PROCEEDINGS OF THE AUTHORITY FOR …ctax.kar.nic.in/press/YAKULT - final.pdfYakult is a delicious...

18

GOVERNMENT OF KARNATAKA (Department of Commercial Taxes) PROCEEDINGS OF THE AUTHORITY FOR CLARIFIATION AND ADVANCE RULINGS UNDER SECTION 60 OF THE KARNATAKA VALUE ADDED TAX ACT,2003 r/w RULE 165 OF THE KARNATAAKA VALUE ADDED TAX RULES, 2005 Present : 1) R. Jagadish Prasad, Chairman 2) Sayeed Ahmed Khan, Member 3) B.V.Ravi, Member Name & Address of the Applicant : M/s Yakult Damone India Private Ltd., 102, Gangadhar Chetty Road, Bengaluru-560042. TIN : 29830575687 Jurisdictional Assessing Authority : ACCT, LVO-45 Applicant represented by : Shri. G. Shivadass, Advocate. ORDER NO. AR.CLR.CR.23/2011-12 DATED 15.02.2016 * * * * * * M/s Yakult Damone India Private Ltd., 102, Gangadhar Chetty Road, Bengaluru- 560042(herein afterwards referred to as ‘Applicant’) had sought clarification on the rate of tax under the provisions of the Karnataka Value Added Tax Act, 2003 applicable to ‘Yakult’. The Authority for Clarification and Advance Ruling (herein afterwards referred to as ‘ACAR’) vide order No. AR.CLR.23/2011-12 Dated 21-04-2012 had clarified the rate of tax on this commodity. The applicant had preferred appeal before the Hon’ble High Court of Karnataka against this order on the ground that the order passed by ACAR consisting of two members, namely Chairman and another member, is not sustainable and is not in conformity with the statutory provision of sub-section(1) of Section 60 of the Karnataka Value Added Tax Act, 2003.

Transcript of PROCEEDINGS OF THE AUTHORITY FOR …ctax.kar.nic.in/press/YAKULT - final.pdfYakult is a delicious...

GOVERNMENT OF KARNATAKA

(Department of Commercial Taxes)

PROCEEDINGS OF THE AUTHORITY FOR CLARIFIATION AND ADVANCE

RULINGS UNDER SECTION 60 OF THE KARNATAKA VALUE ADDED TAX

ACT,2003 r/w RULE 165 OF THE KARNATAAKA VALUE ADDED TAX RULES, 2005

Present : 1) R. Jagadish Prasad, Chairman

2) Sayeed Ahmed Khan, Member

3) B.V.Ravi, Member

Name & Address of the Applicant : M/s Yakult Damone India Private Ltd.,

102, Gangadhar Chetty Road,

Bengaluru-560042.

TIN : 29830575687

Jurisdictional Assessing Authority : ACCT, LVO-45

Applicant represented by : Shri. G. Shivadass, Advocate.

ORDER NO. AR.CLR.CR.23/2011-12 DATED 15.02.2016

* * * * * *

M/s Yakult Damone India Private Ltd., 102, Gangadhar Chetty Road, Bengaluru-

560042(herein afterwards referred to as ‘Applicant’) had sought clarification on the rate of tax

under the provisions of the Karnataka Value Added Tax Act, 2003 applicable to ‘Yakult’. The

Authority for Clarification and Advance Ruling (herein afterwards referred to as ‘ACAR’) vide

order No. AR.CLR.23/2011-12 Dated 21-04-2012 had clarified the rate of tax on this

commodity. The applicant had preferred appeal before the Hon’ble High Court of Karnataka

against this order on the ground that the order passed by ACAR consisting of two members,

namely Chairman and another member, is not sustainable and is not in conformity with the

statutory provision of sub-section(1) of Section 60 of the Karnataka Value Added Tax Act, 2003.

2 [AR.CLR.CR.23 /2011-12]

The Hon’ble High Court of Karnataka Vide order No. STA 119/2012 Dated 30th

September 2015

allowed the appeal and has quashed the order of the ACAR dated 21.04.2012 and remanded the

matter to be decided afresh by the ACAR properly constituted under Section 60 of the KVAT

Act, 2003 consisting of at least three Additional Commissioners. It is also directed that the

properly constituted Authority shall hear and decide the matter as expeditiously as possible, but

not later than four months from the filing of certified copy of this order before the respondent.

The Hon’ble High Court has also clarified that, the Court has not looked into the merits of the

claims of the applicant and the Authority constituted for deciding the matter shall look into the

merits of the claims of the applicant.

2. The Commissioner of Commercial Taxes has constituted the Authority for Clarification and

Advance Ruling vide Order NO.PRO/AR.CLR/MISC-4/15-16Dated 31.10.2015 which consists of

three Additional Commissioners which is the minimum prescribed by the statute. As per the

direction of the Hon’ble High Court of Karnataka, the applicant has filed a letter dated 30th

November 2015 enclosing a copy of the order of the Hon’ble High Court of Karnataka. This letter

is received on 2.12.2015. The applicant in this letter had requested to take up the matter and to

grant hearing in the matter before passing any order. Further submissions were filed on 22.1.2016.

3. As per the request of the applicant, in the interest of natural justice, notice for hearing was

issued to the applicant and the matter was posted for hearing on 28.12.2015. In response to this

notice, Shri Shivadass, Learned Advocate duly authorized by the applicant appeared before

ACAR and he was heard. At the time of hearing he reiterated the contentions raised in the

application filed for seeking clarification and also filed Annexure-4 to the letter dated 30.11.2015

and also copies of the judgements relied on. He argued the matter and pleaded that ‘Yakult’ is a

probiotic fermented milk drink which is like ‘Lassi’ and falls under entry 19 of the First Schedule

to KVAT Act, 2003 and is to be classified as ‘Curd and Butter Milk’.

