Presentation on SA Automotive Sector

21

1 9 June 2015 PPC PRESENTATION: AUTOMOTIVES EDD Parliamentary Portfolio Committee Presentation on SA Automotive Sector Department of Trade and Industry

-

Upload

nguyenduong -

Category

Documents

-

view

220 -

download

4

Transcript of Presentation on SA Automotive Sector

1

9 June 2015 PPC PRESENTATION: AUTOMOTIVES

EDD Parliamentary Portfolio Committee

Presentation on SA Automotive Sector

Department of Trade and Industry

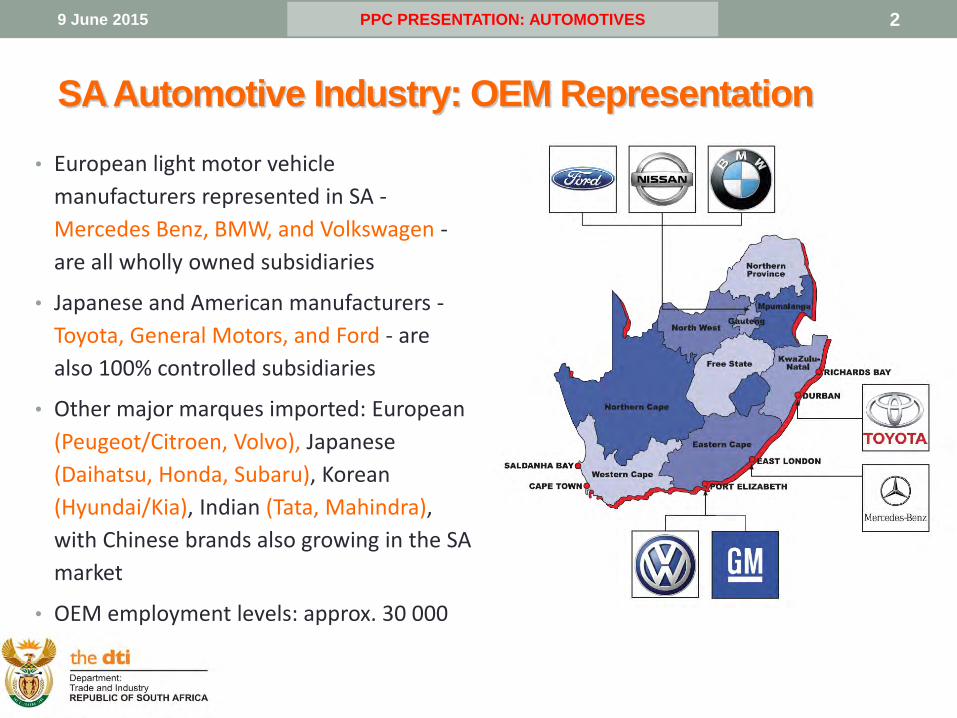

2 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

SA Automotive Industry: OEM Representation

• European light motor vehicle

manufacturers represented in SA -

Mercedes Benz, BMW, and Volkswagen -

are all wholly owned subsidiaries

• Japanese and American manufacturers -

Toyota, General Motors, and Ford - are

also 100% controlled subsidiaries

• Other major marques imported: European

(Peugeot/Citroen, Volvo), Japanese

(Daihatsu, Honda, Subaru), Korean

(Hyundai/Kia), Indian (Tata, Mahindra),

with Chinese brands also growing in the SA

market

• OEM employment levels: approx. 30 000

3 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

SA Automotive Industry:

Component Manufacturing

• Widespread base of auto component suppliers including global first tier suppliers such as Faurecia, Johnson Controls, Mothersons, Yazaki, Sumitomo, Bosch and Behr

• 120 1st tier suppliers, 75% of them multinationals

• Over 200 2nd and 3rd tier suppliers, mostly local

• Supplier Employment Level approximately 80 000 in 2014 :

