Presented by: Erike Young, MPPA, CSP, ARM-E · 2018-10-29 · –Regression analysis...

69

Presented by: Erike Young, MPPA, CSP, ARM-E 1

Transcript of Presented by: Erike Young, MPPA, CSP, ARM-E · 2018-10-29 · –Regression analysis...

Presented by:

Erike Young, MPPA, CSP, ARM-E

1

Chapter 4

Operational, Financial and Strategic Risk

Operational Risk

• Organizations may view hazards and operational risk as separate categories– Explore increasing positive risk while managing negative risk– Operational risk is integrated in every activity of an

organization and should be evaluated based on an organization’s strategic objectives, risk appetite and risk tolerance.

• Typical framework for managing operation risk includes these categories– People– Process– Systems– External events

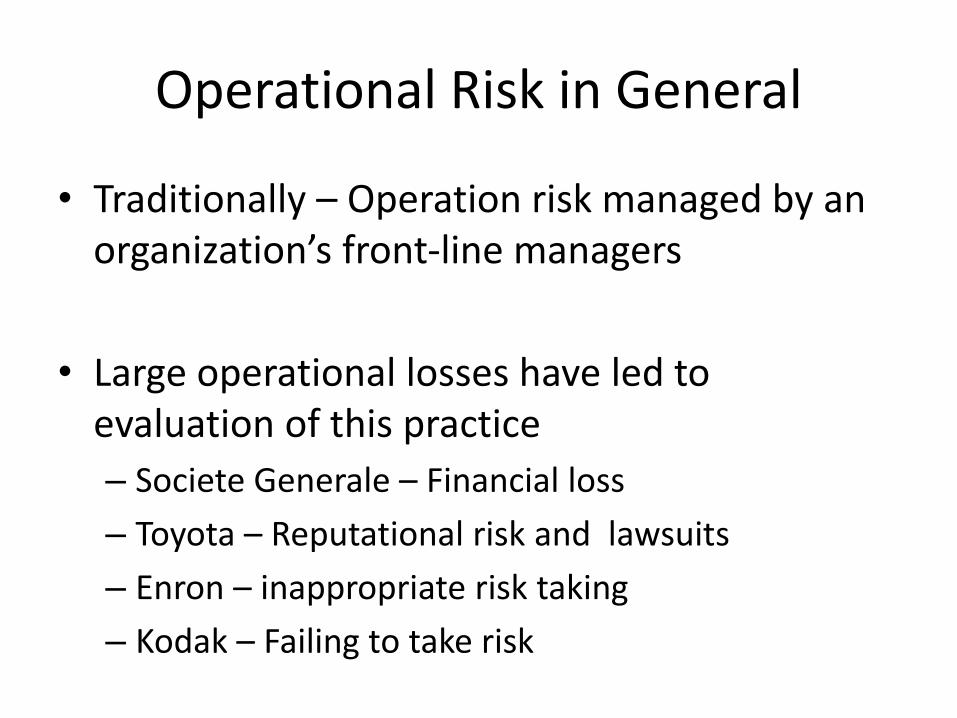

Operational Risk in General

• Traditionally – Operation risk managed by an organization’s front-line managers

• Large operational losses have led to evaluation of this practice

– Societe Generale – Financial loss

– Toyota – Reputational risk and lawsuits

– Enron – inappropriate risk taking

– Kodak – Failing to take risk

Operational Risk: People

• Includes all employees of an organization– May include organization’s contractors, vendors, clients, and

others

• Typically risks associated with people are hazard risk or other insurable risk– Injury– EPL (insurable and reputational damage)– Resignation– Theft and dishonesty – Wells Fargo 2017

• Non-insurable – Reputational risks• Organizational Culture can influence risk taking/avoidance

– Risks related to opportunities that manager and employees do not take are not insurable

Strategies to Mitigate People Risk

Operational Risk: Process, Systems, External Events

• Process Risk

– Procedures and practices organizations us to conduct business activities.

– Risk occurs at point at which practice departs from procedure

– Procedures should represent best practices designed for quality and safety of products and employees

– Examples: Bay Bridge Bolt Inspection Process, counting cash tills, Overbooking of airline passengers

Operational Risk: Process, Systems, External Events

• Systems Risk– Technology

• Function of technology, risks of intentional or accidental failure, and security risks