4. Application filed by the applicant seeking clarification with regard to rate of tax on ‘Yakult’

under the provisions of the KVAT Act, 2003 is examined by the ACAR with reference to the

submissions made in the application, annexures to the application, arguments made by the learned

Advocate and law. The applicant pleads that, their product ‘Yakult’ is like ‘Lassi’ and akin to

3 [AR.CLR.CR.23 /2011-12]

‘Curd and Butter Milk’ as both are fermented milk product and involves similar processing steps.

He has submitted that being basic nature and substance of the product in the instant case is akin to

curd/buttermilk, the product ‘Yakult’ is to be classified under entry No.19 of the First Schedule to

KVAT Act, 2003. He submits that Curd, buttermilk and Lassi are fermented milk product/drinks

made by the process of fermentation using lactic acid and bacteria and curd is the most

concentrated form and the buttermilk is the most diluted form and Lassi falls in between curd and

buttermilk. He further submits that the Curd or Dahi is known to be in various forms as Milk

Dahi, Skim Milk Dahi, Sweet Dahi or Flavored types, Salt or Sour Dahi, Probiotic Dahi,

Symbiotic Dahi, Fruit Dahi and Dahi is also known as ‘Yogurt’ in some parts of which may be in

different flavours and similarly buttermilk and lassi also come in different flavours like mango,

straw berry, rosewater, plain, masala and says that lassi and buttermilk are variations of curd. He

has relied on the definition ‘Curd’ as per the Food Safety and Standards Act, 2006 & Food Safety

and Standards (Food products Standards and Food Additives) Regulations, 2011 and states that in

the States like AP, UP, Haryana, Delhi etc., the VAT Acts have put the products Curd, Buttermilk

and Lassi in the same heading/category and in the same entry as they belong to the same species

and the family. In support of his submissions the applicant has relied on the following decisions.

i. Mauri Yeast India Pvt Ltd. Vs. State of UP 2008(225)ELT321(SC)

ii. Commissioner of Central Excise vs. Wockardt Life Sciences Ltd. 2012(277)ELT299(SC)

iii. Indian Aluminium Cable Ltd. Vs. UOI-(1985)3SCC284

iv. Commissioner of Sales Tax, MP vs. Jaswant Singh Charan Singh(1967)2SCR720

v. Ramavatar Budhaiprasad Vs. Assistant Sales Tax Officer, Akola -1962(1)SCR 279

vi. K.V. Varkev Vs. Agricultural Income Tax and Rural Sales Tax Officer, Peermade-

(1954)5STC 348

vii. Aluva Sugar Agency Vs. State of Kerala-(2011) 9 SCC 658

viii. C.C.E. vs. Pioneer Scientific Glass Works [2006(197)E.L.T.308]

ix. Naturalle Health Products(P)Ltd. Vs. Collector of Central Excise, Hyderabad

[(2004) 9 SCC 136]

x. Asian Paints India Ltd vs. CCE – [(1988)2SCC470]

xi. State of Maharashtra Vs. Bradma India Ltd (2005)140STC17 SC

xii. Alladi Venkateshwaralu and Others Vs. Government of Andhra Pradesh and Another

[1978]41STC394(SC)

4 [AR.CLR.CR.23 /2011-12]

xiii. Nandi Printers Private Limited Vs State of Karnataka [2001] 122 STC 164(Kar)

xiv. Aluva Sugar Agency Vs. State of Kerala [2011]45VST 1 (SC)

xv. Union of India & Others Vs. Garware Nylons Ltd.(1996)10(SCC)413

xvi. Allahabad Dugdh Utpadak Sahakari Vs. Commissioner of Trade Tax decided on

9.10.2006

xvii. R.F. Enterprises Vs. State of Kerala (2009)23VST 148(Ker)

5. The applicant at the time of hearing placed annexture-4 to letter dated 30.11.2015 by

enclosing note on Probiotics, Fermented Milk Drink, Lactic Acid Bacteria, LCS and

Manufacturing process, Extracts of literature called ‘Dahi and Related Products’ of Jashbhai

B.Prajapati and Sreeja V New Delhi Publishers, Extracts of Outlines of Dairy Technology,

Sukumar De, Oxford University Press, Extracts of Technology of India Milk Products, extracts

of Handbook on Process Technology Modernization for professionals, Entrepreneurs and

Scientists by R.P. Aneja, B. N. Mathur, R. C. Chandan, A. K. Banerjee, Dairy India Publication,

Certificate by Indian Dairy Association dated 23.01.2007, Certificate by Dairy Science College

and Certificate by Dairy Technology Society of India, Dairy Research Institute an pleaded that

‘Yakult’ is a Lassi falling under entry 19 of First Schedule to KVAT Act and hence exempted.

Further submissions also reiterates these contentions.

6. The main contention of the applicant that their product ‘Yakult’ is like ‘Lassi’ and akin to

curd and Butter milk’ as both are fermented milk product which involves similar processing steps

and that being basic nature and substance of the product in the instant case akin to

curd/buttermilk, the product ‘Yakult’ is to be classified under entry No.19 of the First Schedule to

KVAT Act, 2003 is required to be viewed in the background of classification of Commodities for

the purpose of taxation by the Legislature. Entry no. 19 of the First Schedule reads as follow:

19. Curd and Butter Milk

Claim of the applicant that ‘Yakult’ is ‘Lassi’ akin to Curd and Butter Milk and hence it shall be

classified under entry 19 cannot be accepted for the reason that, legislature has not included

‘Lassi’ in that entry and exempted only ‘Curd’ and ‘Butter Milk’. The applicant in its website

5 [AR.CLR.CR.23 /2011-12]

http://www.yakult.co.in/faqs.php has brought out the difference between Yakult and

Yoghurt in FAQ as follow:

What is the difference between Yakult and Yoghurt?

