Private Strategies Fostering Broadband in Italy - wik.org · Step1 ‐Download Step2 ‐Form for...

26

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010 Berlin April 26th 2010 Public Policies & Private Strategies Fostering Broadband in Italy 1

Transcript of Private Strategies Fostering Broadband in Italy - wik.org · Step1 ‐Download Step2 ‐Form for...

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

BerlinApril 26th 2010

Public Policies & Private Strategies Fostering Broadband in Italy

1

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

Agenda

The Italian Framework Broadband Drivers Public Policies & Private Strategies

2

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

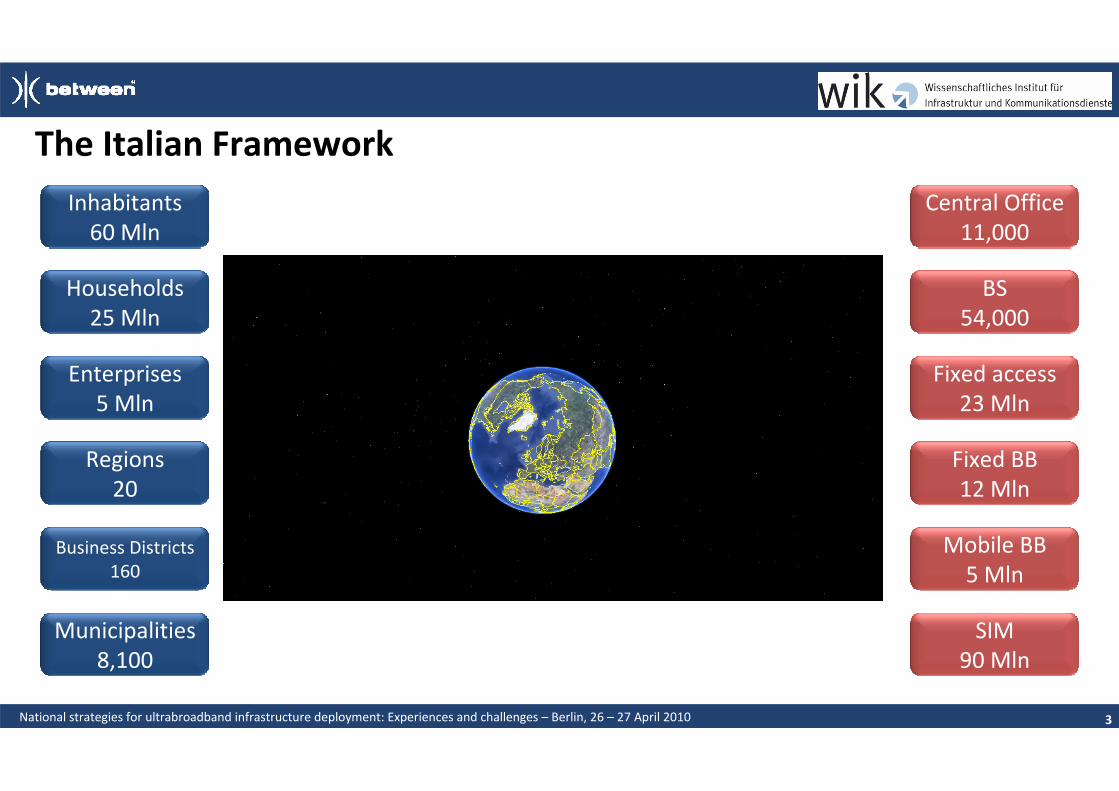

The Italian Framework

3

Inhabitants60 Mln

Households25 Mln

Enterprises5 Mln

Regions20

Business Districts160

Municipalities8,100

Central Office11,000

Fixed access23 Mln

Fixed BB12 Mln

Mobile BB5 Mln

SIM90 Mln

BS54,000

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

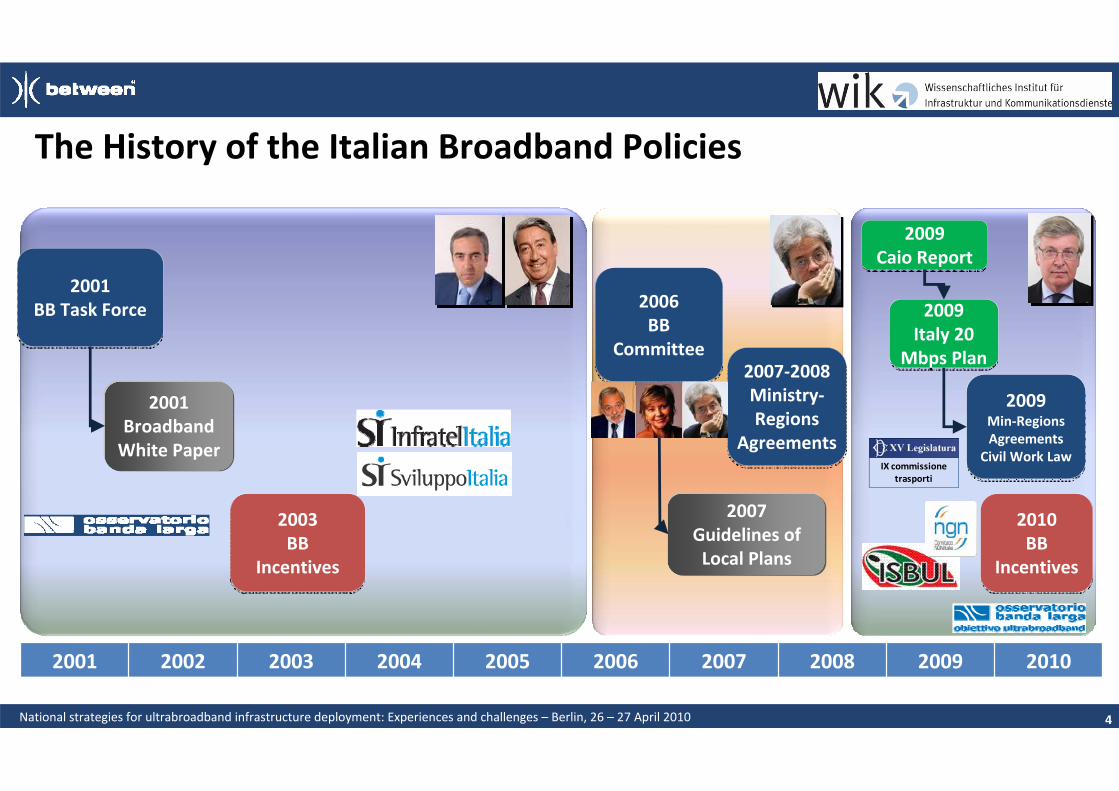

The History of the Italian Broadband Policies