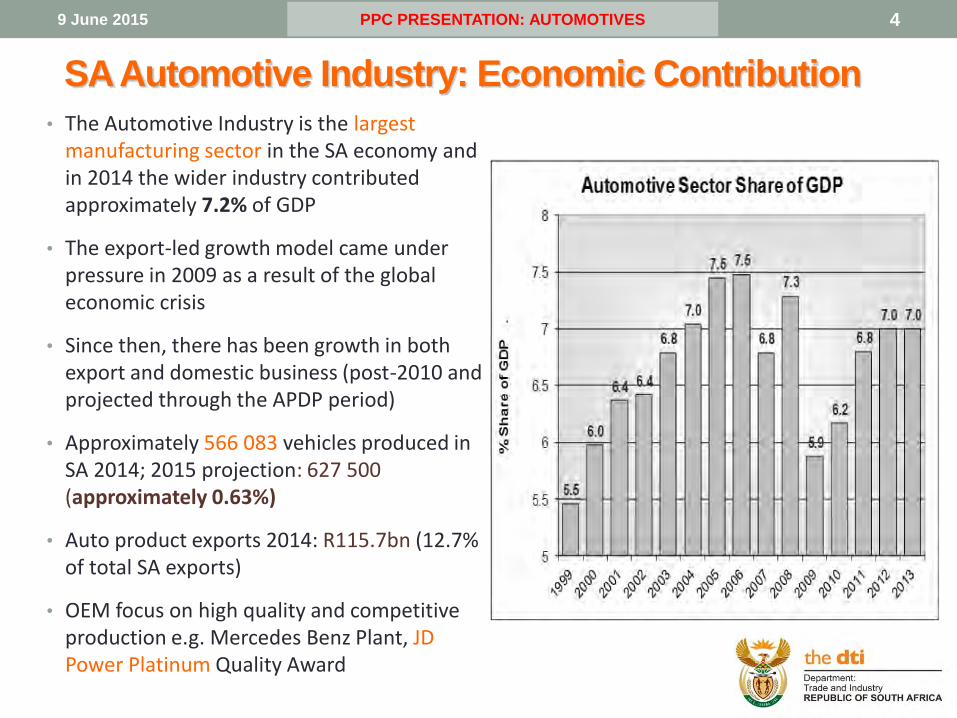

4 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

SA Automotive Industry: Economic Contribution

• The Automotive Industry is the largest manufacturing sector in the SA economy and in 2014 the wider industry contributed approximately 7.2% of GDP

• The export-led growth model came under pressure in 2009 as a result of the global economic crisis

• Since then, there has been growth in both export and domestic business (post-2010 and projected through the APDP period)

• Approximately 566 083 vehicles produced in SA 2014; 2015 projection: 627 500 (approximately 0.63%)

• Auto product exports 2014: R115.7bn (12.7% of total SA exports)

• OEM focus on high quality and competitive production e.g. Mercedes Benz Plant, JD Power Platinum Quality Award

5 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

Major SA Automotive Exports

• OEMS • Nissan – 1-ton pickup into Africa

• Volkswagen - Polo series to EU

• BMW – 3 Series to Japan, Australia and USA

• Mercedes Benz – C Class

• Toyota - Corolla/Hilux to EU and Africa

• Components (Quoted in R million) – See table

• Major export destinations: EU, Africa, USA, Brazil, Japan, followed by Australia, S Korea, India and China

