presents FAS 109 and Valuations of Deferred Tax...

66

presents FAS 109 and Valuations of Deferred Tax Assets Tackling Tough Valuation and Disclosure Challenges for NOLs and Other presents Delayed Benefits A Live 110-Minute Teleconference/Webinar with Interactive Q&A Today's panel features: Charles Chubb, Managing Director, WTAS LLC, Philadelphia David Bussius, CPA, Managing Director, Tax Group, CBIZ Tofias, Providence, R.I. Mark Sumlin, Senior Director, Alvarez & Marsal Taxand, Chicago Layne Albert, Managing Director , Alvarez & Marsal Taxand, Houston Ron Cohen, Partner, Greenstein Rogoff Olsen & Co., Fremont, Calif. Wednesday, June 9, 2010 The conference begins at: The conference begins at: 1 pm Eastern 12 pm Central 11 am Mountain 10 am Pacific 10 am Pacific You can access the audio portion of the conference on the telephone or by using your computer's speakers. Please refer to the dial in/ log in instructions emailed to registrations.

-

Upload

duongthuan -

Category

Documents

-

view

215 -

download

0

Transcript of presents FAS 109 and Valuations of Deferred Tax...

presents

FAS 109 and Valuations of Deferred Tax Assets Tackling Tough Valuation and Disclosure Challenges for NOLs and Other

presents

Delayed Benefits

A Live 110-Minute Teleconference/Webinar with Interactive Q&A

Today's panel features:Charles Chubb, Managing Director, WTAS LLC, Philadelphia

David Bussius, CPA, Managing Director, Tax Group, CBIZ Tofias, Providence, R.I.Mark Sumlin, Senior Director, Alvarez & Marsal Taxand, Chicago

Layne Albert, Managing Director, Alvarez & Marsal Taxand, Houstony , g g , ,Ron Cohen, Partner, Greenstein Rogoff Olsen & Co., Fremont, Calif.

Wednesday, June 9, 2010

The conference begins at:The conference begins at:1 pm Eastern12 pm Central

11 am Mountain10 am Pacific10 am Pacific

You can access the audio portion of the conference on the telephone or by using your computer's speakers.Please refer to the dial in/ log in instructions emailed to registrations.

For Continuing Education purposes, gplease let us know how many people are listening at your location by g y y

• closing the notification box • and typing in the chat box your• and typing in the chat box your

company name and the number of attendeesattendees.

• Then click the blue icon beside the box to sendto send.

For live event only

• If the sound quality is not satisfactory• If the sound quality is not satisfactory and you are listening via your computer speakers please dial 1-866-873-1442speakers, please dial 1 866 873 1442 and enter your PIN when prompted. Otherwise, please send us a chat or e-, pmail [email protected] so we can address the problem.

• If you dialed in and have any difficulties during the call, press *0 for assistance.

FAS 109 And Valuations OfFAS 109 And Valuations Of Deferred Tax Assets Webinar

June 9, 2010

Charles Chubb, WTAS [email protected]

M k S li Al & M l L Alb t Al & M l

David Bussius, CBIZ Tofias [email protected]

Mark Sumlin, Alvarez & Marsal Layne Albert, Alvarez & [email protected] [email protected]

Ron Cohen, Greenstein, Rogoff, Olsen & [email protected]

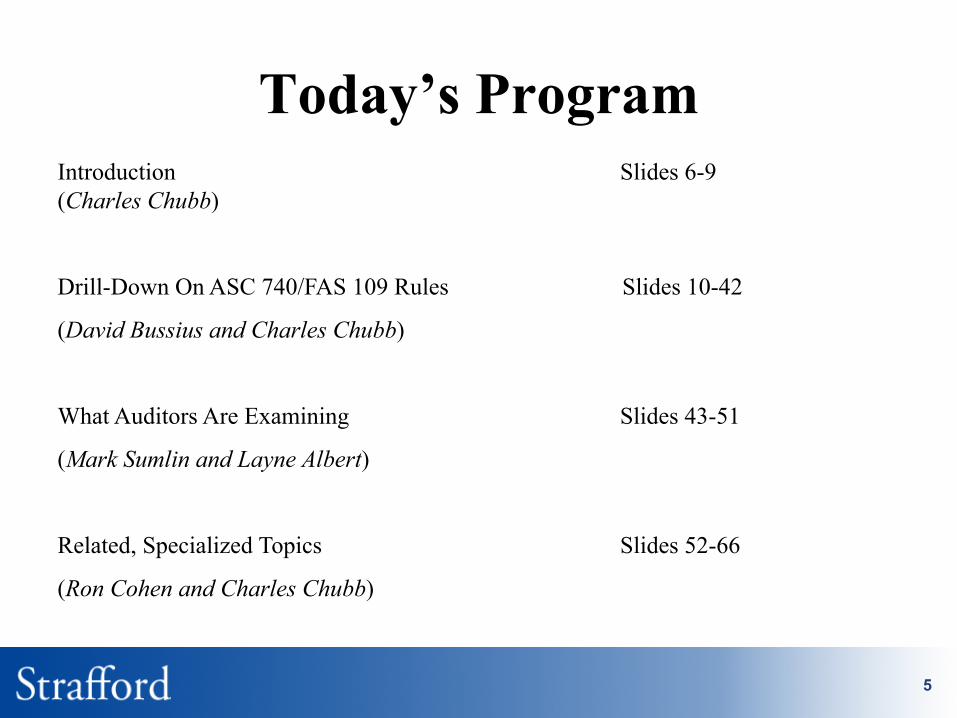

Today’s ProgramToday s ProgramIntroduction Slides 6-9 (Charles Chubb)(Charles Chubb)

Drill-Down On ASC 740/FAS 109 Rules Slides 10-42

(David Bussius and Charles Chubb)

Wh t A dit A E i i Slid 43 51What Auditors Are Examining Slides 43-51

(Mark Sumlin and Layne Albert)

Related, Specialized Topics Slides 52-66

(Ron Cohen and Charles Chubb)

5

Introduction

Charles Chubb, WTAS LLCCharles Chubb, WTAS LLC

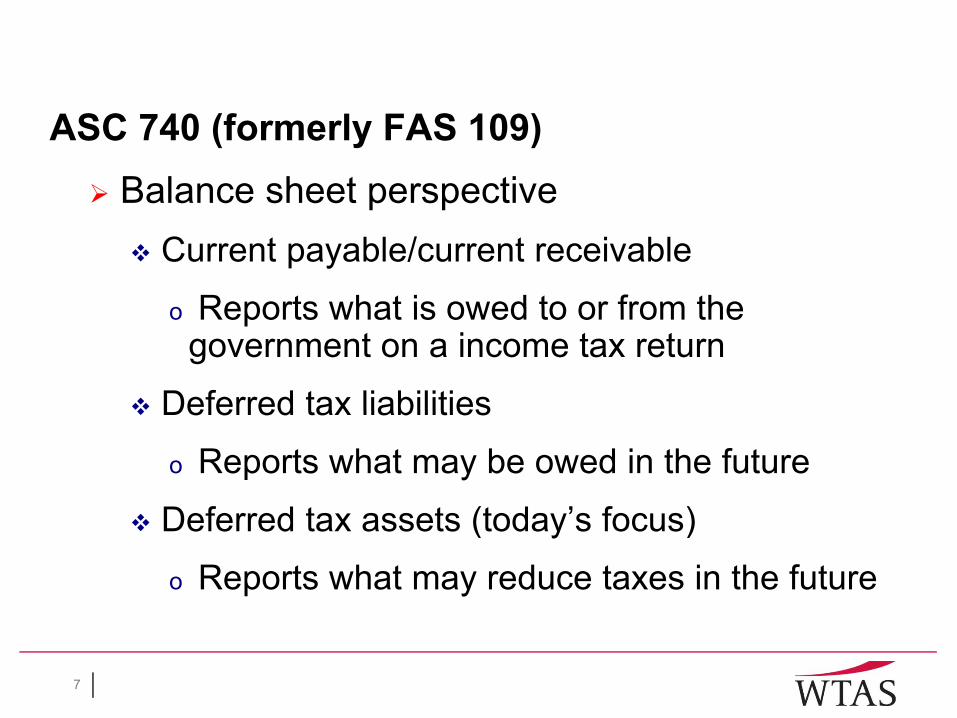

ASC 740 (formerly FAS 109)Balance sheet perspectivep p

Current payable/current receivable

o Reports what is owed to or from theo Reports what is owed to or from the government on a income tax return