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

4

2001BB Task Force

2001BB Task Force

2001BroadbandWhite Paper

2003BB

Incentives

2003BB

Incentives

2009Italy 20

Mbps Plan

2009Italy 20

Mbps Plan

2009Min‐Regions Agreements

Civil Work Law

2009Min‐Regions Agreements

Civil Work Law

2010BB

Incentives

2010BB

Incentives

2009Caio Report

2009Caio Report

IX commissione trasporti

2007Guidelines of Local Plans

2007‐2008Ministry‐Regions

Agreements

2007‐2008Ministry‐Regions

Agreements

2006BB

Committee

2006BB

Committee

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

Agenda

The Italian Framework Broadband Drivers Public Policies & Private Strategies

5

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

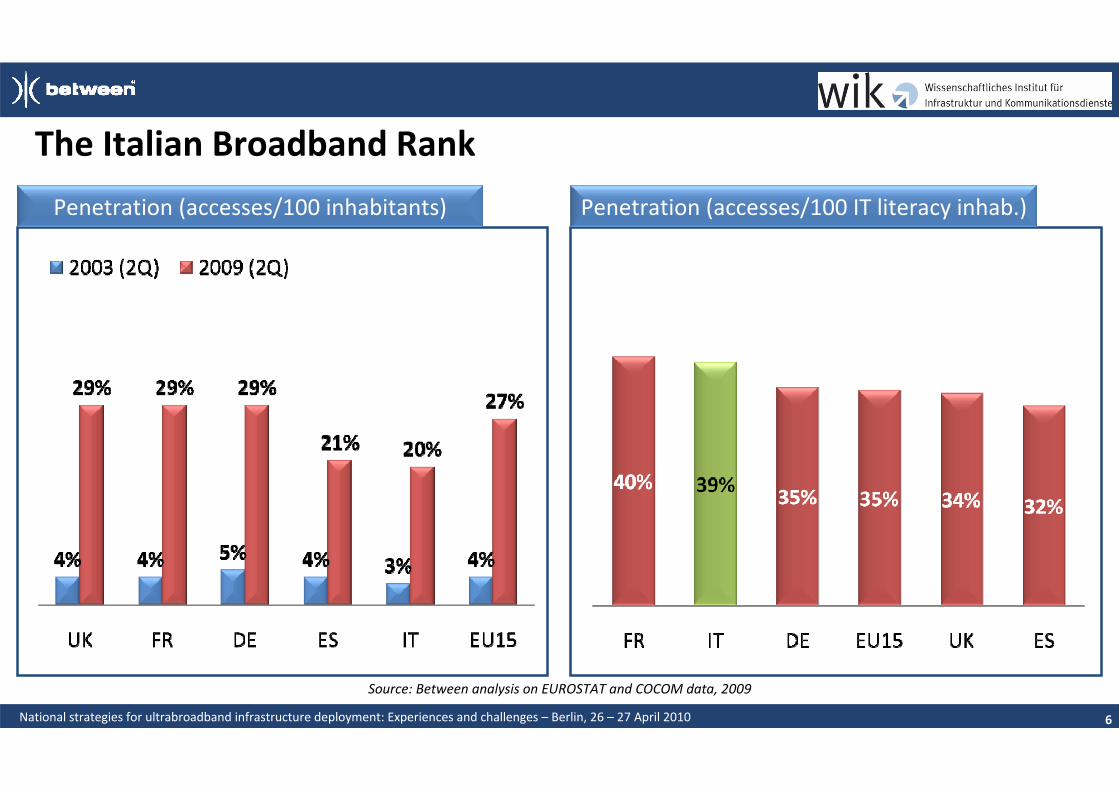

The Italian Broadband Rank

6

Penetration (accesses/100 IT literacy inhab.)Penetration (accesses/100 inhabitants)

Source: Between analysis on EUROSTAT and COCOM data, 2009

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

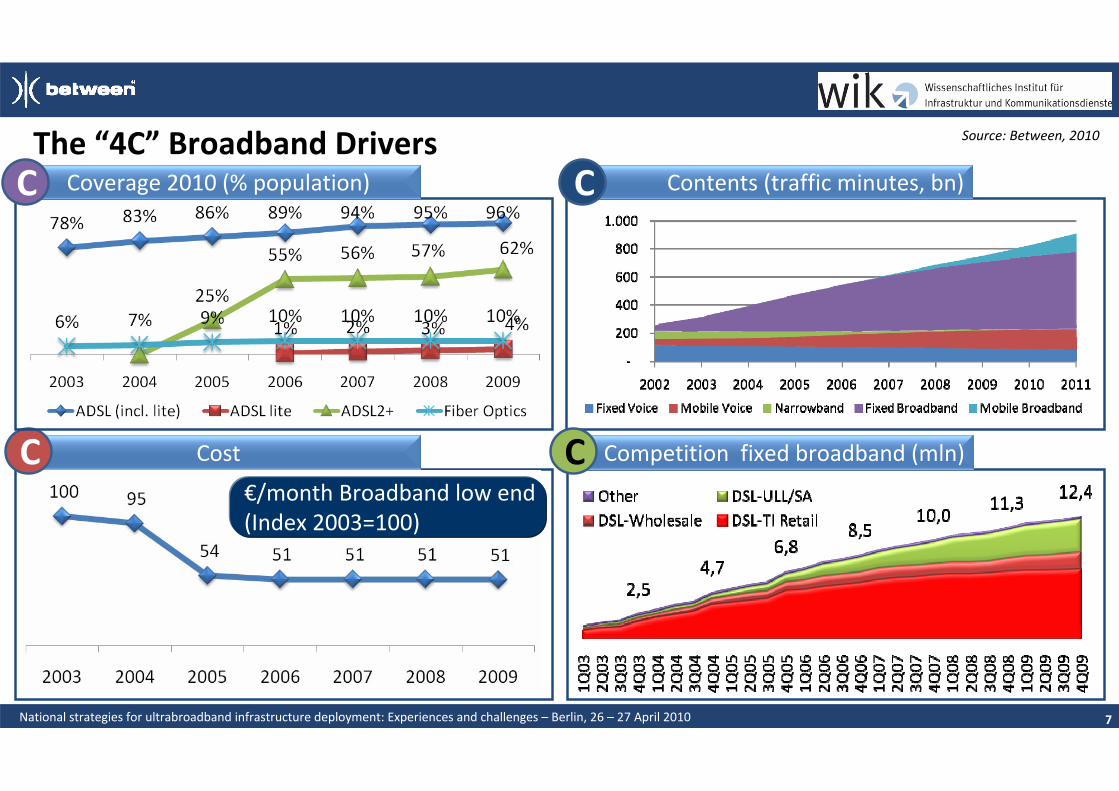

The “4C” Broadband Drivers

7

Source: Between, 2010

Cost

€/month Broadband low end(Index 2003=100)

