Private Equity in Africa

51

Private Equity in Africa April 2014 1

Transcript of Private Equity in Africa

Private Equity

in Africa

April 2014

1

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Conclusion

2

The Project

Maera Capital, an investment and advisory firm specialized in Africa and

with offices in London (UK) and Casablanca (Morocco), has asked a group

of five INSEAD MBA students (Astrid Suermondt, Francisco Meneses,

Helene Baudon, Jorge Fernández Vidal and Wafic Mounla) to assist them in

the analysis of the Private Equity market in Africa, as part of INSEAD’s

Private Equity class with Professor Vikas Aggarwal

In this project, we have tried to provide a brief overview of the Private Equity

market in Africa and have outlined a potential investment strategy for Maera

Capital

For this purpose, we have carried out extensive desk research and have

interviewed a number of PE practitioners in Africa, as well as consultants,

academics and operators during the months of March and April of 2014

3

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Conclusion

4

Africa is the fastest

growing continent

in the world, and its

increasing income

and population

create significant

opportunities for

investors

Sub-Saharan Africa has recently been one of the fastest growing

regions in the world and it is expected to continue the trend

Sub-Saharan countries

1.8951.292

731331

8977476571.016

211133

7028

2018 2013 2001 2006

GDP (current)

$ billion

Population

# billion

Fixed Investment

$ billion

Source: Global Insight

1.6281.4101.2181.032Real GDP per

capita

$

5

Institutional reforms and an increasing middle class are creating

opportunities for investment

“350 million Africans now earn between $2 and $20

per day and are increasing the ranks of Africa’s

middle class”

African Development Bank, Annual Development

Effectiveness 2013

“After years of headlines about Africa's poverty, its

emerging middle class is now grabbing attention as

a driver of growth and democracy and an

expanding pool of consumers for market-hungry

retailers”

Reuteurs, “Africa's emerging middle class drives

growth and democracy” - 2013, May 10

“More than two-thirds of African countries have

improved their quality of governance, leading to a

better business climate, improved basic services

and expanded economic opportunities”

African Development Bank, Annual Development

Effectiveness 2013

“These structural changes have helped invigorate

markets and commerce, creating an environment

that is increasingly conducive to business and

investment. Furthermore, widespread reform,

together with steady improvements in political

governance, the commodities boom, substantially

increased levels of disposable income, urbanization

and a rapidly developing services sector, have

contributed to a continued and, what we believe to

be, a sustainable growth path for Africa,

“Building Bridges - Africa” Ernst & Young’s 2012

attractiveness survey

6

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Conclusion

7

Private Equity is set to grow rapidly across Africa, but there are

some specific opportunities that should not be overlooked

Source: “Uncovering hidden investment opportunities in Africa”, McKinsey & Company

Demand for capital in

Africa is expected to grow

by 8% p.a. from 2014-

2018

There are wide variations

by country and industry

and there seems to be a

mismatch between supply

and demand for capital

Small and mid cap funds

in East, West and

Southern Africa

(excluding South Africa)

seem to be very

attractive, with growing

capital needs but relatively

limited funding

8

Most PE investors (+60%) focus on growth, infrastructure, buyout

and venture funds

Preferred investment strategies for PE funds in Africa in 2013

% # of respondents

1 Includes Co-Investment (4%), Early Stage (4%), Mezzanine (2%) and Infrastructure Fund of Funds (2%)

Source: “How do private equity investors create value”, 2013 Study, EY and AVCA

Growth 21%

Infrastructure 16%

Buyout 12%

Venture 11%

Fund of Funds 10%

Expansion / late stage

7%

Natural Resources

7%

Real Estate 6%

Other1 12%

9

Most deals are achieved via relationship or network, and funds

typically take a minority stake

Source: “How do private equity investors create value”, 2013 Study, EY and AVCA

Sourcing of deals Participation on deals

9% of deals made through auctions (vs.

proprietary deals)

80% of auctions took place in South Africa,

but number is increasing in other countries

as well

Majority

stake

20% Minority

stake

80%

Use of minority protection rights to influence

management and direction of a company, :

Board seats

Veto rights on major decisions

Right to change management

Right to change auditor

Importance of being comfortable with existing

management team:

Prior relationship with management team

helps

Due diligence of management is critical

Relation-ship /

Network 48%

Sector tracking

33%

Opportu-nities

brought to PE 14%

Other 5%

10

% # of deals % # of deals

Southern Africa as a region, and the financial and industrial goods

sectors have the highest share of exits in Africa

Source: “How do private equity investors create value”, 2013 Study, EY and AVCA

Geography breakdown Sector breakdown

11%

11%

42%

25%

11%

118 exits between 2007 and 2012

South Africa, Nigeria, Egypt, Kenya

and Ghana accounted for 74% of the

exits

23% Financials

13% Industrial goods

9% Food & beverage

9% Agriculture

Utilities, oil & gas

Travel & leisure

2%

1%

3%

3% Mining & metals

Media

Autimobile & parts

3%

Health care

Business services

Construction

6%

Retail & consumer goods

8%

6%

Telecommunications

4%

5%

Technology

8%

11

% # of deals % # of deals

Local and regional strategic buyers are responsible for the

majority of purchases from PE funds

Source: “How do private equity investors create value”, 2013 Study, EY and AVCA

Exit route

23%

32%

18%

14%

52%

14%

29%

55%

21%

47%

63%11%

12%

7%

8%

11%

12%

12%

11%

12%

7%

12% 12%

51%

41%

2007

2009

2008

4% 2011

2010

2012

4%

5%

Trade

Private

Stock sale on public market

IPO

Creditors / banks PE

Breakdown of exits by trade buyer

50% 40%

40%

33%40% 33%40% 33%

20% 25%

20m-50m 0m-5m 5m-20m

25%

20%

50m+

Local buyer

Multinational buyer

Regional buyer

Average exit returns and drivers

1,90,9

1,0

PE return Market

return

Strategic &

operational

improvements

12

% # of deals % # of deals

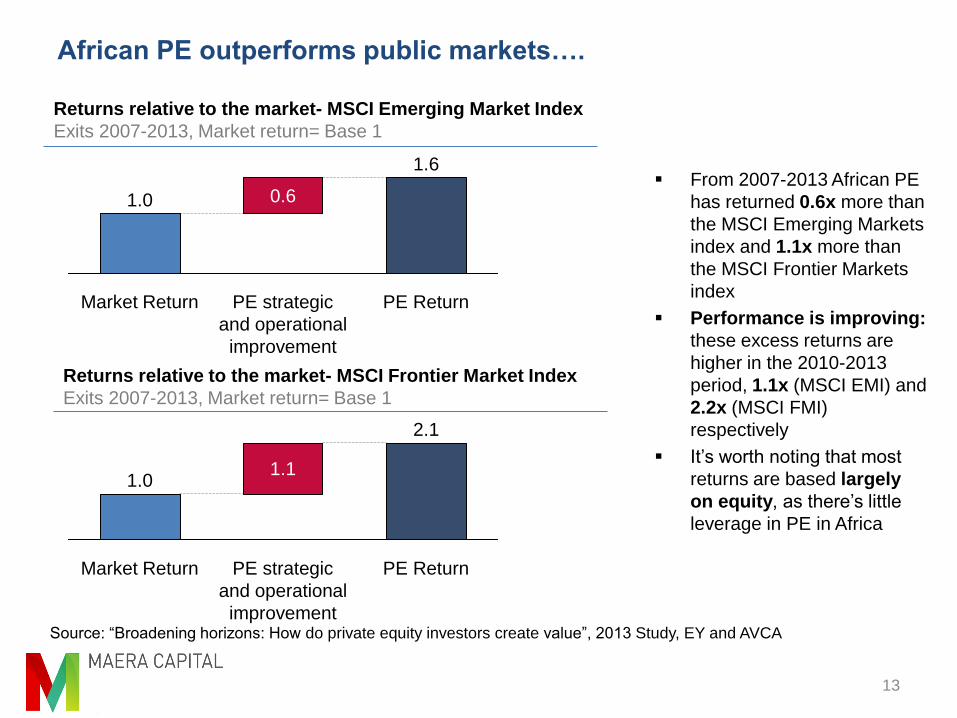

African PE outperforms public markets….

13

0.6

PE Return

1.0

Market Return

1.6

PE strategic

and operational

improvement

Source: “Broadening horizons: How do private equity investors create value”, 2013 Study, EY and AVCA

2.1

PE strategic

and operational

improvement

PE Return

1.1

Market Return

1.0

Returns relative to the market- MSCI Emerging Market Index

Exits 2007-2013, Market return= Base 1

Returns relative to the market- MSCI Frontier Market Index

Exits 2007-2013, Market return= Base 1

From 2007-2013 African PE

has returned 0.6x more than

the MSCI Emerging Markets

index and 1.1x more than

the MSCI Frontier Markets

index

Performance is improving:

these excess returns are

higher in the 2010-2013

period, 1.1x (MSCI EMI) and

2.2x (MSCI FMI)

respectively

It’s worth noting that most

returns are based largely

on equity, as there’s little

leverage in PE in Africa

…as well as more established PE markets

14

1.04 1.00

Africa North America

1.20

Europe

Relative multiples, Africa versus Europe and North America

Exits 2010-2012, North America= Base 1

Source: “Broadening horizons: How do private equity investors create value”, 2013 Study, EY and AVCA; Team interviews

Exit multiples in Africa are

higher than those of other

established markets in

Europe and North America

(by as much as one-fifth)

The higher multiples are

explained by the positive

outlook in the continent

Although PE returns in

Africa are higher (~15%-

~+30% depending on fund,

sector and geographies),

they are also

commensurate with the

higher risk of investing in

Africa

Successful PE deals in Africa seem to share some common traits

15

Case Study 1: Compagnie de Distribution de Côte d’Ivoire (CDCI)

Case Study 2: Vitalait

Case Study 3: Southey Holdings

Case Study 4: Société Internationale de Plantations d’Hévéas

Case Study 5: ABC Transport

Selected case studies

Introduction of best-practices in a wide number of areas (finance, IT,

governance, operations, etc)

Strengthening of management teams (new hires, incentive programs, etc)

Focus on growth (increase in product offerings, expansion into new

markets, etc)

EBITDA improvements (cost reduction, focus on high-margin products, etc)