Component (R m) 1995 2000 2013 2014

Catalytic Converters 389 4 683 17 620 19 479

Seats, Stitched Leather 1 019 1 915 1 524 1 277

Engines and Parts 111 485 2 938 3 491

Tyres 213 682 1 215 1 531

Silencers/Exhausts 76 377 1 214 497

Radiators 55 127 1 088 1 144

Wheels 157 551 413 331

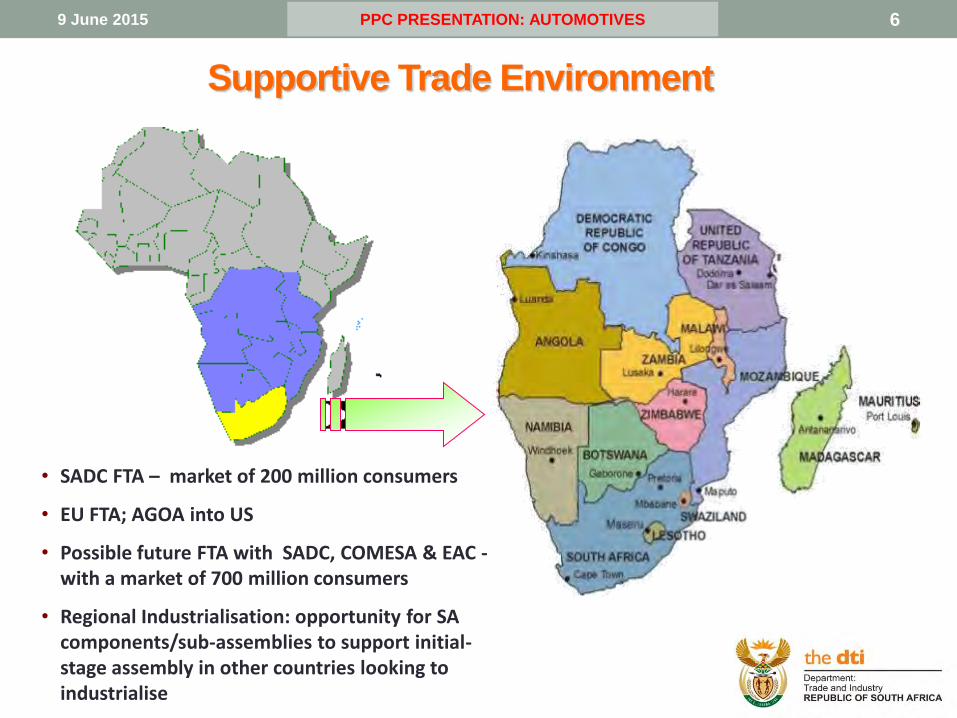

6 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

Supportive Trade Environment

• SADC FTA – market of 200 million consumers

• EU FTA; AGOA into US

• Possible future FTA with SADC, COMESA & EAC - with a market of 700 million consumers

• Regional Industrialisation: opportunity for SA components/sub-assemblies to support initial-stage assembly in other countries looking to industrialise

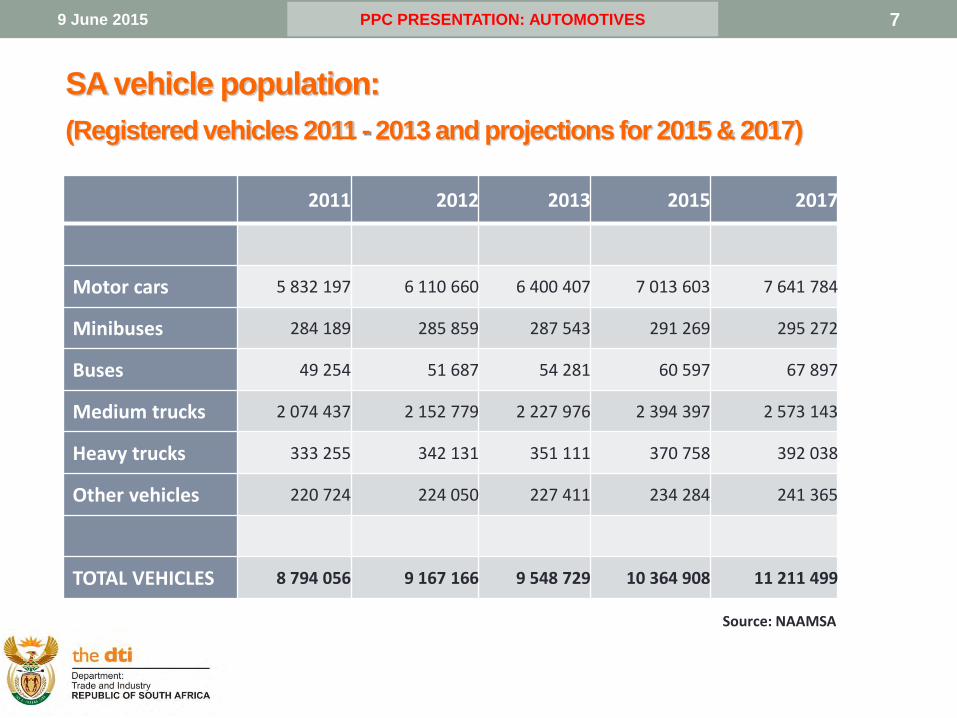

7 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

SA vehicle population:

(Registered vehicles 2011 - 2013 and projections for 2015 & 2017)

