Belarus Denmark Estonia Finland Germany Latvia Lithuania Norway Poland Russia Sweden

Upload

nguyenlienCategory

view

213download

0

April 20, 2006 F. Gubina

PRICE SETTING IN THE ELECTRICITY MARKETS

WITHIN THE EU SINGLE MARKET

A report to the Committee on Industry, Research and Energy of the

European ParliamentFebruary, 2006

April 20, 2006 F. Gubina

Outline

• Characteristics of the main electricity markets,

• European price structures and trends,• Impact on electricity prices of emissions

trading,• Long-term contracts effects,• Conclusions.

April 20, 2006 F. Gubina

Main electricity markets characteristics

• Facts:– Common agreement on unified electricity market,– Cross-border trade at about 8% of EU consumption,– Lack of interconnecting capacity between countries,– Very low number of producers as bidders,

• Results:– No EU integrated market yet ►

• Local markets,• Regional markets- operating and developing.

– Not all regional markets function up to standards,– W.EU vs. E.EU countries market development: indecisive,

• More detailed insight needed.

April 20, 2006 F. Gubina

International interdependence, 2003

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100

UK & Ireland

Iberia

Western Europe

Eastern Europe

Nordic

Baltic

EU

Import Capacity as a % of InstalledCapacity*

Exports %

Imports %

April 20, 2006 F. Gubina

Level of network unbundling, 2005

0 0,5 1 1,5 2 2,5 3 3,5 4 4,5 5

GreeceLuxembourg

CyprusCzech Republic

EstoniaHungary

IrelandLatvia

PolandSlovakiaSlovenia

AustriaBelgium

DenmarkFrance

GermanyLithuania

FinlandItaly

NetherlandsPortugal

SpainSweden

UK†

Unbundling index (5 max)