Deferred tax liabilitiesDeferred tax liabilities

o Reports what may be owed in the future

D f d t t (t d ’ f )Deferred tax assets (today’s focus)

o Reports what may reduce taxes in the future

7

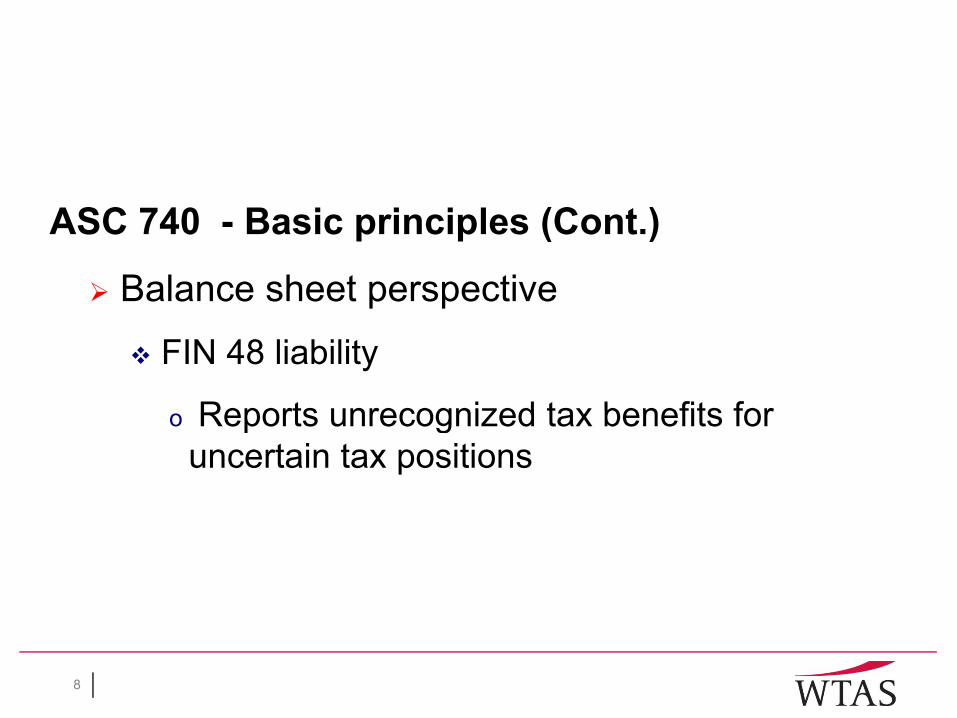

ASC 740 - Basic principles (Cont.)

Balance sheet perspectivep p

FIN 48 liability

Reports unrecognized tax benefits foro Reports unrecognized tax benefits for uncertain tax positions

8

ASC 740 - Basic principles (Cont.)

GAAP (generally accepted accountingGAAP (generally accepted accounting principles) – Provide the guidelines in evaluating the amounts reported in the financial g pstatements

Key point: FAS 109 is governed byKey point: FAS 109 is governed by accounting standards, and many of the important principles in FAS 109 are similar to other elements of the financial statement accounting.

9

Drill-Down On ASC 740/FAS 109 R l740/FAS 109 Rules

David Bussius, CBIZ TofiasDavid Bussius, CBIZ Tofias Charles Chubb, WTAS LLC

Overview

• Valuation allowance defined

– Financial accounting principle that reduces a deferred tax asset to its net realizable value

– The conceptual framework is similar to evaluating other assets on the balance sheet.

• Accounts receivable• Intangibles

11

Overview (Cont.)

• A deferred tax asset must be reduced by a valuation allowance if based on:

– … the weight of all the evidence available it is more likely than not (a likelihood of > 50%) that somelikely than not (a likelihood of 50%) that some portion or all of the deferred tax asset will not be realized.

12

Overview (Cont.)

• Valuation allowances do not deal with the existence ofValuation allowances do not deal with the existence of the asset; instead they address the realizability of an asset.

– This is an important distinction from ASC 450 (formerly FAS 5) and ASC 740-10 (formerly FIN 48)(formerly FAS 5) and ASC 740-10 (formerly FIN 48), which determine whether an asset is recognizable (meets the criteria to be benefitted).

• For example: A net operating loss [NOL] created through an aggressive tax position on a tax returnthrough an aggressive tax position on a tax return may not be recognizable.

13

Overview (Cont.)

• All available evidence, both positive and negative, needs to be considered.

• Assessing the need for and amount of a valuation allowance for DTAs requires significant judgment.allowance for DTAs requires significant judgment.– Early coordination with the F/S auditors is important

to avoid/reconcile inconsistencies between the ’ d dit ’ j d tcompany’s and auditor’s judgments.

14

Key Concepts

• Realizability: The question is:– “Will the company have enough future taxable income

t li h b fit?to realize a cash benefit?

• More likely than not (> 50%) standard

• Positive and negative evidence: Weight given based on objective verifiability– Key concept: Must be based upon documentation

that supports conclusion reached by company and also provide adequate financial statement auditalso provide adequate financial statement audit support

15

Key Concepts (Cont.)Evaluation

Analysis is done on a separate jurisdiction-by-jurisdiction basisjurisdiction basis

Important concept in evaluating multi-national or multi-state groupsmulti state groups

o Winners-and-losers issueOften missed in groups that are profitable overall but ghave some loss companies.

o Other positive or negative evidence may be different among the jurisdictions.among the jurisdictions.

Scheduling out the reversal of temporary differences may be required

16

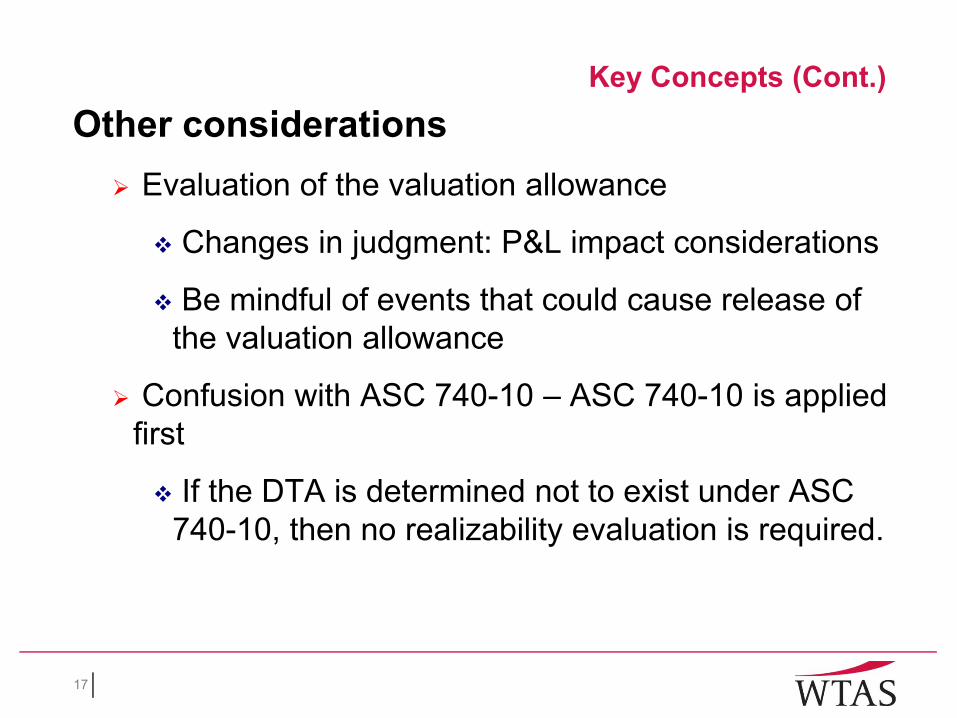

Key Concepts (Cont.)Other considerations

Evaluation of the valuation allowance

Changes in judgment: P&L impact considerations

Be mindful of events that could cause release ofBe mindful of events that could cause release of the valuation allowance

Confusion with ASC 740-10 – ASC 740-10 is applied ppfirst

If the DTA is determined not to exist under ASC 740-10, then no realizability evaluation is required.

