PRODUCING EXPLORING GROWING

25

PRODUCING EXPLORING GROWING BUILDING A MID-TIER CHILEAN COPPER PRODUCER June 2021 TSXV: TVC

Transcript of PRODUCING EXPLORING GROWING

PRODUCINGEXPLORING

GROWINGBUILDING A MID-TIER CHILEAN COPPER PRODUCER

June 2021

TSXV: TVC

Certain statements in this presentation or the accompanying oral remarks, including in response to questions, contain forward-looking information (collectively referredto herein as the “Forward-Looking Statements”) within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”,“may”, “will”, “project”, “should”, “believe”, “plans”, “intends” and similar expressions are intended to identify Forward-Looking Statements. In particular, but without limitingthe forgoing, this presentation contains Forward-Looking Statements pertaining to: (i) expectations regarding cash flows; (ii) estimated corporate G&A, explorationdrilling and other costs; (iii) expectations regarding the economic, exploration, production and expansion potential of TVC; (iv) production estimates; (v) the expecteddrilling and exploration strategy, including expected results therefrom; (vi) the LOM plan; (vii) expectations regarding copper, including supply/demand fundamentals,price and cost of production; (viii) mineral reserve estimates; and (ix) statements concerning anticipated future events, results, circumstances, performance orexpectations, that reflect management’s current expectations and are based on information currently available to the management of TVC and its subsidiaries. Forward-Looking Statements are based on a number of expectations or assumptions which have been used to develop such statements and information but which may prove to beincorrect.

Although TVC believes that the Forward-Looking Statements are reasonable, they are not guarantees of future results, performance or achievements and should not beunduly relied upon. A number of factors or assumptions have been used to develop the Forward-Looking Statements, including: (i) the availability of capital on acceptableterms to finance exploration activities; (ii) all necessary permits and approvals for TVC will be obtained and maintained; (iii) the effects of regulation and tax laws ofgovernmental agencies will not materially change; (iv) a long-term flat copper price forecast of $2.75/lb and/or $4.50/lb; and (v) other assumptions identified in thepresentation. Actual results, performance or achievements could vary materially from those expressed or implied by the Forward-Looking Statements shouldassumptions underlying the Forward-Looking Statements prove incorrect or should one or more risks or other factors materialize, including: (i) general economic, marketand business conditions; (ii) commodity price fluctuations and uncertainties; (iii) risks associated with the copper industry; (iv) risks inherent in mining explorationactivities; (v) those risks described under the heading “Risk Management” in TVC’s Management’s Discussion and Analysis for the year ended December 31, 2020; and(vi) those risks described under the heading “Risk Factors” in TVC’s Annual Information Form datedMarch 3, 2021. The Forward-Looking Statements speak only as of thedate hereof and, unless otherwise specifically noted, TVC does not assume any obligation to publicly update any Forward-Looking Statements, whether as a result of newinformation, future events or otherwise, except as may be expressly required by applicable Canadian securities laws.

Cautionary Statement Regarding Forward-Looking Information

DisclaimerTSXV: TVC

2

Certain scientific or technical information in this presentation relating to MTV is based on information prepared by Dr. Antonio Luraschi, RM CMC, Manager ofMetallurgic Development and Senior Financial Analyst, Wood; Mr Alfonso Ovalle, RM CMC, Mining Engineer, Wood; Mr Michael G. Hester, FAusIMM, Vice Presidentand Principal Mining Engineer, Independent Mining Consultants, Inc.; Mr Enrique Quiroga, RM CMC, Mining Engineer, Q&Q Ltda; Mr Gabriel Vera, RM CMC,Metallurgical Process Consultant, GVMetallurgy; and Mr Sergio Alvarado, RM CMC, Consultant Geologist, General Manager and Partner, Geoinvestment SergioAlvarado Casas E.I.R.L., all of whom are independent “Qualified Persons” as such term is defined in National Instrument 43-101 – Standards of Disclosure for MineralProjects (“NI 43-101”), and included in the technical report filed in respect of MTV on December 14, 2018 and Revised and Amended on May 27, 2021 (the“ConsolidatedMTV Technical Report”).

Scientific and Technical Information

Disclaimer (cont’d)

Mineral resources described in this presentation are not mineral reserves and do not have demonstrated economic viabilityA “Qualified Person” means an individual who is an engineer or geoscientist with a university degree, or equivalent accreditation, in an area of geosciences orengineering, relating to mineral exploration or mining, with at least five years of experience in mineral exploration, mine development or operation or mineral projectassessment, or any combination of these, that is relevant to his or her area of professional degree or area of practice; has experience relevant to the subject matter of themineral project and the technical report; and is in good standing of a professional association that is relevant to his or her professional degree or area of practice.

The ConsolidatedMTV Technical Report has been filed under the Company's profile on SEDAR and can be found at www.sedar.com. Readers are encouraged to read thereport in its entirety.

Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Mineral ResourcesThis presentation may use the terms "measured", "indicated" and "inferred" mineral resources. United States investors are advised that while such terms are recognizedand required by Canadian regulations, the United States Securities and Exchange Commission does not recognize them. "Inferred mineral resources" have a greatamount of uncertainty as to their existence, and as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource willever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or other economic studies.United States investors are cautioned not to assume that all or any part of measured or indicated mineral resources will ever be converted into mineral reserves. UnitedStates investors are also cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable.

