CIA PROCEDURAL MANUAL · Title: CIA PROCEDURAL MANUAL Subject: CIA PROCEDURAL MANUAL Keywords

CA SANJAY M DHARIWAL

PROCEDURAL ASPECTS OF VAT

CONTENTS

Reconciliation of returns and annual reports

Sale of Assets

Analyzing events occurring after balance sheet

date

Analyzing data under allied laws, viz. Excise,

customs and service tax

Analyzing commodity classification (HSN/CTH

Codes)

RECONCILIATION OF RETURNS AND ANNUAL

REPORTS

• The objective under VAT law is to ensure that all the dealers are complying with the VAT Laws through independent professional examination.

• The turnover has to be compared with the Financials to know whether the dealer has disclosed the right turnover and has discharged the VAT liability.

• The difference in reconciliation of returns and annual reports will be due to non accounting of sales invoices and purchase invoices and other varied reasons.

RECONCILIATION OF RETURNS AND ANNUAL

REPORTS

Sales

Total Turnover as per Monthly returns xxxx

Total Turnover as per KVAT Audit Report xxxx

Difference in Total Turnover xxxx

Reasons

Non Accounting of sales Invoice

Difference in CST Turnover

Other reasons

xxxx

RECONCILIATION OF RETURNS AND ANNUAL

REPORTS

Sales

Taxable Turnover as per Monthly returns xxxx

Taxable Turnover as per KVAT Audit Report xxxx

Difference in Total Turnover xxxx

Reasons

Tax Collected

Freight charges

Discount

Labour and like charges

xxxx

RECONCILIATION OF RETURNS AND ANNUAL

REPORTS

Purchase

Total Purchase as per Monthly returns xxxx

Total Turnover as per KVAT Audit Report xxxx

Difference in Total Purchase xxxx

Reasons

Non Accounting of Purchase Invoice

Difference in CST Purchase

Other reasons

xxxx

RECONCILIATION OF RETURNS AND ANNUAL

REPORTS

Input Tax credit

Eligible input tax credit as per Monthly returns xxxx

Eligible input tax credit as per KVAT Audit Report xxxx

Difference in Eligible Input tax credit xxxx

Reasons

Eligible input tax credit on capital goods

Other reasons

xxxx

RECONCILIATION OF RETURNS AND ANNUAL

REPORTS

Other issues 1)Test check

2)Monthly returns- Disclosure monthly or annually

3) Management Certificate for

a) Stock

b) Classifications of goods and rate of taxes

c) Monthly return filed

d) Visit register of the department

e) Non declared sales

f) Input tax credit on registered purchases

SALE OF ASSETS

The term Sale has been defined under section 2(29)

of the Karnataka Value Added Tax Act, 2003 as

under:

“Sale” with all its grammatical variation and cognate

expressions means every transfer of the property in

goods (other than by way of a mortgage, hypothecation,

charges or pledge) by one person to another in the course

of trade or business for cash or for deferred payment or

other valuable consideration and includes (a) .. (d)

SALE OF ASSETS

Any transfer of property in goods by one person to another in the course of business is liable to tax under the KVAT Act. Hence sale of fixed assets is liable to VAT.

Therefore the dealers are liable to discharge VAT on sale of fixed assets even though the dealer is not dealing in purchase and sale of the assets in the course of his business.

However there is contrary view held by the Hon’ble Karnataka High Court in the case of Ciniplex Pvt Ltd.

SALE OF ASSETS

Hon’ble High Court of Karnataka in the case of

CINIPLEX PVT LTD V STATE OF KARNATAKA [2012] 53

VST 84, wherein it was held that sale of used/discarded

Metal detectors, water coolers and lockers by assessee

engaged in business of sale of food articles, snacks and

beverages is one time sale of discarded goods. The

assessee is not a dealer in these goods and hence not

liable to tax on sale of such discarded goods.

ANALYZING EVENTS OCCURRING AFTER

BALANCE SHEET DATE

Events occurring after the balance sheet date are

those significant events, both favourable and

unfavourable, that occur between the balance sheet

date and the date on which the financial statements

are approved by the Board of Directors in the case of

a company, and, by the corresponding approving

authority in the case of any other entity.

ANALYZING EVENTS OCCURRING AFTER

BALANCE SHEET DATE

Two types of events can be identified:

a) those which provide further evidence of

conditions that existed at the balance sheet date; - Adjustment to assets and liabilities

b) those which are indicative of conditions that

arose subsequent to the balance sheet date – Disclosure to be made

ANALYZING DATA UNDER ALLIED LAWS, VIZ

EXCISE, CUSTOMS, AND SERVICE TAX

• Excise

• Turnover declared under excise and turnover declared under VAT

• Whether VAT is charged inclusive of excise duty

• Verification of transactions whether excise is collected separately or in the excise invoice – to check evasion of VAT on excise duty.

• Cross check if exports turnover is declared under VAT whether the same is followed under excise. If not then the reason for differential approach

ANALYZING DATA UNDER ALLIED LAWS, VIZ

EXCISE, CUSTOMS, AND SERVICE TAX

• Service Tax

• Check whether sale of goods transactions are

declared or shown as service provided to evade

VAT.

• Analyze whether certain transactions are

covered under service tax or VAT. Example

hiring of movable goods, transfer on intellectual

property rights or C & F Agent service.

ANALYZING COMMODITY CLASSIFICATION

HSN Code is the Harmonised System of Nomenclature and has 8 digit

code.

The eight digit code shows the HSN at 8 digit level under the name

"Tariff Item".

The first two digit of the code provides chapter number, the next two

digits gives the Customs Tariff Head (CTH) grouping. The third set of

two digits in the code gives the Customs Tariff Sub-heading.

This six digit code is aligned with Harmonized System of

Nomenclature adopted by World Customs Organization.

