private equity - corporate tax - antitrust international corporate finance

Upload

chris-mercerCategory

view

156download

1

Private Company Corporate FinanceZ. Christopher Mercer, ASA, CFA, ABARMercer [email protected] | 901.685.2120

Exit Planning, Transaction Advisory Services, and Healthcare Valuation ConferenceNovember 17, 2015

2

Ownership Transfer Matrix Vertical or Horizontal?

See Figure 3 on page 22 in Unlocking Private Company Wealth.© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

Partial Sale/Transfer

Total Sale/Transfer

Voluntary Transfer

• Private Equity/PE

• Sales to Insiders/Relatives

• Gifting Programs

• Sale of Business

• ESOP/Management Buyout

• Buy-Sell Agreements

Involuntary Transfer

• Personal Financial Issues

• Divorce

• Death

• Divorce

• Buy-Sell Agreements

There are legitimate, effective, and available alternative techniques to create shareholder liquidity and cash flow, enhance business performance and returns, and provide opportunities for overall portfolio diversification

Not all are appropriate for all companies at all times

May be appropriate for consideration under specific conditions and circumstances

4

Private Company Finance Options

Easily implemented optionsRegular dividends

Special dividend

Repurchase shares from owners desiring to sell

Establish a management buy-in program

Significant & Realistic Minority OptionsLeveraged dividend recap

Leveraged stock recap (buy-back)

ESOP

Non-control private equity investment for liquidity/growth

Control-Level OptionsLeveraged dividend recap

Leveraged stock recap (buy-back)

ESOP

Private equity (majority investment)

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

5

Today’s Session

Dividend policy

Special dividends

Leveraged dividend recaps

Leveraged share repurchases

Balance sheet optimization

EBITDA multiple

ESOPs

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

6

The

Solution

Using One Percent

Solution strategies is

tantamount to applying

basic tools of corporate

finance to private

corporate America

See page 36 in Unlocking Private Company Wealth.© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

7

The

Solution

Basic ToolsDividend Policy

Capital Investment Decisions

Share Repurchases

Leverage

See page 36 in Unlocking Private Company Wealth.© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

8

Dividend Policy

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

Every company has a dividend policy

Dividend policy is a starting point for portfolio diversification

Special dividends enhance personal liquidity and diversification

Dividend policy matters

Boards of directors need to establish thoughtful dividend policies

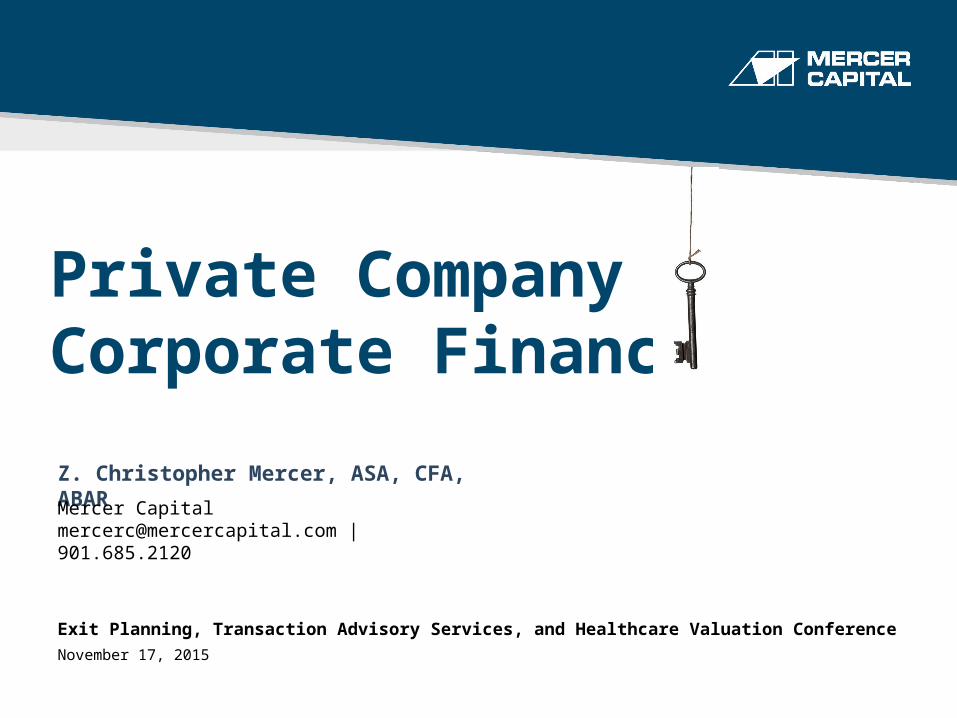

Dividends and Dividend Policy for Private Cos

Never pay a dividend One time dividend Special dividend

Constant dollar dividend

Set a dividend payout ratio target

Dividend yield target

Residual dividend policy

Spin-out for spin-off of subsidiaries or

other assets

Leveraged dividend

recapitalization

10 Types of Dividend Policies

Distributions for tax pass-through liabilities

Dividend Policy Influences Return

on Business Investment

Theory – Neutral

Reality – If you run the company well, pay dividends, and maintain normal capital

structure, you may well beat the theoretical

12© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

13© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

14

A key benefit of this type of policy is that shareholders retain a regular quarterly dividend, but the company has more flexibility in how it returns additional excess cash beyond the regular dividend rather than having to repurchase share regardless of price.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

15© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

16© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

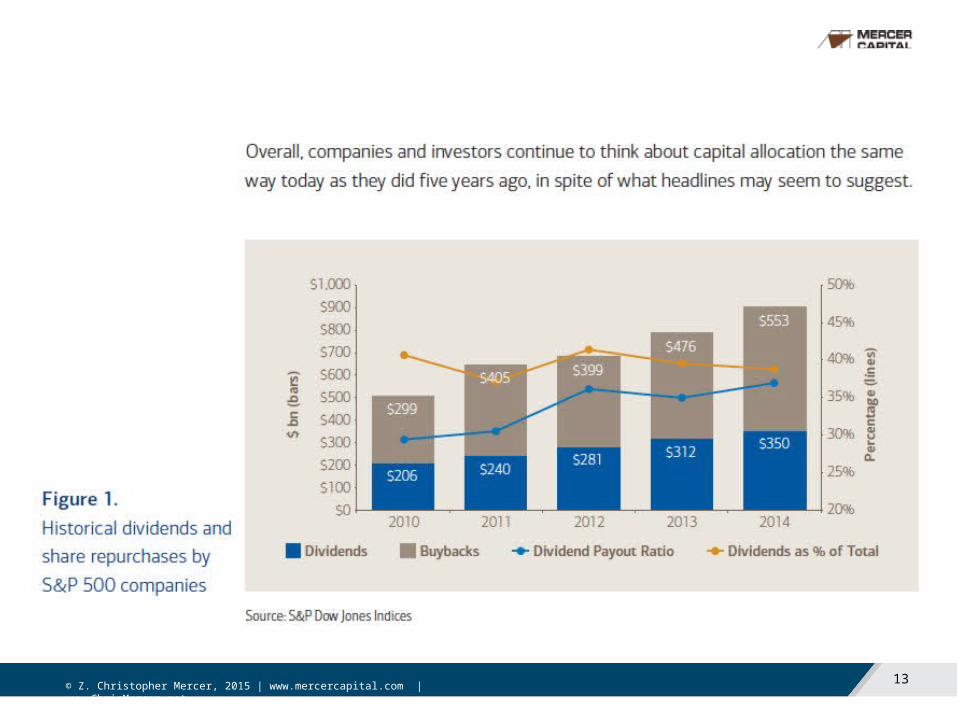

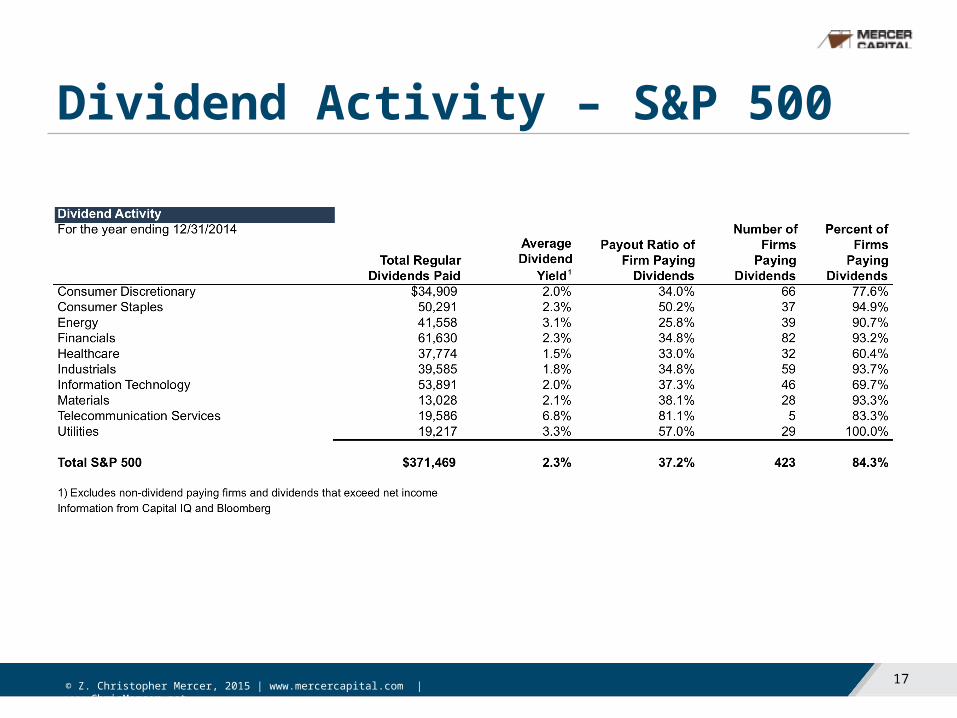

17

Dividend Activity – S&P 500

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

18

Dividend Policy Influences Return on Business Investment

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

19

Return Concepts

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

20

Special Dividends

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

21

Special Dividends – S&P 500

22

Leveraged Dividend Recaps

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

Leveraged Dividend Recap

23

Debt

EquityEquity

Debt

Cash Dividend to Shareholders

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

24

Leveraged Dividend RecapLiquidity & Diversification Leveraged Dividend Recap

Means of Achieving Partial LiquidityCreating Diversification Opportunities Yes, for all shareholders

Creating Diversification Opportunities Yes, for all shareholders

Tax Treatment Dividend rates

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

25

Leveraged Dividend RecapLiquidity & Diversification Leveraged Dividend Recap

Shareholder BenefitsEffect on Number of Shares Outstanding No effect

Relevant Shareholders All shareholders (no change in ownership)

Effect on Earnings Per Share (EPS) Decrease (earnings lowered by interest expense)

Effect on Return on Equity (ROE) Increase (equity reduced relatively more than earnings lowered)

Effect on Expected Future Value Growth Increase (as debt is repaid)

Effect on Dividends Per Share None (assuming any prior dividend is retained)

Effect on Price/Book (P/B) Value Ratio Increase (equity reduced relatively more than earnings lowered)

Effect on Pro Rata Ownership of Company No effect (no change in number of shares outstanding)

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

26

Leveraged Dividend RecapLiquidity & Diversification Leveraged Dividend Recap

Additional Benefits to Company & OwnersEffect on Capital Structure Move toward optimizing (assuming reasonable leverage)

Effect on Management Should focus attention on operating so that debt can be reduced timely

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

27

Leveraged Recapitalizations

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

Two types of transactions look similar to company

Share Repurchases Dividends

28

Leveraged Recapitalizations

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

Look similar to company

29

Leveraged Recapitalizations

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

30

Leveraged Recapitalizations

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

Which is best? You decide

31

Leveraged Share Repurchases

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

32

Leveraged Share RepurchasesLiquidity & Diversification Leveraged Share RepurchasesMeans of Achieving Partial Liquidity

Creating Diversification OpportunitiesYes, partial or full liquidity for selling owners

