Presented by: Janet Wong KPMG LLP 6 November 2007 G L O B A L G R A N T S P R O G R A M T A X Annual...

36

Presented by: Janet Wong KPMG LLP 6 November 2007 G L O B A L G R A N T S P R O G R A M T A X Annual High Tech Tax Annual High Tech Tax Institute Institute International Corporate International Corporate Grantmaking Grantmaking

-

Upload

kelley-cameron -

Category

Documents

-

view

215 -

download

1

Transcript of Presented by: Janet Wong KPMG LLP 6 November 2007 G L O B A L G R A N T S P R O G R A M T A X Annual...

Presented by: Janet Wong KPMG LLP

6 November 2007

Presented by: Janet Wong KPMG LLP

6 November 2007

G L O B A L G R A N T S P R O G R A M

T A X

Annual High Tech Tax InstituteAnnual High Tech Tax Institute

International Corporate International Corporate GrantmakingGrantmaking

2© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

The information contained herein is general in nature and based on authorities that are subject to change. Applicability to specific situations is to be determined through consultation with your tax adviser.

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

The information contained herein is general in nature and based on authorities that are subject to change. Applicability to specific situations is to be determined through consultation with your tax adviser.

3© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

International Giving TrendsInternational Giving Trends

4© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Philanthropy on the Rise Philanthropy on the Rise

Corporate DonationsCorporate Donations

Grew by 6%Grew by 6%

Source: The Source: The Chronicle of PhilanthropyChronicle of Philanthropy, August 23, 2007, growth from 2005 to 2006, August 23, 2007, growth from 2005 to 2006

5© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Charitable Giving in 2006Charitable Giving in 2006

6© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Corporate Giving on the RiseCorporate Giving on the Rise

Total dollar amount of Total dollar amount of cashcash donations rose to $3.8 donations rose to $3.8 billion in 2006 from $3.5 billion in 2005.billion in 2006 from $3.5 billion in 2005.

Based on a survey by The Chronicle of Philanthropy, Based on a survey by The Chronicle of Philanthropy, corporate giving is expected to increase in 2007.corporate giving is expected to increase in 2007.

Top focus areas for corporate donations in 2006 and Top focus areas for corporate donations in 2006 and 2007: 2007:

- environment and- environment and

- improving education.- improving education.

7© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

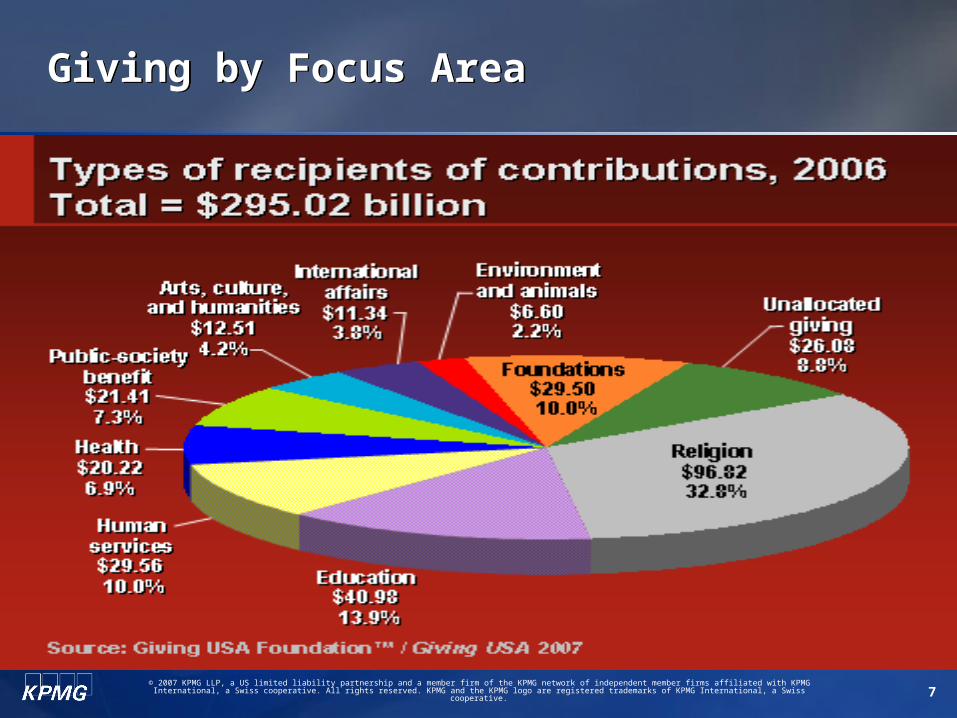

Giving by Focus AreaGiving by Focus Area

8© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Corporate Giving by Program Type – 2005

Source: Foundation Center, Key Facts on Corporate Foundations, May 2007

Corporate Giving by Program Type – 2005

Source: Foundation Center, Key Facts on Corporate Foundations, May 2007

9© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

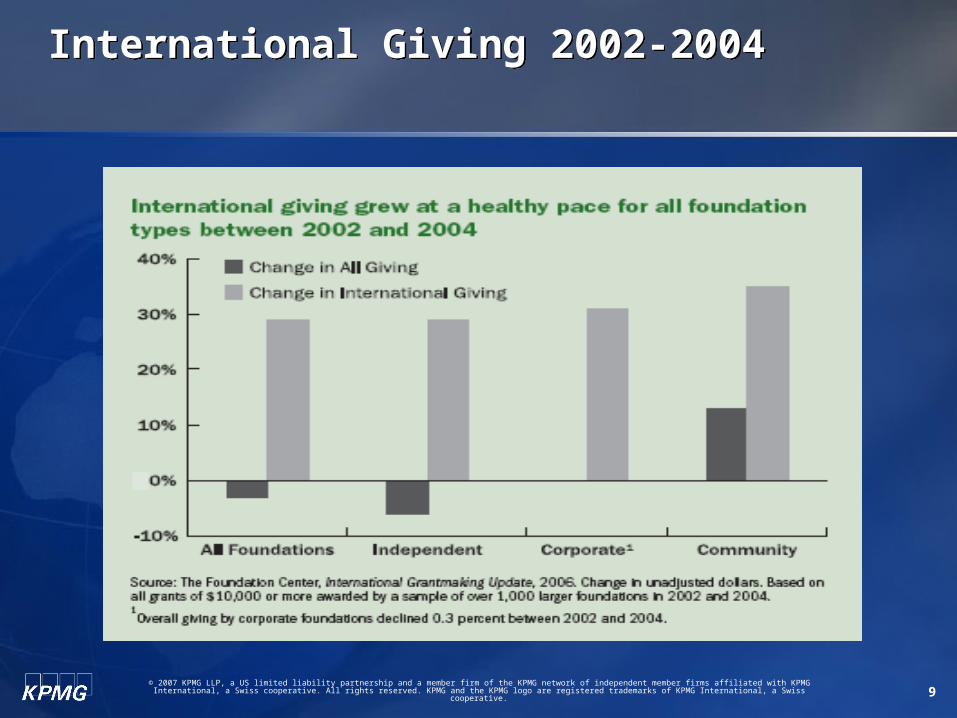

International Giving 2002-2004International Giving 2002-2004

10© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

International Giving 1998-2005International Giving 1998-2005

11© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

International Giving 1998-2005International Giving 1998-2005

Growth in international giving was temporarily Growth in international giving was temporarily curtailed by 9/11, but has rapidly accelerated since curtailed by 9/11, but has rapidly accelerated since 2003.2003.

Human catastrophes of epic scale have drawn attention to Human catastrophes of epic scale have drawn attention to international giving opportunities.international giving opportunities.