17

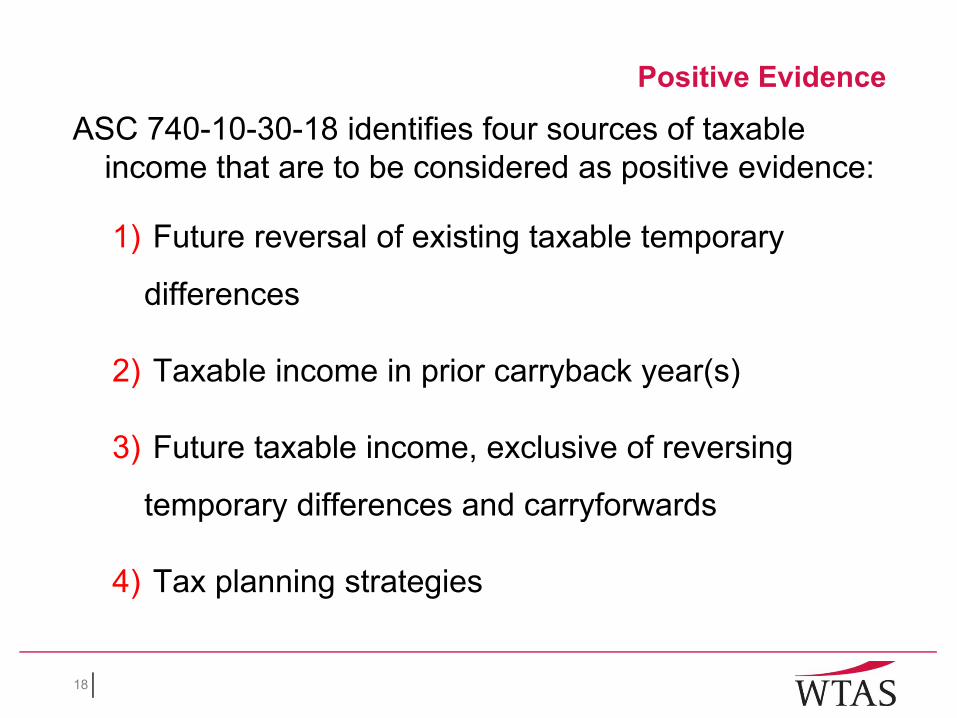

Positive Evidence

ASC 740-10-30-18 identifies four sources of taxable income that are to be considered as positive evidence:

1) Future reversal of existing taxable temporary

differences

2) Taxable income in prior carryback year(s)

3) Future taxable income, exclusive of reversing

temporary differences and carryforwardstemporary differences and carryforwards

4) Tax planning strategies

18

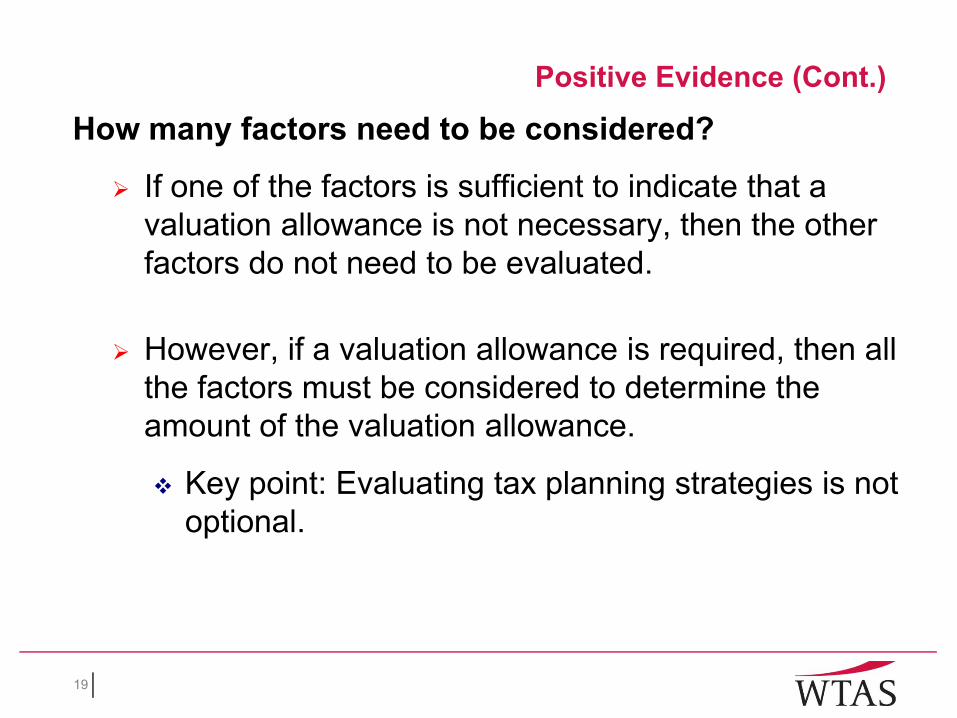

Positive Evidence (Cont.)

How many factors need to be considered?

If one of the factors is sufficient to indicate that a valuation allowance is not necessary, then the other factors do not need to be evaluated.

However, if a valuation allowance is required, then all the factors must be considered to determine the amount of the valuation allowance.

Key point: Evaluating tax planning strategies is not ti loptional.

19

Positive Evidence (Cont.)

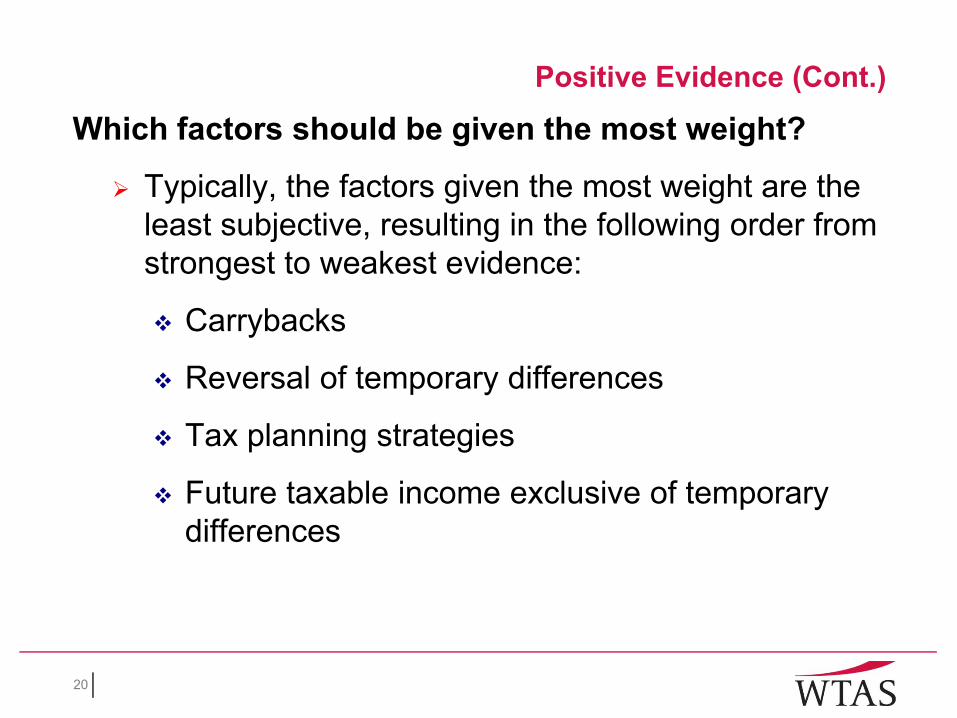

Which factors should be given the most weight?

Typically, the factors given the most weight are the least subjective, resulting in the following order from strongest to weakest evidence:

Carrybacks

Reversal of temporary differences

Tax planning strategies

Future taxable income exclusive of temporary differences

20

Positive Evidence (Cont.)

• Future reversal of existing taxable temporary difference

– Consideration must be given to the timing of the reversal of the temporary differences into taxable income.income.

– Assumes zero book income

21

Positive Evidence (Cont.)