Creating Diversification Opportunities Yes, for selling owners

Tax Treatment Capital gains rates

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

33

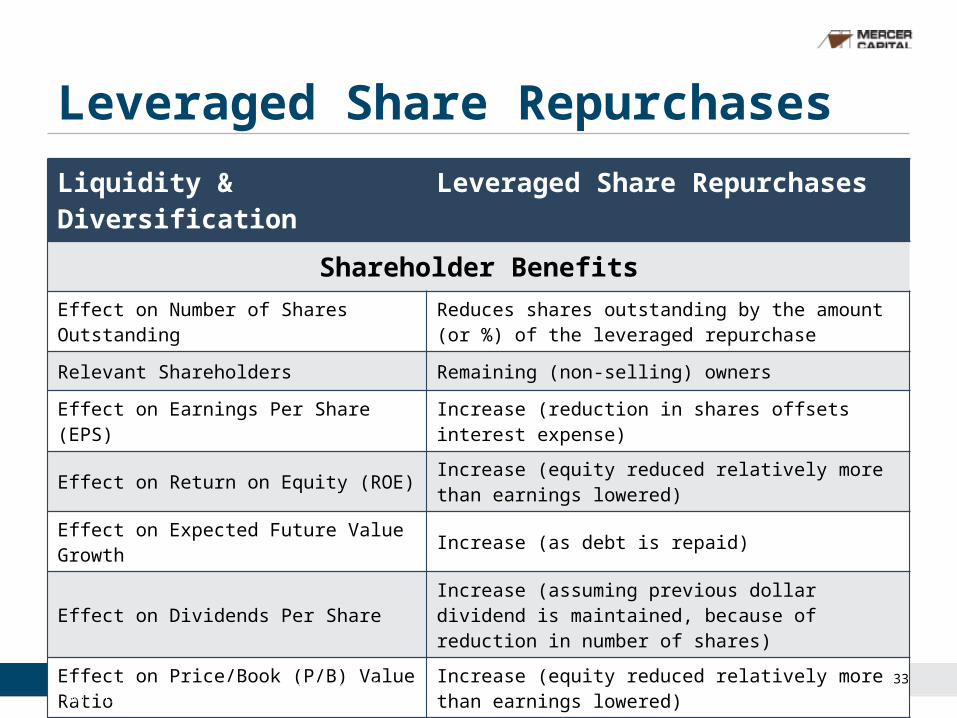

Leveraged Share RepurchasesLiquidity & Diversification Leveraged Share Repurchases

Shareholder Benefits

Effect on Number of Shares Outstanding Reduces shares outstanding by the amount (or %) of the leveraged repurchase

Relevant Shareholders Remaining (non-selling) owners

Effect on Earnings Per Share (EPS) Increase (reduction in shares offsets interest expense)

Effect on Return on Equity (ROE) Increase (equity reduced relatively more than earnings lowered)

Effect on Expected Future Value Growth Increase (as debt is repaid)

Effect on Dividends Per Share Increase (assuming previous dollar dividend is maintained, because of reduction in number of shares)

Effect on Price/Book (P/B) Value Ratio Increase (equity reduced relatively more than earnings lowered)

Effect on Pro Rata Ownership of Company Increase (by number of shares owned divided by (1-% of total shares repurchased))

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

34

Leveraged Share RepurchasesLiquidity & Diversification Leveraged Share Repurchases

Additional Benefits to Company & Owners

Effect on Capital Structure Move toward optimizing (assuming reasonable leverage)

Effect on Management Should focus attention on operating so that debt can be reduced timely

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

35

Share Repurchases – S&P 500

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

36

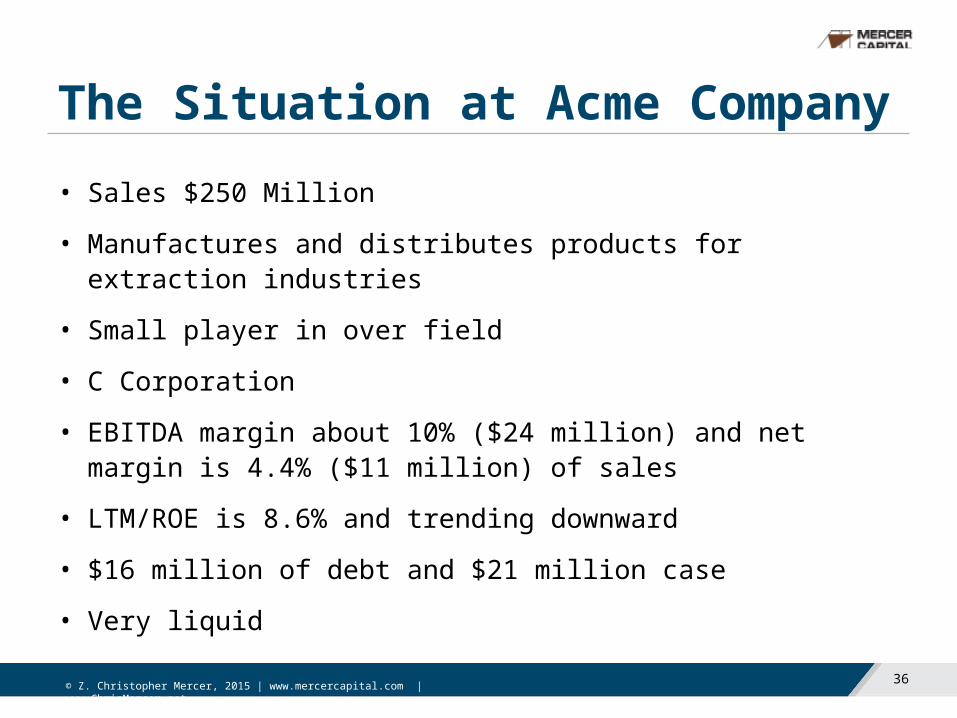

The Situation at Acme Company• Sales $250 Million

• Manufactures and distributes products for extraction industries

• Small player in over field

• C Corporation

• EBITDA margin about 10% ($24 million) and net margin is 4.4% ($11 million) of sales

• LTM/ROE is 8.6% and trending downward

• $16 million of debt and $21 million case

• Very liquid

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

37

The Situation• Working capital as a percentage of sales is about 32% (vs 20% for

publics)

