Prime Minister at Nikkei Conference, Japan - The Board of

12

Prime Minister Yingluck Shinawatra led a delegation to visit Japan on 22-25 May 2013, and took the opportunity to explain to the audience Thailand’s major investment plans and how both countries would benefit. She said that Japan is now the largest group of foreign investors in Thailand. Apart from the automotive industry, Thailand invites Japanese business people to invest more in energy development and agricultural processing in Thailand. The Prime Minister pointed out that Japan invested in the Laem Chabang deep-sea port on Thailand’s Eastern Seaboard 20 years ago and that it should place additional investment in the planned Dawei deep-sea port in Myanmar, as well. The Dawei deep-sea port will link with Laem Chabang and will also offer great business opportunities. In her keynote address at the Nikkei Conference on the Future of Asia, held in Tokyo on 24 May, Prime Minister Yingluck cited the apparent and continuing progress and prosperity of the Asia-Pacific. She indicated that “Asian innovation and creativity, together with a productive workforce supported by new technology, will promote sustainable growth for the region”. Moreover, over the past 20 years there has been closer and effective partnership in the economic arena with the establishment of organizations like the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation and of forums such as the Asia Cooperation Dialogue. Prime Minister at Nikkei Conference, Japan CONTENTS June 2013 Volume 23 No. 06 Page Cover Story 1 News Bites / BOI Net Applications 2 North East India Investment Cooperation 4 BOI Extends Certain Investment Policies 6 NESDB Q1 Performance and Outlook 2013 7 Alternative Energy 8 Global Consumer Confidence on the Rise 10 Jetro Surveys Service Industry 10 Framework for Thailand’s Economic Stability 2013 11 2014 National Budget 11 Thailand Economy-At-A-Glance 12 Continued on P. 3

Transcript of Prime Minister at Nikkei Conference, Japan - The Board of

Prime Minister Yingluck Shinawatra led a delegation to visit Japan on 22-25 May 2013, and took the opportunity to explain to the audience Thailand’s major investment plans and how both countries would benefit. She said that Japan is now the largest group of foreign investors in Thailand. Apart from the automotive industry, Thailand invites Japanese business people to invest more in energy development and agricultural processing in Thailand. The Prime Minister pointed out that Japan invested in the Laem Chabang deep-sea port on Thailand’s Eastern Seaboard 20 years ago and that it should place additional investment in the planned Dawei deep-sea port in Myanmar, as well. The Dawei deep-sea port will link with Laem Chabang and will also offer great business opportunities.

In her keynote address at the Nikkei Conference on the Future of Asia, held in Tokyo on 24 May, Prime Minister Yingluck cited the apparent and continuing progress and prosperity of the Asia-Pacific. She indicated that “Asian innovation and creativity, together with a productive workforce supported by new technology, will promote sustainable growth for the region”. Moreover, over the past 20 years there has been closer and effective partnership in the economic arena with the establishment of organizations like the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation and of forums such as the Asia Cooperation Dialogue.

Prime Minister at Nikkei Conference, Japan CONTENTS

June 2013 Volume 23 No. 06

Page

Cover Story 1

News Bites / BOI Net Applications 2North East India Investment Cooperation 4

BOI Extends Certain Investment Policies 6NESDB Q1 Performance and Outlook 2013 7

Alternative Energy 8Global Consumer Confidence on the Rise 10

Jetro Surveys Service Industry 10Framework for Thailand’s Economic Stability 2013 11

2014 National Budget 11Thailand Economy-At-A-Glance 12

Continued on P. 3

NEWS BITES BOI NET APPLICATIONSGovernment’s Medical Hub Plan Focuses on Private Hospitals

The Government, in its medical hub plan, will serve as a facilitator for private hospitals, helping them to improve their medical services to foreign visitors seeking health care in Thailand.

According to Public Health Minister Pradit Sinthawanarong, in 2012 almost one million foreign visitors entered Thailand for health care, bringing in 140 billion baht. The number of medical tourists visiting Thailand is on the rise. In facilitating their trips to Thailand, the Government has granted visa extensions from 30 days to 90 days for nationals of six countries in the Middle East in the initial stage, so that they can stay in Thailand for a longer period for medical services. Visa extensions will later be granted to medical tourists from other countries.

The Government has set a target for medical tourism to grow by 10 percent a year, depending on the ability of private hospitals. To date, many private hospitals have been recognized and approved as meeting the standards set for the Hospital Accreditation of Thailand and international standards, such as ISO.

In developing Thailand into a regional medical hub, the Government will emphasize four areas. In the first area, Thailand will be promoted as a wellness hub with full-cycle services. The second area is that the medical service hub will link with spa services and health tourism. The third area seeks to turn Thailand into an academic hub for health care. The fourth area seeks to develop Thailand into a pharmaceutical and health products center.

Thailand and the United Kingdom Agree to Further Promote Investment-Friendly Conditions

Thailand and the United Kingdom have agreed to further promote investment-friendly conditions, as well as to eliminate trade impediments and ease necessary regulations.

The agreement was reached at the first session of the Thailand-United Kingdom Strategic Dialogue, held at the Ministry of Foreign Affairs in Bangkok on 20 May 2013.

On the economic front, the two sides reviewed the growing two-way trade and investment, where the United Kingdom continues to be one of Thailand’s largest trading partners in the European Union. Both sides shared the view that the current bilateral trade volume could be increased substantially. The meeting suggested that both Governments look into doubling the current bilateral trade volume by 2018.

The two delegations also welcomed the signing of the MOU on SME Cooperation between the Office of SME Promotion and United Kingdom Trade

and Investment (UKTI), which is aimed at promoting collaboration between Thai and British SMEs, as well as the MOU between the Royal Mint and the Royal Thai Mint to enhance Thailand’s capacity in becoming a regional hub for production and distribution of coins.