• Future reversal of existing taxable temporary difference (Cont.)

M ti i diff b d t– Many timing differences based on current reserves (i.e. payroll accruals) reverse in one year.

– Other DTAs are more challengingOther DTAs are more challenging• Warranty reserves• Depreciation

22

Positive Evidence (Cont.)

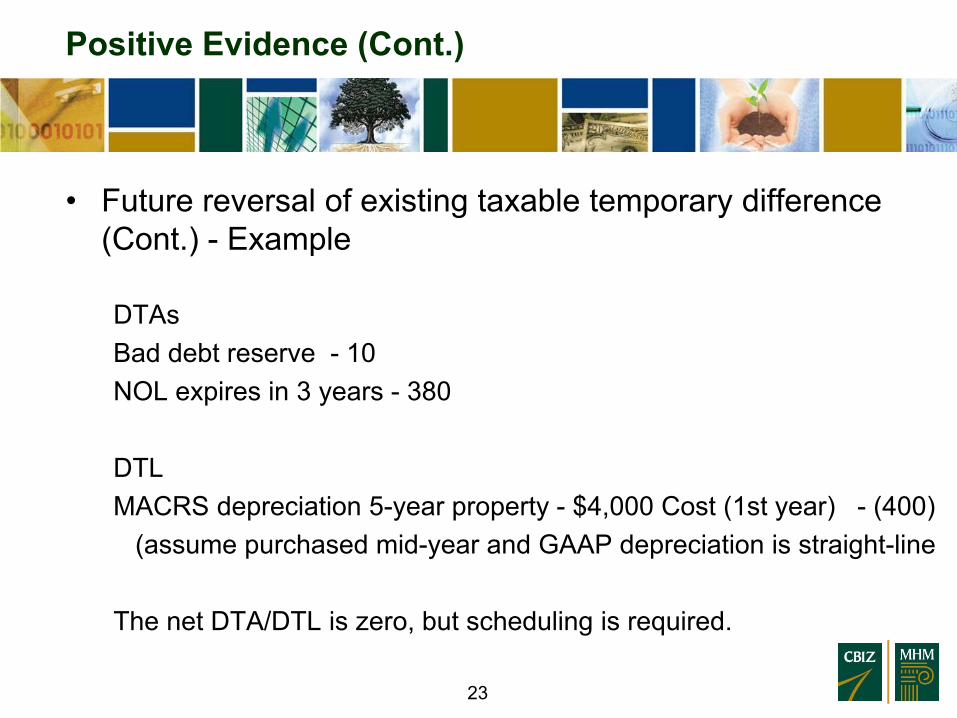

• Future reversal of existing taxable temporary differenceFuture reversal of existing taxable temporary difference (Cont.) - Example

DTADTAsBad debt reserve - 10NOL expires in 3 years - 380

DTLMACRS depreciation 5-year property - $4,000 Cost (1st year) - (400)MACRS depreciation 5 year property $4,000 Cost (1st year) (400)

(assume purchased mid-year and GAAP depreciation is straight-line

Th t DTA/DTL i b t h d li i i dThe net DTA/DTL is zero, but scheduling is required.

23

Positive Evidence (Cont.)

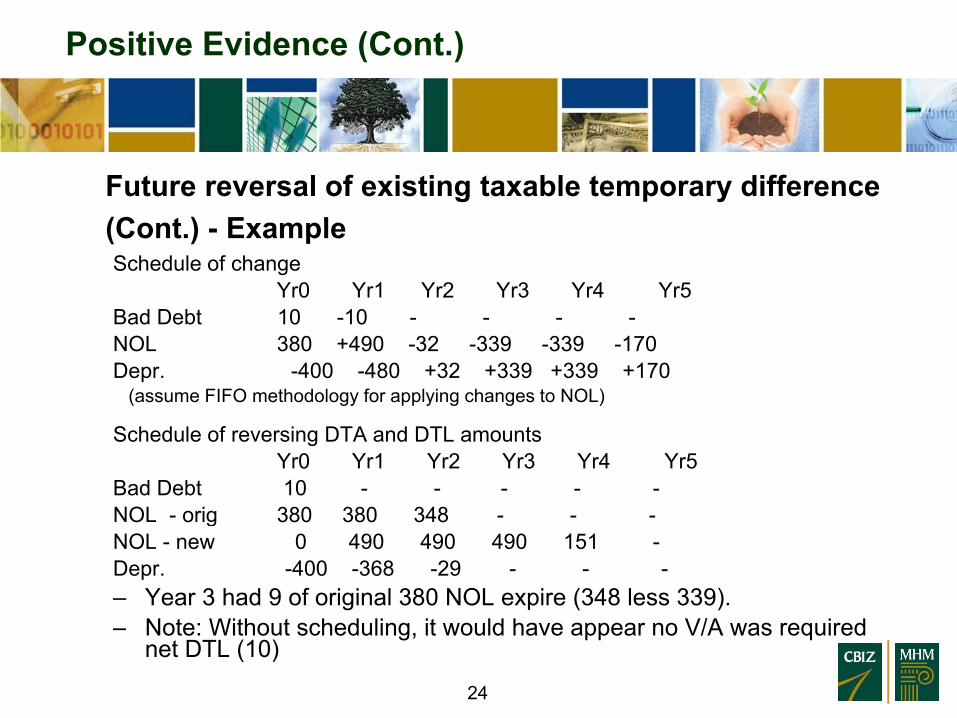

Future reversal of existing taxable temporary difference (Cont.) - ExampleSchedule of change

Yr0 Yr1 Yr2 Yr3 Yr4 Yr5Bad Debt 10 -10 - - - -NOL 380 +490 -32 -339 -339 -170Depr. -400 -480 +32 +339 +339 +170

(assume FIFO methodology for applying changes to NOL)

Schedule of reversing DTA and DTL amounts Yr0 Yr1 Yr2 Yr3 Yr4 Yr5

Bad Debt 10 - - - - -NOL orig 380 380 348NOL - orig 380 380 348 - - -NOL - new 0 490 490 490 151 -Depr. -400 -368 -29 - - -– Year 3 had 9 of original 380 NOL expire (348 less 339).– Note: Without scheduling, it would have appear no V/A was required

net DTL (10)

24

Positive Evidence (Cont.)

• Future reversal of existing taxable temporary difference (Cont.)

– DTLs related to indefinite lived intangibles cannot be used to benefit most deferred tax assets (Exception: ( pFederal AMT credits).

• Re-enforces the gross DTA vs. net DTA requirement of ASC 740requirement of ASC 740

25

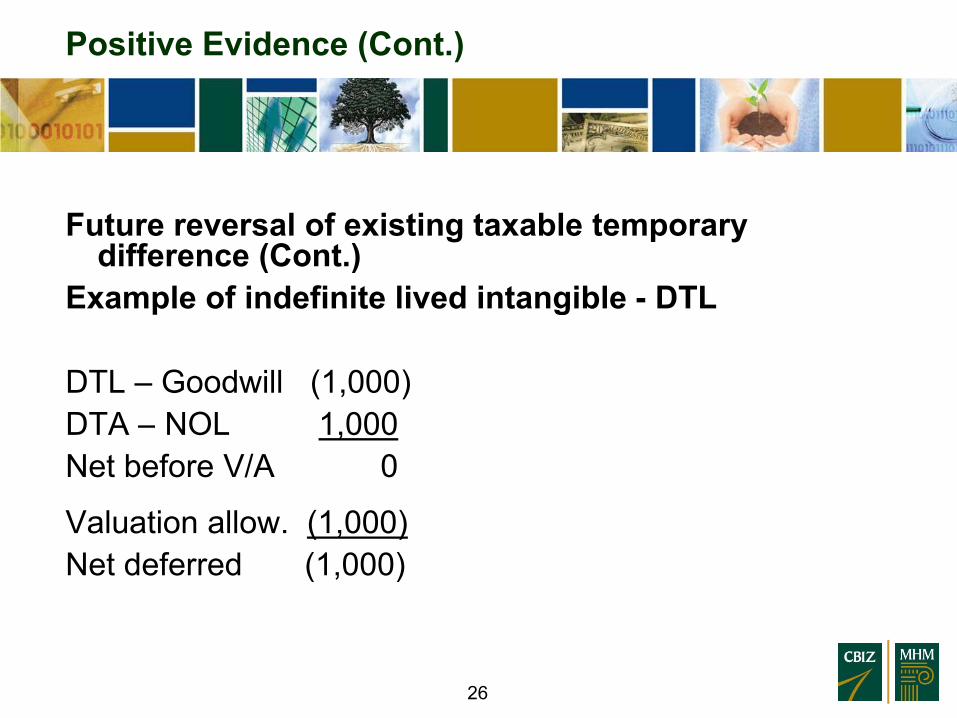

Positive Evidence (Cont.)

