Presentation_on_companies_act2013 - K C Mehta

109

Com pani es Ac t 2013 Highlight s and Key Feat ures

Transcript of Presentation_on_companies_act2013 - K C Mehta

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 1/116

Companies Act 201Highl i ght s and Key Feat ures

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 2/116

ContentsIntroductionMajor ChangesNew types of companiesIncorporationManagement of companyBoard MeetingsCommittees of the BoardAccountsDividendAudit & AuditorsShare Capital and DebenturesRelated Party TransactionLoans and InvestmentDepositsWay Forward

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 3/116

Timeline

Companies

Bill 2011

Lok Sabha18 th Dec ‘12

Rajya Sabha8th Aug ‘13

Companies

Act 201329 Aug ‘13

• Rules

corresponding

to

the

above

sections

notified• E

-

forms

available

for

filing

from

28

th

April,

2014

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 4/116

Outline of the ActCompanies

Act 2013

Companies

Act 1956Companies Act 201• Concise• Forward looking• Subordination to Ru

• Uniformity• Easy navigation

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 5/116

• Less number of sections and more number of rules to enable

adaptation of changing economic technological environments• New types of companies defined

• E forms numbered with reference to chapter

• Meetings through video conferencing allowed

• Penalties for non compliance increased manifold

• Increased compliances for Private Limited Companies(Deposits, Loans, Meetings, etc.)

Key Highlights

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 6/116

Entity Structure in new ActEntity Structure in the new Act

Access tocapital

Listed

Unlisted

Members

OnePerson

Company

PrivateCompany

PublicCompany

Control

Holdingcompany

Subsidiarycompany

Associatecompany

Liability

Limited

Shares

Guarantee

Unlimited

Size

SmallCompany

Activity

DormantCompany

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 7/116

Major changes

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 8/116

• Private Company: Maximum no. of members = 200•

Public Company: Subsidiary of public company deemed to bepublic company• Associate Company: Company in which significant influence is

held (except subsidiary, includes joint venture)• Holding Subsidiary relationship: Control of > ½ of total share

capital• Subsidiary Company: Not permissible to have more than 2 layers

of investment subsidiaries. Following are the exceptions: – Acquisition of company incorporated outside India (having more than 2 layers) – Investment made to meet requirements of any law in force

Types of companies

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 9/116

• Books of Account: Allows maintenance of books of account inelectronic form

• Financial Statements: Defined as a compilation of following: – Balance Sheet – Profit and loss account – Cash Flow statement – Statement of changes in equity – Explanatory statement

• Financial Year: 1st April to 31 st March (Companies with holdingsubsidiary company outside India can make an application for change[Transitional Period: 2 years i.e. by 1 st April 2016]

Accounts

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 10/116

• Promoter: –

Shareholder / director having direct / indirect control – Company is accustomed to act on instructions (except prof. advise) – Person named as promoter in prospectus – First subscribers to memorandum

• Related Party: Scope of definition expanded (discussed later)

• ESOP: – Option to purchase shares at future date at predetermined price. – Can be given to directors / employees / officers of company / holding co. /

subsidiary co.

Management

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 11/116

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 12/116

New types of companies

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 13/116

One Person Company (OPC)• Only one member / shareholder

• Minimum of one director

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 14/116

• Only one person as member (except minors)

• Requires nominee (except minors)

• Only a natural person can form / nominate

• Can be incorporated only with 1 Director but can have upto 15 directors

• Member / nominee to be citizen & resident

• One Person can incorporate a single One Person Company and a Nominee can act as

such only in 1 OPC• Compulsory conversion to Pvt. / Public company on meeting certain criteria

• Cannot be formed / converted into Section 8 Company

• Cannot carry out NBFC activities

One Person Company (under Pvt. Co.)

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 15/116

• No requirement of holding AGM / EGM

•

Ordinary / special resolution need only be communicated bymember to company and entered in minutes book

• Where there is only one director, the resolution of Board meanscommunication by the director to the company and suchresolution shall be entered in the minutes book

• Need not annex cash flow statement to its financials• Annual return can be signed by only one person i.e. Company

secretary, and in absence of company secretary, by the directorof the company

Benefits / Relaxations

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 16/116

• Only one director needs to sign the financial statements

• Board’s report will only include the statement of director(s)on every qualification, reservation, adverse remark ordisclaimer by auditor(s)

• Financial statements to be filed with the Registrar within180 days of closure of financial year

• Board meetings: Only one in each half year and gap betweentwo meetings not to be less than 90 days. (Not applicable incase of one director)

Benefits / Relaxations (cont

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 17/116

Small Company• Private company

• Paid up share capital ≤ 50 lakhs, or

• Turnover ≤ 2 crores

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 18/116

• Meaning: – Paid up share capital ≤ 50 lakhs or – Turnover as per last P&L ≤ 2 crores

• Exclusions: – Holding company / subsidiary company

– Section 8 company (not for profit)

– Company / corporate governed by special Acts

Small Company (only for private company)

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 19/116

• Need not annex cash flow statement to its financials

• Annual return can be signed by only one person i.e.Company secretary, and in absence of companysecretary, by the director of the company

• Board meetings: Only one in each half year and gapbetween two meetings not less than 90 days

Benefits / Relaxations

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 20/116

Dormant Company• Companies meeting eligibility criteria can

make application for dormant status

• Inactive companies not filing financials andannual return for 2 years

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 21/116

• Eligibility: –

formed for a future project, or – to hold an asset / intellectual property – and has no significant accounting transaction

• Companies fulfilling the above criteria can make application

for change in status from “active” to “dormant”• Change of status by ROC: Where a company does not file annu

return / financial statements for 2 consecutive financial years,ROC can enter its name in Dormant Companies Register

Dormant company

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 22/116

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 23/116

Incorporation

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 24/116

• Forms of memorandum and articles for all types of

companies given as Schedules• Objects: (i) Main objects (ii) objects necessary for furtherance

of main objects

• Entrenchment: Articles may provide for additional restrictions

to make changes in Articles than that given by the Act

Memorandum & Articles

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 25/116

• ROC will carry out the following verification: – Trademark database – Existing similar name – Proposed name includes prohibited name (except where CG approval is

taken)

• If proposed name conforms with above disqualifications, namewill be rejected

• No automatic approval

• Approval valid for only 60 days; no extension possible

• No resubmission possible

Application for name

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 26/116

• In case place of registered office is not yet decided, facilityto provide for temporary address for communication (validfor 15 days from incorporation)

• Payment of amount subscribed to be made upon registration

• List of companies having same registered address to beprovided to ROC

• Interest of directors in other entities to be filed with ROC

• Additional procedural compliances required such as filing ofaffidavit etc

Changes in Incorporation Process

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 27/116

• No company with share capital can commence business

or borrow money unless: – A declaration has been filed with the Registrar that the

subscribers to memorandum have paid the necessary amount

– Registered office has been verified

• If no declaration is filed within 180 days ofincorporation, Registrar will initiate process for removalof name

Commencement of business

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 28/116

Every company shall:

• Paint / affix its name and address of registered office ateach office / branch / business location in local language

• Name / address of Reg. Office /CIN / tel. no. / fax / email /website on all business letters, billheads, letter papers,

notices, official publication• In case name has been changed, former name to appear in

all the above documents

Display of name, co. documents, etc.

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 29/116

Management of company[ Sec 149 , Sec 152 , Sec 196 t o Sec 205 ]

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 30/116

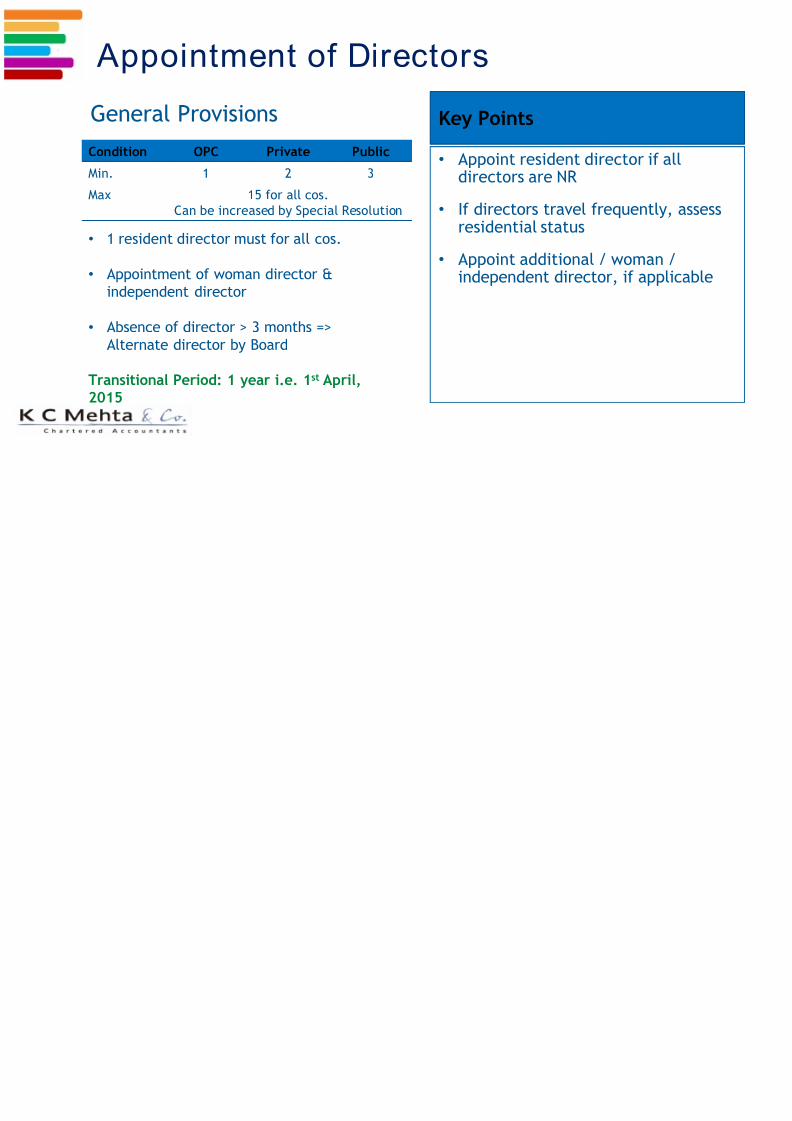

Appointment of Directors

General Provisions

Condition OPC Private PublicMin. 1 2 3

Max 15 for all cos.Can be increased by Special Resolution

Key Points

• Appoint resident director if directors are NR

• If directors travel frequentlyresidential status

• Appoint additional / woman

independent director, if appl

• 1 resident director must for all cos.

• Appointment of woman director &independent director

• Absence of director > 3 months =>Alternate director by Board

Transitional Period: 1 year i.e. 1 st April,2015

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 31/116

• Max. no. of directorships = 20 (not more than 10 public cos.)

• Register of directors to include details of KMP• Every change in director / KMP to be notified to ROC in DIR-12

• Absence from meetings for 12 months with / without leave ofabsence will vacate office

• Resigning director to intimate ROC within 30 days ofresignation along with reasons for resignation

Other provisions

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 32/116

Independent Director • Applicable to public companies

• Better governance

• Rotation after max. 2 terms of 5 years

• Cooling period of 3 years

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 33/116

Type of company Number of independent directors

Listed public company 1/3 rd of total number of director

Public companies meeting any of thefollowing criteria:– Paid up share capital ≥ 10 crores– Turnover ≥ 100 crores– Outstanding loans + deposits +

debentures ≥ 50 crores

2 (two)

Independent Director

Transitional Provision:Every company meeting the above criteria shall appoint such number of independent directorswithin one year of commencement. i.e. by 1 st April 2015.

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 34/116

• Director other than MD / WTD / nominee director, – person of integrity and posseses relevant expertise and experience – is / was not a promoter of the company / holding / subsidiary

company – not related to promoter / directors of company / holding /

subsidiary company – no pecuniary relationship with company / holding / subsidiary

company, or promoters / directors of above during immediatelypreceding 2 financial years

– no relative has pecuniary relationship with abovementioned partiesin excess of 2% of gross turnover or 50 lakhs rupees (lower of thetwo) during immediately preceding 2 financial years

Eligibility Criteria of Independent director

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 35/116

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 36/116

• Possessing skills / expertise / knowledge in any or more

of the below mentioned fields: – management, law, finance, sales, marketing, administration,

research, corporate governance

– technical operations / other disciplines related to company’sbusiness

Qualification requirement

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 37/116

• Clause 49 of Listing Agreement prescribes requirement

of appointment of independent director(s)• Different eligibility criteria in Listing Agreement and Act

• Till such time as SEBI / MCA comes out withclarification, companies will have to follow strictereligibility criteria

• Companies will have to reconsider their appointments inlight of new provisions of Companies Act 2013

Requirement of Listing Agreement

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 38/116

Woman DirectorsMandatory appointment by companiesmeeting specified criteria

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 39/116

Following companies are required to have at least one womandirector on its Board:

• Every listed company

• Every other public company having: – Paid up share capital ≥ 100 crores

– Turnover ≥ 300 crores

Appointment of woman director

Transitional Provision:Existing companies meeting above criteria shall fulfil requirementwithin 1 year i.e. by 1st April 2015

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 40/116

Key Managerial Personnel• Holds specified designations

• Stricter liabilities & responsibilities prescribed

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 41/116

Key Managerial Personnel

Meaning / Inclusions

• Defined to include CEO, MD,manager, CS, WTD, CFO

• Designations of CEO and CFOgiven recognition

• KMP included in the definitionof “officer”, “officer who is indefault” and “related party”

Key Points• Disclosure of interest by KMP

the same way as directors• Cannot enter into forward

contracts / carry on insidertrading

• Liabilities of officer / officer idefault to be applicable to KM

• KMP not to hold office in morthan one company. However, wBoard’s permission, can holdposition of director in anothercompany.

A i f KMP

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 42/116

• Applicability: – Listed Company – Public company: Paid up cap. > 10 crore

• Cos. fulfilling above criteria to have: – MD / CEO / Manager / WTD – CS – CFO

• Appointment of MD / CEO / chairperson to be authorized by articles (except incase of multiple businesses where each business can have a CEO)

• Authorization by articles required (except in case of multiple businesses whereeach business can have a CEO)

• Only Board resolution required except in case of a related party being appointedas such.

Appointment of KMP

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 43/116

• Functions: –

Compliance with Act / Rules – Reporting to Board

– Secretarial standard compliance

– Facilitate and attend BM / CM / GM & maintain minutes

– Obtain approval from Board / GM / Govt. to represent beforeregulators, discharge duties on behalf of company

– Assist board for conducting affairs, good corporate governance

Company Secretary

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 44/116

• Provisions for appointment of MD/WTD are applicable to Private Companiesalso.

• MD and manager cannot be appointment at a time• One Term limited to 5 years, maximum such terms not specified

• Reappointment possible only one year prior to end of term

• Board resolution & Special Resolution for appointment (mentioning terms ofappointment, remuneration, etc.)

• CG Approval where applicable

• Disqualifications: Min. & Max. Age: 21 and 70 years; Undischarged insolvent; Suspendedpayment to creditors / composition with them; Conviction of offence (sentence > 6m) at anytime

Appointment of MD / WTD

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 45/116

Remuneration

Remuneration to Other Directors

Where there is no MD / WTD = 3% Where there is a MD / WTD = 1%

Remuneration to a MD / WTD

Where there is only one MD / WTD = 5% Where there are more than one MD / WT10%

Remuneration Payable by Profit making public company

Total Remuneration = 11%

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 46/116

Inadequate profits: Profits which are not sufficient to pay the remuneration to the managerial persons as perthe employment contract with the managerial personnel and based on estimated profits.

Applicable to Private Companies also!!!

Higher of the two (A) or (B): (Requires ordinary resolution)

In the case of a managerial person who was not a shareholder (holding nominal value of Rs. 500,000),employee or a Director or a relative of a director or promoter of the Company at any time during the 2 yearsprior to his appointment as a managerial person, — 2.5% of the current relevant profit.

Special resolution: Limits get doubled. For more than double, CG approval required

Remuneration in case of inadequate profits

Where the Effective Capital (EC) is Yearly remuneration (

Negative or less than 5 Crores 30 Lakhs

5 Crores and above but less than 100 Crores 42 Lakhs

100 Crores ad above but less than 250 Crores 60 Lakhs

250 Crores and above 60 Lakhs plus 0.01% of the EC in excess of R

A

B

f d f

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 47/116

• Conditions: –

Resolution in general meeting as required (notice to containdetails as per Rules)

– Approval of Board / NRC

– No default in repayment of debts / deposits / debentures forcontinuous period of 30 days in previous FY

– Special resolution for a period not exceeding 3 years has beenpassed

Remuneration in case of inadequate profits

N CG A l f

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 48/116

• Unlisted public cos. and private cos. (above conditions to be fulfilled)

• Remuneration paid by either foreign co. or Indian co. with shareholdersapproval

• Remuneration 2 times the amount stated: – Newly incorporated co. (7 years) : remuneration 2 times the amount stated

– 5 years from sanction of scheme of revival (BIFR / NCLT)

• Limits sanctioned by BIFR / NCLT in excess of mentioned in table + co. is regular in

payment to creditors / depositors + Certified by CS / Auditor / PCS as applicable• In case of a company in a SEZ: An amount up to Rs. 2.40 Crores PA (should not have

raised money from public, no default in repayment of debts for continuous period of 30days in previous FY)

No CG Approval for

Di l f ti

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 49/116

• Listed Companies: – Board’s report: Ratio of remuneration of each director to median of employees

remuneration, other details as per Rules – Name of every employee

• Employed throughout the whole FY• Employed for a part of year but drawing remuneration > Rs. 5 Lacs p.m.• Employed throughout or for a part of year but was drawing remuneration at a > MD /

/ manager and holds > 2% shares (himself / spouse / dependent children)

– Employees deputed outside India (not directors / relatives) and drawing aremuneration of Rs. 60 Lacs p a or Rs. 5 Lacs p m: Circulated to members in theBoard’s report and filed with the ROC along with the financials and Board’s Repo

– All appointments of KMP to be intimated to ROC within 30 days

Disclosure for remuneration

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 50/116

Board Meetings[ Sec. 110 , Sec. 173 t o Sec. 175 & Sec. 179 t oSec. 18 4]

Board Meetings

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 51/116

• First Board Meeting within 30 days of incorporation• Min. 4 BM in a year (gap < 120 days)• Notice of 7 days. (Shorter notice requires presence of

independent director at the meeting)• Quorum: 1/3 rd of total directors or 2, whichever is higher•

In case of circular resolution: Notice to be sent to alldirectors with draft resolution, approval of majorityrequired

• Circular resolution to be noted in general meeting

Board Meetings

Video conferencing

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 52/116

• Board meetings through video conferencing allowed

• Record & storage must, for recognition of participation

• Chairperson / CS to ensure proper security / availability of equipment forrecording & identification

• Director willing to attend by video conferencing during the year to intimateBoard in beginning of each calendar year

• No video conferencing for following: – Approval of Financial Statement & Board’s Report – Approval of prospectus – Audit committee for consideration of accounts – Approval for amalgamation / merger / demerger / acquisition / takeovers

Video conferencing

Matters to be considered at BM

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 53/116

• Securities – Make calls on amount unpaid on shares, authorize buy-back, issue securities within / ou

India• Funds:

– Borrow money, grant loans / guarantee / security, invest funds, political contributions – Buy / sell investments (other than trade investments) > 5% of paid up cap. & free reserv – Invite / accept / renew public deposits, change of terms

• Re-organization: Diversify business, amalgamation, merger, reconstruction, takeover•

KMP & their team, Directors: – Appointment, note of changes in level below KMP, – Note disclosure of directors interest / shareholding

• Appoint internal & secretarial auditors• Approve quarterly, half yearly, annual financial statements / reports

Matters to be considered at BM

Matters not to be considered at BM

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 54/116

• Matters requiring special resolution in GM –

Sell / dispose off whole / substantially whole undertaking – Invest compensation of amalgamation / merger (except trust

securities)

– Borrow money, after which total borrowings will exceed paidup cap. & free reserves (excludes temporary loans)

– Remit / give time for repayment of loans due by director

• All matters applicable to private company also

Matters not to be considered at BM

Matters requiring Postal Ballot

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 55/116

• Matters to be considered only through postal ballot (only public companies) – alteration of Object clause, –

alteration of AOA – specifically relating to registered office, – change in registered office outside local limits, – issue of shares with differential rights, – change in objects for which company has raised money but it is still unutilized, – variation in rights of class of shares or debentures, – buy-back of shares, – election of director u/s 151, – sale of an undertaking, – giving loans / guarantee / security in excess of limits specified u/s 186 or – Where any businesses in respect of which Directors or Auditors have a right to be

heard at the meeting.

Matters requiring Postal Ballot

Directors interest and register

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 56/116

Directors interest and register

• Contracts > Rs. 500,000 to be entered in Register

• Director / KMP to disclose interest in Form MBP-1 within 30 days of appointment relinquishment

• Director to give notice of interest in his first BM as director and every first BM of fyear and notify change in BM after every change

Entity Type of interest to be disclosed by director / KMP (not toparticipate in Board Meeting)

Body Corporate Director either:•

holds > 2% shareholding (incl. in association with any perso• Is a promoter• Is manager / CEO

Other than body corporate Director is a partner / owner / member

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 57/116

Committees of Board[ Sec. 17 7 a nd Sec. 17 8]

Audit Committee

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 58/116

• Applicability: – Listed Company; – Public Company: Paid up cap ≥ 10 crores, turnover ≥ 100 crores, o/s borrowings ≥ 50 cr

• Composition and Conduct: – At least 3 directors (majority independent directors) – Almost all directors should be capable to understand financials – Auditor to be present when financials are being considered – Scope includes: review of auditor’s independence, performance, remuneration, matters

concerning financials – Deleted from CA 1956: Compulsory half yearly review of financials; Compulsory

attendance of chairman to general meeting

• Transit period : 1 year• Composition & Recommendations to be part of Boards report along with

reasons

Nomination & Remuneration Committee

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 59/116

• Applicability: – Listed Company; – Public Company: Paid up cap ≥ 10 crores, turnover ≥ 100 crores, o/s

borrowings ≥ 50 crores

• Composition & Conduct: – Min. 3 non-exec. Directors (majority independent directors) – Chairperson of company can be member but not chairperson of

committee – Role: Policy for qualification & appointment of Board & independent

directors, remuneration of directors/ KMP / employees – Policy to be disclosed in Board’s report

Nomination & Remuneration Committee

Stakeholders Relationship Committee

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 60/116

• Applicability: – All Companies having more than 1000 shareholders

• Composition & Conduct: – Non-executive Chairperson

– Members to be decided by Board

– Role: Solve grievance of stakeholders / members – Chairperson (or member authorized) to attend general

meeting

Stakeholders Relationship Committee

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 61/116

Accounts[ Sec. 123 t o Sec. 148]

Maintenance of records

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 62/116

Maintenance of records

Provisions• Books to be kept at registered office

including for branch office• May keep books at other place after

resolution in Board Meeting• Accrual basis• Electronic mode of book-keeping

recognized• Open for inspection• Maintenance for 8 financial years

(excluding current FY) includingvouchers… unless investigation isordered

Key Points•

Can maintain electronic records• Retain books for 8 years

• Pass Board resolution if books arkept at a place other thanRegistered Office

Books of branch office

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 63/116

Books of branch office

Provisions•

To be kept at registered office• May be kept at other place if

resolution passed at BoardMeeting

• In case of branch outside India,

periodic returns to be sent toIndia and kept at Registeredoffice or other place asmentioned above

Key Points•

Instead of sending returns aevery 3 months, periodicreturns should be sent.(reasonable judgment to beapplied)

• Open for inspection.

Financial Statements

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 64/116

Provisions• Comply with prescribed accounting

standards

• Shall be laid before AGM

• Consolidated financials must for everycompany (Subsidiary includes associate andjoint venture)

• Salient features (notes) for each subsidiaryalso to be attached

• Deviation from accounting standards to begiven in notes along with explanations

• To be signed by chairperson of the companyor by 2 directors (MD and CEO, if director),CFO and CS

Key Points• Increased costs and compliance

• Multiple compliances: consolidfinancials, notes

• Conflicting definitions of assoc joint venture , etc. in CompanAccounting standards to pose ducompliances until NFRA prescraccounting standards / comes ouclarification.

• Signatures as per Act, annex audreport to financial statements

Director’s Responsibility Statement

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 65/116

• Additional responsibilities for directors – In case of listed companies

• internal financial controls followed by the company are adequate andwere operating efficiently

– Devising proper systems ensuring compliance with allapplicable laws

•

Systems shall be adequate and operating efficiently

p y

Director ’s Responsibility Statement

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 66/116

• Internal financial controls shall mean – Policies and procedures adopted by company for ensuring

• the orderly and efficient conduct of business• Adherence to company’s policies• Safeguarding of its assets• Prevention and detection of frauds and errors•

Accuracy and completeness of accounting records• Timely preparation of reliable financial information

p y

Board’s Report

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 67/116

Additional disclosures in the Board’s report with respect to

• Financials – Extract of Annual Return – Financial highlights – Adequacy of internal financial controls with respect to financials – Particulars of loans and investments u/s 186, contracts with related parties u/s

188 –

CSR policy and responsibilities taken• Board

– Number of meetings of the Board – Independent director’s declaration

p

Board’s Report (cont

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 68/116

– Company’s policy on appointment and remuneration in case it has NRC – Annual evaluation of the performance of the Board, its committees and

individual directors – Details of directors and KMPs appointed or resigned during the year

• Others – Explanation and comments on qualification, reservation of CS – Risk management policy of the company

– Change in nature of business – Companies ceased to be subsidiaries, associates or JVs with reasons thereof – Deposits accepted, remained unpaid and the reason for default – Orders if any passed by the regulators

p (

Re-opening & revision of accounts

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 69/116

Re-opening & Recasting• Conditions:

–

Fraudulent accounts – Mismanaged affairs

• Application by: – Central Govt. – Income Tax Authorities – SEBI, etc

• Implication: – Tribunal may order re-opening of

accounts

Revision• Conditions: Financial statemen

Board’s report do not comply with

provisions of governing sections• Application by: Director(s)

• Period: Any of the three (3) precfinancial years (only once in finanyear)

• Implication: – Tribunal may order re-casting

accounts – Detailed reasons for revisions

given in Board’s report

Corporate Social Responsibility

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 70/116

• Applicability – Any Company with net worth of 500 Crores or more, T/O of 1000 Crores or more, or Net Pr

of 5 Crores or more.•

Composition and Conduct of committee – It shall consist of at least three or more directors of which at least one shall be an

independent director – The Committee shall formulate and recommend to the Board, a Corporate Social Responsibi

Policy containing the details of activities to be undertaken and should also recommend theamount of expenditure to be incurred.

– The company shall spend 2% of its avg. net profits of the immediate preceding 3 FYs on CSactivities during the year.

• Preference to be given to local area and areas around which it operates forspending towards CSR

• Company can also undertake such activities through a registered Trust or society orSec 8 company etc.

• Reasons for not spending amount to be mentioned in Board’s Report

Penalties

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 71/116

Violation of Responsibility Minimum fine Maximum FinePreparation of books orfinancial statements

Company and KMPcharged withresponsibility of

this compliance

For both :Rs. 50,000

For company :Rs. 500,000For KMP :

Rs. 500,000Imprisonment of 1Or both

Approval of financialstatement by Boardand Board’s Report

Company andofficer

For both :Rs. 50,000

For company :Rs. 25,00,000For officer :Rs. 500,000Imprisonment of 3

Annual filing Company andofficer

For Company :Rs. 1000 per dayFor officer :Rs.100,000

For company :Rs. 10,00,000For officer :Rs. 5,00,000Imprisonment of 6

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 72/116

Schedules relating toaccounts

Depreciation

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 73/116

• Applicable from FY 2014-15

• Useful life and rates of depreciation prescribed for different assets

• Residual value not to be > 5%

• No different rates for shift working. 2 shift: add 50%, 3 shift: add 100% ofdepreciation

• Depreciation on intangibles to be governed by Accounting Standards

• If any part of asset significant to total cost has a different useful life, useful life ofsuch part shall be determined separately

• Disclosure – depreciation methods used and useful lives considered if they aredifferent from those specified

Transitional Provision:• Carrying amount to be depreciated as per Schedule II• If remaining useful life is NIL, carrying amount to be transferred to retained earnings

Depreciation – current rates

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 74/116

NATURE OF ASSETSSchedule XIV

W.D.V(%)

S.L.M(%) Useful Lif

Buildings (other than factory buildings) 5.00 1.63 58

Factory Building 10.00 3.34 28

Motor-cars 25.89 9.5 10

Furniture & Fitting 18.10 6.33 15

Data Processing Machines including computers 40.00 16.21 6

Plant and Machinery; other than continuous processplant for which no special rate has been prescribed

13.91 4.75 20

Plant and Machinery; continuous process plant, otherthan those for which no special rate has beenprescribed

15.33 5.28 18

Instructions to prepare BS / PL

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 75/116

• Accounting Standards (AS) to be followed

• Disclosure requirements in Act in addition to AS

• Rounding off as follows:

• Format similar to Schedule VI of CA 1956 (revised)

• Additional information in case of consolidation prescribed

Turnover Rounding off

Less than 100 crores Nearest hundreds, thousands, lakhs or millions

100 crores or more Nearest lakhs, millions or crores

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 76/116

Dividends

Dividends

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 77/116

• Sources of dividends: – Profit for the year (after dep.) – Undistributed profits (after dep.) – Money granted by CG / SG for declaration of dividend

• Transfer to general reserve not mandatory as in CA 1956

• Declaration only out of free reserves

• Inadequacy of profits(out of accumulated reserves): –

Rate of dividend not more than last 3 yrs avg. rate (no dividend in last 3 years, no limitsapplicable) – Total amount drawn from reserves not more than 1/10 th of paid up cap & free res – Amount drawn to be set off against losses in the current year before declaration – Balance of reserves not to fall below 15% of paid up capital

Dividends (cont

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 78/116

• Interim dividend: – Out of surplus profits of current year

– In case of loss, the conditions of “inadequacy of profits” to apply

• Amount declared to be transferred to separate accountwithin 5 days

•

Payment in electronic mode recognised• Companies with default in deposit acceptance / repayment

cannot declare dividend

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 79/116

Appointment of Auditors - Internal

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 80/116

• All listed cos. and public cos. with – paid up capital Rs. 50 Crores or more, –

T/O Rs. 200 Crores or more, – O/s loans and borrowings Rs. 100 Crores or more, or – O/s deposits of Rs. 25 Crores or more

• Shall appoint an Internal Auditor

• Who can be a CA, CWA, or such professional decided by the Board who

may or may not be an employee of the company• Transit period for existing companies is 6 months from the

commencement of Sec. 138 of the Act. i.e., by 30 th September, 20

Appointment of Auditors - Statutory

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 81/116

• First appointment for 5 years at the first AGM

• Rotation Applicability (other than listed):

• Rotation period:

• No audit firm having a common partner to other audit firm shall be appointed as anauditor during the cooling period of the company

• Transit Period: 3 years

Company Paid up capital BorrowingsPublic 10 Crore 50 crore

Private 20 crore 50 crore

Auditor type No. of Years Cooling Period

Individual 1 term of 5 years 5 years

Firm 2 terms of 5 years (10 years) 5 years

Cost Audit

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 82/116

• Applicable to all companies (including foreign companies) – Engaged in strategic sector – Industry regulated by a Sectoral regulator or ministry or department of CG – Other specified companies (railways, base metals, minerals, fuels (organic / inorganic) – Providers of health care and educational (including philantrophy) services – Net worth > Rs. 5 Crores – T/O > Rs. 20 Crores

• Cost Auditor (CWA) & statutory auditor cannot be same, all qualifications / disqualificationapply mutatis mutandis

• Cost Auditor to be appointed by Board and Report to be submitted to the Board only• Copy of report to be furnished to CG within 30 days with explanation on every reservation

qualification• Provisions of punishment for contravention apply to cost audit / auditor also

Eligibility, qualifications, disqualifications

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 83/116

• List of disqualifications now include criteria based onrelatives also

• Following non-audit services attract disqualifications: – Accounting and book keeping services – Internal audit – Design and implementation of financial information system – Actuarial services – Investment advisory services – Outsourced financial services – Management services

Additional reporting responsibility

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 84/116

• Details of issues where company has failed to provide information and explanation

• Observation on financial transactions / matters having adverse effect on

functioning of company• Qualification, reservation or adverse remark relating to maintenance of accounts

• Comment on adequacy of internal financial controls and its effectiveness

• Impact of pending litigations on financial statements

• Provision on material foreseeable losses on long term contracts

• Fraud reporting to Central government

• Transfer to IEPF

Penalties

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 85/116

Violation of Responsibility Minimum fine Maximum Fine

Duties of auditors CA / CS / CWA,as applicable

Rs. 1 lakh Rs. 25 lakhs

Appointment,eligibility,remuneration,duties, etc. withrespect to statutoryauditors or costauditors

Company,officer andauditor

For company :Rs. 25,000For officer :Rs. 10,000For auditor :Rs. 25,000

For company :Rs. 5 lakhFor officer :Rs. 1 lakh or 1 yr.imprisonment or botFor auditor :Rs. 1 lakh

Secretarial Audit

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 86/116

• Applicability – All listed cos. and public cos. with capital more than Rs. 50 Cr., T/O

more than Rs. 250 Cr. shall have a secretarial audit conducted

• Compliance – The audit shall be conducted by a PCS

– The report of the same shall be annexed to the Board’s Report

– The Board of Directors, in their Report, shall explain in full, anyqualification or observation or other remarks made by the PCS in itsAudit Report

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 87/116

Share capital & Debentures[ Sec. 4 2, Sec. 4 3, Sec. 4 7, Sec. 4 8 a nd Sec. 6 2]

Raising capital

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 88/116

• New company cannot commence business until confirmationhas been given regarding receipt of subscription money

• Share certificates to be issued within 2 months ofincorporation, within 1 month of transfer / transmission

• Certificate to be issued within 3 months of allotment ofdebentures

• Shares, other than sweat equity, cannot be issued at adiscount.

• Shares with differential rights will not exceed 26% of thetotal Post issue Paid up capital of the company.

• All offer to subscribe / allotment of shares otherwise than by

Private Placement

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 89/116

All offer to subscribe / allotment of shares otherwise than bypublic offer means private placement

• Applicable to both private & public companies & for all securities• Offer to not more than 50 persons at one point in time 200

persons in one year (excl. ESOP / QII)• Should be within Rs. 20,000 per person (face value)• Approval by special resolution for making offer• Person to whom the offer is made shall make the payment (only

bank account of offeree) (No cash payment allowed)• No further offer of shares unless allotment for previous offers

have been completed• Allotment within 60 days of receipt of application money (details

to be filed with ROC)

I l d i h f ll / l ibl d b h ibl

Preferential Allotment

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 90/116

• Includes equity shares, fully / partly convertible debentures, other convertiblesecurities

• To be approved by Articles & Special Resolution

• Detailed notice of meeting giving particulars of persons to whom offered, pre& post issue holding of promoter group, value, etc.

• It may / may not include existing shareholders or employees

• Consideration in cash / other than cash (fully paid at allotment)

•

Valuation to be done by registered valuer (except listed co.)• Conditions of private placement to apply

• To be completed within 12 months of passing special resolution

Preference shares

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 91/116

• Special Resolution for issue

• Further issue in case the company is not in a position topay dividend / redeem earlier shares to be consented by3/4 th preference capital holders and Tribunal

• No subsisting default in dividend payment / redemptionat the time of issue of further issue

• Redemption – to be done within 20 years

Voting rights

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 92/116

• Preference shareholders can vote on reduction /repayment of equity / pref. capital; matters affecting

pref. capital• In case of unpaid preference dividend for 2 years,

holders can vote on all resolutions placed before themeeting

• Proportion of voting rights in ratio of paid up capital

• Only sweat equity shares can be issued at discount

Sweat Equity Shares

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 93/116

Only sweat equity shares can be issued at discount

• Sweat equity can be issued to employees of subsidiary / holding company

•

Approval by special resolution in case of unlisted companies issuing shares todirectors / employees for providing intellectual property / knowhow

• Sweat equity capital not to exceed 25% of paid up cap.

• Value at which shares shall be issued to be carried out by Registered Valuer

• Valuation of intellectual property / knowhow to be carried out by Registered

Valuer• Disclosure in board’s report in the year of issue of sweat equity shares

• Bonus shares can be issued out of:

Bonus Shares

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 94/116

Bonus shares can be issued out of: – Free reserves

–

Securities premium account – Capital redemption reserve

• Conditions: – Authorised by articles & approval in general meeting

–

No default in repayment of deposits / debt securities – No default in payment of PF / gratuity / bonus for employees

– Outstanding partly paid up shares to be made fully paid up

– No bonus in lieu of dividend

ESOP (for unlisted & pvt. co.)

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 95/116

Can be issued to• Permanent employee in India /

outside India• Director (excl. Independent director)

• Employee / director of holding /subsidiary / associate (excl.independent director), does notinclude

– Promoter group – Director (along with relatives)

holding > 10% of existing equitycapital

Conditions• Approved by special resolution• Separate resolution in case of gran

option to employee of holding /subsidiary / associate; or in case gof option to identified employees of existing paid up cap

• Minimum 1 year between grant anvesting of option

• No voting / dividend rights until exercised• Non transferable (except legal hei• Disclosure in Board’s Report

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 96/116

Related Party Transaction

[ Sec. 2(7 6) and Sec. 188 ]

Related PartyHolding

company

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 97/116

p y

Director / KMP / relative

Co-subsidiaryCompany

SubsidiaryAssociateDirector /Manager /relatives

Firm Pvt. Co. Publiccompany

Other KMP /relatives

Accustomed to a

Director /manager /

relatives arepartner(s)

Director /manager isdirector /member

Director /manager isdirector / 2%holder of eq.shares

• Sale / purchase / supply of goods/material

Related Party Transaction

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 98/116

Sale / purchase / supply of goods/material

• selling / disposing / buying of property of any kind

• leasing of property• availing / rendering of services

• appointment of any agent for purchase or sale of goods, material,services or property

• appointment to any office or place of profit in the company, subsor associate

• underwriting the subscription of any securities or derivatives thereof

• The transaction should be entered in normal course of business and at arms length

Conditions

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 99/116

g• In case of transactions not at arms length, Board’s approval will be required• In following cases, special resolution in members meeting is required:

– Paid up cap. > 10 crores – Sale / purchase (incl. through agents) > 25% of annual turnover – Selling / disposing / buying property (incl. through agents) > 10% of net worth – Leasing of property > 10% of net worth – Availing / rendering services (incl. through agents) > 10% of net worth – Appointment at place of profit in co. / subsidiary / associate > 2.5 lakhs remuneration – Underwriting remuneration > 1% of net worth

• Interested member not to vote at such meeting• For all the transactions, the approval of Audit Committee is a must• All related party transaction to appear in Board’s meeting

• Full disclosure along with justification to be given in

Compliances

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 100/116

Full disclosure along with justification to be given inBoards report

• Ratification by Board in case previous approval nottaken (ratification by shareholders after 3 m)

• Heavy penalties including disqualification to beappointed elsewhere if convicted for offence for relatedparty transaction

• In case of violation of the provisions of this section:

Penalties

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 101/116

In case of violation of the provisions of this section:

• In case of a listed Company : punishable withimprisonment upto 1 year or with fine < Rs. 25,000/- >Rs. 5,00,000 or both.

• In case of any other Company : fine < 25,000/- >5,00,000/-

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 102/116

Loans & Investment[ Sec. 18 5 & Sec. 18 6]

• No loan (including loan represented by book debt) / guaran

Loans to Directors

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 103/116

No loan (including loan represented by book debt) / guaransecurity to directors (or person in whom director is interestedexcept:

– MD / WTD as a part of service condition

– Pursuant to scheme approved by members

– Cos. in business of granting loans (ROI ≥ RBI rate)

– Loan / guarantee / security to subsidiary against own loan / bank loan / FI

loan (amounts to be utilized for principal business activity)

• Applicable to directors of private companies also

Person in whom director is interestedDirector of holding

(i l P /

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 104/116

DirectorFellow Director(s)

company (incl. Partner /Relative)

Relative

Partner of firm

Firm in whichpartner

Pvtdirec

BodyCorporate

BOD / MD / manageraccustomed to Act oninstruction of Board /Director

Individually / together,controls 25% voting

power

Back

• In case of violation of the provisions of this section:

Penalties

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 105/116

In case of violation of the provisions of this section:

• Company shall be punishable with a fine < Rs.5,00,000/- > Rs. 25,00,000 .

• Director or other person to whom loan is advanced:Imprisonment which may extend to 6 months or withfine < 5,00,000/- > 25,00,000/- or with both.

• Total Loans / guarantees / security and Investments should not be more thanhigher of:

Other loans & investments

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 106/116

– 60% of its paid up capital, free reserves and securities premium account or – one hundred percent of its free reserves and securities premium account

• For loans / guarantee / security / investment more than above limits: (ExceptHolding to Wholly owned Subsidiary)

– Special Resolution mentioning total amount that can be granted (incl. currentlevels)

– Approval from PFI from whom loans are taken• Restrictions on investments:

–

Max. 2 layers of subsidiaries, except:• Acquisition of a company outside India (which has more than 2 layers of

investment subsidiaries), or• required to keep an investment subsidiary by any other law

• Restrictions on loans / guarantees / security and investments:

Other loans and investments

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 107/116

– Companies registered under SEBI Act to adhere to limits of loans prescribed bySEBI

– Default in payment of interest / principal for deposits: Cannot give loans /guarantee / security / takeover until default is made good

• The provisions of this section are made applicable to a private company also.• Other conditions:

– Rate of Interest not to be lower than govt. security close to loan tenor

– Disclosure of all loans & investments & their purpose in financial statements – If securities are not in name of company, maintain a special register

• Provisions not applicable to:

Other loans and investments

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 108/116

– Allotment of shares in pursuance of further issue of capital – Banking / Insurance / housing co. in business of loans / investments – Cos. in business of financing / infrastructural facilities – NBFC (for inv. / lending) or co. in business of acquisition of securities

• In case of contravention of these provisions:

Penalties

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 109/116

p

• Company shall be punishable with a fine < Rs. 25,000/-> Rs. 5,00,000

• Officer in default : Imprisonment which may extend to 2years or with fine < 25,000/- > 1,00,000/-

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 110/116

Deposits[ Sec. 73 t o Sec. 76]

Meaning - Includes receipt of money by way of deposit / loan

Deposits

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 111/116

/ any other form but excludes receipts from: – Banks and govt. authorities – Foreign parties (incl. banks and govt. authorities) – Other companies – For issue of securities – Directors [Declaration to be obtained that deposits are not placed

out of borrowings] – Non-interest security deposit from employee – Business purpose

Sr. No Particulars Eligible Companies Other Companies

Public Co with NW> 100 Crores or Companies other than Eligible

Eligible Companies and Others

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 112/116

1 Coverage Public Co. with NW> 100 Crores orT/O > 500 Crores

Companies other than EligibleCompanies

2 Can Accept

deposits fromPublic and Members Members Only

3LimitsApplicable*

10% for Members, 25% for Public &35% in special cases**

25%

4Repayment ofexistingdeposits

Not Necessary to repay subject tocertain conditions

Compulsory repayment within onfrom the commencement of this A

5Conditions foracceptingdeposits

Same for both the cases

*Limits are applicable to the aggregate of paid up capital and free reserves of the company**35% is applicable in case the company is a government company, the other limits areapplicable for all eligible companies other than government companies

Conditions for accepting deposits• Issue Circular to members / public and file such circular with ROC where circular:

T di l fi i l d il di i d il f d i d i i d

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 113/116

– To disclose financial details, credit rating, details of depositors and existing duedeposits of the company

–

Can be circulated by way of advertisement in newspapers also – A copy signed by majority of directors to be filed with the ROC 30 days before such

advertisement – To be valid only for 6 months from the close of FY or until the presentation of

financials in the AGM• Deposit Repayment Reserve:

– Minimum sum of 15% of amt. of deposits maturing during FY and next FY in a separatbank account

• Deposit Insurance: – Cos. to acquire deposit insurance 30 days before issue of advt. / date of renewal

(insurance on principal + interest)

• Charge on assets : – In case of secured deposits, charge to be created on assets other than intangibles

Conditions for accepting deposits (con

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 114/116

p , g g – Security by way of insurance / charge / both ≥ deposit + interest –

Register of deposits to be maintain as per Rules• Rate of interest / brokerage :

– Rate of interest / brokerage <= max. rate prescribed by RBI for acceptance ofdeposits by NBFC

– Currently, max. int. rate = 12.5%, –

max. brokerage rate = 0.5%• Period of deposits repayable on demand :

– 6 m to 36 m (except if < 10% of paid up capital + free reserves), and repayable notbefore 3 m

• Existing Deposits unpaid on or becoming due after thet f thi A t

Deposits existing prior to this Act

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 115/116

commencement of this Act – File their details with ROC within 3 months from the

commencement of the Act i.e., 30 th June 2014 under Form DPT – Return of Deposits under Form DPT-3 to be filed on 30 th June

every year is different from this statement – Repay within 1 year of commencement (01/04/2015) or due date,

whichever is earlier

• For Eligible Companies – if the re-payments of deposits tilldate are made on time and terms and conditions are in linewith CA 1956, no repayment under this Act is required

Milin MehtaPartner

Office: +91 265 3086 401Mobile: +91 98240 00926Email: [email protected]

Darshana MankadPartner

Office: +91 265 3086 412Mobile: +91 98244 53635Email: [email protected]

D i R St ti T i di

Vishal DoshiPartner

Office: +91 265 Mobile: +91 9824Email: vishal.

7/21/2019 Presentation_on_companies_act2013 - K C Mehta

http://slidepdf.com/reader/full/presentationoncompaniesact2013-k-c-mehta 116/116

Dayavanti RanaManager

Office: +91 265 3086 456Mobile: +91 94262 10614Email: [email protected]

Stuti TrivediAssistant Manager

Office: +91 79 4032 6400Mobile: +91 99982 40000Email: [email protected]