The last two digits provide Customs Tariff Sub-sub-head for the entry.

They are specific to India.

Thus the Code is the same as that in other countries only at six digit.

ANALYZING COMMODITY CLASSIFICATION

• As far as VAT is concerned the rules of interpretaion of

Central Excise Tariff Act, 1985 is applicable.

• However, where any commodities described against the

Heading or sub-headng and the aforesaid description is

Different from the corresponding description in the Central

Excise Tariff Act then only those commodities described

under VAT will be covered and other commoditeis though

covered by corresponding description in Central Excise

Tariff will not be covered in VAT

About us

NATIONAL INFORMATICS CENTRE is a

Govt of India organization under Min. of ICT

NIC, Karnataka State Unit started functioning

from 1987

• Provides state-of-art IT solution with offices at the State and at District HQ

• Nation-wide Satellite Communication -NICNET

Services

System Study, Analysis, Design & Development of Software

Issue of Digital Certificates

Networking

Training

Web design & hosting

Video Conferencing

e-mail & Internet facilities

Hardware & Software for paid projects through NICSI

What is e-governance

E-governance is the application of Information and

Communication Technology (ICT) for delivering

government services, exchange of information

communication transactions, integration of various

stand-alone systems and services between

government-to-customer (G2C), government-to-

business (G2B), government-to-government (G2G)

as well as back office processes and interactions

within the entire government framework.

Benefits of e-governance

1 • Simplification of processes

2 • Transparency

3 • Accountability

4 • Online Service Delivery

5 • Anywhere and Anytime

6 • Seamless integration with other system

7 • Effective Monitoring

Online Request

Online Delivery

Status Checking

Online Process

Time-bound Processing

Effective Service Delivery

1 • Systems Requirement Specifications

2 • Design the System

3 • Software Development/Coding

4 • Developer Testing/User Acceptance Testing

5 • Roll out Plan (Pilot and Phased)

6 • Software Change Management

Not owning the project / Depending on outsiders

Inaccurate estimates of needed resources

Badly defined systems requirements

Poor reporting of the project’s status

Not planning of the project – Schedules, Roles, etc

Poor communication among stakeholders

No Monitoring Cell (e-governance cell)

Information Security (IS)

The protection of Information and Information

Systems from unauthorized access, use,

disclosure, disruption, modification or

destruction in order to provide confidentiality,

integrity and availability

• Maintaining and assuring the accuracy and consistency of data over its entire life-cycle Integrity

• Available when it is needed

• IT system is functioning properly Availability

• Data is not available for un-authorized / un-classified people Confidentiality

• Validate the parties invloved are who they claim to be Authenticity

• Implies one’s intention to fulfil their obligations to a contract Non-repudiation