2011(US$ = 31.68THB)

2012 (Jan-Mar)(US$ = 30.69THB)

2013 (Jan-Mar)(US$ = 29.51THB)

Number of projects Value Number of

projects Value Number of projects Value

Total Investment 2,584 47,586 443 7,207 610 9,318

Total Foreign Investment 1,584 20,849 312 4,371 338 5,343

By Sector

Agricultural Products 85 1,042 13 319 32 621

Minerals / Ceramics 34 514 7 109 12 306

Light Industries / Textiles 80 1,097 19 286 16 51

Automotive / Metal Processing 532 7,541 91 895 109 2,170

Electrical / Electronics 289 5,021 73 1,570 57 497

Chemicals / Paper 228 2,707 52 648 41 306

Services 336 2,926 57 545 71 1,390

By Economy

Japan 872 12,033 173 2,541 176 2,964

Europe 166 1,724 41 511 36 364

Taiwan 53 285 13 38 14 126

USA 53 795 17 297 24 147

Hong Kong 72 1,695 6 175 10 516

Singapore 134 871 25 164 20 182

By Zone

Zone 1 417 2,660 82 960 102 790

Zone 2 922 15,101 172 2,506 165 2,970

Zone 3 245 3,088 58 905 71 1,582

Unit: US$ MillionNote: Investment projects with foreign equity participation from more than one country are reported in the figures for both countries.

June 2013

Page 2

Continued from P. 1

Despite the diversity of the Asia-Pacific, it is imperative that governments work together on promoting greater flow of goods, services and people between their respective countries. With that in mind, Prime Minister Yingluck highlighted railways as the most effective and efficient approach to actualizing economic integration throughout the region. She proposed that Asia should direct its investments to build connectivity, both on land and sea, since Asia is mostly a large land continent bordered by two oceans, the Indian and the Pacific. From ASEAN in Southeast Asia, logistics/transportation corridors must be built to North and Northeast Asia, and on the opposite end, to South Asia, Central Asia, and the Middle East. A modern Silk Road to connect the region with high speed trains, and feeder tracks for cargo and passengers will become the new Asia-Euro land bridge linking the two continents, while opening up new growth areas along the way.

Thailand intends to pour money into mega-infrastructure projects in pursuit of a more productive economy. This course of action will propel Thailand’s full transformation into a newly industrialized country – an Asian dynamo of the 21st century. Furthermore, the Kingdom seeks to be Japan’s gateway for investment in Southeast Asia. Japan is already Thailand’s biggest source of foreign direct investment, and the two countries have excellent diplomatic and economic relations, Yingluck pointed out. Also, the Prime Minister said she hopes for expanded investment and cooperation from Japan in railway construction technology and other industrial sectors, such as energy and food processing.

Soon after Yingluck took office in the summer of 2011, the Thai economy came to a virtual standstill as flooding swept much of the central part of the country. But growth rebounded last year to a robust 6.4%, due in large part to voracious domestic spending and a healthy manufacturing sector. Prime Ministeer Yingluck stated that the economy is expected to maintain growth at around 4.5-5.5% in 2013. To ensure longer-term growth, her government will devote itself to strengthening the Kingdom’s economic foundations. Thailand will spend 2.2 trillion baht (US$75.1 billion) -- roughly equivalent to its annual budget -- on infrastructure over the next seven years.

Thailand hosts the biggest concentration of Japanese businesses in Southeast Asia. About 4,000 Japanese firms operate in the country, and Japan provides more than 40% of the country’s FDI. Prime Minister Yingluck described both the infrastructure plan and the water resource management project as an opportunity that will deliver major benefits for Japanese companies and further deepen bilateral economic linkages. One major endeavor will likely be the construction of four high-speed rail lines connecting Bangkok with other key cities across the Kingdom and beyond. Japan, China, South Korea and France are among the countries vying to provide rail-car systems for the project. Prime Minister Shinzo Abe made a sales pitch for Japanese shinkansen bullet train technology while on a trip to Thailand in January this year.

Thailand has been an outspoken advocate of free trade both within the Association of Southeast Asian Nations and elsewhere. The Prime Minister stressed that the Kingdom still has great potential to grow as a hub of trade and investment in the region. Stronger transportation links with neighboring countries, she mentioned, would give businesses easy access not only to Thailand’s 60 million people but also to the 600 million living in the entire ASEAN region. Plus, the scheduled inauguration of the ASEAN Economic Community in December 2015 will transform not only Southeast Asia but also will have an impact upon the entire Asia-Pacific as the region will serve as a genuine bridge between the thriving markets of South Asia and Northeast Asia.

Thailand stands to gain immensely from the launching of the AEC yet steps must be taken now in order to prepare for the country’s integration into this regional bloc.

Meanwhile, in cooperation with the Organization for Small and Medium Enterprises and Regional Innovation – Japan (SMRJ), the Thailand Board of Investment organized a Thai-Japanese SME seminar in parallel with the Prime Minister’s recent visit to Japan. This event was held on the 23rd of May at the Okura Hotel in Tokyo and was well-attended with more than 200 Japanese companies participating. H.E. Prasert Boonchaisuk, Minister of Industry, opened the seminar together with Mr. Hiroshi Takada, Chairman and CEO of SMRJ. Equally important, the occasion featured speeches from leading figures of the Thai economy such as Mr. Viroj Siritanasat, President of the Alliance for Supporting Industries Association, Mr. Seubtrakul Binthep, Managing Director of Single Point Parts (Thailand), Mr. Narong Sakulsirirat, Managing Director of NR Industry, and Mr. Tan Passakornnatee, Managing Director of Ichi Tan Group. These four speakers from the Thai private sector represented Auto Parts and Mold & Die, Machinery & Parts, Electrical and Electronics, and Food. It is worth mentioning that these industries are an integral part of the BOI’s campaign to attract Japanese SMEs and to match them with Thai SMEs. Indeed, the speakers indicated the rapid development of Thai subcontractors and their readiness to partner with Japanese companies. Such collaboration with Thai SMEs would benefit greatly Japanese enterprises as they would be able to concentrate on production in their areas of specialization.

During the networking reception that followed the seminar both sides had much interaction with free-flowing conversation and the exchange of business cards. In fact, a number of Japanese SMEs requested a visit to Thailand on the spot, showing their interest in establishing a presence in the Kingdom.

June 2013

Page 3

The Asia-Pacific is a part of the world that continuously has experienced dynamic change and reinvention, particularly since the late 1980s. Indeed, the forces of globalization and regional integration have been at the forefront of this transformation. As such, national governments, companies and individuals search for both investment and business opportunities around the world that, in turn, create linkages between them and facilitate the establishment of a “global marketplace”. Thailand is a country that has reaped the benefits of and has been a proponent of greater economic connectivity both across the Asia-Pacific and beyond. Moving up the development ladder, the Kingdom finds itself confronted with a plethora of choices when it comes to launching and intensifying its trade and commercial relations. When looking at a map of Southeast Asia India is a logical choice, especially India’s inviting North East.