Several large foundations began major international initiatives, Several large foundations began major international initiatives, while a large number of organizations began to participate in while a large number of organizations began to participate in international giving programs.international giving programs.

The increasing population of U.S. immigrants has continued to The increasing population of U.S. immigrants has continued to provide support back to their country of origin.provide support back to their country of origin.

12© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

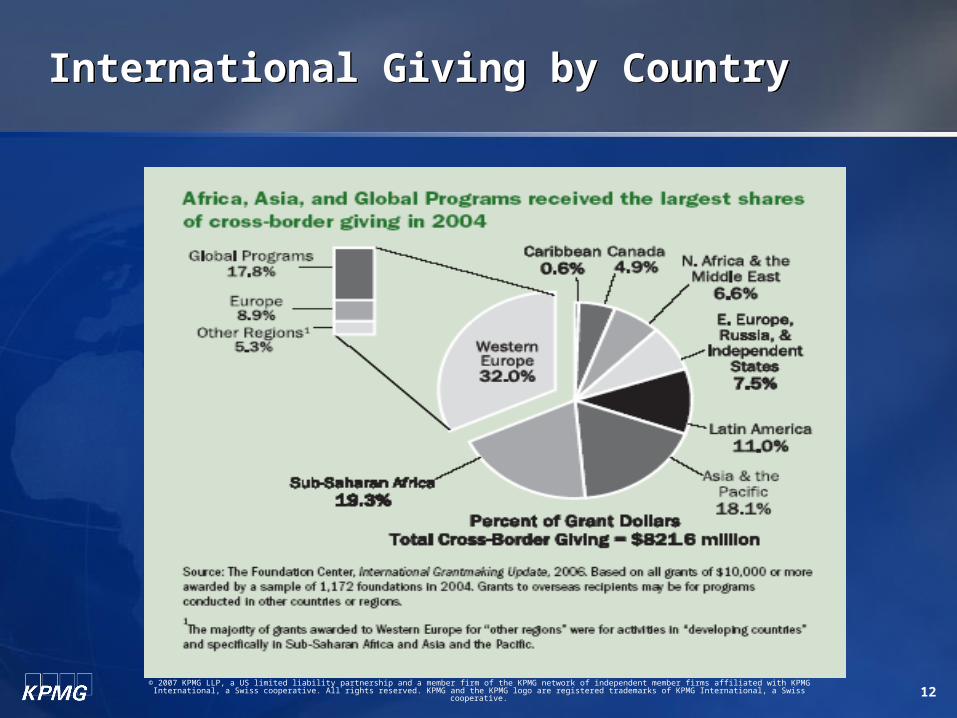

International Giving by CountryInternational Giving by Country

13© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Companies that Gave More Than $1 million to Charities Outside the United StatesCompanies that Gave More Than $1 million to Charities Outside the United States

In a survey conducted by The Chronicle on In a survey conducted by The Chronicle on Philanthropy, 39 Fortune 500 companies reported Philanthropy, 39 Fortune 500 companies reported giving over $1M to charities outside the US in 2006.giving over $1M to charities outside the US in 2006.

The range of giving was from $1.2M to $790M.The range of giving was from $1.2M to $790M.

14© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

2005 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2006

2005 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2006

15© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

2006 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2007

2006 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2007

16© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

2006 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2007

2006 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2007

17© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

2006 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2007

2006 Corporate International Giving

Source: Committee Encouraging Corporate Philanthropy, Giving by the Numbers 2007

18© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Challenges of International Giving and Grantmaking