2011 2012 2013 2015 2017

Motor cars 5 832 197 6 110 660 6 400 407 7 013 603 7 641 784

Minibuses 284 189 285 859 287 543 291 269 295 272

Buses 49 254 51 687 54 281 60 597 67 897

Medium trucks 2 074 437 2 152 779 2 227 976 2 394 397 2 573 143

Heavy trucks 333 255 342 131 351 111 370 758 392 038

Other vehicles 220 724 224 050 227 411 234 284 241 365

TOTAL VEHICLES 8 794 056 9 167 166 9 548 729 10 364 908 11 211 499

Source: NAAMSA

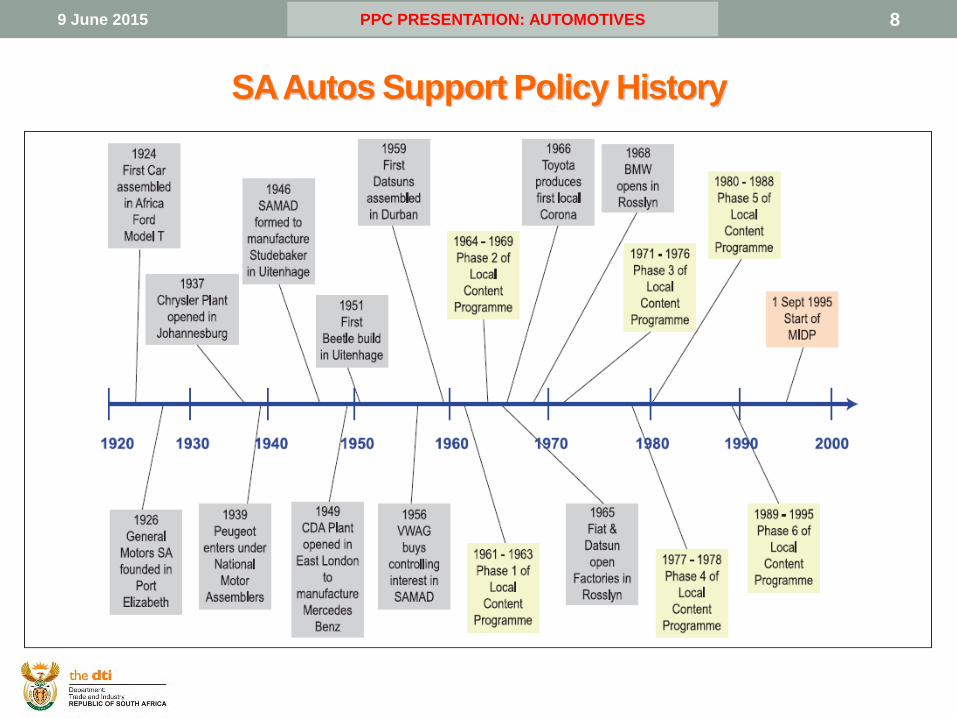

8 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

SA Autos Support Policy History

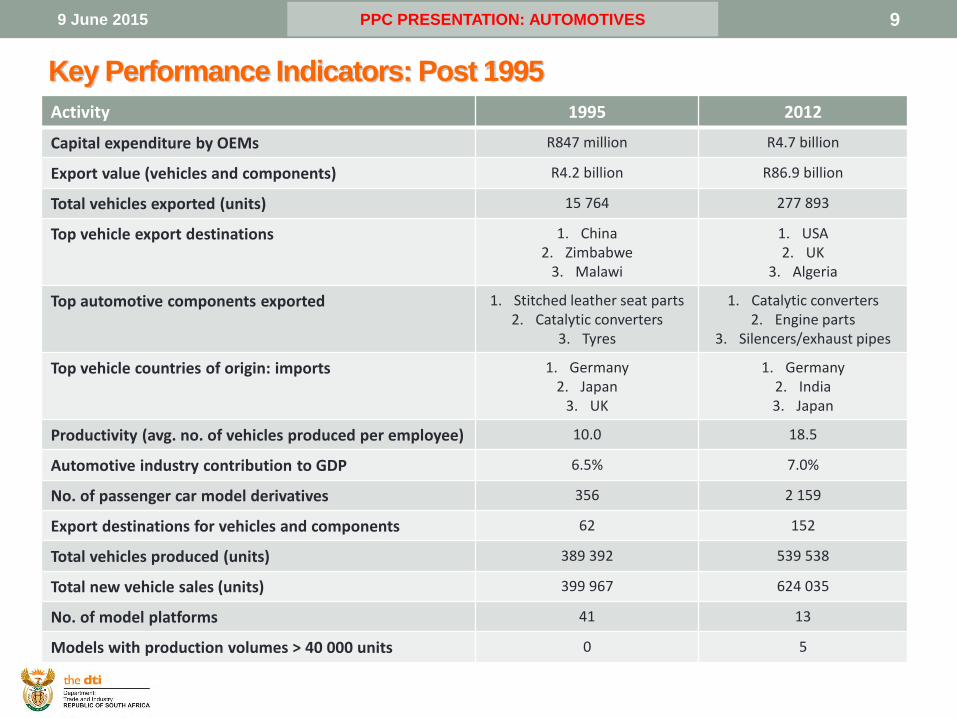

9 June 2015 PPC PRESENTATION: AUTOMOTIVES 9

Key Performance Indicators: Post 1995

Activity 1995 2012

Capital expenditure by OEMs R847 million R4.7 billion

Export value (vehicles and components) R4.2 billion R86.9 billion

Total vehicles exported (units) 15 764 277 893

Top vehicle export destinations 1. China 2. Zimbabwe

3. Malawi

1. USA 2. UK

3. Algeria

Top automotive components exported 1. Stitched leather seat parts 2. Catalytic converters

3. Tyres

1. Catalytic converters 2. Engine parts

3. Silencers/exhaust pipes

Top vehicle countries of origin: imports 1. Germany 2. Japan

3. UK

1. Germany 2. India 3. Japan

Productivity (avg. no. of vehicles produced per employee) 10.0 18.5

Automotive industry contribution to GDP 6.5% 7.0%

No. of passenger car model derivatives 356 2 159

Export destinations for vehicles and components 62 152

Total vehicles produced (units) 389 392 539 538

Total new vehicle sales (units) 399 967 624 035

No. of model platforms 41 13

Models with production volumes > 40 000 units 0 5

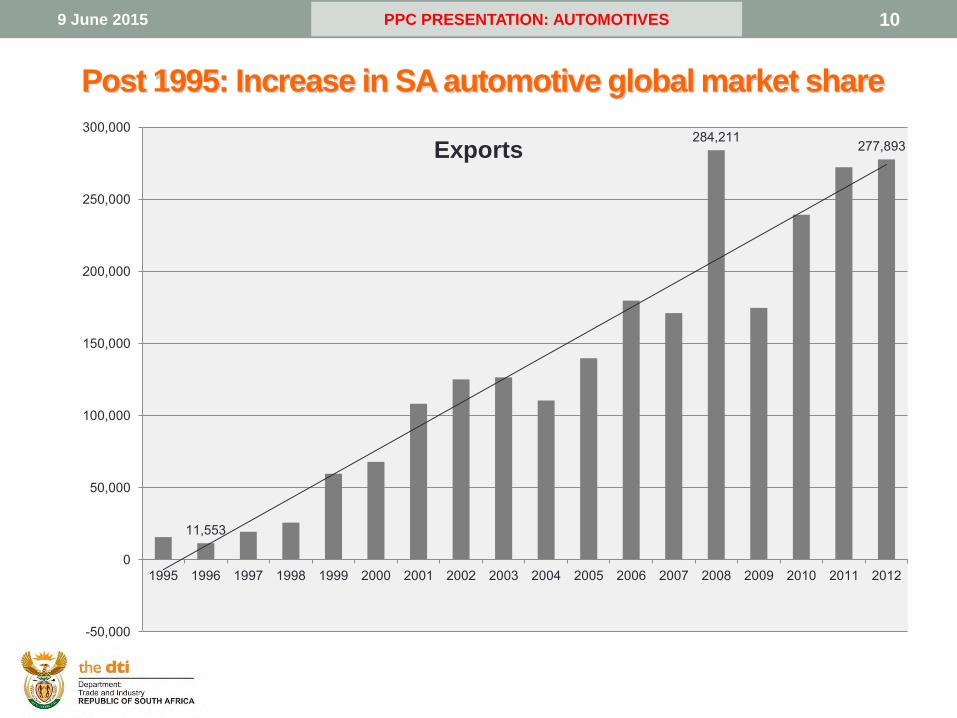

10 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

Post 1995: Increase in SA automotive global market share

11,553

284,211 277,893

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Exports

11 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

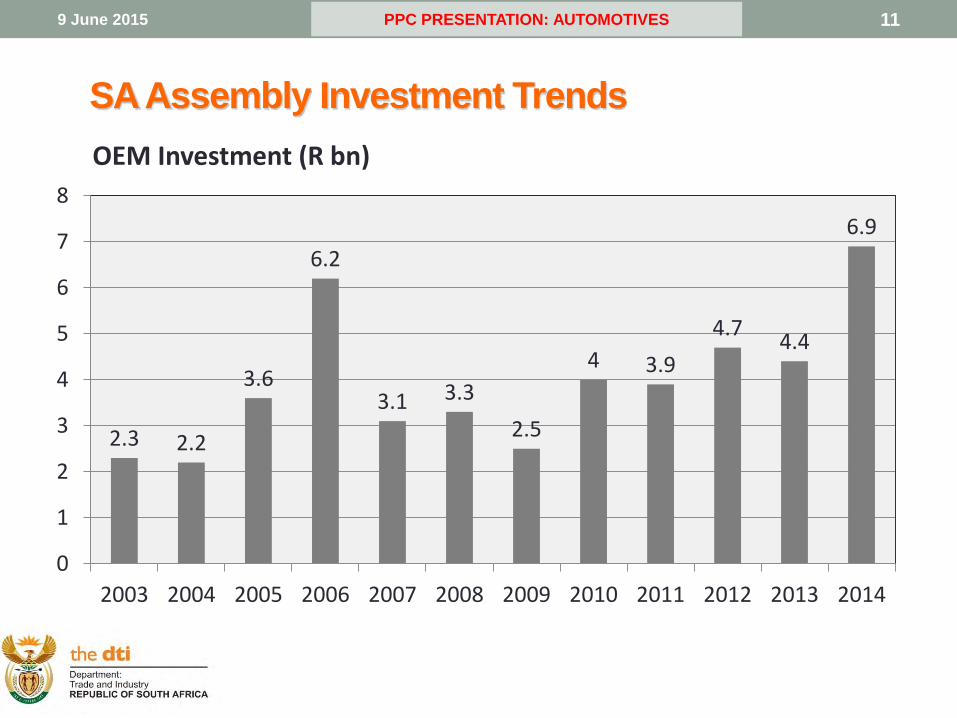

SA Assembly Investment Trends

2.3 2.2

3.6

6.2

3.1 3.3

2.5

4 3.9

4.7 4.4

6.9

0

1

2

3

4

5

6

7

8

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

OEM Investment (R bn)

