Presentation for BSE delhi road show 30.09.2016 w.r.t opportunities in IFSC at GIFT City

17

BSE Brokers meet on business prospects in IFSC at New Delhi Date: 30.09.2016 By Ashish Jhagarawat Director and CEO MOON SEZ Consultants Pvt Ltd Contact: +91 9373618577, email: [email protected]

-

Upload

ashish-jhagarawat -

Category

Economy & Finance

-

view

28 -

download

0

Transcript of Presentation for BSE delhi road show 30.09.2016 w.r.t opportunities in IFSC at GIFT City

BSE Brokers meet on business prospects in

IFSC at New Delhi Date: 30.09.2016

By Ashish Jhagarawat Director and CEO

MOON SEZ Consultants Pvt Ltd Contact: +91 9373618577, email: [email protected]

Agenda for this evening

1 Regulatory framework • What is SEZ? • What is IFSC? And Salient features of IFSC • Progress made so far • Comparison between tax incentives of SEZ & IFSC

2 What is there for Capital Markets Intermediaries • Types of Intermediaries allowed • Permissible securities • Nature of clients • Approval process

3 Business Opportunities • Business Opportunities from IFSC in India • Questions

The biggest risk in Life is “Not to take

any risk at all”

Regulatory Framework

01

What is SEZ?

• SEZ is a specially designated duty free enclave deemed to be a foreign territory for the purpose of trade operations, duties and tariffs.

• A Special Economic Zone (SEZ) is a geographical region that has economic laws more liberal than rest of the country’s general economic laws.

• SEZ Act and Rules were framed to attract foreign investments into India, encourage exports from India to bring in more and more foreign exchange into India.

• All Goods and services supplied from Domestic Tariff Area (DTA) to SEZ are treated as exports and all Goods and services supplied by SEZ units to Domestic Tariff Area (DTA) are treated as imports into India and subject to all procedures and rules applicable in case of normal imports into India.

• SEZ’s are deemed to be a airport, port, Land Custom stations, and Inland container depot under the Customs Act.

• SEZ Developers/Co-developers/Units are entitled for various fiscal/Non Fiscal incentives and benefits as per SEZ Act and Rules.

• Manufacturing, Servicing, trading, re-conditioning, repair etc are allowed in the SEZ’s.

• SEZ policy was introduced in year 2000 under Export Import Policy, However SEZ Act was enacted in 2005 and passed by Parliament and rules was framed in 2006.

SEZ

DTA (Domestic Tariff Area)

What is IFSC?

SEZ

DTA (Domestic Tariff Area)

IFSC

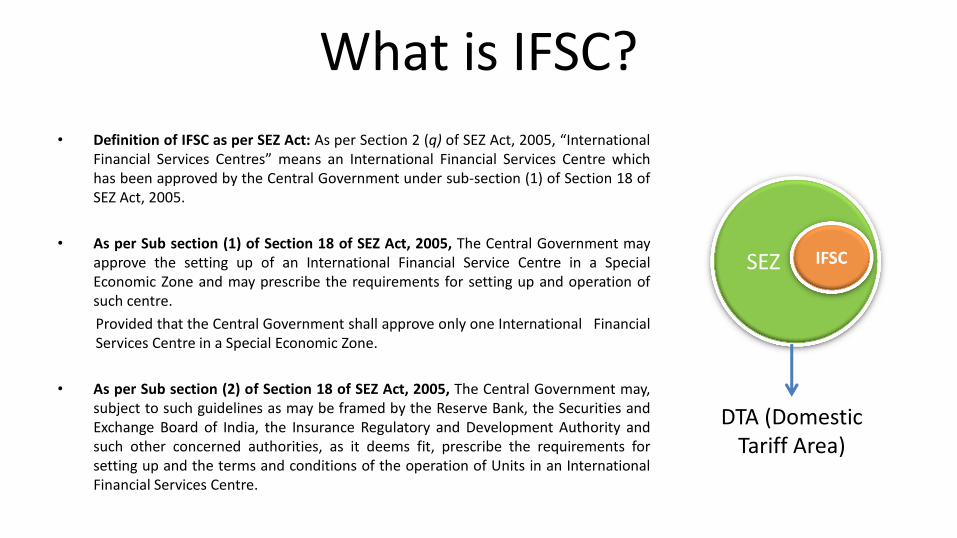

• Definition of IFSC as per SEZ Act: As per Section 2 (q) of SEZ Act, 2005, “International Financial Services Centres” means an International Financial Services Centre which has been approved by the Central Government under sub-section (1) of Section 18 of SEZ Act, 2005.