Challenges of International Giving and Grantmaking

19© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

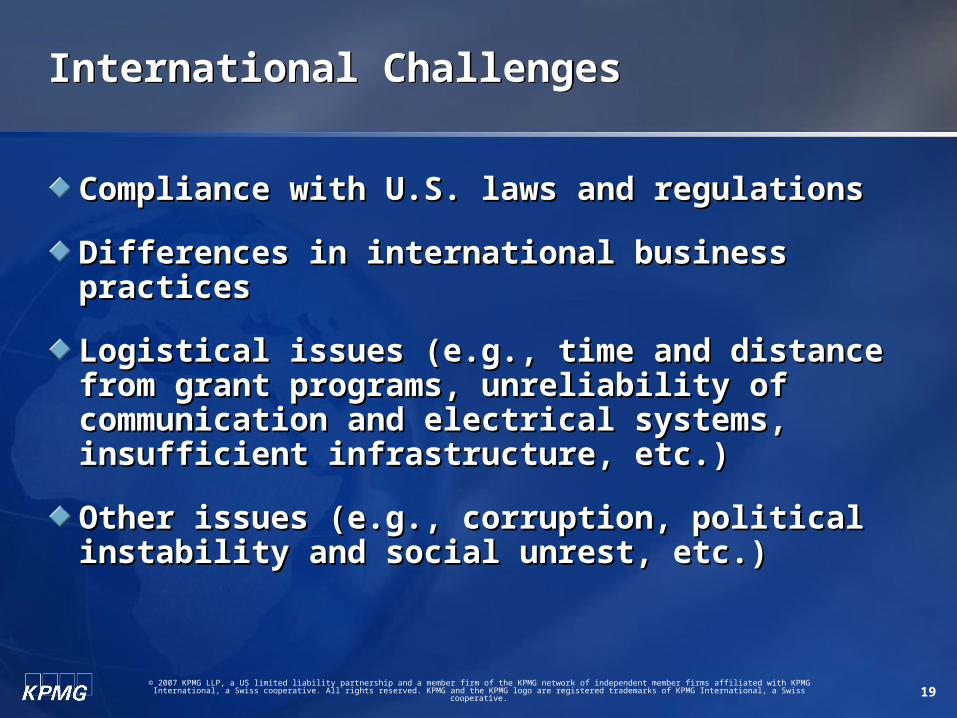

International ChallengesInternational Challenges

Compliance with U.S. laws and regulationsCompliance with U.S. laws and regulations

Differences in international business practicesDifferences in international business practices

Logistical issues (e.g., time and distance from grant Logistical issues (e.g., time and distance from grant programs, unreliability of communication and programs, unreliability of communication and electrical systems, insufficient infrastructure, etc.)electrical systems, insufficient infrastructure, etc.)

Other issues (e.g., corruption, political instability and Other issues (e.g., corruption, political instability and social unrest, etc.)social unrest, etc.)

20© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

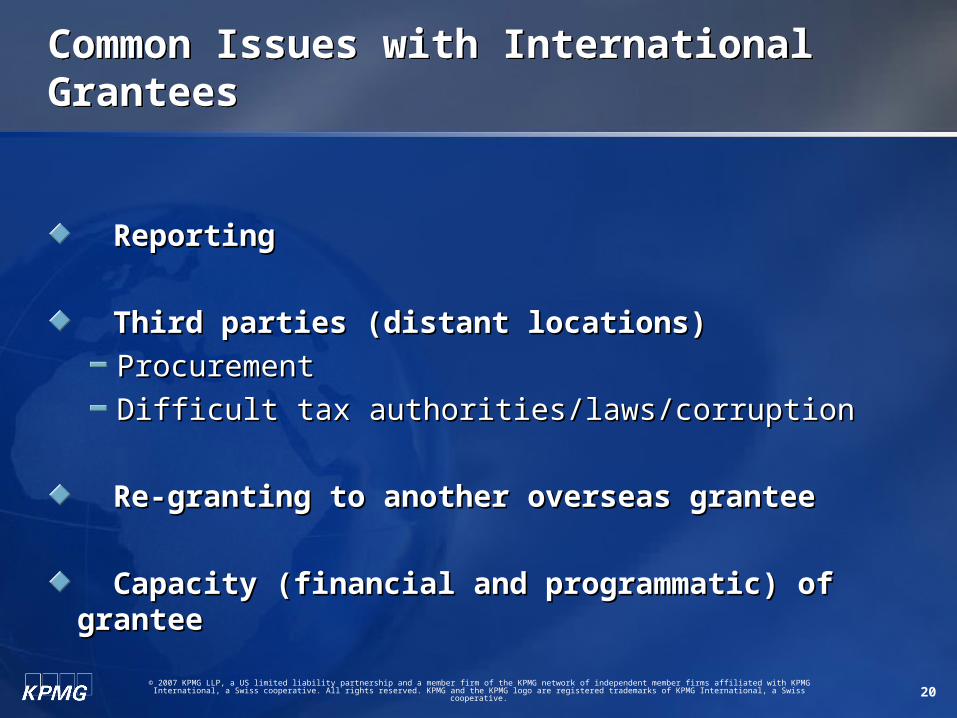

Common Issues with International GranteesCommon Issues with International Grantees

Reporting Reporting

Third parties (distant locations)Third parties (distant locations)

ProcurementProcurement

Difficult tax authorities/laws/corruptionDifficult tax authorities/laws/corruption

Re-granting to another overseas granteeRe-granting to another overseas grantee

Capacity (financial and programmatic) of granteeCapacity (financial and programmatic) of grantee

21© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

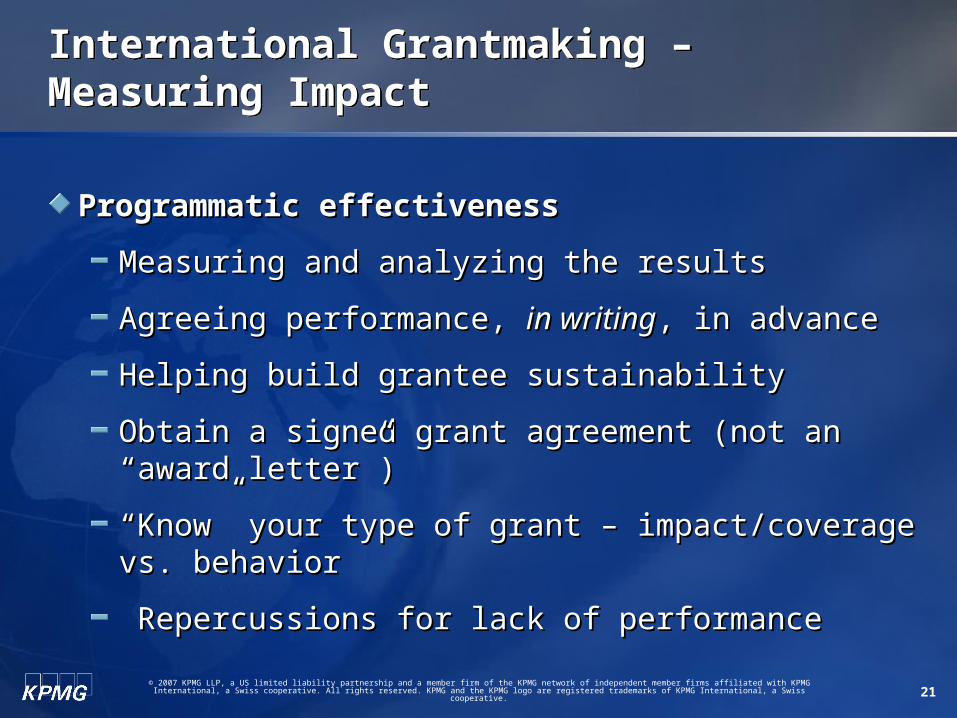

International Grantmaking – Measuring ImpactInternational Grantmaking – Measuring Impact

Programmatic effectivenessProgrammatic effectiveness

Measuring and analyzing the resultsMeasuring and analyzing the results

Agreeing performance, Agreeing performance, in writingin writing, in advance, in advance

