Presented by Lawrence G. McMillan · Presented by Lawrence G. McMillan ... Therefore, buy 600...

76

www.optionstrategist.com 1-800-724-1817 [email protected] Risk Management Presented by Lawrence G. McMillan “The Option Strategist” Continuing Webinar Series

Transcript of Presented by Lawrence G. McMillan · Presented by Lawrence G. McMillan ... Therefore, buy 600...

www.optionstrategist.com 1-800-724-1817 [email protected]

Risk Management

Presented byLawrence G. McMillan“The Option Strategist”Continuing Webinar Series

www.optionstrategist.com 1-800-724-1817 [email protected]

McMillan Analysis Corp.A Derivatives Firm

Recommendations (newsletters)

Money Management

Option Educationincluding Mentoring

www.optionstrategist.com/mentoring

www.optionstrategist.com 1-800-724-1817 [email protected]

Special offers on most of our newsletters,

software, and educational

products

Visit: www.optionstrategist.com/webinar

www.optionstrategist.com 1-800-724-1817 [email protected]

Today’s TopicsPosition Sizing

The Concept Of Expected Return

Stops and Partial Profits

Using Greeks to Manage Risk

Portfolio Protection

www.optionstrategist.com 1-800-724-1817 [email protected]

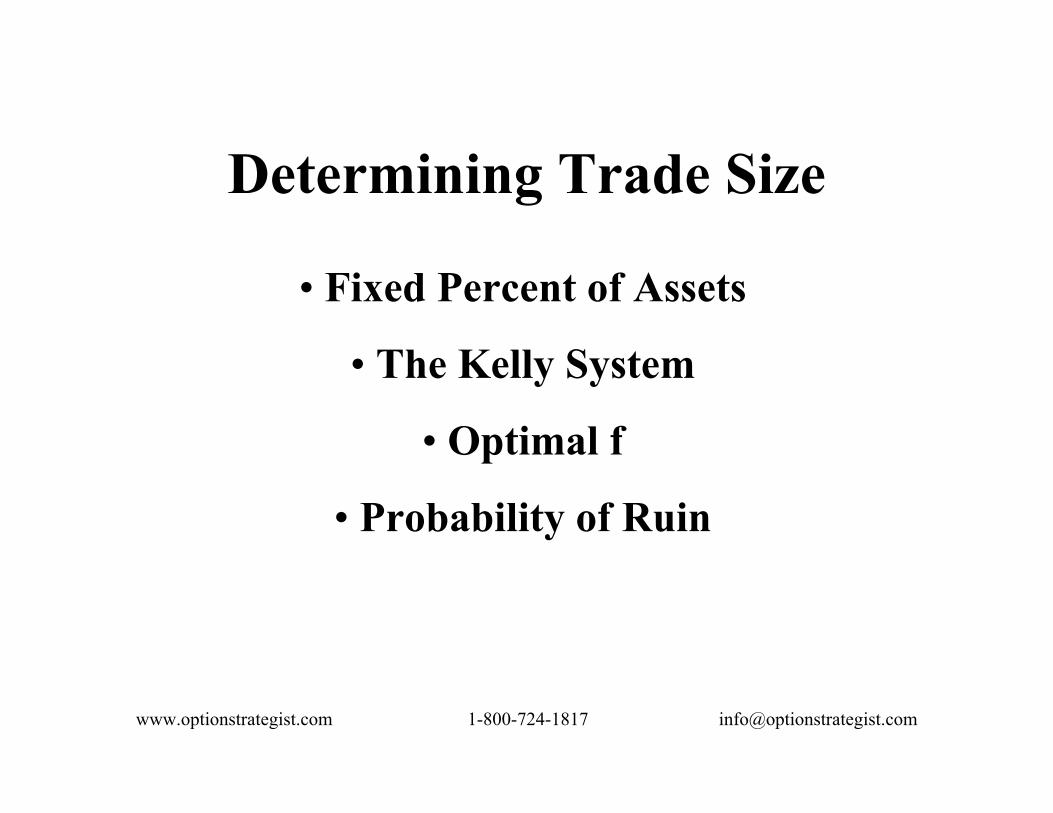

Determining Trade Size

• Fixed Percent of Assets

• The Kelly System

• Optimal f

• Probability of Ruin

www.optionstrategist.com 1-800-724-1817 [email protected]

What NOT To Do…• Double up to catch up

• Martingale:

–1 –2 –4 –8 –16 +32 = +1

www.optionstrategist.com 1-800-724-1817 [email protected]

A Better Approach…

• Increase size as you profit

• Fibonacci-style:

10, 15, 25, 40, 65, 105, 170, 275, …

7 wins, 1 loss: +$155 vs +$60

Return to initial size ($10) when you lose

www.optionstrategist.com 1-800-724-1817 [email protected]

How Many Options Should I Buy?Fixed Percentage Risk Management

Risk a fixed percent of your account on each trade (3%, e.g.)