• Examples: Data breach

– Equipment• Failure of equipment to continue operations

– Could be considered an insurable risk

• Potential loss of customers

• Example: Raley’s Distribution Center Battery Rack

Operational Risk: Process, Systems, External Events

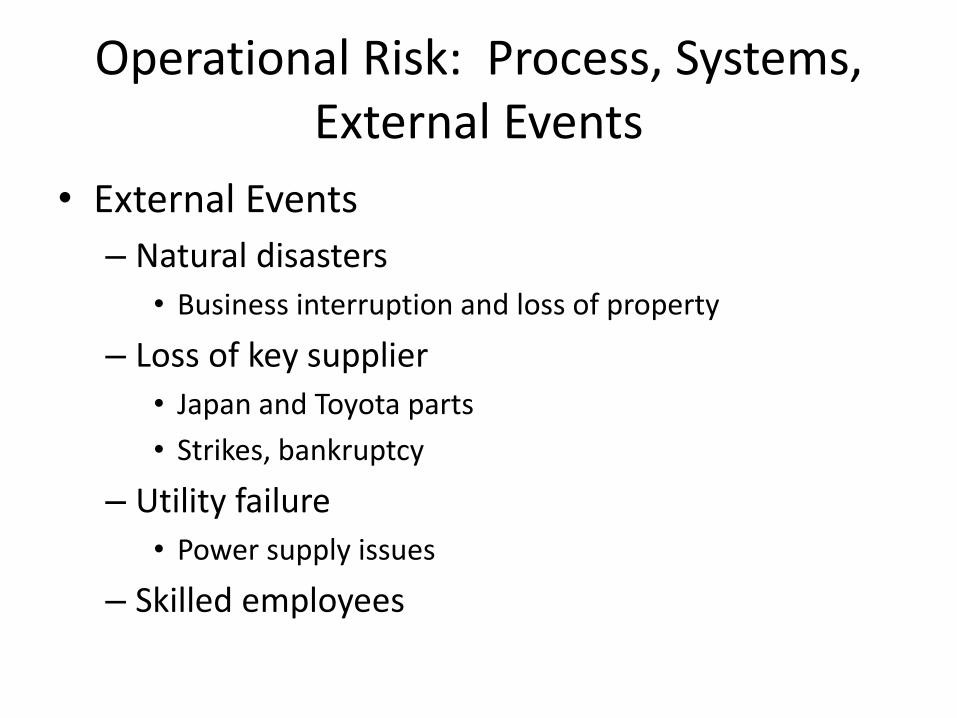

• External Events

– Natural disasters

• Business interruption and loss of property

– Loss of key supplier

• Japan and Toyota parts

• Strikes, bankruptcy

– Utility failure

• Power supply issues

– Skilled employees

Operational Risk Indicators

• Root Causes– The event or circumstance that directly leads to an

occurrence.

– Retrospective reviews can help identify root causes, but may be too late to prevent catastrophic loss

• Key Risk Indicator (KRI)– A financial or non-financial metric used to help

define and measure potential losses.• Must be leading, not lagging, to be effective

Heinrich’s Theory

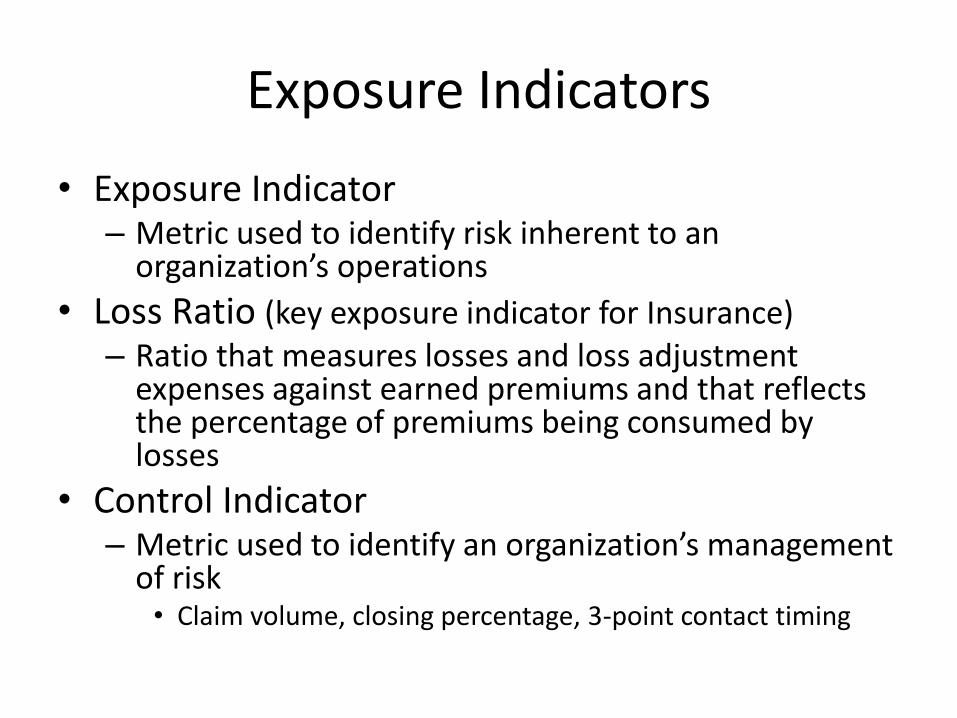

Exposure Indicators

• Exposure Indicator– Metric used to identify risk inherent to an

organization’s operations

• Loss Ratio (key exposure indicator for Insurance)– Ratio that measures losses and loss adjustment

expenses against earned premiums and that reflects the percentage of premiums being consumed by losses