C

Contents (traffic minutes, bn)C

Competition fixed broadband (mln)C

Coverage 2010 (% population)C

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

Focus on Coverage and Content Quality

8

The different variables should be addressed using specific tools

Network side

Customer side

C C

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

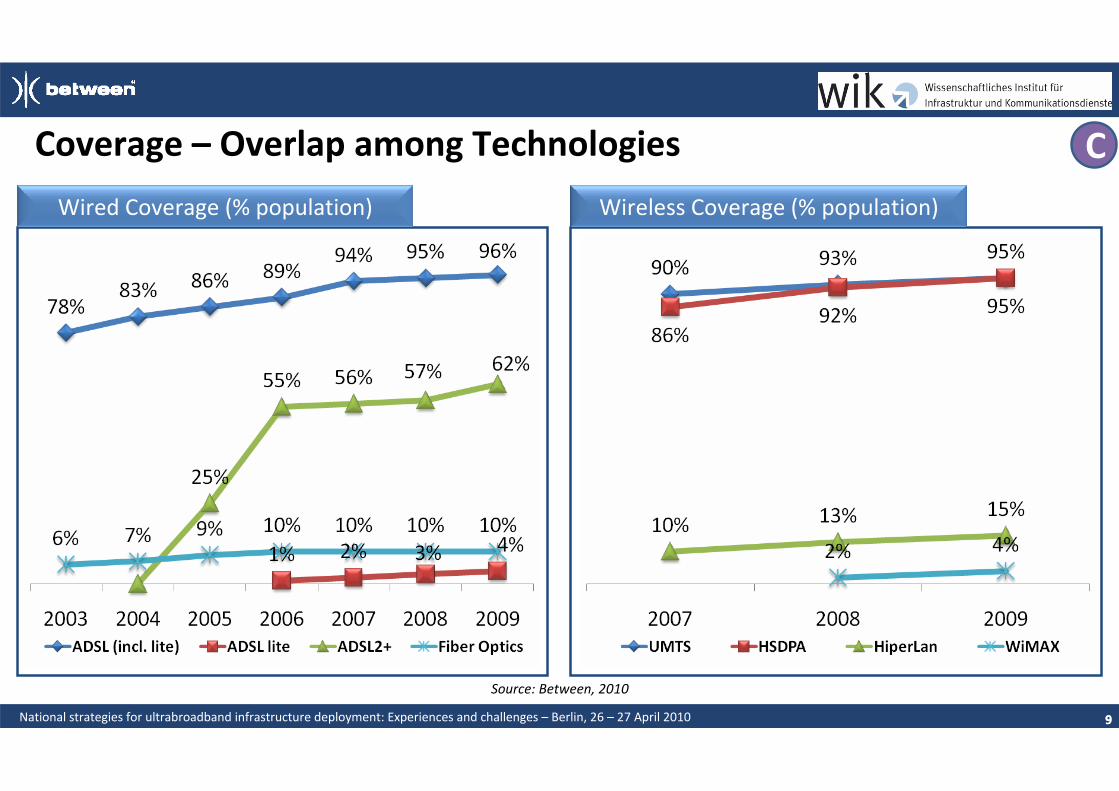

Coverage – Overlap among Technologies

Wireless Coverage (% population)Wired Coverage (% population)

Source: Between, 2010

99

C

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

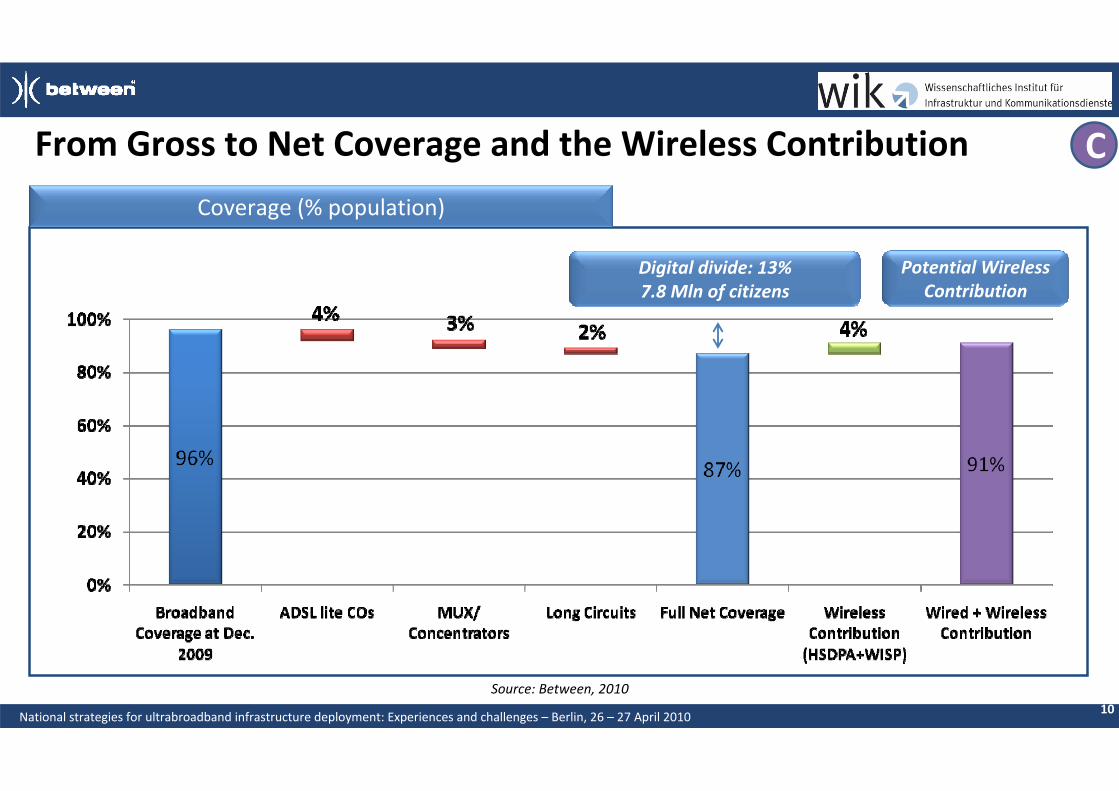

From Gross to Net Coverage and the Wireless Contribution

10

Coverage (% population)

Digital divide: 13%7.8 Mln of citizens

Potential Wireless Contribution

Source: Between, 2010

C

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

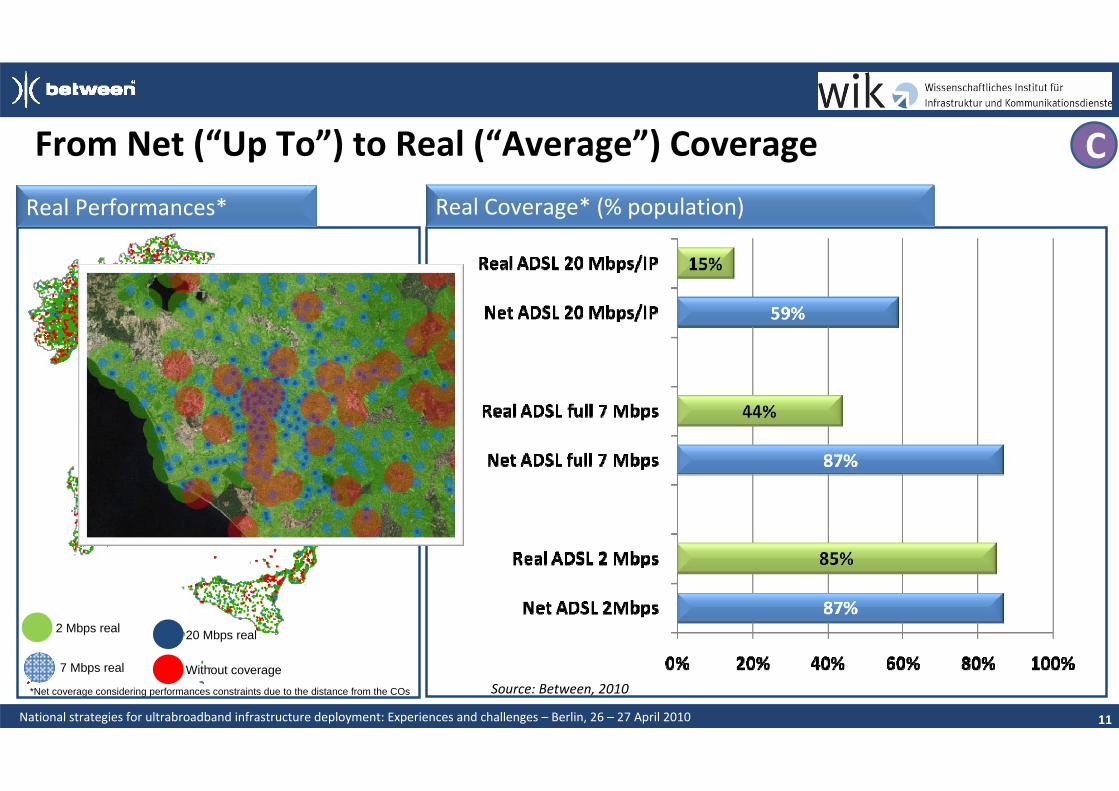

From Net (“Up To”) to Real (“Average”) Coverage

2 Mbps real

7 Mbps real Without coverage

*Net coverage considering performances constraints due to the distance from the COs

