Presentation to the Saskatchewan Assessment Appraisers’ Association May 16, 2012.

29

Presentation to the Saskatchewan Assessment Appraisers’ Association May 16, 2012

-

Upload

richard-hancock -

Category

Documents

-

view

212 -

download

0

Transcript of Presentation to the Saskatchewan Assessment Appraisers’ Association May 16, 2012.

Presentation

to the

Saskatchewan Assessment Appraisers’

Association

May 16, 2012

Appeals (2009 to 2011)

Regina Decisions

• 2 Court of Appeal decisions

• 18 SMB Committee decisions (57 properties)

• Numerous issues and principles

Appeals (2009 to 2011)

Onus

Assessor Discretion

Presumption of Correctness

Information Requests from Owners

Adjustments

Shortfall

Non-Recoverable Expenses

Capitalization Rates

Notice of Appeal

Grounds of Appeal

Record of Appeal

Expert Witness

Evidence

Market Data

Market Valuation Standard

Market Value Handbook

Typical v. Actual

Mass Appraisal Methodology

Authorities

Appraisal Practices

Units of Comparison

Time-Adjusting Sales

Weighting

Industry Norms

Appeals (2009 to 2011)

Onus

Assessor Discretion

Presumption of Correction

Information Requests from Owners

Adjustments

Shortfall

Non-Recoverable Expenses

Capitalization RatesNotice of Appeal

Grounds of Appeal

Record of Appeal

Expert Witness

Evidence

Market Data

Market Valuation Standard

Market Value Handbook

Typical v. ActualMass Appraisal Methodology

Authorities

Appraisal PracticesUnits of Comparison

Time-Adjusting Sales

Weighting

Industry Norms

Appeals (2009 to 2011)

Significant Points and Key Principles

• Market Value Assessment Handbook (31)

• Onus (23)

• Assessor Discretion (28)

• Typical v. Actual (9)

• Market Data (5)

Market Value Handbook

The Canada Life Assurance Company v. Regina (City) (SMB 2009-0016)

[35] The Committee accepts that assessors are not required to follow the

methodology in any of these publications for non-regulated properties. However, as

SAMA has the mandate to provide the framework for the valuation of real property for

property tax purposes, it is reasonable for the public, the reviewing tribunals and the

courts to expect that the methodologies identified in the publications will be used

as presented. Additionally, the Committee accepts that an assessor may move to

other methods at any time, but acting in good faith as a professional with the

responsibility of reporting his or her findings to the public, the reviewing tribunals and

the court, the Committee expects that the assessor should disclose and be

prepared to explain the basis and support for deviation whenever such a move

is made.

Market Value Handbook

The Canada Life Assurance Company v. Regina (City) (SMB 2009-0016)

[35] The Committee accepts that assessors are not required to

follow the methodology …. However … it is reasonable … to expect

that the methodologies … will be used as presented …. the

Committee expects that the assessor should disclose and be

prepared to explain the basis and support for deviation whenever

such a move is made.

Market Value Handbook

The Canada Life Assurance Company v. Regina (City) (SMB 2009-0016)

[46] The Committee notes the following guidance as provided in the

Office Building Section of the Handbook as found at page 26:

…

In the Committee’s view this direction is clear …

Market Value Handbook

Chainlink Enterprises Limited et al v. Regina (City) (SMB 2009-0026)

[24] … the previous Manual was silent on the use of …. This is

not so for the current Handbook as the direction provided by it

expressly provides for the use of … at page 15 of section 3.3 where

it states ...

Market Value Handbook

Points to remember …

• Committee views Handbook similar to Manual

• Assessor must explain and support any deviation from direction

in Handbook

• If no support … must use Handbook

Onus

614630 Saskatchewan Ltd. et al v. Regina (City) (SMB 2009-0033)

[15] It is up to the appellant to prove that the assessor had erred …

not for the assessor to prove that he was correct.

Onus

The Canada Life Assurance Company v. Regina (City) (SMB 2009-0016)

[52] The onus is on the appellant to draw all important documents to

the Board’s attention and to establish relevancy of the documents to

the issues at hand.