Helping build grantee sustainabilityHelping build grantee sustainability

Obtain a signed grant agreement (not an “award letter”)Obtain a signed grant agreement (not an “award letter”)

““Know” your type of grant – impact/coverage vs. Know” your type of grant – impact/coverage vs. behaviorbehavior

Repercussions for lack of performance Repercussions for lack of performance

22© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Corporate Giving Priorities and Challenges in 2007 Corporate Giving Priorities and Challenges in 2007

In a survey conducted by The Conference Board, In a survey conducted by The Conference Board, international giving was noted as a top concern for international giving was noted as a top concern for individuals in-charge of corporate giving programs:individuals in-charge of corporate giving programs:

- - “The challenge of global giving was mentioned most “The challenge of global giving was mentioned most frequently as the single biggest new challenge to be frequently as the single biggest new challenge to be addressed in 2007.”addressed in 2007.”

- - “The size of the business presence in a foreign market is “The size of the business presence in a foreign market is the most important factor in determining international the most important factor in determining international giving priorities.”giving priorities.”

23© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Compliance with U.S. Tax and Other Laws – What to Be Aware of When Giving Cash, Products

or Services

Compliance with U.S. Tax and Other Laws – What to Be Aware of When Giving Cash, Products

or Services

24© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Compliance with U.S. Tax and Other LawsCompliance with U.S. Tax and Other Laws

Compliance with Anti-Terrorism MeasuresCompliance with Anti-Terrorism MeasuresExecutive Order 13224Executive Order 13224

The Patriot ActThe Patriot Act

Treasury Department GuidelinesTreasury Department Guidelines

Grants from Private FoundationsGrants from Private FoundationsInternal Revenue Code Section 4945, Taxes on Internal Revenue Code Section 4945, Taxes on Taxable ExpendituresTaxable Expenditures

25© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Compliance with Anti-Terrorism MeasuresCompliance with Anti-Terrorism Measures

Patriot ActPatriot ActSigned into law by President Bush on 26 October 2001Signed into law by President Bush on 26 October 2001Enhanced the authority of U.S. law enforcement for the stated Enhanced the authority of U.S. law enforcement for the stated purpose of fighting terrorist acts in the United States and abroadpurpose of fighting terrorist acts in the United States and abroadProhibits an organization from willfully providing or collecting funds Prohibits an organization from willfully providing or collecting funds with the intention or knowledge that such funds will be used to carry with the intention or knowledge that such funds will be used to carry out terrorismout terrorism

Executive Order 13224Executive Order 13224Executed by President Bush on 23 September 2001Executed by President Bush on 23 September 2001Blocks property and property interests in the U.S. of certain Blocks property and property interests in the U.S. of certain individuals and entities (“persons”)individuals and entities (“persons”)Prohibits U.S. persons and persons within the U.S. from dealing in Prohibits U.S. persons and persons within the U.S. from dealing in blocked property or making or receiving contributions of funds, blocked property or making or receiving contributions of funds, goods and services to or for the benefit of persons subject to the goods and services to or for the benefit of persons subject to the Executive OrderExecutive OrderProhibits donations of food, clothing, medicine and other such Prohibits donations of food, clothing, medicine and other such items to persons whose property is blocked under the Executive items to persons whose property is blocked under the Executive Order, even if the donations are intended to relieve human Order, even if the donations are intended to relieve human sufferingsuffering

26© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Compliance with Anti-Terrorism MeasuresCompliance with Anti-Terrorism Measures

OFACOFAC

The Treasury Guidelines (2002, 2005, and 2006)The Treasury Guidelines (2002, 2005, and 2006)

Voluntary guidelines issued in 2002Voluntary guidelines issued in 2002

Amended version and invitation for public comment Amended version and invitation for public comment issued in 2005issued in 2005

Upon receipt of comments, revised version issued in Upon receipt of comments, revised version issued in September 2006September 2006

27© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Code Section 4945, Taxable ExpendituresCode Section 4945, Taxable Expenditures

Taxable Expenditures include: Taxable Expenditures include: Grants to carry on propaganda, or otherwise attempt to influence Grants to carry on propaganda, or otherwise attempt to influence legislation, legislation,

Grants to influence the outcome of any specific public election, Grants to influence the outcome of any specific public election, or to carry on, directly or indirectly, any voter registration drive,or to carry on, directly or indirectly, any voter registration drive,

Grants to an individual for travel, study, or other similar purposes Grants to an individual for travel, study, or other similar purposes by such individual (except as specifically provided)by such individual (except as specifically provided)

Grants to organizations which are not U.S. public charities Grants to organizations which are not U.S. public charities or exempt operating foundations, unless expenditure or exempt operating foundations, unless expenditure responsibility is exercised with respect to the grantresponsibility is exercised with respect to the grant, or, or

Grants for a purpose other than one specified in Section 170(c)Grants for a purpose other than one specified in Section 170(c)(2)(B).(2)(B).

28© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Grants to Non-Public CharitiesGrants to Non-Public Charities

Good Faith Determination of U.S. Public Charity Good Faith Determination of U.S. Public Charity Equivalency:Equivalency:

Equivalency AffidavitEquivalency AffidavitOpinion of CounselOpinion of Counsel

Expenditure Responsibility: To exert all reasonable Expenditure Responsibility: To exert all reasonable efforts and to establish adequate procedures to efforts and to establish adequate procedures to

See that the grant is spent solely for the purpose for which See that the grant is spent solely for the purpose for which made,made,Obtain full and complete reports from the Grantee on how the Obtain full and complete reports from the Grantee on how the funds were spent, andfunds were spent, andMake full and detailed reports with respect to such expenditures Make full and detailed reports with respect to such expenditures to the Secretary.to the Secretary.

29© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Expenditure Responsibility-RequirementsExpenditure Responsibility-Requirements

Pre-grant inquiryPre-grant inquiryWritten grant commitment, signed by an appropriate Written grant commitment, signed by an appropriate officer of the Grantee, containing the Grantee’s officer of the Grantee, containing the Grantee’s agreement to:agreement to:

Repay any portion of the grant not used for the purposes of the grant,Repay any portion of the grant not used for the purposes of the grant,Submit full and complete annual reports on the manner in which the Submit full and complete annual reports on the manner in which the funds are spent and progress made in accomplishing purposes of the funds are spent and progress made in accomplishing purposes of the grant,grant,Maintain records of receipts and expenditures and make its books and Maintain records of receipts and expenditures and make its books and records available to the Grantor, andrecords available to the Grantor, andNot use any grant funds to carry on propaganda, or otherwise attempt Not use any grant funds to carry on propaganda, or otherwise attempt to influence legislation; to influence the outcome of any specific public to influence legislation; to influence the outcome of any specific public election or to carry on directly or indirectly any voter registration drive; to election or to carry on directly or indirectly any voter registration drive; to make any grant which does not comply with 4945(d)(3) or (4) or to make any grant which does not comply with 4945(d)(3) or (4) or to undertake any activity for any purpose other than one specified in undertake any activity for any purpose other than one specified in section 170(c)(2)(B).section 170(c)(2)(B).

Receipt of Grantee reportsReceipt of Grantee reportsReporting to Internal Revenue ServiceReporting to Internal Revenue Service

30© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Expenditure Responsibility-Special ConsiderationsExpenditure Responsibility-Special Considerations

Grants for Endowments or Capital ExpendituresGrants for Endowments or Capital ExpendituresLong term required reporting (shorter for capital expenditures)Long term required reporting (shorter for capital expenditures)

Program Related InvestmentsProgram Related InvestmentsSlight modifications to the Expenditure Responsibility Slight modifications to the Expenditure Responsibility requirementsrequirements

