Presented by - saudiarabia-jccme.jp · PDF fileIn Y2012, IFCs Doing Business Ranked KSA on the...

35

25 th September 2013 Presented by Mr. Venkatesan Subramanian VP & Global Leader- Metals & Minerals

Transcript of Presented by - saudiarabia-jccme.jp · PDF fileIn Y2012, IFCs Doing Business Ranked KSA on the...

25th September 2013

Presented by Mr. Venkatesan Subramanian VP & Global Leader- Metals & Minerals

Story Board for Non-Oil Wealth Diversification-

GCC Region

KSA

Need for Non-Oil Wealth Diversification- GCC Region

The Dependence on Oil – The Need for Diversification

Non-oil vs Oil GDP contribution (%)

Bahrain

UAE

Qatar

Iran

Oman

Saudi Arabia

GCC Overall

Oil Non- Oil

Real GDP Growth, Oil-Exporting Countries (Annual percent change)

Source: Frost & Sullivan Mega Trends for GCC Industrialization.

IMF, International Financial Statistics; and IMF Staff estimates.

In Y2012, Real GDP Growth of Oil exporters (Especially GCCs) had witnessed improvements in

non-oil sectors

Major Government based oil companies & investment bodies are venturing into the Aluminium industry in GCC to diversify and take advantage of the low cost utilities & further value additions it can offer

which will boost the GDP and oftake the risk of diminishing oil reserves in the region.

Where KSA Economy is Heading?

Source: IMF

KSA - GDP Growth (%) Forecast- Oil & Non-Oil

FDI Trend: KSA Market ($ Mn)

Anticipated FDIs in non-oil segment, especially Metals &

Mining sector to drive the GDP

In Y2012, IFCs Doing Business Ranked KSA on the following:

3rd - Paying Tax 12th – Getting Electricity

19th - Protecting Investors 22nd – Ease of Doing Business 36th – Trading Across Border

With non-oil GDP easing at 6% growth in Y2013, FDIs focused on non-oil segments will continue to grow- especially metals, minerals

and fabricated products

* Rank 1 – 185

Primary Metal - Feedstock

Downstream Potential

Power Advantage- 1/3rd of Cost of Production

Proximity - Strategic Location

Liquid aluminium from GCC smelters. Only about 25% smelter utilization rate whereas rest is exported

Aluminium downstream industry still under – developed apart from extrusion which is also heavily focused only in construction industry

Proximity to end – user markets in major geographies like Europe, Americas & Asia

Power Tariffs (US cent/KWh)

KSA 3.2

GCC 3.8

World Avg. 8.5

1 2

3 4

Key Advantages

~ 3

.5 m

illio

n M

T

The MENA region is likely to be a powerhouse for aluminum production and downstream, driven largely by the following four factors:

Source: Frost & Sullivan.

Captive bauxite mine and alumina

refinery in KSA

The KSA Downstream Advantage : 3 Ps (Power/Primary Liquid Metal /Proximity)

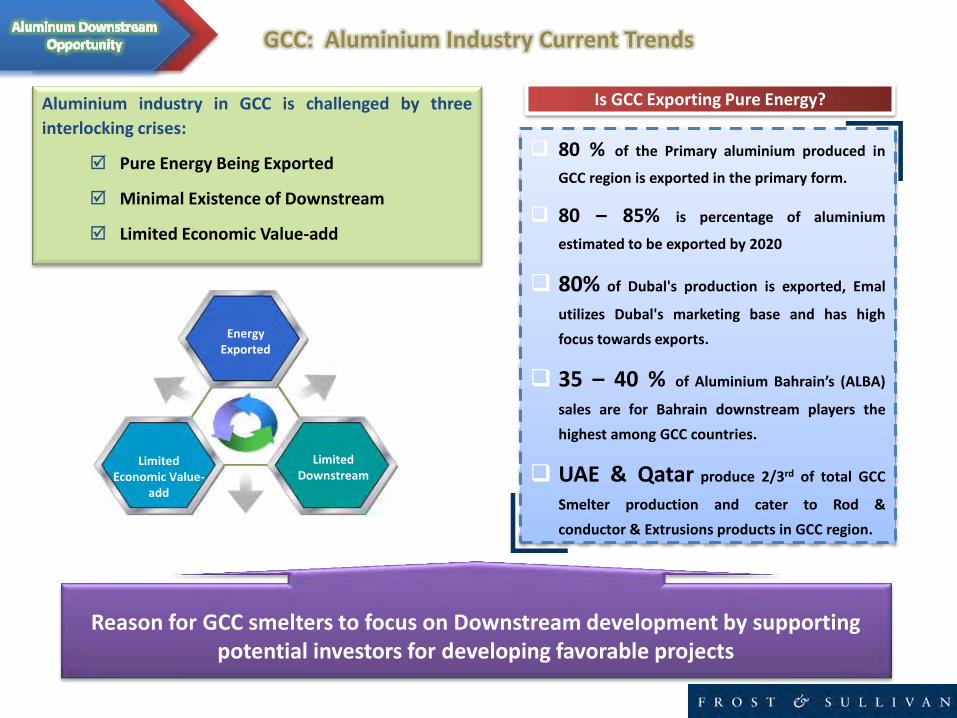

80 % of the Primary aluminium produced in

GCC region is exported in the primary form.