12 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

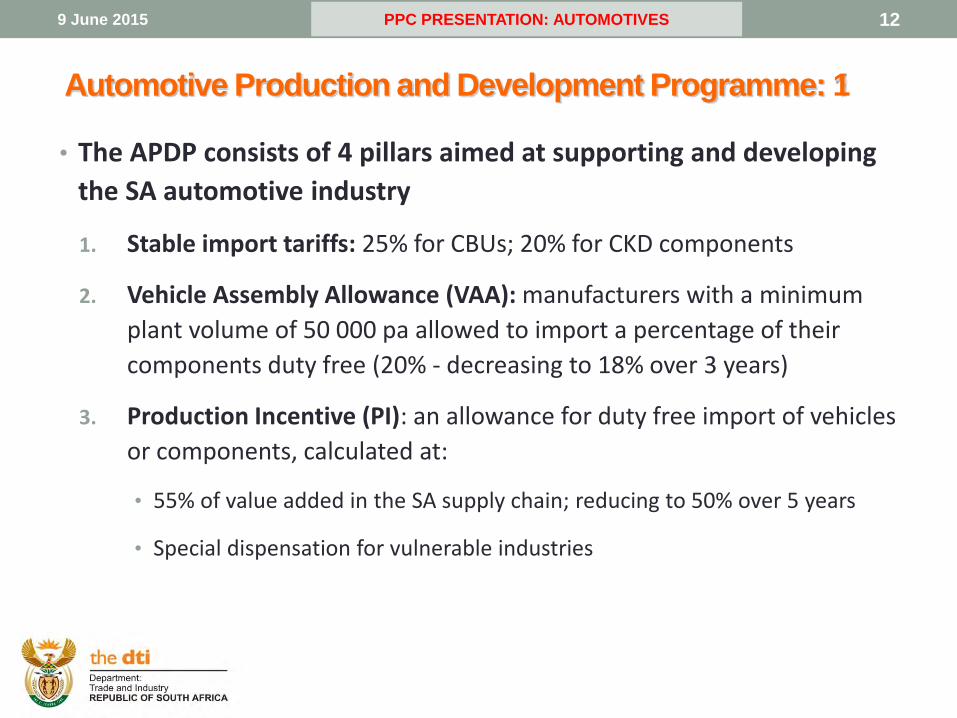

Automotive Production and Development Programme: 1

• The APDP consists of 4 pillars aimed at supporting and developing

the SA automotive industry

1. Stable import tariffs: 25% for CBUs; 20% for CKD components

2. Vehicle Assembly Allowance (VAA): manufacturers with a minimum

plant volume of 50 000 pa allowed to import a percentage of their

components duty free (20% - decreasing to 18% over 3 years)

3. Production Incentive (PI): an allowance for duty free import of vehicles

or components, calculated at:

• 55% of value added in the SA supply chain; reducing to 50% over 5 years

• Special dispensation for vulnerable industries

13 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

4. Automotive Investment Scheme (AIS)

Purposes:

• To stimulate investment and job creation in SA’s automotive sector - in particular:

• Investment in technologically advanced automotive production & new and

replacement models/components

• Increased plant production volumes

• Overall strengthening of the automotive value chain

Mechanisms:

• A non-taxable cash grant paid over 3 years with minimum benefit calculated at

20% for OEMs and 25% for suppliers

• An additional 5% and 10% benefit - subject to Economic Benefit criteria

• Available to OEMs and component suppliers

Automotive Production and Development Programme: 2

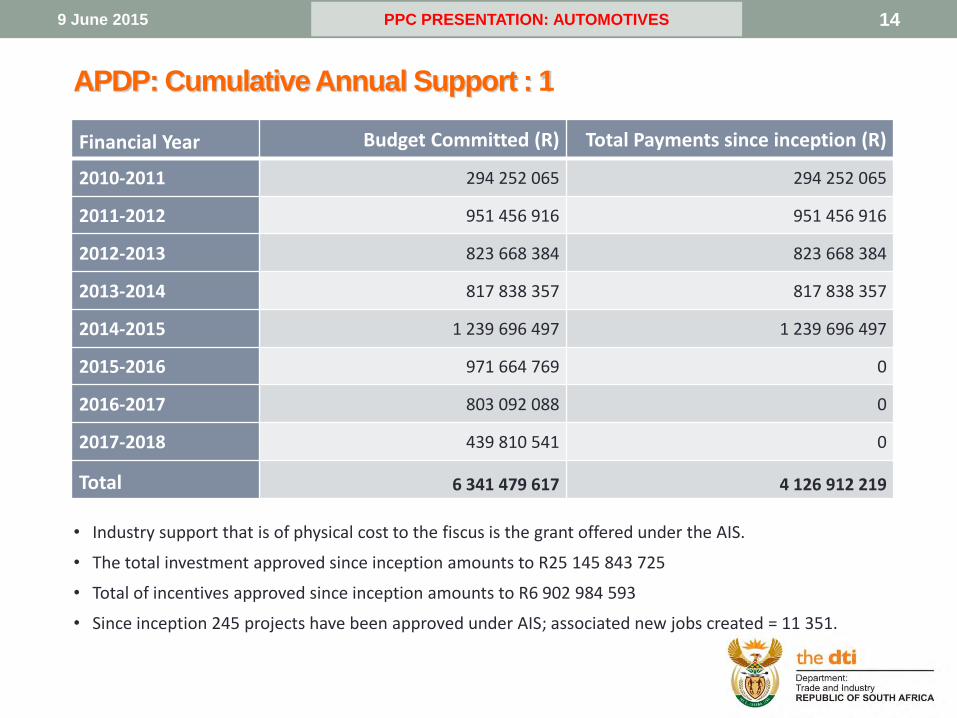

14 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

Financial Year Budget Committed (R) Total Payments since inception (R)

2010-2011 294 252 065 294 252 065

2011-2012 951 456 916 951 456 916

2012-2013 823 668 384 823 668 384

2013-2014 817 838 357 817 838 357

2014-2015 1 239 696 497 1 239 696 497

2015-2016 971 664 769 0

2016-2017 803 092 088 0

2017-2018 439 810 541 0

Total 6 341 479 617 4 126 912 219

• Industry support that is of physical cost to the fiscus is the grant offered under the AIS.

• The total investment approved since inception amounts to R25 145 843 725

• Total of incentives approved since inception amounts to R6 902 984 593

• Since inception 245 projects have been approved under AIS; associated new jobs created = 11 351.