• Control Indicator– Metric used to identify an organization’s management

of risk• Claim volume, closing percentage, 3-point contact timing

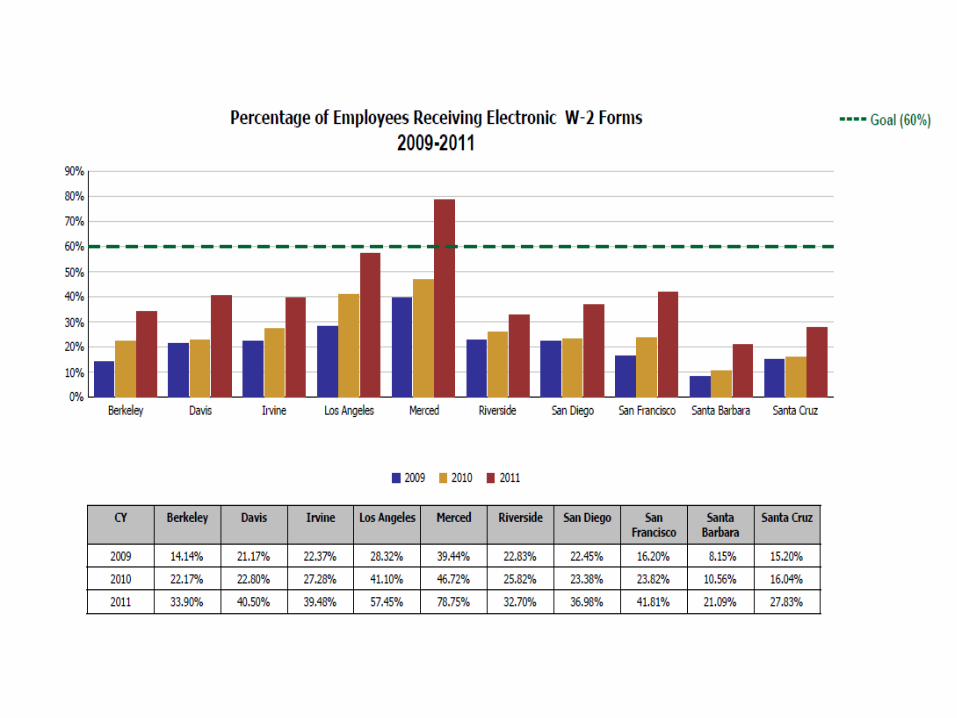

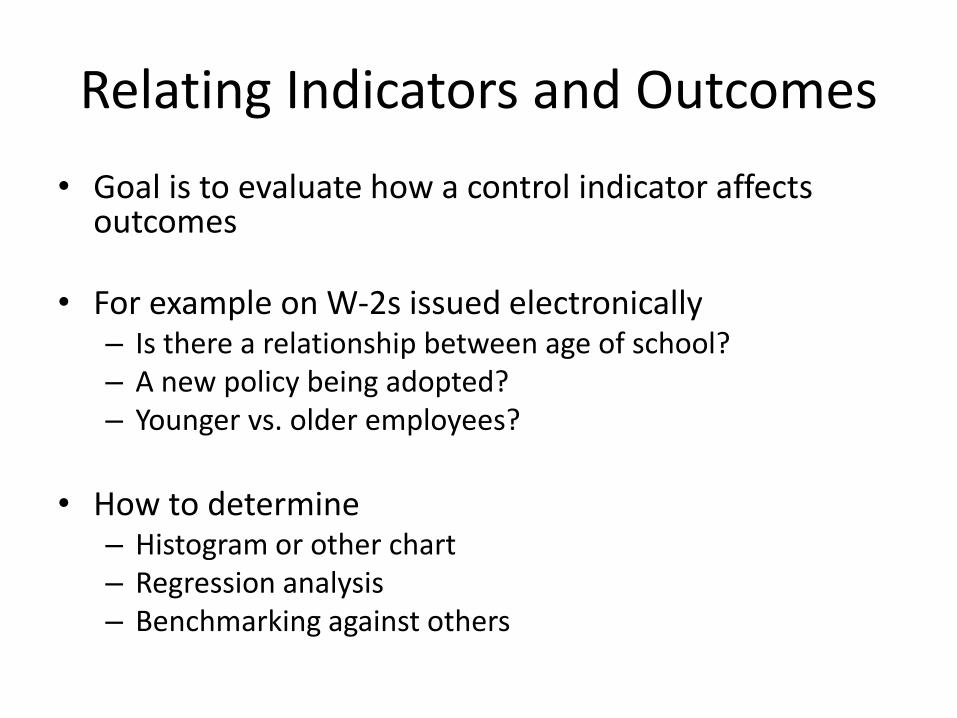

Relating Indicators and Outcomes

• Goal is to evaluate how a control indicator affects outcomes

• For example on W-2s issued electronically– Is there a relationship between age of school?– A new policy being adopted?– Younger vs. older employees?

• How to determine– Histogram or other chart– Regression analysis– Benchmarking against others

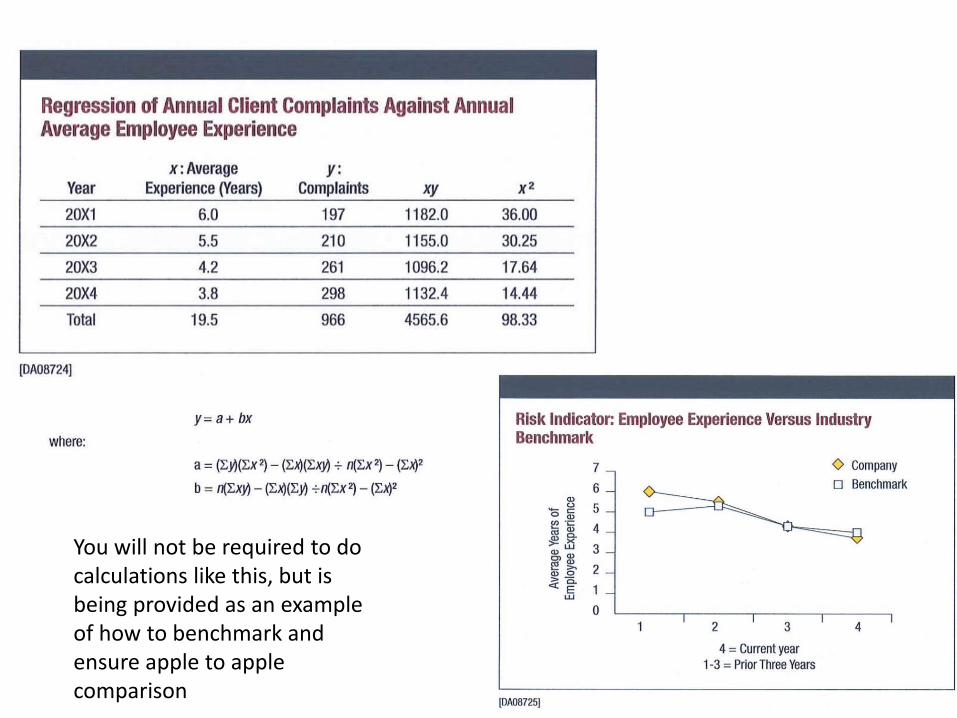

You will not be required to do calculations like this, but is being provided as an example of how to benchmark and ensure apple to apple comparison

Financial Risk

• Three major types of financial risk– Market Risk

– Credit Risk

– Price Risk

• Two main characteristics– External risk with the potential to affect an organization’s

objectives

– Risk can be reduced through financial contract, such as derivative

• Goal of financial risk management is risk optimization– Protecting against downside risk

– Capturing upside risk

Financial Risk

• Risk Optimization

– A state whereby risk and return are balanced so that a maximum return is achieved for the level of risk accepted by an organization.

• Hedging

– A financial transaction in which one asset is held to offset the risk associated with another asset.