Information Security - Key Concepts

• Administrative

• Logical

• Physical

Security Controls

• Unclassified

• Restricted

• Confidential

• Secret

Data Classifications

• Identification

• Authentication

• Authorisation

Access Controls

Information Security – Some Concepts

Natural Disasters

Technical Failure

Software Mal-

functioning

Stakeholders Intentions

Hacker Attacks

Threats to Information Security

Data

Define Security Policy & Procedure

Define Roles & Responsibilities of stakeholders

Create awareness and training

Conduct 3rd party Security Auditing

Backup & Disaster Recovery Plan

Information Security Management

1 • Organization of Information Security

2 • Asset Management

3 • Human Resource Security

4 • Physical and Environment Security

5 • Communication and Operations Management

6 • Access Control

7 • IS acquisition, development and maintenance

8 • IS incident management

9 • Business Continuity Management

10 • Regulatory Compliance

Information Security Policy and Procedure

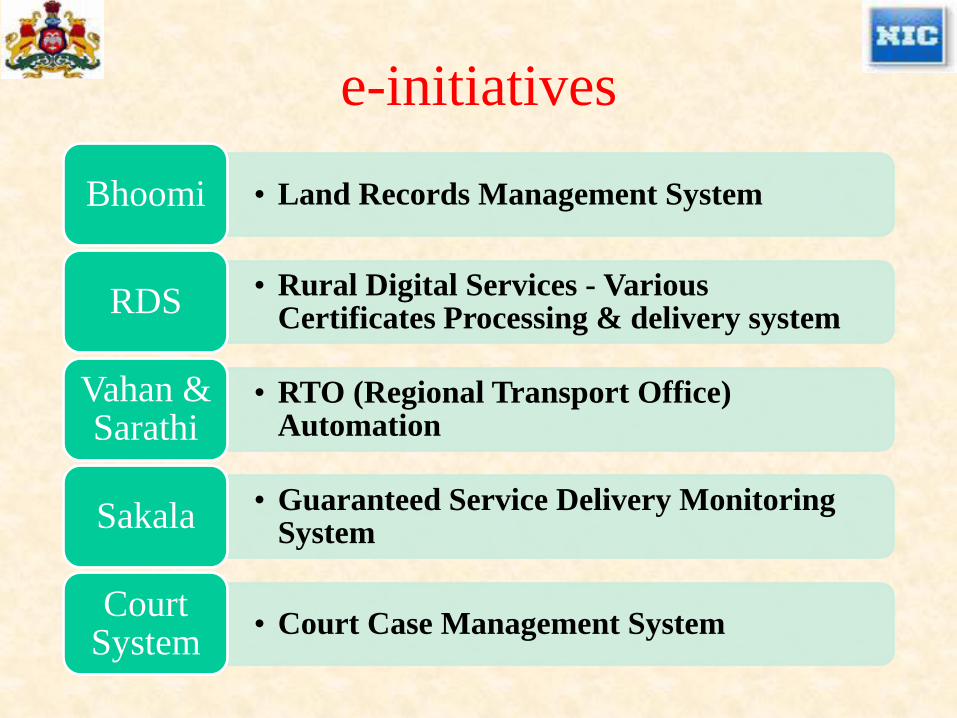

e-initiatives

• Land Records Management System Bhoomi

• Rural Digital Services - Various Certificates Processing & delivery system

RDS

• RTO (Regional Transport Office) Automation

Vahan & Sarathi

• Guaranteed Service Delivery Monitoring System

Sakala

• Court Case Management System Court

System

e-initiatives

• VAT Processing System for Commercial Taxes

E-VAT

• Management System for Ration Cards and Public Distribution System

Ahara

• Panchayat Automation System Pancha tantra

• File and Letter Monitoring System FMS/LMS

• Online Seat allotment system for Professional Colleges

CET

• Online Recruitment/Counselling System Recruitment

The Commercial Taxes Department

• The Commercial Taxes Department in Karnataka contributes

about 61% of the revenue by way of own taxes to the State

• Collects about Rs. 37,000 crores per annum.

• Has a total strength of about 7000 employees including 800

officers.

• Administers 9 different Tax laws – VAT, KST, CST, Luxury

Tax, Profession Tax, Entry Tax, Betting Tax and

Entertainments Tax

• The Department is structured in a combination of Territorial

and Functional jurisdictions.

• Has 13 administrative divisions, 118 VAT offices, 20 check

posts, 7 enforcement divisions, 13 appeals divisions and 100

mobile check posts. 17

Commercial Taxes Department Backbone of state’s finances but:

Outdated systems lead to pilferage and corruption.

Cost of compliance very heavy for tax payers – permissions,

frequent visits, harassment

Paper based systems unable to cope with high volumes.

Emphasis on regulatory role and policing

Bogged down by routine work – no attention to analysis

High pilferage

More physical controls

Higher cost of compliance and

discretion

More corruption

Objective of Project

Department as regulator

Frequent visits by dealers

Policing by Department

Paper based information

Old paradigm – Post event confirmation

Department as a service provider

All services at doorsteps

Self Policing by Dealers

Everything is electronic

New paradigm - Pre event confirmation

A new Paradigm

Making

Checkpost

Hassle free

Accessibility

Through

Mobile phones

Policing by

Citizens

Transparency

and

Accountability

E - SUGAM

E - SUVEGA

Comprehensive

Assessment

System

E - GRAHAK

E - CST

E - VARDAN

E - VARADI

E - GRIEVANCE

E - PAYMENT

Services at

doorsteps

M - SUGAM

E-reconcile

Project

Transformation

E- SERVICES of VATsoft

20

E-enforcement

system

21

Dealers

• E-VARDAN – Online registration request & processing

• E-VARADI – Online submission of returns

• E-payment – Online payment of Taxes

• E-CST – Online request & issue of the CST forms

• E-Grievance – Online grievance redressal

• E-Clearance – Online request & issue of Clearance Certificate

• M-Services – Mobile Based Alerts

Dealers/ Transporters

• E-SUGAM/M-SUGAM forms – Online request and download of Form for Goods movement

• E-SUVEGA forms – Online request for Transit Pass for movement of goods through State

CItizens

• e-Grahak/m-Grahak – SMS based information/complaint by public on the dealer

Officers

• E-CAS – Comprehensive Audit System

• E-reconcile – Tax Collection Reconciliation system

• E-enforcement System

• E-DCB – Demand Collection Balance System

• E-Dealer File – Consolidated Dealer Information System and Analysis

E-SERVICES FOR MAIN STAKEHOLDERS

E-Services – ALL Services are online and at the doorstep of the dealer

22

1 • E-VARDAN – Online registration request & processing

2 • E-VARADI – Online submission of returns

3 • E-payment – Online payment of Taxes

4 • E-SUGAM forms – Online request and download of Form for Goods movement

5 • E-SUVEGA forms – Online request for Transit Pass for movement of goods through State

6 • E-CST forms – Online request and issue of the CST forms

7 • E-Grievance – Online grievance redressal

8 • E-Clearance – Online request and issue of the Clearance Certificate

M-SERVICES – MOBILE BASED SERVICES

1 • M-SUGAM request – SMS based request and issue of SUGAM Form

2 • M-TIN Verify – SMS based verification of dealer details

3 • M-CST form Verify – SMS based verification of CST forms

4

• M-SUGAM alert – SMS based daily alert to dealer on SUGAM downloads from his account

5 • M-payment Alert – SMS based alert to dealer on e-Payment receipt

6

• M-SUGAM Verify – SMS based verification of SUGAM form by mobile Check Post Officers

7 • M-Grahak– SMS based information/complaint by public on the dealer

23

THE CHALLENGES

E - governance

BPR – New Laws, Rules &

Procedures

Technological Interventions –

Environment Building Capacity Building

Supervision and Discipline

BUSINESS PROCESS RE-ENGINEERING

1

• Change in law – Policy advocacy

• Unique Selling Proposition was – Checkposts become hassle free.

2

• Change in Rules – Trade Bodies involved in drafting new rules.

• Guaranteed Service Delivery

3

• Change in form – Re-design of forms

• The forms and screens designed by end users.

TECHNOLOGY INTERVENTION

Web based system for 4,50,000 + dealers.

CTDWAN for networking 2000 systems located in 176 offices/check posts.

Integrated with SMS gateway of NIC.

A control room, working 24X7, has been established.

The software development by an in-house team of NIC.

ENVIRONMENT BUILDING – WINNING OVER THE DEALERS

Interactive meets with trade bodies to introduce the concept.

Main selling point – dealers no longer required to come to tax offices to obtain ‘Delivery Notes’ and trucks would get instantaneous clearance at checkposts.

Guaranteed Service Delivery On ground success seen when different

trade bodies started competing with each other to organize training programmes. Department just provided the resource personnel.