TSXV: TVC

3

Investment Highlights

PartnershipsInfrastructure 46,000 ha2 deposits

Three Valley Copper has a 90% interest in two deposits in Chile with a combined NPV of ~USD$300MM @ $4.50 copper NPV(8%) on a large underexplored land package with high probability exploration targets1. Don Gabriel (open pit) – in

production2. Papomono (underground) – in

construction3. Seven satellite deposits

Fully built infrastructure –permitted, operating and expandable1. Four-stage crushing and

agglomeration facility2. Heap leach optimized for

chloride media for salt leaching3. Solvent extraction-

electrowinning (SX-EW) plant

Strong partners – Strategic partnership with Anglo American and Kimura Capital as senior debt providers – Agreement with Anglo American for 100% of offtake

Geologic potential and strategic land package – immediate exploration potential around and between existing orebodies –46,000+ hectares of land holdings with less than 10% explored

*Fixed price option exercised by Anglo American in August 2020 for 40% of agreed upon forecasted production at $2.89/lb expiring July 2022

TSXV: TVC

4

Independent Chairman

TERRENCE A. LYONS ( ICD.D)

Mr. Lyons is a Civil Engineer (UBC) with an MBA fromWestern University. Terry is currently a Director ofCanaccord Genuity Group Inc, Martinrea International Inc.andMineral Mountain Resources Ltd. Mr. Lyons is a retiredManaging Partner of Brookfield Asset Management andalso President andManaging Partner of B.C. Pacific CapitalCorporation. Previously Mr Lyons was Chairman of PolarisMaterials Corporation, Northgate Minerals Corporation,Eacom Timber Corporation, Westmin Mining and Vice-Chairman of Battle Mountain Gold. He sits on the AdvisoryBoard of the Richard Ivey School of Business, is a pastGovernor of the Olympic Foundation of Canada, pastChairman of TheMining Association of B.C., past Governorand member of the Executive Committee of the B.C.Business Council, Past Director of the Institute ofCorporate Directors (BC) and in 2007 was awarded theINCO Medal by the Canadian Institute of Mining andMetallurgy for distinguished service to themining industry.

President, CEO, Director

MICHAEL STARESINIC ( ICD.D)

Mr. Staresinic has 20 years of experience in the financialservices and mining industry and was previously a directorof Jerritt Canyon Gold, Sprott Mining Inc. and the VicePresident of Finance at Sprott Inc., where he was also a keymember of the mergers and acquisitions team. Prior tojoining Sprott Inc., he spent nine years as Vice President ofFinance at a publicly-listed alternative asset managementfirm. Mr. Staresinic is a Chartered Professional Accountant,Chartered Accountant, CFA® charterholder and aChartered Alternative Investment Analyst. He holds anHonours Bachelor of Mathematics in CharteredAccountancy from the University of Waterloo and holdsthe ICD.D designation from the Institute of CorporateDirectors.

Independent Director

LENARD BOGGIO ( ICD.D)

Mr. Boggio is a retired partner of PwC, where he was theBritish Columbia leader of the firm’s mining industrypractice. He has significant expertise in financial reporting,auditing matters and transactional support, previouslyassisting, amongst others, clients in the mineral resourceand energy sectors, including exploration, developmentand production stage operations in the Americas, Africa,Europe and Asia. Mr. Boggio currently serves as a directorof Equinox Gold Corp., Pure Gold Mining Inc., Titan MiningCorporation and Augusta Gold Corp. He has a BA and anHBCom from the University of Windsor, is a Fellow of theCPA of BC and has previously served as the president ofthe Institute of Chartered Accountants of BC (now "CPABC”). He is also a past Chair of the Canadian Institute ofChartered Accountants.

Independent Director

JOAN E. DUNNE ( ICD.D)

Directors

Over the course of her career Ms. Dunne has served asVP Finance and CFO of Painted Pony Petroleum Ltd,True Energy Inc, True Energy Trust and Ionic Energy Inc.Ms. Dunne currently serves on the board of directors ofTundra Oil & Gas Limited and InPlay Oil Corp. Previousdirectorships include Painted Pony Energy Ltd. andCapital Markets Authority ImplementationOrganization. She was awarded with the designation ofFellow Chartered Accountant. Ms. Dunne was amember of the Canadian Performance Reporting Boardof CPA Canada from 2012 until 2020. She was also amember and Chair of CPA Canada's -7- Small CompanyAdvisory Group of CPACanada.

Independent DirectorBO LIU

Mr. Liu has held the position of Senior Manager ofResources Development with Baosteel, a mineral resourceinvestment, trade and logistic services company, sinceSeptember 2017. Previously, Mr. Liu held several positionswithin Baosteel Resources International Co. Ltd andBaosteel Resources Co. Ltd, mineral resource investment,trade and logistic services companies, including SeniorManager of Global Resources Development (November2010 to August 2017), Senior Manager of ResourcesPlanning and Developing Department (August 2008 toOctober 2010) and Senior Manager of Alloys Trading andDeveloping (August 2006 to July 2008). Mr. Liu joined theBaosteel group of companies in 2001. Mr. Liu currentlyserves on the board of directors of Noront Resources Ltd.(TSX-V:NOT). Mr. Liu graduated from Tongji University inShanghai, China with a Master Degree of BusinessManagement.

DirectorJOE PHILLIPS

Mr. Phillips is a senior mining executive with 48 years ofexperience in the construction, commissioning, andoperation of mining projects in 13 countries (7 in LatinAmerica) in 5 continents. Mr. Phillips is a registeredProfessional Mining Engineer, graduating from theColorado School of Mines ("CSM"), and with graduatestudies in Engineering Management at the University ofSouth Florida. Over his career he has directed theconstruction, commissioning, and operation of 11 plantsand mining operations, all of which met or exceeded theirdesigned capacities. Mr. Phillips was COO and Chairman ofthe Board of Lydian Resources, Armenia, ChiefDevelopment Officer of Coeur Mining, COO of SilverStandard Resources, and Senior VP Development for PanAmerican Silver Corp. He has held Directorships in theChambers of Mines in three countries including Chile,Mexico and Ghana, Africa. He was also a Director ofAbosso Goldfields Ltd., the second largest gold miningcompany in Ghana, Africa.