• Futures contracts

• Credit default swap

Market Risk

• Market risk arises from changes in the value of financial instruments– Systemic risk is risk that is common to all securities of the

same general class and therefore cannot be eliminated by diversification

• Five major categories of market risk– Currency price risk– Interest rate risk– Commodity price risk– Equity price risk– Liquidity risk

Market Risk

• Currency Price Risk

– Risks related to changes in the currency exchange rates of countries

– Can hedge by procuring locally

Market Risk

• Interest Rate Risk

– Risk that a security’s future value will decline because of changes in interest rates

• Swaps can be used to hedge against interest rate volatility –

• Swap is an agreement between two organizations to exchange payments based on changes in the value of an asset, yield, or index over a specific period of time.

– Insurers vulnerable because

• they typically use bonds with durations linked to expected payments and

• earn much of income from investment returns on reserves

Market Risk

• Interest Rate Risk

– Cash matching

• Process of matching an investment’s maturity value with the amount of expected loss payments

– Zero-coupon bond

• A corporate bond that does not pay periodic interest income

– Reinvestment risk

• Risk that the rate at which periodic interest payments can be reinvested over the life of the investment will be unfavorable.

Market Risk

• Commodity Price Risk

– Risk associated with a change in the prices of commodities that are necessary to an organization’s operations – Example of Oil

– Commodity price can effect cash flow

– Commodity futures contract

• A contract either to make or accept delivery of a specified quantity of a commodity on a given date– Form of hedging

Market Risk

• Equity Price Risk– Risk that changes in the price of a stock or another security

will increase or decrease

– Can be classified as the following• Risks related to organization’s share price

• Risks related to organization’s investments in external stocks and other securities

• Risk related to average share price in a market or market sector

– Call Option• Option to buy a set amount of underlying security at any time

within a specified period

– Put Option• Option giving the holder the right to sell a set amount of

underlying security at any time within a specified period

Market Risk

• Liquidity Risk– Organization’s liquidity is related to its cash or ability

to raise cash.• Possibility that large numbers of clients could withdraw

funds (run on the bank)

• Possibility of line of credit being available or revoked

• Credit Risk– Risk that borrows will not pay back loan

– Only has a downside or negative potential

– Inherent risk for financial institutions

Market Risk

• Credit Risk– Two types of credit risk

• Firm specific credit risk

• Systemic credit risk

– Firm specific risk can be reduced through• diversification of type and duration of credit issued

• Evaluation of creditworthiness

• Transfer of some risk by selling loans to other organizations

– Systemic credit risk was caused by the selling of loans to other organizations with poor underwriting• Managed through regulatory oversight

Market Risk

• Price Risk

– Potential for a change in revenue or cost because of an increase or decrease in the price of a product or an input

• Price charged for products and services

• Price of assets purchased or sold by an organization

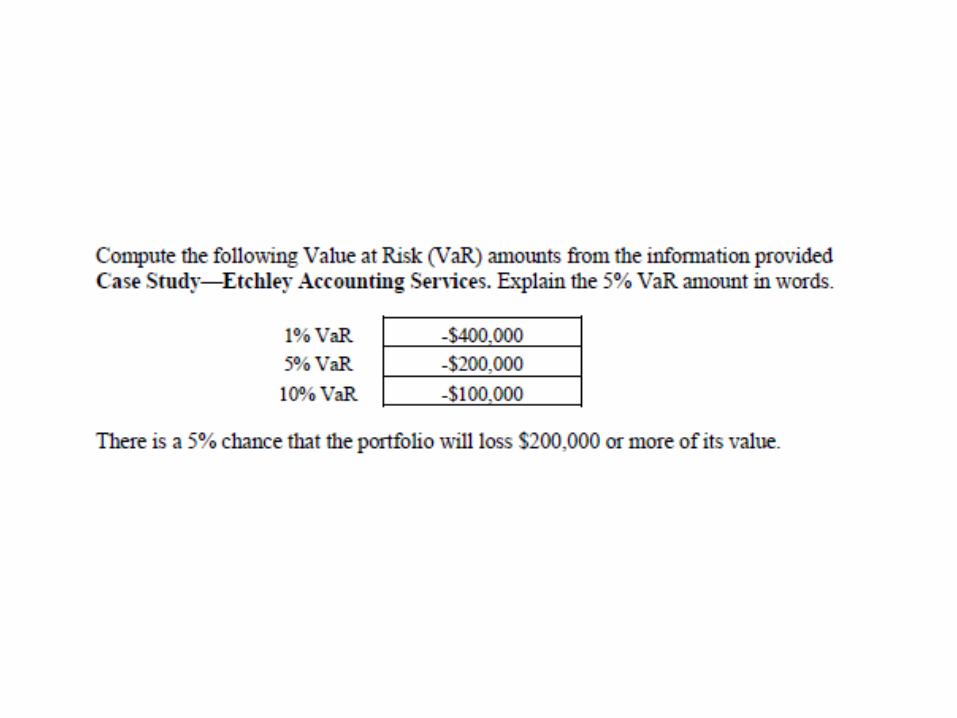

Value at Risk and Earnings at Risk

• Earnings at Risk (EaR)– Maximum expected loss of earnings within a specific

degree of confidence

• Value at Risk (VaR)– measures the probability of the loss in an investment’s

value exceeding a threshold level– VaR provides three key benefits as a risk measure:

• Potential loss associated with an investment can be quantified

• Complex positions are expressed as a single figure• Loss is expressed in easily understood monetary terms

– VaR limitations• Does not accurately measure the extent to which a loss

might exceed the VaR threshold

Earnings at Risk

• EaR is used primarily by nonfinancial organizations to model the effects of changes in various factors of an organization’s earnings– Prices of products