CAPACITY BUILDING – ENABLING THE OFFICERS AND OFFICIALS

All officers/officials imparted week

long mandatory training on E-

governance initiatives and basic

Computer skills.

Administrative Training Institute

and District Training Institutes

used.

Training programme was

completely hands on, with Trainers

selected from the department.

INTEGRATED ANALYSIS

E-RETURN

E-SUGAM: Sales & Purchases

E-CST: Issues and Receipts

E-240 form (audited annual

form)

E-TDS

E-Registration

E-payment & Other Payments

No Service Transaction

Volume Coverage

1 E-returns 4.1 Lakhs 100%

2 E-payment 1.5 Lakh 80 %

3 E-Sugam 24 lakhs 100%

4 E-Suvega 0.25 lakh 100%

5 E-CST forms 1.35 Lakhs 100%

6 E-grievance, NOC 1,500 100%

7 E-registration 5,000 100%

8 E-240 forms (in one year) 0.6 Lakh 100%

MONTHLY VOLUME OF THE TRANSACTIONS

THE OUTCOMES - 1

Advantage Trade

• Services at door steps

• Dealers no longer come to the offices.

• About 30,000 visits of dealers saved/day.

• Zero scope for corruption.

Fast Track Transportation

• Check posts became much more friendly.

• The delays at check posts were reduced.

THE OUTCOMES - 2

Efficient Tax Administration • Tax administration has become more

efficient.

• There was a marked increase in revenue (cannot be ascribed to Sugam only).

• The drudgery of officer has reduced and his/ her accountability has increased.

• Effective analysis of dealer file by officers

Environment friendly • Saves about one ton of paper per day.

• Saves waiting time and fuel consumption at check posts for transporters.

No Key Area Before After

1 Number of persons visiting offices/day 30,000 1000

2 Number of dealers filing e-returns 0 100%

3 % of tax coming through e-payment 0 92%

4 Waiting time at checkposts 7 min 1 min

5 Number of returns processed 5% 100%

6 Review of assessment orders 5% 100%

7 Timely delivery of services Not Av. 99.9%

8 No. of sheets consumed per day 1,00,000 0

9 Time required for issue of transit pass 1 hour 3 min

KEY PARAMETERS – COMPARATIVE ANALYSIS

Very Low0% Low

1%

Average19%

High 55%

Very High23%

Invalid response2%

Dealers - Overall Rating

Very Low0%

Low3%

Average31%

High 49%

Very High13%

Invalid response4%

Practitioners - Overall Rating

IMPACT ASSESSMENT OF E-GOVERNANCE INITIATIVES

BY ERNST AND YOUNG

Very Low0%

Low2%

Average8%

High 65%

Very High25%

Employees - Overall Rating on effectiveness of VAT E-filing system

IMPACT ASSESSMENT OF E-GOVERNANCE INITIATIVES BY ERNST AND YOUNG

78%

61%

83%

70% 71%

76%

59%

73%

44%

81%

55%57%

68%

55%

Computer Literacy

Availability of prof icient ICT conversant

manpower

Ease of use of VAT E – Filing

system

Departmental assistance

Cost ef f iciency Reliability of VAT E – Filing

system

Data / transaction

security wrt e-

Services

Factors facilitating switch to e-Services

Dealers STPs

IMPACT ASSESSMENT OF E-GOVERNANCE INITIATIVES

BY ERNST AND YOUNG

THE UNIQUE FEATURES

1 • It was totally home grown.

2

• An excellent example of convergence of Government agencies and resources.

3 • Magnitude is huge.

4 • Self-policing by trading community.

5 • In the last three years, not even once has the system failed.

6

• Because of in-house team of NIC, managing the software, and updating software becomes hassle free.

7 • This project represents a WIN-WIN-WIN situation.

REPLICABILITY

1

• NIC is supporting North Eastern States - Arunachal Pradesh, Manipur, Nagaland, Tripura, and Mizoram and Union Territories - Diu, Daman and Nagar Haveli in implementing these modules.

2

• E-CST module is replicated in Goa, TN, Chattisgarh, Pondicherry by NIC

• E-payment concept is being replicated for GST system

3

• Number of states have visited and studied the system for replication – Gujarat, UP, Uttarakhand, Chhattisgarh, TN, Bihar, AP, Maharastra, etc.

VAT-Concepts, in

relation to Works

Contract, Leasing,

Hire Purchase

Dr B V Murali Krishna,

JCCT-(eAudit)