• As per Sub section (1) of Section 18 of SEZ Act, 2005, The Central Government may approve the setting up of an International Financial Service Centre in a Special Economic Zone and may prescribe the requirements for setting up and operation of such centre.

Provided that the Central Government shall approve only one International Financial Services Centre in a Special Economic Zone.

• As per Sub section (2) of Section 18 of SEZ Act, 2005, The Central Government may, subject to such guidelines as may be framed by the Reserve Bank, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority and such other concerned authorities, as it deems fit, prescribe the requirements for setting up and the terms and conditions of the operation of Units in an International Financial Services Centre.

Salient Features of IFSC

SEZ

DTA (Domestic Tariff Area)

IFSC

• An IFSC caters to customers outside the jurisdiction of the domestic economy. Such centres deal with flows of finance, financial products and services across borders. London, New York and Singapore can be counted as global financial centres. Many emerging IFSCs around the world, such as Shanghai and Dubai, are aspiring to play a global role in the years to come.

Salient Features of IFSC in India: As per Foreign Exchange Management (International Financial Service Centre) Regulations, 2015 dated: 02.03.2016

1. Any financial institution or branch of a financial institution set up in the IFSC and

permitted/recognised as such by the Government of India or a Regulatory Authority shall be treated as a person resident outside India.

2. A financial institution or branch of a financial institution shall conduct such business in such

foreign currency and with such persons, whether resident or otherwise, as the concerned Regulatory Authority may determine.

3. Subject to the provisions of Section 1(3) of the Act, and save as otherwise provided in these

Regulations or any other Regulations or directed by the Reserve Bank of India from time to time, nothing contained in any other regulations shall apply to a financial institution or branch of a financial institution set up in an IFSC.

Announced IRDA (IFSC) Guidelines, 2015

IRDA

Announced SEBI (IFSC) Guidelines, 2015

SEBI

Foreign Exchange Management

(International Financial services

Centre), Regulations, 2015 were issues

RBI

Announced outlines of IFSC

Ministry of Finance

06.04.15

27.03.15

02.03.15 01.03.15

Progress So far- Post budget 2015

01.04.15

Guidelines for setting up IFSC Banking Unit (IBU) were

announced

RBI

Laid down guidelines for setting up an IFSC units in SEZs

Ministry of Commerce

08.04.15 Budget 2016

Reduction of MAT

from 18.50% to 9%,

Exemption from

STT, CTT, Long

Term capital gain tax and DDT

Union Budget

2016

Comparison between SEZ and IFSC on Taxation front

SEZ IFSC

During development, Construction

and operation stage

SEZ Units IFSC Units

Exemption from: 1. Custom Duty & Excise Duty 2. Central Sales Tax 3. Service Tax 4. Exemption from VAT, Stamp duty etc. as per State Govt.

Policy

Exemption from: 1. Custom Duty & Excise Duty 2. Central Sales Tax 3. Service Tax 4. Exemption from Securities transaction tax leviable

under sec. 98 of Finance (No. 2) Act, 2004, Commodity Transaction Tax, Long Term capital gain tax and Dividend distribution tax

5. Exemption from VAT, Stamp duty etc. as per State Govt. Policy

For First 5 years- 100% of eligible profits or gains. For Next 5 years- 50% of eligible profits or gains. For Next 5 years- 50% of the ploughed back export profits

For First 5 years- 100% of eligible profits or gains. For Next 5 years- 50% of eligible profits or gains.

MAT is applicable at the rate of 18.5% (Surcharge, cess extra) MAT is applicable at the rate of 9% (As per Union Budget 2016)- Surcharge, cess extra

Income tax holidays

MAT

What is there for capital market Intermediaries

02

Intermediaries allowed To set up operations In IFSC for rendering

Financial services relating to securities

market

A trustee of trust deed

A registrar to an issue

A share transfer

agent

An underwriter

A portfolio

manager A depository

participant

A custodian of

securities.

A stock broker and

sub-broker.