Yakult and yoghurt are both cultured dairy products made from milk fermented with

live bacteria. However Yakult contain 6.5 billion live bacteria that reach our

intestine alive. Also the strain of bacteria Lactobacillus casei strain Shirota is

unique and different from the strain of bacteria found in yoghurt and dahi. The

applicant admits the difference between ‘Yakult’ and ‘Dahi’ or ‘Curd’ and

pleads to equate both of them for the purpose of rate of tax.

7. If the intention of the legislature was to exempt ‘Lassi’, then it would have found mention

in the entry. As admitted by the applicant manufacturing process of ‘Curd’ and ‘Butter Milk’

being similar, the legislature specifically segregated ‘Curd’ and ‘Butter milk’ as two different

and independent commodities by using conjunction ‘and’ which shows that the legislature has

recognised these two products as separate commodities for the purpose of taxation and exempted

them and excluded all other items which are akin to ‘Curd’ and ‘Butter Milk’ such as ‘Lassi’

Fruit Dahi, Sweet Dahi, etc. The applicant’s contention that ‘Curd’ and ‘Butter Milk’ and

Yakult’ or ‘Lassi’ has the same process of manufacturing cannot be accepted for the reason that

‘Curd’ is manufactured through process of fermentation in a more solidified form which has

more fat contents and that can be further processed to get Butter Milk, Butter, Ghee, Lassi,

Yakult, and other products. What is common to manufacture ‘Curd’, ‘Butter Milk’ and ‘Yakult’

is fermentation of Milk. Just because there is a process of ‘fermentation’ to obtain these

products, that does not mean that all of them are one and the same. If all these commodities were

to be one and the same the legislature would not have made any distinction to separate them as

‘Curd’ and ‘Butter Milk’. The Hon’ble Supreme Court of India in the case of Hira Lal Rattan

Lal Vs. Sales Tax Officer, Section III Kanpur and Another Tilok Chand Prasan Kumar

and Another Vs. State of U.P. and Others [1973] 31 STC 178(SC) has held that the

Legislature was competent to separate processed or split food grains from unsplit or unprocessed

food grains and treat them as two separate and independent goods. Likewise the legislature has

6 [AR.CLR.CR.23 /2011-12]

differentiated ‘Curd, Butter Milk, Lassi, Yoghurt, Yakult as independent goods and has

considered only ‘Curd and Buttermilk’ for exemption.

8. The applicant in its website http://www.yakult.co.in/whyyakult.php has defined ‘Yakult’

as follow:

Yakult is a delicious probiotic drink that helps improve

digestion and helps build Immunity. Yakult contains 6.5 billion

beneficial bacteria (Lactobacillus casei strain Shirota) that

reach our intestines alive and restore the balance of the

beneficial or friendly bacteria in the gut. Daily consumption of

Yakult improves intestinal health and builds immunity. Over 30

million people in more than 30 countries including India trust

Yakult and drink it every day!

Ingredients of Yakult as explained in the webpage are as follow:

Skimmed Milk Powder, Sugar, Glucose, Natural and Natural Identical Flavour, Water and

6.5 billion Lactobacillus casei strain Shirota.

Further the ‘Yakult’ cannot be compared with ‘Lassi’ also. ‘Lassi’ is processed form of Butter

Milk wherein the fermented milk is further processed either by adding salt, sugar, or rosewater,

strawberry, lemon or fruit juices. While ‘Yakult’ is manufactured through a process of

fermentation as an health drink. The website gives the origin of ‘Yakult’ as follow:

In 1930 Dr. Minoru Shirota, a Japanese scientist, was the

first in the world to isolate and culture a probiotic strain which

reached the intestines alive in large numbers and imparted

health benefits to the host. He used this strain to make Yakult, a

fermented milk drink, so as to reach the benefits of the strain to

people at large. Yakult was first launched in Japan in 1935, and

today with over 80 years of history, Yakult is a global leader in

the probiotic drinks market with the wide range of probiotic

products using Lactobacillus casei strain Shirota (LcS)

and Bifidobacterium breve. The flagship product Yakult contains

7 [AR.CLR.CR.23 /2011-12]

over 6.5 billion beneficial bacteria (Lactobacillus casei strain

Shirota) which have proven health benefits. It helps improve

digestion and helps build Immunity. It has been scientifically

proven to be safe and effective.

9. Thus, ‘Yakult’ is sold more as a health product than as ‘Lassi’ which is prominently used as

food and drink in North India. Thus, there is a manufacturing process to obtain ‘Yakult’ and marketed

as health drink. The claim of the applicant to classify the product under ‘Curd and ‘Butter Milk’ is

based only on fermentation process involved. This argument of the applicant cannot be accepted for

the reason that process of manufacture is not the criteria to categorise the commodity. For example,

Skimmed Milk Powder, UHT Milk, Cottage Cheese, buttermilk, curds, Khova, etc., are products of

milk have their own distinct usages and are understood as different commodities by the general public

and the trade. Fresh Milk is the basic ingredient of all these products. We cannot equate all these

products as ‘Milk’ as such but can be called as ‘Milk Products’. Thus, Butter Milk, Curds, Lassi

and Yakult, UHT Milk, Khova or Skimmed Milk powder are milk products obtained through

different processes. While Skimmed Milk Powder or Powdered milk or dried milk is a

manufactured dairy product made by evaporating milk to dryness. Powdered milk and dairy

products include such items as dry whole milk, nonfat (skimmed) dry milk, dry buttermilk, and

dry dairy blends. Fresh Milk is heated to certain temperature and through a process of

evaporation powdered milk, skimmed milk powder is manufactured and through a process of

fermentation and further processes ‘curd’ and ‘butter milk’ ‘lassi’ and ‘Yakult’ and even dry

butter milk and other products are manufactured. But they cannot be equated on a same pane

based on the basic process involved. The Hon’ble Supreme Court of India in the case of Ujagar