e-mail: mkprakruthi@ yahoo.co.in

[email protected], Cell: +9198440 41308

Wednesday, September 10,

2014

2

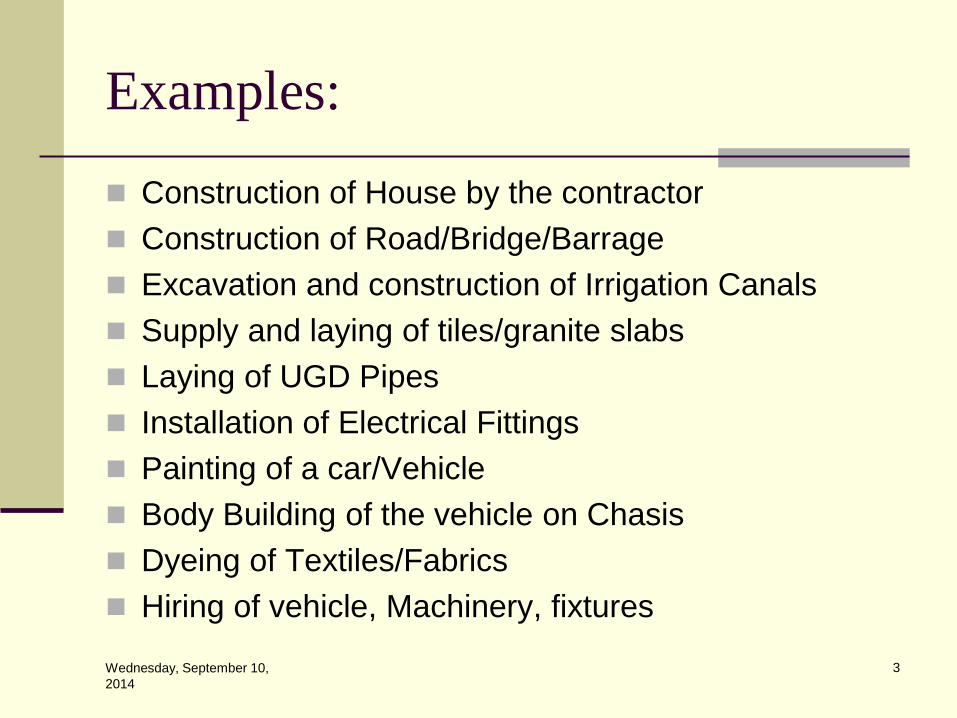

Stages of Building Construction

Examples:

Construction of House by the contractor

Construction of Road/Bridge/Barrage

Excavation and construction of Irrigation Canals

Supply and laying of tiles/granite slabs

Laying of UGD Pipes

Installation of Electrical Fittings

Painting of a car/Vehicle

Body Building of the vehicle on Chasis

Dyeing of Textiles/Fabrics

Hiring of vehicle, Machinery, fixtures

Wednesday, September 10,

2014

3

BASICS

Wednesday, September 10,

2014

4

Do you Know….?

Bailment

Barter

Capital

Hiring

Hire Purchase

Hypothecation

Lease

Mortgage

Sale

Service

Works Contract-Job work, Labour work, Material and

Labour work

Wednesday, September 10,

2014

5

9/10/2014 6

Tax Element

Profit Element

Purchase Value

Key Provisions of……

Dealer

Business

Sale

Deemed sale-works contract, Leasing, HP

{Sale- CST- 11/5/2002- Deemed Sale}

Input Tax

Out Put Tax

Re-assessment

Tax Period

Wednesday, September 10,

2014

7

Definition of “Goods”-KVAct

Sec 2 (15)- “Goods” means all kinds of movable property (other than newspaper, actionable claims, stocks and shares and securities) and includes livestock, all materials, commodities and articles(including goods, as goods or in some other form) involved in the execution of works contract or those goods used to be in the fitting out, improvement or repair of moveable property, and all growing crops, grass or things attached to, or forming part of the land which are agreed to be severed before sale or under the contract of sale.

9/10/2014 8

Definition of “Goods”-BVAct

Sec 2 (l)- Goods means all kinds of movable

property including livestock, computer

software, any electronic chip used for the

purpose of storing or transmitting data or

voice and all materials, commodities and

articles (as such or in some other form) but

excluding newspapers, electricity, actionable

claims, stocks, shares or security.------

9/10/2014 9

Kinds of Properties

Movable Property.

Immovable Property.

Intellectual Property.

9/10/2014 10

Definition of “Sale”-KVAT

Sec 2 (29) “Sale”- with all grammatical

variation and cognate expressions means

every transfer of property in goods(other than

by way of a mortgage, hypothecation, charge

or pledge) by one person to another in the

course of trade or business for cash or for

deferred payment or other valuable

consideration and includes.- …………..

Sec 2(zc)-BVAT

9/10/2014 11

Definition of “Sale”……

and includes.-……

(a) a transfer, otherwise than in pursuance of a contract, of

property in any goods for cash, deferred payment or other

valuable consideration;

(b) a transfer of the property in goods (whether as goods or

in some other form) involved in the execution of a works

contract;

(c) a delivery of goods on hire-purchase or any system of

payment by installments;

(d) a transfer of the right to use any goods for any purpose

(whether or not for a specified period) for cash, deferred

payment or other valuable consideration;

Wednesday, September 10,

2014

12

Bundle of Rights…..

Owner of property has bundle of rights:

Right to possess,

Right to destroy

Right to use and/ enjoy

Right to usufruct (right to use or enjoy & right

to derive profit )

Right to consume

Right to alienate

Right to transfer

9/10/2014 13

What is transferred…?

Sale

Lease

Bailment

Hire Purchase

All the rights of owner

Only the Right to

use(passage of

control over the

economic benefits)

Delivery of goods for

a particular period

All the rights of the

owner- payment by

installments

9/10/2014 14

Sec 2 (37) :Any agreement for carrying out for cash,

deferred payment or other valuable consideration

the building, construction, manufacture,

processing, fabrication, erection, installation,

fitting out, improvement, modification, repair or

commissioning of any movable or immovable

property

Definition of “Works Contract”:KVA

Sec 2(zh)- Works Contract: means any agreement

for carrying out for cash or deferred payment or

other valuable consideration, the construction,

fitting out, improvement or repair of any building,

road, bridge or other immovable or movable

property

Definition of “Works Contract”:BVA

Types of Contract

Pure Labour Contract-Service

Material Contact-Sale

Works Contract-Material and

Labour(Composite Contract)

Divisible by legal fiction Wednesday, September 10,

2014

17

EVOLUTION

Wednesday, September 10,

2014

18

Article 366

366.Definitions.-(12)”goods” shall include all materials,

commodities, and articles;

(29A)” tax on sale the sale or purchase of goods” includes-(46 Amend..1982)

(a) a tax on the transfer..

(b) a tax on the transfer of property in goods…

© a tax on the delivery of goods on hire-purchase..

(d) a tax on the transfer of the right to use any goods…

(e) a tax on the supply of goods by an unincorporated association or body of..