APDP: Cumulative Annual Support : 1

15 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

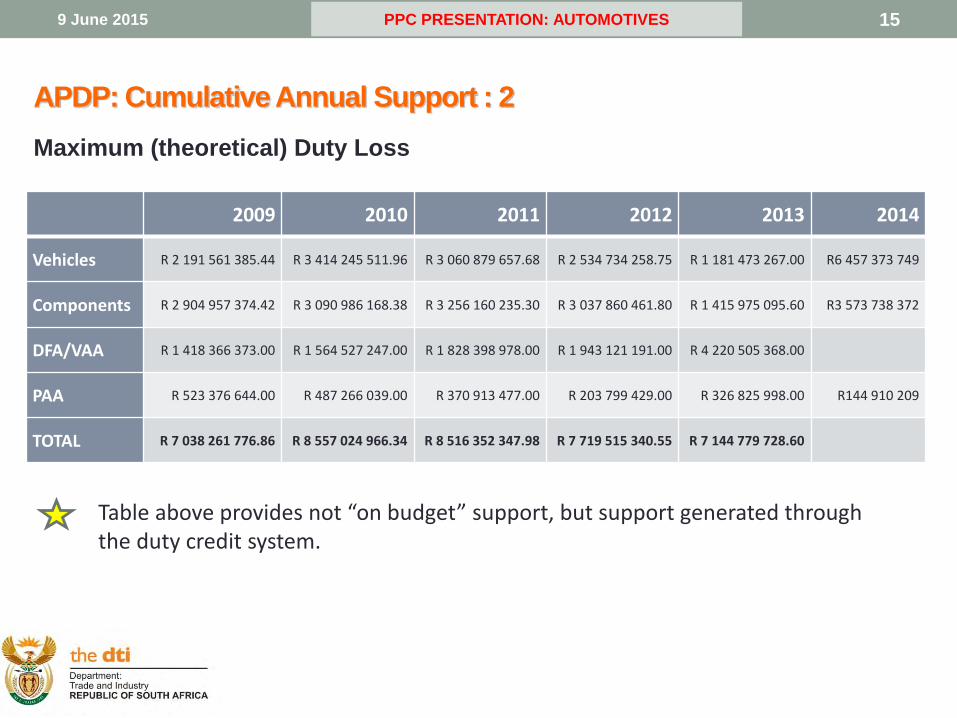

APDP: Cumulative Annual Support : 2

Maximum (theoretical) Duty Loss

2009 2010 2011 2012 2013 2014

Vehicles R 2 191 561 385.44 R 3 414 245 511.96 R 3 060 879 657.68 R 2 534 734 258.75 R 1 181 473 267.00 R6 457 373 749

Components R 2 904 957 374.42 R 3 090 986 168.38 R 3 256 160 235.30 R 3 037 860 461.80 R 1 415 975 095.60 R3 573 738 372

DFA/VAA R 1 418 366 373.00 R 1 564 527 247.00 R 1 828 398 978.00 R 1 943 121 191.00 R 4 220 505 368.00

PAA R 523 376 644.00 R 487 266 039.00 R 370 913 477.00 R 203 799 429.00 R 326 825 998.00 R144 910 209

TOTAL R 7 038 261 776.86 R 8 557 024 966.34 R 8 516 352 347.98 R 7 719 515 340.55 R 7 144 779 728.60

Table above provides not “on budget” support, but support generated through the duty credit system.

16 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

Policy Developments: 1

• Electric Vehicles and Green Production

• Finalisation of SA EV Roadmap: multi-departmental approach

Framework rests on two main pillars:

• Creating an environment in which electric vehicles can be operated on South African roads

• Supporting the development and production of electric vehicles and relevant EV components

• Supporting emerging regional production locations

• Other SSA countries looking to kick-start nascent auto industry

• Assembly in such countries presents opportunities for expanded SA supply chain developement in the short to medium term

17 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

• Medium Heavy Commercial Vehicle (MHCV) segment

• Significant MHCV opportunity:

• Encourage higher levels of localisation e.g. through Preferential

Procurement

• Support increased levels of R&D spend; encourage commercialisation

of R&D

• Support deepening of component manufacture

• Widen distribution and after-sales support in regional markets

• Review of APDP under way in consultation with all stakeholders -

in the context of maintaining policy certainty

Policy Developments: 2

18 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

Policy Developments: 3

• The present policy implementation in the MHCV segment has

facilitated an improved operating environment for the industry

• A number of positive developments have since emerged:

• Bus bodies have been designated for public procurement, further

catalysing local manufacturing

• The Automotive Investment Scheme (AIS) package has been

extended to people-carriers/mini-buses, trucks and buses

• Large new investments from companies like Iveco, Tata, BAW,

Toyota, FAW and Hyundai have recently been announced

19 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

Policy Developments: 4

• Strengthening the Supply Chain

• Auto Supply Chain Competitiveness Initiative (ASSCI)

• Collaboration between all major industry role-players

• Wide ranging, 3-year Business Plan activities - all aimed at competitiveness

improvement and supplier development

• Co-ordinating, measuring and targeting value-adding opportunities

20 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

SA Automotive Sector - Now and Beyond: 1

• Vision 2020

• Stimulate expansion of automotive vehicle production to 1.2

million vehicles p/a by 2020 - with associated deepening of the

components industry

(To be accomplished through long-term partnerships and

relationships built with the industry)

• Sector-specific Support Programmes - APDP and related:

• Encouraging higher levels of investment and value addition

• Support for firm- and industry-level competitiveness

improvement and supply chain development

21 9 June 2015 PPC PRESENTATION: AUTOMOTIVES

• Recent Investment Announcements:

• Mercedes Benz: R5bn

• General Motors: R1bn

• Ford: R3.6bn

• Metair Group: R400mill (2008-10)

• Johnson Controls: R380m

• Opportunities:

• Engine parts/components, vehicle interiors, electronic, drive train

components, body parts and exterior finishes, aluminium forgings

and castings (vis-à-vis OEM project-specific opportunities)

• Attract new vehicle assembly opportunities

SA Automotive Sector - Now and Beyond: 2