Onus

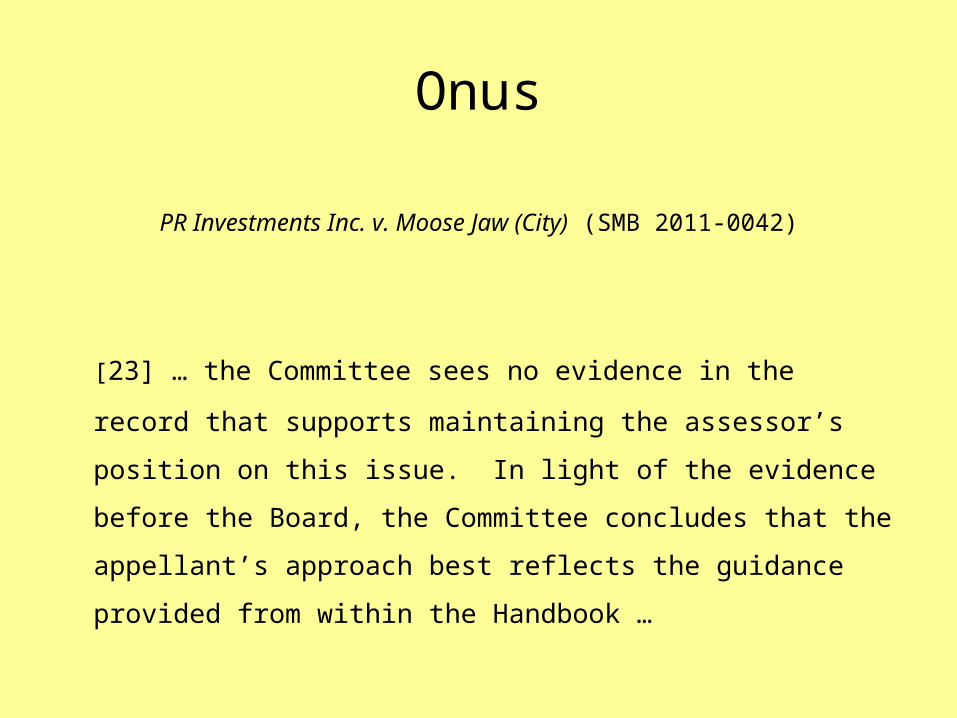

PR Investments Inc. v. Moose Jaw (City) (SMB 2011-0042)

[23] … the Committee sees no evidence in the record that supports

maintaining the assessor’s position on this issue. In light of the

evidence before the Board, the Committee concludes that the

appellant’s approach best reflects the guidance provided from within

the Handbook …

Onus

RM of Corman Park No. 344 v. Peter and Maureen Coad (SMB 2009-0100)

[20] The Committee notes that [the assessor] maintains a …

property sales database in its computer. One would think that … it

would take little effort to code … sites and abutting sites so a sales

analysis could be completed to determine whether a property … has

suffered a loss in value…. Completion of this type of sales analysis

would assist all parties … to better understand the impact, if any …

on property values.

Onus

Points to remember …

• Onus still rests (initially) with Appellant

• Onus on Appellant to show relevancy of supporting documents

• Onus can shift to Assessor if error proven

• Onus on Assessor to do proper research and explain assessment

Assessor Discretion

Acklands Limited v. Swift Current (City) (SMB 2011-0092)

[11] [quoting 959630 Alberta Inc. 2010 SKCA 136] The Court goes on to

point out that an appellate body cannot “overturn an assessor’s

discretion merely on the basis that the appellate body considers

other factors more relevant, or other properties more comparable,

than those determined by the Assessor.”

Assessor Discretion

Manitou Springs Hotel Inc. v. Manitou Beach (Resort Village) (SMB 2011-0046)

[49] [quoting Sasco Developments 2000 SKCA 90] “… It is not open to

an assessor to interpret or apply one term of the manual … in a way

that makes other terms of the manual unworkable, so as to avoid

what he sees to be an undesirable result. That is an abuse of

discretion, rather than a valid exercise of it.”

Assessor Discretion

Manitou Springs Hotel Inc. v. Manitou Beach (Resort Village) (SMB 2011-0046)

[50] The discretionary powers afforded the assessor by the Court, is

not absolute. The Court is clear in stating the assessed value

resulting from the assessor in applying his discretion can not

produce an undesirable result.

Assessor Discretion

PR Investments Inc. v. Moose Jaw (City) (SMB 2011-0042)

[25] The Committee recognizes there is a presumption of

correctness for the assessment as calculated. In the Committee’s

view, however, deference can only be given where there are equally

plausible positions.