Prints Vs. Union of India and Others [1989] 074 STC 0401 has held that the prevalent and

generally accepted test to ascertain that there is manufacture is whether the change or the series of

changes brought about by the processes take the commodity to the point where commercially, it

can no longer be regarded as the original commodity but is, instead, recognized as a distinct

and new article that has emerged as a result of the processes. [Emphasis supplied] The Hon’ble

Supreme Court of India in the case of Rajasthan Roller Flour Mills Association Vs. State of

Rajasthan [1993] 091 STC 0408(SC) has held that when wheat is consumed for producing flour

or Maida or Soji, the commodities obtained are different commodities from wheat. Wheat loses

its identity, it gets consumed and in its place new goods/commodities emerge. The new goods so

8 [AR.CLR.CR.23 /2011-12]

emerging have a higher utility than the commodity consumed. They are different goods

commercially speaking. The Hon’ble Supreme Court of India in the case of Empire Industries

Ltd vs. Union of India (1985 (3) SCC 314) has held that the moment there is transformation

into a new commodity commercially known as a distinct and separate commodity having its

own character, use and name, whether be it the result of one process or several processes

`manufacture' takes place and liability to duty is attracted. These facts clearly show that ‘Curd’

and ‘Butter Milk’ are entirely different from ‘Yakult’ or ‘Lassi’ for the reason that ‘Curd’ and

‘Butter Milk’ are processed using milk through fermentation process which does not contain

any additives or flavours. But to manufacture ‘Lassi’ or Yakult’ it is further processed by adding

sugar, glucose and flavours. In the Trade and commercial and common parlance all the

commodities are understood differently and used for different purposes also. ‘Curd’ is used with

rice which has high content of fat and no sugar is added when it is called as ‘curd’. While ‘Lassi’

and ‘Yakult’ cannot be conceived as curds as such since it has flavours and sweeteners added to

it. Nobody will add lassi or ‘Yakult’ to Rice in their meal. In the same manner Buttermilk is

consumed as ‘Butter Milk’ not as ‘Curd’ since it has less fat and diluted to reduce the fatty

effects. Thus, Curd, Buttermilk, Lassi and Yakult are independent marketable commodities.

People buy ‘Curd’ as ‘Curd’ not as ‘Butter Milk’ or ‘Lassi’ or ‘Yakult’. Likewise, ‘Yakult’ or

‘Lassi’ cannot be bought as ‘Butter Milk’ or ‘Curd’. Thus Common parlance and Commercial

Parlance plays an important role in classification of commodities for the purpose of taxation. The

Hon’ble Supreme Court of India in the case of State Of Uttar Pradesh vs. M/S. Kores (India)

Ltd on 18 October, (1976)1977 AIR 132, 1977 SCR (1) 837

A word which is not defined in an enactment has to be understood in its

popular and commercial sense with reference to the context in which it occurs.

It has to be understood according to the well-established canon of construction

in the sense in which persons dealing in and using the article understand

it.

Hon’ble High Court of Bombay in the case of Commissioner of Sales Tax, Maharashtra State,

Mumbai VS Cadila Healthcare Limited[Sales Tax Appeal No. 1 of 2010, VAT Appeal No.

16 of 2007 Date Of Decision : Fri Mar 04 2011] has held as follow:

9 [AR.CLR.CR.23 /2011-12]

It is never expected that the product should pass all the tests or

all the guiding principles should be made applicable to it, rather

the most important and paramount test of fixing the

classification and the entry of the commodity under the VAT is

whether the product in issue is a distinct marketable commodity

or not. A commodity should be distinguishable from its mother

product in its character, ingredients, nature, form, look, use,

pack, etc., and secondly, it is to be recognized as an independent

separate commodity in the market. The term marketable

connotes two aspects, i.e., firstly the product should be saleable

in the market and secondly it should establish its own identity as

a commodity in the eyes of the consumer. Thus though one or

two guiding principles may be applicable to a product but if the

product refuses to merge into its original product and establishes

its own identity in the market then it is treated as a distinct

marketable commodity.

10. In this case also the words defined in the enactment is ‘Curd’ and ‘Buttermilk’ which is to

be understood in the sense people understand it based on its usage not on the way these

commodities emerge. ‘Lassi’ and ‘Yakult’ cannot be understood as ‘Curd’ and ‘Butter milk’.

‘Yakult’ is distinguishable from Curds, Butter Milk in its character, ingredients, nature, form,

look, use, pack, etc., and secondly, it is recognized as an independent separate commodity in the

market. The product is sold in the market establishing its own identity as a commodity in the

eyes of the consumer as ‘Yakult’ not as ‘Curd’ or ‘Butter Milk’. Thus, just because it is obtained

through fermentation process that does not mean that ‘Yakult’ does has not have its own identity

in the market,, distinct marketable commodity distinct from ‘Curd’ and ‘Buttermilk’. If the

argument of the applicant is accepted then all the commodities obtained through process of

‘fermentation’ are to be invariably classified as one and the same as Curd and Butter milk. Then,

Lassi, Butter and Ghee obtained through further processing of ‘curd’ should also be brought

under this entry. This is not the way the classification of commodities for the purpose of taxation

will take place. Thus ‘Curd and Butter Milk’ are independent commodities by themselves

classified by the legislature for the purpose of exemption and has excluded ‘Lassi’ or ‘Yakult’

10 [AR.CLR.CR.23 /2011-12]

or all other forms for the purpose of levy. Even in common parlance ‘Curd’ and ‘Butter Milk’

and ‘Lassi’ are treated separately. Nobody calls ‘Curd’ as ‘Butter Milk’ and Butter Milk as Curd

or Curd and Buttermilk as Lassi. Once the Legislature has omitted certain commodities from

exemption, then those commodities are liable to tax. The argument of the applicant for

exemption could have been more relevant if the entry were to be ‘Curd and Butter Milk and the

like’. But, in this case as specific entries are carved out to exclude others, it is not correct to say

‘Yakult and Lassi’ can be called as ‘Curd’ and ‘Buttermilk’.