80 – 85% is percentage of aluminium

estimated to be exported by 2020

80% of Dubal's production is exported, Emal

utilizes Dubal's marketing base and has high

focus towards exports.

35 – 40 % of Aluminium Bahrain’s (ALBA)

sales are for Bahrain downstream players the

highest among GCC countries.

UAE & Qatar produce 2/3rd of total GCC

Smelter production and cater to Rod &

conductor & Extrusions products in GCC region.

Aluminium industry in GCC is challenged by three

interlocking crises:

Pure Energy Being Exported

Minimal Existence of Downstream

Limited Economic Value-add

Is GCC Exporting Pure Energy?

Energy Exported

Limited Downstream

Limited Economic Value-

add

GCC: Aluminium Industry Current Trends

Reason for GCC smelters to focus on Downstream development by supporting potential investors for developing favorable projects

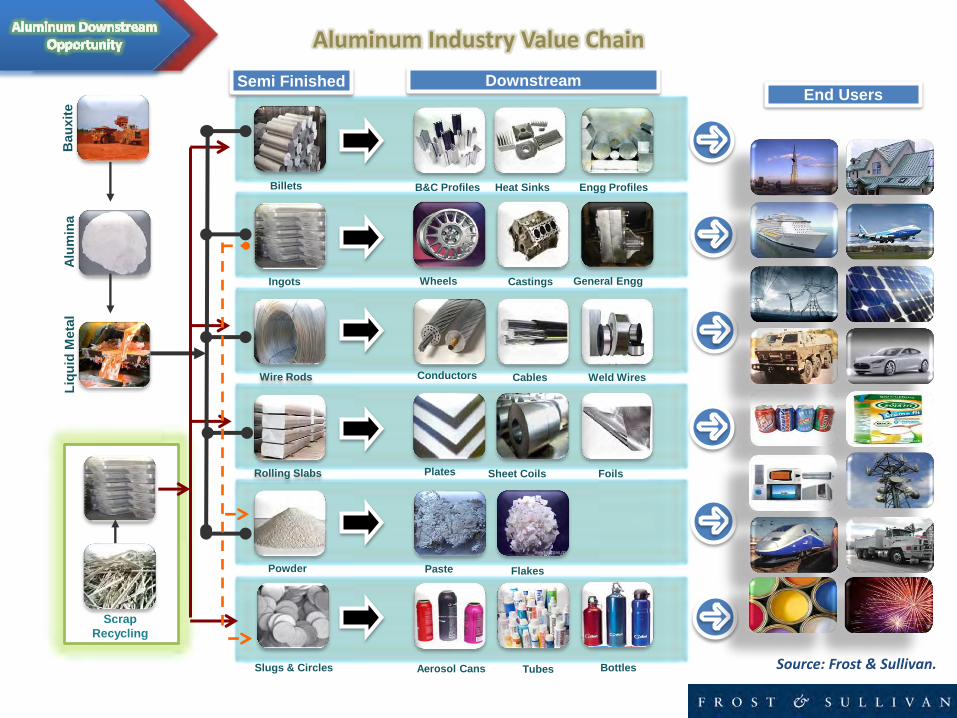

Billets

Ingots

Wire Rods

Rolling Slabs

Powder

Slugs & Circles

B&C Profiles

Wheels Castings

Conductors Cables Weld Wires

Plates Sheet Coils Foils

Paste Flakes

Aerosol Cans Tubes Bottles

Scrap

Recycling

Bau

xit

e

Alu

min

a

Liq

uid

Meta

l

Heat Sinks

Engg Profiles

General Engg

`

`

Semi Finished Downstream End Users

Source: Frost & Sullivan.

Aluminum Industry Value Chain

Implications for KSA

Economic Triggers - KSA

With the current progress of Ninth Five year plan (2009-14) to accelerate the pace of economic growth & attract FDI (currently slowed down) to diversify economic base …

National Industry Strategy (NIS) goal to increase the contribution of the manufacturing sector to the GDP to 20% by the Y 2020 from the current 11%”

Indicators Targeted Average Annual Growth Rate (%)

Real Gross Domestic Product (GDP) 5.2

Gross Fixed Capital Formation (GFCF) 10.4

Merchandise and Services Exports 4.5

Non-oil Exports 10.0

Final Consumption 5.4

Rate of Saudization (%) (By end of plan) 53.6

Unemployment Rate (%) (By end of plan) 5.5

Economic 360 Perspective: Key Indicators for the Ninth Five Year Plan, KSA, 2009–2014 To attract FDI into KSA