20 Mbps real

Real Performances* Real Coverage* (% population)

Source: Between, 2010

C

11

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

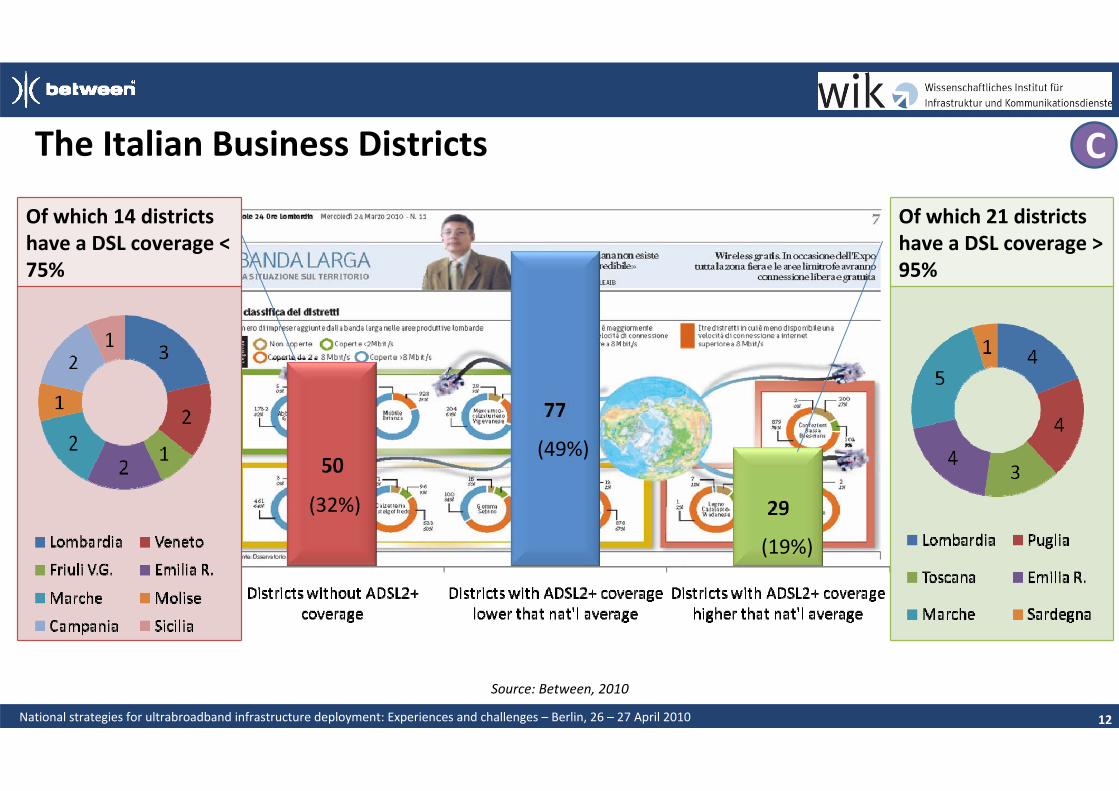

CThe Italian Business Districts

Of which 14 districts have a DSL coverage < 75%

Of which 21 districts have a DSL coverage > 95%

(32%)

(49%)

(19%)

12

Source: Between, 2010

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

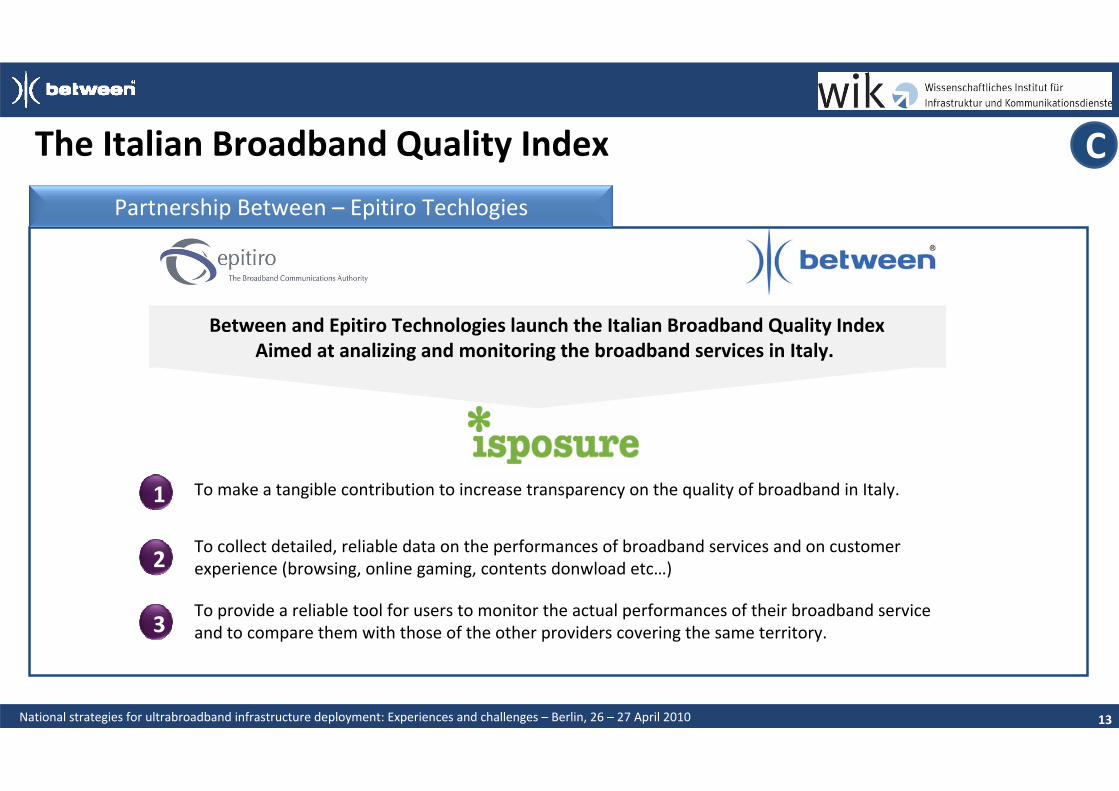

The Italian Broadband Quality Index

Between and Epitiro Technologies launch the Italian Broadband Quality IndexAimed at analizing and monitoring the broadband services in Italy.

