Private equity e venture capital - Politecnico di Milano pe vc.pdf · 1 1 Private equity e venture...

22

1 1 Private equity e venture capital prof. Giancarlo Giudici Corso di Corporate e Investment Banking 2014 MIP – Giancarlo Giudici 2 Fundraising • Private Equity (PE) and Venture Capital (VC) investors may use: – Their own capital (i.e. business angels) – Finance provided by affiliated entities (e.g. corporate or bank) – Finance collected on the market by investors like banks, foundations, family offices, funds of funds, companies and wealthy investors • In the latter case, promoters compete to collect financial resources, as they have to convince investors to finance their project • The fundraising process is divided into several phases: – setup of the General Partner (entity owned by promoters) – submission of the investment memorandum to potential investors – collection of ‘soft commitments’ – (in case of success) setup of the Fund Vehicle – call for cash payments

Transcript of Private equity e venture capital - Politecnico di Milano pe vc.pdf · 1 1 Private equity e venture...

1

1

Private equity e venture capital

prof. Giancarlo GiudiciCorso di Corporate e Investment Banking

2014 MIP – Giancarlo Giudici2

Fundraising

• Private Equity (PE) and Venture Capital (VC) investors may use:

– Their own capital (i.e. business angels)

– Finance provided by affiliated entities (e.g. corporate or bank)

– Finance collected on the market by investors like banks, foundations, family offices, funds of funds, companies and wealthy investors

• In the latter case, promoters compete to collect financial resources, as they have to convince investors to finance their project

• The fundraising process is divided into several phases:

– setup of the General Partner (entity owned by promoters)

– submission of the investment memorandum to potential investors

– collection of ‘soft commitments’

– (in case of success) setup of the Fund Vehicle

– call for cash payments

2

2014 MIP – Giancarlo Giudici3

The General Partner

The GP is typically a limited liability company, participated only

by the fund promoters, and is

an unlimited shareholder of the fund. For

sake of credibility, it also

provides a (small) fraction

of the fund

Investors are limited shareholders of the fund, with priority in case of liquidation

2014 MIP – Giancarlo Giudici4

The investment memorandum

• The Investment Memorandum is presented and distributed among potential investors. It contains:– A profile of the promoters and of the investment team

– Investment policy: type of investments (business sector, geographical area, majority/minority stakes, seed/early stage, …) and how the fund will create value (active management, support, M&A or internal growth…)

– Lifecycle: typically a PE fund is built on a 10-year period; the first period is devoted to investment selection, the second to venture management, the third to the exit

– Governance provisions: how investment decisions are made, mechanisms of investor consultation, monitoring, committees, conflicts of interest

– Budget plan: target fundraising, cost and revenues, expected IRR

– Management fee (typically 2-3% of the committed capital / called down capital)

– Profit sharing: typically capital gains are shared by the GP and the investors (‘carried interest’), above a certain IRR (‘hurdle rate’) 6%-8%

Example: Initial investment = 100

Net realization at vintage (time 10) = 280 Capital gain = 180

100 * (1+8%)^10 = 215,89 => 115,89 to investors

64,11 is divided e.g. 75% investors, 25% promoters

3

2014 MIP – Giancarlo Giudici5

The fund vehicle

• The fund may me established in the form of:– A (domestic or foreign) holding company: in such a case, the desired governance

structure is obtained through provisions contained in the Statutes of the company and/or shareholder agreements

– A (domestic or foreign) supervised vehicle (e.g. a closed-end fund promoted by a SGR company in Italy, a SICAR in Luxembourg, a Trust…): the fund will be authorised and supervised by a public authority; this option offers more guarantees to investors, and occasionally tax benefits

• ‘Anchor investors’ are early investors supporting the collection

• As soon as the ‘soft’ commitments are collected, the fund will be established and activity will begin. If the target capital is not reached, the project is withdrawn.