Leverage the PE investor’s networks and know-how to identify new

customers, acquisition targets and potential buyers

How PE firms create value in Africa

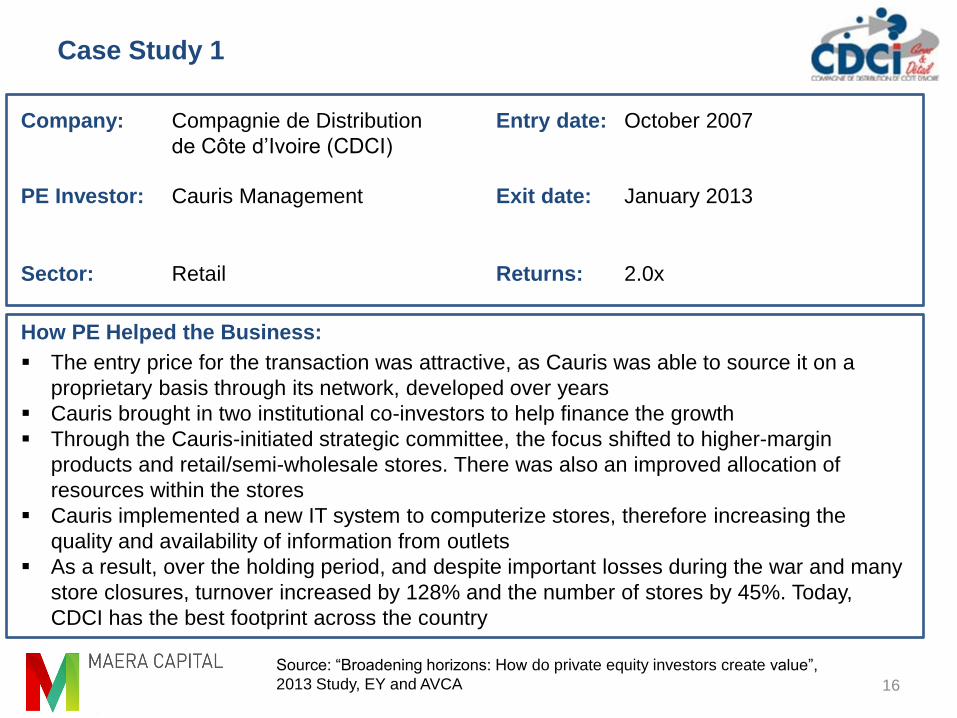

Case Study 1

16

Company:

PE Investor:

Sector:

Entry date:

Exit date:

How PE Helped the Business:

Compagnie de Distribution

de Côte d’Ivoire (CDCI)

Cauris Management

Retail

October 2007

January 2013

2.0x Returns:

The entry price for the transaction was attractive, as Cauris was able to source it on a

proprietary basis through its network, developed over years

Cauris brought in two institutional co-investors to help finance the growth

Through the Cauris-initiated strategic committee, the focus shifted to higher-margin

products and retail/semi-wholesale stores. There was also an improved allocation of

resources within the stores

Cauris implemented a new IT system to computerize stores, therefore increasing the

quality and availability of information from outlets

As a result, over the holding period, and despite important losses during the war and many

store closures, turnover increased by 128% and the number of stores by 45%. Today,

CDCI has the best footprint across the country

Source: “Broadening horizons: How do private equity investors create value”,

2013 Study, EY and AVCA

Case Study 2

17

Company:

PE Investor:

Sector:

Entry date:

Exit date:

How PE Helped the Business:

Vitalait

AfricInvest Fund I and Maghreb

Private Equity Fund II

Agribusiness, dairy products

September 2006

December 2011

2.2x Returns:

Improved governance and reinforced the management team

Created a strong local brand and diversified the product range from one SKU in milk to a

wider milk and fresh dairy products

Put in place a long environmental and social program reducing waste and improving the

waste management process

Put in place a large farmers’ empowerment program (the company buys milk from more

than 5,000 families)

Source: “Broadening horizons: How do private equity investors create value”,

2013 Study, EY and AVCA

Case Study 3

18

Company:

PE Investor:

Sector:

Entry date:

Exit date:

How PE Helped the Business:

Southey Holdings

The Abraaj Group

Industrials

July 2009

May 2013

48% (IRR) Returns:

Southey consolidated its business operations in South Africa and focused on new markets

in Africa. Under Abraaj’s guidance, the company expanded into seven new country

markets to a position where 40% of the Group’s profits were generated from markets

outside of South Africa at the time of Abraaj’s exit

With Abraaj’s involvement, Southey created a sustainable business model by

strengthening governance, including establishing a compensation committee, restructuring

the business to better leverage African growth opportunities, implementing a

comprehensive management information system, improving growth in terms of service and

geography, and introducing new marketing strategies

Abraaj’s established an employee share trust to promote broad-based equity ownership

and to further enable the institutionalization of this family business

Source: “Broadening horizons: How do private equity investors create value”,

2013 Study, EY and AVCA

Case Study 4

19

Company:

PE Investor:

Sector:

Entry date:

Exit date:

How PE Helped the Business:

Société Internationale

de Plantations d’Hévéas

Emerging Capital Partners (ECP)

Agriculture/forestry

March 2005

July 2007

3.4x Returns:

ECP’s investment allowed the company to expand production and implement cutting-edge

techniques. The funding, combined with ECP’s support in establishing the right

partnerships and management team, resulted in revenue growth of 44 % annually over

ECP’s two-year holding period

ECP helped the company to become more attractive to investors by implementing

standard financial reporting and identifying appropriate acquisition targets

In 2006, ECP played an instrumental role in negotiating the acquisition of Michelin’s rubber

plantations in Nigeria in exchange for a 20% stake in SIPH

Source: “Harvesting growth: How do private equity investors create value”,

2013 Study, EY and AVCA

Case Study 5

20

Company:

PE Investor:

Sector:

Entry date:

Exit date:

How PE Helped the Business:

ABC Transport

African Capital Alliance (ACA)

Transportation

August 2003

February 2008

4.7x Returns:

ACA helped improve corporate governance and financial reporting and also assisted with

recruiting senior management

ACA introduced some key corporate customers

ACA worked with management on expansion of the company’s operations beyond Nigeria

further into West Africa

ACA worked with management to prepare the company for and ensure a successful listing

on the Nigerian Stock Exchange

Source: “Harvesting growth: How do private equity investors create value”,

2013 Study, EY and AVCA

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Recommended Geographical Focus

▪ Recommended Sectorial Focus

▪ Potential Investment Vehicles

▪ Conclusion

21

We propose to use a broad and flexible investment strategy

Details of investment strategy

Geographic

Focus

Focus on a number of selected countries that have promising economic fundamentals

and an adequate investment environment (i.e. Transition countries)

Diversify geographical reach, but limited to a number of countries to build strong local

networks and knowledge

Sectorial

Focus

Investment

vehicle

Target a broad range of diverse sectors to take advantage of upcoming opportunities and

untapped markets

Focus on one of Africa’s biggest opportunities: the emerging consumer; around a wide

range of sectors (e.g. pharmaceuticals, food and beverages, textiles, etc)

Tap into these opportunities by investing in businesses with manufacturing operations

targeting emerging consumers

Choose the investment vehicle that better suits our investors’ needs and preferences (to

be discussed with investors)

Simplify initial investment strategy by operating on a deal-by-deal basis, with a view of

creating a fund or dedicated investment firm in the future (potentially covering both debt

and equity investments)

22

Deal Size

Target small and mid transactions (€5-€30m) are the most underserved markets for a

new investment manager (i.e. supply and demand mismatch; page #9)

Remain flexible to invest or co-invest in larger transactions on a case-by-case basis

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Recommended Geographical Focus

▪ Selected Opportunities by Sector

▪ Potential Investment Vehicles

▪ Conclusion

23

We have defined 3 criteria to identify African economies with high

potential

Analysis of countries

according to exports per

capita and economic

diversification

We follow McKinsey’s approach in the report “Lions on the move” (with

updated data), where countries are distributed in homogeneous groups

according to exports per capita and economic diversification (share of

manufacturing and services in GDP)

Studies show these variables are correlated with economic growth:

Countries need to export to fund investments (including imports) in a

sustainable manner

Manufacturing and services sector expand as urbanization increases and

as middle class rises, creating opportunities for investments in different

areas

Countries in transition (with increasing exports and economic diversification)

are the ones with better prospects for investment

1

2014 Index of

Economic Freedom by

the Heritage Foundation

We consider that certain countries lack a conducive business, legal and

political environment for investment

We look at the 2014 Index of Economic Freedom by the Heritage Foundation

and exclude countries with an index below 50 (i.e. repressive)

2 Individual reports /

interviews

We believe economic data in Africa is not fully reliable so we consider a

number of countries that according to studies and interviews appear to be

attractive investment destinations, at least in selected sectors 3

Criteria Rationale

Source: Team Analysis

24

The first analysis allows us to clearly split countries into 4

categories Exports per capita vs. Share of Manufacturing and Services in GDP; Size of

bubbles proportional to GDP

10

100

1.000

10.000

75 90 65 85 0 25 30 70 35 40 45 50 55 60 80

Exports per capita ($)

20121

Namibia

South Africa Tunisia

Morocco

Botswana

Mauritius

Rwanda Sudan

Burkina Faso Mali

Cameroon

Cote d’Ivoire

Liberia

Ghana Nigeria

Libya Gabon

Equatorial Guinea

Congo, Rep.

Chad

Angola

Algeria

Ethiopia

Kenya Mozambique

Senegal

Share of Manufacturing and Services in GDP (%)

20121

Egypt, Arab Rep. Zambia

Uganda Tanzania Congo, Dem. Rep.

1 When data for 2012 was not available, previous period were used (see backup)

Note: Included countries with GDP in 2012 above $10 billion or GDP growth rate 2005-2012 above 7%

Source: World Bank Economic Development Indicators; www.econstats.com; “Lions on the Move (Africa), McKinsey Global Institute”

Transition economies

Pre-transition economies

Diversified economies

Oil exporters

25

Some African countries have “Repressed Economies”

according to the IEF

Mauritius

Botswana

Cape Verde

Rwanda

Ghana

South Africa

Madagascar

Swaziland

Zambia

Uganda

Gambia

Namibia

Burkina Faso

Morocco

Gabon

Tanzania

Côte d'Ivoire

77

72

66

65

64

62

62

61

60

60

60

59

59

58

58

58

58

8

27

60

65

66

75

79

82

88

91

92

94

98

103

105

106

107

Country Score

World

rank

Tunisia

Kenya

Benin

Seychelles

Djibouti

Mali

Malawi

Senegal

Niger

Mozambique

Nigeria

Guinea

Mauritania

Egypt

Cameroon

Liberia

Burundi

57

57

57

56

56

56

55

55

55

55

54

54

53

53

53

52

51

109

111

113

117

118

122

124

125

127

128

129

133

134

135

136

138

141

Country Score

World

rank

Comoros

Guinea-Bissau

Algeria

Sierra Leone

Ethiopia

Togo

Lesotho

São Tomé and Príncipe

Angola

Central African Republic

Chad

Equatorial Guinea

Congo, Republic of

Congo, Dem. Republic

Eritrea

Zimbabwe

51

51

51

51

50

50

49

49

48

47

45

44

44

41

38

36

142

143

146

148

151

152

154

157

160

161

167

168

169

172

174

176

Country Score

World

rank

Note: The Index is computed as a simple average of scores on Property Rights, Freedom from Corruption, Fiscal Freedom, Government

Spending, Business Freedom, Labor Freedom, Monetary Freedom, Trade Freedom, Investment Freedom and Financial Freedom

Source: 2014 Index of Economic Freedom by the Heritage Foundation

According to the Heritage Foundation an

Index below 50 represents a “Repressed

Economy”

26

According to our pre-defined criteria, we have identified 8

countries with high potential for investment

6 transition economies…

Kenya

Ghana

Tanzania

Cameroon

Senegal

Mozambique

… and 2 economies commonly perceived today as being attractive investment destinations

Nigeria Ethiopia

Oil exporter country

with high level of

exports per capita

and currently making

a significant effort to

diversify its economy

Pre-transition

economy which is

seen today as one of

the most promising

economies in Sub-

Saharan Africa

Source: Press Research; Team Interviews; Team Analysis

27

The countries we have selected have shown consistent growth of

GDP and population (1/2)

Kenya

Ghana

Tanzania

Cameroon

2619

+5%

1811

+8%

2214

+7%

2117

2005 2012

+3%

43 36

+3%

25 21

+2%

4839

+3%

2218

2005 2012

+3%

595524

+2%

724502

+5%

483375

+4%

964915

2005 2012

+1%

Real GDP

$ billions

Population

Millions

Real GDP per capita

$

Source: World Bank Economic Development Indicators; www.econstats.com

CAGR 2005-2012

28

Senegal

Mozambique

Nigeria

Ethiopia

The countries we have selected have shown consistent growth

of GDP and population (2/2)

119

+3%

117

+7%

178112

+7%

2312

+10%

2012 2005

1411

+3%

2521

+3%

169140

+3%

9276

2012

+3%

2005

797773

0%

417313

+4%

1.053 804

+4%

253160

2005

+7%

2012

Real GDP

$ billions

Population

Millions

Real GDP per capita

$

CAGR 2005-2012

Source: World Bank Economic Development Indicators; www.econstats.com

29

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Recommended Geographical Focus

▪ Recommended Sectorial Focus

▪ Potential Investment Vehicles

▪ Conclusion

30

There are multiple opportunities for PE investors in Africa across

several sectors

Consumer Goods Logistics

Oil & Gas

acquired

Shell Ghana

Aug’13 Nov’13 Nov’13

Nov’13 Dec’13 Jun’13

acquired

acquired

Utilities

acquired

Manufacturing

Financial Services

acquired acquired

SAMPLE OF DEALS

Source: Press Research

31

A large number of African PE investors have a sector(s)-specific

investment strategy and it seems to be the trend going forward

“Being a generic private equity

investor, a generalist, isn’t going to

deliver you superior returns. The only

way to do that is through domain

knowledge, deep understanding of

sectors that you’re interested

in, and having the ability to bring

other types of value-add to the party”

John van Wyk, Head of Africa, Actis

The Africa Handbook, PEI

Supplement, Sep’12

“There is a growing trend toward funds that

target specific sectors, largely to capitalize

on opportunities in sectors benefiting from

consumer growth as well as much-needed

infrastructure investment (i.e.,

infrastructure, real estate and agri funds)”

Private equity roundup- Africa,

Ernst & Young, Feb’13

Source: Press Research; Team Interviews

“With so many firms fundraising in the

market, we are looking for teams that have

deep sector expertise and know local

markets very well”

DFI PE investment officer

32

There are a number of sectors that seem to attract a lot of

attention from investors

33

Key sectors

However, we believe

that the greatest

opportunities for new

investors are in the

consumer space

and, in particular, in

consumer-focused

manufacturing

Agriculture

Infrastructure

Source: Press Research; Team Interviews

Manufacturing Real Estate

Natural Resources

Consumer Goods

Financial Services Energy

The African consumer will drive growth in the continent going

forward, offering attractive investment opportunities

0

200

400

600

800

2012 2014 2016 2008 2018 2010 2004 2006 2000 2002

+9,3%

Source: Global Insight

5,67,14,84,64,74,34,47,5

-0,2

10,9

-6,3

24,9

2008 2009 2007 2013 2014 2018 2015 2016 2011 2012 2010 2017

Nominal Private Consumption

Current US$, Sub-Saharan Africa

Real Private Consumption

Growth Rate (%), Sub-Saharan Africa

34

Share of households in each income bracket

%, millions of households

Consuming middle class

(10,000–20,000)

Emerging consumers

(5,000–10,000)

Household income brackets

$ PPP1 2005

Globals (>20,000)

Basic consumer needs

(2,000–5,000)

Destitute (<2,000)

Households with

income >$5,000

Million

59 85 128

Basic needs

Discretionary

income

3424

18

29

32

29

1821

23

6 8100% =

17

2020F

244

12

14

196 163

2008 2000

11

Source: “Lions on the move”, McKinsey Global Institute

By 2020, it is estimated that half of African households will have

discretionary income

Trends indicate that consumer-facing industries in Africa are likely

to outgrow most other sectors in the continent

36

Estimated annual Revenue by industry in

2020, $ Billion Main drivers of growth in the consumer industry in

Africa are:

Youngest population in the world (200 million

people between 15 an 24) and increasing levels

of education which will result in high levels of

workforce

Increasing levels of urbanization, which makes it

easier to reach consumers and raises their

income (with higher wages earned)

Growing middle-class, shifting purchasing

patterns from basic needs only to other

products

Technology development and higher

penetration, with social media representing an

important role in consuming, and with the creation

of an opportunity for online commerce

Improving business climate with stable levels of

inflation and accelerated regional integration

Source: “Lions on the Move (Africa), McKinsey Global Institute”; “African Consumers: Driving the African Private Equity

Opportunity, FMO and Fairview”

Growth 2008-2020

($ billion)

540

500

To

tal

Re

so

urc

es

Infr

astr

uctu

re

2,620 200

Co

nsu

me

r

Ag

ricu

ltu

re

1,380

520 110 220 130 980

There are a wide range of alternatives to serve the “emerging

African consumer”

37

Manufacturing Distribution Provision of Raw

Materials

Logistics and Market Linkages

Provision of Services Advertising

Banking

Insurance

Mobile services

Telecom

Construction materials

Food and beverages

House appliances

Pharmaceutical

Retail

Textiles

Infrastructure

Transportation

Potential sectors of

interest The “Consumer” Value Chain

Recommended

focus

We believe that the manufacturing sector represents an attractive

and untapped investment opportunity for PE investors in Africa

38

▪ African consumers demand African products: companies need to produce for

the local markets, adapting to the local tastes

▪ Africa has all the necessary inputs for a competitive manufacturing sector:

low-wage labor, abundant and diverse natural resources, privileged access to

selected high-income markets for exports, sufficiently large local or regional market

to allow emerging producers to develop high-volume production

▪ Africa’s manufacturing sector can benefit from China’s growth: China is

shifting from an export-driven model to one more focused on domestic markets,

creating huge opportunities for low-cost manufacturing locations like Africa

▪ PE investors can make a difference in the African manufacturing sector: PE

investors can provide their capital, best-practices know-how, strategic and

operational skills and networks to yet-not-very-productive manufacturing business

1

2

3

Source: “African Consumers: Driving the Private Equity Opportunity” FMO Fairview; Press Research; Team Interviews;

Team Analysis

4

The African manufacturing sector is growing very rapidly

“…a quiet boom in manufacturing in

Africa is already taking place. Farming

and services are still dominant,

backed by the export of commodities,

but new industries are emerging in a

lot of African countries”

The Economist, Feb’14

1 Mozambique includes ‘04-11 and Cameroon ‘04-07 data only

Source: Press Research; Team Interviews; Team Analysis

Mozambique

11,1%

5,6%

Tanzania

Senegal

Ethiopia

16,3%

12,2%

5,7%

Nigeria

8,2%

Ghana

13,1%

8,0%

Kenya

Cameroon

Manufacturing Value Added Growth

CAGR 04-121, Current US$

39

The African manufacturing sector is attracting a lot of attention

and investments in recent years from large corporates…

Ethiopia

Textile Production

Nigeria

Electrical Gear

Plant

Madagascar

Chocolate Bar

Production

Kenya

Car Production

Kenya

Pharmaceutical

Plant

Nigeria

Car Production

South Africa

Multi-category

Manufacturing Plant

Tanzania

Food-processing

Plant

Mozambique

Cement Plant

Cameroon

Agro-processing

Plant

Source: Press Research

40

…as well as from PE investors

41

Selected PE Deals in the Consumer/Manufacturing space in 2013

GP Company Country Sector Value

Abraaj Group &

Danone

Fan Milk Ghana Dairy Products US$400m

CapitalWorks Construction Products

Africa

South Africa Construction

Materials

US$135m

Pearl Capital Partners Freshco Kenya Ltd Kenya Agribusiness US$0.6m

Catalyst Principal

Partners

Chai Bora

Tanzania Agribusiness

N/A

Centum

Almasi Beverages

Kenya Food and

beverages

US$5m

Pearl Capital Partners

and Voxtra

Biyinzika Enterprises Uganda

Food and

beverages

US$4m

Catalyst Principal

Partners

Yes Brands

Ethiopia N/A Food and

beverages

Tanzanian Food

Corporation

Agri Vie Tanzania Food and

beverages

US$4.9m

Source: “Private Equity Confidence Survey 2014”, Deloitte and Africa Assets

The African manufacturing sector is very likely to continue to

grow at a fast pace

Growth drivers of the manufacturing sector in Africa

Urbanization

Economic

Growth Trade Policy

Regional

Integration

Low-cost

Base

Investment

Policy

Human

Capital

Natural

Resources

Emergence of middle-class

and increase in household

consumption and

discretionary income

Accelerating urbanization

(50% of Africa’s population

will be urban by 2020)

Huge pool of young workers

available for labor-intensive

light manufacturing

Africa is emerging as the

new global provider of low-

cost, low-skilled labor

Source: Press Research; Interviews; “Light Manufacturing in Africa” World Bank Report

Abundant natural resources

used as inputs in the

manufacturing industry

Opening up of markets,

increased competitiveness

and productivity

African products have

preferential access to the

USA and to the EU

Increased public investment

by governments and DFIs

Attraction of FDI

42

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Recommended Geographical Focus

