Private pension schemes and their impacts on the public systems in the time of crisis The CMKOS –...

15

Private pension schemes and their impacts on the public systems in the time of crisis The CMKOS – FES Conference Prague 31st March 2011 The Destiny of Mandatory Pension Funds in Hungary

-

Upload

randolf-park -

Category

Documents

-

view

216 -

download

2

Transcript of Private pension schemes and their impacts on the public systems in the time of crisis The CMKOS –...

Private pension schemes and their impacts on the public systems in the time of crisis

The CMKOS – FES ConferencePrague 31st March 2011

The Destiny of Mandatory Pension Funds in Hungary

2

The Destiny of Mandatory Pension Funds in Hungary

The success story

How could things go wrong?

The rules of the new game

... and the changes

What is next?

3

The success story – Starting of the new system

The mandatory pension pillar was implemented in 1998 in the windfall of the recovery of the 1995 crisis

Established by parametric reforms, e.g. increase of retirement age

The Budget took on the liability to repay the mandatory pension fund contributions to the 1st pillar

The institution was similar to 3rd pillar pension funds, non-profit mutual funds

In practice there were two major types:

– Affiliate of a financial group

– Independent or employer/industry based

The difference is in governace

Original Law included provisions on – for example –

Annuitization and a minimum standard for the annuities

Pension Guarantee Fund

Investment return benchmarking

4

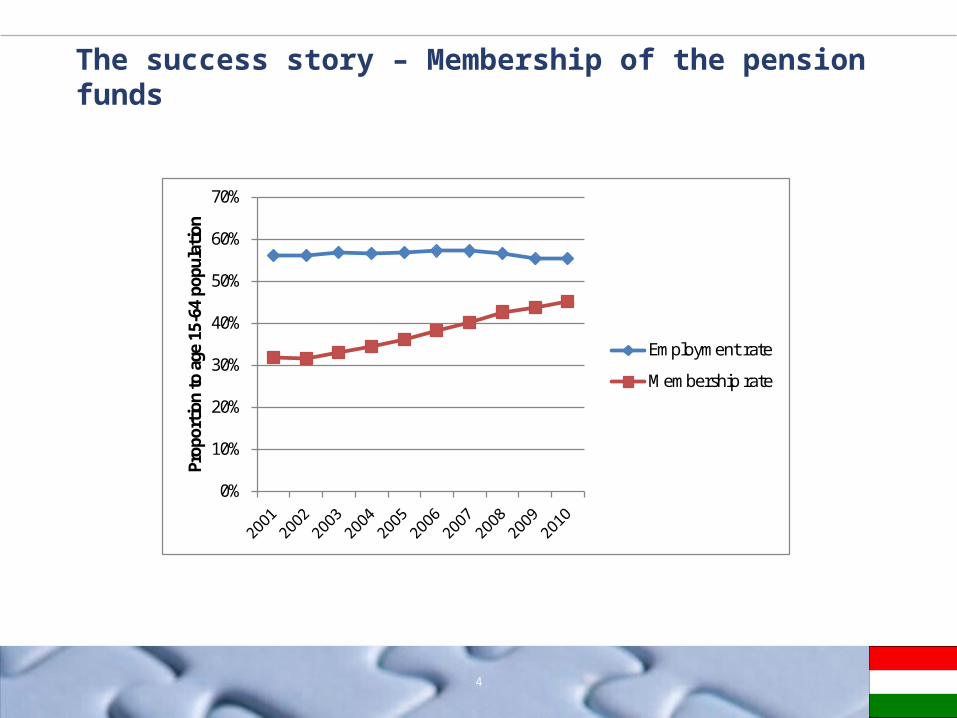

The success story – Membership of the pension funds

0%

10%

20%

30%

40%

50%

60%

70%Pr

opor

tion

to a

ge 1

5-64

pop

ulati

on

Employment rate

Membership rate

5

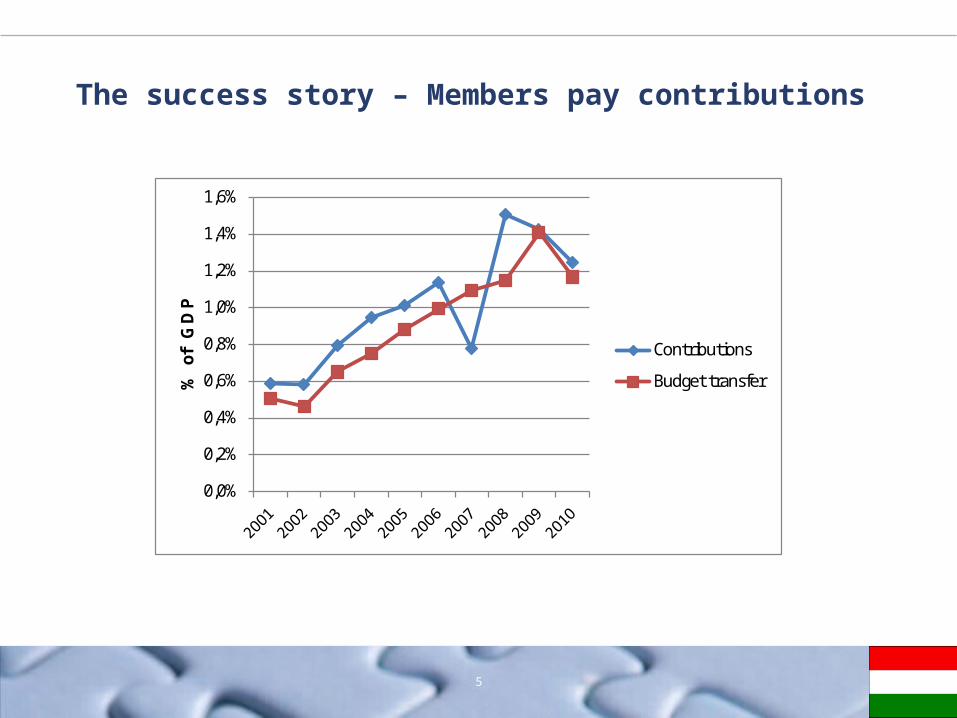

The success story – Members pay contributions

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

1,6%%

of

G

D P

Contributions

Budget transfer

6

The success story – Contributions are invested

Bank deposit1%

Debt securities4%

Government bonds47%

Equity10%

Investment funds35%

Other3%

7

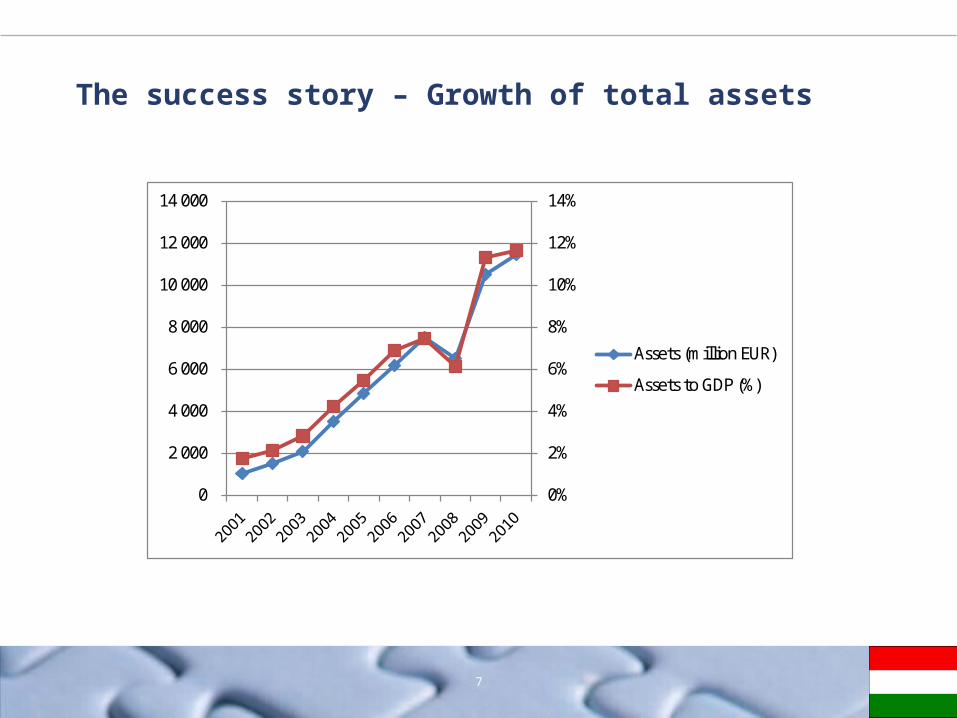

The success story – Growth of total assets

0%

2%

4%

6%

8%

10%

12%

14%

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

Assets (million EUR)

Assets to GDP (%)