Distribution system operatorTransmission system operator

April 20, 2006 F. Gubina

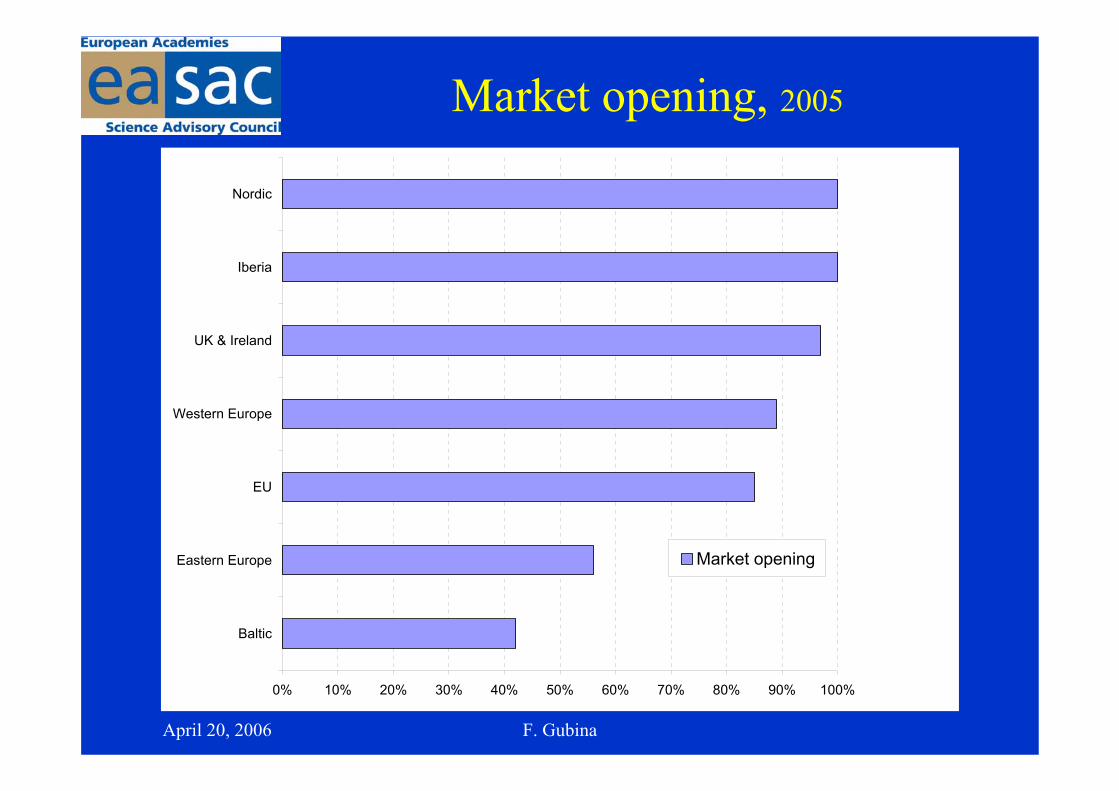

Market opening, 2005

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Baltic

Eastern Europe

EU

Western Europe

UK & Ireland

Iberia

Nordic

Market opening

April 20, 2006 F. Gubina

Regulatory independence, 2003

April 20, 2006 F. Gubina

Competition in retail and generation, 2005

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Poland

Italy

Czech Republic

Germany

Hungary

UK

Austria

Nordic

Slovenia

Slovakia

Spain

France

Ireland

Netherlands

Belgium

Latvia

Portugal

Cyprus

Greece

Lithuania

MaltaSh

are

(%)

Country

Largest producer bycapacity**

Top 3 suppliers' share(all consumers)

To high market power?

April 20, 2006 F. Gubina

Level of customers switching supplier, 2005

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Cyprus

Estonia

Greece

Latvia

Malta

Portugal

Luxembourg

Poland

Slovakia

Slovenia

Italy

Lithuania

Spain

Austria

France

Hungary

Netherlands

Belgium

Germany

Denmark

Finland

Ireland

Sweden

UK

Small commercial / domesticLarge eligible industrial users

April 20, 2006 F. Gubina

Pricing structures

• Tariffs:– Liberalisation let to more competing tariffs,– Number of tariffs reduced with market regulation,– Social tariffs to domestic customers,– Industrial consumers have a wider choice of tariffs than

domestic customers.• Price convergence:

– Regions reached more price convergence than EU as a whole,

– Convergence of prices improves with stronger interconnection,

• Accession members without electricity taxes.

