 1. Quartal 2008 2. Quartal 2008 3. Quartal 2008

monokristalline Module polykristalline Module Dünnschicht-Module

Quelle: EuPD Research 08/2008

Entwicklung der Anteile der PV-Modultechnologien an der installierten Leistung im Quartalsvergleich

n = 100

Development of technology shares-3,61

0,770,70

1,64

0,96

2,49

0,97

0,31

5,00

-1,92

1,74

0,000,63

3,47

-0,96

0,00

-4,0%

-3,0%

-2,0%

-1,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

deutscheMarkenhersteller

ausländischeMarkenhersteller

ausländische No-Name-Hersteller

deutscheMarkenhersteller

ausländischeMarkenhersteller

ausländische No-Name-Hersteller

deutscheMarkenhersteller

ausländischeMarkenhersteller

1. Quartal bis 2. Quartal 2008 2. Quartal bis 3. Quartal 2008

Quelle: EuPD Research 08/2008

Wie haben sich die Netto-Einkaufspreise zwischen dem ersten Quartal 2008 und dem zweiten Quartal 2008 zu dem zweiten und dritten Quartal 2008 verändert (Mittelwerte)?

n = 100

monokristalline Module polykristalline Module Dünnschicht-Module

Development of net purchase prices-3,61

0,770,70

1,64

0,96

2,49

0,97

0,31

5,00

-1,92

1,74

0,000,63

3,47

-0,96

0,00

-4,0%

-3,0%

-2,0%

-1,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

deutscheMarkenhersteller

ausländischeMarkenhersteller

ausländische No-Name-Hersteller

deutscheMarkenhersteller

ausländischeMarkenhersteller

ausländische No-Name-Hersteller

deutscheMarkenhersteller

ausländischeMarkenhersteller

1. Quartal bis 2. Quartal 2008 2. Quartal bis 3. Quartal 2008

Quelle: EuPD Research 08/2008

Wie haben sich die Netto-Einkaufspreise zwischen dem ersten Quartal 2008 und dem zweiten Quartal 2008 zu dem zweiten und dritten Quartal 2008 verändert (Mittelwerte)?