11. Thus, the intention of the legislature is to include only ‘curd’ and ‘butter milk’ as used in

South India more so in Karnataka wherein ‘Curd’ is understood as a commodity obtained

through traditional way of fermentation of milk which has high fat content and used with rice

during meal. Likewise ‘Buttermilk’ is understood as a commodity obtained by further processing

of ‘curd’ to remove fat or by adding more water to dilute the curd by stirring and churning

method. Buttermilk is used for a meal or a drink who want that to be used with less fat or

cholesterol. In changing society the dietary habits of human beings demands new products to

sort out health related problems. The applicant in its website in http://www.yakult.co.in/faqs.php

in the sub-menu Science behind Yakult has mentioned healing effects of Yakult with regard to

Diarrohea, Constipation, irritable Bowler Syndrome, Inflammatory Bowel Syndrome, Short

Bowel Syndrome, Helicobacter pylori, Liver Disorders, Gastrointestinal disorders, immune

modulation, cancer, viability, metabolic disorders. In one of the component with regard

inflammatory bowel disorder it is authenticated as follow:

A component of polysaccharide peptidoglycan complex

on Lactobacillus induced an improvement of murine

model of inflammatory bowel disease and colitis-

associated cancer.

12. All these factors points to the fact that the applicant manufactures these products and sell

to the public more as health related food products than as part of meal as understood by general

public with regard to ‘curd’ and ‘buttermilk’. The legislature has consciously exempted ‘curd’

and ‘buttermilk’ which are manufactured by milk dairies through a process which are used as

11 [AR.CLR.CR.23 /2011-12]

part of food. Thus, Food and drink which are unscheduled goods are taxable at 14.5% under

section 4(1)(b)(iii) of KVAT Act,2003 and ‘Curd’ and ‘Buttermilk’ are brought under First

Schedule under entry 19 to exempt them. ‘Lassi’ which is used as food and drink in North India

with salt or sugar and other ingredients and ‘Yakult’ which is exclusively manufactured by the

applicant which is different from ‘Dahi’ or ‘curd’ are excluded from the exempted entry. ‘Curd’

and ‘Butter Milk’ with a traditional meaning of food and drink were used as a part of balanced

diet. Legislature has excluded only ‘Curd’ or ‘Butter milk’ as understood in South India, more

particular in the State of Karnataka and has not included ‘Yakult and Lassi’. As explained

above, with the march of time and modernization and globalization, health aspects of foreign

countries are also adopted to the needs of the society. Revolutionary changes brought about in

socio-economic activities of human activity has brought ‘Yakult’ which is a health drink

different from ‘curd’ or ‘Dahi’ has drawn the attention of the common man more so in the higher

strata of the society. Thus, by taking the traditional meaning of ‘curd’ and ‘butter milk’ and

‘Dahi’ the applicant cannot equate his product ‘Yakult’ on par with them since in commercial,

trade and common parlance it has its own usage and meaning distinct and independent of them.

This is the result of changes with times which has brought new commodity to the fore. Thus, the

law recognizes the dynamics of the society to take into its ambit new inventions which are

commercially exploited for the well-being of the society. It is unreasonable to attribute the

meaning of ‘Curd’ and ‘Buttermilk’ to ‘Yakult’. As authenticated by the applicant in it website

Yakult contains 6.5 billion beneficial bacteria (Lactobacillus casei strain Shirota) that reach our

intestines alive and restore the balance of the beneficial or friendly bacteria in the gut. Daily

consumption of Yakult improves intestinal health and builds immunity. Over 30 million people in

more than 30 countries including India trust Yakult and drink it every day! Thus, in commercial

parlance or common parlance it is distinct commodity different from ‘Curd’ and ‘Buttermilk’.

Hence the claim of the applicant to classify ‘Yakult’ under entry 19 of the First Schedule to

KVAT Act, 2003 cannot be accepted.

13. The Division bench of Hon’ble High Court of Andhra Pradesh in the case of Yakult

Danone India Private Limited, Hyderabad Vs State of Andhra Pradesh [T.A.No.358 of 2012

Judgment Dated 14th

March 2013] has held that

12 [AR.CLR.CR.23 /2011-12]

Yakult probiotic Drink’ the term ‘probiotic’ means for life and it is

defined by Food & Agricultural Organization/World Health

Organization in (2002), Probiotic which life microorganisms, when

administered in adequate amounts confer a health benefit on the

host. The probiotic boosts the immunity and protects health,

increases number of beneficial bacteria in the gut, increases the

production of antibodies, prevents deficiency which lower the

immunity etc. Yogurt is different from milk, though mentioned as

fermented milk, and to make yogurt, boiled milk is allowed to

become lukewarm, in which certain yogurt is added, and after a few

hours this milk will ferment. This completely changes the milk and

yogurt contains iodine, calcium phosphorus, vitamin B12,

tryptophan, zinc and potassium. It contains beneficial bacterial

while milk doesn’t. This beneficial bacteria is known to cure all the

digestive system related problems like bloating, acidity, ulcers,

colon problems etc. Therefore, yakult probiotic drink made out of

fermented milk, water, sugar, glucose, nutritional fats, skimmed

milk powder, etc by manufacturing process in drink form cannot be

treated as lassi, fresh milk and pasteurized milk and skimmed milk

powder and UHT milk. Only curd, lassi, buttermilk and separated

milk in liquid form alone is exempt from tax.