• $126 million of equity, which comprises 72% of assets

• Equity value - $149 million

• 6 X EBITDA – Debt + Cash

• Cash dividend of $3.0 million per year for years

• Payout ratio of 27.5%

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

38

Transaction AssumptionsKey Transaction Assumptions Values Comments

1 Number of Shares to be Purchased 300,000 30% of the outstanding shares

2 % of Cash Considered Excess 100.0% Use all cash on balance sheet

3 EBITDA Multiple for Pricing Transaction 6.0 Assumption

4 Dollars of Current Annual Dividends $3,000,000 Factual

5 Given Number of Shares for Example 100,000 10% block

6 Interest Rate on Pro Forma Cash 1.00% Assumption of CFO

7 Interest Rate on Pro Forma Debt 6.00% Assumption per bank discussions

8 Effective Tax Rate 36.20% Factual

9 EBITDA Multiple for Pro Forma #1 Valuation 6.00 No Change in EBITDA Multiple

10 Price/Earnings Multiple for Pro Forma #2 13.7 Proxy for future benefit of recap

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

39

Financing of Transaction

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

40

Pro Forma AnalysisBalance Sheet Ratios Before Pro Forma Comments

Current Ratio 4.4Lots of liquidity

3.5 Adequately liquid

Acid Test Ratio 2.2 1.3 Reasonable

Working Capital % of Sales 31.6% 23.5% Reasonable

Total Liabilities / Assets 28.3% 47.5% Reasonable

Total Liabilities / Equity 39.9% 91.8% Reasonable

Interest Bearing Debt / Equity 13.0%Low leverage

50.2% Moderate leverage

Interest Bearing Debt / Assets 9.2% 26.0% Reasonable

Assets / Equity 1.4 1.9 Reasonable

Debt / MVTC 11.3% 28.0% Reasonable

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

41

Income Statement Analysis

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

42

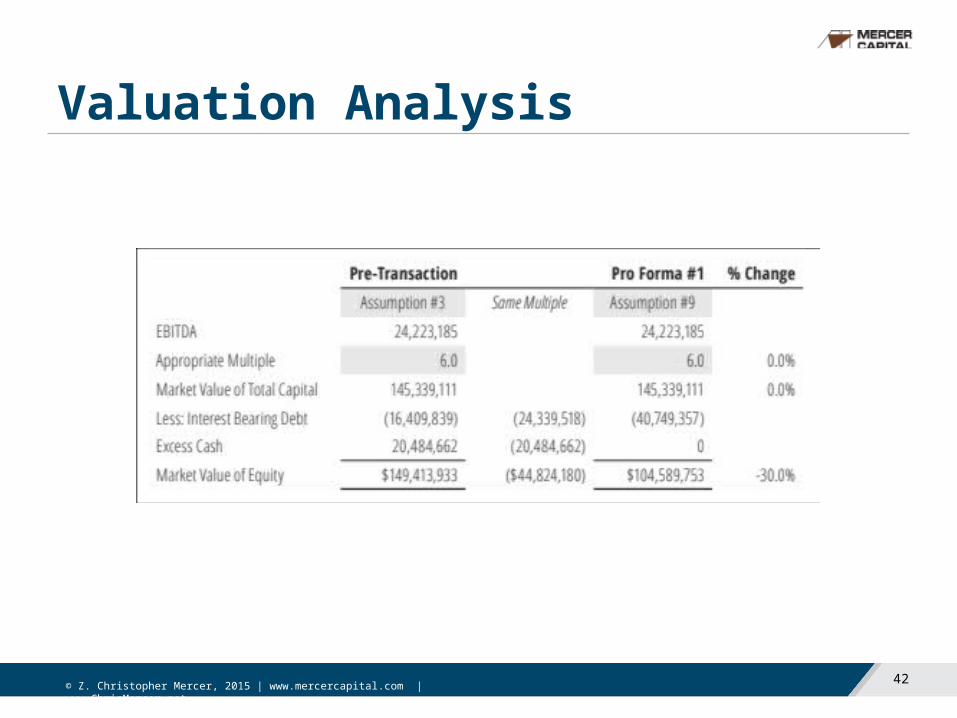

Valuation Analysis

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

43

Return Analysis

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

44

Benefits to Remaining Owners

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

45

Balance Sheet Optimization

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

46

Apple Balance SheetApple, Inc (AAPL)in $ millions, except per share data

Balance Sheet Reported Adjusted

Cash & Short Term Investments $41,601 ($41,601) $0Other Current Assets $47,777 $47,777Long Term Investments $164,065 ($164,065) $0Other Long Term Assets $37,036 $37,036Total Assets $290,479 $84,813

Current Liabilities $80,610 $80,610Long Term Debt $53,463 $53,463Other Liabilities $37,051 $37,051Total Liabilities $171,124 $171,124

Total Equity $119,355 ($205,666) ($86,311)Total Liabilities & Shareholders' Equity $290,479 $84,813

Value of Adjustment $205,666Common Shares Outstanding (millions) 5,578.75Special Dividend $36.87

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

47

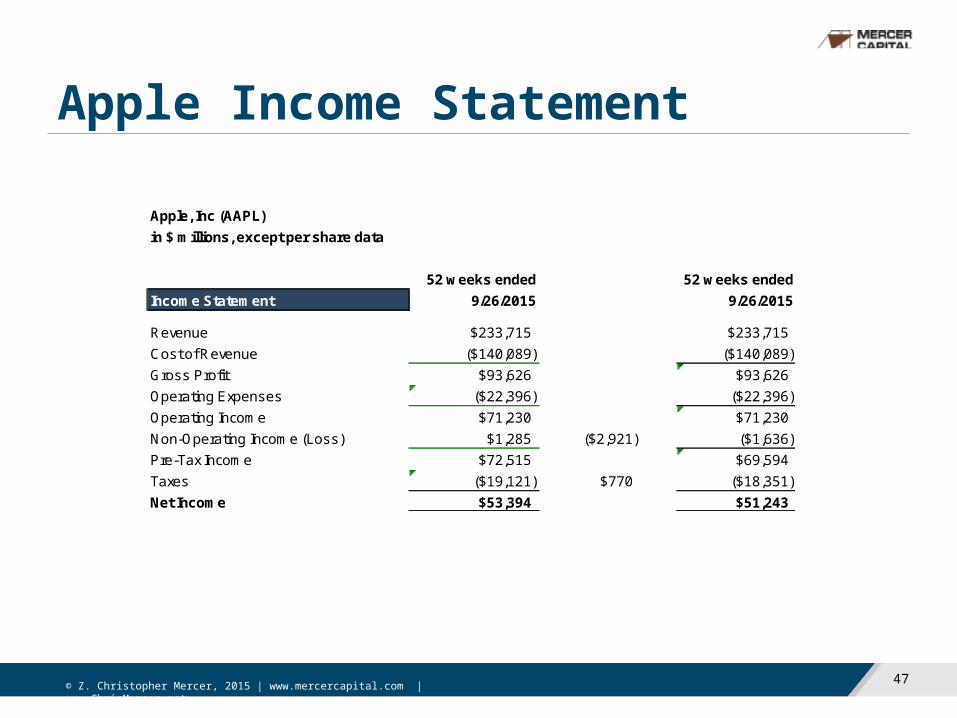

Apple Income Statement

Apple, Inc (AAPL)in $ millions, except per share data

52 weeks ended 52 weeks endedIncome Statement 9/26/2015 9/26/2015

Revenue $233,715 $233,715Cost of Revenue ($140,089) ($140,089)Gross Profit $93,626 $93,626Operating Expenses ($22,396) ($22,396)Operating Income $71,230 $71,230Non-Operating Income (Loss) $1,285 ($2,921) ($1,636)Pre-Tax Income $72,515 $69,594Taxes ($19,121) $770 ($18,351)Net Income $53,394 $51,243

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

48

Apple Shareholder Statistics

Shareholder Information Actual AdjustedShares Oustanding (millions) 5578.75 5578.75Price Per Share $114.71 $77.84Earnings per Share $41.89 $41.89Dividends Per Share $1.98 $38.85Book Value Per Share $4.91 $4.91Price/Earnings Multiple 2.74 1.86Price/Book Value 23.34 15.84Dividend Yield 1.73% 49.90%Dividend Payout Ratio 0.05 0.93Return on Equity 44.7% -59.4%

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

49

EBITDA Multiple

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

50

Public Markets Provide Context for Private Company Valuation

Consider Google (NASDAQ: GOOG). Its price changes every day. Often, there will be observable trends in the price.

We want to buy cheap and sell dear when we invest in public companies

• With private companies, there is no market for shares. Many private companies never obtain a business valuation (or appraisal), and little is known about value

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

51

Public Markets Provide Context for Private Company Valuation

With public companies there is a tension between reinvesting in the business for future growth and with returning money to shareholders, either in the form of dividends or stock repurchases or buybacks

• Private company values also change over time, even if no one is watching, i.e., even if there are no appraisals of a business. Private company values are a function of expected cash flows, expected growth, and risk, just like with public companies.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

52

Public Markets Provide Context for Private Company Valuation

Shareholders of public companies have access to enormous amounts of information about each company that provides, at least in concept, sufficient information for investors to make informed investment decisions

• Private companies have virtually no required public disclosure, or even shareholder disclosure. A bank may require that a lending client obtain an annual audit, but that is about the extent of required financial disclosure. Investors in most private companies, sometimes even significant owners, often lack good information about their company’s performance and value

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

53

Public Markets Provide Context for Private Company Valuation

Many sets of eyes are looking at most public companies

• Sell-side analysts

• Buy-side analysts

• Analysts at asset management firms

• Technical analysts

• Individual investors as analysts

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

54

Public Markets Provide Context for Private Company Valuation

Another result of all of this attention being paid to public companies.

An inherent discipline imposed on public companies to report their financial results and prospects and to run their companies for the benefit of shareholders.

• Private companies have no analysts following them. They provide little or no financial disclosure to shareholders or to anyone else. Bank credit analyst do look at the financial performance over time of significant lending customers of their banks. But that’s about it.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

55

Public Markets Provide Context for Private Company Valuation

Now, let’s take one final look at private companies in the context of this overview discussion of the context of public company pricing and valuation in the public markets

• The value of private companies, like that of public companies, is based on expectations regarding cash flow, growth and risk. Value is always future-based

• There are virtually no external analysts following or even looking at most closely held and family businesses, regardless of their size

• Value changes for private companies over time and with changes in external and internal conditions, even if no one is watching the change

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

56

Public Markets Provide Context for Private Company Valuation

We look at the focus on public company valuation for an important reason. When markets are public, there is keen focus on pricing and valuation from many differing viewpoints. When we think about the value of private companies, we will employ a bit of this public market viewpoint.

• Financial disclosure

• Analytical attention

• Value changes over time

The business valuations we do are the first step in applying basic corporate finance and market knowledge to help manage private company wealth.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

57

Discounted Cash Flow Method (DCF)

In theory, the DCF model requires a forecast of expected annual cash flows for every year after the valuation date into the indefinite future. Valuation is a perpetuity concept. The business is expected to continue to generate cash flows into perpetuity.

Algebraically and conceptually, the DCF model looks like this:

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

58

The Gordon Model

In a 1962 text, Professor Myron Gordon proved that the DCF equation above could be simplified to the following equation:

Two Key Assumptions

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

59

Two-Stage DCF Model

In the two-stage model, the analyst forecasts cash flows for a finite period of years, quite often five years (or three years or ten years). Conceptually, the two-stage DCF model looks like this:

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

60

Valuation Basics for Business Owners

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

61

(Net) Cash Flow

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

62

Growth and Risk Impact Multiples

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

63

Growth and Risk Impact MultiplesAssume that the discount rate is 15% and the expected growth rate for the long term is 5%. Doing a little math, we can determine that under these assumptions, the multiple, M, is 10x (i.e., 1 / (15% – 5%))

• Risk impacts the multiple and value. The discount rate, r, has a positive sign in the denominator. That means that if risk goes up, other things being equal, then value goes down. It works the other way as well. If risk goes down, other things being equal, then value will rise.