Future reversal of existing taxable temporary difference (Cont.)

Example of indefinite lived intangible - DTLExample of indefinite lived intangible DTL

DTL – Goodwill (1,000)DTA – NOL 1,000Net before V/A 0

V l ti ll (1 000)Valuation allow. (1,000)Net deferred (1,000)

26

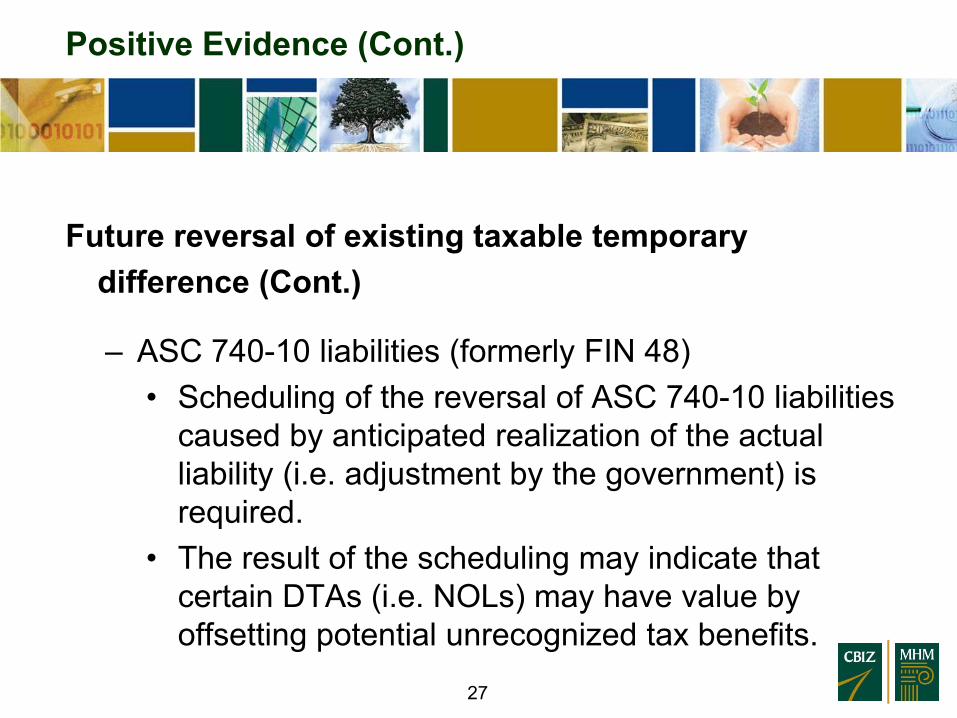

Positive Evidence (Cont.)

Future reversal of existing taxable temporary difference (Cont.)

– ASC 740-10 liabilities (formerly FIN 48)• Scheduling of the reversal of ASC 740-10 liabilities g

caused by anticipated realization of the actual liability (i.e. adjustment by the government) is requiredrequired.

• The result of the scheduling may indicate that certain DTAs (i.e. NOLs) may have value by offsetting potential unrecognized tax benefits.

27

Positive Evidence (Cont.)

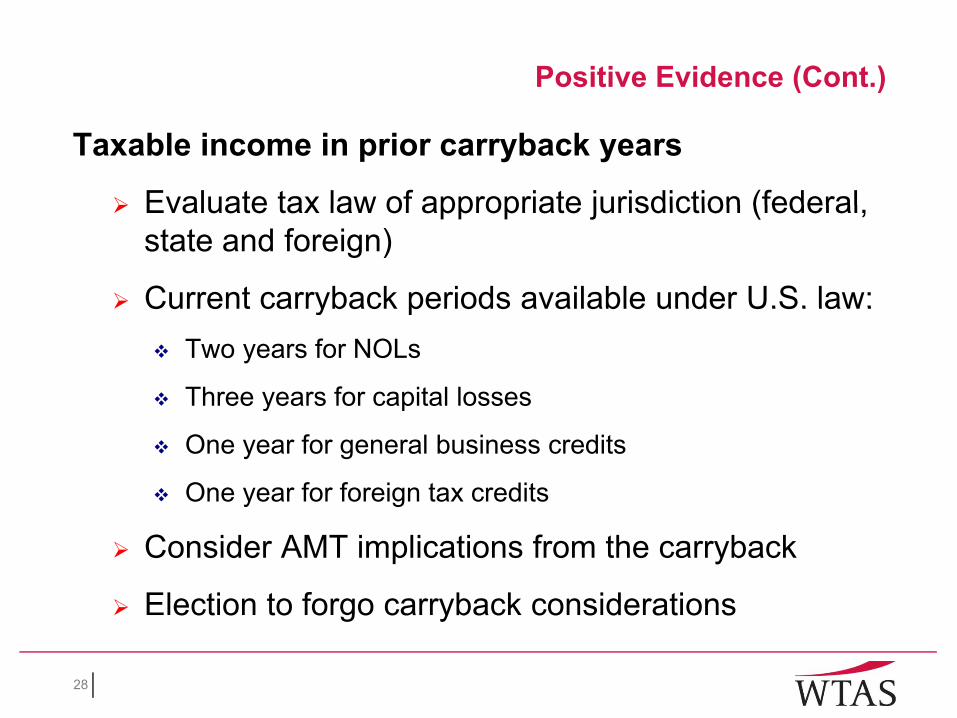

Taxable income in prior carryback years

Evaluate tax law of appropriate jurisdiction (federalEvaluate tax law of appropriate jurisdiction (federal, state and foreign)

Current carryback periods available under U.S. law:Current carryback periods available under U.S. law:Two years for NOLs

Three years for capital lossesy p

One year for general business credits

One year for foreign tax credits

Consider AMT implications from the carryback

Election to forgo carryback considerations

28

ect o to o go ca ybac co s de at o s

Positive Evidence (Cont.)

Future taxable income, exclusive of reversing temporary differences and carryforwards

Anticipates new permanent and temporary differences

The reversing of historic temporary differences is accounted for in a separate evaluation.

In practice, book income is often used, when permanent and future temporary items are not a significant factorsignificant factor.

29

Positive Evidence (Cont.)Future taxable income, exclusive of reversing

temporary differences and carryforwards (Cont.)P j ti f f t t b k iProjections of future years pre-tax book income

Needs to be consistent with other projections used by company (i e goodwill impairmentused by company (i.e. goodwill impairment analysis)

Considerations related to how many years to project

Character and nature of historic losses

Quality of future projectionsy p j

o History of performance against prior plan

As this is the most subjective area, often a

30

j ,relatively short period is allowed.

Positive Evidence (Cont.)

Future taxable income, exclusive of reversing temporary differences and carryforwards (Cont.)

Character of DTA may affect analysis

Capital losses

Foreign tax creditsForeign tax creditso May be planning idea to elect to expense foreign taxes

rather than taking the credit to avoid valuation allowance

31

Positive Evidence (Cont.)

Tax planning strategiesTax planning strategies that could accelerate income p g gso that the company can take advantage of future deductible differences

ASC 740-10-30-19 provides criteria:

Prudent and feasible

Company ordinarily might not take, but would take to prevent an operating loss or tax credit carryforward from expiring unusedcarryforward from expiring unused

Would result in realization of deferred tax assets

32

o Not the minimization of DTLs

Positive Evidence (Cont.)

Tax planning strategies (Cont.)The company does not have to actually implement p y y pthe strategy.

In practice, some auditors have attempted to apply a higher standard regarding the likelihood of implementing the strategy.