A foreign portfolio

investor

A merchant

banker

A banker to

an issue

An investment

advisor

A credit rating agency

Any other intermediary or

any person associated with

the securities market as may

be specified by the board

from time to time

Stock Exchanges, Clearing

Corporations, Mutual funds,

Alternate Investment Funds

Permissible Securities

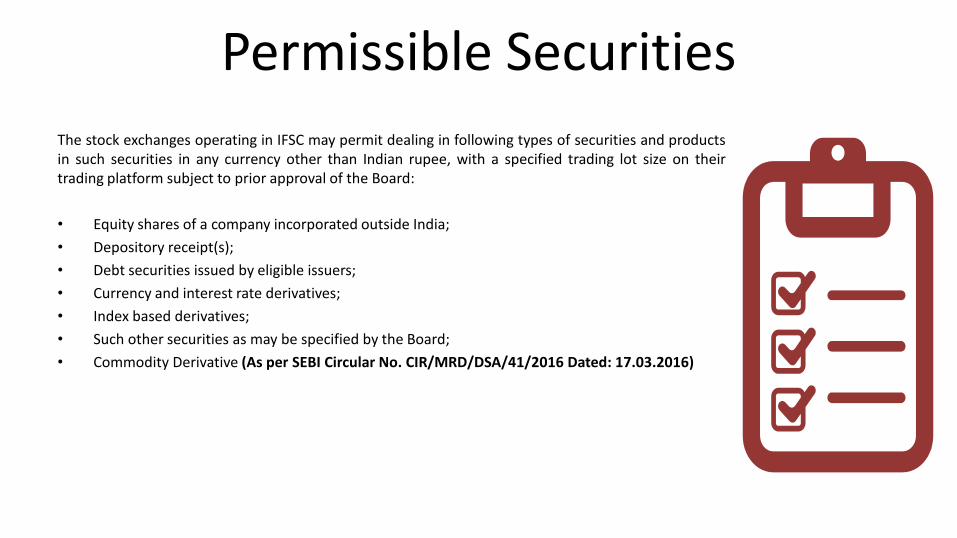

The stock exchanges operating in IFSC may permit dealing in following types of securities and products in such securities in any currency other than Indian rupee, with a specified trading lot size on their trading platform subject to prior approval of the Board:

• Equity shares of a company incorporated outside India;

• Depository receipt(s);

• Debt securities issued by eligible issuers;

• Currency and interest rate derivatives;

• Index based derivatives;

• Such other securities as may be specified by the Board;

• Commodity Derivative (As per SEBI Circular No. CIR/MRD/DSA/41/2016 Dated: 17.03.2016)

Nature of Clients

Nature of clients to whom an Intermediary in IFSC can provide financial services:

(i) a person not resident in India;

(ii) a non-resident Indian;

(iii) a financial institution resident in India who is eligible under FEMA to invest funds offshore, to the extent of outward investment permitted;

(iv) a person resident in India who is eligible under FEMA, to invest funds offshore, to the extent allowed under the Liberalized Remittance Scheme of Reserve Bank of India, subject to a minimum investment as specified by the Board from time to time:

Provided that clients referred to in clauses (ii) to (iv) may be provided services, subject to guidelines of Reserve Bank of India.

Approval Process After provisional allotment of

space, apply for company formation with ROC and

obtain certificate of Incorporation and also apply

for PAN Card allotment

Representation before unit approval committee, if no query found on scrutiny of

application

Issuance of Letter of Approval (‘LOA’) as per SEZ Act, 2005

and Rules, 2006 and submission of acceptance letter

Application to be made to Regulatory authority such as

RBI, SEBI, IRDA of India as the case may be for setting up

operations in IFSC

7

Execution of Bond Cum Legal undertaking in accordance to

SEZ Act and Rules for availing various types of benefits

available under SEZ policy

8

After name availability confirmation from ROC

(Registrar of companies), obtain NOC from GIFT SEZ or any co-developer for usage of

GIFT address for incorporation

2

Apply for name availability for incorporating new

company/LLP with ROC for setting up IFSC unit including (IFSC) word as a part of name

1

Post formation of company/LLP an application

is to be made to the concerned Development Commissioner

of SEZ for unit

3

4 6 5

Business Opportunities

03

Business opportunities in IFSC

Major business opportunities in IFSC: • Fund-raising services for individuals, corporations and governments. • Asset management and global portfolio diversification undertaken by pension funds, insurance companies and mutual

funds. • Wealth management. • Global tax management and cross-border tax liability optimization, which provides a business opportunity for financial

intermediaries, accountants and law firms. • Global and regional corporate treasury management operations that involve fund-raising, liquidity investment and

management and asset-liability matching. • Risk management operations such as insurance and reinsurance. • Merger and acquisition activities among trans-national corporations. • Exchanges, Brokerage services. • Corporate Banking, servicing JV/WOS of Indian cos registered abroad, factoring/factoring of export receivables. • Fund accounting, investment services, custodian services, Trust services etc However for all purposes transactions can happen in currency other than Indian Rupee and with Non residents only (Except as permitted under FEMA norms and LRS scheme).

?

![[ifsc] retificadores](https://static.fdocuments.in/doc/165x107/56d6beb41a28ab3016933cf3/ifsc-retificadores.jpg)