Prestudy China eCommerce Growth, 27.10.2015

14

China’s ecommerce boom opens up for new opportunities INNOVATION BUSINESS ACCELERATOR ERIC CHENG, [email protected] OCTOBER 22, 2015

Transcript of Prestudy China eCommerce Growth, 27.10.2015

China’s ecommerce

boom opens up for

new opportunities

INNOVATION BUSINESS ACCELERATOR

ERIC CHENG, [email protected]

OCTOBER 22, 2015

China ecommerce Market Overview

Despite a macroeconomic slowdown in China,

online consumer spending is growing at close to

50 %, particularly in fast-growing second and

third-tier cities.

The Chinese Government is supportive of

ecommerce as it’s in line with their long-held

policy aim of driving domestic consumption.

China has around 417 million online consumers.

According to China’s National Bureau of Statistic,

China online shopping accounts for about 10.7 %of total retail sales of consumer goods.

According to eMarketer ecommerce will

account for nearly 30 % of all retail sales in 2018.

$472,91

$672,01

$911,25

$1 208,31

$1 568,39

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

0

200

400

600

800

1000

1200

1400

1600

1800

Y 2014 Y 2015 Y 2016 Y 2017 Y 2018

Billio

n U

SD

Year

Retail ecommerce sales in China 2014-2018

Retail eCommerce

Sales

% Change

% of total retail sales

Ecommerce Market – Two Main

Players control 80 % of the Market

Around 90 % of the online retail transactions in China occur on

marketplaces – including Taobao, TMall – where

manufacturers, retailers and

individuals list products to sell

to consumers.

Alibaba’s Tmall holds the

largest market share with more

than 60 % of retail ecommerce

sales in 2014. Alibaba has an

even more commanding share

of mobile retail ecommerce

and C2C sales, at over 85 %.

61,40%

18,60%

3,20%

2,90%

1,70%

1,40%

1,30%

1,30%

1,10%

0,70%

6,50%

0% 10% 20% 30% 40% 50% 60% 70%

Tmall

JD.com

Suning

vip.com

Gome

Yihaodian

Dangdang

Amazon.cn

Yixun

Jumei

Other

B2C Retail E-commerce Sales Share in China, by Site, 2014

Ecommerce Trends & Developments

MOBILE

BRICK AND MORTAR ARE

TURNING INTO “PRODUCT

SHOW ROOM”

GROWTH IN RURAL AREAS

THE RISE OF CROSS-BORDER

ECOMMERCE

FROM C2C

TO B2C

Connected Consumers – Drivers

According to Nielsen research, the typical online buyer of imported products in China is

female, younger than 30 and with an income of more than RMB 11,000 per month.

Frequently cited reasons for shopping online include:

Accessibility

Convenience

Low prices

Greater assortment

Detailed product information & customer reviews

Confidence: consumers place higher levels of trust in the authenticity of purchases