S fSignificant expenses to implement a tax-planning strategy or any significant losses that would be recognized if that strategy were implemented (net of g gy p (any recognizable tax benefits associated with those expenses or losses) shall be included in the valuation allowance

33

allowance.

Positive Evidence (Cont.)

Tax planning strategies (Cont.)

P iti lPositive examples

Sale-leaseback of operating assets

(Substitution Issue)

Sale of appreciated marketable securities

Sale of loans with bad debt to reduce reversal period

Changing of filing methods – elect to file g g gconsolidated

34

Positive Evidence (Cont.)

Tax planning strategies (Cont.)

Examples that do not qualifyExamples that do not qualify

Sale of core assets

Cost red ction initiati esCost reduction initiatives

Change of filing status from C corp. to S corp.

35

Positive Evidence (Cont.)

Other positive evidence

Existing contracts or sales backlogExisting contracts or sales backlog

Appreciated asset value over tax value

Strong earnings history

36

Negative Evidence

Examples of negative evidence

Cumulative losses in recent years (generally use a three-y (g y

year period)

Hi t f ti l t dit f dHistory of operating loss or tax credit carryforwards

expiring unused

Expectation of future losses

Contingencies with material adverse long-term affectsContingencies with material adverse long-term affects

Short carryover periods

37

Financial Statement Considerations

Recording and releasing a valuation allowance differs based on how the deferred tax assets were recorded

Operating activities– Operating activities– Other comprehensive income (appreciation of securities in

current period)

Important to tag the deferred tax asset to which the valuation allowance relates, to verify that it reverses properly.p ope y

– In some cases, an NOL created through stock options deductions (APIC-related) is comingled with operating NOLs (P/L-related). An election is available to deem which is assumed to be used first.

38

Financial Statement Considerations (Cont.)

The valuation allowance for a particular jurisdiction will be allocated between current and non-current deferred tax assets on a pro rata basis determined by the ratio ofassets on a pro-rata basis, determined by the ratio of current and non-current DTAs over total DTAs) (ASC 740-10-45-5).In general, DTAs and DTLs are classified on the balance sheet as current or long-term based on how the related assets and liabilities are classified for financial reportingassets and liabilities are classified for financial reporting purposes. If the DTA or DTL does not relate to a specific asset or liability, then it will be classified based on when th diff i t d t b li dthe difference is expected to be realized.

39

Business Combinations

• Acquired company’s establishment of a valuation allowance at acquisition– Recorded as part of purchase price accountingRecorded as part of purchase price accounting

• Acquired company valuation allowance subsequent to acquisition– Recorded through income tax expense Acquiring company V/A reduction caused by an acquisition• Acquiring company V/A reduction caused by an acquisition– Affects provision expense

• Acquiring company V/A increase caused by an acquisition– Affects provision expense

40

Interim Considerations

ASC 740-270 approach for quarterly provisions– Annual projected effective rate

• Effect of valuation allowance• Effect of valuation allowance– Reduction in valuation allowance related to current-year

projected income increase is accounted for in the projected annual effective rateannual effective rate.

– Changes in judgment related to historic valuation allowance requirements are a discrete item accounted for in that period.

Judgments regarding recording or reversing valuation• Judgments regarding recording or reversing valuation allowances should be considered EVERY quarter.

41

Disclaimer

The opinions and analyses expressed herein do not necessarily reflect those of WTAS LLC or any affiliate thereof. Any suggestions contained herein are general, and do notLLC or any affiliate thereof. Any suggestions contained herein are general, and do not take into account an individual’s specific circumstances or applicable governing law, which may vary from jurisdiction to jurisdiction and be subject to change.

No warranty or representation, express or implied, is made by WTAS LLC, nor doesNo warranty or representation, express or implied, is made by WTAS LLC, nor does the WTAS LLC accept any liability with respect to the information and data set forth herein. Distribution hereof does not constitute legal, tax, accounting or other professional advice. Recipients should consult their professional advisors prior to acting on the information set forth herein.acting on the information set forth herein.

© COPYRIGHT 2008 WTAS LLC ALL RIGHTS RESERVED.

No part of this presentation may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of WTAS LLC.

42

What Auditors Are E i iExamining

Mark Sumlin, Alvarez & MarsalMark Sumlin, Alvarez & Marsal Layne Albert, Alvarez & Marsal

Objectives

I. Determining the need for a valuation allowance

II. Considerations in assessing whether the gallowance is adequate

III Internal control issues related to valuation allowances andIII. Internal control issues related to valuation allowances and changes in the determination regarding the measurement

IV D t i t l th d f d tifi ti fIV. Document appropriately the need for and quantification of a valuation allowance

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved. 44

Disclosures

I. The adequacy and consistency of disclosures also have been challenged. Auditors will not allow assertions, whether stated or implied, in the forepart of the prospectus for a public offering or a periodic report that are inconsistent with the assumptions used in the preparation of the financial statements.

II. Additional disclosures regarding valuation allowances may be required by ASC 275, Risks and Uncertainties. When it is at least reasonably possible that a material adjustment of the valuation allowance will occur in the near term, the financial statements must disclose this possibility.

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved. 45

Internal Control Implications

I. Does the company appropriately document its position with respect to the discrete events that give rise to the determinations made related to the need for a valuation

ll ?allowance?II. Does the company have a methodology in place for assessing

the realizability of deferred tax assets, such that the need for a l ti ll b dd d i th i tvaluation allowance can be addressed in the appropriate

period?III. Does the company have effectively operating internal controls

th t b th ti i t d t th l f l tithat both anticipate and support the release of a valuation allowance?

IV. When changes to the measurement of a valuation allowance d th i l h i ti t ti foccur, do they imply a change in estimate or correction of a

prior period error?

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved. 46

Internal Control Procedures

I. Tax reviews with Finance Department the annual forecast and/or actual results, to monitor profit/loss jurisdictions.

II. Any changes in the business environment are incorporated into II. Any changes in the business environment are incorporated into the analysis of whether a valuation allowance is necessary.

III. Maintain documentation on the type and nature of all tax attributes, including how they will be realizedattributes, including how they will be realized

IV. Monitor statute limitations on tax attributes, including forecasts for potential expiration

V Consider scheduling the reversal of significant deferred taxV. Consider scheduling the reversal of significant deferred tax liabilities

VI. Track pending legislation and law changes that have been enacted in varying jurisdictionsenacted in varying jurisdictions

VII. Maintain a rolling three-year cumulative loss computation for relevant jurisdictions

VIII P f f l i ll

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved.

VIII. Prepare forecast of valuation allowance movement

47

Auditing Considerations – Valuation Allowance

I. Determine whether valuation allowance is reasonable in light of grelevant factorso Experience, knowledge and authority of those responsible for

determining allowanceo Management’s motivationso Whether outside experts and consultants are usedo Whether management monitors the reasonableness of the

ltresultso Whether policies and procedures are refined when errors are

detectedManagement’s internal process for communication ando Management s internal process for communication and information sharing between tax and others (treasury, legal, etc.)

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved. 48

Auditing Considerations – Valuation Allowance (Cont.)

I. Audit procedures applied using the following:p pp g go An understanding of the company’s business, industry and

tax positionso An understanding of the company’s valuation allowance

determination process o Weight given negative and positive evidence is

commensurate, to the extent it can be objectively verifiedE l ti f i bilit f t’ t ti b to Evaluation of viability of management’s expectations about future taxable income − Identification of significant elements in plan

Evidential matter in support of plan− Evidential matter in support of plan− Consider bases for significant assumptions

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved. 49

Auditing Considerations – Valuation Allowance (Cont.)

I. Making an assessment as to whether positive evidence outweighs negative evidence in determining the need for and outweighs negative evidence in determining the need for and amount of a valuation allowance requires considerable judgment (a subjective process)

II. The extent of audit scrutiny with respect to the valuation allowance will vary based on specific facts and circumstances (e.g., significance of deferred tax assets and the extent of(e.g., significance of deferred tax assets and the extent of positive and negative evidence surrounding its realizability)

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved. 50

Notice

I. These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

II. Any tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

© Copyright 2010. Alvarez & Marsal Holdings, LLC. All Rights Reserved. 51

Related, Specialized T iTopics

Ron Cohen, Greenstein, Rogoff, Olsen & Co.Ron Cohen, Greenstein, Rogoff, Olsen & Co. Charles Chubb, WTAS LLC

Determination Of Valuation Allowances

• Analysis is done on a separate jurisdiction-by-jurisdiction basis– Important concept in evaluating multi-national or multi-state p p g

group• Winners-and-losers issue

– Often missed in groups that are profitable overall, but have some loss companies in the group.

