Pricing of Forward and Futures Contracts Finance (Derivative Securities) 312 Tuesday, 15 August 2006...

25

Pricing of Forward Pricing of Forward and Futures and Futures Contracts Contracts Finance (Derivative Securities) 312 Tuesday, 15 August 2006 Readings: Chapter 5

-

Upload

colin-ford -

Category

Documents

-

view

229 -

download

1

Transcript of Pricing of Forward and Futures Contracts Finance (Derivative Securities) 312 Tuesday, 15 August 2006...

Pricing of Forward Pricing of Forward and Futures and Futures ContractsContracts

Finance (Derivative Securities) 312

Tuesday, 15 August 2006

Readings: Chapter 5

Consumption v Consumption v InvestmentInvestment

Investment assets are assets held by significant numbers of people purely for investment purposes (eg gold, silver)

Consumption assets are assets held primarily for consumption (eg copper, oil)

Short SellingShort Selling

Selling securities you do not ownBroker borrows securities from another

client and sells on your behalfObligation to reverse the transaction at a

later dateMust pay dividends and other benefits to

owner of securities

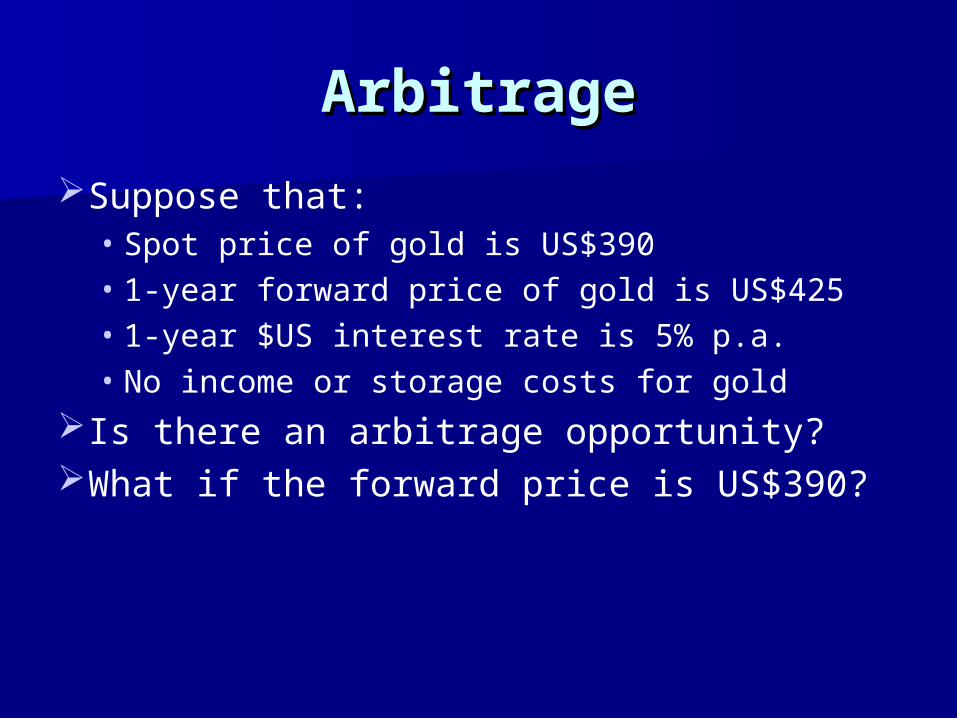

ArbitrageArbitrage

Suppose that:• Spot price of gold is US$390• 1-year forward price of gold is US$425• 1-year $US interest rate is 5% p.a.• No income or storage costs for gold

Is there an arbitrage opportunity?What if the forward price is US$390?