n = 100

monokristalline Module polykristalline Module Dünnschicht-Module

Development of net purchase prices

EuPD Research 2011 33

Product Data Sheet

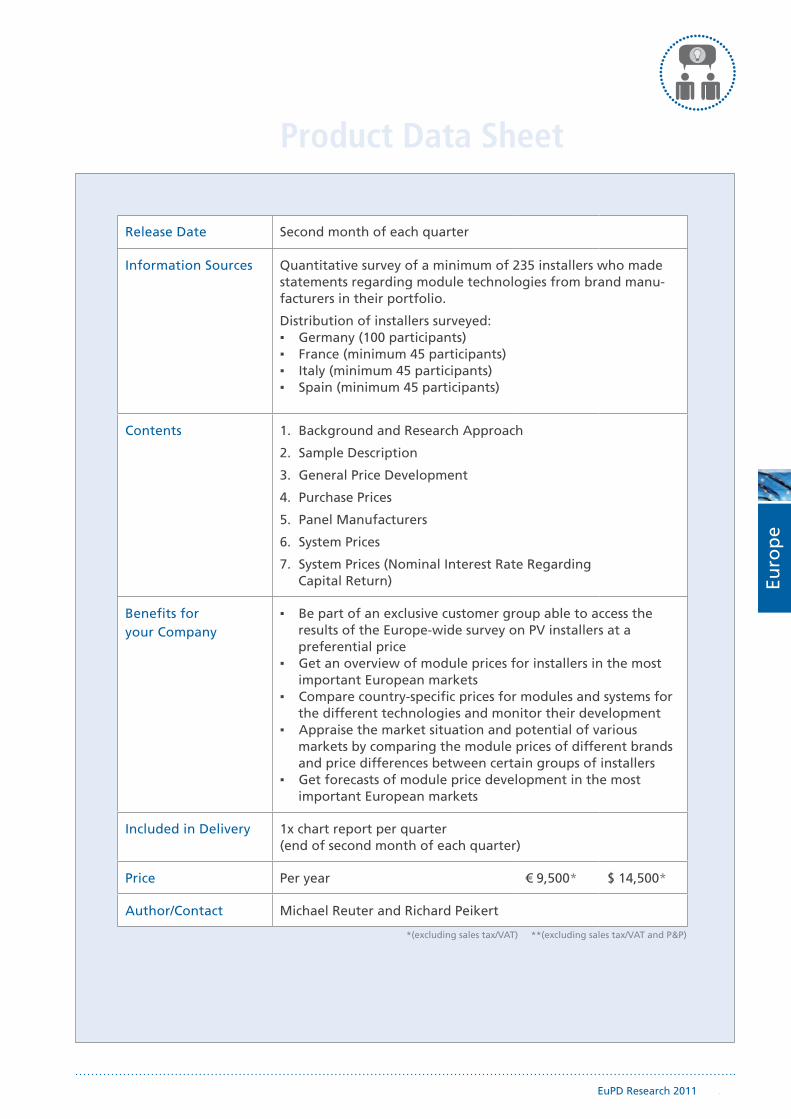

Release Date Second month of each quarter

Information Sources Quantitative survey of a minimum of 235 installers who made statements regarding module technologies from brand manu-facturers in their portfolio.

Distribution of installers surveyed:Germany (100 participants) ▪France (minimum 45 participants) ▪Italy (minimum 45 participants) ▪Spain (minimum 45 participants) ▪

Contents Background and Research Approach1.

Sample Description2.

General Price Development3.

Purchase Prices4.

Panel Manufacturers5.

System Prices6.

System Prices (Nominal Interest Rate Regarding 7. Capital Return)

Benefits for your Company

Be part of an exclusive customer group able to access the ▪ results of the Europe-wide survey on PV installers at a preferential price

Get an overview of module prices for installers in the most ▪ important European markets

Compare country-specific prices for modules and systems for ▪ the different technologies and monitor their development

Appraise the market situation and potential of various ▪ markets by comparing the module prices of different brands and price differences between certain groups of installers

Get forecasts of module price development in the most ▪ important European markets

Included in Delivery 1x chart report per quarter (end of second month of each quarter)