Automatically increases when you winand decreases when you lose

Example: Account size = $100,000You plan to risk 5 points on a stock trade

Therefore, buy 600 shares of stock (3% risk)

www.optionstrategist.com 1-800-724-1817 [email protected]

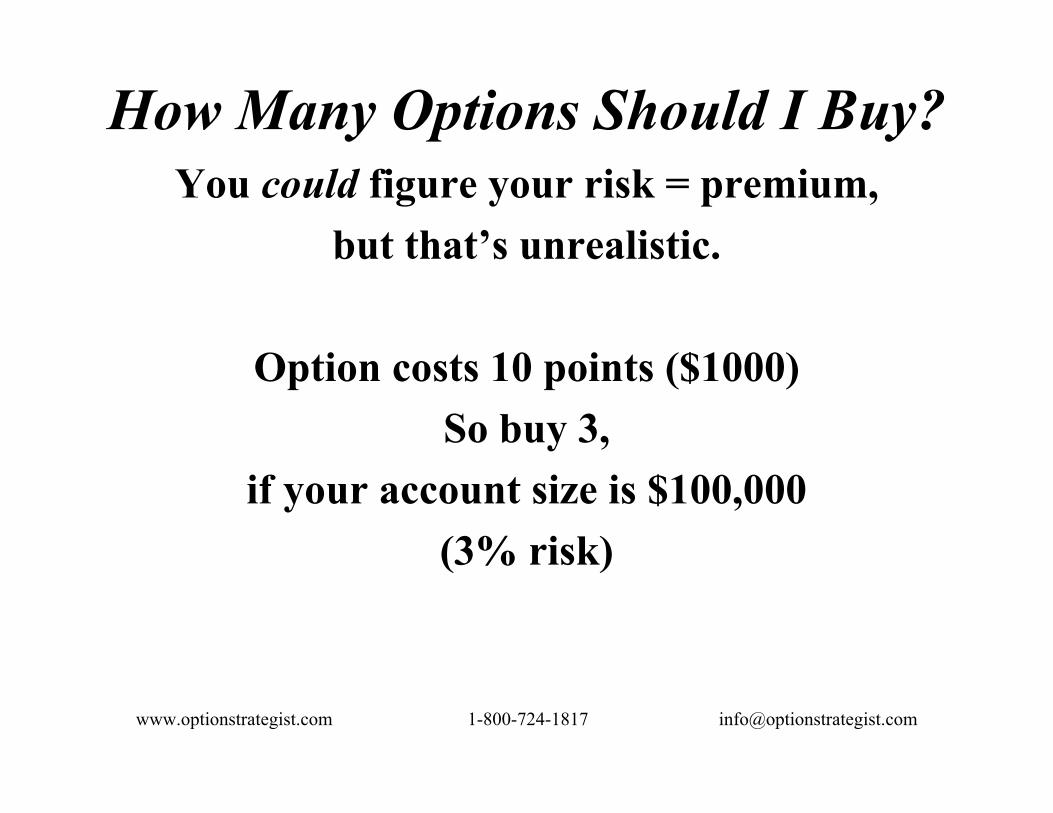

How Many Options Should I Buy?You could figure your risk = premium,

but that’s unrealistic.

Option costs 10 points ($1000)So buy 3,

if your account size is $100,000(3% risk)

www.optionstrategist.com 1-800-724-1817 [email protected]

How Many Options Should I Buy?Using the model to estimate risk.

Oct 100 call costs 10 today ($1000).What would it be worth if XYZ fell to 95

in a week?

Black-Scholes model says:In 1 week, if XYZ = 95, Oct 100 call = 7

Therefore, risk = 3 points ($300)so you can buy 10 calls, not 3!

www.optionstrategist.com 1-800-724-1817 [email protected]

Another Approach:The Kelly Criterion

J. L. Kelly, Bell Labs, 1954

Original Formula:

Amount to bet = (W + L) * p – L Where W = amount you could win

L = amount you could losep = probability of winning

If result is negative, don’t bet

www.optionstrategist.com 1-800-724-1817 [email protected]

Applying Kelly: Sports BettingIn sports betting L = 1.1 * W

(you lay $110 to win $100)

Amount to bet = (W + 1.1W) * p – 1.1W

= W *( 2.1p – 1.1)

Will be negative if p <= .52

Assume W = 1 (your risk bankroll)

Amount to bet = 2.1p – 1.1

www.optionstrategist.com 1-800-724-1817 [email protected]

Kelly: Sports ExampleAmount to bet = 2.1p – 1.1

Example, assume p = 60% (i.e., you can predict sports winners with 60% accuracy*)

Then amount to bet = 2.1 * .60 – 1.1 = .16 which means risk 16% of your bankroll on

the next bet.