To collect detailed, reliable data on the performances of broadband services and on customer experience (browsing, online gaming, contents donwload etc…)2

1 To make a tangible contribution to increase transparency on the quality of broadband in Italy.

To provide a reliable tool for users to monitor the actual performances of their broadband service and to compare them with those of the other providers covering the same territory.3

Partnership Between – Epitiro Techlogies

13

C

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

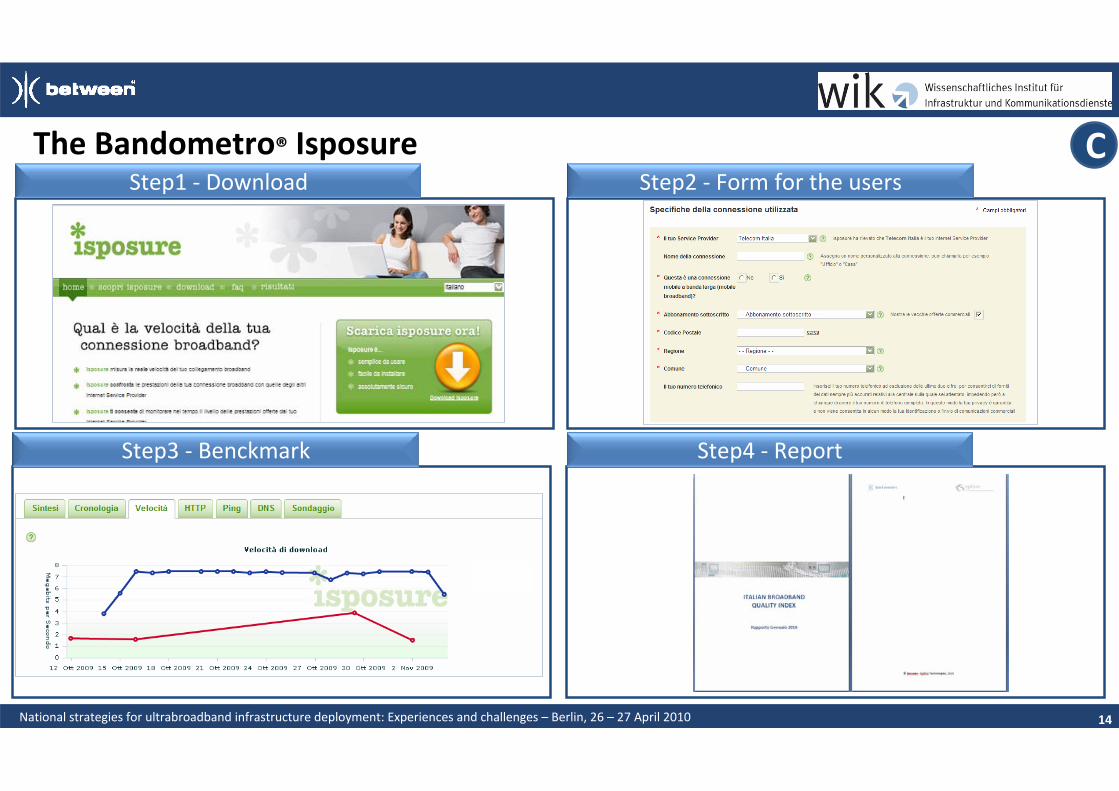

The Bandometro® Isposure

14

CStep1 ‐ Download Step2 ‐ Form for the users

Step4 ‐ ReportStep3 ‐ Benckmark

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

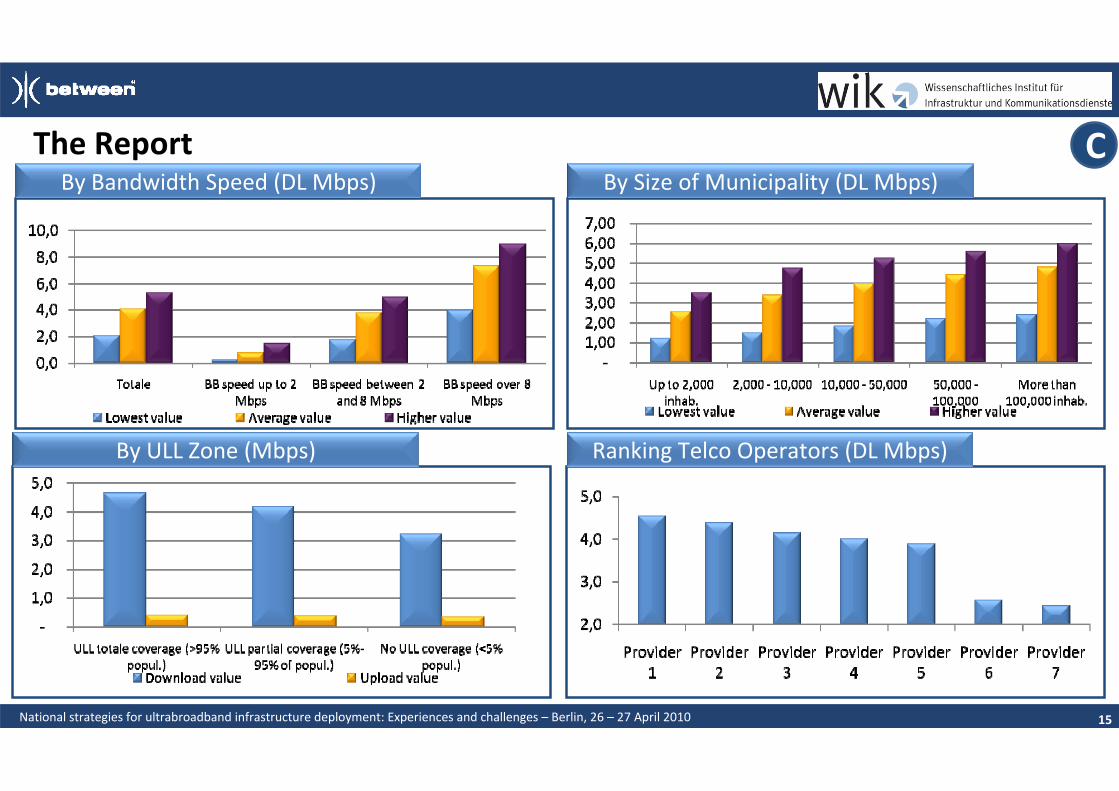

The Report

15

CBy Bandwidth Speed (DL Mbps) By Size of Municipality (DL Mbps)

By ULL Zone (Mbps) Ranking Telco Operators (DL Mbps)