Price Per year € 9,500* $ 14,500*

Author/Contact Michael Reuter and Richard Peikert

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

34 EuPD Research 2011

MODULE 1: ExCEL-TOOL

MODULE 2: CHART REPORT

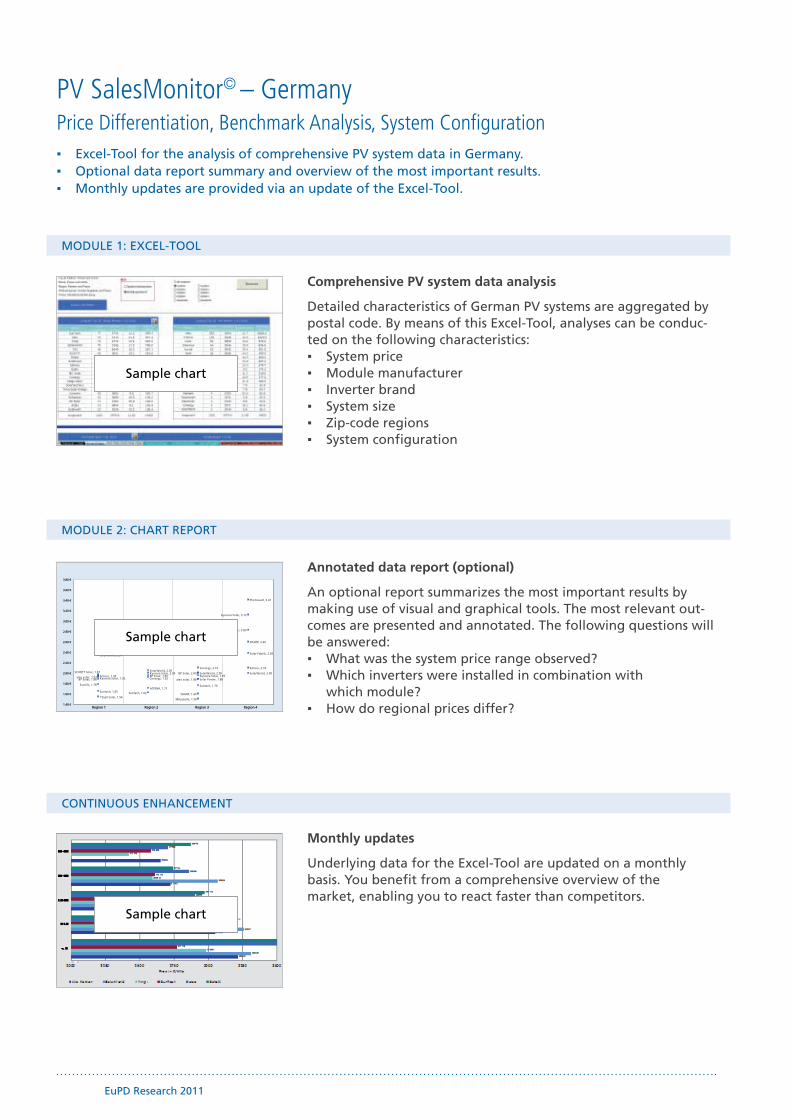

PV SalesMonitor© – Germany Price Differentiation, Benchmark Analysis, System Configuration

Excel-Tool for the analysis of comprehensive PV system data in Germany. ▪Optional data report summary and overview of the most important results. ▪Monthly updates are provided via an update of the Excel-Tool. ▪

Comprehensive PV system data analysis

Detailed characteristics of German PV systems are aggregated by postal code. By means of this Excel-Tool, analyses can be conduc-ted on the following characteristics:

System price ▪Module manufacturer ▪Inverter brand ▪System size ▪Zip-code regions ▪System configuration ▪

Annotated data report (optional)

An optional report summarizes the most important results by making use of visual and graphical tools. The most relevant out-comes are presented and annotated. The following questions will be answered:

What was the system price range observed? ▪Which inverters were installed in combination with ▪

which module?How do regional prices differ? ▪

aleo solar, 1.93aleo solar, 1.88

SCHOTT Solar, 1.97

SCHOTT Solar, 2.83

Schüco, 1.95

Schüco, 2.10

SolarWorld, 2.34

SolarWorld, 2.05SolarWorld, 2.00 SolarWorld, 2.00

Sovello, 1.78

BP Solar, 1.95Kyocera Solar, 2.00

Kyocera Solar, 1.95

Suntech, 1.65

Suntech, 1.76

Yingli Solar, 1.54

ATERSA, 1.71

Conergy, 2.10

Solar Power, 1.88

Mitsubishi, 1.50

SHARP, 2.60

Photowatt, 3.41

Solar-Fabrik, 2.38

BP Solar, 2.00

BP Solar, 1.88 Kyocera Solar, 1.92

Kyocera Solar, 3.12

Suntech, 1.62

Conergy, 1.92

SHARP, 1.60

1.40 €

1.60 €

1.80 €

2.00 €

2.20 €

2.40 €

2.60 €

2.80 €

3.00 €

3.20 €

3.40 €

3.60 €

3.80 €

Region 1 Region 2 Region 3 Region 4

aleo solar, 1.93aleo solar, 1.88

SCHOTT Solar, 1.97

SCHOTT Solar, 2.83

Schüco, 1.95

Schüco, 2.10

SolarWorld, 2.34

SolarWorld, 2.05SolarWorld, 2.00 SolarWorld, 2.00

Sovello, 1.78

BP Solar, 1.95Kyocera Solar, 2.00

Kyocera Solar, 1.95

Suntech, 1.65

Suntech, 1.76

Yingli Solar, 1.54

ATERSA, 1.71

Conergy, 2.10

Solar Power, 1.88

Mitsubishi, 1.50

SHARP, 2.60

Photowatt, 3.41

Solar-Fabrik, 2.38

BP Solar, 2.00

BP Solar, 1.88 Kyocera Solar, 1.92

Kyocera Solar, 3.12

Suntech, 1.62

Conergy, 1.92

SHARP, 1.60

1.40 €

1.60 €

1.80 €

2.00 €

2.20 €

2.40 €

2.60 €

2.80 €

3.00 €

3.20 €

3.40 €

3.60 €

3.80 €

Region 1 Region 2 Region 3 Region 4

CONTINUOUS ENHANCEMENT

Monthly updates

Underlying data for the Excel-Tool are updated on a monthly basis. You benefit from a comprehensive overview of the market, enabling you to react faster than competitors.

Sample chart

Sample chart

Sample chart

Product Data Sheet

EuPD Research 2011 35

Contents The product contains information regarding the following aspects:

System prices1.

Module brands2.

Inverter brands3.

System sizes4.

Zip-code regions5.

System configuration6.