2014 MIP – Giancarlo Giudici6

Case studies

• 360 capital partners is a VC company managed by an Italian-French team. The company operates through Luxembourg vehicles: 360 Capital Investments SA (2007) and 360 Capital 2011 Investments SA. Investments comprise: Eataly net, Venere.com, BeMyEye, Leetchi.com

• Dpixel is a VC company founded by Gianluca Dettori. The vehicle is a Luxembourg company, Digital Investments SCA SICAR. Investments include ViaMente, Vivaticket, Ciceroos, Mangatar

• Principia SGR is an Italian company established in 2002 managing closed-end VC funds (Principia Fund and Principia II). Investments include Banzai, Vivocha, Jusp, MoneyFarm

€ 90 M

€ 300 M

€ 40 M

4

2014 MIP – Giancarlo Giudici

Statistics on fundraising

7

2014 MIP – Giancarlo Giudici

Statistics on VC fundraising

8

5

2014 MIP – Giancarlo Giudici

VC money

9

2014 MIP – Giancarlo Giudici10

Deal origination

• Managers of a PE fund have first to seek for opportunities i.e. interesting projects to be financed

• The main sources of origination are:

– Business plans submitted by entrepreneurs

– Incubators

– Internet and magazines

– Consultants with mandates (in this case a ‘blind profile’ may be submitted)

– Universities and R&D centres

– Startup competitions

– Bank advisors

• The origination is a crucial phase, since:

– The fund manager shall be able to collect many projects, in order to maximize the probability of finding the good cherry

but

- Time has a cost!

6

2014 MIP – Giancarlo Giudici11

Screening

• What PE and VC investors consider:

– Quality of the business plan and coherence with investment policies

– Team commitment, skills, capability of execution and track record (this is the real challenge!)

– Expected growth of the business

– Competitive advantage

– Innovation (and means to protect it)

– Synergies with other portfolio investments

– Sustainable financing plan

– Way-out perspectives (4-7 years)

• Market conditions and timing are important

• Specialization vs. diversification

RATE OF RETURN

2014 MIP – Giancarlo Giudici12

Not easy at it looks

Bessemer Venture Partners (BVP) is the longest-standing venture capital partnership in the United States. Since its inception in 1911, BVP has provided capital to companies such as Box, Pinterest, Quidsi(Diapers.com), Skype, Staples Inc., VeriSign and Dick’s Sporting Goods. More than 100 VC-backed companies have gone public.

BUT

They refused to invest in:

GOOGLE: the VC’s college friend rented her garage to Sergey and Larry for their first year. She tried to introduce him to “these two really smart Stanford students writing a search engine”. He said: “How can I get out of this house without going anywhere near your garage?”

e.BAY: ‘Stamps? Coins? Comic books? You've GOT to be kidding… no-brainer pass’

APPLE: ‘outrageously expensive’

PAYPAL: ‘a rookie team… a regulatory nightmare’

7

2014 MIP – Giancarlo Giudici13

First screening

• VCs tend to be very selective: only a small percentage of business plans submitted are effectively analysed

• A first interview aims at clarifying managerial and technical issues contained in the business plan

• Elevator pitches are also common

• If necessary, more data are released upon signing a ‘non-disclosure agreement’ (NDA)

• The VC may be assisted by consultants, expert in the related technology

• Often the VC asks for exclusivity in the bargaining, in order to protect the time and knowledge investment

• Any binding commitment for investment is released after an adequate ‘due diligence’

• A ‘memorandum of understanding’ (MoU) is the document that may be signed at this stage

• This phase is also called ‘light due diligence’

2014 MIP – Giancarlo Giudici14

The deal structuring

• The main issues to be discussed between the PE fund and the entrepreneur are related to:

– Price to be paid for the shares, in excess of the par value; if the price is ‘low’ the entrepreneur is selling his project at a discount, while if the price is ‘high’ the VC profitability will be lower (target IRR)

– Financing plan (the fund may also subscribe junior or convertible debt, or preferred stock, ‘call’ options and/or warrants)

– Stage financing, according to the achievement of the business plan milestones

– Composition of the board

– Options held by the fund (e.g. ‘tag-along’ or ‘drag-along’ clauses)

– Super-majority, take-over clauses, pre-emption and veto rights (‘moral hazard’ issues)

– Wayout perspectives

• As soon as there is a first informal agreement on the matters above, a ‘letter on intents’ (or ‘term sheet’) is signed between the parties

8

2014 MIP – Giancarlo Giudici15

Due diligence

• The (‘hard’) due diligence aims at reducing information asymmetry between the entrepreneur and the fund, as well as the investment risk:

– Business due diligence: study of the business model, in order to understand if the entrepreneur’s estimates about revenues and costs are affordable

– Technical due diligence: required if the technology proposed is rather specific and/or innovative

– Legal due diligence: required in order to avoid legal troubles or litigation risks (i.e. patent infringement, national laws, pending procedures, …)

– Tax due diligence: required in order to minimize tax effects

– Environmental due diligence: required if there are potential hazards

• For VC investments, since the company is not yet existing (or is just a start-up) the latter tests are less crucial

• The due diligence costs are generally paid by the fund

2014 MIP – Giancarlo Giudici16

The contract (‘closing’)

• Finally the two parties agree on the ‘pre-money’ valuation of the company:

‘Pre-money’ = outstanding shares * price

New capital raised = shares subscribed by fund * price

‘Post-money’ = (outstanding + subscribed shares) * price

• Usual valuation methodologies include: comparables, NPV, terminal value discounting, option analysis

• In case of misalignment of expectations, an ‘earn-out’ scheme can be adopted

• The final contract is written with the assistance of the lawyers, and the partnership begins

• A syndication with other funds may be introduced, in order to share risks and capture network effects

• A shareholders’ agreement will be signed

9

2014 MIP – Giancarlo Giudici17

Covenants

• Sale / purchase of assets: typically forbidden not to modify the business model or to spin-off the ‘crown jewels’

• Distribution of dividends: typically forbidden in order to preserve cash for sustaining the growth

• Change of control: the fund wants the entrepreneur to stay in control

• Issuance of new securities (dilution effect): typically forbidden without the consent of the fund

• Accounting ratios (especially for debtholders)

– Avoid excess leverage

– Ensure liquidity equilibrium

2014 MIP – Giancarlo Giudici18

Case study: Rovio

• In 2003, three students from Helsinki University of Technology, NiklasHed, Jarno Väkeväinen, and Kim Dikert developed a multiplayer game called ‘King of the Cabbage World’. Renamed to ‘Mole War’, this became the first commercial real-time multiplayer mobile game in the world.

• In January 2005, they received a first round of finance ($1 million for 87% of equity) from a business angel (Niklas’ uncle, an IT entrepreneur), and the company took the name Rovio (‘bonfire’ in finnish)

• 2009: closed to bankrupt, release of ‘Angry Birds’ game (52nd of the series), one of the most successful game ever (>1 billion downloads) generating $50 million in revenues each year

• 2011: Rovio raised $42 million in venture capital funding from Accel Partners, Atomico(VC company founded by Skype entrepreneurs) and Felicis Ventures, for 21% of equity

10

2014 MIP – Giancarlo Giudici19

Case study: Mosaicoon

• Mosaicoon is a viral marketing and video company created by UgoParodi Giusino (1981) in Palermo in 2007 with an equity capital of 10k€

• 2009: first round of venture capital (650 k€) by Vertis Venture

• 2011: meet the target of 800k€ revenues

• Opening of three new offices in Milan, London, Rome, with 25 employees

• 2012: winner of the PNI-cube (Italian prize for innovation)

• 2013: second round of financing (2,5 M€) by Vertis Venture and Atlantethrough equity and warrant subscription

• The equity capital is divided into four class of shares:

type A, B (owned by the founder), C, D, with

different claims and restrictions on voting power

2014 MIP – Giancarlo Giudici20

Statistics on investments in Europe

11

2014 MIP – Giancarlo Giudici21

Statistics on investments in Europe

2014 MIP – Giancarlo Giudici22

VC investments as % of GDP

12

2014 MIP – Giancarlo Giudici23

VC investments by sector

2014 MIP – Giancarlo Giudici24

Managing the venture

• The fund is willing to help the entrepreneur in managing the company

• His task is, above all, to find customers, to recruit capable managers, to build a network with banks, suppliers, media, and to advise on the management

• The mentorship may be provided by the fund manager himself, or by managers hired on the market

• Take-over clauses are seldom exercised

• Monitoring is crucial, and the fund asks the entrepreneur to provide periodical data on costs and revenues (especially if the fund has to produce statements to its investors)

13

2014 MIP – Giancarlo Giudici25

Case study: Shazam

• Shazam is a commercial mobile phone based music identification service, with its headquarters in London.