– Sales

– Prices of commodities and components

– Production costs

• Based upon a specific confidence level and distribution curve

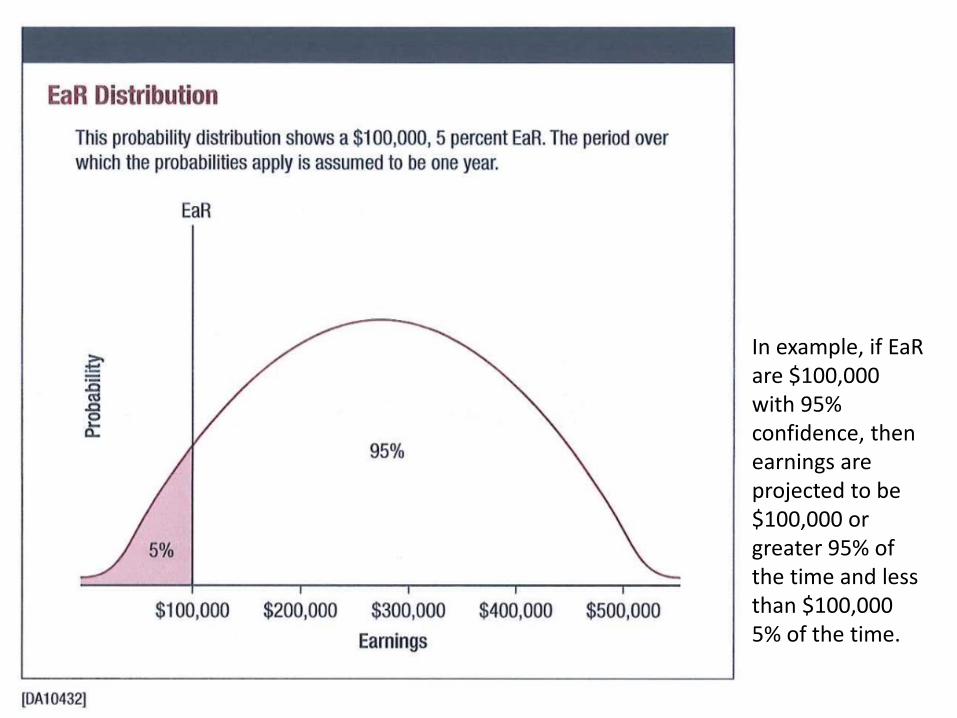

Distribution Curve

Source: Risk Assessment

In example, if EaRare $100,000 with 95% confidence, then earnings are projected to be $100,000 or greater 95% of the time and less than $100,000 5% of the time.

Regulatory Capital

• Governments are increasingly prescribing capital requirements– Capital is the accumulated assets of a business or an

owner’s equity in a business

– Risk capital is the level of capital required to provide a cushion against unexpected loss of economic value at a financial institution

– Equity Capital – preferred stock, surplus, common stock and capital reserves that are not available for sale

– Leverage – the practice of using borrowed money to invest• Major factor of the 2008 financial crisis

Regulatory Capital

• Basel II

Regulatory Capital• Basel II major pillars

– Minimum capital requirements that address risk

– Supervisory review

– Market discipline

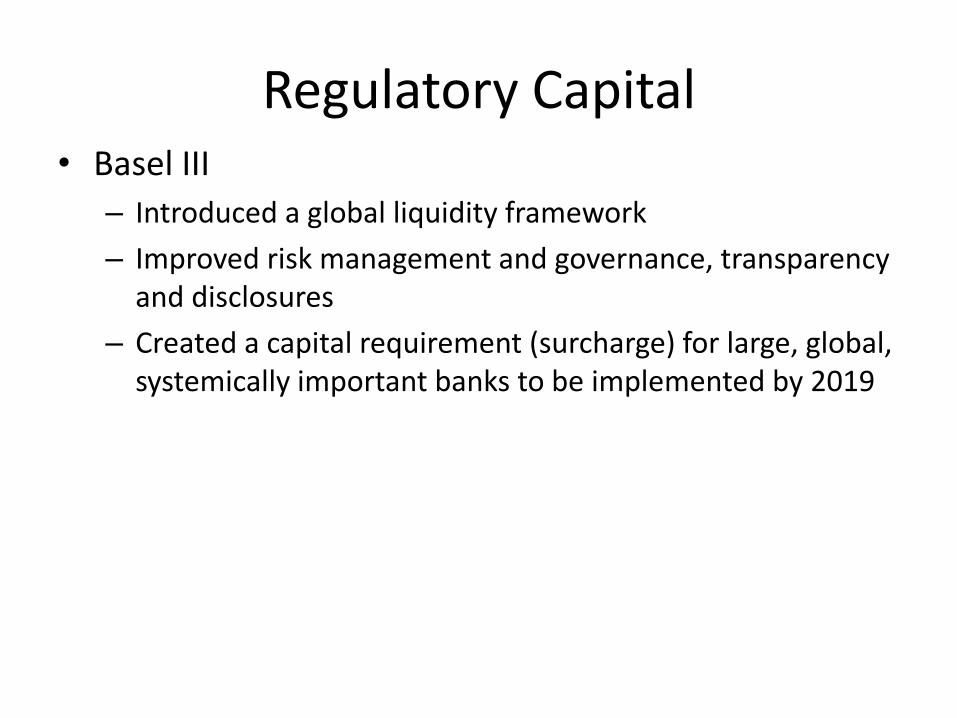

Regulatory Capital• Basel III

– Introduced a global liquidity framework

– Improved risk management and governance, transparency and disclosures

– Created a capital requirement (surcharge) for large, global, systemically important banks to be implemented by 2019

RBC Requirements for Insurers• Purpose of insurer’s capital is to enable it to meet its

obligations to policyholders and claimants in the event of unexpectedly poor investment performance or underwriting results