• Expected growth impacts the multiple and value. The growth rate, g, has a negative sign in the denominator. If the growth rate increases, the denominator gets smaller and the multiple rises. That’s why business appraisers and market participants focus on the outlook for growth when they are valuing companies.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

64

Growth and Risk Impact Multiples

Earnings = Net income, net cash flow, debt free net income / cash flow

Multiple = Build up, ACAPM, equity discount rate (R), WACC

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

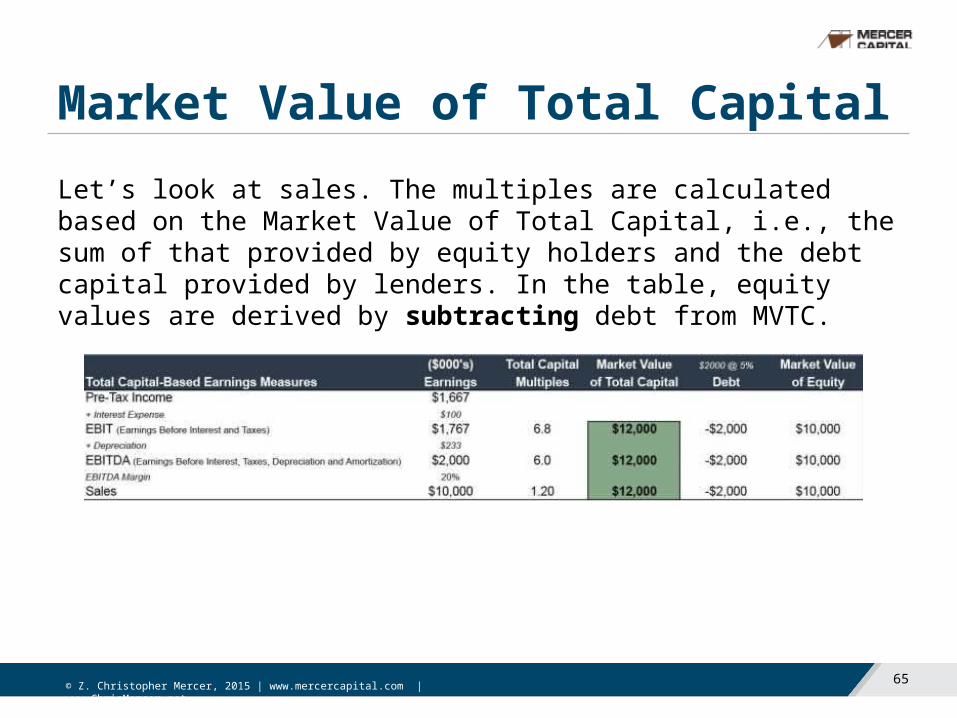

65

Market Value of Total CapitalLet’s look at sales. The multiples are calculated based on the Market Value of Total Capital, i.e., the sum of that provided by equity holders and the debt capital provided by lenders. In the table, equity values are derived by subtracting debt from MVTC.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

66

Building the Equity Discount Rate

Using the assumptions above, we can show the actual build-up of a discount rate in a table to make clear what we have done.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

67

Developing the Weighted Average Cost of Capital

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

68

Using the WACC in Valuation

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

69

MVTC, Enterprise Value, and MVEs

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

70

Is It Okay to Consider EBITDA?Can we look at EBITDA as an earnings measure to use in developing total capital value indications? Well, yes, and appraisers and market participants do so every day. Two commonly used valuation methods when valuing public (and private) companies are:

• The guideline (comparable) public company method, capitalizing EBITDA (or expected EBITDA) of a private company based on analysis of EBITDA multiples of similar publicly traded entities.

• The guideline transactions method, capitalizing EBITDA of a private company based on analysis of EBITDA multiples found in transactions involving the sale of similar companies.

Then we have the seemingly ubiquitous rules of thumb that, for example, companies in the widget-gadget industry trade in a range of 4.0x to 6.0x EBITDA, or so.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