• The company was founded in 1999 by Chris Barton and Philip Inghelbrecht, students at Berkeley. Searching for an audio specialist, they brought on board Avery Wang, a Stanford PhD. They had difficulty finding investors in Silicon Valley (“The reality was that in North America the investor sentiment was very much focused on the Internet … whereas in Europe … mobile services were more established”) and so moved to London, partnering with some business angels and funds like IDG Ventures, Acacia, Lynx (funding in 2001: € 7.5 million; 2003: € 5 million; funding in 2004: € 6 million)

• The service was launched initially in the UK in 2002 and was known as ‘2580’, since customers dialled the shortcode from their mobile phone to get music recognised.

• The first few years were tough: the company had trouble figuring out the right business model and was losing money

2014 MIP – Giancarlo Giudici26

• Two of its investors bailed, the founders were removed from day-to-day management roles, and Shazam was forced to accept a “down round.” It had a pre-money valuation of € 500,000. London venture firm DN Capital invested into the company in 2009 (undisclosed amount).

• IDG brought in the company’s current CEO, Andrew Fisher, and DN Capital helped with Shazam's first U.S. hire, a saleswoman who closed a deal with AT&T and Verizon to embed the Shazam app into phones

• Shazam for iPhone 2.0 debuted on 10 July 2008.

• 2011: new equity round ($ 32 million from Kleiner Perkins and IVP) to finance the TV business; Shazam reported revenues for 15.6 million GBP and yet no profits

• The company has now a following of 300 million people worldwide.

14

2014 MIP – Giancarlo Giudici27

Exit

• The exit strategy for a fund is already planned in the investment phase, and is part of the deal signed with the entrepreneur

• Most of the times, the manager of a fund is expected to capitalise the investment and pay back money to investor

• The exit may occur in one of the following ways:

– IPO: the company is taken public with an Initial Public Offering, and accessthe Stock Exchange; the fund stake is part of the IPO;

– Trade sale: the fund stake is sold with a private offer, to a biddingcompany, or to another fund, or the entrepreneur buys back the shares;

– Write-off: in case of failure and poor performance, the venture is left to itsown destiny and the investment is written-off.

• The choice of the exit alternative is strongly affected by market conditions and momentum

• The timing may generate conflicts between the founder and the investor, the latter being interested in capitalising the investment

2014 MIP – Giancarlo Giudici28

Statistics about exit in Europe

15

2014 MIP – Giancarlo Giudici29

Statistics about exit in Europe

All private equity

2014 MIP – Giancarlo Giudici

Statistics about exit in Europe (VC)

30

16

2014 MIP – Giancarlo Giudici31

IPO

• An Initial Public Offering (IPO) is the way to the stock exchange for a venture-backed companies

• The public offering is necessary to build up the floating capital, to be traded on the exchange

• The offering may be related to:

– Primary shares: newly issued shares, allowing the IPO company to raisenew funds

– Secondary shares: existing shares sold by pre-IPO shareholders (e.g. venture capitalists); this is the exit opportunity

• Rarely the VC completely exits from the investment at the IPO (thussignalling to the market that the IPO company has still margins to create value)

• The IPO is the most costly exit strategy. Generally 5%-7% of the IPO proceeds are burned by IPO commissions.

2014 MIP – Giancarlo Giudici32

Yoox is a a global Internet retailing seller of fashion & design brands.

The business idea is to offer to retail consumers off-season branded apparel and accessories, at good prices.

The second line of business, developed more recently (TheCorner.com), is an in-season web commerce of premium apparel and accessories, covering a more sophisticated market.

Yoox manages also mono-brand platform for top branded maisons.

The company was founded by Federico Marchetti in 2000 (31 years old), but revenues started in 2006.

The project was financed by venture capitalists: Kiwi (funds I and II), Nestor and Benchmark Capital (holding 55% of the company). A number of friends also contributed in risk capital, holding 15% of the company. Marchetti had 15% and other managers the remainder.

Example of VC-backed IPO: Yoox

17

2014 MIP – Giancarlo Giudici33

Marchetti served as brand and luxury expert in Lehman Brothers, and then worked for Armani in NY. In this period he had the idea of a distribution channel for end-season branded apparel.