A high-profile delegation from North East India, led by H.E. Mr. Nilamani Sen Deka, Minister of Agriculture, Horticulture and Food Processing, Government of the State of Assam, gave a series of informative presentations on the key economic features of North East India and the region’s unique business opportunities. The event was organized by the Thailand Board of Investment at the Grand Hyatt Erawan Hotel on the 9th of May 2013. Both Ms. Vassana Mututanont, Deputy Secretary General, Thailand Board of Investment, and Mr. Visit Limprana, Vice President, Federation of Thai Industries, attended and spoke about the burgeoning bilateral economic relationship between Thailand and India. Afterwards there was a business networking reception that was hosted by the Thailand Board of Investment. Mr. Udom Wongviwatchai, Secretary General, Thailand Board of Investment welcomed the delegation.

Thailand: North East India Investment Cooperation Seminar and Business Networking Reception

What was the purpose of the seminar? And what are the attractions of North East India to Thai businesses and investors?

It was mentioned that expanding and deepening trade and investment relations between Thailand and India are a priority for the governments of both countries. Indeed, the benefits of greater cooperation far outweigh the risks. As such, a crucial step that must be taken is the improvement and construction of a transnational transportation and logistics network that connects the Thai and Indian markets together. This enterprise would open the door of opportunity for the Thai private sector, particularly construction companies that specialize in infrastructure projects. Moreover, Thai trucking firms and airlines would stand to gain from increased bilateral trade and commercial traffic. Besides construction, other sectors of the North East Indian economy that have opportunities for Thai investors are food processing, energy (oil and gas), and tourism. In fact, since the formation of a free trade agreement between Thailand and India in September 2004, through an early-harvest scheme, economic connectivity has risen across the board. Interestingly, the Thailand Board of Investment will celebrate the opening of a new office in India’s financial hub of Mumbai this June.

Regarding North East India, the region is a prospective hub of international trade and commerce. It comprises of the Seven Sister States of Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland and Tripura. Also included is the Himalayan state of Sikkim. The geographic proximity of North East India to Asia’s fastest growing economies (e.g. China) heightens the region’s appeal to potential foreign businesses and investors.

June 2013

Page 4

Indeed, the region nowadays is being seen as an important and attractive market and soon will be linked with other Asian countries through the trilateral highway project between India, Thailand and Myanmar. Agreement for this development scheme was reached in 2009. It will enhance physical connectivity and provide opportunity for Thai construction firms to pursue joint ventures with Indian partners in upgrading the transportation system as well as air transport, telecommunication and IT logistic services. Furthermore, this artery going through Myanmar not only will bond North East India to the Thai market but also will open the way to other ASEAN members. As such, it will play a crucial role in boosting trade and investment flows amongst the three countries and creating jobs.

With the possibilities of the ASEAN Economic Community fast approaching in 2015, India, Myanmar, and Thailand stand to gain immensely as the three countries will reinforce each other’s respective strengths. It is for this reason that connectivity is at the core of Thailand’s foreign economic strategy concerning the Asia-Pacific. In fact, the convergence of New Dehli’s “Look East” policy of 1993 and Bangkok’s “Look West” policy since 1996 has resulted in mutually beneficial cooperation covering diverse dimensions ranging from trade and investment, science and technology, defense, agriculture to tourism, culture and education. Thailand today is actively involved in cultivating closer economic ties with its western neighbors, such as Myanmar, Bangladesh, India, Sri Lanka, and Nepal, as well as with the greater Middle East. Similarly, for India a tilt towards the “East” means developing its trade and commercial relations with China, South Korea, Japan, and ASEAN member countries as well as with Australia and New Zealand. At the crossroads of this “Look West-Look East” policy approaches lies North East India.

The delegation from North East India throughout their individual presentations highlighted a number of key features that make the region a logical choice for Thai businesses and investors to establish a foothold. First, it is a part of India that is rich in natural resources such as minerals (coal, iron ore, limestone, granite) and biodiversity. Secondly, land fertility is good and there is an abundance of water as the region is dominated by the Brahmaputra River valley. Additionally, the climatic conditions of North East India favor cultivation of a wide range of plantation crops. Thirdly, there is to be found a qualified and skilled manpower base in the region that can be employed at a competitive cost. Finally, there is a social and cultural affinity between Thailand and North East India. The region, especially

the State of Assam, is home to a large and vibrant Tai Ahom community. Tai Ahom are descendants of the ethnic Tai people that accompanied the Tai prince Sukaphaa into this corner of the Indian subcontinent in 1228 and ruled the area for six centuries until 1826. The current Chief Minister of Assam, H.E. Mr. Tarun Gogoi, is from the Tai Ahom family.

Yet, more importantly, there are numerous investment and business opportunities for Thai companies and entrepreneurs to explore. For instance, agri-horticulture (rice, fruits, vegetable, plants, spices), water management (irrigation and flood prevention), construction (highways, bridges, canals, factories, warehouses, hotels, housing), power generation (electricity), food processing (for both the domestic and overseas markets), and tourism are sectors wherein Thai capital and expertise can prosper. Accordingly, the Union Government of India has put together an

attractive incentive package for investment in North East India known as North East Industrial and Investment Promotion Policy (NEIIPP) 2007-2017. The incentives are such as 100% income tax exemption, capital investment subsidy that covers 30% of investment in plants and machinery without ceiling limit, a 100% excise duty exemption for 10 years as well as a transport subsidy of 90% from Siliguri (gateway to North East India) to point of production for both raw materials and products and a 50% transport subsidy within North Eastern Region etc.

In addition, the State of Assam offers an additional incentive package that includes the following points:

• VAT exemption for 7 years• Interest subsidy on term loans• Financial assistance for power utilization• Subsidy on quality certification / technical know-how• Special government enticements for mega infrastructure

projects

The delegation from North East India over the course of the presentation stressed the value of joint marketing of products and ventures in order to improve the region’s economic links with Thailand. In the end, as was mentioned frequently during the seminar, the overriding goal is sustainable bilateral cooperation.

Interestingly, bilateral trade between India and Thailand has grown substantially to a margin of 74 billion baht in Q1 2013. Presently, Thailand is ranked by the Thailand Ministry of Commerce as the 38th largest investor in India with an FDI outflow to India about US$ 111.10 million with most of these investment going into machinery, car sector, frozen food, livestock and construction. On the other hand, India invested about 18.2 billion baht in Thailand last year mostly in chemicals, papers plastics, metal products and automobiles. Nonetheless, New Delhi and Bangkok need to focus more specifically on North East India, which has a geographical area of only about 8 percent of India’s total land mass but is equal to about half the size of Thailand. Moreover, this part of India is well connected by a dense network of railways, surface roads and airports. Indeed, all the presenters emphasized that the region is open for business and ready for improved land, air, and sea connectivity with Thailand.