Assessor Discretion

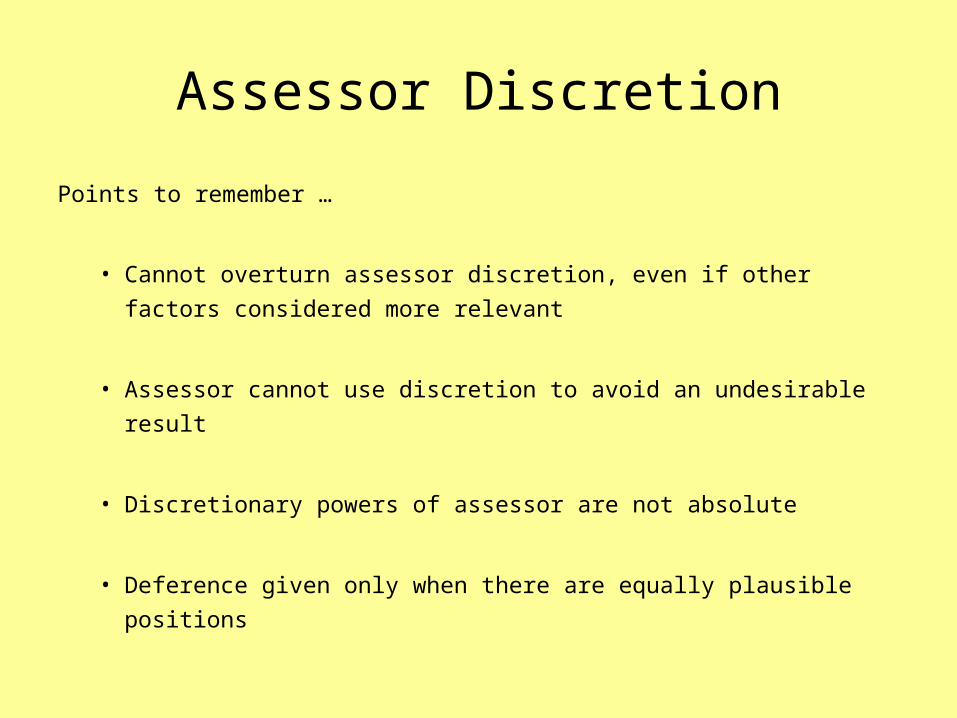

Points to remember …

• Cannot overturn assessor discretion, even if other factors

considered more relevant

• Assessor cannot use discretion to avoid an undesirable result

• Discretionary powers of assessor are not absolute

• Deference given only when there are equally plausible positions

Typical v. Actual

Sasco Developments v. Moose Jaw (City) [2012 SKCA 24]

[50] … it was not open to the [Assessor] to estimate the market

value of the … property based in general on “its own income and

expenses.” This would amount, in effect, to single property

appraisal, using single property appraisal techniques.

Typical v. Actual

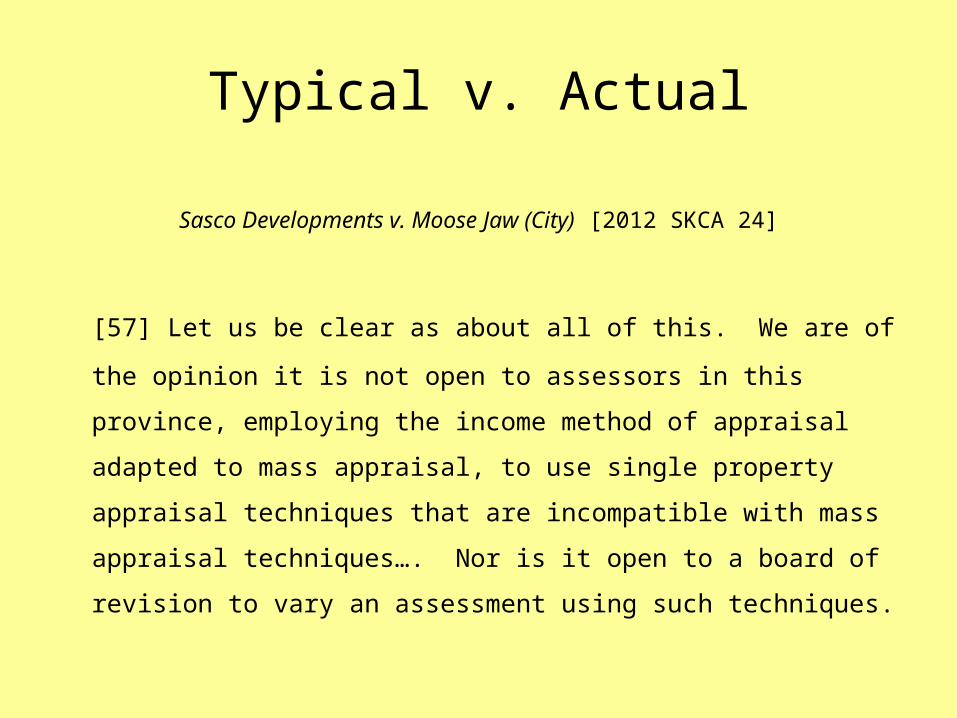

Sasco Developments v. Moose Jaw (City) [2012 SKCA 24]

[57] Let us be clear as about all of this. We are of the opinion it is

not open to assessors in this province, employing the income

method of appraisal adapted to mass appraisal, to use single

property appraisal techniques that are incompatible with mass

appraisal techniques…. Nor is it open to a board of revision to vary

an assessment using such techniques.