• Other positive or negative evidence may be different among the jurisdictions.

– Scheduling out the reversal of temporary differences may be required.

53

FIN 48 Applied First And Stabilized

– Confusion with FIN 48; FIN 48 is applied first• If the DTA is determined not to exist under FIN 48, then no

realizability evaluation is required regarding a valuation y q g gallowance.

• Uncertain tax positions• Unfiled IRS Forms 5471 and 5472 – Open yearsUnfiled IRS Forms 5471 and 5472 Open years• Cost-sharing arrangements and “buy-in” controversies with the

IRS• Unfiled state returns in various states• Unfiled state returns in various states

• Aggressive transfer pricing, Sect. 6662 risks

54

FIN 48

• FIN 48 … is it ever stable?- Ongoing tax audits, with issues evolving- Tax court cases: Xilinx on stock options and cost-sharing. Taxpayer

wins then lose on appeals then wins on rehearing; waiting to learnwins, then lose on appeals, then wins on rehearing; waiting to learn whether IRS will appeal

UNCERTAINTY! Possible restatement of NOLs and tax credits that are part of the DTAare part of the DTA

Silicon Valley experience with FIN 48: Months and months or work and “re-dos” as Big Four rejects analysis

55

Expenses Of A Tax Planning Strategy

– Significant expenses to implement a tax-planning strategy or any significant losses that would be recognized if that strategy were implemented (net of any recognizable tax benefits associated with those expenses or losses) shall be included in the valuation allowance.

-- Lawyers, accountants, tax litigation costs can be very significant.

-- My experience with capital gain generator deals The CPA firm-- My experience with capital gain generator deals. The CPA firm wanted 50% of the tax benefit from an expiring capital loss.

56

Consistency Of ProjectionsFuture taxable income, exclusive of reversing temporary differences

and carryforwards (Cont.)

– Projections of future years pre-tax book income• Needs to be consistent with other projections used by the

company (i.e. goodwill impairment analysis). Client is often very uncertain about the future, and we must make this “land” to apply test.

– Considerations related to how many years to project• Character and nature of historic losses• Quality of future projections (General Motors!)

– History of performance against prior plan• As this is the most subjective area, often a relatively short

period is allowed.

57

Foreign Tax Credit Fun!Foreign Tax Credit Fun!• Character of DTA may affect analysis

• Capital losses• Foreign tax credits – Planning strategies

– May be planning idea to elect to expense foreign taxes rather than take the credit to avoid valuation allowance

– Multi-national company with “deferral Strategy” via offshore holding company … timing and utilization of FTC can be of mind-numbing complexity … by year, by g p y y y , y“basket”, overall foreign loss carryforwards, Sect. 861-8 allocations. Check out Forms 5471 and 1118 instructions. Also, PFIC and Subpart F? Tremendous complexity in repatriation policy for a multi-national corporation. Question: What if we pay a dividend? Very hard to evaluate; is E&P study needed?

58

Practical Reality?• Start-ups, development-stage businesses

- No book income in sight?M t k th d ill l ti ll- Management knows the drill on valuation allowances.

• Other , more mature businesses- The CROSS-OVER PERIOD IS MOST COMPLEX

- Company moving into profits (for the first time) or ending a profitable period. Example: General Motors, where billions of DTAs had to be expensed.

- Always watch for corporate AMT- Anticipated use of tax NOL and tax credit DTA can be limited.

• Obviously, VERY close work with tax department/advisors is needed Obv ous y, V c ose wo w a depa e /adv so s s eededto avoid an earnings or tax footnote error.

59

Bad Experiences

• DTA valuation allowance analysis goes right to CFO, CEO and board of directors.

• “Don’t you believe in us?”

• “Do you really need to book that valuation allowance?”Do you really need to book that valuation allowance?

• “You’re killing our EPS, and Wall Street will drop the stock price!”

• “Maybe you’re not the right CPA firm.”

60

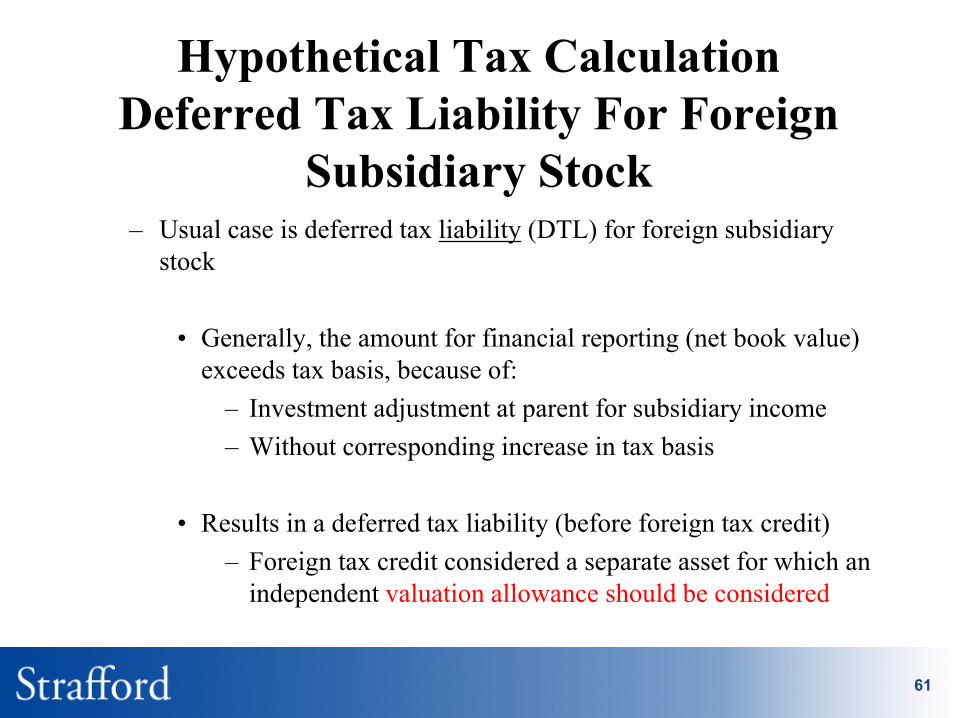

Hypothetical Tax CalculationD f d T Li bilit F F iDeferred Tax Liability For Foreign

Subsidiary Stock– Usual case is deferred tax liability (DTL) for foreign subsidiary

stock

• Generally, the amount for financial reporting (net book value) exceeds tax basis, because of:

– Investment adjustment at parent for subsidiary income– Investment adjustment at parent for subsidiary income– Without corresponding increase in tax basis

• Results in a deferred tax liability (before foreign tax credit)– Foreign tax credit considered a separate asset for which an