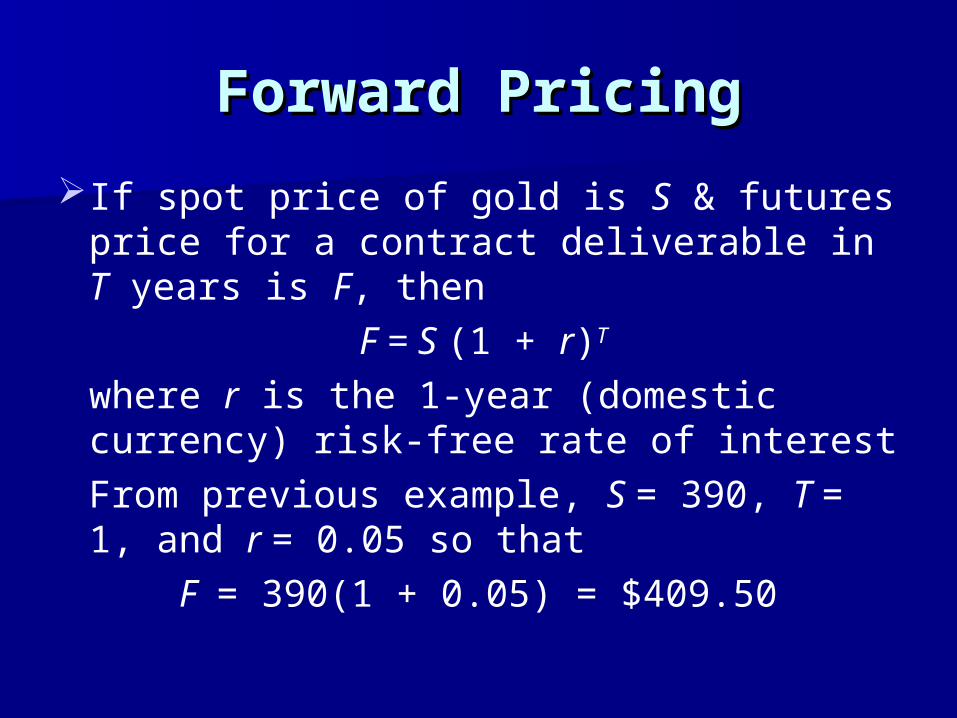

Forward PricingForward Pricing

If spot price of gold is S & futures price for a contract deliverable in T years is F, then

F = S (1 + r)T

where r is the 1-year (domestic currency) risk-free rate of interest

From previous example, S = 390, T = 1, and r = 0.05 so that

F = 390(1 + 0.05) = $409.50

Forward PricingForward Pricing

Arbitrage strategy:

Now After 1 year

Borrow US$390 Sell Gold under Forward

Buy Gold Receive US$425

Short Forward Repay US$409.50

Initial cost of portfolio = 0

CF after one year = US$15.50 (riskless profit)

Forward PricingForward Pricing

If forward price is US$390, reverse strategy:

Now After 1 year

Sell Gold Investment pays $409.50

Invest US$390 Buy Gold under Forward

Long Forward Pay US$390

Initial cost of portfolio = 0

CF after one year = US$19.50 (riskless profit)

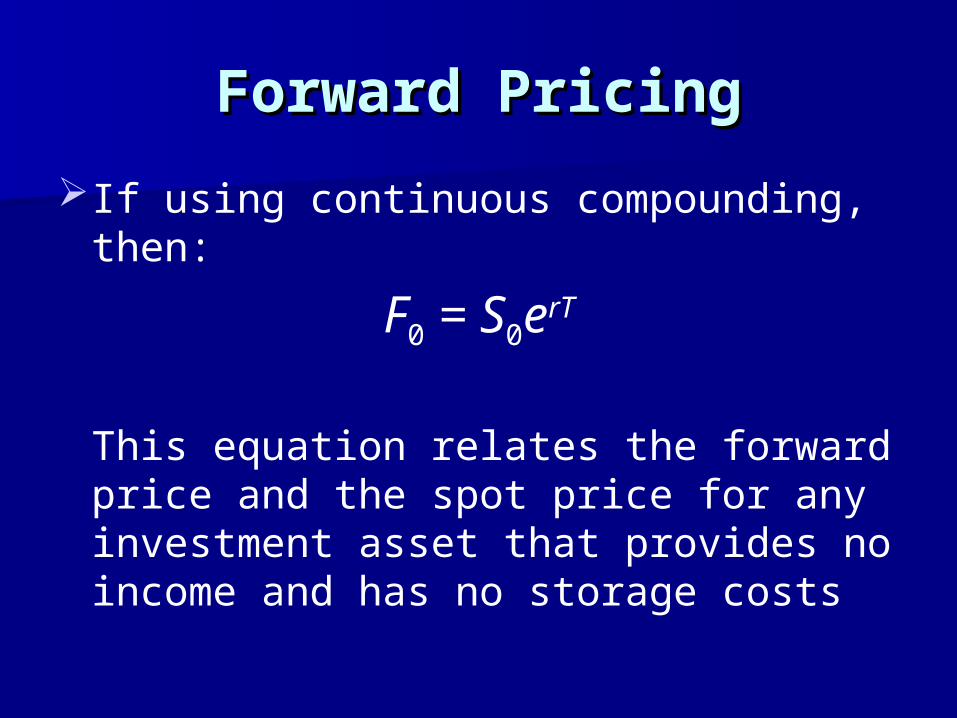

Forward PricingForward Pricing

If using continuous compounding, then:

F0 = S0erT

This equation relates the forward price and the spot price for any investment asset that provides no income and has no storage costs

Forward PricingForward Pricing

If asset provides a known income:

F0 = (S0 – I)erT

where I is the present value of the income

If asset provides a known yield:

F0 = S0e(r–q)T

where q is the average yield during the life of the contract (continuous compounding)

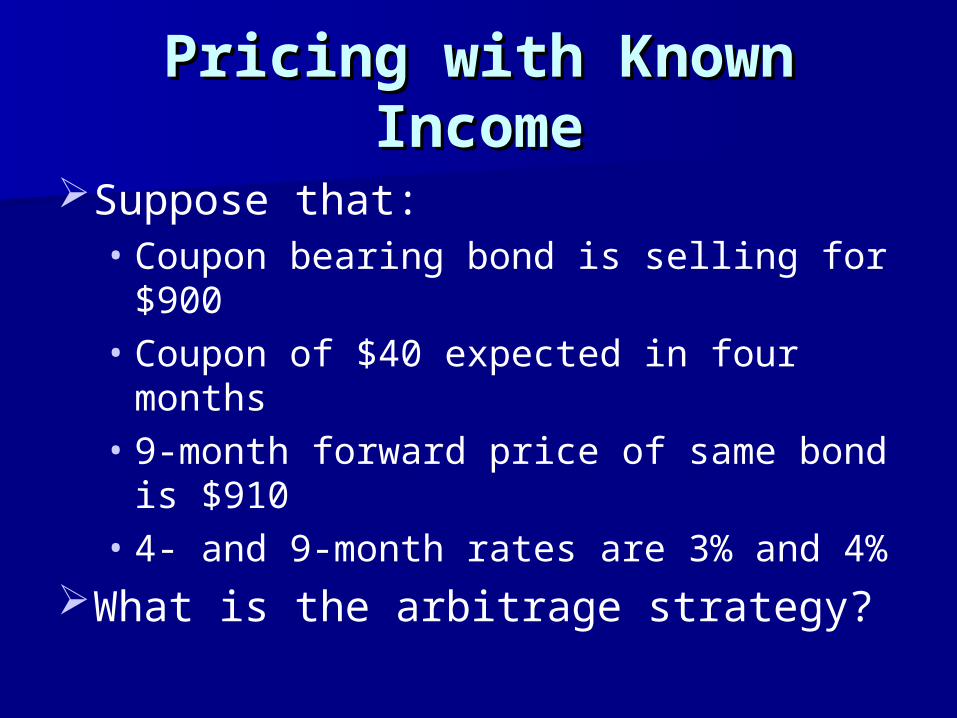

Pricing with Known Pricing with Known IncomeIncome

Suppose that:• Coupon bearing bond is selling for $900• Coupon of $40 expected in four months• 9-month forward price of same bond is $910• 4- and 9-month rates are 3% and 4%

What is the arbitrage strategy?

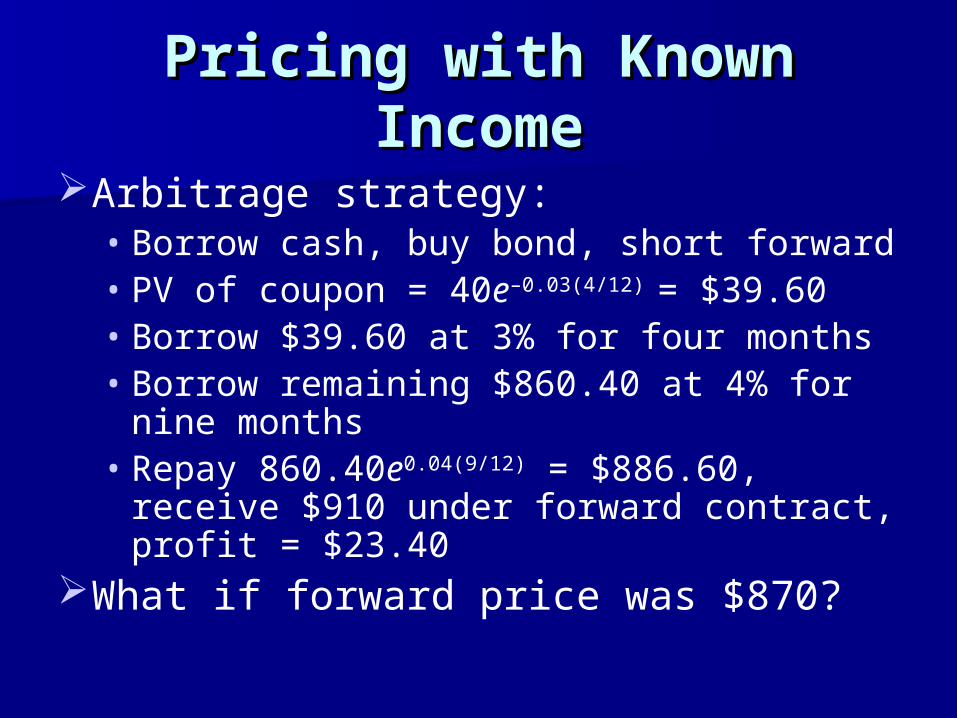

Pricing with Known Pricing with Known IncomeIncome

Arbitrage strategy:• Borrow cash, buy bond, short forward• PV of coupon = 40e–0.03(4/12) = $39.60• Borrow $39.60 at 3% for four months• Borrow remaining $860.40 at 4% for nine

months• Repay 860.40e0.04(9/12) = $886.60, receive $910

under forward contract, profit = $23.40What if forward price was $870?

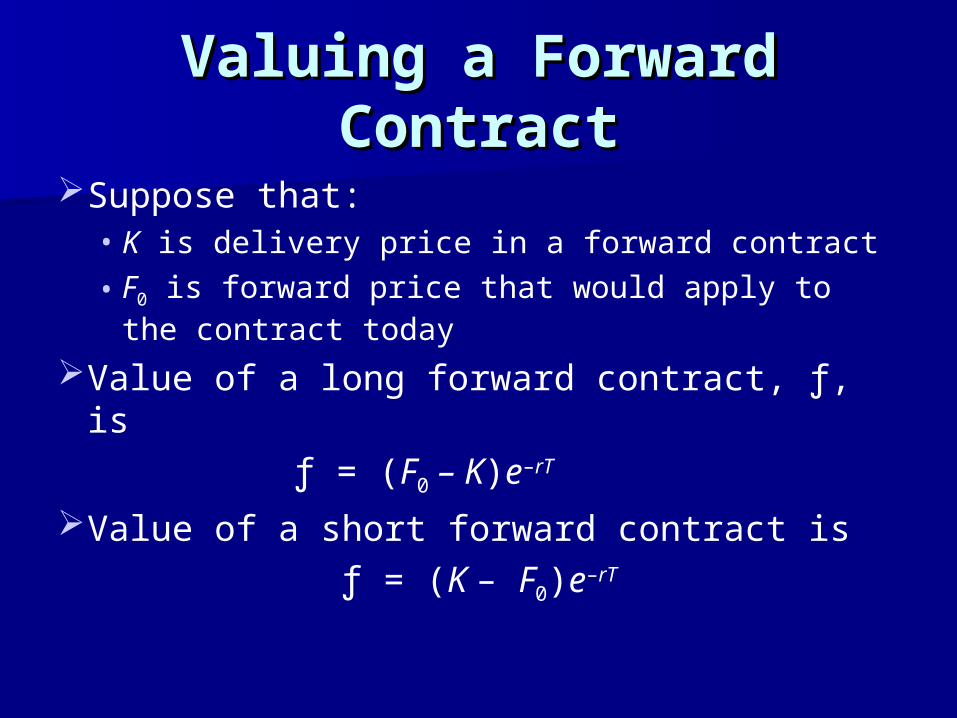

Valuing a Forward Valuing a Forward ContractContract

Suppose that:• K is delivery price in a forward contract

• F0 is forward price that would apply to the contract today

Value of a long forward contract, ƒ, is

ƒ = (F0 – K)e–rT

Value of a short forward contract is

ƒ = (K – F0)e–rT

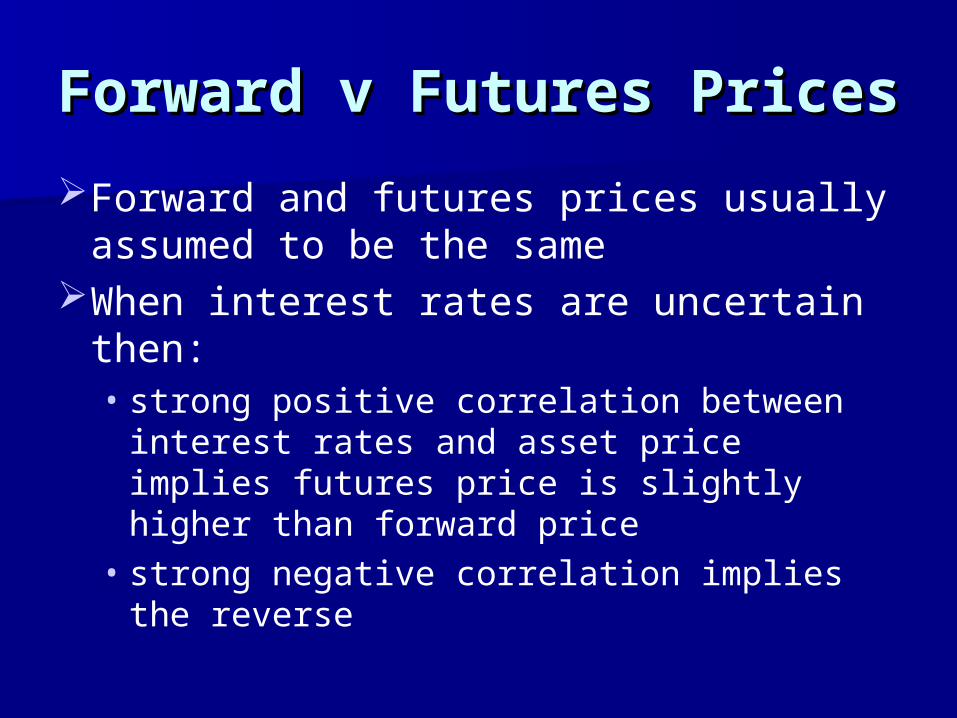

Forward v Futures PricesForward v Futures Prices

Forward and futures prices usually assumed to be the same

When interest rates are uncertain then:• strong positive correlation between interest

rates and asset price implies futures price is slightly higher than forward price

• strong negative correlation implies the reverse

Stock IndicesStock Indices

Can be viewed as an investment asset paying a dividend yield

The futures price and spot price relationship is therefore

F0 = S0e(r–q)T

where q is the dividend yield on the portfolio represented by the index

Stock IndicesStock Indices

For the formula to be true it is important that the index represent an investment asset

Changes in the index must correspond to changes in value of a tradable portfolio

Nikkei Index viewed as a dollar number does not represent an investment asset

Index ArbitrageIndex Arbitrage

When F0 > S0e(r–q)T an arbitrageur buys the stocks underlying the index and sells futures

When F0 < S0e(r–q)T an arbitrageur buys futures and shorts the stocks underlying the index

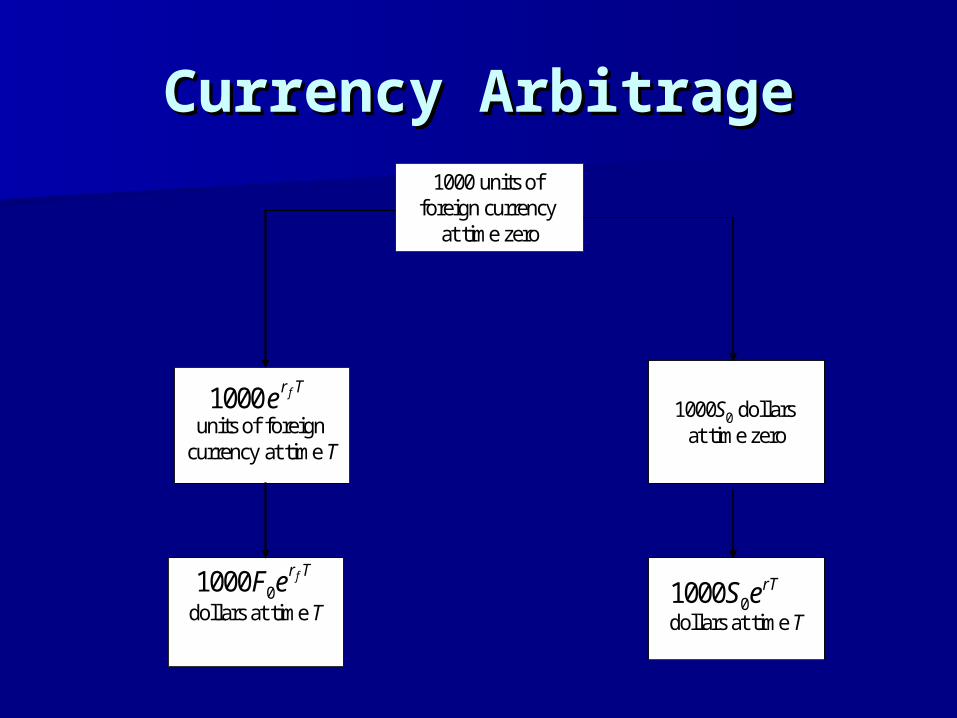

Currency ArbitrageCurrency Arbitrage

Foreign currency is analogous to a security providing a dividend yield

Continuous dividend yield is the foreign risk-free interest rate

If rf is the foreign risk-free interest rate:

F S e r r Tf

0 0 ( )

Currency ArbitrageCurrency Arbitrage

1000 units of

foreign currency at time zero

units of foreign currency at time T

Tr fe1000

dollars at time T

Tr feF01000

1000S0 dollars at time zero

dollars at time T

rTeS01000

1000 units of foreign currency

at time zero

units of foreign currency at time T

Tr fe1000

dollars at time T

Tr feF01000

1000S0 dollars at time zero

dollars at time T

rTeS01000

Currency ArbitrageCurrency Arbitrage

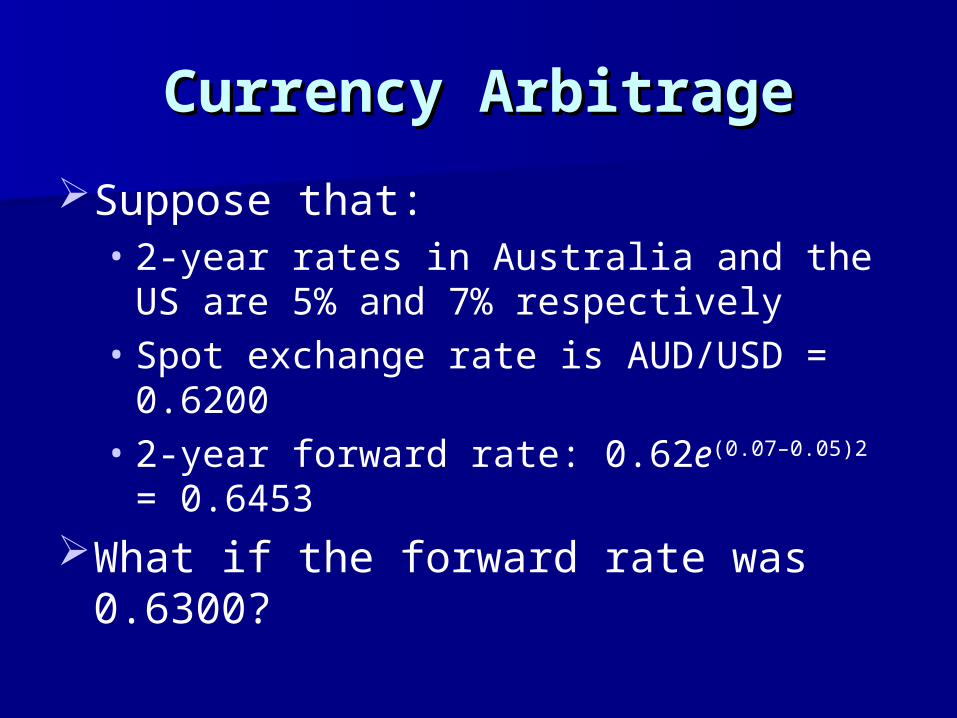

Suppose that:• 2-year rates in Australia and the US are 5%

and 7% respectively• Spot exchange rate is AUD/USD = 0.6200• 2-year forward rate: 0.62e(0.07–0.05)2 = 0.6453

What if the forward rate was 0.6300?

Currency ArbitrageCurrency Arbitrage

Arbitrage strategy:• Borrow AUD1,000 at 5% for two years,

convert to USD620, and invest at 7%• Long forward contract to buy AUD1,105.17 for

1,105.17 x 0.63 = USD696.26• USD620 will grow to 620e0.07x2 = 713.17• Pay USD696.26 under contract• Profit = 713.17 – 696.26 = USD16.91

Consumption AssetsConsumption Assets

F0 S0e(r+u)T

where u is the storage cost per unit time as a percent of the asset value

Alternatively,

F0 (S0+U)erT

where U is the present value of the storage costs

Cost of CarryCost of Carry

Cost of carry, c, is storage cost plus interest costs less income earned

For an investment asset F0 = S0ecT

For a consumption asset F0 S0ecT

Convenience yield on a consumption asset, y, is defined so that

F0 = S0e(c–y)T

Risk in a Futures Risk in a Futures PositionPosition

Suppose that:• A speculator takes a long futures position• Invests the present value of the futures price,

F0e–rT

• At delivery, speculator buys asset under contract, sells in market for (expected) higher price

Value of the investment?

Risk in a Futures Risk in a Futures PositionPosition

PV of investment = –F0 e–rT + E(ST )e–kT

If securities are priced based on zero NPVs, then the PV should equate to zero

F0 = E(ST)e(r–k)T

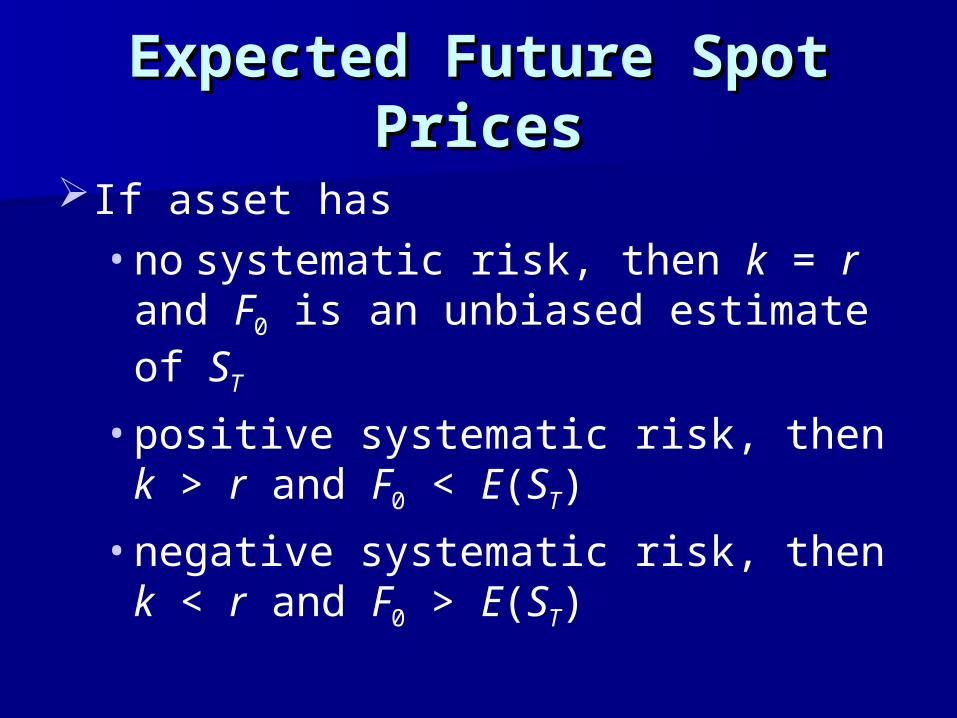

Expected Future Spot Expected Future Spot PricesPrices

If asset has

• no systematic risk, then k = r and F0 is an unbiased estimate of ST

• positive systematic risk, then k > r and F0 < E(ST)

• negative systematic risk, then k < r and F0 > E(ST)