(f) a tax on the supply , by way of or as part of any service or in any other

manner whatsoever, of goods, being food or any other article for human

consumption or any drink…

and such transfer, delivery or supply of any goods shall be deemed to be a sale

of those goods by the person…

Wednesday, September 10,

2014

19

Evolution of WCT

State of Madras Vs. Gannon Dunkerley & Co (Mad) Ltd.

[1958] 9 STC 353 (SC)

Clause 29(A)inserted in Article 366- 46th Amendment-

Deemed Sale – A legal fiction

A Transfer of property in goods ( whether as goods or in

some other form) involved in the execution of works

contract

Builders India Association Vs Union of India [1989] 73

STC 370 (SC) All restrictions will apply to WCT

Gannon Dunkerley & Co Vs State of Rajasthan (1993) 88

STC 204 (SC)- Constitutional Validity

Wednesday, September 10,

2014

20

Evolution of WCT

Builders Association of India Vs State of Karnataka

(1993) 88 STC 288 (SC)-Theory of Accretion & Deductions

Builders Association Of India Vs State of Kerala (1997)

104 STC 134 (SC)-Composition, No deduction

BSNL Vs Union of India [2006] 3 VST 95 (SC)- Splitting of

Sale element & Service element only in case of

WCT/Catering [(2006) 145 STC 91(SC)-Aspect Theory

State of A P Vs Kone Elevators [2005] 140 STC 22 (SC)-

Contract for Sale or work-Lifts-Sale-Overruled-06.05.2014

Wednesday, September 10,

2014

21

Later References-WCT Mittal Investment corporation Vs Addl Commr of Commercial

Taxes [2001] 141 STC 14 (Kar)- Nature of Agreement

K. Raheja Development Corporation Development Vs State

of Karnataka[ 2005] 141 STC 298 (SC)- Development

Agreement.

Assotech Reality Private limited Vs State of UP [2007(7)

STR 129],

Continental Builders & Developers Vs State of Karnataka

[2008] 64.Kar.L.J 104(HC)(DB)- Developmental Charges

Not exigible to WCT ?

Magus Construction Pvt. Ltd. and another v. Union of India

and others (2008) 015 VST 0017 (Gauhati).

Wednesday, September 10,

2014

22

Later References-WCT Imagic Crative (P) Ltd Vs CCT,Bangalore [2008] 12 VST 366

(SC)-Composite Contract- Sale & Service-Exemption

towards service –Correct-Mutually exclusive

State of Andhra Pradesh & Others Vs Larsen & Turbo Ltd

(L&T) & Others, [2008] 17 VST 1(SC), One Deemed sale

L& T Vs State of Karnataka [2008] 17 VST 460(SC)-KRDC-

Review- Referred to larger bench

L& T Vs State of Karnataka [2013] 26.09.2013 65 VST 1

(SC)- 3 Member Bench-Larger Bench

Kone Elevators Vs State of Tamil Nadu [2014] 06 May

2014(SC) 4:1 Constitutional Bench [2014] 71 VST 1(SC)

Wednesday, September 10,

2014

23

Declared goods- Rate of Tax-WCT

Gannon Dunkerley & Co Vs State of Rajasthan (1993) 88 STC 204

(SC)

Builders Association of India Vs State of Karnataka (1993) 88 STC

288 (SC)

B V Subbareddy Vs DCCT [2008] 11 VST 715 (Kar)(DB)-

Construction of Bridge

URC Construction Ltd Vs DCCT [2008] 11 VST 896 (kar HC)

Afcon Infrastructure Ltd Vs State of Assam [2007}9VST 195

(Assam)- Declared goods Sec 14/15 apply under VAT

Nagarjuna Construction Company Limited Vs State of Kar

[2011] 45 VST 390 (Kar)- Subject to restrictions under CST Act.

Wednesday, September 10,

2014

24

Issue of goods in WCT- Sale ?

N.M. Goel & Co. v. Sales Tax Officer [1989] 72 STC 368

(SC); (1989) 1 SCC 335,

Rashtriya Ispat Nigam Ltd. v. State of Andhra Pradesh

[1998] 109 STC 425 (SC); (1998) 8 SCC 439

Cooch Behar Contractors' Association v. State of West

Bengal [1996] 103 STC 477 (SC)

Rajasthan Taxation Board, Ajmer and others (and other

appeals)-[2004] 136 STC 641 (SC)

Wednesday, September 10,

2014

25

INCIDENCE &

PROCEDURE

Wednesday, September 10,

2014

26

Incidence, Levy of Tax,

Assessment-BVAT Chapter-II Incidence of Tax

Chapter-IV Rate of Tax and Point of Levy

Chapter-VI Returns, Assessment, Re-Assessment and Payment of Tax

Rule 18; Taxable Turnover: In the case of works contract, the amount remaining after deducting from the gross value of the contract the amount on account of the following— (a) Labour charges for execution of the works contract, (b) Amount paid to sub-contractor on account of labour and services, (c) Charges for planning, designing and architects fees, (d) Charges for obtaining on hire machineries and tools used in the execution of the works contract, (e) Cost of consumables such as water, electricity, fuels, etc. used in execution of the works contract the property in which is not transferred in the course of execution of a works contract, (f) Cost of establishment of the contractor to the extent it is relatable to supply of labour and services, (g) Other similar expenses relatable to supply of labour and services, (h) Profit earned by the contractor to the extent it is relatable to the supply of labour and services, and (i) Goods or transactions exempted under section 6 or section 7 of the Act;

Wednesday, September 10,

2014

27

Why Composition: KVAT Act..