Mr. Udom Wongviwatchai, BOI Secretary General, welcomes Northeast India delegation

June 2013

Page 5

BOI Extends Certain Investment PoliciesThe Thailand Board of investment is in the process of revising its investment promotion policies, but in the meantime it has already revised several individual policies. These include extending the investment promotion measures for companies listed on the Stock Exchange of Thailand (SET) and the Market for Alternative Investment (MAI). These measures had expired on 31 December 2012, but have now been extended until December 31, 2013.

The BOI is also granting import duty exemption on moulds and dies that cannot be manufactured in Thailand (according to the list below) until December 31, 2013.

To facilitate promoted foreign juristic persons to own land for the establishment of offices and residences of investors and workers as well as support the economic stimulation policy and growth in real estate sector, the land ownership policy which had expired on 31 December 2012 has been extended to December 31, 2017.

Investors should visit www.boi.go.th and go to BOI announcements section for further detail. (BOI announcement No. 1/2556 dated 28 February 2013)

(Unofficial Translation) List of Moulds and Dies Eligible for Import Duty Exemption

Type of Mould and Die Name of Mould and DiePlastic Injection Mould High Precision Injection Mould (with tolerance of less than 10 micrometres)

Injection Mould that can create more than 3 colors in 1 workpiece Stack Mould Cube Mould Automation Transfer Insert Injection Mould Injection Mould for packaging that is less than 0.5 millimeter thickIn-Mould Transfer Film In-Mould Labelling

Sheet Metal Press Die Progressive DieTransfer DieSingle Die with tolerance of less than 10 micrometres Single Die for high tensile workpiece (with tensile strength of 590 MPa. or more)

Rubber Mould Rubber Mould with tolerance of less than 20 micrometres Transfer Rubber Mould with tolerance of less than 20 micrometres

Diecasting Mould Diecasting Mould with tolerance of less than 50 micrometres Jig Fixture Jig Fixture with tolerance of less than 10 micrometres

Press Release May 22, 2013: Progress on New Investment Promotion Policy Formulation

• BOI has scheduled the timeframe to announce the new BOI investment promotion policy in December 2013. The new policy is expected to be effective from Jan 1, 2015 onwards. This will allow sufficient time for investors to adjust themselves.

• 10 groups of target industries to be promoted include: » Basic infrastructure and logistics » Basic industry » Medical devices and scientific equipment » Alternative energy and environmental services » Services that support industrial sector » Advance core technologies » Food and agricultural processing industry » Hospitality & Wellness » Automotive and other transport equipment » Electric and electrical appliances

• Promotion by zones will come to an end in order to promote New Regional Clusters.• New incentives consist of basic incentives as well as additional merit-based incentives.

June 2013

Page 6

Quarterly GDP Growth2012 2012 2013

Q1 Q2 Q3 Q4 Q1Agriculture 3.1 3.4 1.8 8.3 3.1 0.5Non agriculture 6.7 0.1 4.7 2.7 21.2 5.8GDP 6.4 0.4 4.4 3.1 19.1 5.3

Source: NESDB

Number of Foreign Tourists (1,000 Persons)2012 2012 2013

Q1 Q2 Q3 Q4 Q1Asian 12,525 2,820 2,849 3,306 3,550 3,624

European 5,651 1,933 952 1,028 1,738 2,132Others 4,178 989 1,077 1,020 1,092 1,073Total 22,354 5,742 4,878 5,354 6,380 6,829Growth rate y-o-y(%) 16.2 8.1 9.8 8.6 40.4 18.9

Sources: office of Tourism Development, Ministry of Tourism and Sports

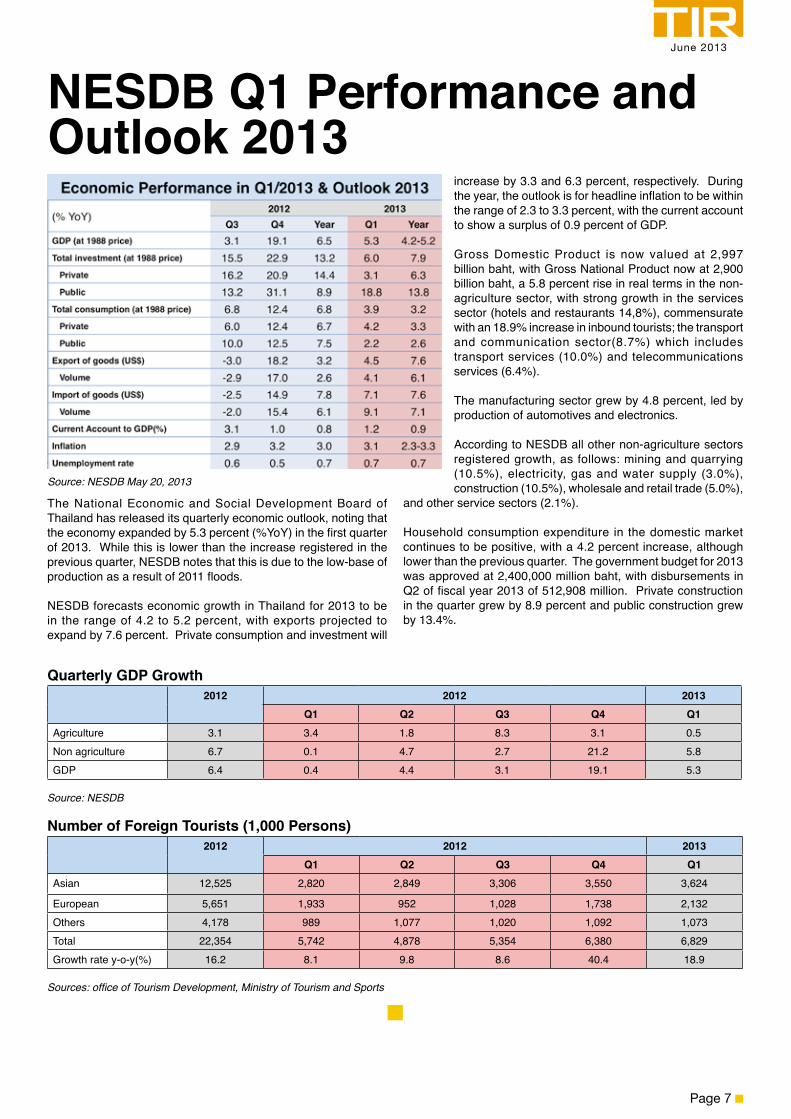

NESDB Q1 Performance and Outlook 2013

The National Economic and Social Development Board of Thailand has released its quarterly economic outlook, noting that the economy expanded by 5.3 percent (%YoY) in the first quarter of 2013. While this is lower than the increase registered in the previous quarter, NESDB notes that this is due to the low-base of production as a result of 2011 floods.