Increased focus on

diversification & investments

Significant impact on

Aluminum markets

0

10

20

30

40

2005 2006 2007 2008 2009 2010 2011 2012

FDI ($Bn)

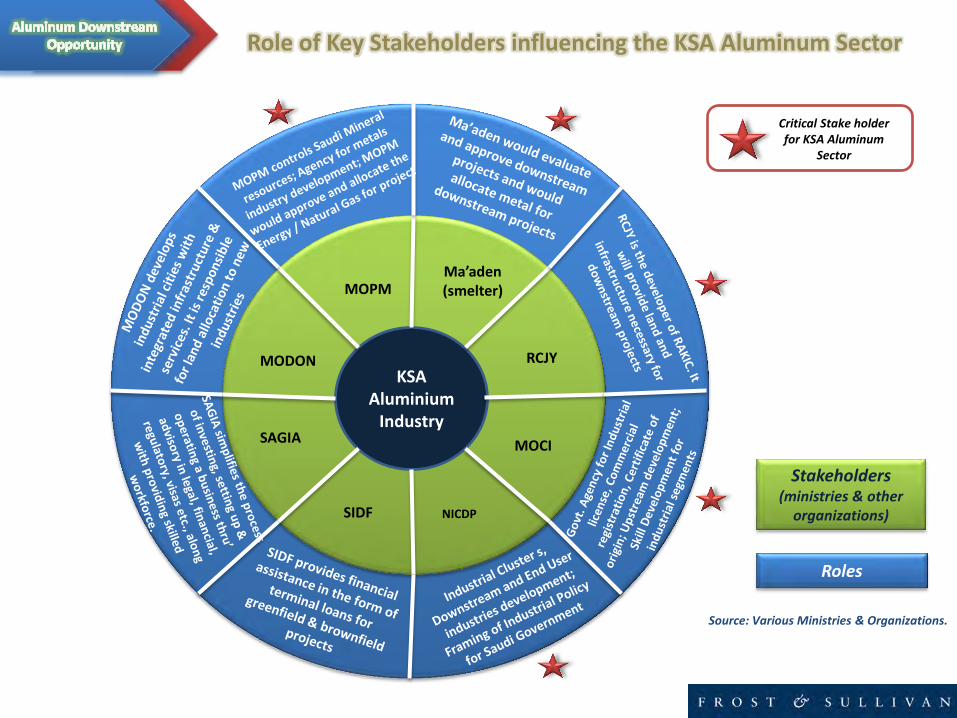

Key Influencers & Participants- KSA Aluminum Industry

Key Ministries & Organizations

Top Aluminum Market Participants

The key influencers refer to Government bodies responsible for development of Aluminum downstream clusters

The Aluminum market participants indicated above represents only key players dominating the market; There are several traders, secondary recyclers dealing with Aluminum products; Other major players include Alinco, Dural, Wofoor etc

Role of Key Stakeholders influencing the KSA Aluminum Sector

Stakeholders (ministries & other

organizations)

Roles

KSA Aluminium

Industry

MOPM Ma’aden (smelter)

RCJY

MOCI

NICDP SIDF

SAGIA

MODON

Source: Various Ministries & Organizations.

Critical Stake holder for KSA Aluminum

Sector

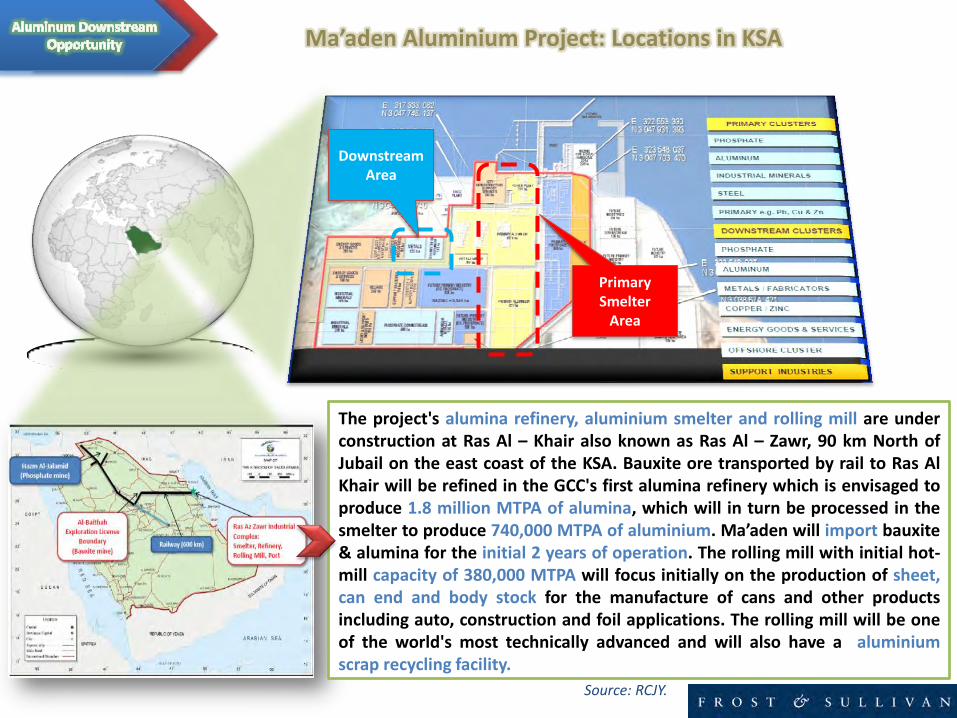

Primary Smelter

Area

Downstream Area

Source: RCJY.