made on major B2C platforms such as Tmall, JD.com and Yihaodian

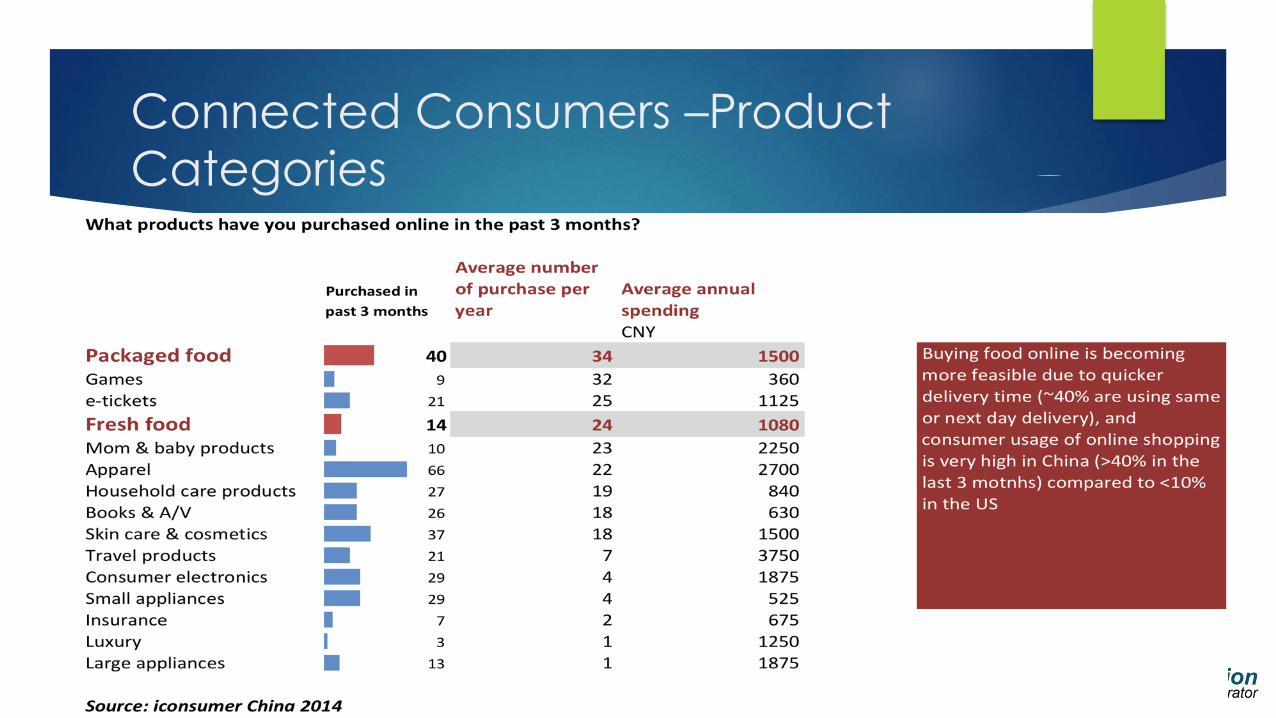

Connected Consumers –Product

Categories

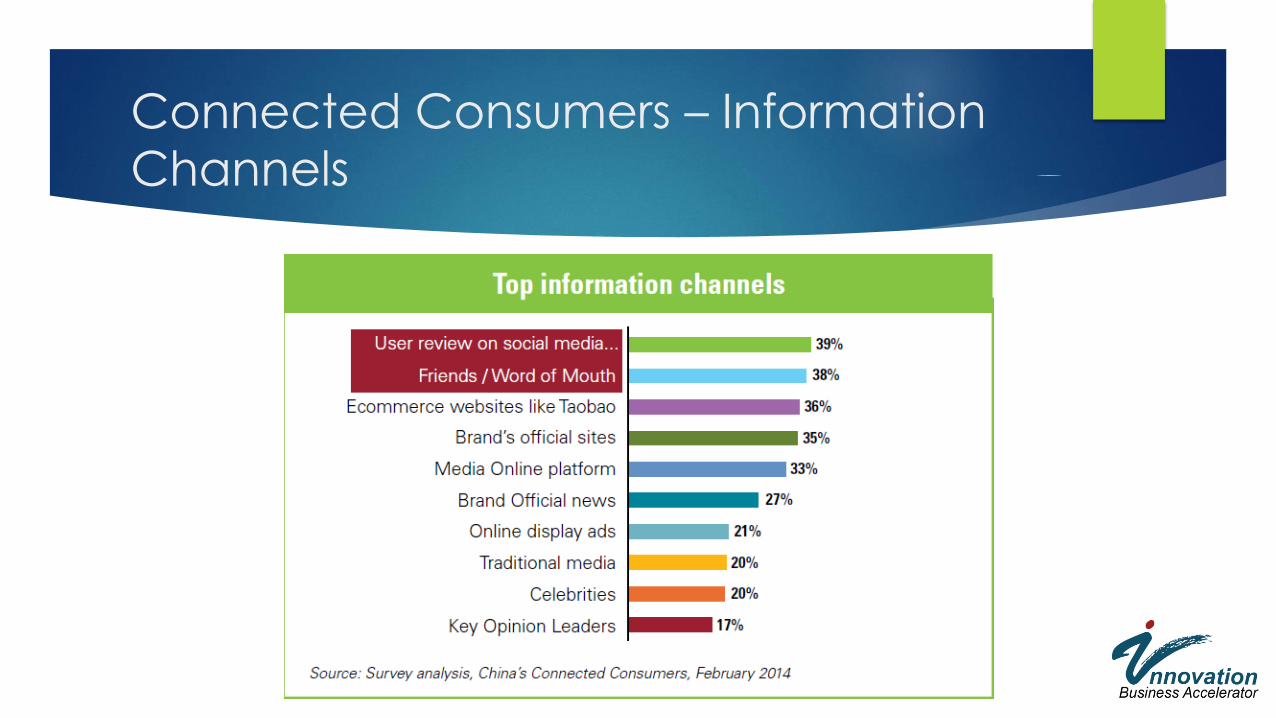

Connected Consumers – Information

Channels

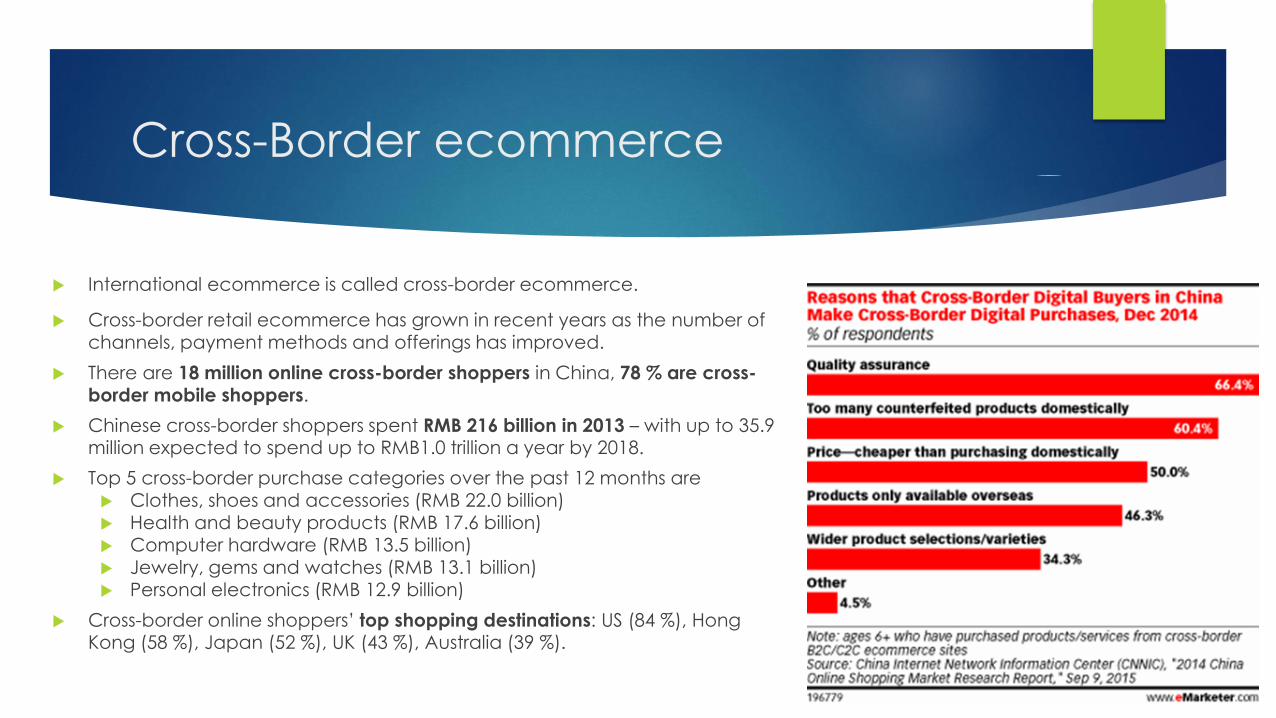

Cross-Border ecommerce

International ecommerce is called cross-border ecommerce.

Cross-border retail ecommerce has grown in recent years as the number of channels, payment methods and offerings has improved.

There are 18 million online cross-border shoppers in China, 78 % are cross-border mobile shoppers.

Chinese cross-border shoppers spent RMB 216 billion in 2013 – with up to 35.9 million expected to spend up to RMB1.0 trillion a year by 2018.

Top 5 cross-border purchase categories over the past 12 months are Clothes, shoes and accessories (RMB 22.0 billion) Health and beauty products (RMB 17.6 billion) Computer hardware (RMB 13.5 billion)

Jewelry, gems and watches (RMB 13.1 billion) Personal electronics (RMB 12.9 billion)

Cross-border online shoppers’ top shopping destinations: US (84 %), Hong Kong (58 %), Japan (52 %), UK (43 %), Australia (39 %).