He presented his idea to a series of VCs that believed in the project and funded the company.

In 2002 the web site had more than 100,000 registered users and 7 million visitors. In the following years the business developed in 67 countries and opened 6 local offices.

Revenues grew steadily and the business was immediately profitable, given the low-cost structure.

In 2008 revenues hit the amount of €100 million with EBITDA equal to €15 million. In 2009 (1H) sales accounted for €106.7 million, and EBITDA for €7.2 million. 70% of revenues were outside Italy.

Shareholders, despite the bearish market momentum, decides to list on the Milan Stock Exchange. The company had virtually no debt.

2014 MIP – Giancarlo Giudici34

Marchetti says that the flotation on the stock exchange allowed the company to raise new capital without loosing control of founders.

September 2009: filing of IPO prospectus; the company offers 2.45 millionshares to retail investors and 21.88 million shares to selectedinstitutional investors. The indicative offer price ranges between €3.6 and €4.5, thus valuing the company pre-money €180 million to €225 million. The final IPO price is set at €4.3. IPO in Novembre 2009.

18 million shares are offered by existing investors; the remaining are newlyissued (thus allowing the company to raise about €25 million).

VC financers partially exit the investments and commit for a 6-month lock-up:

- Kiwi I and II sell 5.4 milllion shares (about 55% of the stake)

- Nestor sells 5.0 million shares (about 55%)

- Benchmark Capital sells 3.0 million shares (about 30%)

VCs completed their exit in 2010, with the exception of Benchmark Capital.

18

2014 MIP – Giancarlo Giudici35

Trade sale

• The VC investor alternatively may sell the stake to another party, through a private sale:

– Another institutional investor (for example a PE fund) specialized in later-stage development, or buyouts

– An industrial group, interested in the technology and value accumulated in the VC-backed company

– The founder, who may be interested in buying back the shares

• The VC may directly seek for a buyer, or give a ‘sell-side’ mandate to a private bank or to a financial advisor

• Compared to the IPO alternative, when a trade-sale occurs, the founderwill more likely cease to be the controlling owner, because the biddermost of the times is interested in taking over the majority of the equitycapital

2014 MIP – Giancarlo Giudici36

IPO vs. trade sale

The flow of M&A and IPO activity is cyclical.

It is typically related to:

- The market momentum (in ‘bullish’ periods, or ‘hot issue’ periods, companies obtain more generous valuation and investors are more willing to subscribe stock)

- Business trends (see the ‘dot.com’ bubble in 1999 and 2000, and the ‘social network’ mania in 2011 and 2012); in such occasions the market learns about the sector and information costs decrease

Source: Ritter et al. (2013)

19

2014 MIP – Giancarlo Giudici37

Example of trade sale: Trivago

• Dusseldorf-based firm founded in 2005 by Peter Vinneimer, MalteSiewert and Rolf Schromgens. It is a travel metasearch engine focusing on hotels.

• December 2007: € 1 M funding by HOWZAT media LLP, an internet media investment fund

• December 2010: Insight Venture Partners, a New York based Venture Capital fund, acquires 25% shares of Trivago for € 40 M cash

• December 2012: Expedia acquires a majority stake in Trivago (61.6%). The deal is € 477 M worth, 434 M cash and 43 M common Expedia shares. The remaining 38.2% of the capital is held by Trivago’smanagement and founders. Expedia has the option to acquire another half of the remaining capital within 3 years and the remaining stake within 5 years. The valuation represents a multiple of 8x the expected 2012 sales (about € 100 M).

• Both the funds completely exit the investment

2014 MIP – Giancarlo Giudici38

Write-off

• When the VC-backed company destroys value and has no opportunitiesfor a recovery, the stake is simply dismantled and the venture isabandoned

• Example: Amp’d Mobile

Amp’d Mobile was a mobile phone service launched in the United States in late 2005. The company took $360 million in venture funding over 5 rounds. Investors include RedPoint Ventures, Highland Capital Partners and Columbia Capital.

The service targeted 18-35 year olds, and was the first integrated mobile entertainment company for youth, young professionals and early adopters.

Its mistake was to receive payments in 90 days, in a foolhardy effort to boost subscribers. It has been reported that 80,000 of the company’s 175,000 customers were unable to pay their bills.