71

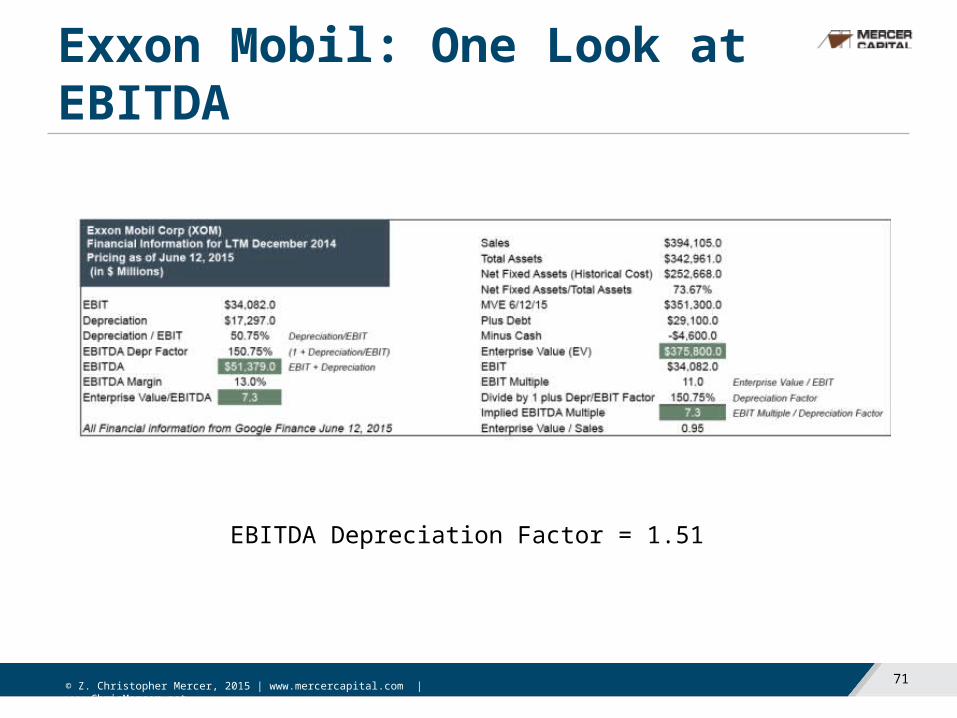

Exxon Mobil: One Look at EBITDA

EBITDA Depreciation Factor = 1.51

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

72

Apple: Another Look at EBITDA

EBITDA Depreciation Factor = 1.17

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

73

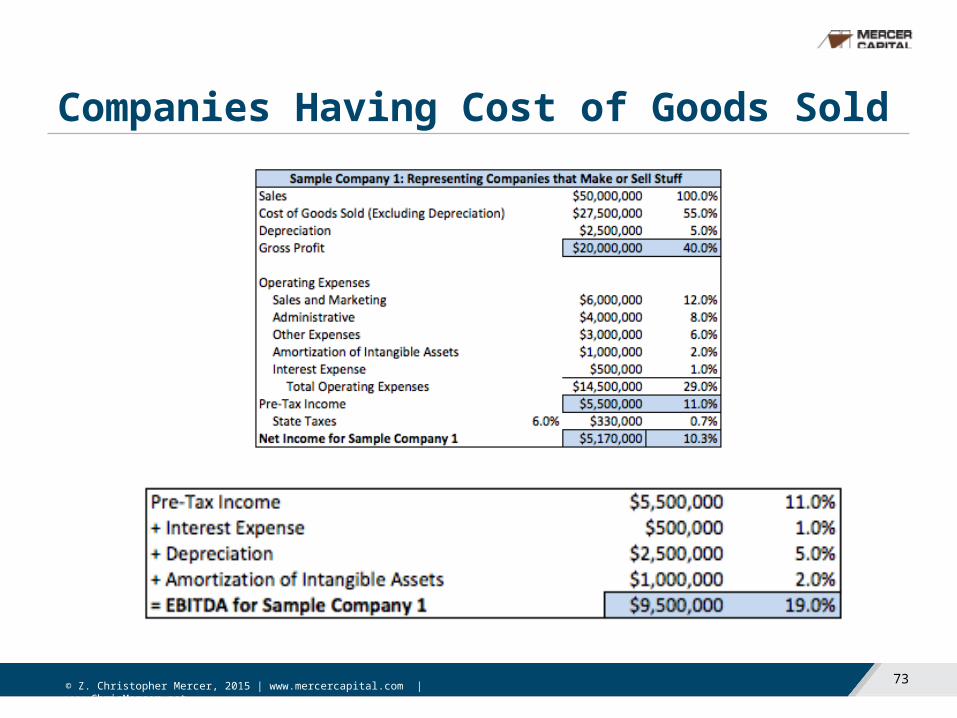

Companies Having Cost of Goods Sold

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

74

Companies That Deliver Services

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

75

What’s the Big Deal with EBITDA?

EBITDA is the topmost level of cash flow that is available (or not) for all of the reinvestments that are necessary to enable businesses to grow and to provide returns for owners.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

76

Debt Free Frequency Before and After Tax

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

77

For Every EBIT There is Depreciation

EBITDA Multiple for Exxon = 11.0x / 1.51 = 7.3x

EBITDA Multiple for Apple = 11.1x / 1.17 = 9.5x

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

78

Building EBITDA Multiples of Enterprise Value

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

79

Key Assumptions of the Analysis

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

80

Developing a Range of Implied EBITDA Multiples

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

81

Tradeoffs Between Expected Growth and Risk and the Impact on Value

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

82

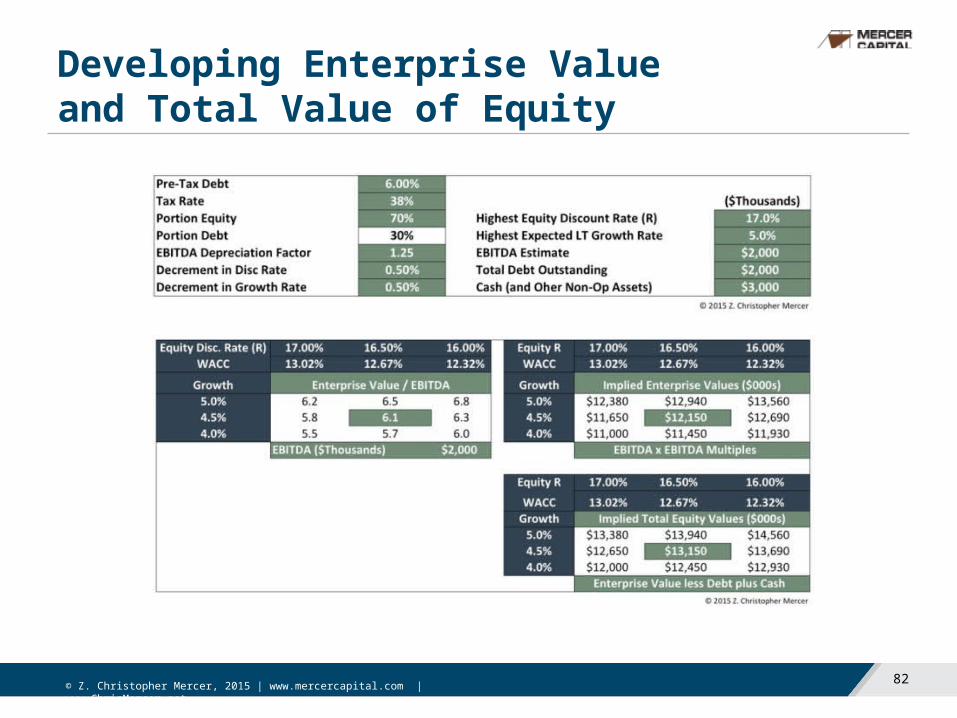

Developing Enterprise Value and Total Value of Equity

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

83

Relationship between Depreciation and EBIT

Depreciation is a non-cash expense that flows through the income statement in the process of deriving EBIT. Amortization is a similar non-cash expense.

Depreciation in any period is based on the existing stock of depreciable assets on a company’s balance sheet at the beginning of the period.

Amortization in any period is based on the existing stock of amortizable intangible assets on the balance sheet.