8

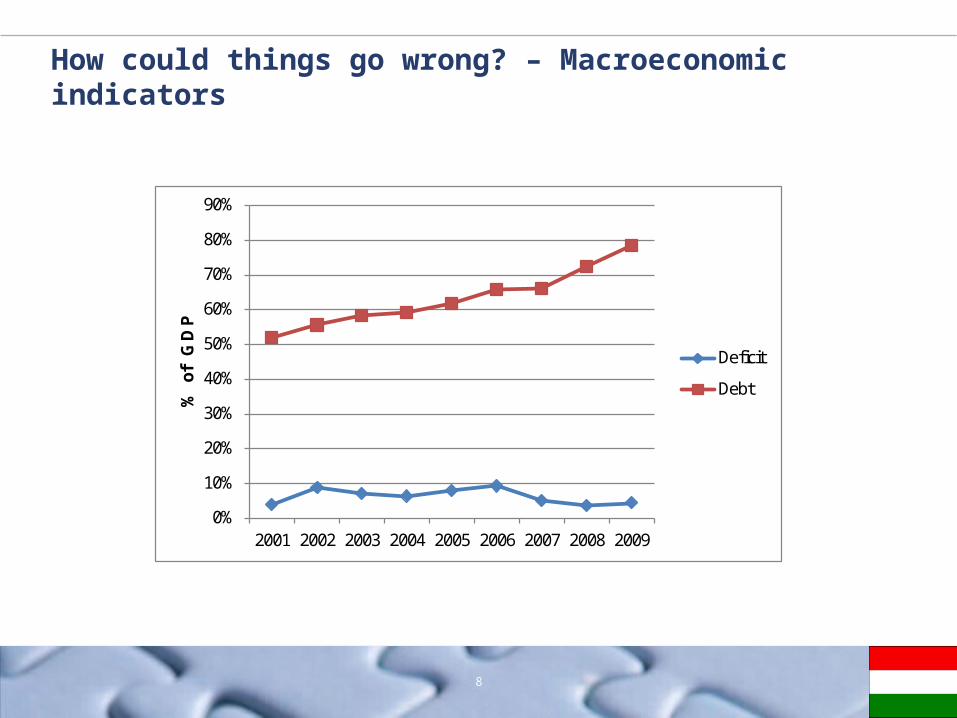

How could things go wrong? – Macroeconomic indicators

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2001 2002 2003 2004 2005 2006 2007 2008 2009

%

of

G D

P

Deficit

Debt

9

How could things go wrong? – Now see the elements together

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2004 2005 2006 2007 2008 2009 2010D

ebt a

nd T

otal

ass

ets

Defi

cit,

Budg

et tr

ansf

er, a

nd G

ov. B

ond

Government bonds toGDP

Total assets to GDP

Debt

Budget transfer

Deficit

10

How could things go even worse?

In 2005 the National Bank initiated discussion on the performance of the mandatory pension funds

The conclusions were that the mandatorty pension funds are

Expensive, and

Achieve low returns

And it was true for the pension funds that cover 80+ % of the membership – the financial groups’ pension funds

The consequence was a wave of new regulations in 2007/8:

Limits on fee deductions

Implementation of the investment portfolio choice (mult-funds)

Unit accounting (why?)

Discussions continued on two regulatory issues:

To change the institutional form to joint stock company

Uniform and detailed regulation of the pension fund annuities

A Law was passed in 2009, but suspended by the Constitutional Court

11

The rules of the new game

First crisis measures

Financial institutions and big corporations – telecoms, retail chains, energy sector companies – pay crisis tax for three years

Mandatory pension funds do not get the contributions until the end of 2011

The rules of contribution payment have changed

Only employee contributions generate rights

– Employee contributions are paid either into the 1st pillar – or completely to the mandatory pension fund [10%]

– Employer contributions will be used to finance the solidarity element of the 1st pillar [24%]

Consequence: Members of the mandatory pension funds shall not generate new accrued rights in the 1st pillar

12

The rules of the new game

Members of the mandatory pension funds were allowed to switch back to the 1st pillar

Their contributions will be transferred to a special fund in the form of assets

– only the contributions – the members may decide about the returns

The special fund is regulated in an Act, and will be

– managed by the Government

– used by definition to guarantee the solvency of the Budget and support the a new pension system

The big question: How many memebrs returned to the 1st pillar?

13

... and the changes

Pension FundYear-end

membershipStill members

Fidelity(%)

% of total

Aegon 602 017 16 889 2,81% 17,34%Allianz Hungaria 477 345 10 782 2,26% 11,07%Aranykor 72 165 3 090 4,28% 3,17%AXA 282 758 13 269 4,69% 13,62%Budapest (GE Money Bank) 30 441 2 680 8,80% 2,75%DIMENZIO 12 546 1 430 11,40% 1,47%Elettút Első Orszagos 2 427 154 6,35% 0,16%ERSTE 66 285 2 390 3,61% 2,45%Évgyűrűk 104 324 2 141 2,05% 2,20%GENERALI 76 156 2 166 2,84% 2,22%HONVED 23 728 609 2,57% 0,63%ING 523 767 19 197 3,67% 19,70%MKB 38 346 3 279 8,55% 3,37%OTP 756 021 17 641 2,33% 18,11%Postas 26 899 457 1,70% 0,47%Quaestor 6 709 170 2,53% 0,17%Vasutas 7 459 216 2,90% 0,22%VIT 8 807 862 9,79% 0,88%

Total 3 118 200 97 422 3,12% 100,00%

14

What is next?

There are other provisions in the new regulation and the in the policy statements

Limits on the operational expenses of the mandatory pension funds

Introduction of individual accounts in the 1st pillar

Strengthening of the voluntary pension funds

Were the mandadatory pension funds too successful?

What will happen to the members of the mandatory pension funds?