Independent DirectorDAVID SMITH (C.DIR)

David Smith is the Senior Vice-President, Finance andChief Financial Officer of Agnico Eagle Mines Limited andhas held this position since October 2012. Mr. Smithcurrently serves as a director of Canada Nickel CompanyInc. Previously Mr. Smith held the position of Senior Vice-President, Strategic Planning and Investor Relations ofAgnico. Prior to joining Agnico's investor relations team in2005, Mr. Smith was a mining analyst and also held avariety of mining engineering positions, both in Canada andabroad. Mr. Smith is a Chartered Director, and a formerdirector of eCobalt Solutions Inc. He has a B.Sc. and M.Sc.in Mining Engineering from Queen's University in Kingstonand the University of Arizona, respectively. Mr. Smith isalso a Professional Engineer.

TSXV: TVC

5

Executives

President & CEOMICHAEL STARESINIC

Mr. Staresinic has 20 years of experience in the financialservices and mining industry and was previously a directorof Jerritt Canyon Gold, Sprott Mining Inc. and the VicePresident of Finance at Sprott Inc., where he was also a keymember of the mergers and acquisitions team. Prior tojoining Sprott Inc., he spent nine years as Vice President ofFinance at a publicly-listed alternative asset managementfirm. Mr. Staresinic is a Chartered Professional Accountant,Chartered Accountant, CFA® charterholder and aChartered Alternative Investment Analyst. He holds anHonours Bachelor of Mathematics in CharteredAccountancy from the University of Waterloo and holdsthe ICD.D designation from the Institute of CorporateDirectors.

CFO & Corporate SecretaryIAN MACNEILY

Mr. MacNeily brings more than 20 years of executivefinancial management and leadership experience in themining sector. As a senior executive for several globalmining and development companies, he has considerableexperience in strategic planning, acquisitions, financialcontrols and reporting, capital restructuring and funding,metal trading, and implementing successful financeprograms that have resulted in improved financial positionand increased shareholder value. Prior mining companieswhere he served in a senior finance capacity includeAbacus Mining Corp., North American Palladium Ltd., SRACorporation, Desert Sun Mining, and Pangea GoldfieldsInc. where he managed the successful $210 millionacquisition by Barrick Gold Corporation. He spent sevenyears with Burns Fry (now BMO Nesbitt Burns) prior toentering the resource sector.

COOJOE PHILLIPS

Mr. Phillips is a senior mining executive with 48 years ofexperience in the construction, commissioning, andoperation of mining projects in 13 countries (7 in LatinAmerica) in 5 continents. Mr. Phillips is a registeredProfessional Mining Engineer, graduating from theColorado School of Mines ("CSM"), and with graduatestudies in Engineering Management at the University ofSouth Florida. Over his career he has directed theconstruction, commissioning, and operation of 11 plantsand mining operations, all of which met or exceeded theirdesigned capacities. Mr. Phillips was COO and Chairman ofthe Board of Lydian Resources, Armenia, ChiefDevelopment Officer of Coeur Mining, COO of SilverStandard Resources, and Senior VP Development for PanAmerican Silver Corp. He has held Directorships in theChambers of Mines in three countries including Chile,Mexico and Ghana, Africa. He was also a Director ofAbosso Goldfields Ltd., the second largest gold miningcompany in Ghana, Africa.

CEO at SiteLUIS VEGA

Luis Vega was named CEO of Minera Tres Valles("MTV") in 2016, previously working as CFO at MTV from2014. During his 25 years of professional experience, hehas held a variety of positions in the areas of finance, assetmanagement, petroleum products logistics anddistribution, mining operations and mining machinerymaintenance. He has actively participated in thetransactions associated with MTV, including the purchaseof the asset from VALE in 2013, the acquisition of thecontrolling interest of Three Valley Copper in 2017 andlater the financing of the expansion projects. Mr. Vega isan Industrial Engineer graduated from the PontificalCatholic University of Chile with an MBA from DukeUniversity in North Carolina, where he specialized inbusiness development in emerging markets. At an earlyage, he studied at the Military Academy in Chile where hegraduated as an army officer, obtaining the highest-ranking position in field artillery.

Exploration GeologistDR. JOHN MARTIMER

John Mortimer is an independent geologist workinginternationally in the metals industry. His technical skillsinclude field geology, 3D geological modelling, explorationgeoscience, exploration targeting and geoscience aspectsof investment evaluation. His experience includesgreenfield, brownfield and advanced project evaluation andmanagement. He has also worked on a variety of majorcapital project studies in multi-disciplinary teams on largecopper projects in South America and Australia.

Consulting Mining Engineer, Block-CavingJAREK JAKUBEC

Jarek is a cave mining specialist with over 35 years ofworldwide operating and consulting experience within themining industry. He has worked globally on over 150mining projects within 30 countries on 6 continents. Jarekis a SRK Corporate Consultant and Practice Leader of itsMining and Geology group in Vancouver. Jarek developedearly-career expertise in mining of diamond deposits withDe Beers, leading to engagements on diamond projects andproducing diamond mines in Canada, Siberia, Africa, SouthAmerica, Australia and China. Jarek remains active inresearch, development, benchmarking and operations-related themes in mass mining, specifically cave mining. Hehas authored or co-authored numerous publications,including the Large Open Pit Guidelines (2009, CSIRO) andGuidelines on Caving Mining Methods (2017, University ofQueensland). He is the founder of the Cave Mining Forum,promoter of responsible and sustainable mining practicesand received the CIM Mining Engineering OutstandingAchievement Award inMassMining (2019).