Cross-Border vs Ordinary Trade

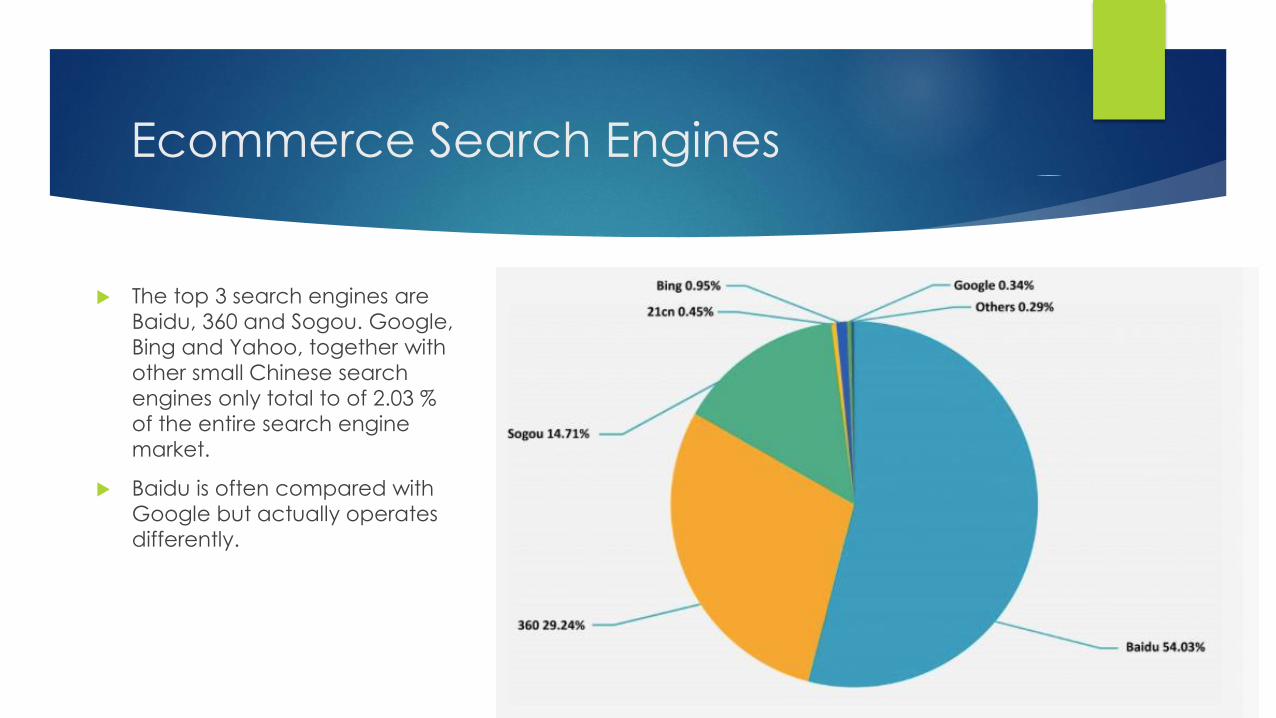

Ecommerce Search Engines

The top 3 search engines are

Baidu, 360 and Sogou. Google,

Bing and Yahoo, together with

other small Chinese search

engines only total to of 2.03 %

of the entire search engine

market.

Baidu is often compared with

Google but actually operates

differently.

Ecommerce Marketplace vs Brand Store

Marketplace store (Tmall, JD)

90 % of all sales

50 % of the brand’s SKUs (mainly bestsellers)

Heavy marketing

Needs a perfect quality of service (chat function, etc)

Sales are public

Volume driven

Enclosed world –the marketplace owns the customers and the data

Vague search results on Baidu

Brand store (.cn store)

10 % of all sales (some brands have less than 1 % sale on their own website)

Full assortment of SKUs

Branding

History

Values

E-magazine

Shop locator

OmniChannel

eCRM

Digital marketing in China is dominated

by local players

Tmall

Taobao

Baidu

Alipay

Wechat / Weibo

Youku / Tudou

Amazon

eBay

Paypal

Facebook / Twitter

Youtube

Future Trends & Market Demand

Aspirational trading up

Chinese buyers continuously look for products that:

have strong brand heritage outside of China

replace local brands that are not trusted (particularly if the end user is

an infant or is elderly)

are innovative and novel

are lifestyle products (e.g. healthcare, vitamins and education)

are ‘natural’ alternatives to artificial products.

Summary

Despite a macroeconomic slowdown in China, online consumer spending is growing at close

to 50 % a year, particularly in fast-growing second and third-tier cities.

Mobile is the most commonly used device for making online purchases.

Apparel is the most popular and widely purchased product. Packaged foods are the most

frequent products people purchase online.

Some18 million Chinese are already paying premium prices for foreign products like food,

cosmetics and luxury items. These are directly imported through ‘cross- border’ ecommerce

trading platforms in seven cities.

The reduced import taxes and simpler quarantine and inspection procedures within these B2C

cross-border channels presents new entry channels and opportunities to Finnish companies.

Digital marketing in China is dominated by local players.

China’s online consumers will continue to trade up and look for specialized imported products.