There is a relationship between EBITDA and EBIT that can be measured by looking at depreciation (and amortization) as a percentage of EBIT. For simplicity, let’s focus on depreciation. If EBIT is $1.0 million and depreciation is $300 thousand, depreciation expense is 30% of EBIT ($300m / $1,000m). Similarly, if depreciation is $500 thousand with the same EBIT, depreciation is 50% of EBIT.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

84

Relationship between Depreciation and EBIT

Depreciation is a proxy for the need for capital expenditures for a business. If there is a lot of depreciation, chances are there will be a need for significant capital expenditures to maintain the capital stock. If a company is growing, it would not be surprising for capital expenditures to exceed depreciation in a given period, or over time.

The ratio of depreciation to EBIT is a measure of the capital-intensity of a business. The higher the ratio, generally, the higher the level of capital-intensity.

We derive EBITDA by adding the D&A, or depreciation and amortization, to EBIT.

We calculate Depreciation as a percentage of EBIT (Depreciation/EBIT).

We then calculate the EBITDA Depreciation Factor by adding one to the result of the above quotient, or [1 + (Depreciation/EBIT)]

We calculate the EBITDA multiple by dividing the EBITDA Depreciation Factor into the base EBIT multiple derived by building up an EBIT capitalization rate – and multiple – for a particular company.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

85

Perspective on the EBITA Depreciation Factor

Depreciation can be thought of as one proxy for expected capital expenditures. It is not a perfect proxy, of course, but assume that for a company to grow, it must spend at least as much on capital expenditures in a year as the depreciation for that year. In other words, assume that a company’s capital stock is replenished by spending the cash flow created by its non-cash depreciation charges. We know that capex tend to be lumpy, but we can clearly infer something about capital intensity by examining the EBITDA Depreciation Factors.

If one company can spend a lower portion of its EBIT on capital expenditures than another, otherwise identical company, then it warrants a higher EBITDA multiple, since there’s more of EBITDA available for non-capex uses (taxes, additional reinvestment, and dividends or distributions).

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

86

Perspective on the EBITA Depreciation Factor

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

87

Public Market Perspectives

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

88

Private Market Evidence

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

89

ESOPs

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

90

Why Would You Use an ESOP for Liquidity?

If your company is similar to the kind of businesses described below, then you might want to consider an ESOP for partial (and, perhaps ultimately, total) liquidity for a number of reasons:

A properly structured ESOP can provide liquidity for a portion of an owner’s shares at a reasonable price

You do not sell to outsiders

Transparent financial management is necessary for the ESOP to succeed and for your employees to believe that it is a real benefit

The ESOP may provide time for smooth, internal management transitions

Contributions and distributions to an ESOP are tax-deferred (and ultimately taxable to employee beneficiaries), so a dollar of cash flow received pro rata is a dollar available to pay principal and interest on the ESOP’s debt

Because you didn’t sell to outsiders, the benefit of ESOP debt pay-down is allocated to employees

An ESOP provides a very real benefit for employees, especially for S corporation ESOPs

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

91

When Do ESOPs Work Best?Based on our experience in working with ESOPs for more than 30 years and with having an ESOP at Mercer Capital since 2006, ESOPs work best if the following conditions are met:

Companies are consistently profitable and have stable and, preferably, growing earnings

Companies do not require heavy reinvestment in working capital, fixed assets or plant and equipment to grow. Service companies, professional service companies, distribution companies with decent margins, non-cyclical manufacturing business, and others may fit the bill

The owner(s) who desire(s) to sell have an interest in staying with the company for at least a period of years and a smooth management transition plan is in place for the future

The owner(s) desiring to sell do not desire to sell all of their stock so that the ESOP can establish and the company can learn about the ESOP absent the pressure of leverage for 100% of the stock. Note that ESOP transactions of whatever size are usually leveraged 100%. It is just easier for the parties to get comfortable with and prove the concept with smaller transactions at the outset

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

92

ESOP Players

1. (Sponsoring) Company

2. ESOP Trust (ESOP)

3. Trustee of the ESOP Trust

4. Selling Shareholder(s)

5. Bank or Other Lender

6. Employee Beneficiaries

7. Plan Administrator

8. Business Appraiser

9. Attorneys

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

93

ESOP Process v

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

94

Mercer Capital’s ESOP

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

95

Questions?

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

96

Unlocking Private Company Wealth

ChrisMercer.net/books

Purchase Unlocking Private Company Wealth

When ordering from website, receive a PDF of complimentary resources

• Buy-Sell Agreements for Closely Held and Family Business Owners

• The Buy-Sell Agreement Review Checklist

• Checklist for Shareholder Promissory Notes

1 - 4 books | $25.00 per5 - 24 books | $20.00 per25 - 49 books | $19.00 per50 - 99 books | $18.00 per

100 - 199 books | $16.00 per200 - 499 books | $15.00 per500 - 999 books | $12.50 per1,000+ books | $10.00 per

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net

97

Z. Christopher Mercer, ASA, CFA, ABAR

www.MercerCapital.comwww.ChrisMercer.netlinkedin/in/zchristophermercer

Mercer Capital5100 Poplar Ave., Suite 2600Memphis, TN 38137

Chris Mercer is the founder and CEO of Mercer Capital, a national business valuation and financial advisory firm.

Chris began his business valuation career in the 1970s and has been involved with hundreds of valuations for purposes related to mergers & acquisitions, litigation, and estate and gift tax planning, among others. He has extensive experience in litigation engagements including statutory fair value cases, business damages, and lost profits. He is also an expert in buy-sell agreement disputes.

Designations held include Accredited Senior Appraiser (ASA) from the American Society of Appraisers, Chartered Financial Analyst (CFA) from the CFA Institute, and Accredited in Business Appraisal Review (ABAR) from the Institute of Business Appraisers.

Chris has written widely on business valuation-related topics and is a frequent speaker on business valuation issues for national professional associations, other business and professional groups, and business owners.

Recent books authored by Chris include Unlocking Private Company Wealth (Peabody Publishing, LP 2014), Buy-Sell Agreements for Closely Held and Family Business Owners (Peabody Publishing, LP 2010) and Business Valuation: An Integrated Theory, 2nd Edition, with Travis W. Harms (John Wiley and Sons 2008).

For a complete list of the books authored by Chris, as well as further information on his valuation-related experience, view his complete CV at www.mercercapital.com.

© Z. Christopher Mercer, 2015 | www.mercercapital.com | www.ChrisMercer.net