An option to be exercised by the dealer

Easy and Simple to Calculate

No need to maintain detailed accounts

Classification of goods/ Nature of works contract is not required

Deductions/exemptions are restricted/ narrow

Levy of Single Rate of Tax

Tax on Total Consideration

Levy is on the consideration relatable to goods/labour

Subject to certain restriction and conditions

Wednesday, September 10,

2014

28

Composition of Tax-WCT

Section 15(1)-COT- Rate of tax not exceeding 5%

4% on the total consideration -by Notification-No FD 55 CSL 2005(7),Bangalore, dated 23-3-2005(Sl No 7),

No FD 116 CSL 2006(13),Bangalore, dated 31.03.2006(Sl No 53)

1.4.2007-Dealer- having more than one type of business, can opt. Ex: Motor vehicle dealer having WCT, can opt for COT for WCT and pay regular tax on motor vehicles.

Can not claim Input tax on purchases effected-Sec 15(4)

COT Dealer Can collect tax -WCT(1/4/2007)

Wednesday, September 10,

2014

29

COT-Continued Section 15(5)-W.e.f 1.4.2006

WCT dealer buying Interstate purchase goods can opt.

Deduct the Turnover relating to ISP from Receipts and pay WCT on remaining and Regular rate for ISP goods.

Can Claim exemption on Sub contractor turnover.

WCT Dealer buys and sells goods other than WCT-pay out put tax- No Input tax claim-Clarity w e f 1.4.2007-ITC 15(4).

Pay URD tax U/s 3(2)- at tax applicable- Inserted from 1/4/2006 by Act No 6 of 2007.

Section 15(5)e- Effect from 1.04.07, Mycon Construction Co Vs S O K [2009] 24 VST 250 (kar), Amendment prospective effect

Under COT-2005-2006-One Sale-Back to Back Contract-Sub Contractor deduction available- Skyline Constructions & Housing Pvt Ltd Vs ACAR[ 2011] 3 VST 290(Kar DB)

Dealer Opting for Composition-Cannot permitted to resile and seek regular assessment in same year- Koothattukulam Liquors Vs DC Sales Tax- [2014] 72 VST 353(SC)

Wednesday, September 10,

2014

30

WCT- Regular Scheme

VI Schedule- 23 entries-01.04.2006

Rate of Tax : 1 %, 4/5/5.5 % and 12.5/13.5/14/14.5%

Declared goods-Sec 4(1) subject to Sec 14 of CST Act

1956

Exemptions: Rule 3(2)- Taxable Turnover-deduct

Sub Contractor Turnover

Labour and Labour Like Charges

Gross Profit Relatable to L & L Charges

Return of goods, Input Tax Credit, Tax Collected

Separately

Proportionate deduction, to the value of goods when the

total turnover is not sufficient Wednesday, September 10,

2014

31

WCT- Labour & Like Charges

Rule 3(2)(m)When not ascertainable: Type of Contracts

Installation of AC and Coolers- 10%

Installation of Plant & Machinery, Lifts, escalators, fixing of sanitary

fittings,—15%

Building of Ship & Boat, barges, ferries, tugs,trawlers, draggers

Painting & Polishing, Construction of Bus bodies/trucks, laying of

pipes-20%

Fixing of marble and granites stones, tiles, -25%

Civil works, Railway coaches-30%

Tyre retreading, Dyeing of printing of textiles -40%

Any other works contract- 25% Ex: AMC in IT Industry

Notes: When deduction under this clause, then no ITC wrt on hire

charges of machinery, tools etc purchase of consumables

Gross Profit shall not apportionable when deduction under this clause

Wednesday, September 10,

2014

32

WCT- Labour & Like Charges

L & L Charges include:

Charges for obtaining on hire or otherwise, machinery and

tools used in the execution of works contract

Charges for planning, designing and architects fees

Cost of consumables used in the execution of works

contract

Cost of establishment to the extent relatable to supply of

labour and services and other similar expenses relatable to

supply of labour and services

Wednesday, September 10,

2014

33

WCT-Input Tax Restrictions

Tax paid on goods as specified in Fifth Schedule, which

are procured other than for resale, or manufacture or any

other process of other goods for sale- Sec 11(2).

Tax Paid on purchases as notified by the Govt or

Commissioner –Sec 11(3)- Cement used in pipe & fittings

and cement bricks.

ITR towards the Sub contractor payment-Sec 11(c)from

1.4.2006-Introduced in Aug 2008/ 01.04.2012

(Cannot claim both Input Tax and Sub Contractor

Turnover of a particular RA Bill)

ITR towards purchase of consumables, claimed as

deduction- Sec 11(c)(ii)-Ex: Dyeing of Textiles Wednesday, September 10,

2014

34

Deduction of Tax @ Source

Collection of Tax by Registered dealer, Govt & Statutory Authorities-Section 9.

TDS-works contract-amount equivalent to the tax payable-Sec 9-A

Certificate of Tax Deduction-Form VAT 156

Wednesday, September 10,

2014

35

Assessment

Section 38 of KVAT Act, 9(2) of CST Act

All are deemed to be assessed based on the return filed, except notified by CCT.

Fails to file return-assessment-best of judgment

When the return filed subsequent to assessment, with in a month-liable for penalty & Interest.

Protective assessment-Section 38(5)-reason to believe that dealer will fail to pay any tax, penalty, interest-by prescribed authority-permission from JCCT or Addl commissioner.

Unregistered Dealer-Section 38(7)

Wednesday, September 10,

2014

36

Re-assessment of Tax

Section 39 of KVAT Act/ 9(2) of CST Act

Return furnished-deemed as assessed- or

assessment U/s 38,-Understates the correct tax

liability of the dealer.

The re-assessment is subject to further re-

assessment based on any “further evidence”.

Unit of assessment and Re-assessment is “Month”

under VAT / “quarter” for COT

Procedural/provisional aspect for CST assessment or

Re-ass, etc., is similar to the powers under general

sales tax law of the state. Section 9(2) of CST Act.

