Presentazione di PowerPoint - Quaynote Communications · PDF fileEzio Vannucci February 2017....

22

Malta – February 23rd, 2017 New VAT and Customs regulations and resolutions for Yachting In ITALY Ezio Vannucci February 2017

Transcript of Presentazione di PowerPoint - Quaynote Communications · PDF fileEzio Vannucci February 2017....

Malta – February 23rd, 2017

New VAT and Customs

regulations and resolutions for Yachting

In ITALY

Ezio Vannucci

February 2017

News on APA ?The official reply of the IT Tax Authority to MYBA with

Consulenza Giuridica no. 954-20-2016 finally clarified the following:

1) The mere transfer of APA from the Charterer to Ownerand/or directly to the Captain is not subject to VAT;

2) The portion of APA funds used by the Captain to meetpersonal needs of the Charterer are not subject to VATas long as adequately recorded in the name of theCharterer ;

3) The portion of APA related to fuel and oil consumptionsare subject to VAT at the end of the Charter period atthe same rate of the Charter Fees .

February 2017

Do you need a charter

permit in Italy?NO, but pursuant article 2 point 3 of the IT Yacht Code 171/2005, every year allCommercial Yachts are required to deposit a specific Form to the Harbor Master in the first Italian Port call .

February 2017

Can the Beneficial owner

use his own yacht?

Yes, with a charter contract in place at a slightly discounted rate and paying VAT. The discount may not be greater thanthe percentage of the broker/charter manager’s commission.

February 2017

Is VAT due if the «place of

supply» is in a non-EU

Country?

Yes, on a pro rata basis for thenumber of days spent in Italianwaters at 22% VAT.

Ref. : article 7-quater point e)

February 2017

Is switching from Commercial to

Pleasure after importation a risk?

YES !! Since the Owning Company was granted a totalrelief of duties on the basis of its “Commercial status”:to ‘switch’ status the Yacht must first be formallyexported and then the Flag Registry must be changedto Pleasure on arrival in an extra EU Harbor.In the event the Yacht wishes to engage in Charteragain, it must be re-imported and the ‘switch’ fromPleasure to Commercial arranged in advance.

February 2017

What about switching from

pleasure to Commercial?

Our best advice is to arrange the switch from

pleasure to commercial before arriving in EU

waters or, anyhow, outside EU territory (i.e.: in Gibraltar, before reaching EU territory).

This solution allows the Yacht to avoid any

potential discussion with EU Customs concerning

the status of the Yacht.

Following the switch, an importation procedure is

necessary in order to start Charter activity in the

EU.

February 2017

NEWS on Customs in Italy for

Export formalities Proof of exit from Italian territory during an export procedure

is established by:

1. formerly: arrival in a NON-EU port

2. the new requirement: a declaration underwritten by the

Captain of the yacht when the same reaches international

waters (beyond 12 miles from the coast)

Ref. new Customs Circular no. 14/D of May 12th, 2016

The declaration should be confirmed by the logging the position

of the yacht in international waters using AIS (Automatic

Identification System) monitored by the Port Authorities.

February 2017

NEWS on Customs formalities in

Italy for onboard provisioning

Italian Tax Authority with Resolution no.1/E dated January9, 2017, in accordance with the new article 269 paragraph2 point c) of the Union Customs Code clarifies that:

- Any kind of goods supply in exemption of VAT and/orExcise, to Vessel should be not considered for VATpurpose and Export;

- Therefore art.8 point 1 letters a) and b) of the IT VATCode cannot be applied from 9th January 2017 to anyonboard provisioning and fuelling both for Pleasure andCommercial yachts;

- Commercial Vessels will remain entitled for the IT VATexemption in accordance with the provisions of article8bis of the IT VAT Code.

February 2017

ITALIAN COMMERCIAL

EXEMPTION

“the Italian BOFIP” by Resolution 2/E

12 January, 2017- Agenzia delle Entrate

It is important to point out, by such Resolution of Agenzia delle Entrate, Italy

follows a “path” already started in France by the so-called “BOFIP “(Bulletin Officiel dated May 12,2015) by French Fiscal Authorities

with the intention to clarify on the right to benefit from exemption on VAT for Commercial

Yacht supplies.

February 2017

“the Italian BOFIP” by Resolution 2/E 12 January 2017Agenzia delle Entrate definitely provides a clear

and correct interpretation of :

“vessel to be used for navigation on high seas”, stated by art. 8-bis, point 1, par. a) of DPR

633/72.

Article 8-bis of the Italian VAT Code, states the

VAT exemption regime can be applied to those

“operations” done by “Vessels used for navigation

on the high seas and carrying passengers for

reward or used for the purpose of commercial

(including Charter), industrial or fishing activities”.

February 2017

“the Italian BOFIP”

The exemption contained in art.8-bis is

applicable to all commercial yachts for:

- supply of goods for the fuelling and

provisioning;

- sales on board equipment, components and

spare parts;

- sales, refit works, repair and maintenance

works.

February 2017

“the Italian BOFIP”

In light of the above clarification, Italian

Tax Authority provides a clear definition

when a Vessel can be considered “to be

used for navigation on the high seas”:

more than 70% of the total “voyage“ of

the Vessel, during a calendar year, should

be on the “ high seas”

(ie. Commercial Vessel wishing to be

entitled to benefit from the VAT

exemption for 2017 will be judged

according to their 2016 records).