The project's alumina refinery, aluminium smelter and rolling mill are under construction at Ras Al – Khair also known as Ras Al – Zawr, 90 km North of Jubail on the east coast of the KSA. Bauxite ore transported by rail to Ras Al Khair will be refined in the GCC's first alumina refinery which is envisaged to produce 1.8 million MTPA of alumina, which will in turn be processed in the smelter to produce 740,000 MTPA of aluminium. Ma’aden will import bauxite & alumina for the initial 2 years of operation. The rolling mill with initial hot-mill capacity of 380,000 MTPA will focus initially on the production of sheet, can end and body stock for the manufacture of cans and other products including auto, construction and foil applications. The rolling mill will be one of the world's most technically advanced and will also have a aluminium scrap recycling facility.

Ma’aden Aluminium Project: Locations in KSA

Ras Al-Khair (Also called Ras Al-Zawr, Ras Azzour) is a town

and port currently under development on the eastern coast of

the Arabian Gulf, 60 km north of Jubail Industrial City.

In July 2011, King Abdullah has changed the name of Ras Al-

Zawr to Ras Al-Khair.

This upcoming ‘Minerals Industrial City’ would be considered

in near future as the biggest integrated mineral industrial

complex of its kind in the world where it has all basic facilities

for mineral industries in one site for export to world markets.

According to the master plan, 90% would be complete by Y

2013 and 100% by Y 2015.

60 km

Total Area 254 sq. km

KSA Map

Nearest Port Ras Al-Khair

Water (SWCC Desalination Plant)

Gas Networks

Rail Networks

Underground Sewerage

Electricity (2,400 MW from SEC)

Universities & Townships

Land Lease for 25 years

Facilities

RAKIC Aerial View

RAKIC (Ras Al-Khair Industrial Complex) is planned to exploit the mineral deposits of Phosphate and Bauxite found within the KSA.

Hence, the following plants were planned within RAKIC: Di-Ammonium Phosphate (DAP) Aluminium Smelter Ammonia Alumina Refinery Phosphoric & Sulphuric Acid Industrial Minerals Steel Zinc & Copper Smelters Energy Goods & Services

Ras Al-Khair – Minerals Industrial City

Ras Al – Khair Industrial Complex (RAKIC) Program

Primary Industries

Phosphate - Primary

Aluminum - Primary

Industrial Minerals

Steel Plant Zinc / Copper

Smelters

Secondary & Downstream

Industries

Phosphate Downstream

Aluminum Downstream

Metals & Fabrication

Copper/Zinc Downstream

Energy, Goods & Services

Offshore Cluster

Support Cluster

RAKIC Port Ras Al-Khair – Connectivity Few example of RAKIC & Jubail Synergies: •Ammonium Phosphate -downstream chemicals •Aluminum Silicate –rubber & plastics •Aluminum –fabrication & building products •Steel -downstream industries •Caustic Soda -Aluminum production •Plastic / Polymers -building products, engineering

plastics and automotive parts

The Royal Commission for Jubail and Yanbu (RCJY) was established

in 1975 for developing the infrastructure facilities necessary to

transform these two cities into planned industrial complexes and

associated urban communities.

In 2009 this was extended to include Ras Al Khair.

Considering the great success of RCJY in the construction,

management & operation of Jubail & Yanbu Industrial Cities,

the Council of Ministers of KSA has agreed to assign the RCJY

with the management of Ras Al-Khair Industrial City (RAKIC) for

mineral industries and the provision of the services for mining &

other industries, on the style of Jubail & Yanbu industrial cities.

This is done via the application of the best practices relating to

expertise, procedures, knowledge & administrative experiences

over more than 30 years in the implementation of industrial

cities according to the highest world standards.

Ras Al-Khair – Role of RCJY

Advanced Comm.

Network Training Support

Labor Stability & Flexibility

Growth Potential

Quality of Life

Quality Public

Service

Local Govt.

Support Incentives

Utilities Support Program

Land Availability

Market Accessibility

Infrastructure

Feedstock Availability

Reasons to Invest in RAKIC

High Value Added Tier 2/3

products

Brand Value for the KSA

Large Employment Opportunity

Import Substitution

No Local Supply or Less

competition

Environment Friendly

Downstream Projects Selection Policy

Downstream projects are selected / approved by Ma’aden if it fulfills following critieria.

