Pricing Inflation Vanillas and Exotics

31

Pricing Inflation Vanillas and Exotics Pricing Inflation Vanillas and Exotics Yann Ticot Bank of America Merrill Lynch, London June 2011 1 / 32

Transcript of Pricing Inflation Vanillas and Exotics

Pricing Inflation Vanillas and Exotics

Pricing Inflation Vanillas and Exotics

Yann Ticot

Bank of America Merrill Lynch, London

June 2011

1 / 32

Pricing Inflation Vanillas and Exotics

Outline

1 Inflation market overview

2 Popular inflation models

3 Pricing challenges

4 Inflation vanilla model

5 Inflation exotic model

6 Conclusion

2 / 32

Pricing Inflation Vanillas and Exotics

Inflation market overview

Outline

1 Inflation market overview

2 Popular inflation models

3 Pricing challenges

4 Inflation vanilla model

5 Inflation exotic model

6 Conclusion

3 / 32

Pricing Inflation Vanillas and Exotics

Inflation market overview

Inflation index

measures cost of living, price of a representative basket ofgoods

RPI (UK), HICP (EU), CPI (US)...

short-term drivers : energy, agriculturals, commodities

long-term drivers : economic outlook, central bank policy

4 / 32

Pricing Inflation Vanillas and Exotics

Inflation market overview

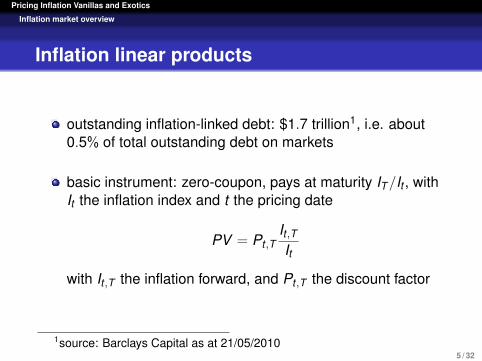

Inflation linear products

outstanding inflation-linked debt: $1.7 trillion1, i.e. about0.5% of total outstanding debt on markets

basic instrument: zero-coupon, pays at maturity IT /It , withIt the inflation index and t the pricing date

PV = Pt ,TIt ,TIt

with It ,T the inflation forward, and Pt ,T the discount factor

1source: Barclays Capital as at 21/05/20105 / 32

Pricing Inflation Vanillas and Exotics

Inflation market overview

Year-on-year rate

zero-coupon is a single payment of the compounding ofinflation over a whole period

It ,T = It exp

(∫ T

tit ,u du

)with it ,u the instantaneous inflation forward rate

some investors prefer a payoff in a “swap” format

year-on-year rate (yoy) is defined as

yoyT =IT

IT−1y− 1

6 / 32

Pricing Inflation Vanillas and Exotics

Inflation market overview

Inflation derivatives: vanilla options

derivatives represent 10% to 15% of the inflation market

yoy options: call/put on yoy rate

zero-coupon options: call/put on zero-coupon rate

investors have appetite for zero-strikes

7 / 32

Pricing Inflation Vanillas and Exotics

Inflation market overview

Inflation derivatives: exotics

Limited Price Indexation (LPI): liquid due to UK pensionsregulation, maturities up to 50y

n∏i=1

(1 +

[yoyTi

]capfloor

)

LPIs have sensitivity to all yoy smiles & correlations

callables, range accruals

apart from LPIs, exotics are not liquidly traded

8 / 32

Pricing Inflation Vanillas and Exotics

Popular inflation models

Outline

1 Inflation market overview

2 Popular inflation models

3 Pricing challenges

4 Inflation vanilla model

5 Inflation exotic model

6 Conclusion

9 / 32

Pricing Inflation Vanillas and Exotics

Popular inflation models

Popular inflation models: nominal-realapproach (Jarrow-Yildirim)

Choose as numeraire the value of inflation index paid at T

Pt ,T It ,T = It exp

(−∫ T

t(nt ,u − it ,u) du

)with nt ,u the instantaneous nominal forward rate.FX analogy:

exp(−∫ T

t (nt ,u − it ,u) du)

is a “real” discount factor

inflation index is the nominal-real FX

for an index-linked payoff IT HT

PV = Pt ,T It ,T Er ,Tt [HT ]

10 / 32

Pricing Inflation Vanillas and Exotics

Popular inflation models

Popular inflation models: modeling inflationforwards (Belgrade-Benhamou-Koehler)

all index-linked payoffs can be expressed as a function ofinflation forwards It ,T

inflation forwards are modeled directly (martingale underforward-neutral measure)

for an index-linked payoff IT HT

PV = Pt ,T ETt[IT ,T HT

]

11 / 32

Pricing Inflation Vanillas and Exotics

Pricing challenges

Outline

1 Inflation market overview

2 Popular inflation models

3 Pricing challenges

4 Inflation vanilla model

5 Inflation exotic model

6 Conclusion

12 / 32

Pricing Inflation Vanillas and Exotics

Pricing challenges

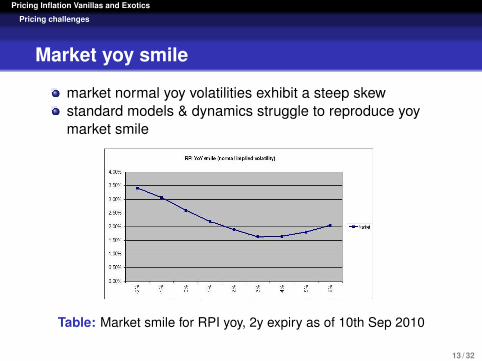

Market yoy smile

market normal yoy volatilities exhibit a steep skewstandard models & dynamics struggle to reproduce yoymarket smile

Table: Market smile for RPI yoy, 2y expiry as of 10th Sep 2010

13 / 32

Pricing Inflation Vanillas and Exotics

Pricing challenges

LPI market prices

difficult to reproduce LPI market prices

however, better match of LPI market if yoy options marketprices are matched

need for a model consistent with the yoy marginaldistributions

14 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

Outline

1 Inflation market overview

2 Popular inflation models

3 Pricing challenges

4 Inflation vanilla model

5 Inflation exotic model

6 Conclusion

15 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

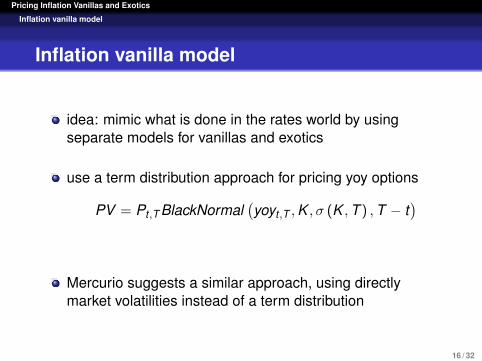

Inflation vanilla model

idea: mimic what is done in the rates world by usingseparate models for vanillas and exotics

use a term distribution approach for pricing yoy options

PV = Pt ,T BlackNormal(yoyt ,T , K , σ (K , T ) , T − t

)

Mercurio suggests a similar approach, using directlymarket volatilities instead of a term distribution

16 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

Inflation vanilla model: consistency

challenge # 1: yoy forward rate is model-dependent, with aconvexity adjustment

ETt

[IT

IT−1y

]−

It ,TIt ,T−1y

⇒ yoy convexity adjustment must be consistent with yoydistribution

challenge # 2: find a term-distribution which fits the yoysmile

17 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

Inflation vanilla model: consistency

For lognormal inflation forwards, the convexity adjustment ofyoyTn is proportional to

∫ Tn−1

0

n−1∑i, Ti≥t

(ρY ,Y

i,n (t)σYi (t)σY

n (t)− ρY ,Li,n−1(t)σ

Yi (t)σL

n−1(t))

dt

withσL

j the normal volatility of the 1y libor starting at Tj

σYi the lognormal volatility of

It,TiIt,Ti−1y

(homogeneous to a yoynormal volatility)ρY ,Y

i,j , ρY ,Li,j the yoy-yoy and yoy-rates correlations

18 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

Inflation vanilla model: consistency

large number of degrees of freedom makes convexityadjustment & optionality “orthogonal”

consider a set of “reasonable” rates & yoy marginals

also consider a set of yoy convexity adjustments

it should be possible to find a set of correlations whichmake the yoy convexity adjustment consistent with themarginals

19 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

Inflation vanilla model: consistency

liquid market quotes available for expiries2y , 3y , 5y , 7y , 10y , 12y , 15y , 20y , 30y

use a simple term-structure model as interpolation tool tocompute yoy forwards at any expiry

handle the optionality with a term-distribution

assume that the convexity adjustment and optionality areconsistent

20 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

Inflation vanilla model: year-on-year distribution

look for a term-distribution which could fit the yoy smile,related to a Levy process (generic class)

diffusion & jump-diffusion processes (finite activity) :shifted lognormal, SABR ?

processes with infinite activity

Generalised Hyperbolic processes tend to fit well empiricaldistributions with fat tails and leptokurtic behaviour

21 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

Inflation vanilla model: Normal InverseGaussian distribution (Barndorff-Nielsen)

NIG is a sub class of Generalised HyperbolicX is NIG if

X |Z ∼ N (µ + βZ , Z )

Z ∼ IG(δ,√

α2 − β2) where 0 ≤ |β| ≤ α

with N (), IG() Gaussian & Inverse Gaussian distributionsthe density is

p(x ;α, β, δ, µ) =αδK1(α

√δ2 + (x − µ)2)

π√

δ2 + (x − µ)2exp (δγ + β(x − µ))

where γ =√

α2 − β2 and K1 the modified Bessel functionof second kind and index 1.

22 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

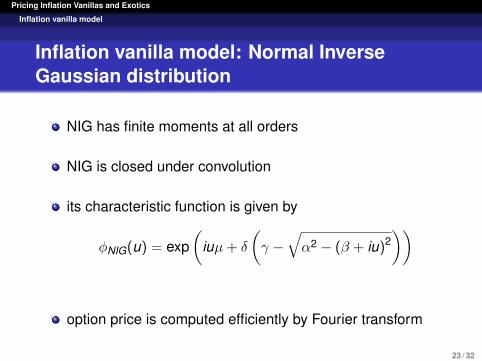

Inflation vanilla model: Normal InverseGaussian distribution

NIG has finite moments at all orders

NIG is closed under convolution

its characteristic function is given by

φNIG(u) = exp(

iuµ + δ

(γ −

√α2 − (β + iu)2

))

option price is computed efficiently by Fourier transform

23 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

NIG smile on RPI yoy, expiry 2Y as of 10th Sep2010

24 / 32

Pricing Inflation Vanillas and Exotics

Inflation vanilla model

NIG smile on HICP yoy, expiry 20Y as of 10thSep 2010

25 / 32

Pricing Inflation Vanillas and Exotics

Inflation exotic model

Outline

1 Inflation market overview

2 Popular inflation models

3 Pricing challenges

4 Inflation vanilla model

5 Inflation exotic model

6 Conclusion

26 / 32

Pricing Inflation Vanillas and Exotics

Inflation exotic model

Inflation exotic model: LPI and non-callables

combine Gaussian copula and Monte Carlo pricing.

CDF of the joint distribution of the n yoy rates is

F (y1, ..., yn) = Cgaussn (F1 (y1) , ..., Fn (yn) ,Ω)

with Cgaussn the n-dimensional gaussian copula, Fi the

marginals, Ω the correlations.

the present value of LPI is

PV = Pt ,T ETt

[n∏

i=1

(1 +

[F−1

i (N (Xi))]cap

floor

)]with Xi correlated Gaussian variables, N() the gaussianCDF

27 / 32

Pricing Inflation Vanillas and Exotics

Inflation exotic model

Inflation exotic model: callables

These trades require a term-structure model

must be able to calibrate to relevant strikes

must at least produce the right shape for the yoy smile

BGM, Cheyette, Quadratic Gaussian

28 / 32

Pricing Inflation Vanillas and Exotics

Conclusion

Outline

1 Inflation market overview

2 Popular inflation models

3 Pricing challenges

4 Inflation vanilla model

5 Inflation exotic model

6 Conclusion

29 / 32

Pricing Inflation Vanillas and Exotics

Conclusion

Conclusion

Possible extensions:a new generation of models is required to price inflationvanillas and exotics

a term-distribution approach for inflation vanillas may be astep in the right direction

in line with traders’ view of the market

satisfactorily reproduces the market smile

30 / 32

Pricing Inflation Vanillas and Exotics

Conclusion

Bibliography

L. Andersen, A. Lipton, Levy processes and their vol smile.Short-term asymptotics, Bank of America Merrill Lynch &Imperial College, 2011.

N. Belgrade, E. Benhamou, E. Koehler, A Market Model forInflation, CDC Ixis Capital Markets, 2004.

X.Charvet, Y. Ticot Inflation vanillas: market overview andoption pricing using NIG distributions, Bank of AmericaMerrill Lynch, Internal document, 2010.

R. Jarrow, Y. Yildirim, Pricing treasury inflation protectedsecurities and related derivatives using a HJM model,Journal of Finance and Quantitative Analysis, 2003.

J. X. Zhang, F. Mercurio, Limited Price Indexation (LPI)Swap Valuation Ideas, Bloomberg L P, 2011.

31 / 32