Typical v. Actual

Various c/o Altus Group Limited v. Regina (City) (SMB 2010-0026 et al)

[29] … the Committee questions whether the use of actual income

and expense information being generated by a specific property to

develop a capitalization rate which is then used to determine

assessed values, would meet the criteria expressed for the “market

valuation standard.” Specifically, it appears to the Committee that

the requirement that the assessed value reflect the estate in fee

simple has been disregarded with this calculation .

Typical v. Actual

Points to remember …

• Cannot value a property using its own rents, income, expenses, etc. –

amounts to single property appraisal

• Assessor cannot use single property appraisal techniques

• A Board of Revision cannot vary an assessment using single property

appraisal techniques

Market Data

614630 Saskatchewan Ltd. et al v. Regina (City) (SMB 2009-0033)

[27] Any further adjustment must be supported by market derived

data that is statistically significant and single point comparisons from

a subset of the data do not present that significance.

Market Data

The Canada Life Assurance Company v. Regina (City) (SMB 2009-0016)

[37] The Committee accepts the assessor’s calculation … on the

basis that the evidence heard by the Board was that the calculation

of this adjustment was based upon income and expense analysis

completed by the assessor in conjunction with interviews and

discussions with local property owners. The Committee agrees with

the assessor that this is the most appropriate process to follow in

order to establish and support an adjustment. .

Market Data

Points to remember …

• Adjustments must be supported by statistically significant market

data

• Speaking with property owners substantiates an appropriate

process to follow in supporting adjustments

Court of Appeal

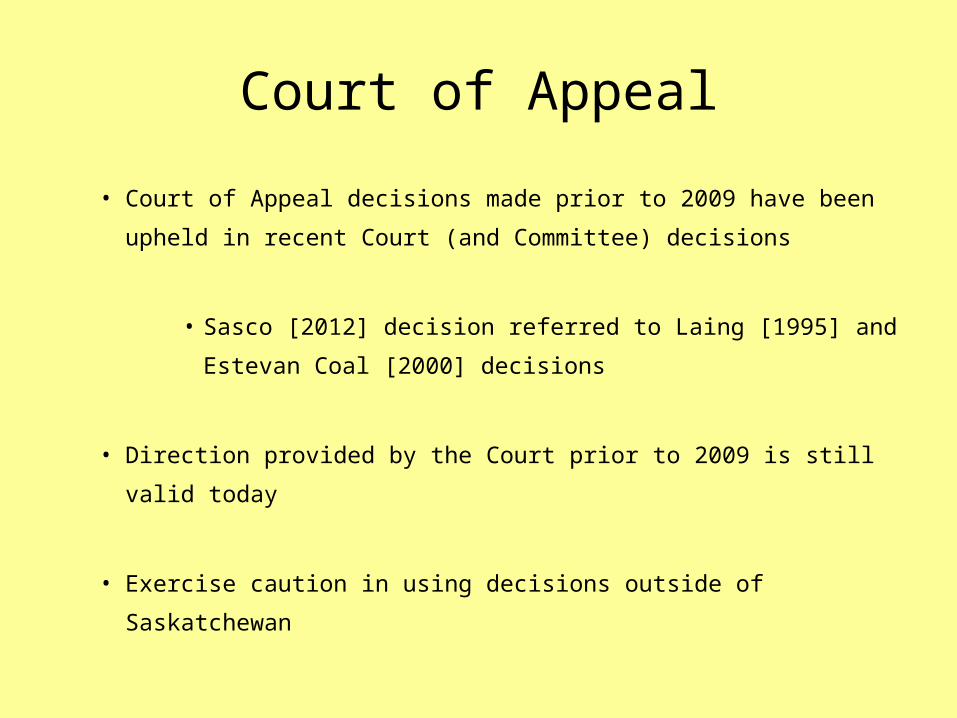

• Court of Appeal decisions made prior to 2009 have been upheld

in recent Court (and Committee) decisions

• Sasco [2012] decision referred to Laing [1995] and

Estevan Coal [2000] decisions

• Direction provided by the Court prior to 2009 is still valid today

• Exercise caution in using decisions outside of Saskatchewan

Court of Appeal

Sasco Developments v. Moose Jaw (City) [2012 SKCA 24]

[56] Decisions from other jurisdictions can be helpful to a better

understanding of things, but assessment schemes vary from

province to province in one respect or another, making it imperative

to pay close attention to the legislation underlying these decisions

so as not to import ideas that are incompatible with the assessment

scheme in place in this province.