*: if you can do that, you don’t need this seminar

www.optionstrategist.com 1-800-724-1817 [email protected]

Kelly: More Complex SituationsApplying (W + L) * p – L

Where p = probability of a winning trade

PDR System: avg win $2359; avg loss $1952

And p = 56.7%

So L = .83W

Amount to bet = (1.83p – 0.83)

Amount to risk = 21%

www.optionstrategist.com 1-800-724-1817 [email protected]

The Probability Of RuinDefine “ruin:” down 80%?

If you risk 50% of your capital, and lose it all on each trade, then:

One loss: 50% left

Two losses: 25% left

Three losses: 12.5% left = ruined!

www.optionstrategist.com 1-800-724-1817 [email protected]

The Probability Of RuinDefine “ruin:” down 80%?

How many losses in a row would ruin you?

(1 – r)n = 0.2, where r = % of assets you risk on each trade

If r = 3%, n = 52

If r = 50%, n = 2.3

www.optionstrategist.com 1-800-724-1817 [email protected]

More on the Probability of RuinKelly is designed to optimize your results, not

protect your capital!

Professional blackjack players rejected Kelly because the probability of their bankroll shrinking

to any percentage was that percentage itself.

50% chance of losing 50%

20% chance of losing 80%

10% chance of losing 90%

Was too much risk for them

www.optionstrategist.com 1-800-724-1817 [email protected]

Kelly for Traders• Our investment is not equal to our risk

• Our win amount is not fixed, either

• We don’t make sequential investments

• Not all of our trades have equal probabilities of profit (unless we only trade one system)

Reference: Google papers by Edward Thorp

www.optionstrategist.com 1-800-724-1817 [email protected]

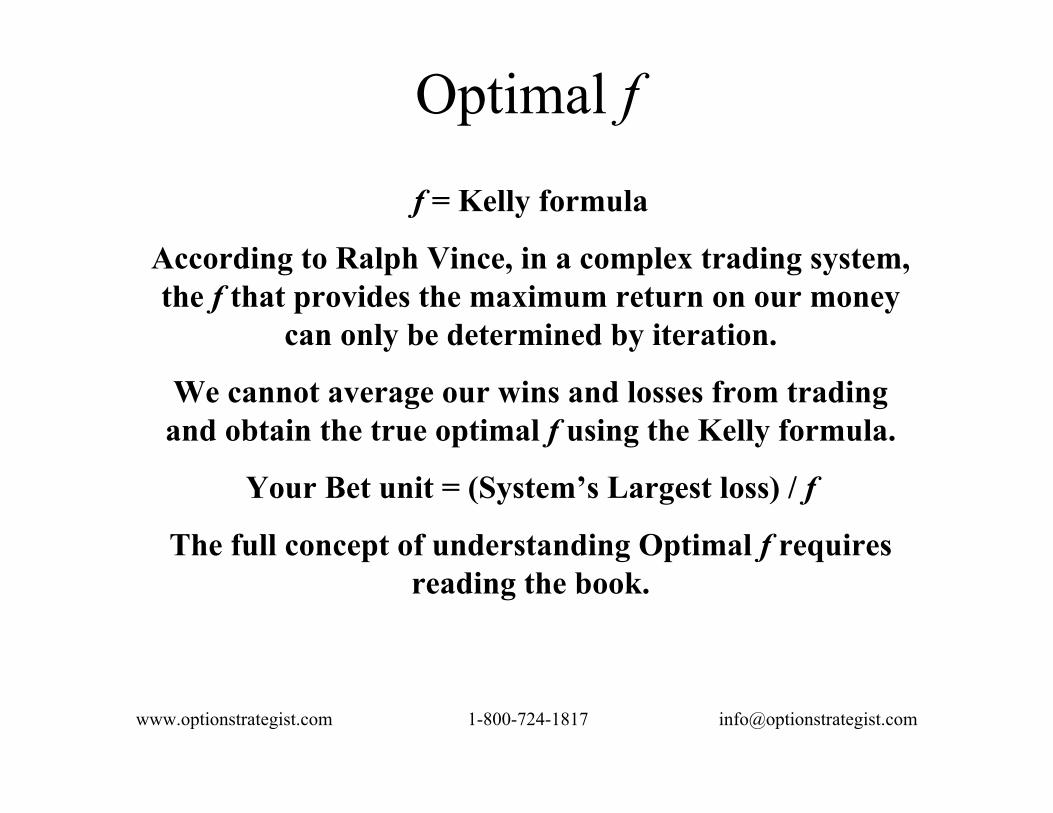

Optimal f

f = Kelly formula

According to Ralph Vince, in a complex trading system, the f that provides the maximum return on our money

can only be determined by iteration.