independent valuation allowance should be considered

61

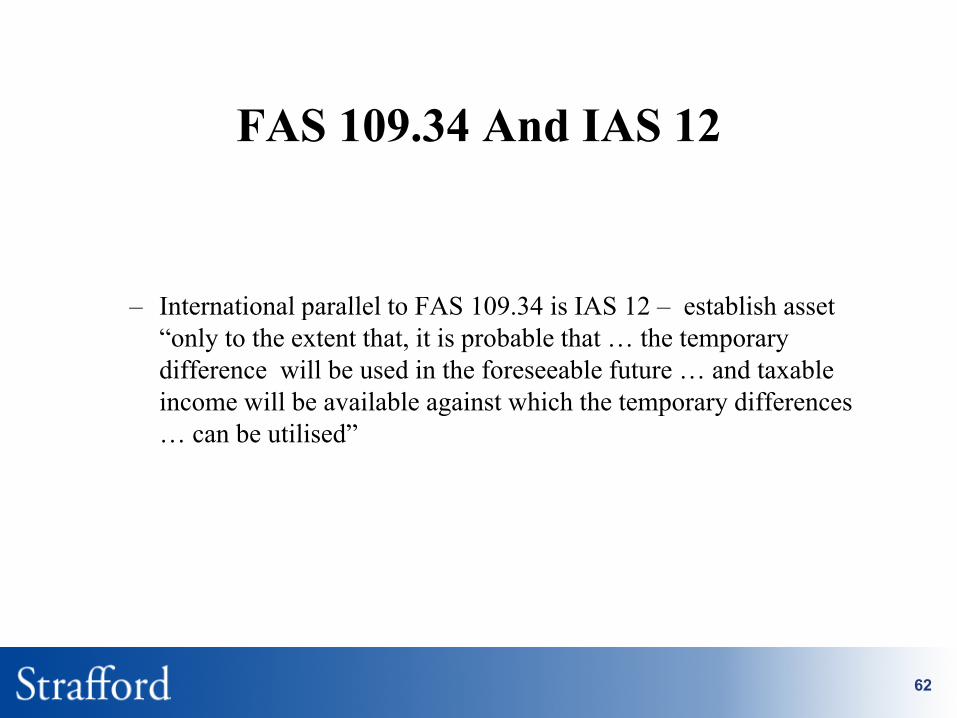

FAS 109.34 And IAS 12

International parallel to FAS 109 34 is IAS 12 establish asset– International parallel to FAS 109.34 is IAS 12 – establish asset “only to the extent that, it is probable that … the temporary difference will be used in the foreseeable future … and taxable income will be available against which the temporary differencesincome will be available against which the temporary differences … can be utilised”

62

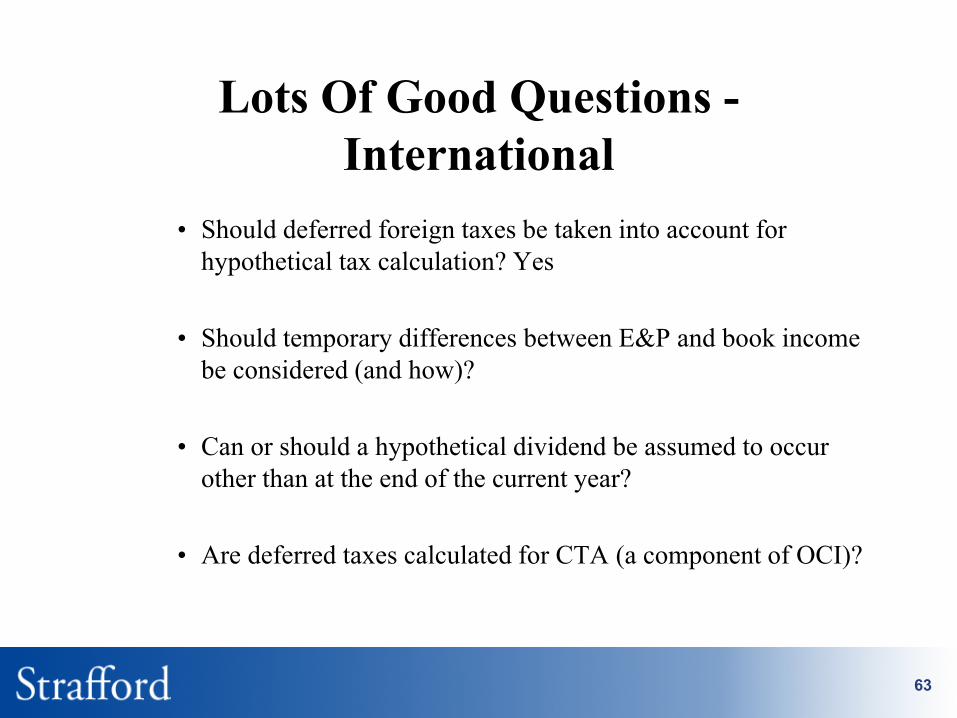

Lots Of Good Questions -Lots Of Good Questions -International

• Should deferred foreign taxes be taken into account for hypothetical tax calculation? Yes

• Should temporary differences between E&P and book income be considered (and how)?

• Can or should a hypothetical dividend be assumed to occur other than at the end of the current year?

• Are deferred taxes calculated for CTA (a component of OCI)?

63

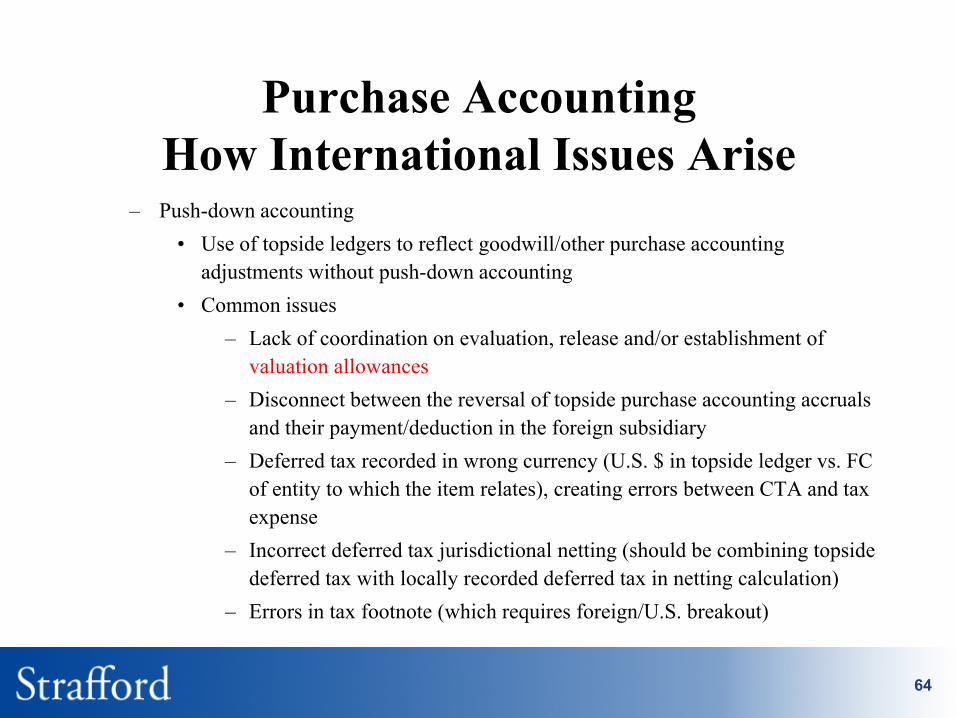

Purchase AccountingPurchase AccountingHow International Issues AriseP h d ti– Push-down accounting

• Use of topside ledgers to reflect goodwill/other purchase accounting adjustments without push-down accounting

• Common issuesCommon issues– Lack of coordination on evaluation, release and/or establishment of

valuation allowances– Disconnect between the reversal of topside purchase accounting accruals p p g

and their payment/deduction in the foreign subsidiary– Deferred tax recorded in wrong currency (U.S. $ in topside ledger vs. FC

of entity to which the item relates), creating errors between CTA and tax expense

– Incorrect deferred tax jurisdictional netting (should be combining topside deferred tax with locally recorded deferred tax in netting calculation)

– Errors in tax footnote (which requires foreign/U S breakout)Errors in tax footnote (which requires foreign/U.S. breakout)

64

Other International ValuationOther International Valuation Allowance Issues

– Difficulties getting tax information regarding acquired company)

• Tax basis of assets and liabilities

Changes to ta basis from transaction (if an )• Changes to tax basis from transaction (if any)

• Tax contingencies/FIN 48

• Tax attributes, such as net operating losses under foreign tax laws

– Determining valuation allowance for deferred tax assets

• Consider tax planning strategies

Don’t miss transfer pricing (losses of a foreign subsidiary that– Don t miss transfer pricing (losses of a foreign subsidiary that are the result of, or can be controlled by, transfer pricing should be carefully evaluated)

I l i i lid t d/ bi d t ti• Inclusion in a consolidated/combined tax reporting group

65

Additional International Issues

– Unidentified exposures

• Transfer pricing (which is also a FIN 48 issue)

• Loss of beneficial tax status (e.g. tax holiday). So now, utilization of a DTA will occur, and valuation allowance is not req iredrequired.

• Permanent establishment issues – Need to file returns and pay tax, so DTA is recognized/valuation allowance reduced, g

66