Consulting Mining Engineer, Block-CavingLUIS MERINO

Luis is considered a cave mining expert with over 50 yearsexperience in civil works. He has specialized in the area ofgeomechanics, providing expert advice to the industrythrough INGEROC SpA, a consulting company in the areasof rock mechanics and engineering. Mr. Merino has morethan 20 years of experience as a consulting engineer and isan industry expert in the areas of rock mechanics, rockengineering, geology and geotechnical engineeringproviding his services in countries such as Chile, Mexico,Argentina and Peru.

Consulting MetallurgistHANS HEIN

Principal and founder of Oryxeio in Chile, Hans’engineering company specializes in metallurgical processesfor the mining and metallurgical industry, particularly inhydrometallurgy. Hans and his team are recognized fortheir skills and experience in hydrometallurgical processesand particularly in the processes of leaching (LX), solventextraction (SX), ion exchange (IX), electrowinning (EW), andcrystallization (CX). Hans has performed projects for manyof the principal producers in Chile and internationally.

TSXV: TVC

6

Capital Structure

Share Price (June 18, 2021) 0.41$

Issued & Outstanding: 55.8 MStock Options: (avg. exercise C$0.31) 2.4 MWarrants: C$0.70 (Exp Oct 2022) 20.0 MWarrants: C$0.55 (Exp Oct 2022) 1.0 MFully Diluted: 79.2 M

Share StructureMarket cap * C$22M

Grossed up to 100% C$24M

USD equivalent US$20M

Debt US$70M

Enterprise Value US$90M

Enterprise Value

*Represents 90.3% ownership of project

TSXV: TVC

7

0

500000

1000000

1500000

2000000

2500000

3000000

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Jun-20

Jul-2

0

Aug-20

Sep-20

Oct-20

Nov-20

Dec-20

Jan-21

Feb-21

Mar-21

Apr-21

May-21

Jun-21

• $45M prepayment facility provided by Anglo American and Kimura Capital• 3 month LIBOR plus 8%• Quarterly instalments

beginning March 2022 ending December 2024

• No penalty for early repayment • Copper price participation

equivalent to ~$0.13/lb at today’s prices

• Up to $6M of additional principal available (at 11%)

Senior Secured

Debt Structure

• $5M converted from accounts payable to unsecured subordinated term debt• Ranks behind Senior Secured and

Unsecured Term debts• Interest rate still under

negotiation (~14%)• Equal quarterly instalments

expected to start September 2025 ending June 2027

Subordinated Term Debt

• $17M converted from accounts payable to unsecured 5 year term debt• 5% fixed interest rate• Equal quarterly instalments for

50% of balance beginning March 2022 ending March 2025; remaining 50% bullet June 2025

Unsecured Term Debt

TSXV: TVC

8

Summary

• Located near Salamanca, Chile, 300km north of Santiago

• Previously developed by Vale, spending ~ US$250 million on the property including associated infrastructure

• 46,348 hectares of mining property• Currently producing copper cathodes ~ 50% capacity;

ramping up during next 12-18 months• Produces high-grade copper cathodes – 99.999% Cu

content; highest quality cathodes on the market

• 4-stage crushing, agglomeration and leachingo Nameplate capacity: 7,000 tpd of oreo Salt leaching system completed in 2020

• Conventional leaching solvent extraction electrowinning (SX-EW) planto Nameplate cathodes capacity: 18,500 tpa

• Ore purchasing from small miners and government entities

• Third-party ore provides alternate source of high-grade ore, de-risks own mining operations and strengthens community relations

Overview

Mining and

Processing

TSXV: TVC

9

Facilities & Infrastructure Already in Place

~ US$250MM of infrastructure benefits

Salt leach system added to infrastructure in 2020

Salt leach reduces costs, increases recoveries and decreases leach time for sulphide ore from ~270 days to ~160 days

Built by Vale S.A. in 2008 – 2009

Cathode Produced on Site -Capacity of 18,500tpa

Crusher - Four-Stage Crushing 7,000tpd Capacity

Processing Plant - Room for Further Expansion

TSXV: TVC

10

In a Great NeighborhoodTSXV: TVC

11

TVC

Production: Don Gabriel Open Pit

• Don Gabriel open pit (shown) currently producing 60,000 to 80,000 tonnes per month ore feed

• One of two principal sources of ore

• The extent of Don Gabriel remains only partially tested by deeper drilling

N

200 m

Tonnes Grade Contained Cu Contained Cu

(kt) (CuT %) (kt) (000 lbs)