Earmarked GrantsEarmarked GrantsLook through to the status of the ultimate GranteeLook through to the status of the ultimate Grantee

Grants to Foreign GovernmentsGrants to Foreign GovernmentsConsider use of a Foreign Government Affidavit and other due Consider use of a Foreign Government Affidavit and other due diligence deemed prudent as good grantmaking proceduresdiligence deemed prudent as good grantmaking procedures

31© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Expenditure Responsibility-ViolationsExpenditure Responsibility-Violations

Diversions by GranteesDiversions by GranteesAre taxable expenditures of the Grantor Are taxable expenditures of the Grantor unlessunless Grantor takes all Grantor takes all reasonable and appropriate steps to recover any diverted grant reasonable and appropriate steps to recover any diverted grant funds and the dedication of other grant funds held by the funds and the dedication of other grant funds held by the Grantee, withhold all future payments until funds are restored, Grantee, withhold all future payments until funds are restored, receives Grantee’s assurances that no future diversions will receives Grantee’s assurances that no future diversions will occur, and requires Grantee to take extraordinary measures to occur, and requires Grantee to take extraordinary measures to prevent future diversionsprevent future diversions

Grantee’s Failure to Make ReportsGrantee’s Failure to Make ReportsAre taxable expenditures of the Grantor Are taxable expenditures of the Grantor unlessunless the Grantor has the Grantor has made a written grant commitment as discussed on the previous made a written grant commitment as discussed on the previous slide, complied with the IRS reporting requirements, made slide, complied with the IRS reporting requirements, made reasonable efforts to obtain the required reports, and withholds reasonable efforts to obtain the required reports, and withholds all future payments on the grant and all other grants to the all future payments on the grant and all other grants to the Grantee until the report is furnishedGrantee until the report is furnished

32© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Expenditure Responsibility- ViolationsExpenditure Responsibility- Violations

Violations by the GrantorViolations by the GrantorFails to make a pre-grant inquiry,Fails to make a pre-grant inquiry,

Fails to make a grant agreement as discussed on the previous Fails to make a grant agreement as discussed on the previous slide, slide, oror

Fails to report to the Internal Revenue ServiceFails to report to the Internal Revenue Service

33© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Grants to U.S. Charities Outside the United StatesGrants to U.S. Charities Outside the United States

Due Diligence and Good Grantmaking Procedures:Due Diligence and Good Grantmaking Procedures: Establish adequate procedures to foster due diligence over the use Establish adequate procedures to foster due diligence over the use

of the funds, including the requirements included under the of the funds, including the requirements included under the Expenditure Responsibility rulesExpenditure Responsibility rules

Pre-grant inquiryPre-grant inquiry

Written grant commitment with limitations as to the uses of the Written grant commitment with limitations as to the uses of the grant fundsgrant funds

Receipt and review of periodic program and financial reportsReceipt and review of periodic program and financial reports

Procedures based upon a “risk-based model”Procedures based upon a “risk-based model”

34© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Product DonationsProduct Donations

Product Donations are a growing percentage of overall Product Donations are a growing percentage of overall corporate giving.corporate giving.

The U.S. federal government has long encouraged The U.S. federal government has long encouraged philanthropy by allowing an income tax donation for philanthropy by allowing an income tax donation for charitable contributions of appreciated property or charitable contributions of appreciated property or money.money.

The issues that companies need to consider when they The issues that companies need to consider when they donate products abroad:donate products abroad:

- Regulations in Foreign Jurisdiction- Regulations in Foreign Jurisdiction

- VAT- VAT

35© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Questions and AnswersQuestions and Answers

36© 2007 KPMG LLP, a US limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Presenter’s contact detailsPresenter’s contact details

Janet S. WongJanet S. Wong PartnerPartner(650) 404-5383(650) 404-5383 [email protected]

www.us.kpmg.comwww.us.kpmg.com

All information provided is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.