This judgment of the Hon’ble High Court of Andhra Pradesh sums up the issue with regard to

classification of ‘Yakult’. The appellant has relied on certain certificates issued by Dean, Daily

Science College, Hebbal, Bangalore, Chairman, Indian Dairy Association, Delhi, President,

Dairy Technology Society of India, National Dairy Research Institute Karnal to prove that

‘Yakult’ is a fermented drink and it is similar to Lassi in taste. These certificates will not support

reasons for exclusion as the legislature has excluded ‘Yakult’ from exemption and has included

‘Curd and Butter Milk’ only. Hon’ble High Court of Andhra Pradesh in the above case has held

that

13 [AR.CLR.CR.23 /2011-12]

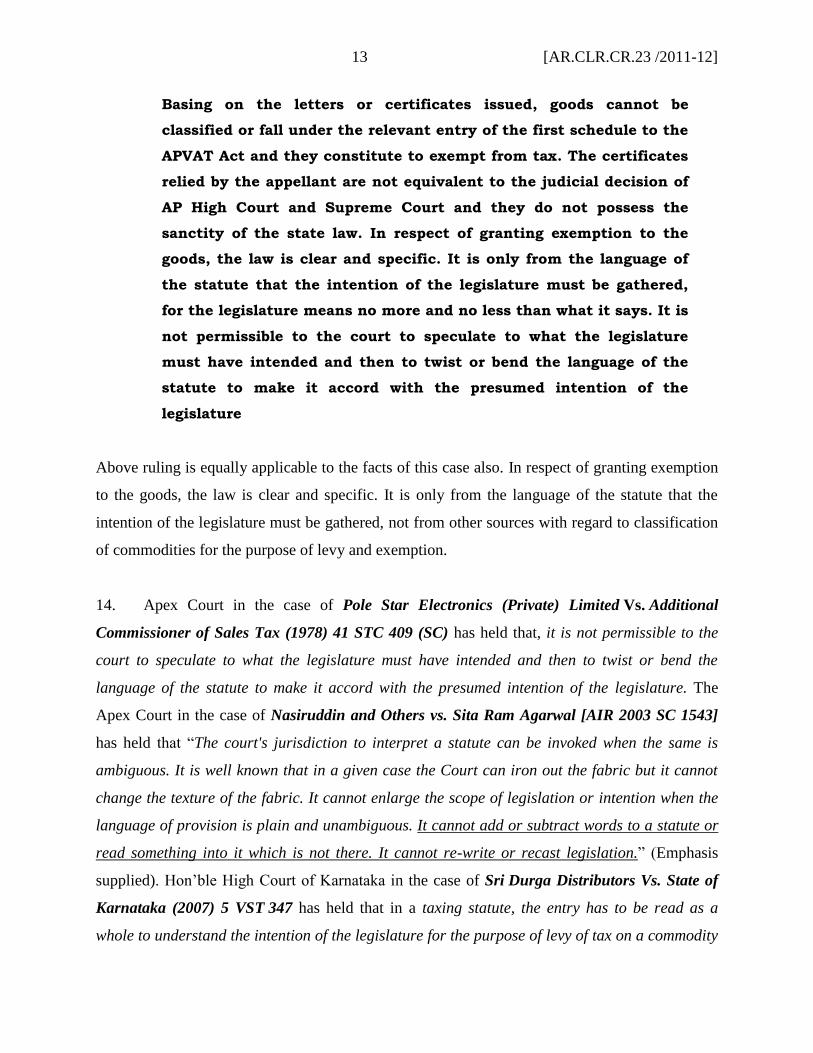

Basing on the letters or certificates issued, goods cannot be

classified or fall under the relevant entry of the first schedule to the

APVAT Act and they constitute to exempt from tax. The certificates

relied by the appellant are not equivalent to the judicial decision of

AP High Court and Supreme Court and they do not possess the

sanctity of the state law. In respect of granting exemption to the

goods, the law is clear and specific. It is only from the language of

the statute that the intention of the legislature must be gathered,

for the legislature means no more and no less than what it says. It is

not permissible to the court to speculate to what the legislature

must have intended and then to twist or bend the language of the

statute to make it accord with the presumed intention of the

legislature

Above ruling is equally applicable to the facts of this case also. In respect of granting exemption

to the goods, the law is clear and specific. It is only from the language of the statute that the

intention of the legislature must be gathered, not from other sources with regard to classification

of commodities for the purpose of levy and exemption.

14. Apex Court in the case of Pole Star Electronics (Private) Limited Vs. Additional

Commissioner of Sales Tax (1978) 41 STC 409 (SC) has held that, it is not permissible to the

court to speculate to what the legislature must have intended and then to twist or bend the

language of the statute to make it accord with the presumed intention of the legislature. The

Apex Court in the case of Nasiruddin and Others vs. Sita Ram Agarwal [AIR 2003 SC 1543]

has held that “The court's jurisdiction to interpret a statute can be invoked when the same is

ambiguous. It is well known that in a given case the Court can iron out the fabric but it cannot

change the texture of the fabric. It cannot enlarge the scope of legislation or intention when the

language of provision is plain and unambiguous. It cannot add or subtract words to a statute or

read something into it which is not there. It cannot re-write or recast legislation.” (Emphasis

supplied). Hon’ble High Court of Karnataka in the case of Sri Durga Distributors Vs. State of

Karnataka (2007) 5 VST 347 has held that in a taxing statute, the entry has to be read as a

whole to understand the intention of the legislature for the purpose of levy of tax on a commodity

14 [AR.CLR.CR.23 /2011-12]

and any benefit available if so received has to be provided to the assessee. However, if non-

inclusion of certain commodity is indicated, then the Court would not be justified in including

those commodities for the purpose of taxing under a particular entry. Any inclusion by the

Court for the purpose of taxation would be usurpation of power which is not available to the

Court in the matter of taxing statute.

15. Reliance placed by the applicant on the judgement in the case of Commissioner of

Central Excise vs. Wockardt Life Sciences Ltd.2012 (277) E.L.T.299 (SC) is also not applicable

to the facts of this case. In Wockardt case the Apex Court was determining whether the

classification of ‘Iodine Cleansing Solution’ was to be classified under ‘Medicament’ or ‘

detergent/ cleansing preparation’ under Central Excise Tariff and held that residuary entry can be

taken refuge of only in the absence of specific entry. In this case also ‘Yakult’ being not defined

under any schedule more specifically in I Schedule for the purpose of exemption, it is to be

treated as goods not falling under any schedules liable to tax at higher rate of tax. In this case all

the commodities obtained through process of fermentation such as Curd, Buttermilk, Yakult,

Lassi and others are not picked by the legislature for exemption. Only ‘Curd’ and ‘Butter Milk’

are picked and brought under entry 19 of the III Schedule for the purpose of exemption. Scheme

of the KVAT Act, 2003 is such that those commodities which are not classified under any of the

Schedules are liable to tax at 14.5% under section 4(1)(b)(iii) of Karnataka Value Added Tax

Act, 2003. This being the case, the judgment rendered with regard to classification of goods

under Central Excise Tariff Act cannot be applied to the facts of the case. Judgement in the case

of Mauri Yeast India Pvt. Ltd. vs. State of UP 2008(225) ELT 321(SC) is with regard to

classification of goods under entry Chemicals of all kinds. In this case such an interpretation is

not required for the reasons discussed above. Judgement in the case of Union of India & Others

Vs. Garware Nylons Ltd. (1996) 10 SCC 413 is with regard classification of commodities under

Central Excise Tariff Act to classify ‘Nylon Twine’ and it was held that nylon twine is a kind of

Nylon. Judgement in the case of Indian Aluminum Cables Ltd Vs Union of India and others

(1987)64STC180 (SC) is with regard to principles of construction in the sense they are

understood in trade. This judgement is applicable to the facts of this case for the reason that

‘Curd’ and ‘Butter Milk’ are understood in common parlance and commercial sense as different

commodities and likewise ‘Yakult’ is also understood differently. Judgement in the case of

15 [AR.CLR.CR.23 /2011-12]

Nandi Printers Private Limited Vs State of Karnataka[2001]122STC164(Kar) is in relation to

classification of paper for the purpose of levy of entry tax used in explanation II to entry 16B at

the relevant point of time which is not applicable to the facts of the present case since the Butter

Milk, Curd, and Yakult have emerged through process of ‘fermentation’ are considered

differently in trade and common parlance and are different commodities for the purpose of levy

as discussed above. Judgement in the case of State of Maharashtra v Bradma India Ltd. 2005

140 STC 17 SC is with reference to entries in the schedule to determine whether specific entry

overrides general entry. In this case what is required to be determined is whether ‘Yakult’ fits

into ‘Curd’ and Butter Milk’ and can be called as same commodity. In the case Alladi

Venkateshwaralu and others vs. Government of Andhra Pradesh and another [1978]41STC

394(SC) relied on, goes against the applicant for the reason that the Hon’ble Supreme Court of

India held that ‘Rice in husk’ is Paddy for the reason that there are no separate entries. The

Apex Court has further held that unless the language of the taxing statute is absolutely clear it

should not be given an obviously unfair meaning against the assessee’. In this case the

legislature has carved separate entries such as ‘Curd’, Butter Milk’ and has brought them under

the ambit of exemption and has left out ‘Yakult’ for the purpose of levy. Thus it is unfair to give

a meaning to ‘Yakult’ which is not part of the entry carved out for exemption and to include with

‘Curd and Butter Milk’. Judgement in the case of Aluva Sugar Agency vs. State of Kerala

[2011] 45 VST 1(SC) is with reference to classification of ‘Margarine’ within the meaning of

‘Edible Oil’. In that case ‘Edible Oil’ was with reference to entry No.90 of First Schedule to

KGST Act, which provided for Margarine and also in entry 17A which provided for ‘edible oil’

and the interpretation of the Apex Court was that ‘Margarine’ was ‘edible oil’ eligible for

reduced rate of tax. In this case the legislature itself has distinguished the entries such as ‘Curd’

Butter Milk’ as separate commodities and brought them under I Schedule for exemption and left

out ‘Yakult’ for the purpose of levy. Hence the facts of that case and the facts of the case of the

applicant are different. Judgement in the case of Allahabad Dugdh Utpadak Sahakari vs.

Commissioner of Trade Tax decided on 9.10.2006 is relating to the Mattha and the Hon’ble

High Court answered the question whether on the facts and in the circumstances of the case, the

Trade Tax Tribunal was legally justified in treating ''Mattha and Lassi' as one and the same

commodity and imposing tax as per Notification No.Kani 2-11/XI dated 15.01.2000 when the

''Mattha' being basically Milk is exempted from tax as per Notification No.ST-II-7038/X dated

16 [AR.CLR.CR.23 /2011-12]

31.01.1985 by holding the view that Mattha is a milk product and is sold after mixing the salt

and jeera etc. and is not a milk. Order of the Tribunal rejecting the claim of exemption on the

turnover of mattha was upheld. Further, in the same case it was held that flavored milk, which is

prepared after mixing the dry fruits etc. in common parlance is understood as soft drink and not

as a milk. This decision is not in favour of the applicant. In applicant’s case products obtained

through fermentation for the purpose of exemption is limited to ‘Curd and Butter Milk’ and is

not extended to other products of fermentation. Judgement in the case of R.F. Enterprises Vs.

State of Kerala (2009)23 VST 148(Ker) is the issue relating to inclusion of both thick and thin

butter milk in various forms under entry ‘Curd and Butter Milk’. This was the judgement

rendered while deciding the applicability of entry 92 of First Schedule to KGST Act relating to

‘Milk Products including milk powder, baby food, ghee, cheese and butter except curd, butter

milk, Horliks, Boost Bournvita, Complan and similar items whether or not bottled , canned or

packed’. As there was already an entry called ‘buttermilk’, the Hon’ble High Court has come to

that conclusion. In this case classification for exemption is limited to ‘Curd and Butter Milk’

and the ‘Curd’ which is thicker form of fermented Milk and ‘Butter milk’ which is diluted form

of thicker fermented milk are considered as two different and distinct commodities and are

picked for exemption excluding other goods such as ‘Lassi’ and ‘Yakult’. Thus, this judgement

is also not applicable to the facts of the applicant. Judgement in the case of C.C.E. Vs. Pioneer

Glass Works [2006(197) E.L.T.308] is also not applicable for the reason that, ‘Yakult and Lassi’

cannot be brought under entry ‘Curd and Butter Milk’ since these two commodities obtained

through process of fermentation are only classified for exemption and leaving out ‘Yakult and

Lassi’. Thus, not being classified under entry 19 of the III Schedule to KVAT Act, 2003,

‘Yakult’ is required to be considered as unclassified commodity. Judgement relied in the case of

Commissioner of Sales Tax, Madhya Pradesh vs. Jaswant Singh Charan Singh

[1967]19STC469(SC) will also not support the cause of applicant for the reason that Hon’ble

Supreme Court has held that ordinary meaning used in commercial sense should be preferred

in place of technical or scientific. The applicant is relying on technical opinion of experts,

scientific meaning of probiotic milk, definitions of Dahi, Science of making these products to

drive home that ‘Yakult’ is to be classified under ‘Curd and Butter Milk’ which goes against the

interpretation of the Apex Court in that case since in commercial sense ‘Yakult’ ‘Butter Milk’

and ‘Curd’ are different commodities even though ‘fermentation’ is the basic scientific name

17 [AR.CLR.CR.23 /2011-12]

given to the processes involved to obtain these products. Reliance placed by the applicant on the

judgement in the case of Ramavatar Budhaiprasad Vs. Assistant Sales Tax Officer, Akola -

1962(1)SCR 279 is also not applicable for the reason that the Apex Court held that “the legislature by

using two distinct and different items i.e. item 6 "vegetables" and item No. 36 "betel leaves" has indicated

its intention, decided cases also show that the word "vegetables" in taxing statutes is to be understood as

in common parlance i.e. denoting class of vegetables which are grown in a kitchen garden or in a farm

and are used for the table. In our view, betel leaves are not exempt from taxation”. In this case also the

legislature has made distinction between ‘Curd’ and ‘Butter Milk’ and ‘Yakult’ and exempted Curd and

Butter Milk’ and excluded ‘Yakult’. Further it is held that it is well settled that in interpreting the item in

Statutes like the Excise Act or the Sales Tax Act, whose primary object to raise revenue and for which

purposes they classify divert products, articles and substances, resort should be had not to the scientific

and technical meaning of the terms or expressions used but to their popular meaning, that is to say, the

meaning attached to them by those dealing in them. Thus the applicant’s resorting to technical or

scientific meaning of the term Lassi, Yogurt, Curd, Butter Milk or Yakult is of no consequence to classify

the commodity for the purpose of taxation. In the case of K.V. Varkey Vs. Agricultural Income Tax

and Rural Sales Tax Officer, Peeramade(1954)5STC 348 also it is held that particular words

used by the legislature in the denomination of articles should be understood according to the

common commercial understanding of the term used, and not in their scientific or technical

sense. In the case of Naturalle Health Products (P) Ltd. Vs. Collector of Central Excise,

Hyderabad (2004) 9 SCC 136] the Apex Court for the purpose of classification under HSN code

with regard a Ayurvedic product has held that when there is no definition of any kind in the

relevant taxing statute, the articles enumerated in the tariff schedules must be construed as far as

possible in their ordinary or popular sense, that is, how the common man and persons dealing

with it understand it. Thus the ‘Curd’ and ‘Butter Milk’ are different products in common man’s

understanding and also with regard to ‘Yakult’. Hence ‘Yakult’ cannot be brought under the

ambit of ‘Curd and Butter Milk’ for the purpose of exemption under the provisions of KVAT

Act, 2003. In Asian Paints India Ltd. v. CCE, [1988] 2 SCC 470 which was a case of emulsion

paint, at para 8 the Apex Court said that "It is well settled that the commercial meaning has to be

given to the expressions in tariff items. Where definition of a word has not been given, it must be

construed in its popular sense. Popular sense means that sense which people conversant with the

subject matter with which the statute is dealing, would attribute to it." Thus, ‘Yakult’ in popular

sense is not ‘Curd’ or ‘Butter Milk’. Applicant’s reliance on the judgement in the case State of