Proven 898 0.80% 7.1 15,653

Probable 4,270 0.82% 34.9 76,941

Total Proven & Probable 5,168 0.81% 42.1 92,815

Classification

Don Gabriel Manto

TSXV: TVC

12

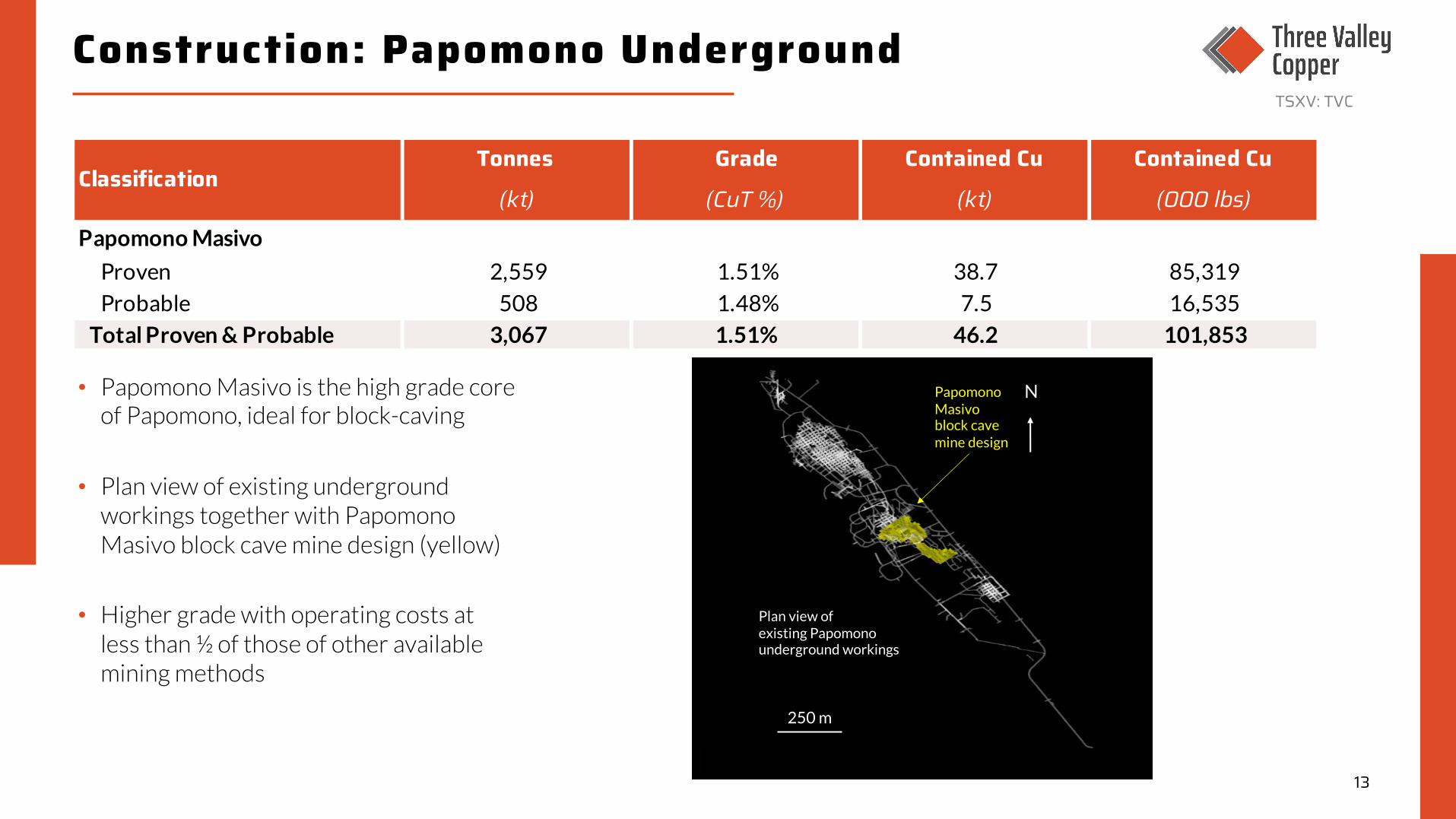

Construction: Papomono Underground

• Papomono Masivo is the high grade core of Papomono, ideal for block-caving

• Plan view of existing underground workings together with Papomono Masivo block cave mine design (yellow)

• Higher grade with operating costs at less than ½ of those of other available mining methods

Papomono Masivoblock cave mine design

N

Plan view ofexisting Papomono underground workings

250 m

Tonnes Grade Contained Cu Contained Cu

(kt) (CuT %) (kt) (000 lbs)

Proven 2,559 1.51% 38.7 85,319

Probable 508 1.48% 7.5 16,535

Total Proven & Probable 3,067 1.51% 46.2 101,853

Classification

Papomono Masivo

TSXV: TVC

13

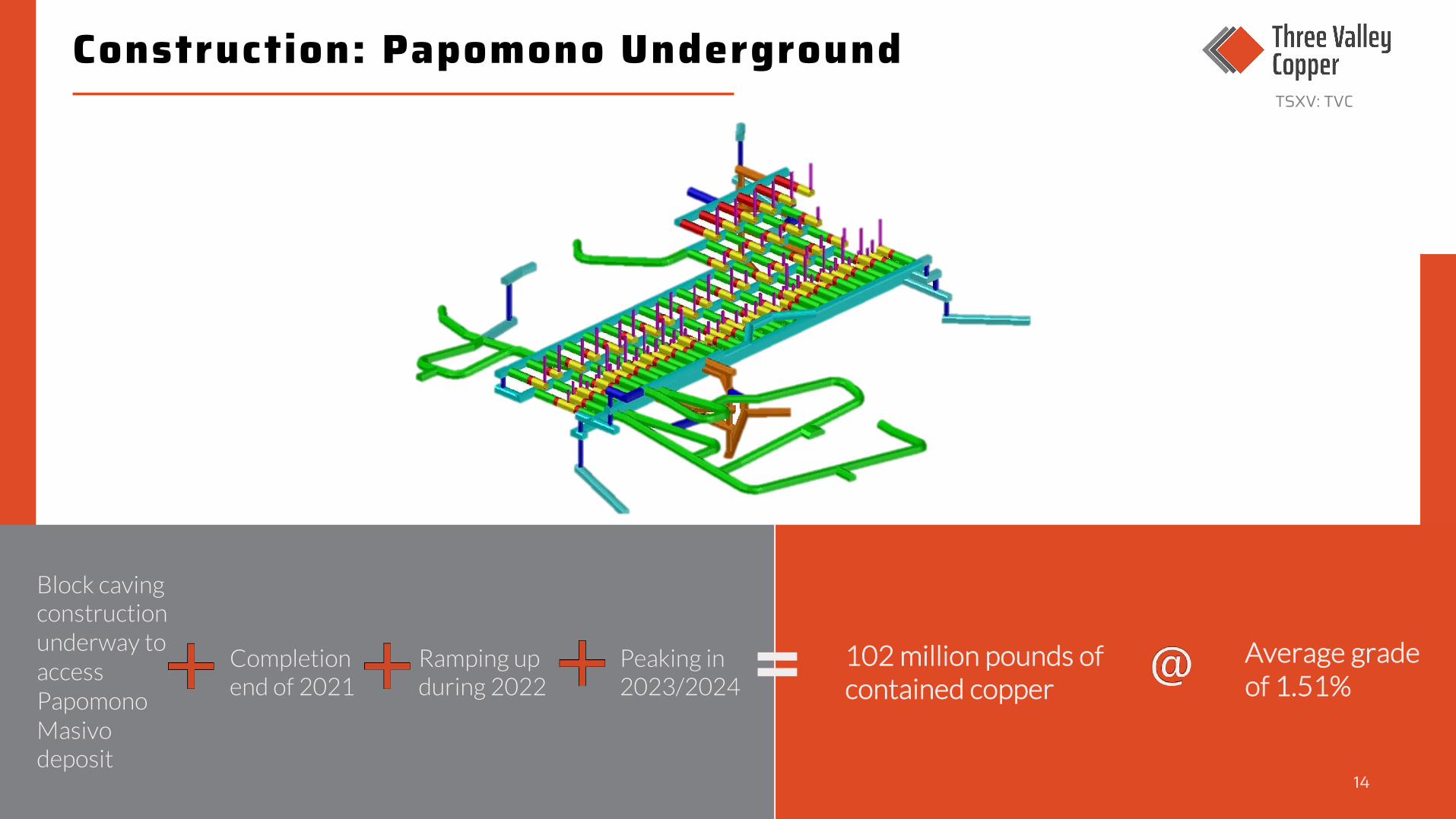

Construction: Papomono Underground

Block caving construction underway to access Papomono Masivo deposit

Completion end of 2021

Ramping up during 2022

Peaking in 2023/2024= 102 million pounds of

contained copperAverage grade of 1.51%

TSXV: TVC

14

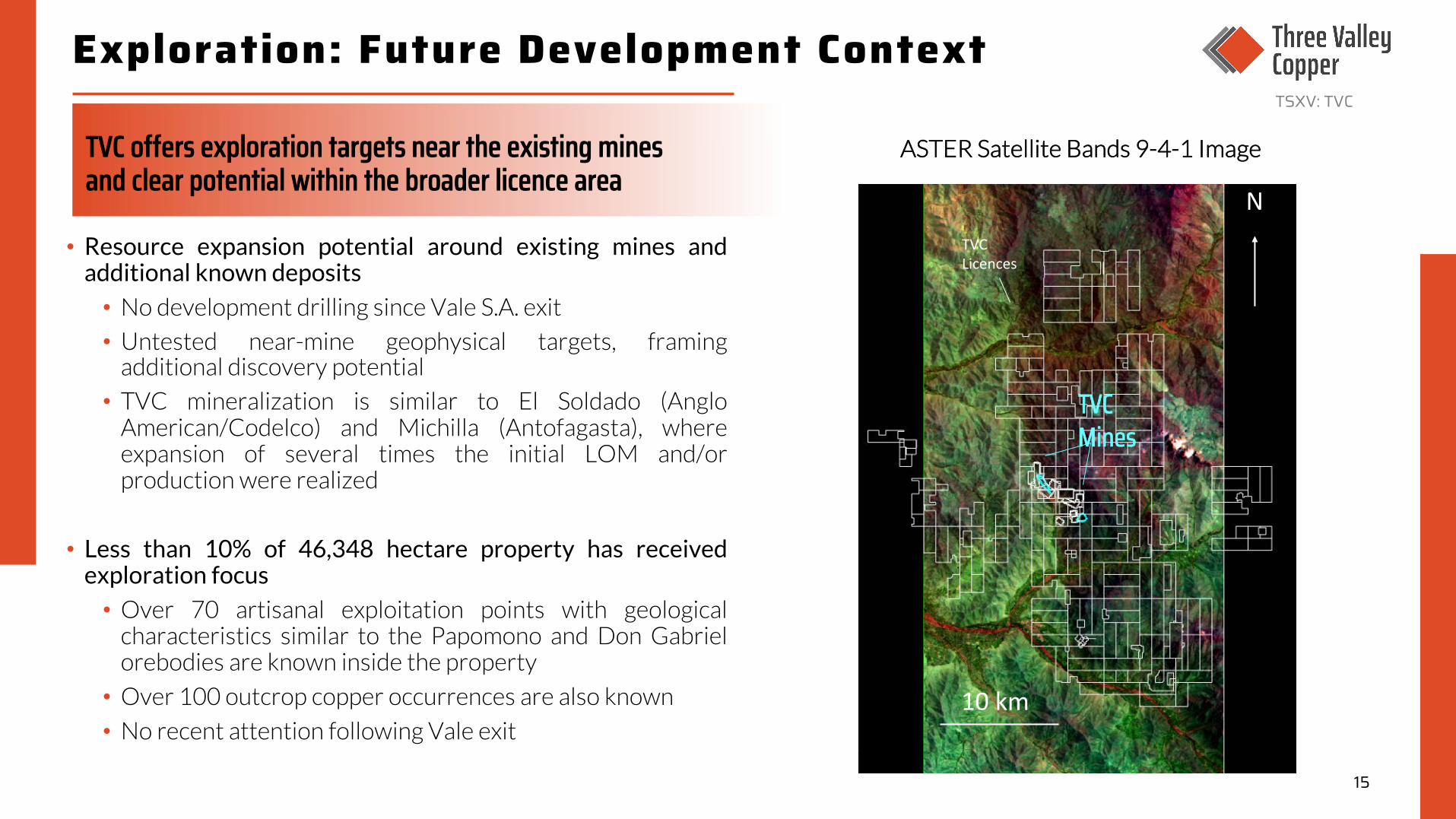

Exploration: Future Development Context

TVC offers exploration targets near the existing mines and clear potential within the broader licence area

• Resource expansion potential around existing mines andadditional known deposits

• No development drilling since Vale S.A. exit

• Untested near-mine geophysical targets, framingadditional discovery potential

• TVC mineralization is similar to El Soldado (AngloAmerican/Codelco) and Michilla (Antofagasta), whereexpansion of several times the initial LOM and/orproduction were realized

• Less than 10% of 46,348 hectare property has receivedexploration focus

• Over 70 artisanal exploitation points with geologicalcharacteristics similar to the Papomono and Don Gabrielorebodies are known inside the property

• Over 100 outcrop copper occurrences are also known

• No recent attention following Vale exit

N

Plan view ofexisting Papomono underground workings

TVC Mines

10 km

N

ASTER Satellite Bands 9-4-1 Image

TVCLicences

TSXV: TVC

15

Near-Term Exploration Focus Between Deposits

NPapomono

Underground Footprint

Don Gabriel Pit Outline

Ground MagneticsAnalytic Signal Image

high

low

1 km

• Existing copper mines are spatiallycoincident with ground magneticsanalytic signal highs, which possiblymap mineralisation-related magnetite /pyrrhotite

• Further mineralisation potential maytherefore be expected in the immediatevicinity

• 2021-2022 exploration drilling will befocused in this area

Copper Oxide in Drill Core Sample

1 cm

TSXV: TVC

16

Exploration: Near-Mine Areas with Potential

Ground MagneticsAnalytic Signal Image

Don Gabriel Pit Outline

high

low

500 m

Existing drill hole traces

12

6

4 5

3

Verde Deposit

Amarilla Deposit

500 m

10.50

Drill samples % copper

• Our near-mine area represents approximately 5 km2 of our 460 km2 area

• These plan views show good spatial correlation between known copper mineralisation and ground magnetics analytic signal highs (red). These magnetic anomalies may map magnetite and/or pyrrhotite, which may in turn be mineralisation-related

• There are areas with similar magnetic highs and no drill holes (1 – 4 green)

• Some areas with magnetic highs have few drill holes and untested areas (5 – 6 orange)

Don Gabriel Pit Outline

TSXV: TVC

17

Exploration: Don Gabriel Depth Potential

N

3D rendition ofDon Gabriel

open pit

Drill samples % copper

0 1.5 3

200 m

• Existing drill holes beneath Don Gabriel Pit have intercepts exceeding 2% copper

• Additional planned drilling will further explore the extent of Don Gabriel beneath the pit