We cannot average our wins and losses from trading and obtain the true optimal f using the Kelly formula.

Your Bet unit = (System’s Largest loss) / f

The full concept of understanding Optimal f requires reading the book.

www.optionstrategist.com 1-800-724-1817 [email protected]

The Concept of Expected Return

A logical way to analyze, compare, enter and exit

strategies

www.optionstrategist.com 1-800-724-1817 [email protected]

What is Expected Return?

The return one could expect to make on a position over a large number of trials.

Assumes the distribution of possible stock prices can be defined; also assumes implied

volatilities of an unexpired option can be estimated as well.

Highly dependent on volatility estimate.

www.optionstrategist.com 1-800-724-1817 [email protected]

Expected Return ExampleA Call Bull Spread

XYZ: 52 Oct 50 call: 7 Oct 60 call: 4

Assume the stock must be at one of the following prices:Stock Price Probability

< 50 45%52 8%54 7%56 6%58 4%>60 30%

Total: 100%

www.optionstrategist.com 1-800-724-1817 [email protected]

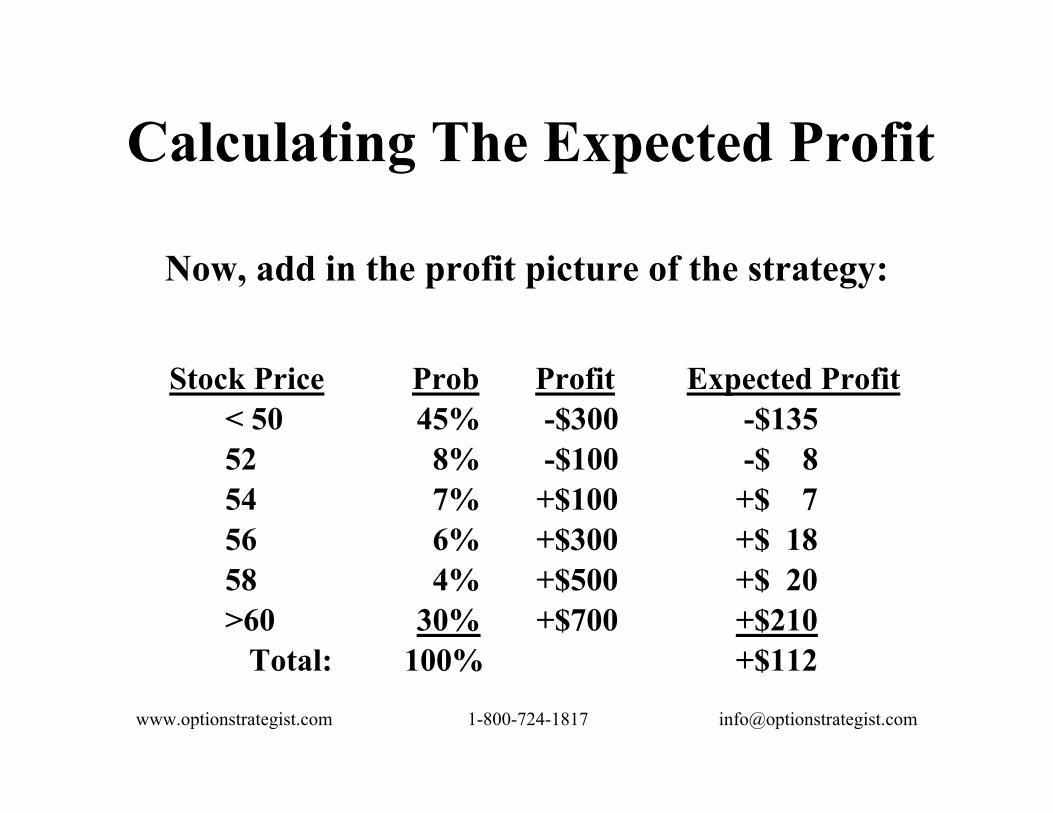

Calculating The Expected Profit

Now, add in the profit picture of the strategy:

Stock Price Prob Profit Expected Profit< 50 45% -$300 -$13552 8% -$100 -$ 854 7% +$100 +$ 756 6% +$300 +$ 1858 4% +$500 +$ 20>60 30% +$700 +$210

Total: 100% +$112

www.optionstrategist.com 1-800-724-1817 [email protected]

How Will This Spread Do?

• Expected Return = $112 / $300 = 37.3%

• Annualized Exp Return = 37.3% x 4 = 112%

• But the only point you actually would make $112 is if stock is at 54.12 at expiration.

• Chance of that is < 0.005

• In any one case, you could make as much as $700 or lose as much as $300

www.optionstrategist.com 1-800-724-1817 [email protected]

What is Expected Return NOT?