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

Agenda

The Italian Framework Broadband Drivers Public Policies & Private Strategies

16

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

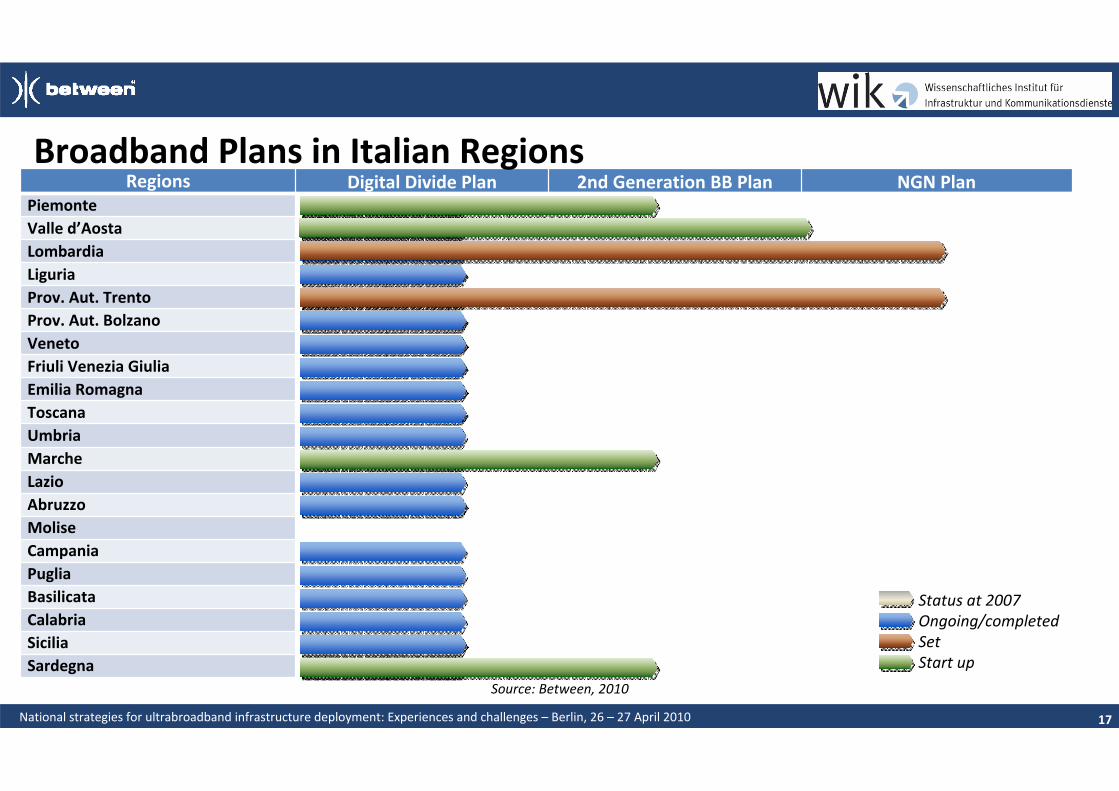

Regions Digital Divide Plan 2nd Generation BB Plan NGN PlanPiemonteValle d’AostaLombardiaLiguriaProv. Aut. TrentoProv. Aut. BolzanoVenetoFriuli Venezia GiuliaEmilia RomagnaToscanaUmbriaMarcheLazioAbruzzoMoliseCampaniaPugliaBasilicataCalabriaSiciliaSardegna

Broadband Plans in Italian Regions

Status at 2007Ongoing/completedSet Start up

Source: Between, 2010

17

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

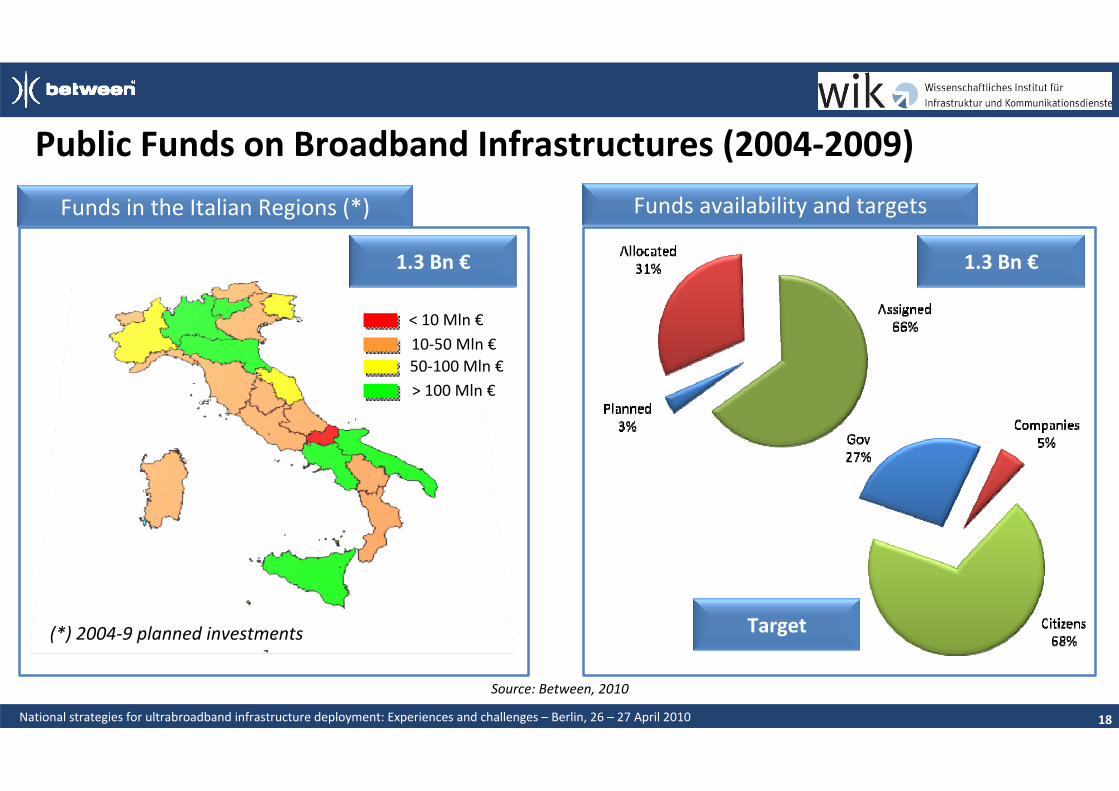

Public Funds on Broadband Infrastructures (2004‐2009)

(*) 2004‐9 planned investments

> 100 Mln €50‐100 Mln €10‐50 Mln €< 10 Mln €

1.3 Bn €

Funds in the Italian Regions (*) Funds availability and targets

Source: Between, 2010

1.3 Bn €

18

Target

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

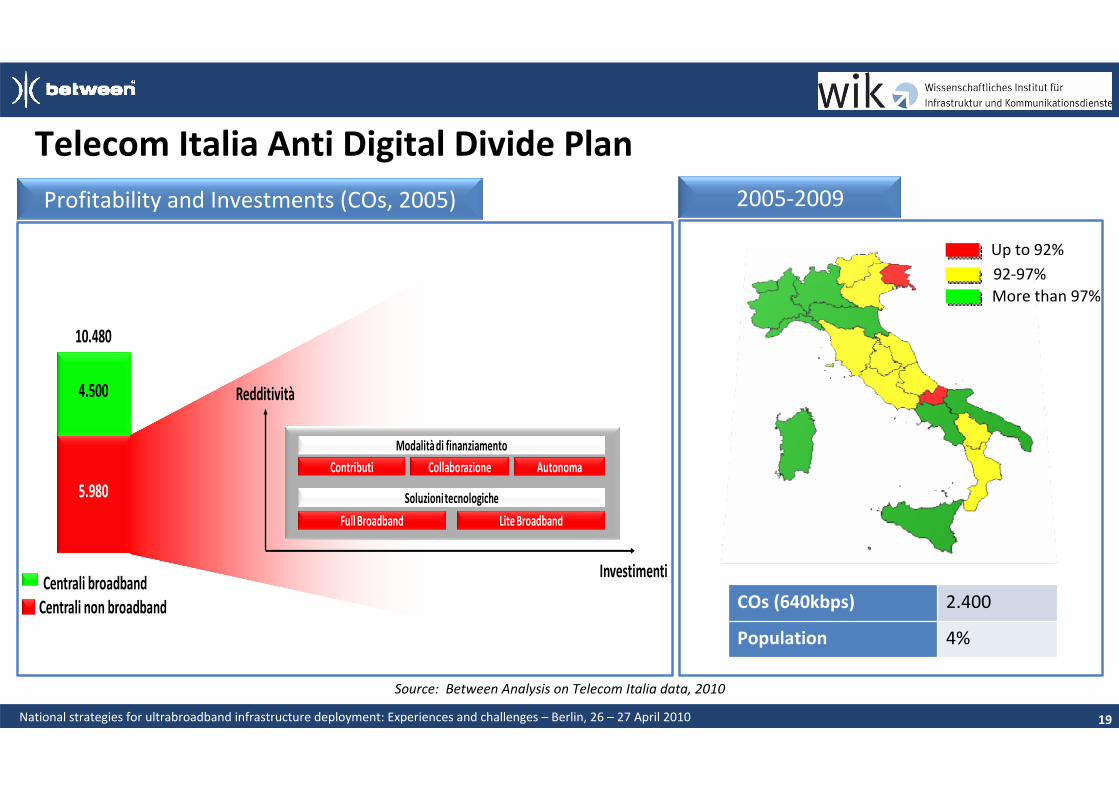

Telecom Italia Anti Digital Divide Plan

5.980

4.500

10.480

Investimenti

Lite Broadband

AutonomaCollaborazioneContributi

Full Broadband

Soluzioni tecnologiche

Modalità di finanziamento

Redditività

Centrali broadbandCentrali non broadband

2005‐2009

Source: Between Analysis on Telecom Italia data, 2010

COs (640kbps) 2.400

Population 4%

More than 97%92‐97%Up to 92%

Profitability and Investments (COs, 2005)