Foils Rod Composite

Panels Castings

(GDC / HPDC)

Wheels (LPDC)

Few aluminium downstream products which fit above criteria

KSA Competitiveness and advantages for downstream projects

Ma’aden’s Aluminium Downstream Policy

Starting of Bauxite mining operations at Al-Baitha mine

Operating Aluminum Smelter at RAKIC

Q3 2013 Q2 2014 Q3 2014

Project Timelines

Commissioning of Rolling mill for production of can sheet & other

sheet coils at RAKIC

Commissioning of Alumina refinery at RAKIC

Strategic location provides access to exports market through sea & air routes

Savings on energy due to liquid, less inventory & oxidation loss, higher

productivity

Well developed infrastructure and land availability from RAKIC

Quality power supply and natural gas at competitive rates vis a vis global

Smelter with own captive bauxite mines and refinery facility ensuring supply

quality & assurance

KSA-largest market for aluminium products in Middle East region

Liquid / Metal from world class smelter operated by Alcoa, global leader

Market Snapshot- KSA Aluminum Industry

Source: Frost & Sullivan.

Share of Production in GCC: 21.8 %

Downstream : Production & Demand : MTPA: Y 2012

Downstream Demand: 618,450 MT (Y 2012)

Share of Production in GCC : Nil %

Downstream Production: 225,600 MT

Top 5 Downstream Producers

Primary Aluminium Production

Nil (2012)

Extrusion Rod Conductor FRP Powder Total

Production 139,000 0 86,600 0 0 225,600

Demand 208,510 90,497 123,049 187,579 8,815 618,450

Share of Demand in GCC : 45%

ALUPCO – 62,000 MT

TALCO – 42,000 MT

Riyadh Cables – 65,000 MT

Saudi Cable company – 50,000 MT

Jeddah Cables – 40,000 MT

Extrusion

Major market for extrusion products; Alupco and

Talco are key suppliers; Net importer of extrusion

Rod & Conductor

Major conductors players present;

No local rods supplier; Net

importer of Rods.

Foils Currently no foils production; Imports

cater to local demand;

Largest foil customer in GCC- Tetra pak in KSA

Coated Sheet Coil Major market in GCC

region, Construction &

Industrial segments major driver. Net importer of sheet

coils

Powder Major powder

market; No local supplier;

Imports mainly from China,

Bahrain

Dem

and

Su

pp

ly

Ma’aden in JV with Alcoa has

commissioned smelter in the Y

2013 with production capacity if

740,000 MTPA.

Ma’aden to expand capacity to

960,000 by the Y 2017.

Products planned include Billets,

ingot, Slab and T-Bars.

380,000 MTPA Rolling Mill also

planned as part of the project

scheduled by the Y 2014.

Cans Currently there

are two major players in KSA

Olayan & Salumco cater to other GCC

countries.

Market Opportunity - KSA compared to Rest of GCC

UAE KSA Kuwait Qatar Bahrain Oman

Rod & Conductor

Extrusion

Foils

Powder

Coated Coils

Foundry Alloys

High Medium Low

Demand Share in

Total GCC Region

32% 45% 6.5% 4.3% 5% 7.2%

Extrusion Building & Construction

Automobile & Transportation Castings

Power / T&D Rods / Cables / Wires

Packaging FRP

Product Key End-user KSA Japan

200,490 793,000

< 1000 * 1,376,000

204,350 18,000

177,800 1,160,000

MEGA Trend on Aluminum Demand - KSA Vs Japan

The market size indicated above are ballpark estimates for comparison. Demand supply varies across product & market segments. Forecasted figures are based on macro economic factors, existing customer base, future projects (approx);

375,000 950,000

50,000 1,670,000

300,000 25,000

260,000 1,450,000

2012

2020

619,000 3,890,000

1,000,000 4,600,000

* Due to no major presence of Auto OEMs consuming Castings (Die cast parts) ; KSA is expected to host major OEMs by 2020 Total aluminum demand includes powder, forgings, imports etc …

Key

Pro

du

cts

& S

egm

en

ts

Source: Frost & Sullivan Analysis and JAA All figures in MT

Opportunity for Japan Investors in KSA

Aluminum Industry

KSA Aluminium Industry Potential

Low Energy & Utilitity costs

KSA enjoys lowest utility costs across the globe, as a result it is an attractive

destination for Energy intensive Aluminium Industry.

China Imports in Aluminum Downstream Industry

Cheaper imports from China especially in Flat rolled industry (Foils, & coated sheet Coils) which hampers local downstream players to expand

or new commissioning becomes a challenge

Wide Demand Supply Gap

Gap exists in Foil , Rod; Opportunity to tier 2 aluminium products from

Extrusion & Sheet coil like ACP, Heat sinks, composite panels, building

access equipment, slugs, cans, aluminium checkered, embossed sheets, auto / ship body sheets,

automobile & industrial castings, metal foams .