Benefits for your Company

Gain competitive advantages by optimizing the application ▪ of marketing instruments

Gain information for the support of your pricing strategy ▪Optimize your sales controlling ▪Monitor your market presence in the several zip-code ▪

regions in GermanyReceive a database for individual benchmark analyses ▪

Included in Delivery Module 1: MS Excel tool (including twelve monthly updates, in German or English language)

Module 2: Optional MS PowerPoint report presents the most important results of module 1 in an annotated presentation

Price Module 1 Module 2 plus For four quarterly updates

€ 4,950* € 3,480 + € 2,460*

$ 6,950* $ 4,890 + $ 3,450*

Author/Contact Till von Versen

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

36 EuPD Research 2011

UNDERSTANDING GRID PARITY

IS A PARADIGM SHIFT IN THE PV INDUSTRY ON THE HORIZON?

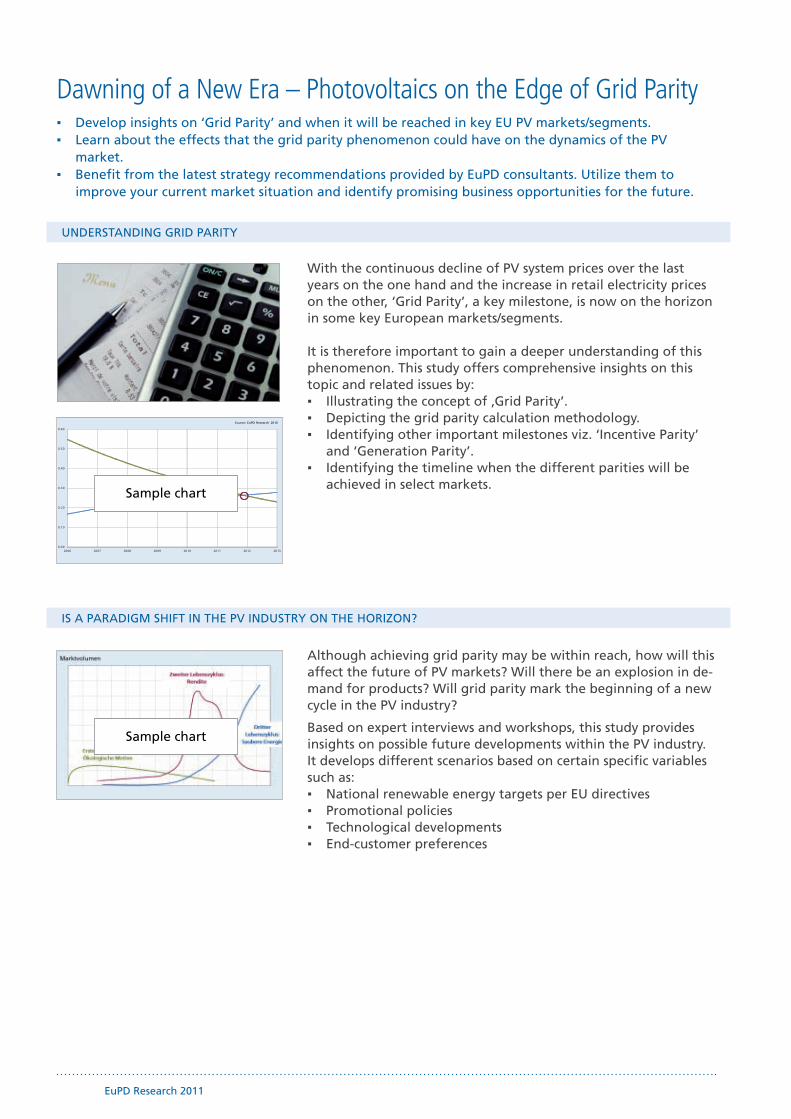

Dawning of a New Era – Photovoltaics on the Edge of Grid Parity Develop insights on ‘Grid Parity’ and when it will be reached in key EU PV markets/segments. ▪Learn about the effects that the grid parity phenomenon could have on the dynamics of the PV ▪

market.Benefit from the latest strategy recommendations provided by EuPD consultants. Utilize them to ▪

improve your current market situation and identify promising business opportunities for the future.