19

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

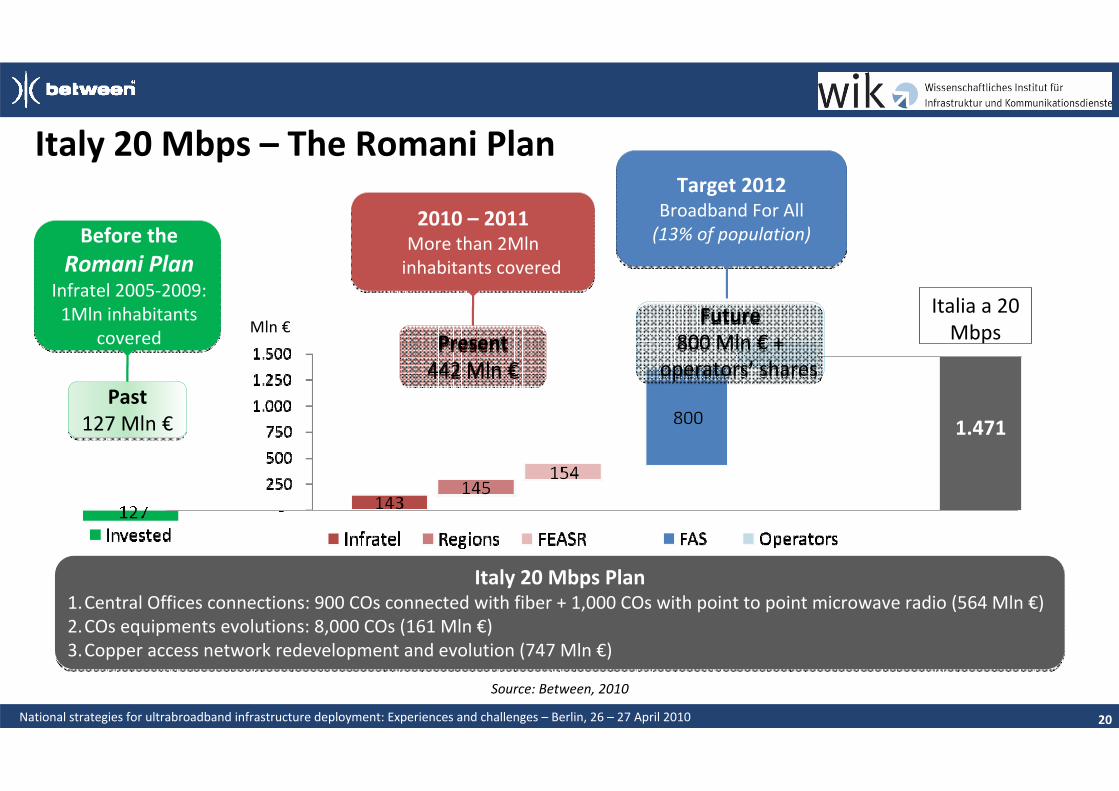

Italy 20 Mbps – The Romani Plan

1.471Past

127 Mln €Past

127 Mln €

Before the Romani Plan

Infratel 2005‐2009: 1Mln inhabitants

covered

Before the Romani Plan

Infratel 2005‐2009: 1Mln inhabitants

covered Present442 Mln €Present442 Mln €

2010 – 2011More than 2Mln inhabitants covered

2010 – 2011More than 2Mln inhabitants covered

Target 2012Broadband For All(13% of population)

Target 2012Broadband For All(13% of population)

Italia a 20 Mbps

Italy 20 Mbps Plan1.Central Offices connections: 900 COs connected with fiber + 1,000 COs with point to point microwave radio (564 Mln €)2.COs equipments evolutions: 8,000 COs (161 Mln €)3.Copper access network redevelopment and evolution (747 Mln €)

Italy 20 Mbps Plan1.Central Offices connections: 900 COs connected with fiber + 1,000 COs with point to point microwave radio (564 Mln €)2.COs equipments evolutions: 8,000 COs (161 Mln €)3.Copper access network redevelopment and evolution (747 Mln €)

Mln €

Source: Between, 2010

Future800 Mln € +

operators’ shares

Future800 Mln € +

operators’ shares

20

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

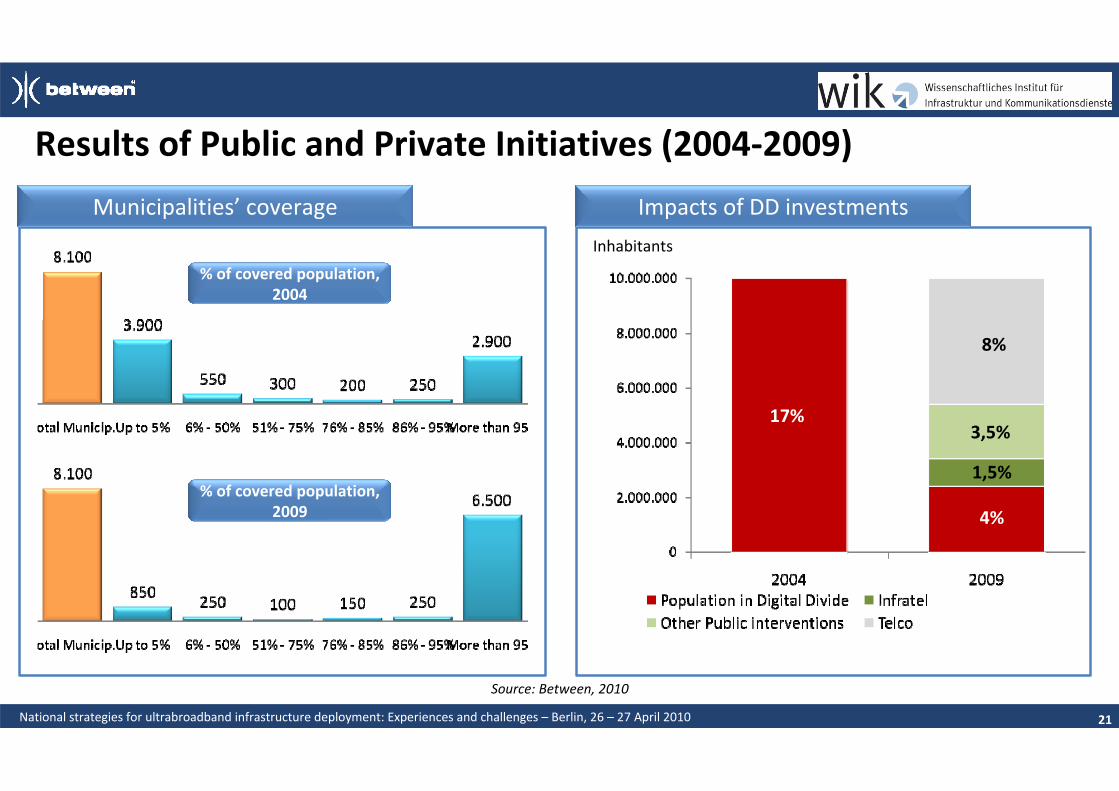

Results of Public and Private Initiatives (2004‐2009)

Municipalities’ coverage Impacts of DD investments

Source: Between, 2010

% of covered population, 2004

% of covered population, 2009

Inhabitants

1,5%

3,5%

4%

17%

8%

21

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

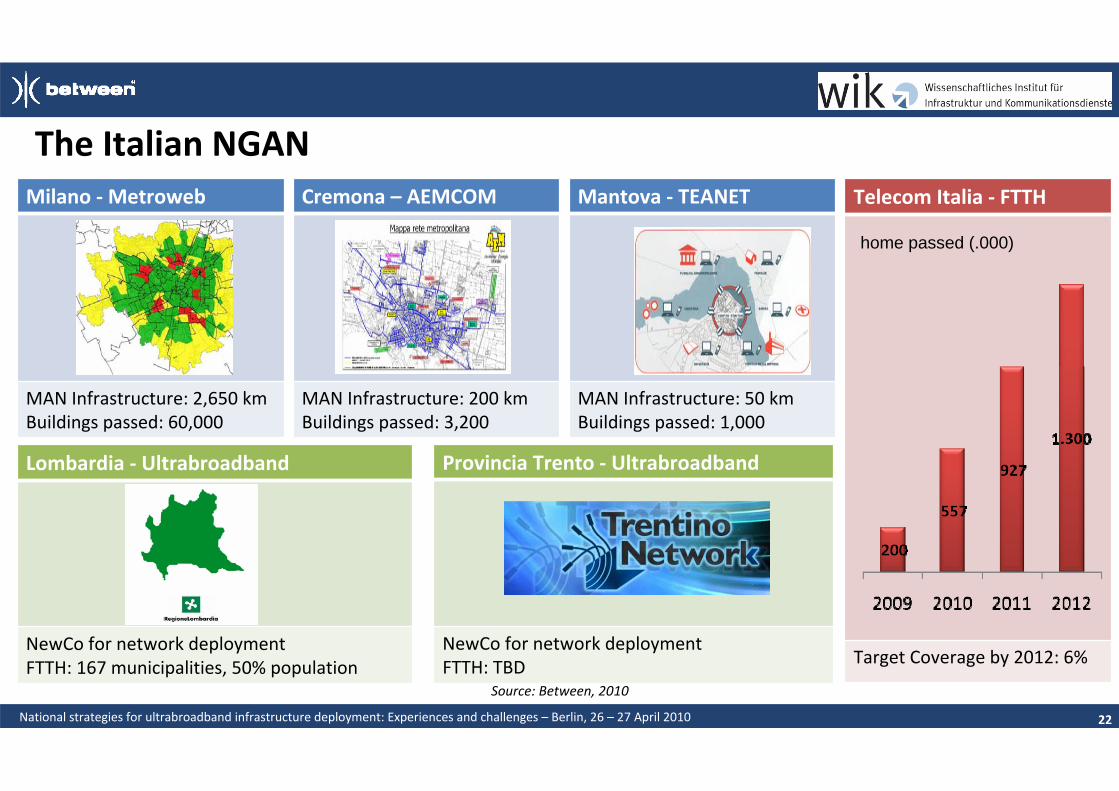

The Italian NGANMilano ‐Metroweb

MAN Infrastructure: 2,650 kmBuildings passed: 60,000

Cremona – AEMCOM

MAN Infrastructure: 200 kmBuildings passed: 3,200

Mantova ‐ TEANET

MAN Infrastructure: 50 kmBuildings passed: 1,000

Telecom Italia ‐ FTTH

Target Coverage by 2012: 6%

home passed (.000)

22

Source: Between, 2010

Lombardia ‐ Ultrabroadband

NewCo for network deploymentFTTH: 167 municipalities, 50% population

Provincia Trento ‐ Ultrabroadband

NewCo for network deploymentFTTH: TBD

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

Thanks

23

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

Thanks

24

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

Thanks

25

National strategies for ultrabroadband infrastructure deployment: Experiences and challenges – Berlin, 26 – 27 April 2010

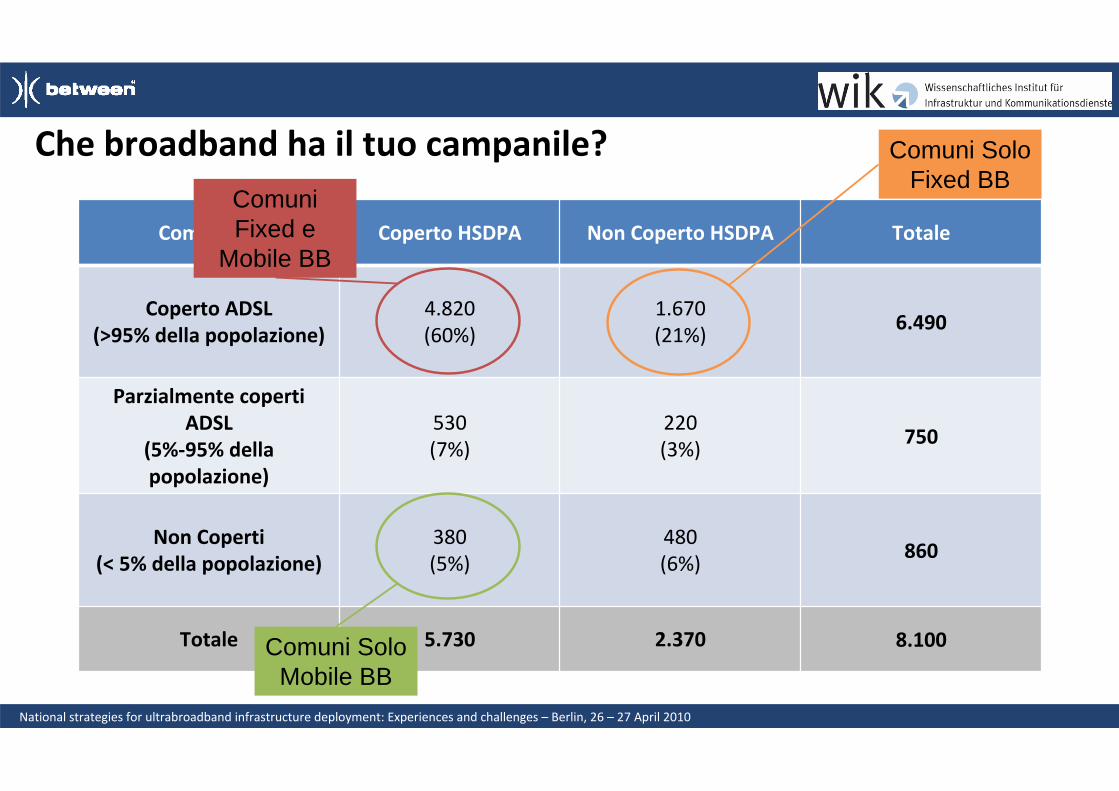

Che broadband ha il tuo campanile?

Comuni (#) Coperto HSDPA Non Coperto HSDPA Totale

Coperto ADSL(>95% della popolazione)

4.820(60%)

1.670(21%)

6.490

Parzialmente coperti ADSL

(5%‐95% della popolazione)

530(7%)

220(3%)

750

Non Coperti(< 5% della popolazione)

380(5%)

480(6%)

860

Totale 5.730 2.370 8.100

Comuni Solo Fixed BB

Comuni Solo Mobile BB

Comuni Fixed e

Mobile BB