Private Client Group - RBC · Private Client Group RBC Dain Rauscher TSX / NYSE: RY ... 2 Morgan...

20

Private Client Group Private Client Group Charley Grose President Private Client Group RBC Dain Rauscher TSX / NYSE: RY Presentation to analysts and institutional investors Toronto - June 18, 2003

Transcript of Private Client Group - RBC · Private Client Group RBC Dain Rauscher TSX / NYSE: RY ... 2 Morgan...

Private Client GroupPrivate Client Group

Charley GrosePresident Private Client GroupRBC Dain Rauscher

TSX / NYSE: RY

Presentation to analysts and institutional investorsToronto - June 18, 2003

2

Who we areWho we are

1,213Raymond James Financial101,322Legg Mason9

1,945**RBC Dain Rauscher85,384A.G. Edwards78,595Edward Jones68,801UBS Paine Webber5

12,000+*Wachovia Securities412,927Salomon Smith Barney313,191Morgan Stanley Dean Witter215,147Merrill Lynch1

Estimated Number of U.S. BrokersCompanyRank

Source: SIA Yearbook (Jan. 2002) *Pending completion of merger with Prudential** Currently 1,850

3

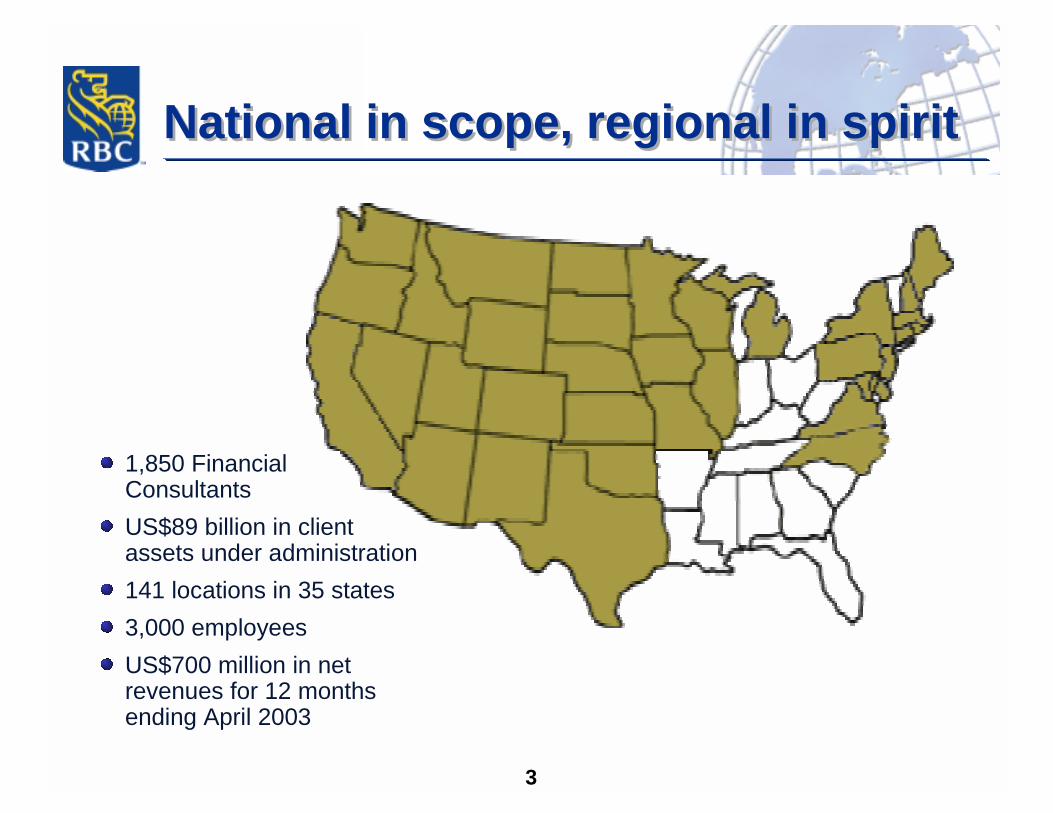

National in scope, regional in spiritNational in scope, regional in spirit

1,850 Financial ConsultantsUS$89 billion in client assets under administration141 locations in 35 states3,000 employeesUS$700 million in net revenues for 12 months ending April 2003

4

Key prioritiesKey priorities

Performance

Execution of strategy

Future profitability

5

PerformanceCost cuttingPerformanceCost cutting

Market values, economic growth and investor activity in declineTactical measures required to maintain profitability

Note: Historical revenues include pro forma Tucker Anthony Sutro results

PCG Quarterly Revenue & Market Trend

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

Q1/

00

Q2/

00

Q3/

00

Q4/

00

Q1/

01

Q2/

01

Q3/

01

Q4/

01

Q1/

02

Q2/

02

Q3/

02

Q4/

02

Q1/

03

Q2/

03

(US$

in th

ousa

nds)

-

200

400

600

800

1,000

1,200

1,400

1,600

PCG NetRevenue

S&P 500(right scale)

6

PerformanceCost cuttingPerformanceCost cutting

225 corporate support job eliminations

down 18% from TAS close to April 2003*92 reduction in force effective April 2003

Retail branch office support staff reduction

194 in past year** 73 in April 2003revenue per branch support employee up 11% from 2001

300,000 ft2 reduction in real estate portfolio

US$10 million in annual rent reductionmajor market projects in process to cut US$2 - $5 million in future rent

Cost containmenthiring and salary freezediscretionary spending

* Pro forma, including Tucker Anthony Sutro** Excludes branch closings

7

PerformanceFuture expensesPerformanceFuture expenses

$44

$30

$14

$0

$70

2002 2003E 2004E 2005E 2006E

(in U

S$ m

illio

ns)

Acquisition retention compensation trend (pre-tax)

8

PerformancePositioned for leveragePerformancePositioned for leverage

($60)

($102)

$Annual Change

$111

$193

Q220011

Platform costs2

Net revenue

in US$ millions

PCG cost takeout impactPCG cost takeout impact

($15)

($26)

$ Change

-13%$96

-13%$167

%Change

Q22003

1 Pro forma including TAS historical results2 PCG costs including Dain corporate support allocations, but excluding FC commissions,settlements, acquisition retention, and parent company allocations

9

Strategy executionStrategy execution

Attract and retain the very best people

Know our clients and meet their needs

Provide excellent service

Grow strategically

10

Enhanced sales productivityReplacing low revenue producing FCs with higher producing FCsIncreased leverage on fixed costs over time

(93)11(104)Net change

4

(24)

28

(144)

51

Total

15

(5)

20

(9)

20> $400k

(11)

(19)

8

(135)

31< $400k

Revenue production per FC

Net change (US$ MM)

Annual revenue departed (US$ MM)

Annual revenue recruited (US$ MM)

Financial Consultants departed

Financial Consultants recruited

Fiscal Q2 Year-to-date Recruiting vs. Attrition Data

Strategy execution1: Attract and retain the best Strategy execution1: Attract and retain the best

11

Attractive compensation levels for highly productive FCs

Compensation fair to the firm

Deferred compensation good for FC and firm

Strategy execution1: Attract and retain the best Strategy execution1: Attract and retain the best

12

Strategy execution2: Meet client needsStrategy execution2: Meet client needs

13

15%

-13%-15%-30%

All Dain

All Participants

Top 25% of Participants

1st Wealth Management ClassChange In revenue(June 2001 – December 2002)

S&P 500 Index

Strategy execution2: Meet client needsStrategy execution2: Meet client needs

14

Fee-based and mutual fund products align FC and client interests

Fixed income partnership+

Diversified product mix smoothes revenue over the cycle

PCG commission revenue mix1

50%33%

15%26%

21%17%

19%6% 6%8%

1998 2002OtherFee-BasedMutual FundsFixed IncomeEquities

1 Excludes net interest, cash and house fee revenue

Strategy execution2: Meet client needsStrategy execution2: Meet client needs

15

2002 survey results

High client satisfaction ratings to Dain and to FCtop 10% of clientsease of doing business with

High ratings from FCswork environment Ease of doing business with

Strategy execution3: Provide excellent serviceStrategy execution3: Provide excellent service

16

Appointed director of servicekey initiatives focus on servicestreamline processes, e.g., account opening

Strategy execution3: Provide excellent serviceStrategy execution3: Provide excellent service

17

Strategy execution3: Provide excellent serviceStrategy execution3: Provide excellent service

Sales leadership in branchesMitigates riskImprove ability to manage business and execute strategy

18

Strategy execution4: Grow strategicallyStrategy execution4: Grow strategically

Leverage RBC’s U.S. platform Focus resources and capital Expand in key markets

CaliforniaTexasNew YorkMassachusetts

Bolt-on acquisitions

19

Future profitabilityFuture profitability

We have materially reduced our cost structureThe platform can be leveragedOne-fourth of PCG’s revenues are fees tied to AUMCustomer leverage is historically low

Estimated Incremental Operating NIAT for RBC

$18$13

$8

$0

$5

$10

$15

$20

$25

10% 20% 30%PCG Revenue Growth vs. Q2 2003

Qua

terly

NIA

T (U

S$)

20

Key takeawaysKey takeaways

Attractive industry positionProactive measures to reduce costs and increase profits in difficult market environmentExecuting strategy for long-term growth and profitabilityPoised for margin expansion upon market recovery

![FIS for the RBC/RBC Handover...4.2.1.1 The RBC/RBC communication shall be established according to the rules of the underlying RBC-RBC Safe Communication Interface [Subset-098]. Further](https://static.fdocuments.in/doc/165x107/5e331307d520b57b5677b3fa/fis-for-the-rbcrbc-handover-4211-the-rbcrbc-communication-shall-be-established.jpg)