Emerging Economy

KSA is one of the major economies in GCC countries with tremendous

growth potential due to construction & Industrialization boom.

Potential for Downstream Industry Development

Aluminium downstream is still in the developing stage apart from extrusion

& conductor.

New investments are observed in Mine, Smelter & Rolling mill facilities.

Strong Foothold in High Growth Market

Market leader in India. Huge future market potential for ECL to leverage –

as Government is increasing fund allocation for improving water &

sewerage infrastructure

Export Potential

KSA is strategically located & has a proximity advantage to cater high

potential markets like MENA countries, Turkey, & Europe.

KSA having FTA tariff advantages to GCC, Europe & Western countries.

High Growth Potential Region

Long term significant downstream opportunity in the region with

development in automotive and other industrial sectors.

Easy Availability of Feedstock

Easy and abundant availability of feedstock and energy. Ma’aden

aluminium smelter and major power projects are underway.

KSA will be a future powerhouse in aluminium production with the advent of Ma’aden. Saudi government’s

friendly industrial policies like industrial cluster development and kingdom’s mission to move & diversify and

create non-oil wealth will carve the future for KSA aluminium industry through downstream products value

addition

KSA Aluminum Industry Potential Summary

$60 0

Key Project Development Index * (PDI)

Foils

Rods & Conductors

Extrusions

Composite Panels

Castings

Foundry Alloys

CAPEX ($ Mn) Job Creation (Nos)

0 200

IRR%

15 - 22%

17 - 24%

14–21%

15-22%

15-22%

12-18%

“Not to scale” There are other potential downstream products to be developed in KSA market; However, Frost & Sullivan recommends these top attractive projects based on current market conditions The above estimates are ballpark indication of parameters represented for listed capacity per year (MTPA) Detailed Feasibility engagement has to be commissioned to get indepth information of market, financial model & engineering aspects

Min

Max

Min

Max

Opportunity for Japanese Companies in Aluminium Downstream Industry

Note: The size of the bubble represent market sizes of the aluminum downstream product

categories.

GCC/KSA Growth Potential for Downstream Opportunities Vs. Local Competition

Aluminum downstream products like rod, conductor, wheels,

castings, composites, panels, castings, foils, drill pipes, forging, laminates, foams, paste etc., where Japanese companies operating in these areas can utilize the opportunities to have a manufacturing presence in the kingdom by utilizing the benefits offered by the KSA government. Japanese companies can also leverage to nurture their domestic demand as well as look at export opportunities in proximity geographies of KSA like Europe & African countries.

Japanese firms are world renowned for their technology & technical expertise. KSA looks to Japan to bring in the necessary technology for the aluminium downstream projects. Their role can be similar to Alcoa support in the tie up with Ma’aden.

Japanese Aluminium firms / technology providers can explore opportunities in the KSA aluminium downstream industry by investing 100% or as a JV with the KSA investors / existing aluminium companies with various equity options (50 / 50, 80 / 20 etc.) along with utilizing industrial friendly policies & incentives offered by the KSA government.

Technical Support KSA firms technical

expertise in shortage to Global standards

Japanese firms are world renowned for technology; KSA looks to Japan to bring in the necessary technology for the downstream projects; Role can be similar to Alcoa support in the tie up with Ma’aden.

Equity Support Financial Investment in project as 100% or as JV

Japanese Aluminium firms shall make investments as 100% owned project or as a JV with KSA firms with various equity options (50 / 50, 80 / 20 etc.)

Downstream player selection

MOPM and NICDP to play key role in JV

partner identification

NICDP & MOPM are the major decision maker for the JV partner. Out of 3-5 identified technology partners, NICDP selects that most suitable one considering their capability related to the highly technical products to be produced.

Government Support Downstream projects development to made

more effective

A new plan termed “Saudi Industrial Development Program” by combining National Industrial Strategy (NIS) & Saudi Industrial Development Fund (SIDF) to mange the Aluminium program more effectively.

Partner selection Process

Matching Value offered with KSA strategy for

Aluminium sector

Downstream products manufacturers are selected based on the value they will bring in the project which match with the strategy of NICDP; MOPM is the final authority to take decision related to Aluminium.

Japanese companies have a brand recognition world wide w.r.t. technology, quality systems, reliability & reputation. so it is a great advantage for the Japanese investors/companies to partner and carve a niche for themselves in the KSA Aluminium industry. they can also have the opportunity to be machinery suppliers / EPC contractors / technology & equity partners by supplying critical high value machinery to extrusion, rolling & foil mills, casting technology and other aluminium down stream manufacturing areas.