• It is not a black box, “magic” formula

• It is not a guarantee of profits

• It is not a shortcut to the diligence needed to trade options profitably

www.optionstrategist.com 1-800-724-1817 [email protected]

What Does It Mean?• On average, if you invest in positions with high expected return, you should

approach that return eventually

• The “Casino Analogy”

• Erroneous Assumptions- Distribution not lognormal

- Bad volatility estimate- Event Risk

www.optionstrategist.com 1-800-724-1817 [email protected]

Trading Decisions Based on Expected ReturnIn the bull spread example,

Suppose XYZ moves from 52 to 55 quickly

And you have a profit of $120.

That’s your expected profit.

Should you take it?

If you do, your annualized return increases!

www.optionstrategist.com 1-800-724-1817 [email protected]

Expected Return onThe Strategy Zone

and Option Work BenchOur statistics on The Strategy

Zone include expected return for

• Calendar spreads

• Covered Call Writes

• Naked Put Sales

www.optionstrategist.com 1-800-724-1817 [email protected]

Position Sizing Using Expected Return

• Kelly is useful because it optimizes results while increasing our trading size when winning and reducing it when losing

• It is a rational way of investing in a consistent manner, placing the most money on the most likely profitable trades

• We have expected return as a guide

• We can also often determine the probability of winning or losing on a trade

• In complex situations, Kelly effectively reduces to:

Amount of account to risk = pwin – ploss

www.optionstrategist.com 1-800-724-1817 [email protected]

Applying KellyIn some cases, we can compute pwin and ploss

but that might not relate well to expected return (naked writing, for example)

Better to use expected return, e

pwin = (1 + e) / (2 + e)

Ploss = 1- pwin

www.optionstrategist.com 1-800-724-1817 [email protected]

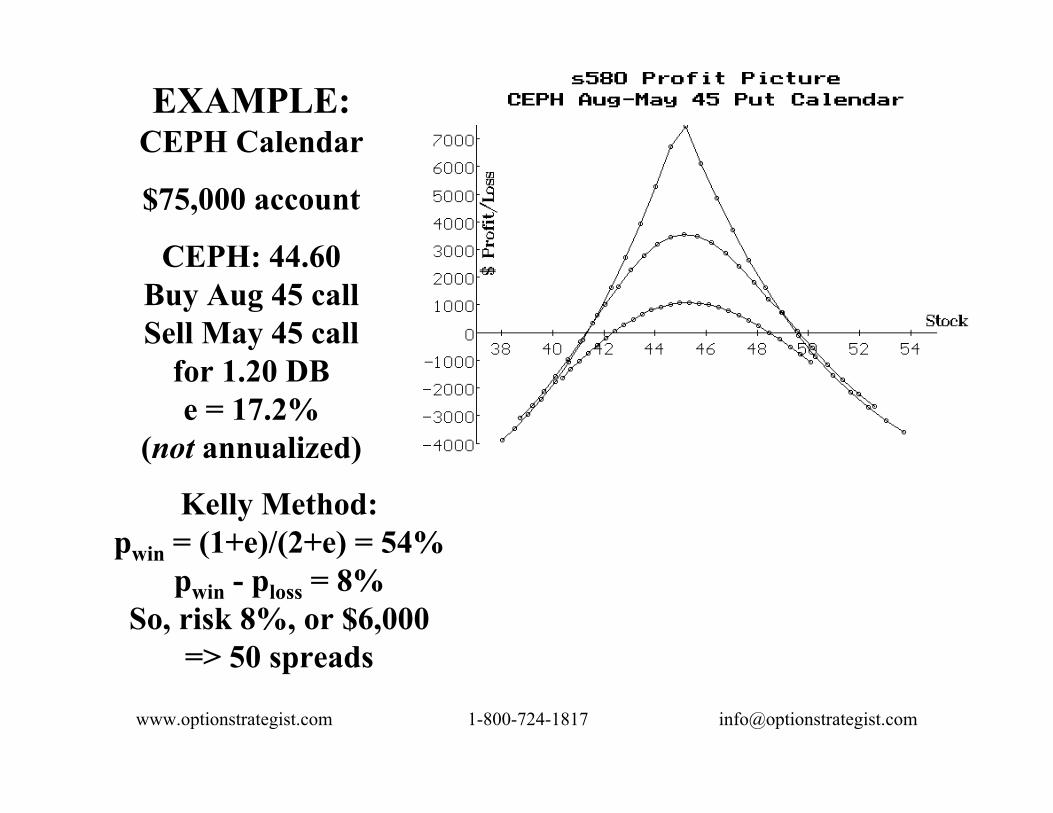

EXAMPLE:CEPH Calendar

$75,000 account

CEPH: 44.60Buy Aug 45 call Sell May 45 call

for 1.20 DBe = 17.2%

(not annualized)

Kelly Method:pwin = (1+e)/(2+e) = 54%

pwin - ploss = 8%So, risk 8%, or $6,000

=> 50 spreads

www.optionstrategist.com 1-800-724-1817 [email protected]

Portfolio Considerations

Can’t just use the Kelly or Optimal f number for each position:

What if Kelly says “invest 12%,” but you have more than 8 positions you want to establish?