• RBC for Insurers Model Act adopted in most states– Enables insurance regulators to take action before an insurer

becomes too financially weak to be rehabilitated

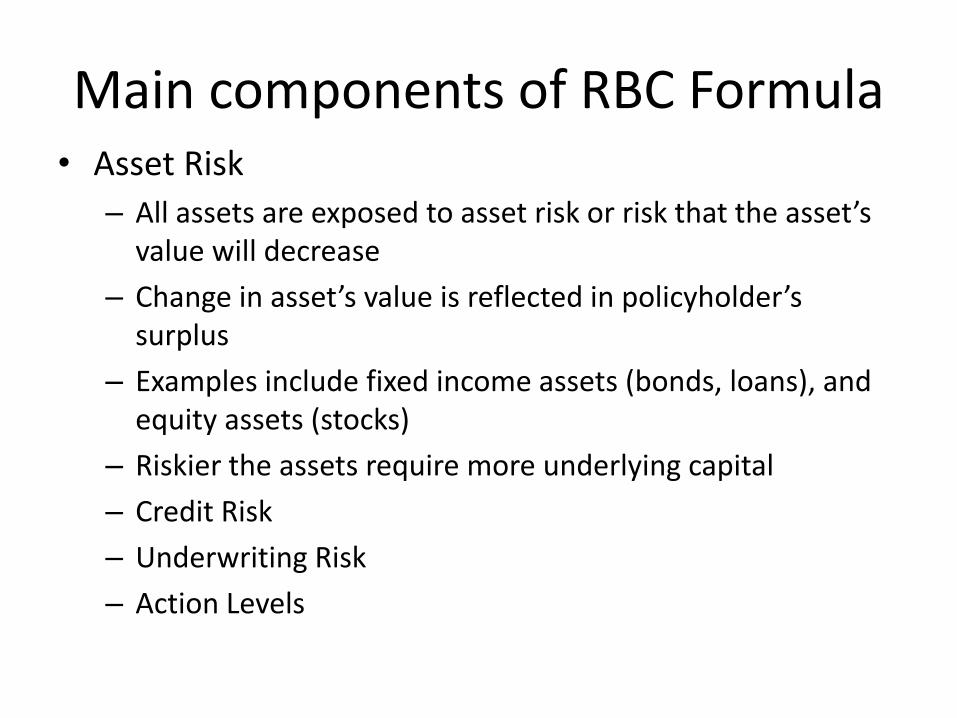

• Main components of RBC Formula– Asset Risk

– Credit Risk

– Underwriting Risk

– Action Levels

Main components of RBC Formula• Asset Risk

– All assets are exposed to asset risk or risk that the asset’s value will decrease

– Change in asset’s value is reflected in policyholder’s surplus

– Examples include fixed income assets (bonds, loans), and equity assets (stocks)

– Riskier the assets require more underlying capital

– Credit Risk

– Underwriting Risk

– Action Levels

Main components of RBC Formula• Credit Risk

– Reflects the possibility that insurer will not be able to collect money that it is owed

– Source of most credit risk is receivables• Federal income tax recoverables

• Interest

• Dividends

• Real estate income

– Each asset multiplied by RBC factor to determine credit risk

Main components of RBC Formula• Underwriting risk

– Risk of loss if it collects insufficient premiums and/or significantly underestimates its loss reserves

– RBC formula applies factor based on different lines of coverage to reflect industry experience

– Takes into account excessive premium growth to account for price cutting

• Action levels– Results of RBC formula determine action to be taken

– 200% or more no action required

– 100-200 – may need to take corrective action

– 70-100 – placed under regulatory control

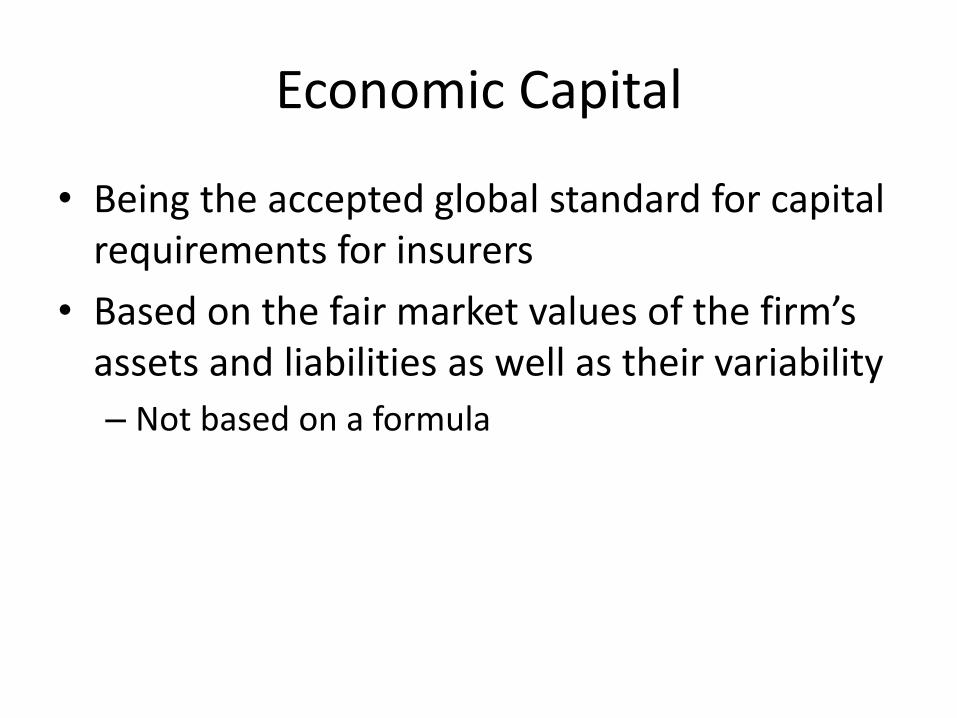

Economic Capital

• Being the accepted global standard for capital requirements for insurers

• Based on the fair market values of the firm’s assets and liabilities as well as their variability

– Not based on a formula

Economic Capital

Fair Value Accounting

• Fair value is a market-based measurement based on the price the asset owner would receive by selling the asset, or that a liability holder would pay to transfer the liability

• Fair value can be influenced by several factors– Most important factors are cash flows and the risk attached to

those cash flows– Example of present value of bond held by you and issued by an

organization in financial difficulty• This is why credit rating agencies are important