Opportunity for Japanese Firms

Ma’aden Aluminium Downstream Policy (1/2)

Emphasize on tier 2 & 3 aluminium products like foils, conductor, composite panels, castings, wheels, etc., which are high value added products yielding higher price premiums on LME

Large employment opportunities for citizens of the KSA

Creates higher brand value and prominent position for KSA on the world aluminium downstream map

Manufacturing products that would serve as Import Substitution

• Ma’aden primarily focus on the upstream activity of Aluminium. Their major focus will be on the primary aluminium and semis. Ma’aden would not develop aluminium downstream product neither they would partner with any other companies in downstream projects. Ma’aden would acts as a facilitator to interested parties like investors, companies etc., who are enthusiastic to develop the downstream project in the Ras Al – Khair Industrial Complex (RAKIC) or anywhere across the kingdom.

• Ma’aden has framed certain policies to select downstream projects of third parties so that it satisfies the following criteria:

Products which have lower domestic competition and is not currently not manufactured in KSA

Environmentally friendly and Non-hazardous aluminium downstream products

Ma’aden Aluminium Downstream Policy (2/2)

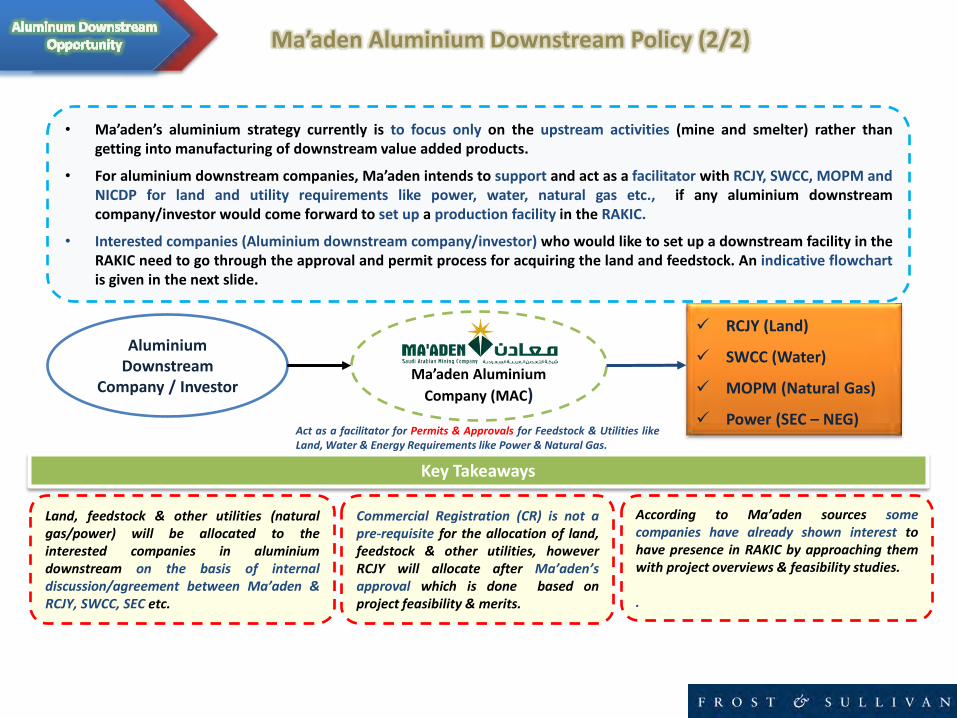

• Ma’aden’s aluminium strategy currently is to focus only on the upstream activities (mine and smelter) rather than getting into manufacturing of downstream value added products.

• For aluminium downstream companies, Ma’aden intends to support and act as a facilitator with RCJY, SWCC, MOPM and NICDP for land and utility requirements like power, water, natural gas etc., if any aluminium downstream company/investor would come forward to set up a production facility in the RAKIC.

• Interested companies (Aluminium downstream company/investor) who would like to set up a downstream facility in the RAKIC need to go through the approval and permit process for acquiring the land and feedstock. An indicative flowchart is given in the next slide.

Aluminium Downstream

Company / Investor

Ma’aden Aluminium

Company (MAC)

Act as a facilitator for Permits & Approvals for Feedstock & Utilities like Land, Water & Energy Requirements like Power & Natural Gas.

RCJY (Land)

SWCC (Water)

MOPM (Natural Gas)

Power (SEC – NEG)

Land, feedstock & other utilities (natural gas/power) will be allocated to the interested companies in aluminium downstream on the basis of internal discussion/agreement between Ma’aden & RCJY, SWCC, SEC etc.

Commercial Registration (CR) is not a pre-requisite for the allocation of land, feedstock & other utilities, however RCJY will allocate after Ma’aden’s approval which is done based on project feasibility & merits.

According to Ma’aden sources some companies have already shown interest to have presence in RAKIC by approaching them with project overviews & feasibility studies. .