Amp'd Mobile filed for Chapter 11 bankruptcy protection in June, 2007, with huge debts outstanding.

20

2014 MIP – Giancarlo Giudici39

2014 MIP – Giancarlo Giudici40

Valuation

21

2014 MIP – Giancarlo Giudici41

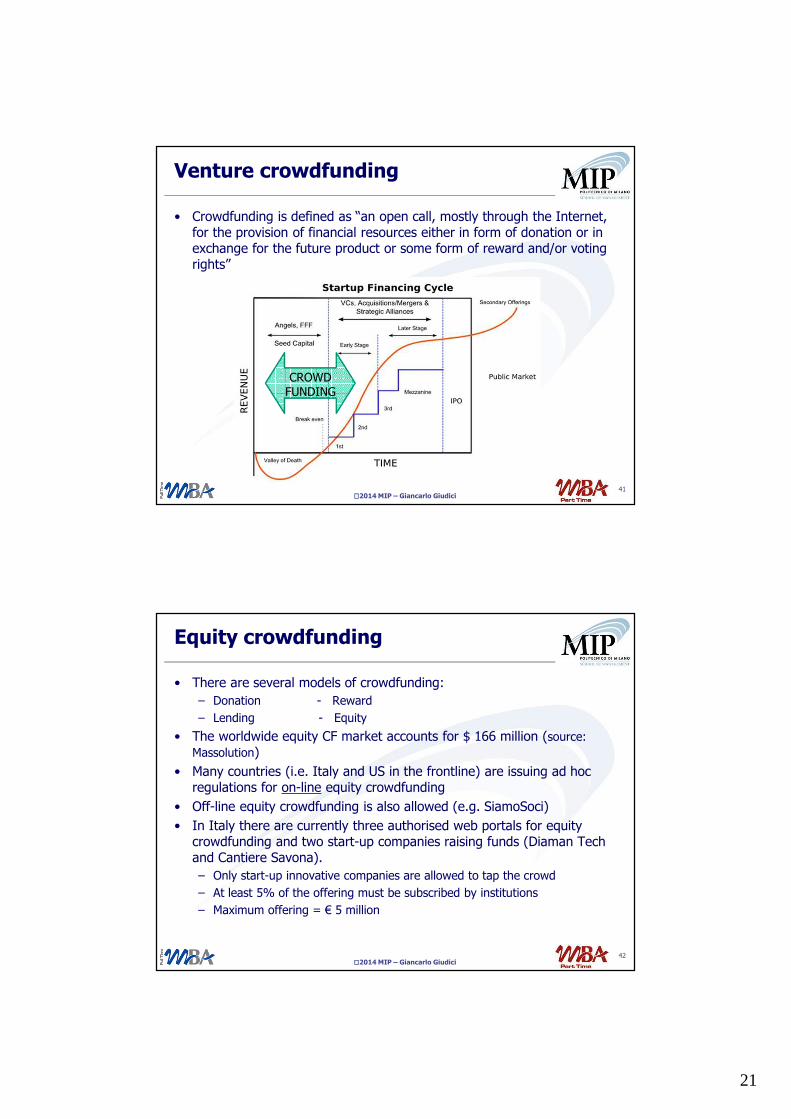

Venture crowdfunding

• Crowdfunding is defined as “an open call, mostly through the Internet, for the provision of financial resources either in form of donation or in exchange for the future product or some form of reward and/or voting rights”

CROWDFUNDING

2014 MIP – Giancarlo Giudici42

Equity crowdfunding

• There are several models of crowdfunding:

– Donation - Reward

– Lending - Equity

• The worldwide equity CF market accounts for $ 166 million (source:

Massolution)

• Many countries (i.e. Italy and US in the frontline) are issuing ad hoc regulations for on-line equity crowdfunding

• Off-line equity crowdfunding is also allowed (e.g. SiamoSoci)

• In Italy there are currently three authorised web portals for equity crowdfunding and two start-up companies raising funds (Diaman Tech and Cantiere Savona).

– Only start-up innovative companies are allowed to tap the crowd

– At least 5% of the offering must be subscribed by institutions

– Maximum offering = € 5 million

22

2014 MIP – Giancarlo Giudici43

Equity crowdfunding: case