▪ Recommended Sectorial Focus

▪ Potential Investment Vehicles

▪ Conclusion

43

We believe that a pledge fund or a deal-by-deal structure might

work better for Maera, given the challenge of raising a Fund Advantages

Pledge

Fund

Structured

Fund

Deal-by-

deal

A structured fund might help in talent hiring

and deal sourcing by giving “prestige and

credibility to investors”

GP doesn’t have to worry about fundraising

or availability of funds once the money is

raised

Relatively easy to form if the investor has access to a good network, given its flexibility, reduced cost and transparency

Gives the investor some form of “comfort” about the availability of funds

Gives LPs flexibility to invest on a deal-by-deal basis

Freest form of investment for both GPs and

LPs, allowing for total flexibility on

investments

Limited operating costs

44

Disadvantages

Difficult to raise money, particularly

given limited track record

Expensive and time consuming

process (e.g. road shows, etc)

Non-biding nature of the LP

commitment does generate some

uncertainty

Sellers look for certainty of close and

might have doubts about the

investor’s ability to raise the

necessary funds

GP might have a hard time raising

funds for a particular transaction,

both pre and post due diligence

Sellers look for certainty of close and

might have doubts about the

investor’s ability to raise the

necessary funds

Source: Team Interviews; Team Analysis

Content

▪ Introduction to the project

▪ Africa as an investment destination

▪ Private Equity in Africa

▪ Proposed Investment Strategy

▪ Conclusion

45

Our main conclusions

46

Africa represents a great investment opportunity for a PE investor like

Maera Capital, with very decent risk-adjusted returns and with plenty of

value-creation opportunities for investors with the right skills and know-

how

Consumer-facing industries seems to have a strong potential and is

likely to be one of the greatest opportunities going forward. Serving the

emerging consumer will require local products and local production,

creating significant opportunities in the (light) manufacturing sector

Finally, while we have recommended a specific investment strategy, we

know very well that there’s not a right answer to the question of how to

invest in PE in Africa and believe that there are many other models that

can work as well as or better than the one we have proposed

ANNEX

47

Economic data per country (1/2) 2012

Algeria

Angola

Benin

Botswana

Burkina Faso

Burundi

Cabo Verde

Central African Republic

Congo, Dem. Rep.

Congo, Rep.

Djibouti

Equatorial Guinea

Ethiopia

Gambia, The

Guinea

Kenya

Liberia

Country

(1) 2011 data

(2) 2010 data

(3) 2008 data

Source: World Bank Economic Development Indicators; www.econstats.com; “Lions on the Move (Africa), McKinsey Global Institute”

Cameroon

Chad

Comoros

Cote d'Ivoire

Egypt, Arab Rep.

Eritrea

Gabon

Ghana

Guinea-Bissau

Lesotho

Nominal GDP

$

Nominal GDP per

capita

$

Real GDP growth

% CAGR 2005-2012

Population

Millions

Share of Manufacturing

and Services in GDP

%

Exports per

Capita

$

206 5,348 2.6% 38 443 1,989

114 5,482 10.3% 21 37 3,295

8 752 3.9% 10 613 1091

15 7,238 4.4% 2 68 3,221

11 652 5.8% 16 44 179

2 251 4.4% 10 52 22

2 3,695 6.0% 0 923 1,177

25 1,167 3.4% 22 693 340

2 483 6.8% 5 38 56

13 1,035 4.7% 12 33 305

1 831 1.7% 1 N/A 1301

17 262 6.0% 66 38 145

14 3,154 4.8% 4 293 2,9031

25 1,244 2.2% 20 713 6352

N/A N/A N/A 1 963 514

263 3,256 5.0% 81 61 567

18 24,036 3.5% 1 213 20,280

3 504 1.6% 6 N/A 611

42 454 9.6% 92 45 64

18 11,257 3.4% 2 393 6,403

1 507 3.4% 2 72 145

41 1,605 8.0% 25 57 736

6 492 2.7% 11 543 146

1 494 2.1% 2 N/A 86

41 943 4.6% 43 63 257

2 1,193 4.8% 2 70 555

2 414 11.4% 4 48 134

48

Economic data per country (2/2) 2012

Libya

Madagascar

Malawi

Mali

Mauritania

Mauritius

Morocco

Namibia

Rwanda

Sao Tome and Principe

Seychelles

Somalia

Sudan

Tanzania

Tunisia

Zambia

Country

Mozambique

Niger

Nigeria

Senegal

Sierra Leone

South Africa

Swaziland

Togo

Uganda

Zimbabwe

Nominal GDP

$

Nominal GDP per

capita

$

Real GDP growth

% CAGR 2005-2012

Population

Millions

Share of Manufacturing

and Services in GDP

%

Exports per

Capita

$

93 15,853 5.2% 6 343 9,940

10 447 2.8% 22 733 1161

4 268 3.5% 16 653 1051

10 699 4.3% 15 553 218

4 1,106 5.5% 4 41 642

10 8,120 4.2% 1 89 4,448

96 2,902 4.9% 33 71 1,068

14 565 6.9% 25 713 168

13 5,786 4.5% 2 72 2,464

7 395 5.5% 17 48 98

263 1,555 6.8% 169 403 862

7 620 8.1% 11 57 82

0 1,400 4.8% 0 N/A 157

14 1,023 3.3% 14 73 249

1 12,783 4.6% 0 92 5,4731

4 635 6.9% 6 373 801

N/A N/A N/A 10 N/A N/A

384 7,352 3.2% 52 81 2,077

59 1,580 2.3% 37 47 99

4 3,042 1.6% 1 93 2,147

28 609 6.8% 48 58 175

4 574 3.8% 7 62 2231

46 4,237 3.4% 11 77 2,032

20 551 7.3% 36 55 128

21 1,463 6.6% 14 51 678

10 714 0.4% 14 68 316

(1) 2011 data

(2) 2010 data

(3) 2008 data

Source: World Bank Economic Development Indicators; www.econstats.com; “Lions on the Move (Africa), McKinsey Global Institute”

49

Detailed Index of Economic Freedom by country (1/2)

Country

Source: 2014 Index of Economic Freedom by the Heritage Foundation

World

Rank

2014

Score

Property

Rights

Freedom

from

Corruption

Fiscal

Freedom

Gov't

Spending

Business

Freedom

Labor

Freedom

Trade

Freedom

Monetary

Freedom

Investment

Freedom

Financial

Freedom

Mauritius 8 77 65 53 92 82 74 78 89 77 85 70

Botswana 27 72 70 61 81 70 69 70 83 72 75 70

Cape Verde 60 66 70 55 77 69 64 48 70 79 70 60

Rwanda 65 65 30 47 80 78 70 84 78 75 65 40

Ghana 66 64 50 40 85 83 63 60 65 66 70 60

South Africa 75 62 50 42 69 69 75 54 76 75 55 60

Madagascar 79 62 40 27 91 92 63 44 78 78 55 50

Swaziland 82 61 40 32 75 71 64 72 82 72 65 40

Zambia 88 60 30 31 72 83 75 50 85 68 60 50

Uganda 91 60 30 24 79 87 45 87 75 71 60 40

Gambia 92 60 30 32 79 80 57 66 65 71 65 50

Namibia 94 59 30 44 67 59 64 82 83 75 50 40

Burkina Faso 98 59 30 31 83 82 61 55 68 79 60 40

Morocco 103 58 40 33 71 64 76 31 59 78 70 60

Gabon 105 58 40 29 74 82 59 63 61 75 55 40

Tanzania 106 58 30 29 80 78 47 61 77 66 60 50

Tunisia 109 57 40 39 74 64 81 73 62 76 35 30

Benin 113 57 30 30 68 86 51 51 60 75 70 50

Djibouti 118 56 30 31 81 63 43 65 55 77 65 50

Mali 122 56 20 28 70 82 48 63 73 77 55 40

Malawi 124 55 45 32 78 63 39 60 73 64 50 50

Senegal 125 55 40 30 65 75 48 41 73 82 60 40

Niger 127 55 30 26 77 88 35 45 66 88 55 40

Mozambique 128 55 30 26 76 65 65 37 76 81 45 50

Côte d'Ivoire 107 58 30 22 79 80 55 59 71 81 50 50

Kenya 111 57 30 21 78 75 56 64 73 75 50 50

Seychelles 117 56 50 48 77 62 68 68 33 75 50 30

50

Detailed Index of Economic Freedom by country (2/2)

Country

World

Rank

2014

Score

Property

Rights

Freedom

from

Corruption

Fiscal

Freedom

Gov't

Spending

Business

Freedom

Labor

Freedom

Trade

Freedom

Monetary

Freedom

Investment

Freedom

Financial

Freedom

Nigeria 129 54 30 23 85 74 48 66 64 73 40 40

Guinea 133 54 20 19 69 86 52 73 61 64 50 40

Mauritania 134 53 25 24 82 76 38 53 69 76 50 40

Egypt 135 53 20 29 86 70 63 46 71 60 45 40

Cameroon 136 53 30 22 72 86 45 56 61 69 35 50

Liberia 138 52 30 34 84 70 62 47 64 73 40 20

Burundi 141 51 20 16 73 52 60 63 72 68 60 30

Comoros 142 51 30 22 64 85 49 50 73 75 35 30

Guinea-Bissau 143 51 20 20 89 87 41 61 61 74 30 30

Algeria 146 51 30 29 81 51 66 48 61 68 45 30

Sierra Leone 148 51 15 25 81 86 55 29 70 70 55 20

Ethiopia 151 50 30 27 77 90 58 55 64 59 20 20

Togo 152 50 30 24 70 82 43 43 63 79 35 30

Lesotho 154 49 40 37 67 0 54 62 69 76 50 40

S. Tomé Príncipe 157 49 20 33 87 28 53 45 75 68 50 30

Angola 160 48 15 18 88 55 48 40 70 64 40 40

Chad 167 45 20 16 46 80 25 43 55 70 50 40

Congo, Rep. 169 44 10 21 67 80 35 47 56 72 20 30

Eritrea 174 38 10 23 57 66 19 64 69 58 0 20

Zimbabwe 176 36 10 19 63 64 35 22 54 73 5 10

Libya N/A N/A 10 18 95 0 50 78 N/A 67 5 20

Sudan N/A N/A N/A 10 85 90 55 49 56 56 15 N/A

Somalia N/A N/A N/A 5 N/A N/A N/A N/A N/A N/A N/A N/A

CAR 161 47 10 21 65 93 34 40 52 72 50 30

Equatorial Guinea 168 44 10 17 75 63 43 42 54 75 35 30

Congo, Dem. Rep. 172 41 10 18 69 75 30 39 63 63 20 20

Source: 2014 Index of Economic Freedom by the Heritage Foundation

51