NESDB forecasts economic growth in Thailand for 2013 to be in the range of 4.2 to 5.2 percent, with exports projected to expand by 7.6 percent. Private consumption and investment will

increase by 3.3 and 6.3 percent, respectively. During the year, the outlook is for headline inflation to be within the range of 2.3 to 3.3 percent, with the current account to show a surplus of 0.9 percent of GDP.

Gross Domestic Product is now valued at 2,997 billion baht, with Gross National Product now at 2,900 billion baht, a 5.8 percent rise in real terms in the non-agriculture sector, with strong growth in the services sector (hotels and restaurants 14,8%), commensurate with an 18.9% increase in inbound tourists; the transport and communication sector(8.7%) which includes transport services (10.0%) and telecommunications services (6.4%).

The manufacturing sector grew by 4.8 percent, led by production of automotives and electronics.

According to NESDB all other non-agriculture sectors registered growth, as follows: mining and quarrying (10.5%), electricity, gas and water supply (3.0%), construction (10.5%), wholesale and retail trade (5.0%),

and other service sectors (2.1%).

Household consumption expenditure in the domestic market continues to be positive, with a 4.2 percent increase, although lower than the previous quarter. The government budget for 2013 was approved at 2,400,000 million baht, with disbursements in Q2 of fiscal year 2013 of 512,908 million. Private construction in the quarter grew by 8.9 percent and public construction grew by 13.4%.

Source: NESDB May 20, 2013

June 2013

Page 7

INDUSTRY FOCUS

Alternative EnergyBeing heavily dependent on imported oil but endowed with a large agriculture sector, it is not surprising that Thailand is one of the first countries in Asia to have a policy to encourage the utilization of alternative energy sources, like biofuels and solar/wind power. Although Thailand has a large amount of agriculture raw materials for the production of ethanol and biodiesel for the past few decades, it is the rise of oil prices, beginning in 2004, along with government policy that led to a dramatic increase in the consumption and production of biofuels in recent years.

Thailand is ASEAN’s leading country in terms of renewable energy, particularly electricity sourced by sunlight. Renewable energy was promoted actively starting in 2010 when the Government announced its aim to make the Kingdom a low-carbon society modeled on the principles of His Majesty the King’s sufficiency economy. One of the goals was to increase the production and consumption of renewable energy in the face of projected average energy demand rising 4.2 per cent per year.

According to the Ministry of Energy’s estimation, under Alternative Energy Development Plan (AEDP 2012-2021), it has been found that in 2021, the demand for energy in Thailand will increase from

71,728 ktoe (kilo tonnes of oil equivalent) today to 99,838 ktoe, or a 39.19% increase. The Thai government is hoping to push the use of alternative energy and renewable energy to reach 25% of total energy consumption. This is because Thailand has agricultural products that can be used as energy sources such as biomass, biogas, biodiesel and ethanol. Food industries also yield a great amount of byproducts that can be made into energy from waste. Thailand’s natural resources also have great potential for energy generation - the country has the average sunlight energy of 18.2

megajoules per square meter a day, not to mention the Kingdom’s potential in wind energy. (Interesting to note, thin-film solar technology, which is cheaper and more efficient than older thick-film technology, was pioneered in Thailand.) This makes the country the right place for alternative energy and renewable energy investment, which will lead to a significant decrease in greenhouse gas emission, making Thailand a low-carbon society in the future.

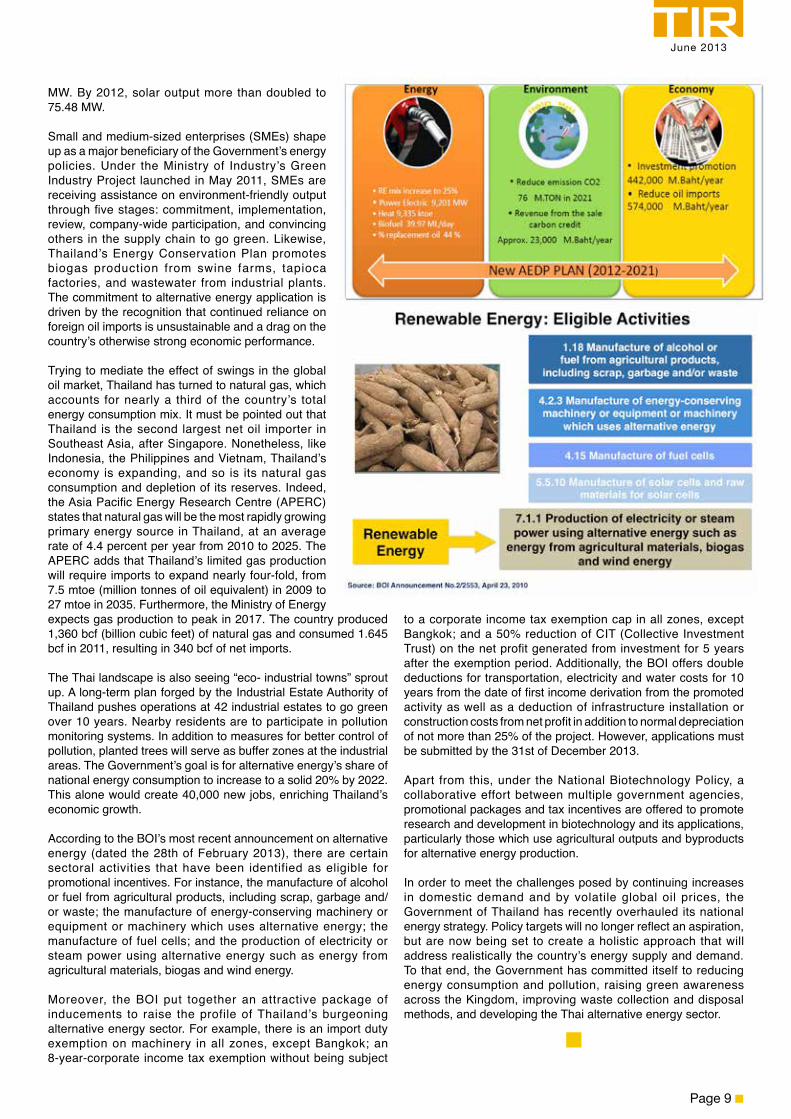

Thailand is a leader in pursuing the development of alternative sources of energy. The country’s 15-year plan to lift alternative and renewable energy’s share of total energy production from 6% today to 20% by 2022 has been implemented with great success and spearheaded fast and expansive growth of the alternative energy sector. In 2010, for example, requests for investing in Thailand’s renewable energy projects increased 300%, as compared to the already impressive numbers of the previous years.