Key Takeaways

Key Conclusions

Favourable Factors – Kingdom of Saudi Arabia

+ Secured feedstock liquid from Ma’aden – smelter major driving force

to downstream

+ Attractive savings on production cost ( Low inventory, higher

productivity, other cost savings) due to use of Liquid. Healthy

project financial to the investor (IRR / Payback…)

+ Utility ( power, gas, land) advantages are the key for aluminium

business

+ Demand supply gap – most of the demand met through imports in

large volume markets such as Wire rods, Foils, ACP, Coated & Sheet

Coils, Industrial Extrusion & Powder

+ Investor friendly Nation – striving to diversify the economy by

supporting non-oil downstream activities by investors

KSA has signed more than 20 Double Tax Agreements (DTAs) with countries viz; Japan (signed in Y 2011), Russia, China, India, Italy, Austria, France, Malaysia, Ireland, Greece. South Africa, South Korea, Spain, Turkey, UK, Syria, Belarus

Cluster benefits of RAKIC

About Us - Metals & Minerals Unit

“We Accelerate Growth”

1961 1990 Today

Emerging Research 1961–1990

Growth Partnership 1990–Today

Visionary Innovation Today–Future

Pioneered Emerging Market & Technology Research

• Global Footprint Begins

• Country Economic Research

• Market & Technical Research

• Best Practice Career Training

• MindXChange Events

Partnership Relationship with Clients

• Growth Partnership Services

• GIL Global Events

• GIL University

• Growth Team Membership

• Growth Consulting

Visionary Innovation

• Mega Trends Research

• CEO 360 Visionary Perspective

• GIL Think Tanks

• GIL Global Community

• Communities of Practice

Covering 12 Industries

across globe, located in

42 Countries.

Over 50 Years,

Our 1700+ Experts have

served 250,000 SME &

Global Companies!!!

Frost & Sullivan’s Value Proposition: “We Accelerate Growth”

About Frost & Sullivan- Milestone

Over 50 Years, We Have Engaged With “250,000 SME & Global Companies, 2 Million Top Executives”

Where are we located?

We do work with your Business Partners!- “Globally, Our 12 business unit analysts are continuously engaged in tracking your peer industries. This ensuring coverage of all possible corners on your Business & Performance”

Aerospace & Defense

Measurement & Instrumentation

Information & Communication Technologies

Consumer Technologies

Health Care

Electronics & Security

Chemicals, Materials & Food

Automotive & Transportation

Energy & Power Systems

Environmental & Building Tech Metals & Minerals

Industrial Automation & Process Controls

Frost & Sullivan’s Coverage of 12 Different Verticals Ensure 360’ Perspective of Your Target Markets

We are across “Length & Breadth of the World!” 40+ Offices Provide Perspective, Coverage & Service

• Tools:

•Tungsten carbide, high speed steel, grinding

• Structural Metal Fabrications (Building Work, Civil, Marine Applications)

• Non-structural Metal Fabrications for Building Work

• Prefabricated Metal Buildings

• Pre-Engineered Building Systems

• Household Metal Products

• Wire Rods, Conductors & Cables

• Billet & Extrusions

• Architectural Products (ACPs)

• Flat Rolled Products- Plates , Sheet Coils

& Can stock & Foils

• Channels & Sections – Rolled, Formed,

Hollow

• Castings, Forgings & Stampings

• Alloy Wheels

• Pipes & Tubes – Seamless, Insulated,

Coiled, Rolled

• Flat Products

• Steel Wires /Ropes, Cables, Chains and Slings

• Channels & Sections – Rolled, Formed, Hollow (Light, Medium,Heavy)

• Tubes & Pipes – Cast Iron, Ductile Iron, SAW, ERW, Welded, Seamless, Plastic Lined, Pre-Insulated

• Stainless Steel Precision Tubes

• Flanges, Fittings, Joints, Couplings

• Reinforced Steel Bars

• Rails, Wheels & Springs

• Castings, Forgings & Stampings

Iron & Steel Copper, Aluminum, Zinc, Lead, Tin & Nickel

• Ferro Alloys

• Tantalum

• Niobium

• Rare Earth Elements

• Silica

• Quartz

• Iron Ore

• Bauxite

• Coal

• Inorganic Minerals – silicates, carbonates, sulphates, halides, oxides, sulphides, phosphates

Ferrous Non- Ferrous

Minerals Specialty Products

Metals and Minerals Specialization

Market Coverage (End-to-End)

Mining Primary/Liquid Metal Semi-finished Products Downstream

(Value added products)

PFS and DFS Components

Plant (3D) Model Plant Layouts

Financial Model Business Model

Competition & Customer

Assessment

Prefeasibility

Studies

(PFS)

Partner

Prospecting &

Due Diligence

Detailed

feasibility

Studies (DFS)

Marketing & Distribution Strategies (concept notes)

Metals

&

Minerals

Metals & Minerals Thank you

Y. S. Shashidhar

Managing Director

Frost & Sullivan International Inc

South Asia, Middle East & North Africa

Email: [email protected]

UAE Mobile: +971-50-9201361

KSA Mobile: +966-53-5763998

Venkatesan Subramanian

Vice President & Global Leader

Metals & Minerals

Frost & Sullivan International Inc

Email: [email protected]

Mobile: +91-95000 12471

Phone: +91-44-6681 4371

+91-44-6681 6666

State your need, we would be happy to serve you…

Contacts: