Presentation to the Treasury Borrowing Advisory Committee · Presentation to the Treasury Borrowing...

64

Presentation to the Treasury Borrowing Advisory Committee U.S. Department of the Treasury Offi f D bt M t Office of Debt Management February 2, 2010

Transcript of Presentation to the Treasury Borrowing Advisory Committee · Presentation to the Treasury Borrowing...

Presentation to the Treasury Borrowing Advisory Committee

U.S. Department of the TreasuryOffi f D bt M tOffice of Debt Management

February 2, 2010

Federal Budget Deficits Year-to-Date

-1 413

600%-1,600

$ Billions

2008 Y-O-Y % Change

-1,086

-1,267

-1,3781,413

400%

500%-1,400

-1,200

20102009

-765

-957

-802

-992

200%

300%

-1,000

-800

-263-311 -319 269

-371

-483 -455

-402

-485

-569

-176-297

-389 100%

200%

-600

-400

-56-154

-106 -88

263

-152-269 -237

-100%

0%-200

0

7 7 7 8 8 8 8 8 8 8 8 8 8 8 8 9 9 9 9 9 9 9 9 9 9 9 9

Office of Debt Management2

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Federal Cash Outlays Year-to-Date

01-Oct 15-Nov 31-Dec 15-Feb 1-Apr 17-May 2-Jul 16-Aug

FY07 FY08 FY09 FY10

-1,000

-500

-1,500

Bill

ion

2 500

-2,000

$

-3,000

-2,500

Office of Debt Management3

-3,500

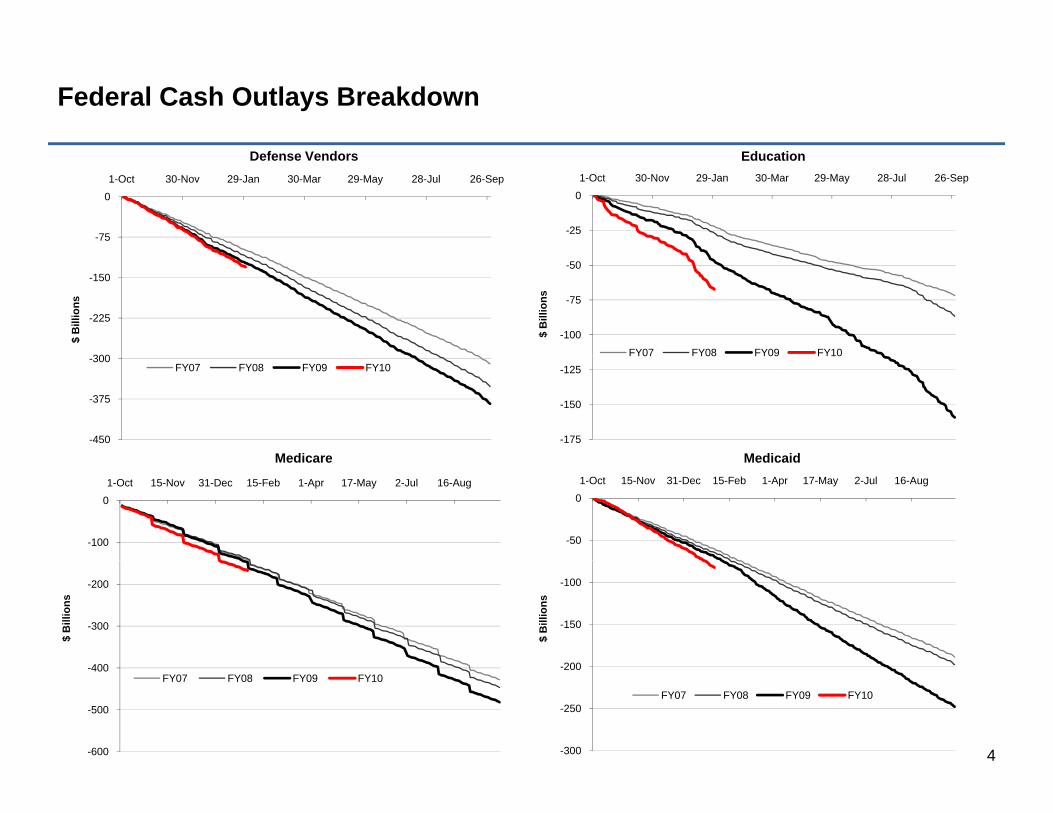

Federal Cash Outlays Breakdown

-75

01-Oct 30-Nov 29-Jan 30-Mar 29-May 28-Jul 26-Sep

Defense Vendors

-25

01-Oct 30-Nov 29-Jan 30-Mar 29-May 28-Jul 26-Sep

Education

300

-225

-150

$ B

illio

ns

-100

-75

-50

$ B

illio

ns

FY07 FY08 FY09 FY10

-450

-375

-300FY07 FY08 FY09 FY10

-175

-150

-125FY07 FY08 FY09 FY10

Medicare Medicaid

-100

01-Oct 15-Nov 31-Dec 15-Feb 1-Apr 17-May 2-Jul 16-Aug

Medicare

-50

01-Oct 15-Nov 31-Dec 15-Feb 1-Apr 17-May 2-Jul 16-Aug

Medicaid

-300

-200

$ B

illio

ns

200

-150

-100

$ B

illio

ns

Office of Debt Management4-600

-500

-400FY07 FY08 FY09 FY10

-300

-250

-200

FY07 FY08 FY09 FY10

Obligations and Cash Outlays for the Recovery Act

300

350

Obligations Outlays

Cash outlays are lagging obligations by $160 bn.

250

150

200

Bill

ions

100

0

50

Office of Debt Management5

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Source: Agency Reported Data for Contracts, Grants, Loans, and Entitlements Federal Recovery Accountability & Transparency Board / Haver

TARP Outflows and Inflows

400

500

100

125Repayments, Dividends, Interest (LHS)Cash Outflows (LHS)Cumulative Net Cash Flow (RHS)

$Billions $Billions

200

300

50

75

Cumulative Net Cash Flow (RHS)

0

100

0

25

-200

-100

-50

-25

-400

-300

-100

-75

Office of Debt Management6

-500-125Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 Mar-09 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09

Federal Cash Receipts Year-to-Date

2,500

FY07 FY08 FY09 FY10

2,000

1,500

$ B

illio

n

1,000

500

Office of Debt Management7

01-Oct 15-Nov 31-Dec 15-Feb 1-Apr 17-May 2-Jul 16-Aug

Optimism for Future Receipts in the Slowing Decline in Corporate Taxes

40%

Rolling 12-Month Growth Rates

Corp TaxesWH Taxes

20%

30% nWH Taxes

0%

10%

-20%

-10%

-40%

-30%

Office of Debt Management8

-50%

Mar

-82

Mar

-83

Mar

-84

Mar

-85

Mar

-86

Mar

-87

Mar

-88

Mar

-89

Mar

-90

Mar

-91

Mar

-92

Mar

-93

Mar

-94

Mar

-95

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

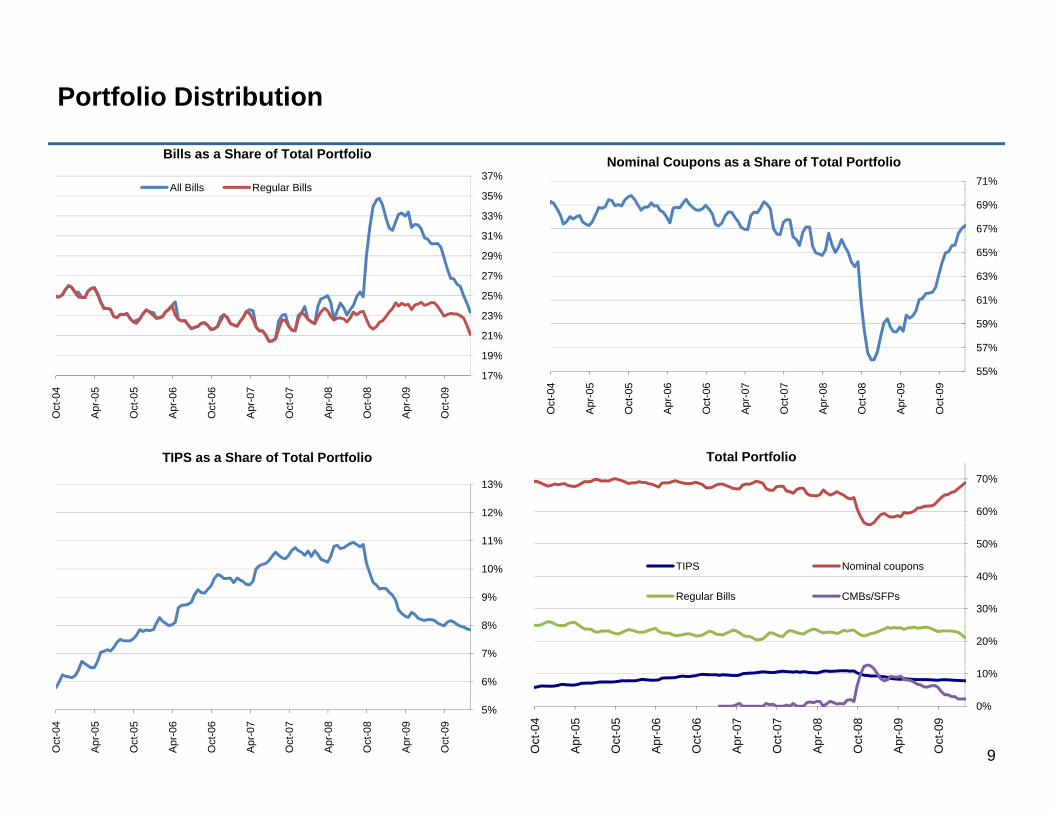

Portfolio Distribution

Bill Sh f T t l P tf li

29%

31%

33%

35%

37%

Bills as a Share of Total Portfolio

All Bills Regular Bills

65%

67%

69%

71%

Nominal Coupons as a Share of Total Portfolio

19%

21%

23%

25%

27%

29%

57%

59%

61%

63%

65%

Total PortfolioTIPS as a Share of Total Portfolio

17%

19%

Oct

-04

Apr

-05

Oct

-05

Apr

-06

Oct

-06

Apr

-07

Oct

-07

Apr

-08

Oct

-08

Apr

-09

Oct

-09

55%

Oct

-04

Apr

-05

Oct

-05

Apr

-06

Oct

-06

Apr

-07

Oct

-07

Apr

-08

Oct

-08

Apr

-09

Oct

-09

50%

60%

70%

Total Portfolio

11%

12%

13%

TIPS as a Share of Total Portfolio

20%

30%

40%TIPS Nominal coupons

Regular Bills CMBs/SFPs

7%

8%

9%

10%

Office of Debt Management9

0%

10%

Oct

-04

Apr

-05

Oct

-05

Apr

-06

Oct

-06

Apr

-07

Oct

-07

Apr

-08

Oct

-08

Apr

-09

Oct

-09

5%

6%

Oct

-04

Apr

-05

Oct

-05

Apr

-06

Oct

-06

Apr

-07

Oct

-07

Apr

-08

Oct

-08

Apr

-09

Oct

-09

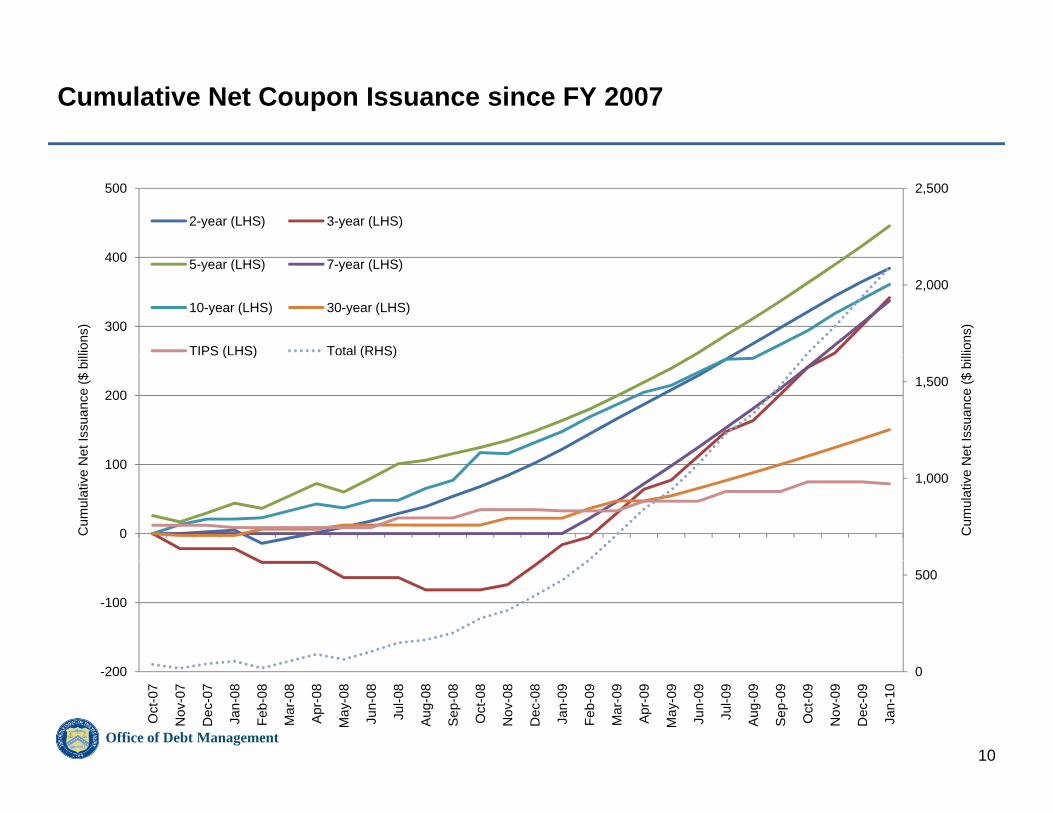

Cumulative Net Coupon Issuance since FY 2007

2,500

400

500

2-year (LHS) 3-year (LHS)

2,000

300

400

lions

)

lions

)

5-year (LHS) 7-year (LHS)

10-year (LHS) 30-year (LHS)

TIPS (LHS) Total (RHS)

1,500200

Net

Issu

ance

($ b

il

Net

Issu

ance

($ b

il S ( S) ( S)

1,000

0

100

Cum

ulat

ive

N

Cum

ulat

ive

N

500

-100

Office of Debt Management10

0-200

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Treasury Daily Operating Cash Balance

175

200$ Billions

Note: Data through January 21, 2010Excludes SFPs

150

175FY 2007 FY 2008

FY 2009 FY 2010Dec. 15 Jun. 15

100

125

Sep. 15Apr. 15

50

75

0

25

Office of Debt Management11

0Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

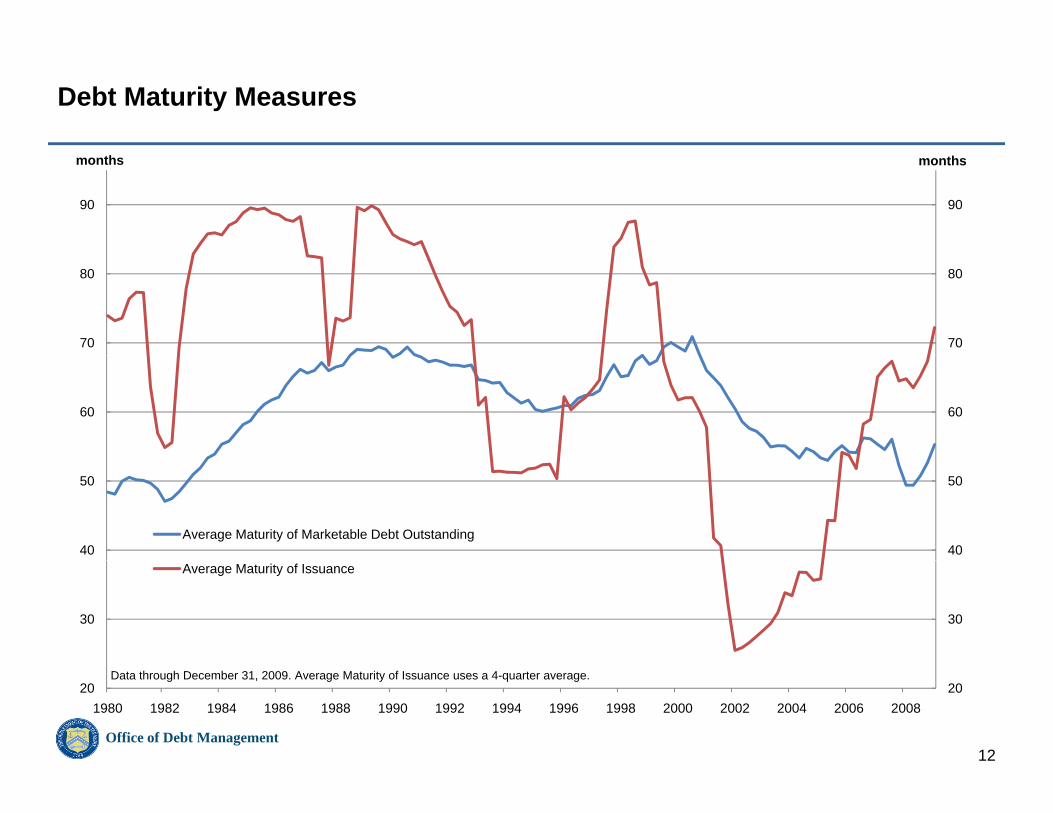

Debt Maturity Measures

9090

monthsmonths

70

80

70

80

6060

40

50

40

50

Average Maturity of Marketable Debt Outstanding

3030

Average Maturity of Issuance

Office of Debt Management12

20201980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Data through December 31, 2009. Average Maturity of Issuance uses a 4-quarter average.

Maturing Coupons

F b 15 2010 N b 15 2039

80

90$ Billions February 15, 2010-November 15, 2039

2 YR NOTE 3 YR NOTE 5 YR NOTE 7 YR NOTE 10 YR NOTE

30 YR BOND 5 YR IIS BOND 10 YR IIS NOTE 20 YR IIS BOND 30 YR IIS BOND

*Based on coupon securities outstanding as of January 21, 2010

In the next 5 years 78 days will have maturities greater

60

70

In the next 5 years, 78 days will have maturities greater than $20 billion and 54 days greater than $30 billion.

40

50

20

30

0

10

20

Office of Debt Management13

0

15-F

eb-1

031

-Mar

-10

15-M

ay-1

030

-Jun

-10

15-A

ug-1

030

-Sep

-10

15-N

ov-1

031

-Dec

-10

15-F

eb-1

115

-Apr

-11

30-J

un-1

131

-Aug

-11

15-N

ov-1

131

-Dec

-11

15-F

eb-1

231

-Mar

-12

15-M

ay-1

230

-Jun

-12

15-A

ug-1

230

-Sep

-12

15-N

ov-1

231

-Dec

-12

15-F

eb-1

315

-Apr

-13

31-M

ay-1

331

-Jul

-13

30-S

ep-1

330

-Nov

-13

31-J

an-1

431

-Mar

-14

15-M

ay-1

415

-Jul

-14

31-A

ug-1

415

-Nov

-14

15-J

an-1

515

-Jul

-15

15-J

an-1

631

-Mar

-16

31-M

ay-1

631

-Jul

-16

30-S

ep-1

630

-Nov

-16

15-F

eb-1

715

-Aug

-17

15-F

eb-1

815

-Aug

-18

15-F

eb-1

915

-Aug

-19

15-F

eb-2

015

-Feb

-21

15-N

ov-2

115

-Feb

-23

15-J

an-2

515

-Jan

-26

15-N

ov-2

615

-Aug

-27

15-A

pr-2

815

-Jan

-29

15-A

ug-2

915

-Apr

-32

15-M

ay-3

715

-Feb

-39

15-N

ov-3

9

Primary Dealer and Government Deficit Estimates

Deficit Estimates $ billionsDeficit Estimates $ billionsPrimary Dealers* CBO** OMB

FY2010: 1,357 1,349 1,556

Range 900-1,750

FY2011: 1,121 980 1,267

Range 750-1,800

Estimates as of: January 2010 January 2010 February 2010

FY 2010 Marketable Borrowing Estimate* 1,363 1,253 1,753

FY 2011 Marketable Borrowing Estimate* 1,150 988 1,201

* P i D l fl t ti t B d P i D l f db k J 28 2010* Primary Dealers reflect average estimate. Based on Primary Dealer feedback on January 28, 2010.

** Based on if current law and policies stayed unchanged (whereas OMB’s projections are based on current law and proposed policy).

Office of Debt Management14

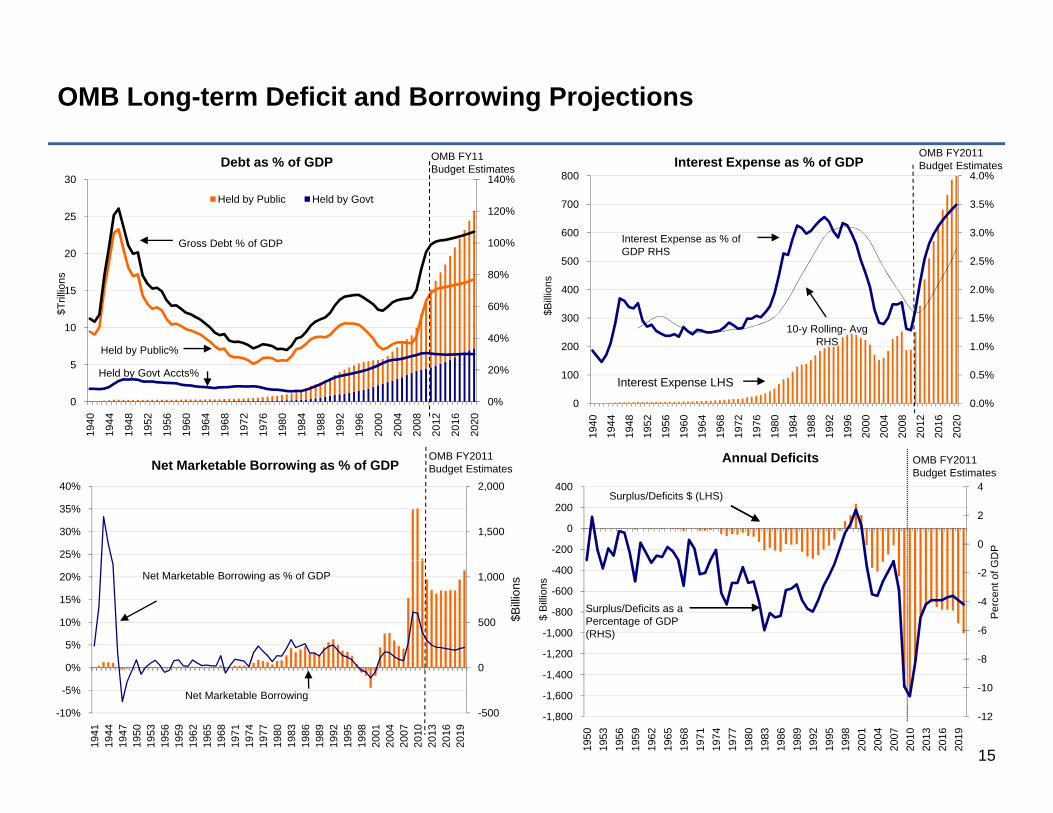

OMB Long-term Deficit and Borrowing Projections

OMB FY2011

3.0%

3.5%

4.0%

600

700

800Interest Expense as % of GDP

OMB FY2011 Budget Estimates

Interest Expense as % of GDP RHS

100%

120%

140%

20

25

30Debt as % of GDP

Held by Public Held by Govt

Gross Debt % of GDP

OMB FY11Budget Estimates

1.0%

1.5%

2.0%

2.5%

200

300

400

500

$Bill

ions

GDP RHS

10-y Rolling- AvgRHS40%

60%

80%

10

15

20

Held by Public%

$Tril

lions

0.0%

0.5%

0

100

1940

1944

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

2020

Interest Expense LHS0%

20%

0

5

1940

1944

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

2020

y

Held by Govt Accts%

OMB FY2011 Annual Deficits OMB FY2011

1,500

2,000

25%

30%

35%

40%

Net Marketable Borrowing as % of GDPOMB FY2011 Budget Estimates

0

2

4

-200

0

200

400

GD

P

Annual Deficits OMB FY2011 Budget Estimates

Surplus/Deficits $ (LHS)

500

1,000

5%

10%

15%

20%

$Billi

onsNet Marketable Borrowing as % of GDP

-8

-6

-4

-2

-1,200

-1,000

-800

-600

-400

Per

cent

of G

$ B

illio

ns

Surplus/Deficits as a Percentage of GDP (RHS)

Office of Debt Management15

-500

0

1941

1944

1947

1950

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

2019

-10%

-5%

0%

Net Marketable Borrowing

-12

-10

-1,800

-1,600

-1,400

1950

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

2019

Outstanding Debt Subject to Debt Limit

$12,500

$Billions

$11,500

$12,000

$11,000

$10,000

$10,500

$9,500

Office of Debt Management16

$9,0003/23/08 5/12/08 7/1/08 8/20/08 10/9/08 11/28/08 1/17/09 3/8/09 4/27/09 6/16/09 8/5/09 9/24/09 11/13/09 1/2/10

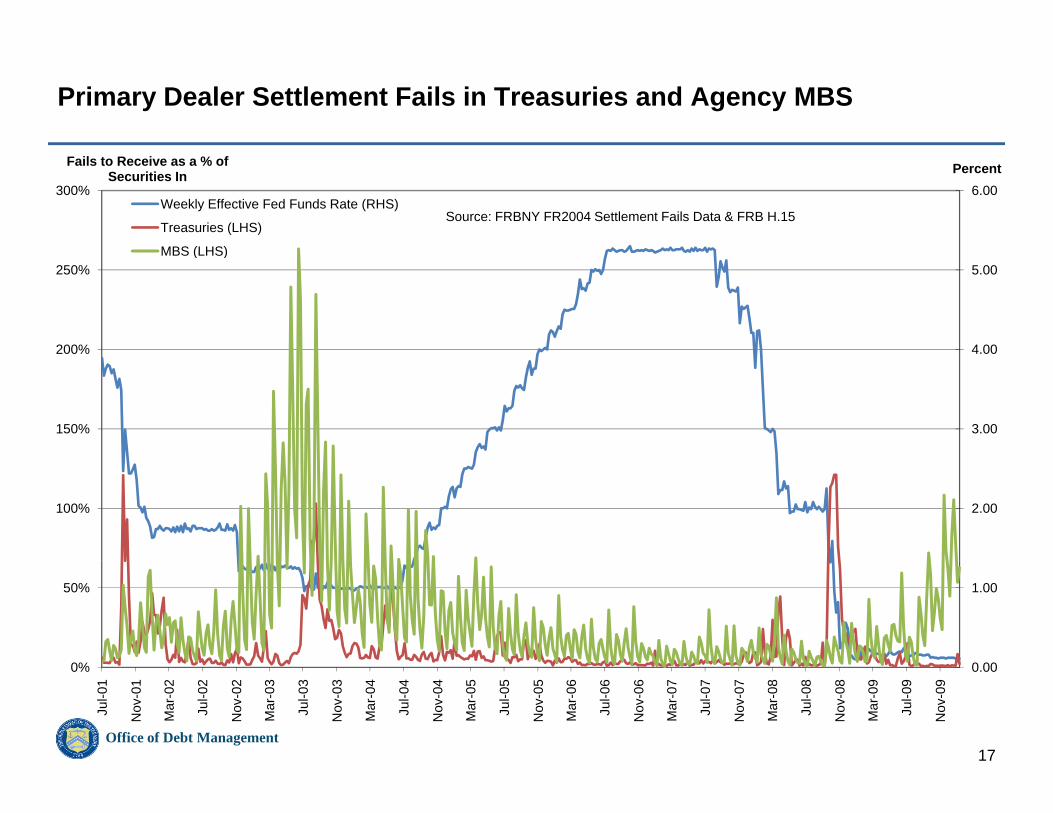

Primary Dealer Settlement Fails in Treasuries and Agency MBS

300% 6.00

Fails to Receive as a % of Securities In Percent

Weekly Effective Fed Funds Rate (RHS)

Treasuries (LHS)

MBS (LHS)

Source: FRBNY FR2004 Settlement Fails Data & FRB H.15

200%

250%

4.00

5.00MBS (LHS)

150% 3.00

100% 2.00

0%

50%

0 00

1.00

Office of Debt Management17

0%

Jul-0

1

Nov

-01

Mar

-02

Jul-0

2

Nov

-02

Mar

-03

Jul-0

3

Nov

-03

Mar

-04

Jul-0

4

Nov

-04

Mar

-05

Jul-0

5

Nov

-05

Mar

-06

Jul-0

6

Nov

-06

Mar

-07

Jul-0

7

Nov

-07

Mar

-08

Jul-0

8

Nov

-08

Mar

-09

Jul-0

9

Nov

-09

0.00

What adjustments to debt issuance if any should Treasury make inWhat adjustments to debt issuance, if any, should Treasury make in consideration of its financing needs in the short, medium, and long term?

Office of Debt Management18

TBAC Presentation to Treasury

February 2, 2010

Global Sovereign Borrowers

February 2, 2010

Global Sovereign BorrowersPlease assess the challenges faced by the global sovereign borrowers over the short, medium and long term. How are these challenges similar or different to the case of the United States?g

3

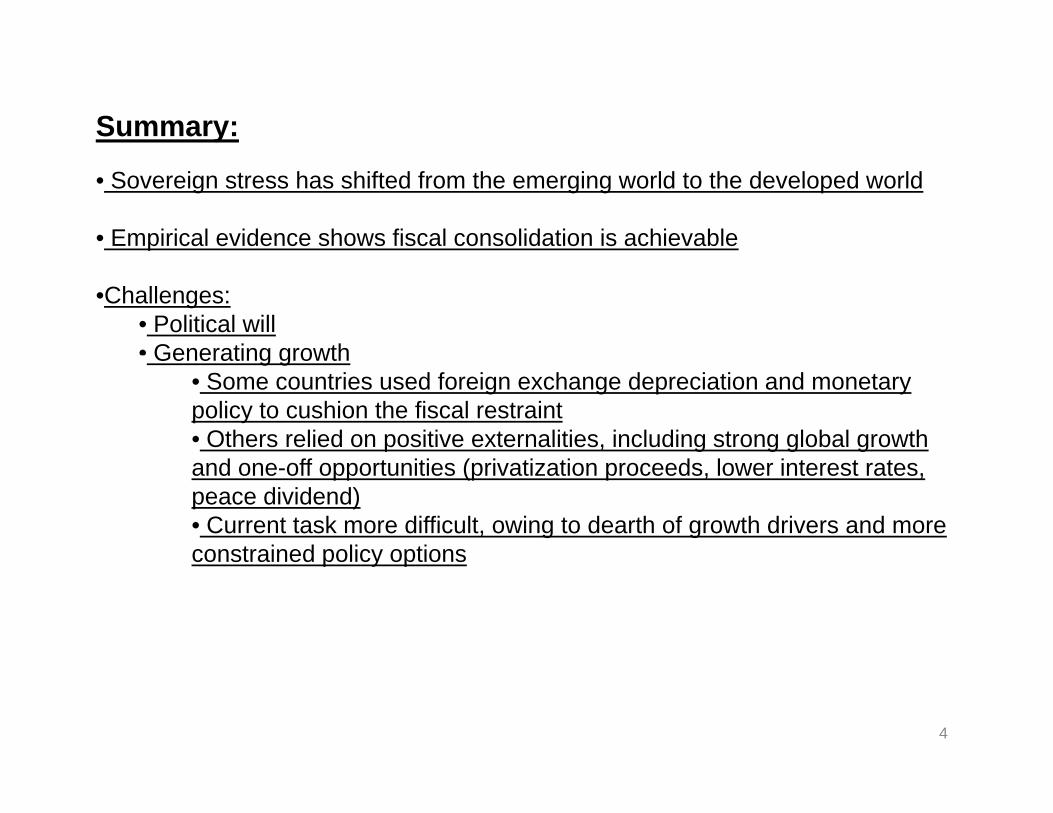

Summary:

• Sovereign stress has shifted from the emerging world to the developed world

• Empirical evidence shows fiscal consolidation is achievable

•Challenges: • Political will• Generating growthGenerating growth

• Some countries used foreign exchange depreciation and monetary policy to cushion the fiscal restraint• Others relied on positive externalities, including strong global growth and one-off opportunities (privatization proceeds, lower interest rates, peace dividend)• Current task more difficult, owing to dearth of growth drivers and more constrained policy optionsconstrained policy options

4

Current Account (% GDP) vs. Budget Deficit (% GDP): 1999 vs. 2009

RUS

151999

CHN

SWN10

2009

SWN

KOR5

10

% o

f GD

P

JPNRUS

GER

KOR

0

5

% o

f GD

P

KOR

GER

CANITA

JPN

TUR IND

FRA

IRECHN

0

5

t Acc

ount

as

a %

USIRE

UKIND

ESP

FRA

TUR

AUSCAN

ITABRA

-5

0

Acc

ount

as

a %

GER

BRAAUS

ESP USUK

GRCICE

-5

Cur

ren

GRC

ICE

-10C

urre

nt

-10-10 -5 0 5

Budget Deficit as a % of GDP

-15-19 -14 -9 -4 1

Budget Deficit as a % of GDP

5

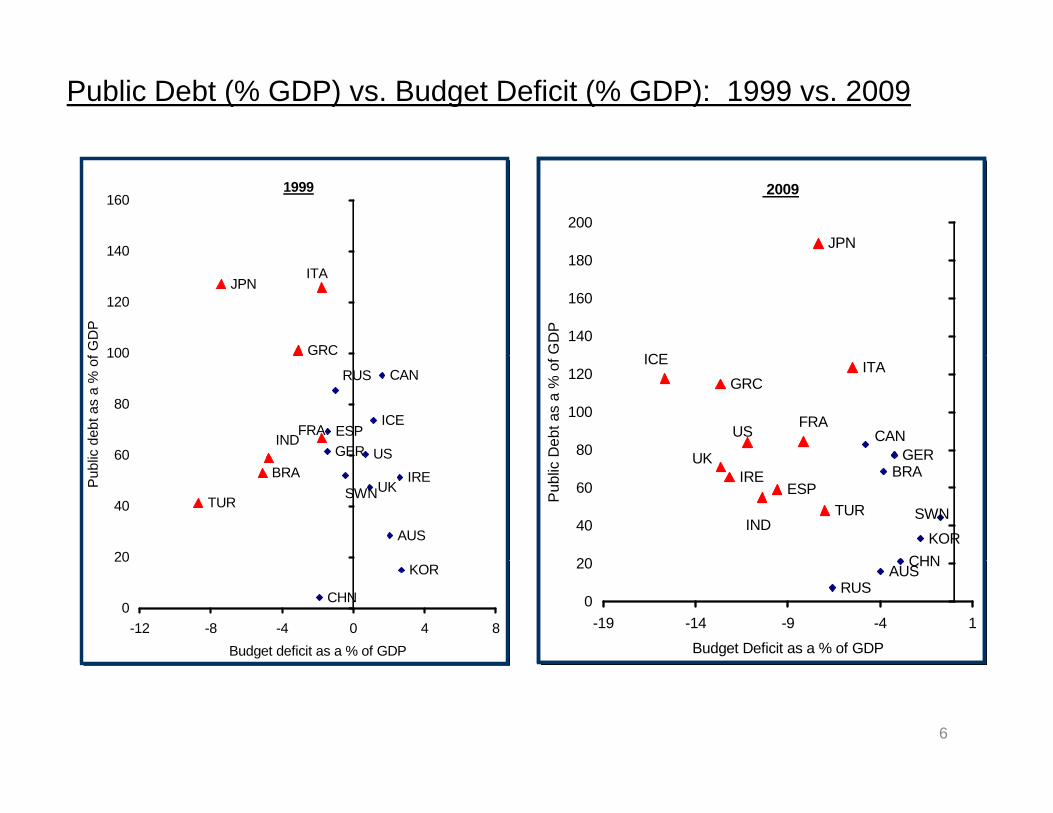

Public Debt (% GDP) vs. Budget Deficit (% GDP): 1999 vs. 2009

140

1601999

JPN200

2009

GRC

ITAJPN

100

120

140

f GD

P

ICE140

160

180

GD

P

INDGERESPFRA

US

ICE

CANRUS

60

80

100

ic d

ebt a

s a

% o

f ICEGRC

UK

US FRA

ITA

CANGER80

100

120

Deb

t as

a %

of

TUR

BRAUS

UK

AUS

IRESWN

20

40

60

Pub

li

ESPIRE

UK

INDTUR

BRAGER

KORSWN

CHN20

40

60Pub

lic

CHN

KOR

0

20

-12 -8 -4 0 4 8Budget deficit as a % of GDP

RUSAUS

CHN

0

20

-19 -14 -9 -4 1

Budget Deficit as a % of GDP

6

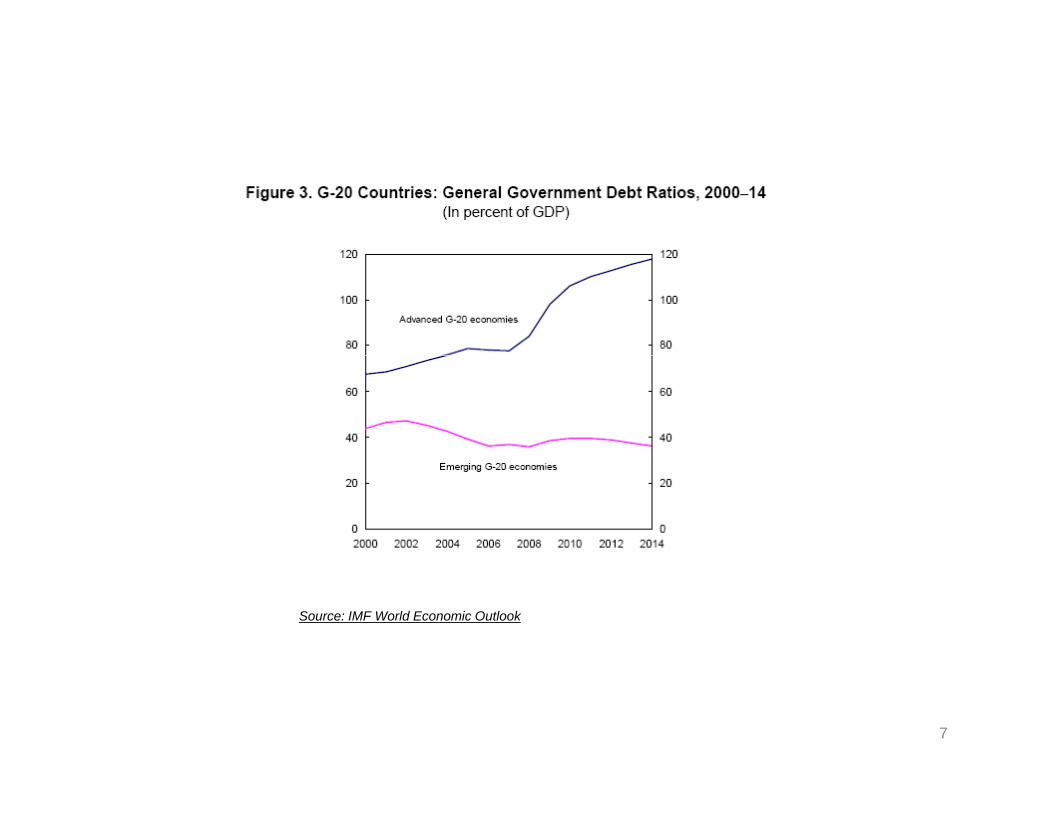

Source: IMF World Economic Outlook

7

Fiscal Balance Cyclically Adjusted Primary Position Gross Debtas a %of GDP as a %of potential GDP as a %of GDPas a % of GDP as a % of potential GDP as a % of GDP

US -11.2% -7.3% 84%

UK -12.6% -6.8% 71%

Japan -7.4% -5.6% 189%

Greece 12 7% 6 0% 113%Greece -12.7% -6.0% 113%

Spain -9.6% -5.6% 59%

8

6 0

Cyclically Adjusted Primary Balance as a % of Potential GDP%

0.0

2.0

4.0

6.0USUKJapan

-8.0

-6.0

-4.0

-2.0

8.01970 1974 1978 1982 1986 1990 1994 1998 2002 2006

6 0

Cyclically Adjusted Primary Balance as a % of Potential GDP%

0.0

2.0

4.0

6.0 GreeceSpain

-8 0

-6.0

-4.0

-2.0

-8.01970 1974 1978 1982 1986 1990 1994 1998 2002 2006

9

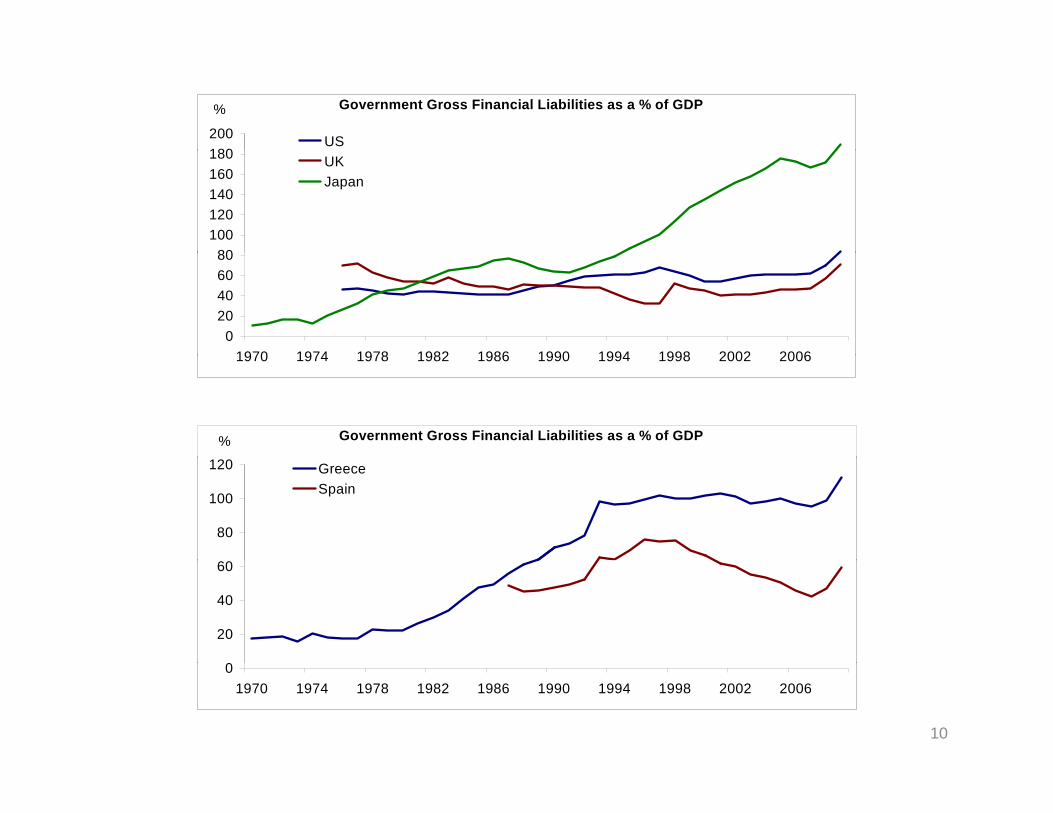

180200 US

Government Gross Financial Liabilities as a % of GDP%

80100120140160180 UK

Japan

020406080

1970 1974 1978 1982 1986 1990 1994 1998 2002 20061970 1974 1978 1982 1986 1990 1994 1998 2002 2006

Government Gross Financial Liabilities as a % of GDP%

80

100

120 GreeceSpain

0

20

40

60

01970 1974 1978 1982 1986 1990 1994 1998 2002 2006

10

Date - Trough Fiscal

Balance

Starting Fiscal

Balance

Date - Peak Fiscal

Balance

Ending Fiscal

Balance

Change in Fiscal

Balance

Date - Trough CAPB

Starting Cyclically

Adjusted Primary Balance

Date - Peak CAPB

Ending Cyclically Adjusted Primary Balance

Change in Cyclically Adjusted Primary Balance

% GDP % GDP % GDP % potential GDP % potential GDP % potential GDPp p GDP

Greece 1990 -14.0 1999 -3.1 10.9 1989 -6.1 1999 5.0 11.0

Spain 1993 -7.3 2006 2.0 9.3 1991 -3.0 2006 2.9 5.9Spain 1993 7.3 2006 2.0 9.3 1991 3.0 2006 2.9 5.9

Sweden 1993 -11.2 2000 3.7 14.9 1993 -4.8 2000 4.7 9.5

US 1992 -5.9 2000 1.5 7.4 1992 -1.6 2000 3.2 4.8

UK 1993 -8.0 2000 3.7 11.7 1993 -4.0 2000 3.0 7.0

Japan 1978 -5.8 1990 2.0 7.8 1977 -4.9 1989 2.2 7.1

11

Fiscal Consolidation

Period

Change in Expenditures as a % of GDP

Change in Revenues as a

% of GDP

Average GDP Growth (trend past 20 years)

Date - Peak Debt to

GDP Ratio

Starting Debt

Date - Trough Debt to

GDP Ratio

Ending Debt

Debt Reduction

% GDP % GDP % % GDP % GDP % GDP

Greece 1989 - 1999 3.8 12.8 2.1 (3.1) 1993 98 1994 96 2.0

Spain 1991 - 2006 -5.9 0.9 3.0 (3.2) 1996 76 2007 42 33.9p ( )

Sweden 1993 - 2000 -14.0 1.0 2.8 (2.4) 1996 84 2008 47 37.4

US 1992 - 2000 -4.8 2.6 3.8 (3.2) 1993 72 2001 54 17.4

UK 1993 - 2000 -8.7 3.0 3.4 (2.6) 1995 52 2001 40 11.2

Japan 1977 - 1989 1.0 6.4 4.0 (4.4) 1987 77 1991 63 13.6

12

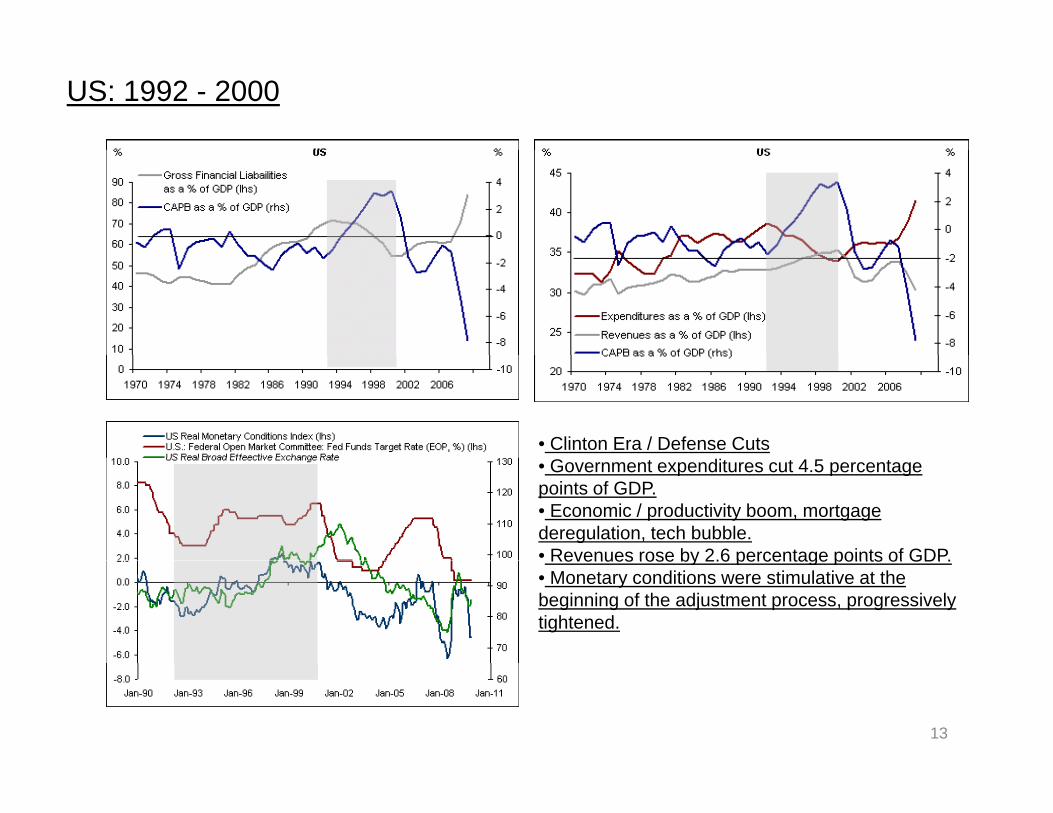

US: 1992 - 2000

• Clinton Era / Defense Cuts• Government expenditures cut 4.5 percentage points of GDP.• Economic / productivity boom, mortgage deregulation, tech bubble.• Revenues rose by 2.6 percentage points of GDP.Revenues rose by 2.6 percentage points of GDP.• Monetary conditions were stimulative at the beginning of the adjustment process, progressively tightened.

13

UK: 1993 - 2000

• Post -ERM Fiscal Consolidation• Government expenditures cut 8.7 percentage points of GDP.• Government employees cut by 10% between 1992 and 1998.• Revenues rose by 3 0 percentage points of GDP• Revenues rose by 3.0 percentage points of GDP.• Pound weak, monetary conditions easy, strong US / global growth.

14

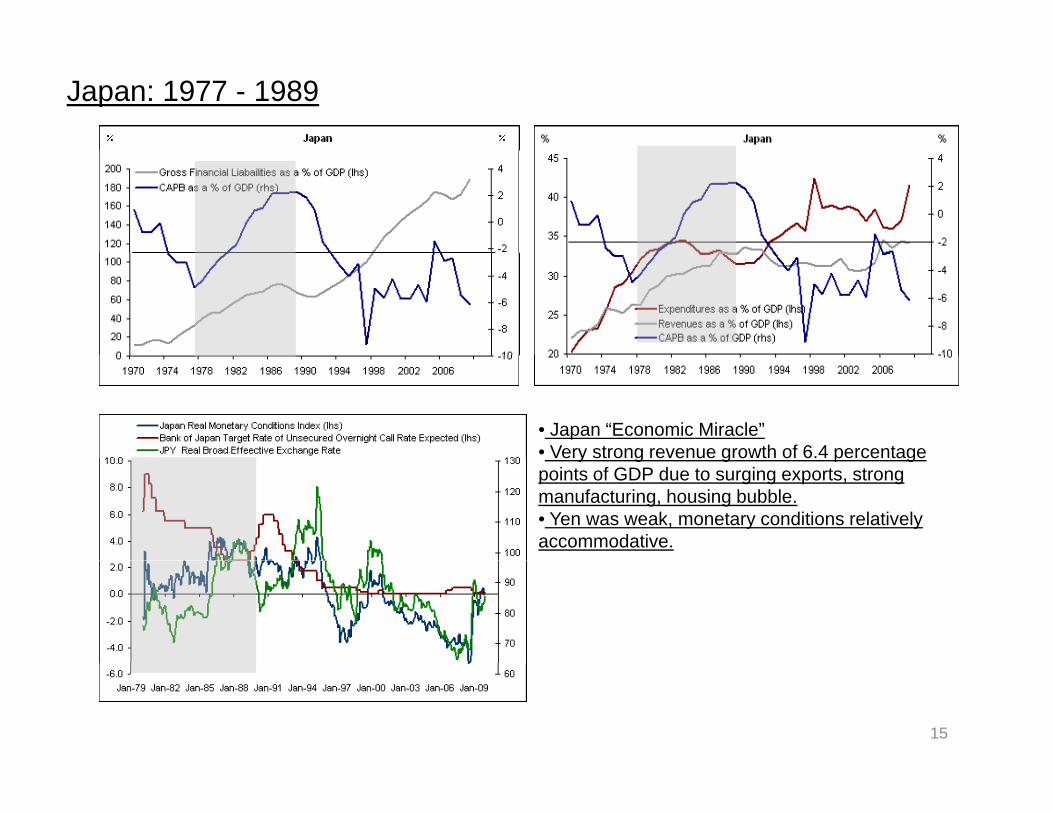

Japan: 1977 - 1989

• Japan “Economic Miracle”• Very strong revenue growth of 6.4 percentage e y st o g e e ue g o t o 6 pe ce tagepoints of GDP due to surging exports, strong manufacturing, housing bubble.• Yen was weak, monetary conditions relatively accommodative.

15

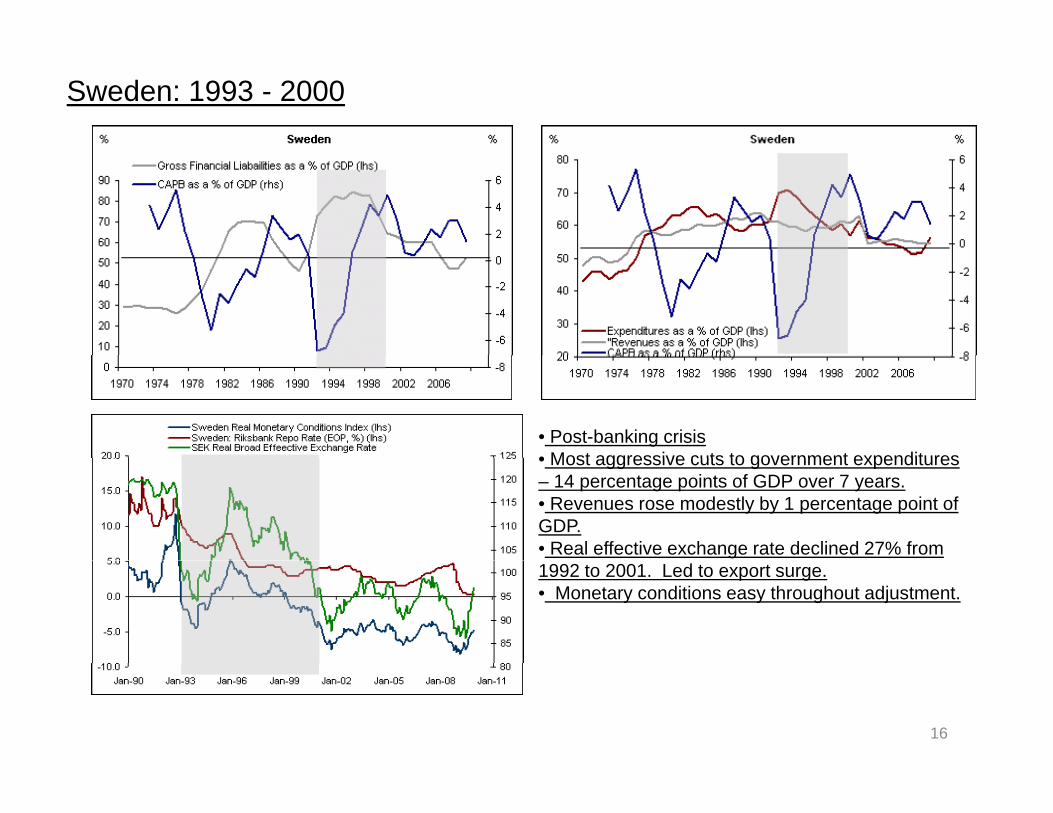

Sweden: 1993 - 2000

• Post-banking crisis• Most aggressive cuts to government expenditures• Most aggressive cuts to government expenditures – 14 percentage points of GDP over 7 years.• Revenues rose modestly by 1 percentage point of GDP.• Real effective exchange rate declined 27% from 1992 to 2001. Led to export surge.• Monetary conditions easy throughout adjustment.

16

Greece: 1989 - 1999

• EMU convergence• EMU convergence• Government expenditures rose by 3.8 percentage points of GDP.• Improvement entirely on the revenue side. Revenues rose 12.8 percentage points of GDP. Around 3.6% of this increase was due to privatizations. p•Tight monetary conditions in first half of adjustment period led to disinflation, followed by massive easing in monetary conditions.• Convergence/risk premium compression: interest payments as a % of GDP fell from 11.2 to 4.1 between 1995

d 2007 D i thi i d t diand 2007. During this period, government spending ex-interest rose by 6.2 percentage points of GDP.

17

Spain: 1991 - 2006

• EMU convergence / Housing boomExpenditures cut 6 9 percentage points of GDP• Expenditures cut 6.9 percentage points of GDP.

• Revenues rose by 0.9% over the adjustment period. Around 0.2% of this increase was due to privatizations. From 1998 to 2006 they rose 2.3% due to the housing boom.

M t diti d i EMU• Monetary conditions easy during EMU convergence. Following Euro launch, ECB rates were accommodative for Spanish growth.• Convergence/risk premium compression: interest payments as a % of GDP fell from 5.1 to 1.6 between 1995 d 2007 D i thi i d t1995 and 2007. During this period, government spending ex-interest fell by 1.7% percentage points of GDP.

18

Fiscal Adjustment Scenarios: 5 year

US: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 5 yrs)Nominal Nominal GDP growth

Interest Rate 2.0 - 4.0 4.0 - 6.0 6.0 - 8.02.0 1.1 - 1.5 0.8 - 1.1 0.5 - 0.8

4.0 1.5 - 1.8 1.1 - 1.5 0.8 - 1.1

6 0 1 8 2 1 1 5 1 8 1 1 1 5

UK: Reduction in primary deficit pa needed to stabilise the gross govt debt to GDP ratio (% pt change over 5 yrs)

6.0 1.8 - 2.1 1.5 - 1.8 1.1 - 1.5

8.0 2.1 - 2.5 1.8 - 2.1 1.5 - 1.8

Initial debt-to-GDP ratio is 84%, and the initial primary balance is -7.3% of GDP

UK: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 5 yrs)Nominal Nominal GDP growth

Interest Rate 2.0 - 4.0 4.0 - 6.0 6.0 - 8.02.0 1.1 - 1.3 0.8 - 1.1 0.5 - 0.8

4.0 1.4 - 1.6 1.1 - 1.4 0.8 - 1.1

6.0 1.6 - 1.9 1.4 - 1.6 1.1 - 1.4

Japan: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 5 yrs)Nominal Nominal GDP growth

8.0 1.9 - 2.1 1.6 - 1.9 1.4 - 1.6

Initial debt-to-GDP ratio is 71%, and the initial primary balance is -6.8% of GDP

Nominal Nominal GDP growthInterest Rate 0.0 - 1.5 1.5 - 3.5 3.5 - 5.5

0.0 0.6 - 1.1 -0.2 - 0.6 -1.0 - -0.2

2.0 1.3 - 1.9 0.6 - 1.3 -0.2 - 0.6

4.0 2.1 - 2.6 1.3 - 2.1 0.6 - 1.3

6 0 2 8 3 4 2 1 2 8 1 3 2 16.0 2.8 - 3.4 2.1 - 2.8 1.3 - 2.1

Initial debt-to-GDP ratio is 189%, and the initial primary balance is -5.6% of GDP

19

Fiscal Adjustment Scenarios: 5 year

Greece: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 5 yrs)Nominal Nominal GDP growth

Interest Rate 3.0 - 5.0 5.0 - 7.0 7.0 - 9.02.0 0.5 - 1.0 0.1 - 0.5 -0.4 - 0.1

4.0 1.0 - 1.4 0.5 - 1.0 0.1 - 0.5

6.0 1.4 - 1.9 1.0 - 1.4 0.5 - 1.0

S i R d ti i i d fi it d d t t bili th t d bt t GDP ti (% t h 5 )

6.0 1.4 1.9 1.0 1.4 0.5 1.0

8.0 1.9 - 2.3 1.4 - 1.9 1.0 - 1.4

Initial debt-to-GDP ratio is 113%, and the initial primary balance is -6.0% of GDP

Spain: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 5 yrs)Nominal Nominal GDP growth

Interest Rate 3.0 - 5.0 5.0 - 7.0 7.0 - 9.02.0 0.8 - 1.0 0.5 - 0.8 0.3 - 0.5

4.0 1.0 - 1.2 0.8 - 1.0 0.5 - 0.8

6.0 1.2 - 1.5 1.0 - 1.2 0.8 - 1.06 0 0

8.0 1.5 - 1.7 1.2 - 1.5 1.0 - 1.2

Initial debt-to-GDP ratio is 59%, and the initial primary balance is -5.6% of GDP

20

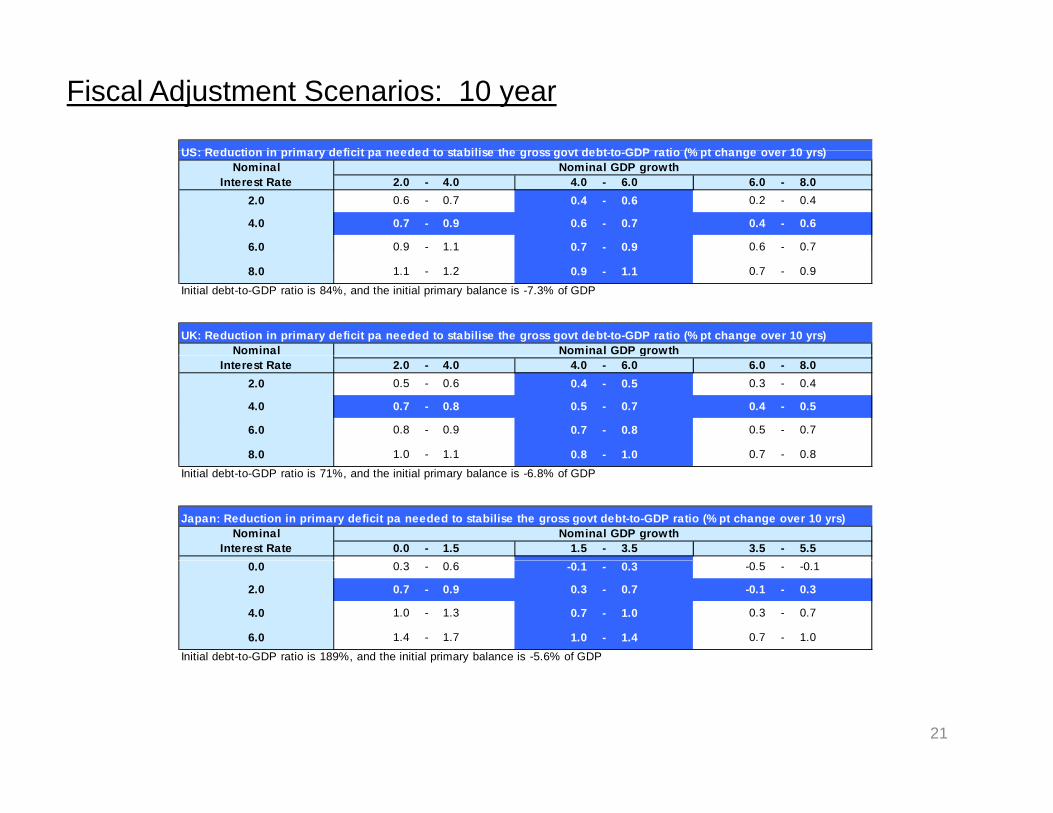

Fiscal Adjustment Scenarios: 10 year

US: Reduction in primary deficit pa needed to stabilise the gross govt debt to GDP ratio (% pt change over 10 yrs)US: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 10 yrs)Nominal Nominal GDP growth

Interest Rate 2.0 - 4.0 4.0 - 6.0 6.0 - 8.02.0 0.6 - 0.7 0.4 - 0.6 0.2 - 0.4

4.0 0.7 - 0.9 0.6 - 0.7 0.4 - 0.6

6.0 0.9 - 1.1 0.7 - 0.9 0.6 - 0.7

8.0 1.1 - 1.2 0.9 - 1.1 0.7 - 0.9

Initial debt-to-GDP ratio is 84%, and the initial primary balance is -7.3% of GDP

UK: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 10 yrs)Nominal Nominal GDP growthg

Interest Rate 2.0 - 4.0 4.0 - 6.0 6.0 - 8.02.0 0.5 - 0.6 0.4 - 0.5 0.3 - 0.4

4.0 0.7 - 0.8 0.5 - 0.7 0.4 - 0.5

6.0 0.8 - 0.9 0.7 - 0.8 0.5 - 0.7

8.0 1.0 - 1.1 0.8 - 1.0 0.7 - 0.88.0 0 0.8 1.0 0 0 8

Initial debt-to-GDP ratio is 71%, and the initial primary balance is -6.8% of GDP

Japan: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 10 yrs)Nominal Nominal GDP growth

Interest Rate 0.0 - 1.5 1.5 - 3.5 3.5 - 5.50.0 0.3 - 0.6 -0.1 - 0.3 -0.5 - -0.1

2.0 0.7 - 0.9 0.3 - 0.7 -0.1 - 0.3

4.0 1.0 - 1.3 0.7 - 1.0 0.3 - 0.7

6.0 1.4 - 1.7 1.0 - 1.4 0.7 - 1.0

Initial debt-to-GDP ratio is 189%, and the initial primary balance is -5.6% of GDP

21

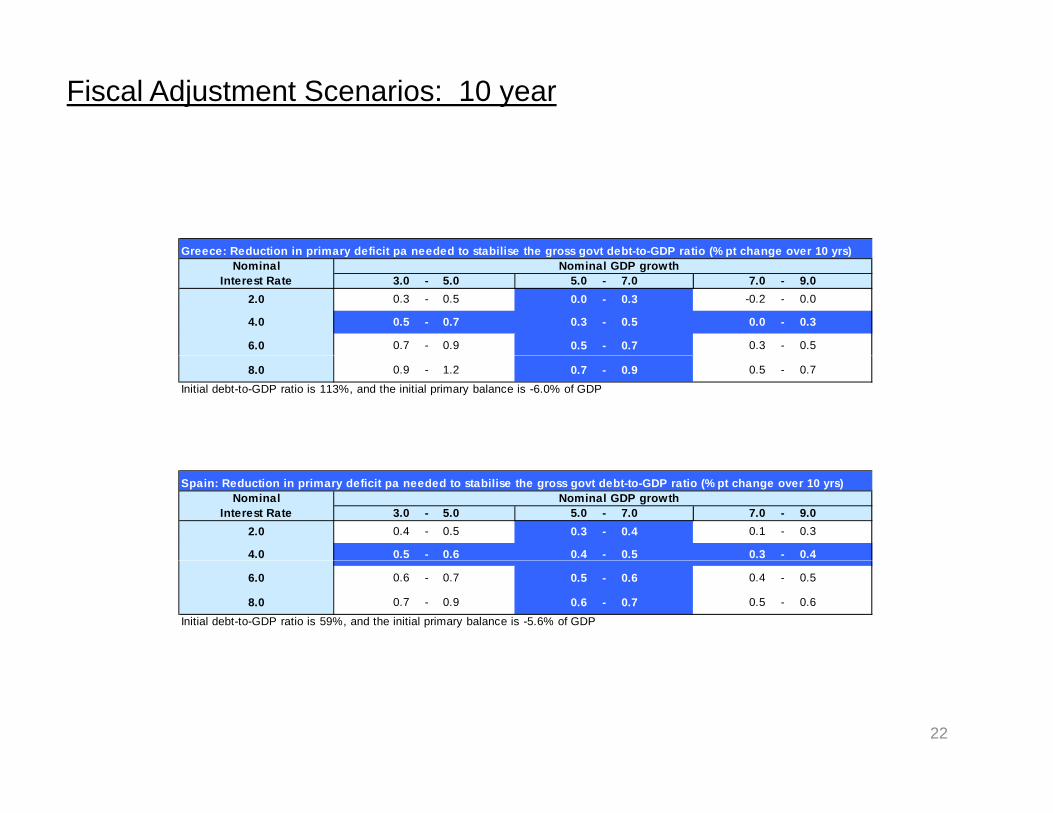

Fiscal Adjustment Scenarios: 10 year

Greece: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 10 yrs)Greece: Reduction in primary deficit pa needed to stabilise the gross govt debt to GDP ratio (% pt change over 10 yrs)Nominal Nominal GDP growth

Interest Rate 3.0 - 5.0 5.0 - 7.0 7.0 - 9.02.0 0.3 - 0.5 0.0 - 0.3 -0.2 - 0.0

4.0 0.5 - 0.7 0.3 - 0.5 0.0 - 0.3

6.0 0.7 - 0.9 0.5 - 0.7 0.3 - 0.5

8.0 0.9 - 1.2 0.7 - 0.9 0.5 - 0.7

Initial debt-to-GDP ratio is 113%, and the initial primary balance is -6.0% of GDP

Spain: Reduction in primary deficit pa needed to stabilise the gross govt debt-to-GDP ratio (% pt change over 10 yrs)Nominal Nominal GDP growth

Interest Rate 3.0 - 5.0 5.0 - 7.0 7.0 - 9.02.0 0.4 - 0.5 0.3 - 0.4 0.1 - 0.3

4.0 0.5 - 0.6 0.4 - 0.5 0.3 - 0.4

6.0 0.6 - 0.7 0.5 - 0.6 0.4 - 0.5

8.0 0.7 - 0.9 0.6 - 0.7 0.5 - 0.6

Initial debt-to-GDP ratio is 59%, and the initial primary balance is -5.6% of GDP

22

Conclusions:• Fiscal consolidation can happen – could result in slower than desired growth• Similarities with the US

• Easy monetary conditions as a a starting pointDiffi lt liti l i t• Difficult political environment

• Modest global growth• Lack of positive externalities

• Differences with the US• Lack of autonomous monetary policy• Currency flexibility• Historical precedent

• If all countries need to stimulate who will provide the savings? Global growth• If all countries need to stimulate, who will provide the savings? Global growth rebalancing is key.

23

Demand for Treasury Securitiesand 2010 Spread Outlookp

February 2, 2010

Foreigners are the largest holders of Treasuries followed byForeigners are the largest holders of Treasuries, followed by households and the Fed

Fig 1 Treasury Holdings by SectorFig. 1 Treasury Holdings by Sector

6,000

7,000

8,000

2,000

3,000

4,000

5,000

$(B

il.)

-1,000

0

1,000

Tota

l

Sect

or

ehol

ds

eser

ve

Gov

'ts

Fund

s

Fund

s

Fund

s

ankin

g

Fund

s

mpa

nies

Fund

s

Dea

lers

Oth

er

Fore

ign

Hou

s

Fede

ral R

e

Stat

e &

Loca

l

Mon

ey M

arke

t

Mut

ual F

Priv

ate

Pens

ion

Com

mer

cial

Ba

& Lo

cal G

ov't P

ensi

on

Life

Insu

ranc

e C

o m

eder

al G

ov't P

ensio

n

Secu

rity

Brok

ers &

D

25

Stat

e & FQ3-07 Q3-08 Q3-09

Source: Federal Reserve

Large shifts in % share of holdings occurred in 2008 2009Large shifts in % share of holdings occurred in 2008‐2009

Fig 2 Share of Treasury HoldingsFig. 2 Share of Treasury Holdings

50%

55%

30%

35%

40%

45%

cent

.

10%

15%

20%

25%

Per

c

0%

5%

Q49

9

Q30

0

Q20

1

Q10

2

Q40

2

Q30

3

Q20

4

Q10

5

Q40

5

Q30

6

Q20

7

Q10

8

Q40

8

Q30

9

Foreign Sector Households Federal Reserve State & Local Gov'ts

26

gMoney Market Funds Mutual Funds Commercial Banking

Source: Federal Reserve

With the expanding federal debt long term Treasury securitiesWith the expanding federal debt, long‐term Treasury securities outstanding rose significantly

Fi 3 Treas r Holdin s b T pe

7,500Bills Notes Bonds TIPS

Q407 22.2% 55.0% 12.3% 10.4%Q408 32 3% 48 3% 10 3% 9 2%

Fig. 3 Treasury Holdings by Type

4,500

6,000

Tril.

)

Q408 32.3% 48.3% 10.3% 9.2%Q409 24.7% 57.6% 9.9% 7.8%

1,500

3,000

$(T

0

Dec

-04

Feb-

05A

pr-0

5Ju

n-05

Aug

-05

Oct

-05

Dec

-05

Feb-

06A

pr-0

6Ju

n-06

Au g

-06

Oct

-06

Dec

-06

Feb-

07A

pr-0

7Ju

n-07

Au g

-07

Oct

-07

Dec

-07

Feb-

08A

pr-0

8Ju

n-08

Aug

-08

Oct

-08

Dec

-08

Feb-

09A

pr-0

9Ju

n-09

Au g

-09

Oct

-09

Dec

-09

Bills Notes Bonds TIPS Total

Source: Treasury

27

Fed data suggests the Fed foreigners and households (incl hedgeFed data suggests the Fed, foreigners and households (incl. hedge funds) dominated the ‘09 increase in Treasury holdings

Fi 4 Q t l Ch i T H ldi b P h

600

700

Fig. 4 Quarterly Change in Treasury Holdings by Purchaser

100

200

300

400

500

$(B

il.)

Foreign

Household/Hedge Fund

F d

-300

-200

-100

0

100 Fed

300

Q40

4

Q10

5

Q20

5

Q30

5

Q40

5

Q10

6

Q20

6

Q30

6

Q40

6

Q10

7

Q20

7

Q30

7

Q40

7

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Q40

9

Federal Reserve Depository InstitutionsHouseholds Dealers and BrokersPension and Retirement Funds and Insurance Cos. Investment Funds ex MMMFForeign and International OtherForeign and International OtherMoney Market Fund Total

Source: Federal Reserve

28

Foreigners’ accumulation in 2009 outpaced prior years

Foreign official institutions are larger holders than foreign private (non US banks pension funds insurance)(non‐US banks, pension funds, insurance)

Fig. 5 Foreign Net Purchases of Long‐Term Treasuries (Year‐to‐date)

Fig. 6 Foreign Treasury Holdings: Official vs PrivateTreasuries (Year to date) Official vs. Private

200

250

300

350

.) .

2,000

2,500

3,000

0

50

100

150

200

YTD

, US

$ (B

il

500

1,000

1,500

US

$ (B

il.)

-50

0

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec

2005 2006 2007 2008 2009

Source: US Treasury

0

Nov

-00

May

-01

Nov

-01

May

-02

Nov

-02

May

-03

Nov

-03

May

-04

Nov

-04

May

-05

Nov

-05

May

-06

Nov

-06

May

-07

Nov

-07

May

-08

Nov

-08

May

-09

Nov

-09

Of f icial Private

Source: US Treasury

29

Foreigners shift to Treasuries away from agenciesForeigners shift to Treasuries, away from agencies

Fi 7 F i N t P h f US L T A tFig. 7 Foreign Net Purchases of US Long‐Term Assets

150

200

50

100

150

US

$ (B

il.)

100

-50

0

U

-100

Nov

-05

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep

-06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Se p

-07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Se p

-09

Nov

-09

Treasurys Agencies Corporates Equities Total (RHS)

30

Source: US Treasury

China surpassed Japan to become the largest foreign holder; thisChina surpassed Japan to become the largest foreign holder; this trend stalled in 2009, though holdings in dollar terms rose

Fi 8 Sh f T t l F i T H ldi

40%

45%

Fig. 8 Share of Total Foreign Treasury Holdings

20%

25%

30%

35%

rcen

t of T

otal

5%

10%

15%

20%

Per

0%

Nov

-04

Feb-

05

Ma y

-05

Au g

-05

Nov

-05

Feb-

06

May

-06

Au g

-06

Nov

-06

Feb-

07

May

-07

Au g

-07

Nov

-07

Feb-

08

May

-08

Aug

-08

Nov

-08

Feb-

09

Ma y

-09

Aug

-09

Nov

-09

Japan China OPEC Caribbean+Cayman Island UK Elsewhere

S US TSource: US Treasury

31

Foreigners’ demand for Treas ries shifted from bills to bonds in 2009 asForeigners’ demand for Treasuries shifted from bills to bonds in 2009 as risk aversion fell and the yield curve steepened, and this trend should continue in 2010

Fig. 9 Foreign Net PurchasesBonds vs. Bills (Private Holders)

Fig. 10 Foreign Net PurchasesBonds vs Bills (Official Holders)Bonds vs. Bills (Official Holders)

200

250

300

350

400

(Bil.

)

200

250

300

350

400

(Bil.

) 100

-50

0

50

100

150

200

12-M

onth

Sum

, $ (

-100

-50

0

50

100

150

200

12-M

onth

Sum

, $

-100

Nov

-00

Mar

-01

Jul-0

1N

ov-0

1M

ar-0

2Ju

l-02

Nov

-02

Mar

-03

Jul-0

3N

ov-0

3M

ar-0

4Ju

l-04

Nov

-04

Mar

-05

Jul-0

5N

ov-0

5M

ar-0

6Ju

l-06

Nov

-06

Mar

-07

Jul-0

7N

ov-0

7M

ar-0

8Ju

l-08

Nov

-08

Mar

-09

Jul-0

9N

ov-0

9

Private: Bonds Private: Bills

Source: US Treasury

100

Nov

-00

Mar

-01

Jul-0

1N

ov-0

1M

ar-0

2Ju

l-02

Nov

-02

Mar

-03

Jul-0

3N

ov-0

3M

ar-0

4Ju

l-04

Nov

-04

Mar

-05

Jul-0

5N

ov-0

5M

ar-0

6Ju

l-06

Nov

-06

Mar

-07

Jul-0

7N

ov-0

7M

ar-0

8Ju

l-08

Nov

-08

Mar

-09

Jul-0

9N

ov-0

9

Of f icial: Bonds Off icial: Bills

Source: US Treasury

32

The Fed increased holdings in 2009 mostly in notes andThe Fed increased holdings in 2009, mostly in notes and bonds, holding fewer bills after the financial crisis started

Fi 11 T H ldi b TFig. 11 Treasury Holdings by Type

800

900 In the spring of 2008 the Fed soldTreasury bills in order to sterilize anexpansion of the TAF program

500

600

700

Bil.

)

100

200

300

400$(

0

100

12/2

2/04

03/1

6/05

06/0

8/05

08/3

1/05

11/2

3/05

02/1

5/06

05/1

0/06

08/0

2/06

10/2

5/06

01/1

7/07

04/1

1/07

07/0

4/07

09/2

6/07

12/1

9/07

03/1

2/08

06/0

4/08

08/2

7/08

11/1

9/08

02/1

1/09

05/0

6/09

07/2

9/09

10/2

1/09

01/1

3/10

33

Bills Notes and Bonds Inf lation Compensation TIPS Total

Source: Federal Reserve

As loan demand fell cyclically US commercial banks held moreAs loan demand fell cyclically, US commercial banks held more government securities

Fi 12 B k L C i l B k T H ldi

600

750

900

Fig. 12 Bank Loans vs. Commercial Banks Treasury Holdings

0

150

300

450

600

Diff

. SA

, $B

il

-600

-450

-300

-150

0

Y-Y

600

Dec

-05

Feb-

06

Apr

-06

Jun-

06

Aug

-06

Oct

-06

Dec

-06

Feb-

07

Apr

-07

Jun-

07

Aug

-07

Oct

-07

Dec

-07

Feb-

08

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb-

09

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

US Government Securities in Bank Credit: All Commercial BanksLoans and Leases in Bank Credit: All Commercial Banks

Source: Federal Reserve

34

The household category has substituted from agencies toThe household category has substituted from agencies to Treasuries; household category likely includes hedge funds

Fi 13 N t A i iti f Fi i l A t B H h ld (NSA)

400

600

800

Fig. 13 Net Acquisition of Financial Assets By Households (NSA)

200

0

200

400

$(B

il.)

Out of agencies, into Treasuries

-800

-600

-400

-200 Treasuries

-800

Q30

4

Q40

4

Q10

5

Q20

5

Q30

5

Q40

5

Q10

6

Q20

6

Q30

6

Q40

6

Q10

7

Q20

7

Q30

7

Q40

7

Q10

8

Q20

8

Q30

8

Q40

8

Q10

9

Q20

9

Q30

9

Checkable Deposits and Currency Time & Savings Deposits Money Market Fund SharesTreasurys Agencies Corporate and Foreign BondsEquities Mutual Fund Shares Security CreditOther Total

Source: Federal ReserveSource: Federal Reserve

35

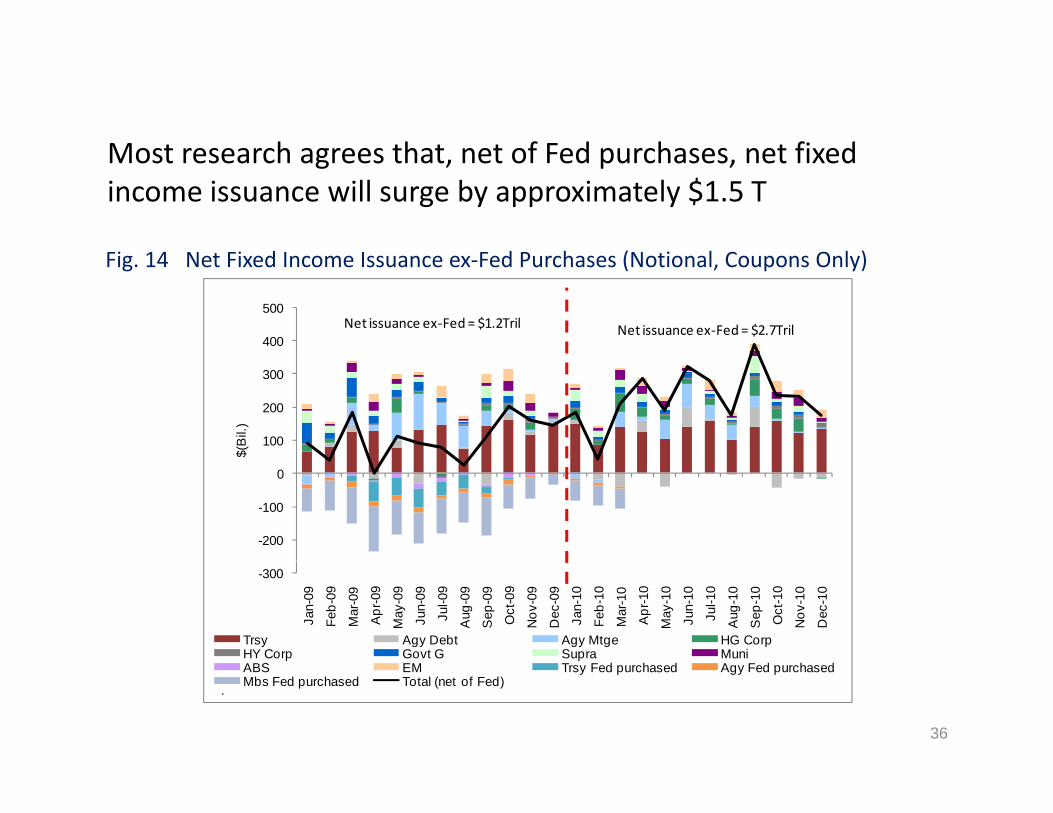

Most research agrees that net of Fed purchases net fixedMost research agrees that, net of Fed purchases, net fixed income issuance will surge by approximately $1.5 T

Fi 14 N Fi d I I F d P h (N i l C O l )Fig. 14 Net Fixed Income Issuance ex‐Fed Purchases (Notional, Coupons Only)

400

500Net issuance ex‐Fed = $1.2Tril Net issuance ex‐Fed = $2.7Tril

100

200

300

$(B

il.)

-200

-100

0

-300

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Trsy Agy Debt Agy Mtge HG CorpHY Corp Govt G Supra MuniABS EM T F d h d A F d h d

36

ABS EM Trsy Fed purchased Agy Fed purchasedMbs Fed purchased Total (net of Fed)

.

Sources of marginal demand for excess net issuance

i 1 ibl d b SFig. 15 Possible Treasury Demand by Sector

($ billions)

Net Net

Coupons + Net

20102009

Bills TIPS BillsNet Supply (Act.+Est.) -73 1385 -400 1400 1400

Assume No Fed & Comparable

Behavior to '08/09

Assume No Fed & 05-09 % Share of

Net Change in Holdings

Net Coupons + TIPS

LowFed 0 300 0 0 0Foreigners 445 620 935 Foreigners addMoney Mkt+MF -165 80 155 Depends on asset allocation and savings behaviorOther 40 145 430 "Other" categories includes pensions and broker dealers Banks 115 60 30 Depends on loan demand and liquidity requirementsHouseholds 650 495 -150 Households/Hedge Funds behavior most price sensitiveNet Demand -73 1385 -400 1400 1400

Pric

e Se

nsiti

vity

HighNet Demand 73 1385 400 1400 1400Sources: Federal Reserve, US Treasury

37

Treasury issuance of bills and coupon securitiesTreasury issuance of bills and coupon securities

Fig. 16 Treasury Supply (Bills) A t l d E ti t

Fig. 17 Treasury Supply (Coupons) A t l d E ti tActual and Estimate Actual and Estimate

400

600

800

1000

1000

1200

1400

1600

-400

-200

0

200

400

$(B

il.)

200

0

200

400

600

800

$(B

il.)

-600

2006

2007

2008

2009

2010

Net Bills Fed Net Purchases

Sources: Federal Reserve, US Treasury and Estimates

-200

2006

2007

2008

2009

2010

Net Coupon +TIPS Fed Net Purchases

Sources: Federal Reserve, US Treasury and Estimates

38

Expectations for the performance of spread products in 2010

• Long-dated swap spreads should widen while short-dated swap spreads should remain stable or tighten slightly

• Corporate credit spreads should continue to stabilize tighter

• Municipal spread levels have tightened with strong demand, but fundamental deterioration continues

• CMBS spreads should continue to improve• CMBS spreads should continue to improve

• Mortgage basis should widen modestly

39

The term structure of swap spreads shouldThe term structure of swap spreads should normalize in 2010

• Long (15-30y) spreads should widen– Increased balance sheet demand for 0% risk-weighted assets that trade LIBOR plus– Very negative forward spread levels

• Short (0-5y) spreads should remain stable or tighten slightly as systemic risk concerns continue to wane

Fig. 18 Historical Swap Spreads

200180

4004080120160

6080

100120140160

bp

ead

(bp)

-160-120-80-40

0204060

23-Jan-95 10-Nov-97 1-Sep-00 4-Aug-03 6-Jul-06 4-Jun-09

Spre

40

2Y (bp) 30Y - 2Y (bp) (2nd axis) 30Y (bp) (2nd axis)

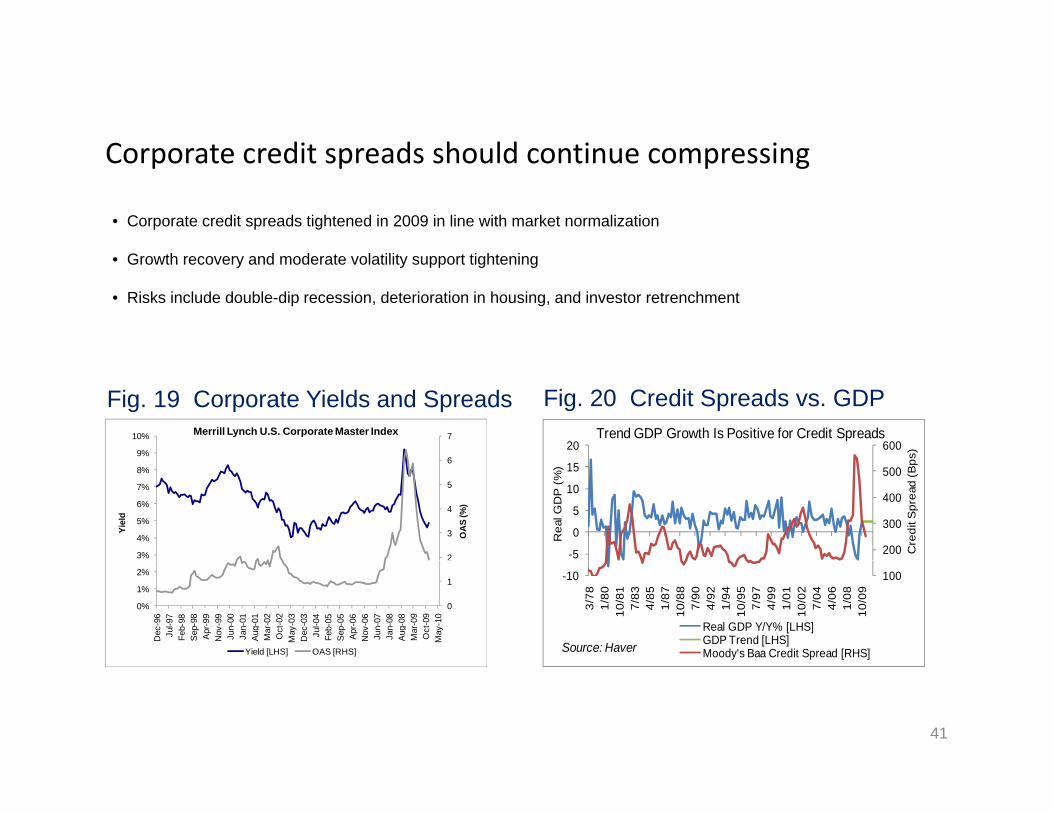

Corporate credit spreads should continue compressing

• Corporate credit spreads tightened in 2009 in line with market normalization

Corporate credit spreads should continue compressing

• Growth recovery and moderate volatility support tightening

• Risks include double-dip recession, deterioration in housing, and investor retrenchment

Fig. 19 Corporate Yields and Spreads Fig. 20 Credit Spreads vs. GDP

6

7

9%

10% Merrill Lynch U.S. Corporate Master Index60020

s)

Trend GDP Growth Is Positive for Credit Spreads

2

3

4

5

6

3%

4%

5%

6%

7%

8%O

AS

(%)

Yiel

d

200

300

400

500

-5

0

5

10

15

Cre

dit S

prea

d (B

ps

Rea

l GD

P (

%)

0

1

0%

1%

2%

Dec

-96

Jul-9

7Fe

b-98

Sep

-98

Apr-9

9N

ov-9

9Ju

n-00

Jan-

01A

ug-0

1M

ar-0

2O

ct-0

2M

ay-0

3D

ec-0

3Ju

l-04

Feb-

05S

ep-0

5Ap

r-06

Nov

-06

Jun-

07Ja

n-08

Aug

-08

Mar

-09

Oct

-09

May

-10

Yield [LHS] OAS [RHS]

100-103/

781/

8010

/81

7/83

4/85

1/87

10/8

87/

904/

921/

9410

/95

7/97

4/99

1/01

10/0

27/

044/

061/

0810

/09

Real GDP Y/Y% [LHS]GDP Trend [LHS]Moody's Baa Credit Spread [RHS]Source: Haver

41

Credit normalization driven by improving fundamentals

• Default rate projections suggest Moody’s Speculative Grade Default Rate peaking

Credit normalization driven by improving fundamentals

• Strong corporate balance sheets with negative financing gap

• Favorable technicals - high grade gross supply to fall

Fig. 21 Corporate Cash/Assets Fig. 22 Projected Corporate Issuance

13%

14% S&P 500 Balance Sheets Are Strong

160

1801,200U.S. Corporate Debt Gross Issuance

8%

9%

10%

11%

12%

13%

%

60

80

100

120

140

160

400

600

800

1,000

U.S

. Mil.

U.S

. Mil.

5%

6%

7%

03/0

008

/00

01/0

106

/01

11/0

104

/02

09/0

202

/03

07/0

312

/03

05/0

410

/04

03/0

508

/05

01/0

606

/06

11/0

604

/07

09/0

702

/08

07/0

812

/08

05/0

910

/09

03/1

0

Cash & Short Term Investments/Total Assets 4QMASource: FactSet

0

20

40

0

200

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

High Grade [LHS] HG Forecast [RHS] High Yield [RHS] HY Forecast [RHS]

42

Weak municipal fundamentals will be somewhat offset byWeak municipal fundamentals will be somewhat offset by supportive technicals

• Municipal revenues have fallen sharply

• Fundamentals and ratings trends remain negative in the municipal market with headline and downgrade risk remaining elevated in 2010

• Spread levels should be sustained with favorable technicals for tax-exempt securities – inflow of money into municipal funds and shift towards BABs supply

8

9

1.4

1.5

Fig. 23 Muni to Treasury Ratio Fig. 24 GDP vs. State Tax Revenue

4

5

6

7

8

10 Y

ear R

ates

%

0 8

0.9

1

1.1

1.2

1.3

1.4M

uni t

o TS

Y R

atio

2

3

1/10

/92

1/10

/93

1/10

/94

1/10

/95

1/10

/96

1/10

/97

1/10

/98

1/10

/99

1/10

/00

1/10

/01

1/10

/02

1/10

/03

1/10

/04

1/10

/05

1/10

/06

1/10

/07

1/10

/08

1/10

/09

1/10

/10

0.6

0.7

0.8

3M Rolling 10 Yr UST Rate LHS 3M Rolling 10 Yr Muni to TSY Ratio RHS

43

Source: Rockefeller Institute.Source: Bloomberg

Hi h G d CMBS d h ld ti t i d t itiHigh Grade CMBS spreads should continue to improve due to positive technicals

• CRE and CMBS fundamentals will continue to deteriorate in the coming months.

• However, tight spreads and light supply should provide a solid tone to high grade CMBS spreads.

• Despite tighter credit spreads, growth of CRE borrowing / financing is small. Market participants are, however, expecting the whole loan market to increase in activity by 2H10.

Fig. 25 CMBS Spreads

400

600

800

1,000

HG CMBS Spreads are still elevated relative to HG Corporates

0

200

400

AAA CMBS IG CDS

44

AAA CMBS IG CDS

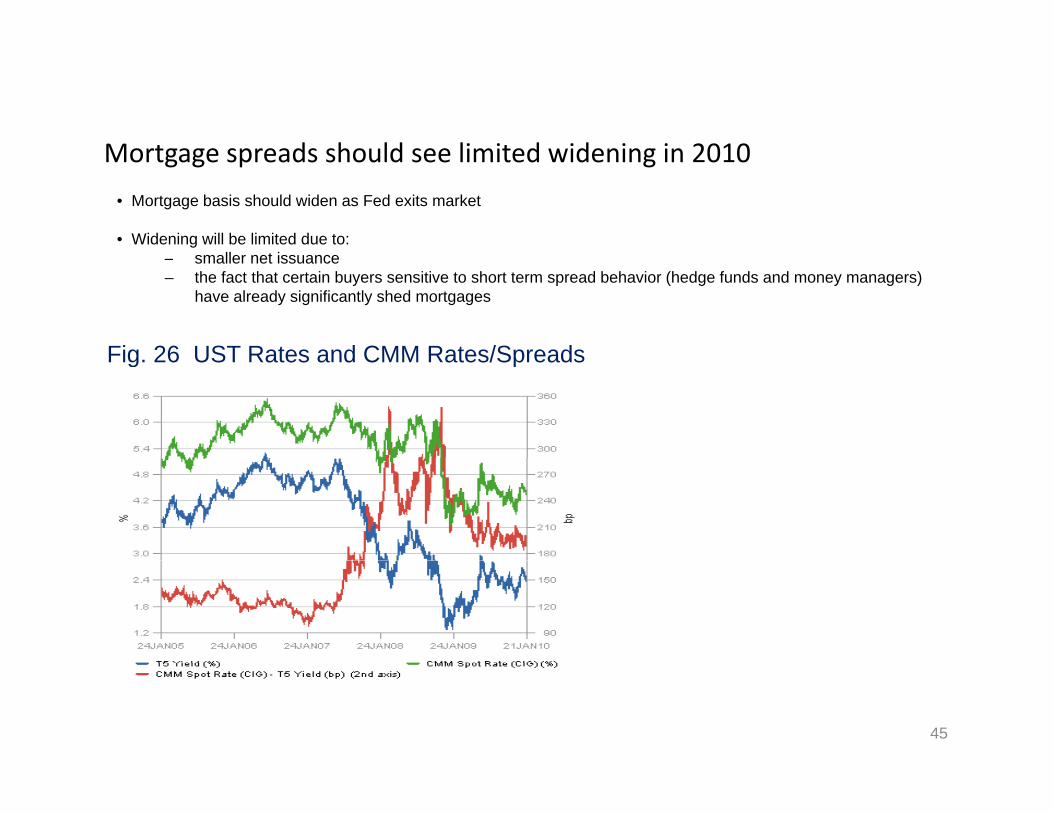

Mortgage spreads should see limited widening in 2010Mortgage spreads should see limited widening in 2010

• Mortgage basis should widen as Fed exits market

• Widening will be limited due to:ll t i– smaller net issuance

– the fact that certain buyers sensitive to short term spread behavior (hedge funds and money managers) have already significantly shed mortgages

Fig 26 UST Rates and CMM Rates/SpreadsFig. 26 UST Rates and CMM Rates/Spreads

45

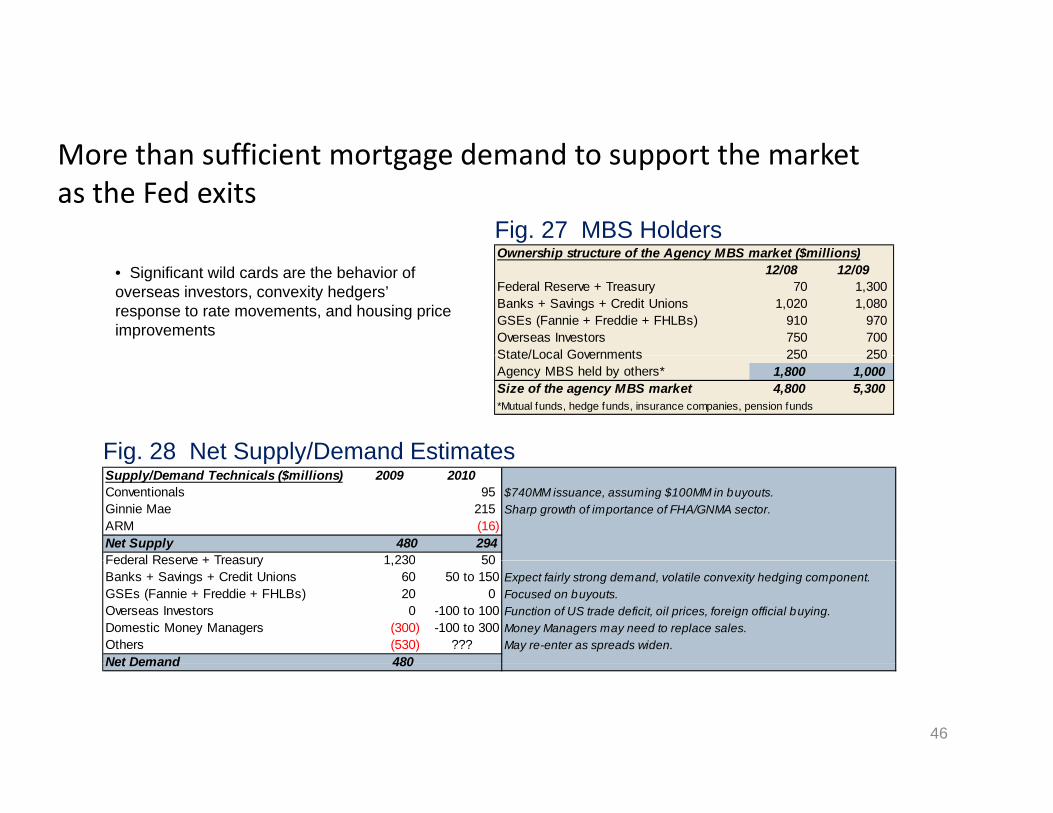

More than sufficient mortgage demand to support the marketMore than sufficient mortgage demand to support the market as the Fed exits

Fig. 27 MBS HoldersOwnership structure of the Agency MBS market ($millions)

• Significant wild cards are the behavior of overseas investors, convexity hedgers’ response to rate movements, and housing price improvements

Ownership structure of the Agency MBS market ($millions)12/08 12/09

Federal Reserve + Treasury 70 1,300Banks + Savings + Credit Unions 1,020 1,080GSEs (Fannie + Freddie + FHLBs) 910 970Overseas Investors 750 700State/Local Governments 250 250

Fig. 28 Net Supply/Demand Estimates

State/Local Governments 250 250Agency MBS held by others* 1,800 1,000Size of the agency MBS market 4,800 5,300*Mutual funds, hedge funds, insurance companies, pension funds

Supply/Demand Technicals ($millions) 2009 2010Conventionals 95 $740MM issuance, assuming $100MM in buyouts.Ginnie Mae 215 Sharp growth of importance of FHA/GNMA sector.ARM (16)Net Supply 480 294Federal Reserve + Treasury 1 230 50

Fig. 28 Net Supply/Demand Estimates

Federal Reserve + Treasury 1,230 50Banks + Savings + Credit Unions 60 50 to 150 Expect fairly strong demand, volatile convexity hedging component.GSEs (Fannie + Freddie + FHLBs) 20 0 Focused on buyouts.Overseas Investors 0 -100 to 100 Function of US trade deficit, oil prices, foreign official buying.Domestic Money Managers (300) -100 to 300 Money Managers may need to replace sales.Others (530) ??? May re-enter as spreads widen.Net Demand 480

46

Net Demand 480