• Understand that GAAP and SAP are used by insurers but may use nonmarket values (depreciation)– Can result in misleading indications of an organization’s financial

status– Example, real estate valued based on cost rather than market

value

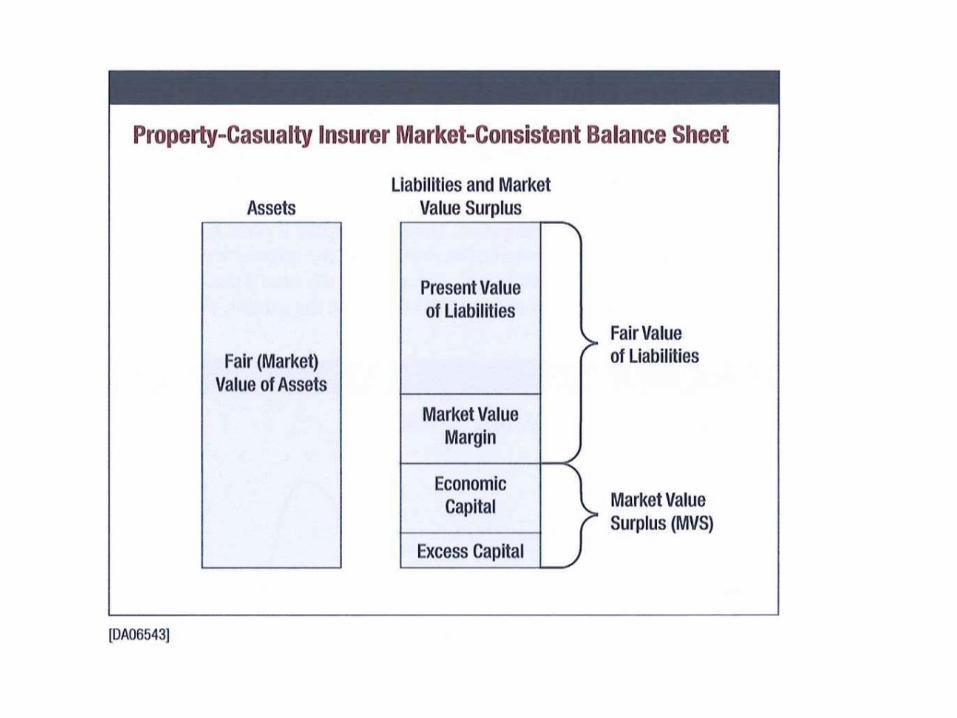

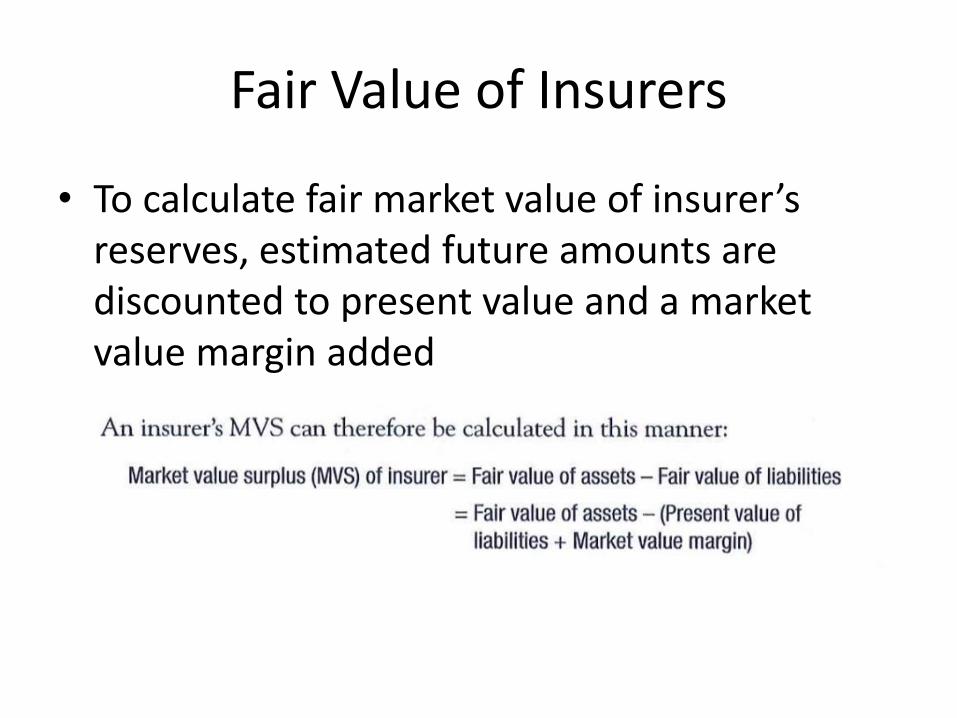

Fair Value of Insurers

• Calculation difficult because no market exists for trading loss reserves and unearned premium reserves– Reserve estimates are uncertain due to future loss

payments and timing of those payments

– Difficult to transfer reserves to reinsurer or another party at present value (loss portfolio transfer or LPT)

– Requires additional payment called risk premium, risk margin, or market value margin

Fair Value of Insurers

• To calculate fair market value of insurer’s reserves, estimated future amounts are discounted to present value and a market value margin added