TSXV: TVC

18

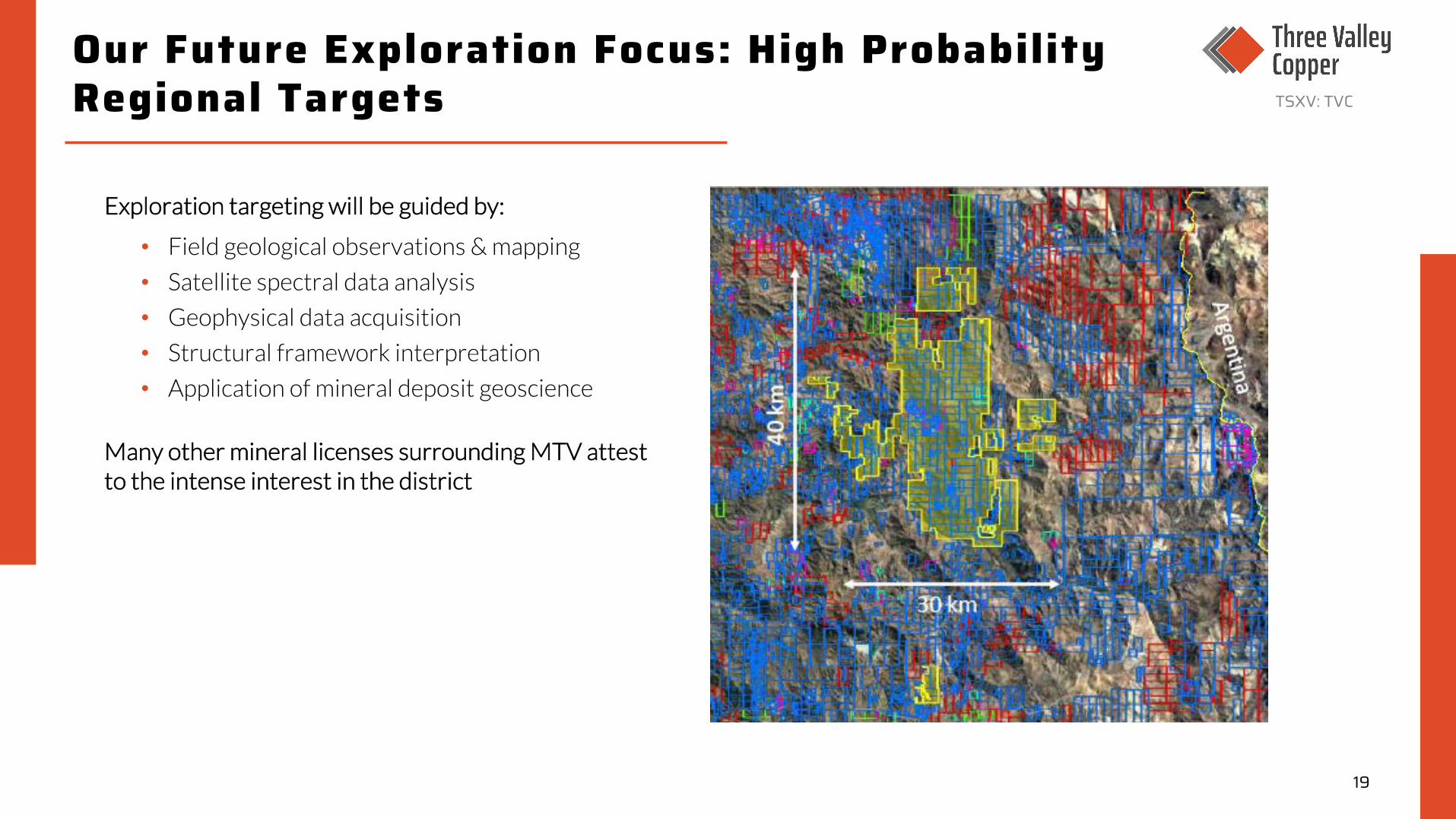

Our Future Exploration Focus: High Probability Regional Targets

Exploration targeting will be guided by:

• Field geological observations & mapping

• Satellite spectral data analysis

• Geophysical data acquisition

• Structural framework interpretation

• Application of mineral deposit geoscience

Many other mineral licenses surrounding MTV attest to the intense interest in the district

TSXV: TVC

19

Environmental, Social and Governance

• Reforestation initiatives in conjunction with local communities – >70,000 trees planted to date

• Strict adherence to water rights, reducing water footprint and supporting local farmers in periods of water stress

• Energy supplied by non-conventional renewable sources

• Stewards of 3 types of forests, 94 species of flora and 60 species of fauna

• Public company practices; TSXV listed

• Code of ethics

• No political contributions / alliances

• Majority independent board

• Whistleblower Policy

• 80% of MTV’s suppliers are local businesses

• 75% of MTV’s combined workforce (employees and contractors) live within 30 km of the mine site

• Unionized employees

• MTV Foundation finances and supports social projects related to education, social infrastructure, rural health posts and more

Environmental Governance Social

TSXV: TVC

20

Investment Thesis Recap – Why TVC?

Supply/ demand disruptions in copper exhibit

attractive long-term market

fundamentals

High torque to improving copper

prices

Fully built infrastructure –

permitted, operating and

expandable

Strong partners –Strategic

partnership with Anglo American

and Kimura Capital as senior debt

providers

Agreement with Anglo American for

100% of offtake

Geologic potential and strategic land

package –immediate

exploration targets around and

between existing orebodies

46,000+ hectares of land holdings with

less than 10% explored

Project NPV of ~US$300M

($4.50/lb copper) versus market cap

of ~US$25M1

1 Assumes 100% ownership of project

TSXV: TVC

21

Contact

18 King Street East, Suite 902Toronto, ON, M5C 1C4www.threevalleycopper.com

Michael StaresinicPresident & CEOBusiness: [email protected]

22

Appendix

23

Macro: Copper Fundamentals –Why We Like Copper

Structural Supply Deficit Expected• Development projects require higher prices – years of low

copper prices and under-investment in new supply means few new projects in the pipeline

• 2017 saw first decline in copper output in 15 years1

• Declining ore grades at current operations, falling 30% since 20001

• Insufficient high quality discoveries – approvals for new projects have hit a plateau despite a production deficit forecast over the long term2

Strong long-term demand growth expected• Chinese demand strong and expanding

• Electrification of transportation and infrastructure; up to 3.5x the copper for electric cars compared to conventional cars and between 11x – 16x for buses

• Paris agreement encouraging countries to seek lower emissions through developing technologies

• Government stimulus spending directed at infrastructure

• Renewable energy and decarbonization adoption

TSXV: TVC

241 Source: Pala Investments 2 Source: Wood Mackenzie

Macro: Copper Fundamentals –Why We Like Chile

• Chile is home to the largest concentration of world-class copper deposits

• #1 global copper producer – 28%1

• #1 global copper reserves – 23%1

• Significant pipeline of attractive mining investment opportunities

• Highly skilled and capable work force

• Well-functioning market economy, rule of law and sophisticated financial markets

28%

12%

8%

7%

7% 5%4%

4%

4%

4%

2%

!"#$%&'%"($%&)"**+,&-,"./0+,1&2 Chile

Peru

China

US

Congo

Australia

Zambia

Mexico

Russia

Kazakhstan

Indonesia

23%

10%

10%

7%6%

6%

3%

3%

2%

2%

2%

!"#$%&'%"($%&)"**+,&3+1+,4+1&2 Chile

Australia

Peru

Russia

Mexico

US

Indonesia

China

Kazakhstan

Congo

Zambia

TSXV: TVC

25

*Source: USGS