February 2017

“the Italian BOFIP” definition of a “ voyage”

- what is the meaning of a “voyage “?

You mean all commercial navigations between

two Ports in national territorial waters, EU

waters or international waters where

embarkation and disembarkation of passengers

take place.

- what is the meaning of a “ qualified voyage in

high seas“ ?

You mean all commercial navigations between

Ports including international waters

February 2017

What about withholding tax

and corporate tax on

Charter Fees?

February 2017

Income Tax, clarification regarding the

term “Branch“A VAT registration in place in a EUCountry is not a proof of the presenceof a Branch and therefore of aPermanent establishment in theterritory

Ref: Art 11, EU Regulation no. 282 of

March 15th , 2011

February 2017

Income Tax: the Italian approachThe Business profit of a Non Resident entity is subject

to Italian Corporate Tax only if it has a “permanent

establishment” in Italy.

Ref. Article 23 of the Italian Tax Code

The definition of “Permanent establishment” (pursuant

to Art. 162 of the IT Tax Code) is the same as provided

in the aforementioned OCSE Convention e.g. a place of

management, a branch, an office .

Under IT Tax Circular 47/E dated 2005 Withholding tax

usually applied to incomes received by Non Resident

subjects (Art. 25 of the DPR 600/73 ) is not applicable

to Charter activity.

February 2017

I

Income Tax and Withholding Tax:

Conclusions If the Owning Company does not have a permanent

establishment in the Italian territory, including the

ownership of a berth in Italy, Income Tax and/or

any withholding tax are not due on the

income/profit from charter activities.

However:

To ensure IT Tax Authorities do not mistakenlyidentify a Non-Resident Company as ‘domestic’, weadvise to ensure that the place of effectivemanagement of the charter activities is basedoutside Italy

February 2017

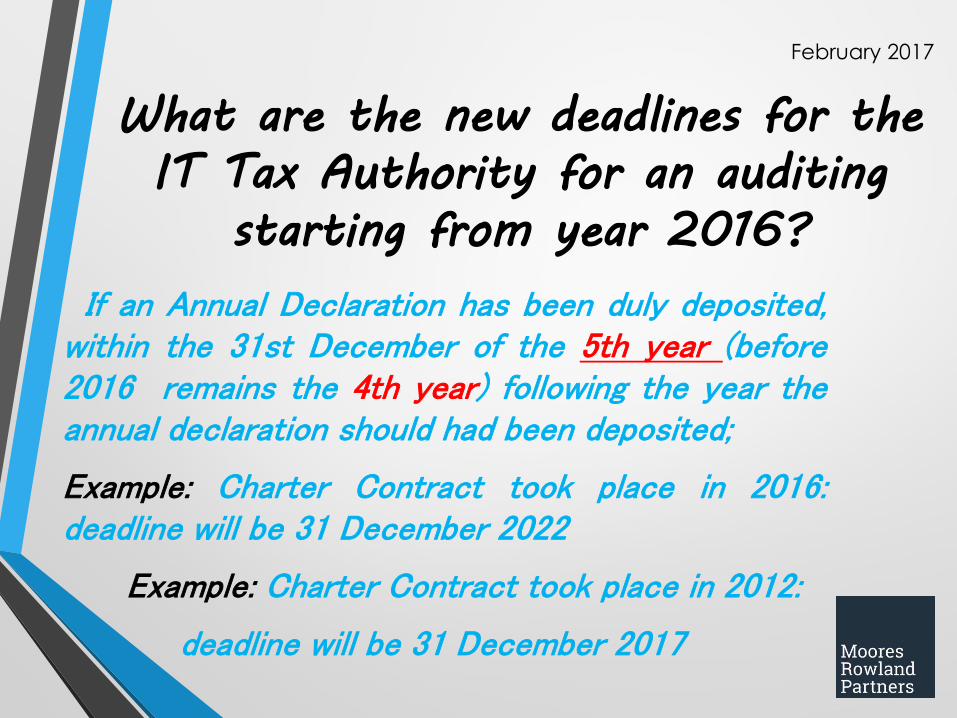

What are the new deadlines for the

IT Tax Authority for an auditing

starting from year 2016?

If an Annual Declaration has been duly deposited,within the 31st December of the 5th year (before2016 remains the 4th year) following the year theannual declaration should had been deposited;

Example: Charter Contract took place in 2016:deadline will be 31 December 2022

Example: Charter Contract took place in 2012:

deadline will be 31 December 2017

February 2017

Deadline for an Audit when the

VAT Annual Declaration has not been

duly deposited If an Annual Declaration has NOT been deposited, the

deadline is within the 31st December of the 7th year(before 2016 remains the 5th year) following the year theannual declaration should had been deposited;

Example: Charter Contract took place in 2016:

deadline will be 31 December 2024

Example: Charter Contract took place in 2011 : deadline will expire

on 31 December 2017.

February 2017

Deadline for an Audit when the

there is a

“complaint for tax offenses “ in

placeIn case the amount of the VAT not declared with an AnnualDeclaration is more than Euro 50.000 and the Tax Authoritysend a complaint for tax offenses to the Court and thedeadline previously indicated will double;

Example: Charter Contract took place in 2012 : if a Complaintfor Tax offenses was opened within 31 December 2018, thenew deadline for the Audit will be 31 December 2023

February 2017

THANK YOU!

For more information please contact

Ezio Vannucci

MOORES ROWLAND PARTNERS

T +39 0584 1667536

Email : [email protected]

February 2017