Two approaches:

1) Use Kelly on remaining equity in account, or

2) Rebalance all positions (daily)

www.optionstrategist.com 1-800-724-1817 [email protected]

Fortune’s Formula“The Untold Story of the Scientific Betting System that Beat The

Casinos and Wall Street”

By William Poundstone-----------------------------------------------

Against The Gods“The Remarkable Story of Risk”

By Peter L. Bernstein-----------------------------------------------

The Handbook of Portfolio Mathematics: Formulas for Optimal Allocation & Leverage

by Ralph Vince

Recommended Reading

www.optionstrategist.com 1-800-724-1817 [email protected]

Risk ManagementOnce the Trade Has Been Made

Stops

Partial Profits

Rolling

Portfolio Greeks

www.optionstrategist.com 1-800-724-1817 [email protected]

Speculative PositionsWhy hedge?

1) Lock in some gains2) Reduce risk

Any time you adjust or hedge a speculative position, you harm your potential profits.

Most harmful: partial profits

Modestly harmful: rolling

As a result, hedging should not be overdone.

I don’t like: selling out-of-moneys against long options,hedging calls with puts and vice versa, or other

methods of converting long option to another strategy.

www.optionstrategist.com 1-800-724-1817 [email protected]

Trailing StopsType of Stops20-day SMA10% EMAChandelierParabolic

Closing stops recommended

Should be applied to all

unhedged trades

www.optionstrategist.com 1-800-724-1817 [email protected]

Profit-taking Methods1) Partial Profit:

Sell a portion (quarter or a third) of your position

Or 2) Roll the position:

Sell the options you own (when they are fairly deep in-the-money)

And buy a strike that is near-the-money

www.optionstrategist.com 1-800-724-1817 [email protected]

Profit-Taking:Allows you to book some gains

“I feel I should be doing something”

ATK:

17 points as shown

43 points if no partial profits had

been taken

www.optionstrategist.com 1-800-724-1817 [email protected]

Partial Profits: Completely eliminates any further gains from the

portion that you sold

Everyone worries about a gain turning into a loss

Works best if stock (or market) is not trending

A huge mistake in a trending situation

www.optionstrategist.com 1-800-724-1817 [email protected]

Rolling (Up)Is moderately harmful.

WHY?

Your position: Long 10 XYZ Jan 50 calls

with XYZ = 60

Roll:

Buy 10 XYZ Jan 60 callsSell 10 XYZ Jan 50 calls

This is a bear spread, but you are bullish!

But at least you retain your upside quantity

www.optionstrategist.com 1-800-724-1817 [email protected]

Speculative Summary• In a trending market, the best gains come from merely holding until your trailing stop is elected.

• Hedging/Adjusting in trending markets is harmful

• It behooves you to know if the underlying is prone to trending or not. Many commodities and

commodity-related stocks trend.

• Stocks that depend on fundamentals for propulsion generally are not trending stocks.

www.optionstrategist.com 1-800-724-1817 [email protected]

Adjusting Hedged PositionsYou should always have a stop whether you are

Speculator

Naked Option Seller

Maybe even in a limited risk spread

So it is not mandatory to adjust; you could just sit back and let the stops take care of things

www.optionstrategist.com 1-800-724-1817 [email protected]

Hedged StrategiesWhether or not to adjust a hedged position, really

depends on the strategy and your attitude.

For example: Long Straddle

Long XYZ July 50 straddle @ $5

Later, XYZ = 55.

“Scalper” would sell some stock, looking to buy it back on a pullback.

“Trender” would sell the puts, and use a trailing stop on the long calls.

www.optionstrategist.com 1-800-724-1817 [email protected]

Simple Adjustment to Hedged Strategies

Adjust stop as time passes to protect unrealized profits:

Assume you Sold XYZ Straddle for 12

Now XYZ is near strike and straddle is selling for 6

Stop yourself out if either side goes 6 points in-the-money

Similar to trailing stop.

www.optionstrategist.com 1-800-724-1817 [email protected]

Simple Adjustment to Hedged StrategiesOr if relationship of profit to stock price is difficult to

discern, then adjust your stop in dollars

Assume you have July-April 60 calendar spread

It is marking up $200 with XYZ near 60,

But there is more to be made if XYZ stays near 60.

Stop yourself out if your profit drops to $150, say.

Similar to trailing stop.

www.optionstrategist.com 1-800-724-1817 [email protected]

Position GreeksCalculate the Deltas (Gammas, Thetas, etc.) for all

options in a position and add them together.