MVS Practice

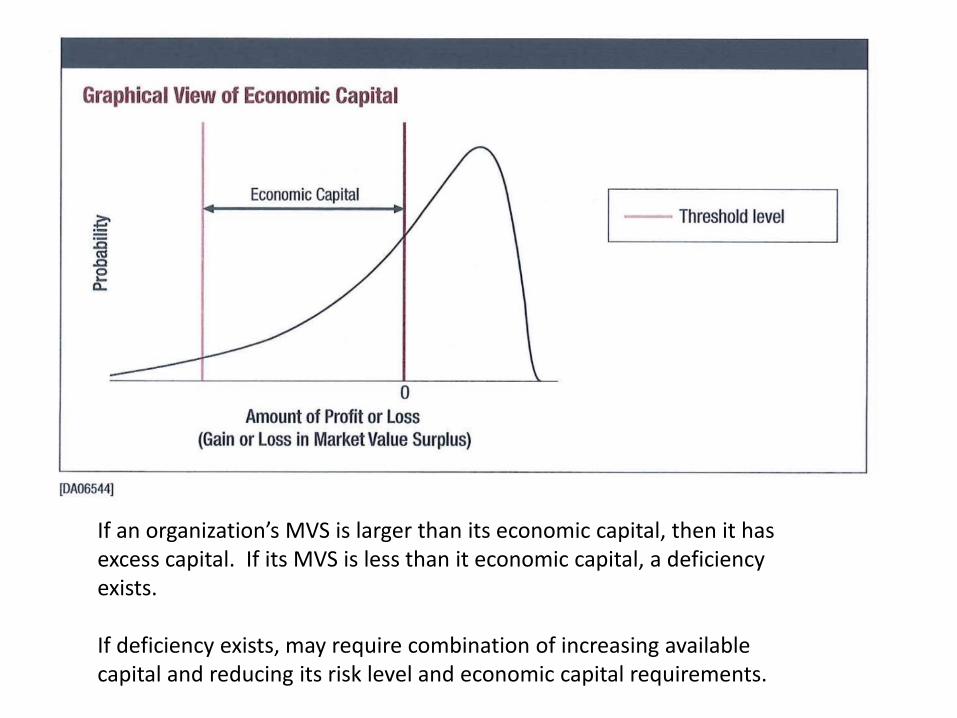

Economic Capital for Insurers

• Form of regulatory capital that is an estimate of capital a firm needs to remain solvent at a given risk tolerance level

If an organization’s MVS is larger than its economic capital, then it has excess capital. If its MVS is less than it economic capital, a deficiency exists.

If deficiency exists, may require combination of increasing available capital and reducing its risk level and economic capital requirements.

Advantages/Disadvantages of Economic Capital Analysis

• Advantages– Focuses attention on risks attached to organization’s

activities and helps define risk tolerance– Places value on an organization’s overall risk– Helps establish capital needs– Reveals capital requirements for different operations

and improve allocation– Helps organization understand economic capital

position and inform investors, rating agencies and regulators

– Quantitative measure for an ERM Program

Advantages/Disadvantages of Economic Capital Analysis

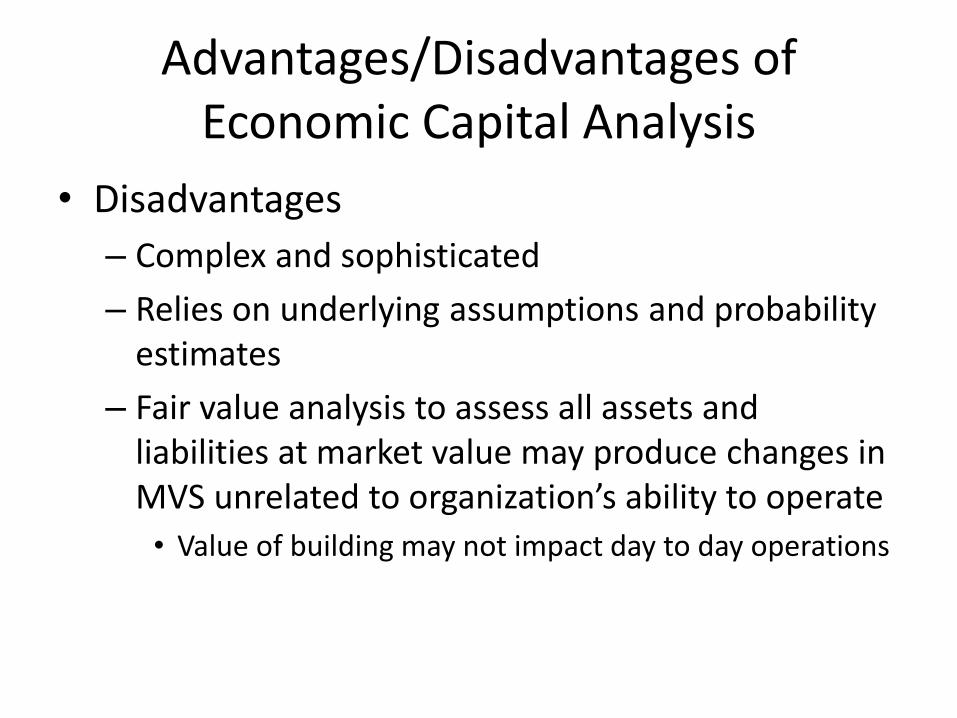

• Disadvantages

– Complex and sophisticated

– Relies on underlying assumptions and probability estimates

– Fair value analysis to assess all assets and liabilities at market value may produce changes in MVS unrelated to organization’s ability to operate

• Value of building may not impact day to day operations

Solvency II and Capital Requirements

• Solvency II is a fundamental review of the capitalization of insurers in the European Union

• Three Pillars– Quantitative requirements of capital based upon

insurer’s specific circumstances• Includes solvency capital requirement similar to economic

capital that would ensure 99.5% probability that insurer would meet it obligations over next year

– Sets requirements for insurer’s internal risk management process and for supervision of insurers

– Focus on reporting, disclosure and transparency of the risk assessment to public and regulators

Strategic Risk

• Strategic Risk Management– A discipline to achieve an organization’s strategic objectives,

cannot be applied to strategic risk

• Strategic risks are external to an organization and are considered systemic risks outside the control of any individual organization– Also includes speculative risks, which have +/- potential

• Three major strategic risks– Economic environment– Demographics– Political environment

Strategic Risk

• Economic Environment in which organization operates may effect an organization’s results.

• Examples:– Gross Domestic Product (GDP)

• Economic expansion or contraction

– Inflation• Deflation may require price cuts• Inflation increases production costs

– Financial Crisis, including sovereign debt crisis• Access to credit (doing business in Greece)

– International trade flows and restrictions• Tariffs and international agreements

Strategic Risk

• Demographics

– Aging workforce, life expectancy, and fertility rates can impact:

• Pool of skilled workers

• Pension fund issues and retiree healthcare obligations

• Shrinking markets for products

• Increased taxation or reduced govt. funding

Strategic Risk

• Political Environment

– Political risk is result of government action

• Defined as any action by a govt. that favors domestic over foreign organizations or poses a threat to a foreign organization

– Includes

• Wars

• Seizure of property

• Regulations

Questions