With the continuous decline of PV system prices over the last years on the one hand and the increase in retail electricity prices on the other, ‘Grid Parity’, a key milestone, is now on the horizon in some key European markets/segments. It is therefore important to gain a deeper understanding of this phenomenon. This study offers comprehensive insights on this topic and related issues by:

Illustrating the concept of ‚Grid Parity’. ▪Depicting the grid parity calculation methodology. ▪Identifying other important milestones viz. ‘Incentive Parity’ ▪

and ‘Generation Parity’.Identifying the timeline when the different parities will be ▪

achieved in select markets.

Although achieving grid parity may be within reach, how will this affect the future of PV markets? Will there be an explosion in de-mand for products? Will grid parity mark the beginning of a new cycle in the PV industry?

Based on expert interviews and workshops, this study provides insights on possible future developments within the PV industry. It develops different scenarios based on certain specific variables such as:

National renewable energy targets per EU directives ▪Promotional policies ▪Technological developments ▪End-customer preferences ▪

0.00

0.10

0.20

0.30

0.40

0.50

0.60

2006 2007 2008 2009 2010 2011 2012 2013

€/kW

p

Source: EuPD Research 2010

Sample chart

Sample chart

Product Data Sheet

EuPD Research 2011 37

Information Sources Quantitative and qualitative interviews with industry experts ▪Systematic desk research (external databases, business ▪

reports, etc.)EuPD DAT – internal database (quarterly EuPD studies, ▪

EuPD market reports, etc.)

Contents(Subject to Change)

Executive Summary

Part I. Growth of Renewable Energy | Top EU Electricity Markets

Part II. PV Market Analysis | Key European Markets

Part III. Major Milestones towards PV Competitiveness

A. Incentive Parity

B. Grid Parity

C. Generation Parity

Part IV. Looking Ahead | The Face of the Future PV Market

Benefits for your Company

Discover future trends and developments in the rapidly ▪ evolving PV industry

Receive information that can assist in developing strategies ▪ for the post grid parity era

Learn about future success factors and pathways to the ▪ ‘sweet spots’ of tomorrow’s PV market

Included in Delivery 1x report, high quality binding

Price € 1,450** $ 1,990**

Author/Contact Parag Bhamre

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

38 EuPD Research 2011

GERMANY – A COMPLEx MARKET

MARKET OVERVIEW

GERMANY – A COMPLEx MARKET

PV MarketMonitor© – GermanyGain detailed information on newly installed capacity and number of plants in all German regions. ▪Identify „blank spots“ per system size and analyze your company’s sales volume in relation to the ▪

total market.Receive quarterly data updates and develop regional sales strategies. ▪

Regional Differences

The German PV market is clearly different from all other country markets. It is not only the political framework conditions that constitute the difference, but also Germany’s regional particula-rities. The PV segment varies extremely in all regions with regard to system size, regional distribution networks, and market satu-ration. The PV MarketMonitor Germany therefore answers the following questions:

Which system sizes dominate which areas? ▪Which types of customers are being addressed? ▪What is the degree of saturation? ▪Where are “blank spots“? ▪

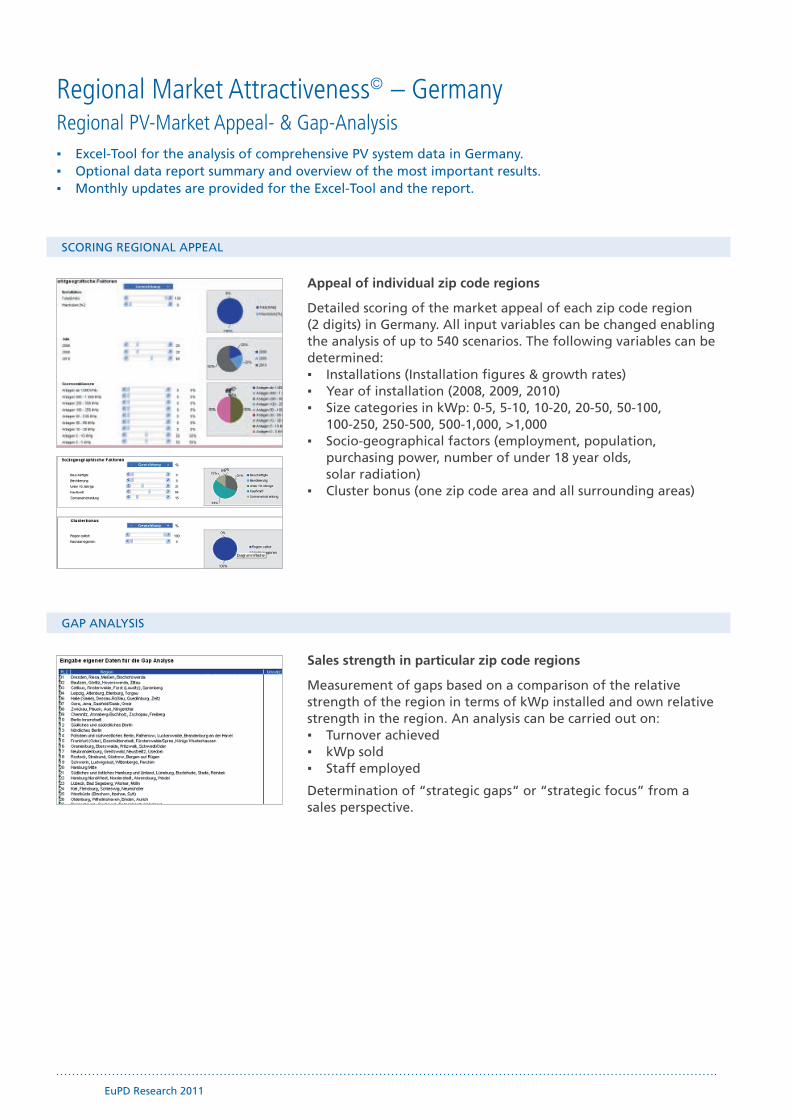

The PV MarketMonitor Germany provides different instruments

Optional: Chart report illustrates, in about 60 slides, the current situation and development of the PV market in the German regions. Numerous diagrams and maps depict all relevant infor-mation:

Market development and segmentation according to system ▪ size and plants installed since 2004.

Market segmentation according to customer groups. ▪A quarterly update gives you information on newly installed ▪

capacity throughout the current year.

Excel-Tool

The second instrument provided by the PV MarketMonitor is the Excel-Tool, which includes all relevant data for regional sales strategies. The data on the Excel-Tool is categorized according to main ZIP code areas as well as the ZIP code regions. It has also been edited with respect to system size and years. The Excel-Tool provides interactive Java maps, in which all data can be visua-lized. The Java tool allows you to:

Include your company‘s own data. ▪Identify your company’s market share. ▪Support the design of regional sales and marketing activities. ▪

Product Data Sheet

EuPD Research 2011 39

Information Sources Federal Network Agency´s Data Base ▪Internal database containing historic information on the ▪

German regional PV markets

Contents(Subject to change)

Market developement1.

Regional Market Segmentation according to system size2.

Regional Market segmentation according to customer 3. groups

Benefits for your Company

Examine the German PV market from a micro perspective ▪ and bring your operative marketing into line with the deci ding customer groups in the respective regions

Find out which regions in Germany have the most potential ▪ for your company

Analyze your company‘s sales and installation volume in ▪ relation to the total market

Identify white flag regions in Germany ▪Create regional strategies to penetrate the German market ▪

more preciselyPut your sales force as well as your advertising and marke- ▪

ting resources to even more cost-saving and efficient use

Included in Delivery Excel-Tool and quarterly updates

Optional: Chart report of approx. 60 slides

Price Standard version Extended version

€ 2,500* € 2,950*

$ 3,500* $ 4,150*

Author/Contact Till von Versen

Euro

pe

*(excluding sales tax/VAT) **(excluding sales tax/VAT and P&P)

40 EuPD Research 2011

SCORING REGIONAL APPEAL

GAP ANALYSIS

Regional Market Attractiveness© – GermanyRegional PV-Market Appeal- & Gap-Analysis

Excel-Tool for the analysis of comprehensive PV system data in Germany. ▪Optional data report summary and overview of the most important results. ▪Monthly updates are provided for the Excel-Tool and the report. ▪

Appeal of individual zip code regions

Detailed scoring of the market appeal of each zip code region (2 digits) in Germany. All input variables can be changed enabling the analysis of up to 540 scenarios. The following variables can be determined:

Installations (Installation figures & growth rates) ▪Year of installation (2008, 2009, 2010) ▪Size categories in kWp: 0-5, 5-10, 10-20, 20-50, 50-100, ▪

100-250, 250-500, 500-1,000, >1,000 Socio-geographical factors (employment, population, ▪

purchasing power, number of under 18 year olds, solar radiation)