The Ministry of Energy has issued two major renewable energy schemes. The first was a 15-year renewable Energy Development Plan (2008-2022) in 2010, followed by the more ambitious 10-year (2011-2021) Alternative Energy Development Plan (AEDP) announced in 2012 which raised the target for renewable energy to comprise 25 per cent of total energy consumption by 2021, thereby saving the country oil imports worth 574,000 million baht. According to the Ministry of Energy’s Department of Alternative Energy Development and Efficiency (DEDE), the entire renewable energy sector in 2010 contributed 2,026 MW (megawatts) of electricity, of which solar sources produced 32

June 2013

Page 8

to a corporate income tax exemption cap in all zones, except Bangkok; and a 50% reduction of CIT (Collective Investment Trust) on the net profit generated from investment for 5 years after the exemption period. Additionally, the BOI offers double deductions for transportation, electricity and water costs for 10 years from the date of first income derivation from the promoted activity as well as a deduction of infrastructure installation or construction costs from net profit in addition to normal depreciation of not more than 25% of the project. However, applications must be submitted by the 31st of December 2013.

Apart from this, under the National Biotechnology Policy, a collaborative effort between multiple government agencies, promotional packages and tax incentives are offered to promote research and development in biotechnology and its applications, particularly those which use agricultural outputs and byproducts for alternative energy production.

In order to meet the challenges posed by continuing increases in domestic demand and by volatile global oil prices, the Government of Thailand has recently overhauled its national energy strategy. Policy targets will no longer reflect an aspiration, but are now being set to create a holistic approach that will address realistically the country’s energy supply and demand. To that end, the Government has committed itself to reducing energy consumption and pollution, raising green awareness across the Kingdom, improving waste collection and disposal methods, and developing the Thai alternative energy sector.

MW. By 2012, solar output more than doubled to 75.48 MW.

Small and medium-sized enterprises (SMEs) shape up as a major beneficiary of the Government’s energy policies. Under the Ministry of Industry’s Green Industry Project launched in May 2011, SMEs are receiving assistance on environment-friendly output through five stages: commitment, implementation, review, company-wide participation, and convincing others in the supply chain to go green. Likewise, Thailand’s Energy Conservation Plan promotes biogas production from swine farms, tapioca factories, and wastewater from industrial plants. The commitment to alternative energy application is driven by the recognition that continued reliance on foreign oil imports is unsustainable and a drag on the country’s otherwise strong economic performance.

Trying to mediate the effect of swings in the global oil market, Thailand has turned to natural gas, which accounts for nearly a third of the country’s total energy consumption mix. It must be pointed out that Thailand is the second largest net oil importer in Southeast Asia, after Singapore. Nonetheless, like Indonesia, the Philippines and Vietnam, Thailand’s economy is expanding, and so is its natural gas consumption and depletion of its reserves. Indeed, the Asia Pacific Energy Research Centre (APERC) states that natural gas will be the most rapidly growing primary energy source in Thailand, at an average rate of 4.4 percent per year from 2010 to 2025. The APERC adds that Thailand’s limited gas production will require imports to expand nearly four-fold, from 7.5 mtoe (million tonnes of oil equivalent) in 2009 to 27 mtoe in 2035. Furthermore, the Ministry of Energy expects gas production to peak in 2017. The country produced 1,360 bcf (billion cubic feet) of natural gas and consumed 1.645 bcf in 2011, resulting in 340 bcf of net imports.

The Thai landscape is also seeing “eco- industrial towns” sprout up. A long-term plan forged by the Industrial Estate Authority of Thailand pushes operations at 42 industrial estates to go green over 10 years. Nearby residents are to participate in pollution monitoring systems. In addition to measures for better control of pollution, planted trees will serve as buffer zones at the industrial areas. The Government’s goal is for alternative energy’s share of national energy consumption to increase to a solid 20% by 2022. This alone would create 40,000 new jobs, enriching Thailand’s economic growth.

According to the BOI’s most recent announcement on alternative energy (dated the 28th of February 2013), there are certain sectoral activities that have been identified as eligible for promotional incentives. For instance, the manufacture of alcohol or fuel from agricultural products, including scrap, garbage and/or waste; the manufacture of energy-conserving machinery or equipment or machinery which uses alternative energy; the manufacture of fuel cells; and the production of electricity or steam power using alternative energy such as energy from agricultural materials, biogas and wind energy.

Moreover, the BOI put together an attractive package of inducements to raise the profile of Thailand’s burgeoning alternative energy sector. For example, there is an import duty exemption on machinery in all zones, except Bangkok; an 8-year-corporate income tax exemption without being subject

June 2013

Page 9

Jetro Surveys Service IndustryThe new Jetro “Field Survey Concerning Overseas Presence in the Service Industry FY2012” has been released. It was conducted among 6,000 companies in the Japanese service industry, from October to November 2012, to better understand the actual situation of overseas expansion in the Japanese service industry by attempting to “quantify the main venture destinations of each company, countries or cities receiving priority attention, the purpose and method of setting up ventures and issues related to overseas expansion, among other matters.”

According to the survey, the three countries to which Japanese companies engaged in the service industry attach the highest value are China, followed by Thailand and the United States. (Thailand and the United States, both of which ranked high also in the last survey, have switched ranks.) “Looking by city, Shanghai still continues to attract the biggest attention since the last survey while other Asian cities such as Bangkok…ranked high on the list.”

The survey also indicates increased interest within such companies to locate in emerging countries in Asia, with “more than 80% of the 106 companies that have expanded into another country after initially setting up operations in China have chosen an Asian country as the second destination”.

Also mentioned is the fact that Japanese SMEs have recently started looking overseas for expansion. “As for the state of overseas ventures, around 70% of the large companies have overseas operations while only around 20% of medium and small sized companies have overseas presence.” It now seems a very timely move for the Thailand BOI to have established an Investment Promotion Network for Thai and Japanese SMEs to assist Japanese SMEs seeking to invest in the kingdom and look for Thai partners or suppliers.