XYZ: 45 Price Delta Gamma

Long 5 XYZ July 50c 0.95 +26 4.9Long 5 XYZ July 50p 5.90 -74 4.9Short 3 XYZ July 40p 0.72 -19 4.1

Delta: (+5x+26) + (+5x-74) + (-3x-19) = -183 (ESP)Gamma: 5x4.9 +5x4.9 – 3x4.1 = +36.7

Long gamma means you want stock to accelerate;Short delta means you have a downside bias;Hedge: buy ~200 common => now neutral

www.optionstrategist.com 1-800-724-1817 [email protected]

To Scalp or Not?Whether or not to adjust a hedged position, really

depends on the strategy.

If you are a “gamma scalper” or “delta neutral trader,” then you would adjust when others might not.

In a long gamma position, all adjustments are for the purpose of taking profits;

In a short gamma position, all adjustments are for the purpose of preventing losses

www.optionstrategist.com 1-800-724-1817 [email protected]

Gamma Determines Attitude

Position Gamma: Long Short

Adjustment Whipsaws Good Bad

Straight-line/gap Move Good Bad

Dull market Bad Good

Stop needed No Yes

www.optionstrategist.com 1-800-724-1817 [email protected]

Neutralizing Several GreeksYou can always neutralize 2 or 3 of the Greeks, moving

exposure to the area you desire.

Example: you want to establish a call ratio spread, but you would like to neutralize your market risk and leave

only the volatility risk.

www.optionstrategist.com 1-800-724-1817 [email protected]

2 Equations in 2 UnknownsPosition Delta Gamma Theta Vega IV

XYZ Jul 50c 45 4.7 -1.9 9.6 35%XYZ Jul 55c 29 3.5 -1.9 8.4 40%

To Neutralize Gamma (delta comes later) , while making $100 per point drop in Vega:

4.7x + 3.5y = 09.6x + 8.4y = -100

Rounding, x = 60; y = -80 (y / x = 1.33)

Delta = 60x45 – 80x29 = 380; so short ~400 shares

Theta = +38 (you make $38 per day in time decay)

www.optionstrategist.com 1-800-724-1817 [email protected]

Staying NeutralLater, XYZ = 52

Position Delta Gamma Theta Vega IV

L 60 XYZ Jul 50c 64 4.9 -2.4 8.1 35%S 80 XYZ Jul 55c 41 4.5 -2.8 8.4 40%S 400 XYZPosition Greeks: 160 -66 80 -186

To Neutralize Gamma and Delta:Buy 15 July 55c: increases Gamma by 15 x 4.5 = 67.5Increases Delta by 41x15 = 615, so short ~800 more XYZ

Leaves Theta +38; Vega –60 (to get back to –100, mult by 1.67)

www.optionstrategist.com 1-800-724-1817 [email protected]

Portfolio GreeksCan’t just add all position greeks together

Because different stocks have different volatilities

For example,

Long 200 deltas in RIMM

+ Long 400 deltas in VZ

Does not make long 600 deltas

Rather you must reduce all deltas to a common factor (EFP), such as SPX or QQQ.

www.optionstrategist.com 1-800-724-1817 [email protected]

Equivalent “Market” PositionAssume “market volatility” = 15% ($SPX, say)

ESP Price Volatility Adj.Factor Adj. Dlrs

L 800 RIMM 35.5 45% 3.0 $85,200

L 2000 VZ 35.5 15% 1.0 $71,000

$156,200

So this portfolio is long $156,200 as “market equivalent”

So, if SPY = 128, then to fully hedge the risk (delta) of this portfolio, you would sell $156,200 / 128 = 1220 SPY

www.optionstrategist.com 1-800-724-1817 [email protected]

What Is Portfolio Protection?

“The use of listed derivatives to reduce or eliminate the risk of a

general market correction”

Most investors view protection as insurance or disaster protection, rather than a complete hedge of

their entire portfolio.

www.optionstrategist.com 1-800-724-1817 [email protected]

Protecting A Stock Portfolio

Buy $SPX Puts (Traditional)

Or

Buy $VIX calls (Modern)

www.optionstrategist.com 1-800-724-1817 [email protected]

“Macro” Protection• Using broad-based index ($SPX or $VIX) options

• Most efficient in terms of cost and effort

• Problem: Tracking error

“Micro” Protection• Hedge each individual stock with its options

• No tracking error

• Can be extremely time-consuming

www.optionstrategist.com 1-800-724-1817 [email protected]

“Macro” Protection• Using broad-based index options

• $SPX or $VIX

• Or other index that represents your stock portfolio

• Most efficient in terms of cost and effort

• Problem: Tracking error

www.optionstrategist.com 1-800-724-1817 [email protected]

“Macro” StrategiesBuy Broad-Based Index Puts

Buy Index Put Spreads

Sell Index Calls

Use Index Collars

Sell Index Futures

Volatility Products

www.optionstrategist.com 1-800-724-1817 [email protected]

Buy Broad-Based Index Puts • Most Popular Approach; not necessarily the best approach

• Typically buy 5% to 15% Out of Money (OOM)

• The OOM portion is the “deductible”

• With care, can keep cost down to 2% - 3% of NAV

• Disadvantage: protection not dynamic if market rallies

• Advantages: fixed cost; upside profits unencumbered

www.optionstrategist.com 1-800-724-1817 [email protected]

Buy Index Put Spreads

• Buy bear spreads as a hedge

• Drawback: cap on protection

• Advantage: lowers cost of protection

• In effect, your insurance benefits only engage between the strikes of your spread – a poor approach if you actually need protection

www.optionstrategist.com 1-800-724-1817 [email protected]

SellIndex Calls

Drawbacks: doesn’t provide disaster

insurance; and may limit upside profits

Advantage: sale ofa wasting asset

www.optionstrategist.com 1-800-724-1817 [email protected]

Index Collars• Buy OOM puts and sell OOM calls

• Calls defray cost of the puts (sometimes completely)

• Limits both risk and reward

• Distance between strikes is hurt by high dividend and/or low volatility

• Best when using LEAPS options (can spread strikes out quite far with LEAPS):

June 2007: $SPX: 1517 Feb 2011: $SPX 1340Dec (’09) 1450 put: 107.6 Dec(’13) 1200p: 120Dec (’09) 1700 call: 118.8 Dec(’13) 1400c: 125

Nowhere nearly as attractive (vol, div, rates)

www.optionstrategist.com 1-800-724-1817 [email protected]

Volatility Products

• $VIX

• Futures on $VIX

• Options on $VIX

www.optionstrategist.com 1-800-724-1817 [email protected]

Hedging With Volatility ProductsSince $VIX moves opposite to $SPX,

Buy VIX futures

Or Buy VIX calls• Advantages: stock upside unencumbered; cost limited to “time value premium.”

• Disadvantages: $VIX derivatives may not track well with $VIX itself.

www.optionstrategist.com 1-800-724-1817 [email protected]

$VIX Calls are a better hedge than $SPX puts

Better than buying $SPX puts: protection is dynamic

If you buy $SPX puts and market rises, your protection is virtually worthless

If you buy $VIX calls and market rises, your protection is still viable

www.optionstrategist.com 1-800-724-1817 [email protected]

$VIX Hedging Is “Cheap”According to a well-known study, a portfolio consisting of 90% $SPX and 10% $VIX outperforms $SPX in both up and down markets.

Later studies suggest 20% for hedging.

So you only need to hedge 10%-20% of your portfolio’s EFP, assuming it performs “in line” with the broad market.

Buy out of the money $VIX calls, one or two months out, and keep rolling them.

Strike ~= futures price + 7

www.optionstrategist.com 1-800-724-1817 [email protected]

How Many $VIX Calls To Buy?• Hedge 20% of your NAV

• Assume EFP = $100,000 on 9/16/2008• VIX Oct 30 call = 4

• You buy $20,000/(30x100) = 7 calls• Stock market down 26% ($SPX 1210 to ~900)

• NAV: -$26,000 loss• Oct $VIX Futures: +125%; $VIX +131%; Oct 30 call = 27

• 7 calls x $2300 profit = +$ 16,100 gain• You lose -$9,300 = your “deductible” (9.3%)

www.optionstrategist.com 1-800-724-1817 [email protected]

$VIX Option Protective “Collar”

Buy VIX calls for protection

And Sell VIX puts to help fund the calls

Problem: Put premiums small

www.optionstrategist.com 1-800-724-1817 [email protected]

SummaryRisk Management is Important:

Position Sizing

Use Trailing Stops For Speculative Positions

For simple hedged positions, use dollar stops

For complex positions, hedge with Greeks

For portfolios, hedge with $VIX

www.optionstrategist.com 1-800-724-1817 [email protected]

Special offers on most of our newsletters,

software, and educational

products

Visit: www.optionstrategist.com/webinar

www.optionstrategist.com 1-800-724-1817 [email protected]

CD Seminar Series

Regularly $499

Show Special $199

www.optionstrategist.com 1-800-724-1817 [email protected]

MentoringMcMillan Analysis Corp.

Offers One-on-one MentoringStructured to your skill level

Conducted on the internet or in person

Call 973-362-4558 or visit:www.optionstrategist.com/mentoring

www.optionstrategist.com 1-800-724-1817 [email protected]

Thank you for attending!Contact information:

Phone: 800-724-1817

email: [email protected]

Fax: 973-328-1303

web site: www.optionstrategist.com/webinar