April 20, 2006 F. Gubina

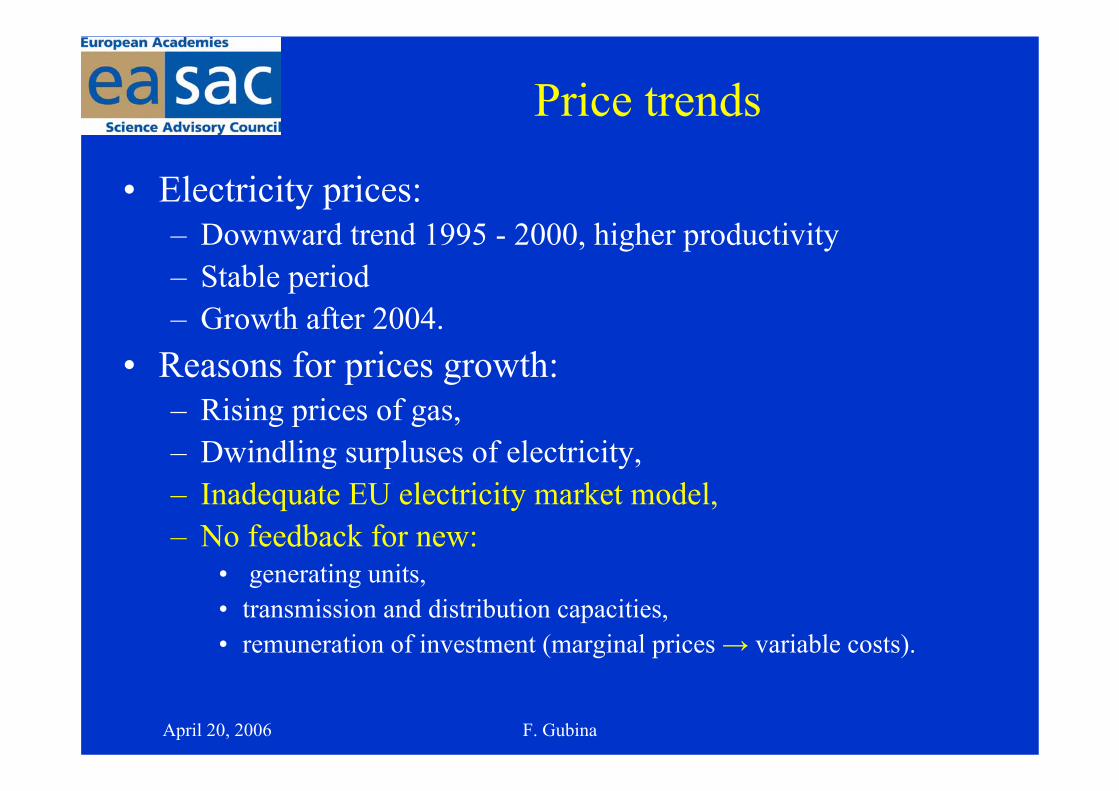

Price trends

• Electricity prices:– Downward trend 1995 - 2000, higher productivity– Stable period– Growth after 2004.

• Reasons for prices growth:– Rising prices of gas,– Dwindling surpluses of electricity,– Inadequate EU electricity market model,– No feedback for new:

• generating units,• transmission and distribution capacities,• remuneration of investment (marginal prices → variable costs).

April 20, 2006 F. Gubina

Average price development

Consumer

3.5 MWh/year

Industrialconsumer

2.0 MWh/year

April 20, 2006 F. Gubina

Price convergence- Coefficient of variation

April 20, 2006 F. Gubina

Breakdown of electricity prices, 2004

(50 MWh /year customer) (€/MWh before taxes)

April 20, 2006 F. Gubina

ETA impact on electricity prices

• Emission trading allowances (ETA) for CO2:– Producer obtains the certificates,– If he needs more he has to buy them in the market.

• Market prices of allowances:– Significant initial price transient,– Less impact on the end user than on wholesale prices (long term contracts),– Industry can not get compensation for its losses.

• Auction could:– Finance the CO2 reduction or– Transfer wealth from polluters to government or reverse,– Appropriate model required.

• Simulation (by sparks spreads): – Most if not all of the allowance cost passed into electricity wholesale price,– Estimated impact on wholesale electricity price (20 - 30)%

• Lack of empirical evidence to judge (to short time).

April 20, 2006 F. Gubina

Price evolution of emission allowance

€

–Shot up in the summer 2005 (due to increased gas prices, drought and adverse weather),–Stabilized afterwards,

April 20, 2006 F. Gubina

Marginal costs and wholesale power prices2005

CO2

April 20, 2006 F. Gubina

Spark spreads (Simulation results)(=the difference between electricity prices and fuel costs for gas plants)

Since the spark spread net allowances are equal the sector passes on its entire costs

April 20, 2006 F. Gubina

Retail prices in Slovenia (band 2003-2005)

Gibanje cen za PAS med leti 2007 do 2009

30,00

35,00

40,00

45,00

50,00

55,00

01.10

.2003

01.12

.2003

01.02

.2004

01.04

.2004

01.06

.2004

01.08

.2004

01.10

.2004

01.12

.2004

01.02

.2005

01.04

.2005

01.06

.2005

01.08

.2005

01.10

.2005

01.12

.2005

datum oblikovanja cene

EUR

/ M

Wh

PAS 07 PAS 08 PAS 09

April 20, 2006 F. Gubina

Long term contracts

• Lack of long-term contracts is considered to be the sole reason behind the California electricity crisis.

• Relatively low energy volume in the EU spot markets.• Reasons:

– High market power of producers in EU electricity market, – Industrial electricity users shield themselves from the volatility of the

market prices - risk reduction,– Collusive activity less attractive,– Ensuring stability of prices,– Encourage investment in a very capital-intensive, slow-return industry,– Incentive for entering new providers,– Timing of essential maintenance work - increase of electricity availability,

• Will not solve growing problem of production and supply mismatch.

April 20, 2006 F. Gubina

Conclusions

• The report: – on various aspect of EU electricity markets and– suggestion for policies development.

• Desirable:– Increasing cross-border connectivity,– Promoting long-term contracts,– Continuous monitoring of price development,– Electricity market model correction to accommodate the

growing problem of production and supply mismatch.• Emission trading scheme:

– Positive for controlling emissions,– Model should be monitored for its possible adverse effects.