Global Consumer Confidence on the RiseNielsen recently released its report entitled Consumer Confidence, concerns and spending intentions around the world, Quarter 1, 2013. The report has been issued since 2005 and measures consumer confidence, major concerns and spending intentions among more than 29,000 respondents with Internet access in 58 countries. Measurement above and below a baseline of 100 indicate degrees of optimism or pessimism.

The company reports that global consumer confidence indexed at 93 during the quarter. This is a 2 point increase from the previous quarter at the end of 2012. “The increase was driven by the positive performance of self-reported key economic indicators (job prospects, personal finances and ability to spend) in the United States, across key Asian markets, and throughout northern and central Europe.”

North America reported the biggest quarter on quarter increase in consumer confidence, followed by Asia. The US, Germany and Japan all reported increased consumer confidence, with

Hong Kong reporting the biggest increase at 23 points. Thailand increase 1 point to reach 116, well above the 100 baseline for optimism.

June 2013

Page 10

Framework for Thailand’s Economic Stability 2013

2014 National Budget

Thailand Public Relations Department reports that a framework has been approved that is designed to maintain Thailand’s economic stability. At its meeting on 28 May, the Cabinet approved the measure, devised by the Office of the National Economic and Social Development Board and the Ministry of Finance, as a way to deal effectively with the financial risks that arise from the appreciation of the baht.

The slow recovery in the global economy and quantitative easing measures implemented by several major countries, as well as currency wars, have resulted in capital inflow to the Asian region. The value of the baht has become stronger than other currencies in the region, affecting Thai exports and services.

Concerning immediate measures the framework seeks to ensure

The Prime Minister has announced that the Government’s proposed 2014 budget of 2.525-trillion-baht emphasizes competitiveness and responding to the needs of people in all areas. The national budget for the 2014 fiscal year aims to drive Thailand’s national strategies and prepare the country for the realization of the ASEAN Community, apart from solving economic and social problems on a continual basis.

2.511 trillion baht will be for the expenditure of various government agencies and state enterprises, and 13.423 billion baht will be allocated as payment for the national reserves.

Regular spending accounts for 79.9 percent of the total budget, payments for the national reserves represent 0.5 percent, investment accounts for 17.5 percent, and debt repayment 2.1 percent.

The Government is expected to earn 2.275 trillion baht in revenue in 2014, accounting for 17.2% of GDP. The Government has set a deficit of 250 billion baht. Thailand’s economic growth in 2014 is projected at 4-5 percent, with inflation of 2.7-3.7 percent. As of 20 May 2013, the national reserves stood at 250.9 billion baht. At the end of April 2013, Thailand’s international reserves came to 178.37 billion US dollars.

The Government has set four national strategies to move the country forward. The four strategies include Growth and Competitiveness, Inclusive Growth, Green Growth, and Good Governance. In preparation for the ASEAN Community, which will be in place in 2015, the Government is striving to upgrade the quality of education and develop foreign language and labor skills to cope with changes in and outside the country.

The national budget also takes into account loans for water resources management and infrastructure development.

that the appreciation of the baht does not affect growth in the Thai economy, and to create sustained economic growth of 5 percent.

The Bank of Thailand will be encouraged to ensure that the policy rate is in line with the economic situation and macro-prudential measures will be implemented. Assistance will be provided for small and medium-sized enterprises (SMEs) to ease impact of currency appreciation. The proportion of SMEs will be increased to 40 percent of GDP.

The government is working to increase international tourist arrivals to 24.7 million in 2013 and to double the country’s tourism revenue by 2015. In addition to achieving the 2013 export growth target at 9 percent, other measures also call for energy security with reasonable prices and cost reduction for low-income earners.

June 2013

Page 11

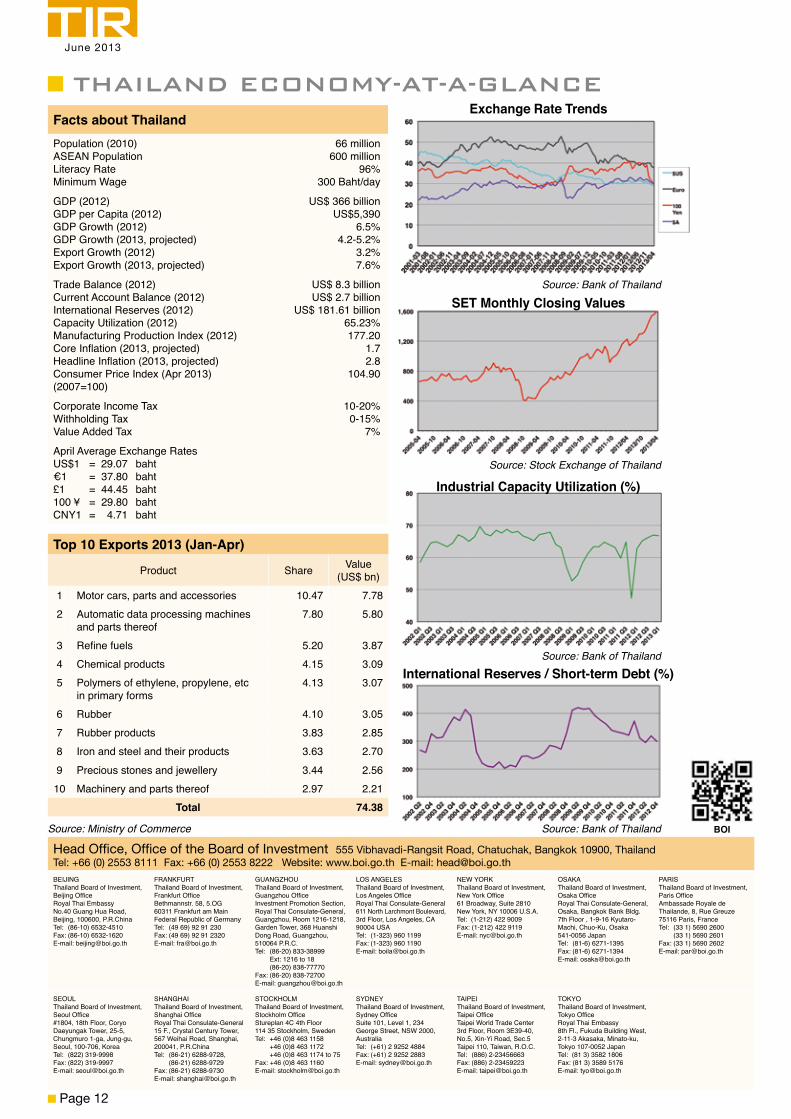

THAILAND ECONOMY-AT-A-GLANCE

Source: Stock Exchange of Thailand

Source: Bank of Thailand

SET Monthly Closing Values

International Reserves / Short-term Debt (%)

Exchange Rate Trends

Industrial Capacity Utilization (%)

Head Office, Office of the Board of Investment 555 Vibhavadi-Rangsit Road, Chatuchak, Bangkok 10900, ThailandTel: +66 (0) 2553 8111 Fax: +66 (0) 2553 8222 Website: www.boi.go.th E-mail: [email protected] Board of Investment, Beijing Office Royal Thai Embassy No.40 Guang Hua Road, Beijing, 100600, P.R.China Tel: (86-10) 6532-4510 Fax: (86-10) 6532-1620 E-mail: [email protected]

FRANKFURTThailand Board of Investment, Frankfurt OfficeBethmannstr. 58, 5.OG60311 Frankfurt am Main Federal Republic of Germany Tel: (49 69) 92 91 230Fax: (49 69) 92 91 2320E-mail: [email protected]

GUANGZHOUThailand Board of Investment, Guangzhou Office Investment Promotion Section, Royal Thai Consulate-General, Guangzhou, Room 1216-1218, Garden Tower, 368 Huanshi Dong Road, Guangzhou, 510064 P.R.C. Tel: (86-20) 833-38999 Ext: 1216 to 18 (86-20) 838-77770Fax: (86-20) 838-72700 E-mail: [email protected]

LOS ANGELES Thailand Board of Investment, Los Angeles Office Royal Thai Consulate-General 611 North Larchmont Boulevard, 3rd Floor, Los Angeles, CA 90004 USA Tel: (1-323) 960 1199Fax: (1-323) 960 1190E-mail: [email protected]

NEW YORKThailand Board of Investment, New York Office 61 Broadway, Suite 2810 New York, NY 10006 U.S.A.Tel: (1-212) 422 9009Fax: (1-212) 422 9119E-mail: [email protected]

OSAKAThailand Board of Investment, Osaka Office Royal Thai Consulate-General, Osaka, Bangkok Bank Bldg. 7th Floor , 1-9-16 Kyutaro-Machi, Chuo-Ku, Osaka 541-0056 Japan Tel: (81-6) 6271-1395 Fax: (81-6) 6271-1394E-mail: [email protected]

PARISThailand Board of Investment, Paris Office Ambassade Royale de Thailande, 8, Rue Greuze75116 Paris, FranceTel: (33 1) 5690 2600 (33 1) 5690 2601Fax: (33 1) 5690 2602E-mail: [email protected]

SEOULThailand Board of Investment, Seoul Office #1804, 18th Floor, Coryo Daeyungak Tower, 25-5, Chungmuro 1-ga, Jung-gu, Seoul, 100-706, Korea Tel: (822) 319-9998 Fax: (822) 319-9997E-mail: [email protected]

SHANGHAIThailand Board of Investment, Shanghai OfficeRoyal Thai Consulate-General15 F., Crystal Century Tower, 567 Weihai Road, Shanghai, 200041, P.R.China Tel: (86-21) 6288-9728, (86-21) 6288-9729 Fax: (86-21) 6288-9730E-mail: [email protected]

STOCKHOLMThailand Board of Investment, Stockholm OfficeStureplan 4C 4th Floor 114 35 Stockholm, Sweden Tel: +46 (0)8 463 1158 +46 (0)8 463 1172 +46 (0)8 463 1174 to 75 Fax: +46 (0)8 463 1160 E-mail: [email protected]

SYDNEYThailand Board of Investment, Sydney Office Suite 101, Level 1, 234 George Street, NSW 2000, Australia Tel: (+61) 2 9252 4884 Fax: (+61) 2 9252 2883 E-mail: [email protected]

TAIPEIThailand Board of Investment, Taipei Office Taipei World Trade Center 3rd Floor, Room 3E39-40, No.5, Xin-Yi Road, Sec.5Taipei 110, Taiwan, R.O.C. Tel: (886) 2-23456663Fax: (886) 2-23459223 E-mail: [email protected]

TOKYOThailand Board of Investment, Tokyo Office Royal Thai Embassy8th Fl., Fukuda Building West,2-11-3 Akasaka, Minato-ku, Tokyo 107-0052 JapanTel: (81 3) 3582 1806Fax: (81 3) 3589 5176E-mail: [email protected]

Facts about ThailandPopulation (2010) 66 millionASEAN Population 600 millionLiteracy Rate 96%Minimum Wage 300 Baht/day

GDP (2012) US$ 366 billionGDP per Capita (2012) US$5,390GDP Growth (2012) 6.5%GDP Growth (2013, projected) 4.2-5.2%Export Growth (2012) 3.2%Export Growth (2013, projected) 7.6%

Trade Balance (2012) US$ 8.3 billionCurrent Account Balance (2012) US$ 2.7 billionInternational Reserves (2012) US$ 181.61 billionCapacity Utilization (2012) 65.23%Manufacturing Production Index (2012) 177.20Core Inflation (2013, projected) 1.7Headline Inflation (2013, projected) 2.8Consumer Price Index (Apr 2013) 104.90 (2007=100)

Corporate Income Tax 10-20%Withholding Tax 0-15%Value Added Tax 7%

April Average Exchange RatesUS$1 = 29.07 baht€1 = 37.80 baht£1 = 44.45 baht100 ¥ = 29.80 bahtCNY1 = 4.71 baht

Top 10 Exports 2013 (Jan-Apr)

Product Share Value (US$ bn)

1 Motor cars, parts and accessories 10.47 7.782 Automatic data processing machines

and parts thereof7.80 5.80

3 Refine fuels 5.20 3.874 Chemical products 4.15 3.095 Polymers of ethylene, propylene, etc

in primary forms4.13 3.07

6 Rubber 4.10 3.057 Rubber products 3.83 2.85 8 Iron and steel and their products 3.63 2.709 Precious stones and jewellery 3.44 2.56

10 Machinery and parts thereof 2.97 2.21Total 74.38

Source: Ministry of Commerce

Source: Bank of Thailand

Source: Bank of Thailand BOI

June 2013

Page 12