Wednesday, September 10,

2014

37

Issues in WCT……

Joint Development Contract-Developer Share/Owner Share

Land Cost in lieu of Construction Cost.

Input Tax Restriction- Owner Share

Sub Contractor Turnover-Owner Share

Sub Contractor Turnover restriction- Immovable property/Commercial Property leased

Labour & Like Charges restriction- Immovable property/Commercial Property leased

Under COT, if JD, Add back Construction cost of Owner share, if the Land Cost is claimed as exemption/un declared.

Land Owner can be considered as prospective flat buyer-JD

Taxable Event on goods-as goods or in other form- Before accretion, or at the time of accretion or after accretion (incorporation)

Taxability- Interstate WCT ? PO or Contract/Agreement..

Wednesday, September 10,

2014

38

Specific Issues under works

contract, leasing…. Rate of Tax on On Iron & Steel when used in same form or other

form

Levy of Tax In case of Back to Back Contracts

VAT Liabality in case of “Agreement to sell” Contracts

VAT applicability on Service tax component & other statutory

liabalities

Exemption of Land value or UDI in Residential Constructions.

Theory of Accretion or Incorporation- Deemed sale of goods

Finance lease/ Operating lease

Theory of Effective Control & Possession- Under leasing

Theory of Effective Control- Incase of Software or IPR ?,

because the ownership always lies with Owner ?

Wednesday, September 10,

2014

39

Leasing & Hire Purchase

Wednesday, September 10,

2014

40

Leasing-Right to use

1. Transferee has the legal right to use the goods in his own

capacity

2. For the period of transfer such right to use is to the exclusion

of the transferor

….Owner can not transfer the same right to another person

3. Normally effective control and possession with the owner

Types of leases:

Operating leases: Normally no option to purchase the property

at the end of lease period

Financial leases: Option available to purchase

Wednesday, September 10,

2014

41

Leasing….

Aggarwal Brothers Vs State of Haryana and Another

[1999] 113 STC 317 (SC)-Hire of Shuttering Material- Transfer of

Right to Use

State of Andhra Pradesh and another Vs. Rashtriya Ispat Nigam Ltd.

[2002] 126 STC 114 (SC)- Effective Control with the owner-No

Transfer of Right to Use

20th Century Finance Corpn. Ltd. and Another Vs. State of

Maharashtra [2000] 119 STC 182 (SC)

Taxable event- Situs of Leasing- Place of execution of

Agreement/Contact-In case of existence of goods

Delivery of goods- In case of future goods/Oral Contact

Vitan Departmental Stores & Industries Limited Vs State of Tamil

Nadu [2014] 68 VST 70 (Mad)-Transfer of Right to use Names,

Marks, Systems, Insignia, Symbols and Goodwill-Exclusive right to

franchisee

Wednesday, September 10,

2014

42

Leasing….

Tata Consultancy Services Vs State of Andhra Pradesh

[2001] 122 STC 198 (SC) Transfer of Right to Use

goods— Software Programme-Branded/Unbranded-Ref to

larger Bench

Bharat Sanchar Nigam Ltd. Vs Union of India [2006] 3

VST 95 (SC)- No Tr of Right to Use-Electromagnetic

waves –Not goods

Indus Towers Ltd Vs DCCT-Enf-1, Bangalore [2012] 56

VST 369 (Karn DB)- No Transfer of Right to use, it is

only a licence to access the facility, Right to use of the

Passive Infrastructure.

Wednesday, September 10,

2014

43

Hire purchase

Possession is transferred (and not mere custody);

Hirer has the obligation to purchase the goods on

payment by installments

Mere hiring is not sale of goods

Wednesday, September 10,

2014

44

Case Laws- Bihar WCT

Supply & Execution of Power Supply System at a mine and Supply &

Erection of electrical equipment for a Plant- It is works contract and it

was not liable to sales tax under the CST Act, 1956 [1971] 27 STC

487 (Pat)

Jamshedpur Contractors' Association and Others Vs State of Bihar and

Others [1989] 75 STC 132 (Pat) – Works contract valid, Supply of

goods(N M Goel case) levy, Declared goods sec-14 of CST

Hindustan Dorr-Oliver Ltd. and Another Vs Union of India and Others

[1989] 75 STC 211 (Pat) . Once the sub contractor is assessed, same

turnover can not be assessed under Main Contractor( The goods in

question would be liable to sale tax only once-Property in goods passes

only once)

Wednesday, September 10,

2014

45

Case Laws- Bihar WCT

Builders Association of India and Others Vs State of Bihar and Others.

[1992] 85 STC 362 (Pat)- Provision for compulsory deduction of tax at

prescribed rate from bills and invoices raised by Contractor-Invalid-Sec

25A [ labour and CST transactions ? [2000] 117 STC 41 (Pat) L & T

Case

Beekay Engineering Corporation Vs State of Bihar [1992] 87 STC 509

(Pat) .works contractor can purchase goods against “C” form

Rungta Projects Limited and Another Vs State of Bihar and Others

[1998] 108 STC 234 (Pat) : Right to use- effective control &

Possession is required

Gammon India Limited Vs NTPC Limited and another [2009] 25 VST

77 (Pat)-Deduction of Tax on Labour charges-Not permissible-BVAT-

Sec 41 Rule 19

Amar Kumar Birley Vs State of Bihar and Others [2012] 48 VST 151

(Pat) – Job of taking photograph of customers-Not a works contract

Wednesday, September 10,

2014

46

Performance always comes from

passion and not from

pressure…..Always be passionate…..

Love what you do and do what you

love…..

Success is yours……..

47 9/10/2014

48

“Taxes shall be collected like honey bee collects honey from a flower”-

Chanakya 9/10/2014